Financial Accounting and Reporting

VerifiedAdded on 2021/04/21

|10

|1367

|32

AI Summary

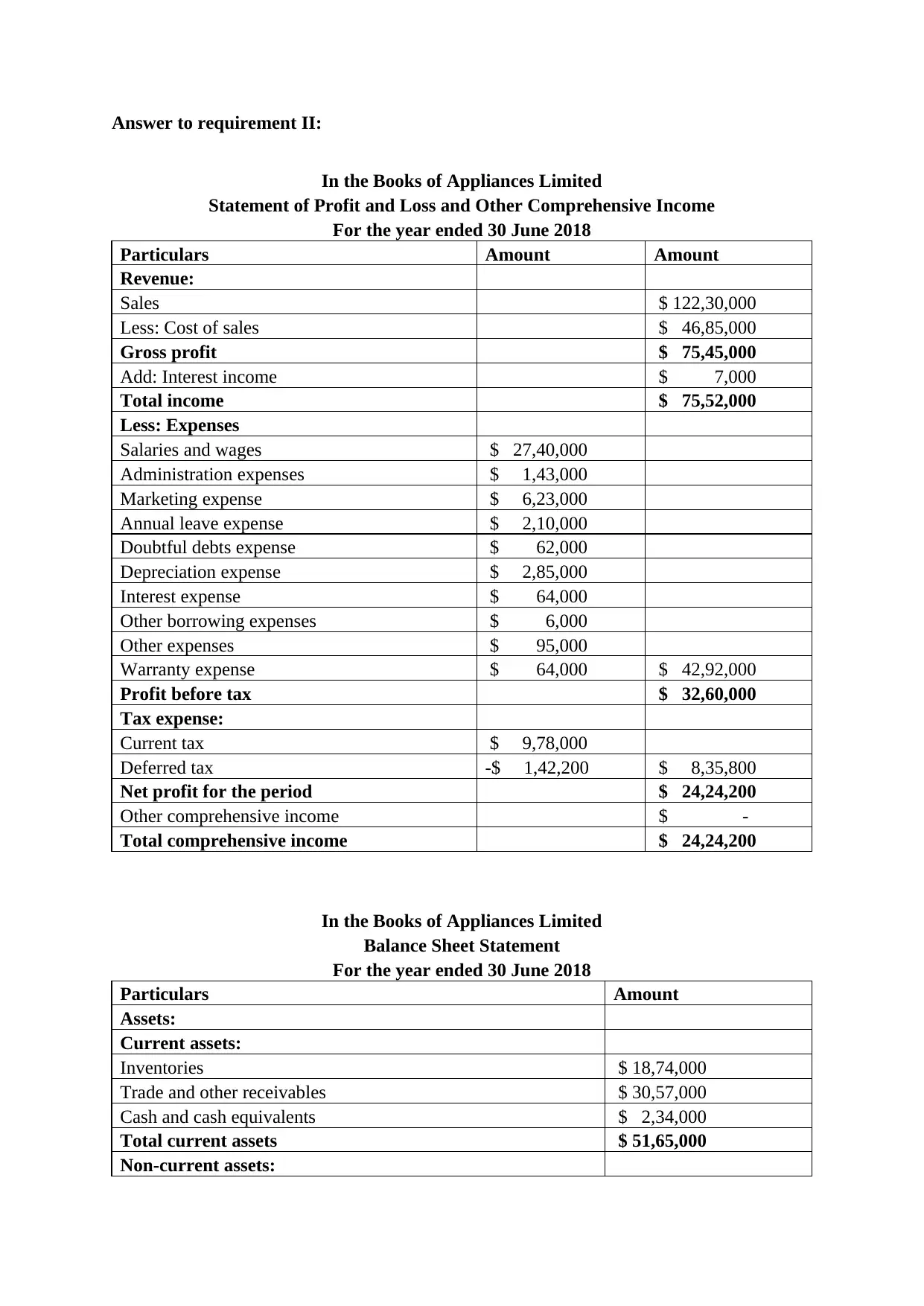

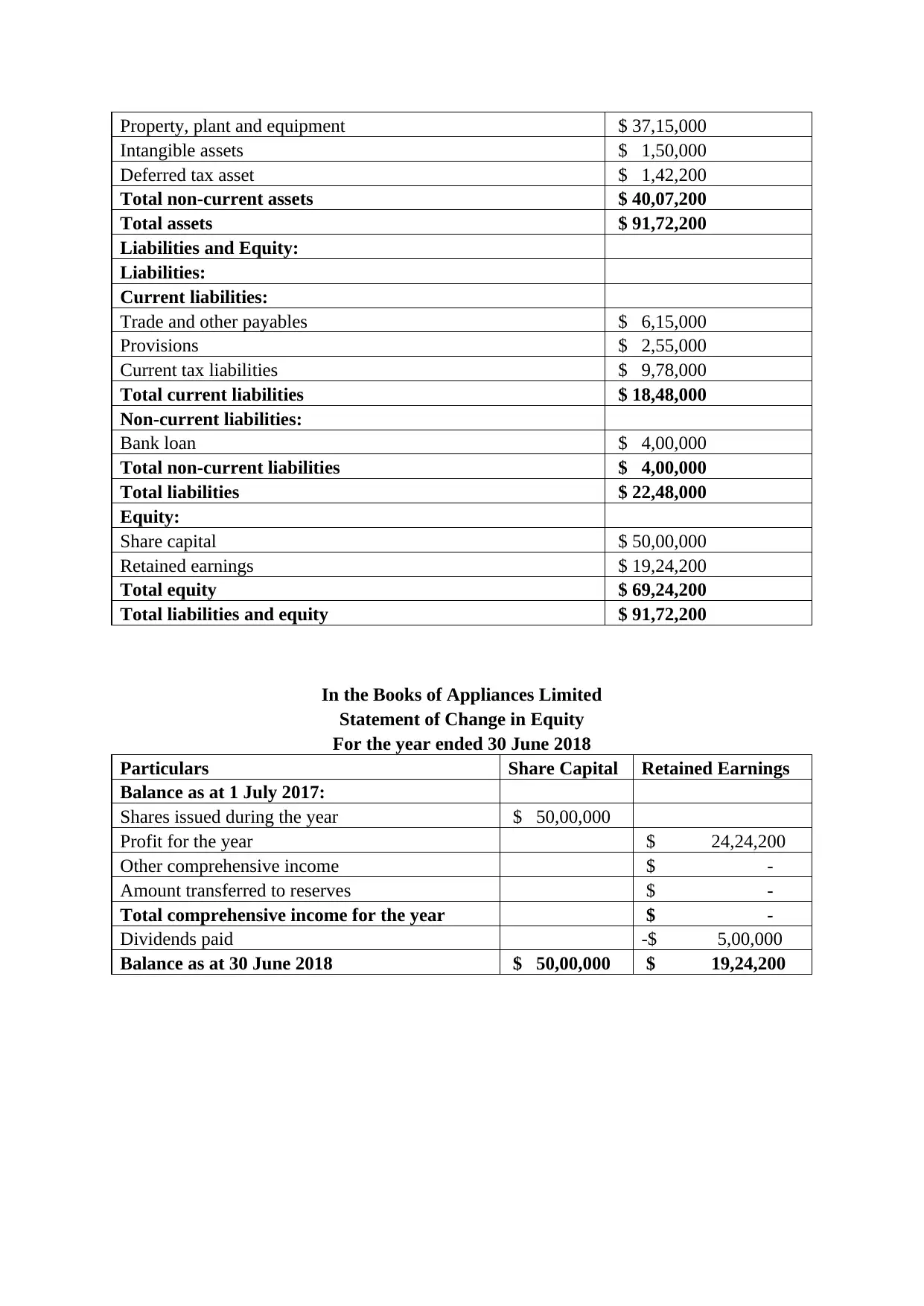

This assignment provides the financial statements, including the balance sheet statement, income statement, and cash flow statement, for Appliances Limited for the year ended 30 June 2018. The statements include details such as assets, liabilities, equity, revenue, expenses, net profit, and comprehensive income. Additionally, it includes a statement of change in equity, which shows the changes in share capital and retained earnings during the year. The assignment also references relevant accounting standards and provides a summary in English.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.