Financial Accounting and Reporting: Principles and Applications

VerifiedAdded on 2020/10/05

|26

|4568

|177

Report

AI Summary

This report provides a comprehensive overview of financial accounting, beginning with a definition and exploring relevant regulations. It delves into accounting rules and principles applicable within an organization, including debit/credit rules, going concern, matching, and revenue recognition principles. The report then examines conventions and concepts such as material disclosure and consistency. Part B applies these principles through several client case studies, including double-entry recording, trial balance preparation, and financial statement analysis (profit and loss, balance sheet). It covers adjustments, depreciation, and bank reconciliation, alongside ledger control accounts and suspense account reconciliation. The report concludes with an understanding of different account types and a brief conclusion. The report offers a detailed analysis of financial accounting concepts and their practical applications through diverse case studies.

Financial Accounting and

principles

principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

1.Define Financial accounting................................................................................................3

2. Regulations relating to financial accounting......................................................................4

3. Various accounting rules and principles applicable in the organisation............................4

4. Conventions and concepts related to the material disclosure and consistency:.................5

PART B............................................................................................................................................6

CLIENT 1........................................................................................................................................6

P1: Double entry recording with concerned ledger:...............................................................6

P2: Produce a trial balance applied the use of the balance off rule to complete the ledger. 16

M1:.......................................................................................................................................17

D1:........................................................................................................................................17

CLIENT 2......................................................................................................................................17

P3: Financial accounts form given trial balance figures adjusting, depreciation and prep. .17

P4: Final accounts subject to sole traders, partnerships or limited companies....................18

M2:.......................................................................................................................................19

D2:........................................................................................................................................19

CLIENT 3......................................................................................................................................19

(a) Profit and loss statement of Raintree Ltd. For the year ended 30th September 2017......19

(b) Statement of financial statement of Braintree Ltd..........................................................20

(c) Accounting Concepts:.....................................................................................................21

(d) Requirement of depreciation in the preparation of financial statements........................22

CLIENT 4......................................................................................................................................23

P5: Apply the bank reconciliation process to make a number of a reconciliation...............23

CLIENT 5......................................................................................................................................24

Ledger control accounts.......................................................................................................24

CLIENT 6......................................................................................................................................24

P6: Process to be taken to reconcile control accounts and clear suspense account..............24

M4: Understanding of the type of accounts.........................................................................25

CONCLUSION..............................................................................................................................25

REFERENCES..............................................................................................................................26

INTRODUCTION...........................................................................................................................3

1.Define Financial accounting................................................................................................3

2. Regulations relating to financial accounting......................................................................4

3. Various accounting rules and principles applicable in the organisation............................4

4. Conventions and concepts related to the material disclosure and consistency:.................5

PART B............................................................................................................................................6

CLIENT 1........................................................................................................................................6

P1: Double entry recording with concerned ledger:...............................................................6

P2: Produce a trial balance applied the use of the balance off rule to complete the ledger. 16

M1:.......................................................................................................................................17

D1:........................................................................................................................................17

CLIENT 2......................................................................................................................................17

P3: Financial accounts form given trial balance figures adjusting, depreciation and prep. .17

P4: Final accounts subject to sole traders, partnerships or limited companies....................18

M2:.......................................................................................................................................19

D2:........................................................................................................................................19

CLIENT 3......................................................................................................................................19

(a) Profit and loss statement of Raintree Ltd. For the year ended 30th September 2017......19

(b) Statement of financial statement of Braintree Ltd..........................................................20

(c) Accounting Concepts:.....................................................................................................21

(d) Requirement of depreciation in the preparation of financial statements........................22

CLIENT 4......................................................................................................................................23

P5: Apply the bank reconciliation process to make a number of a reconciliation...............23

CLIENT 5......................................................................................................................................24

Ledger control accounts.......................................................................................................24

CLIENT 6......................................................................................................................................24

P6: Process to be taken to reconcile control accounts and clear suspense account..............24

M4: Understanding of the type of accounts.........................................................................25

CONCLUSION..............................................................................................................................25

REFERENCES..............................................................................................................................26

INTRODUCTION

Financial accounting is the process of accounting which deals with recording and

summarising of financial transactions which helps in the formulating the financial strategies and

plans. The finance related accounting is the process of recording the transactions in such a

manner that is understandable for the managers and other users of the organisations. The main

purpose is to bring the financial stability in the business. The information’s related to financial

accounting is presented in financial statements such as profit and loss account, balance sheet and

cash flow statement which are prepared in this report ( Motherly and Burney, 2013.) This report

includes two broad parts, one consists of business report that includes rules and principles and

another one includes statements of financial position such as profit and loss statement, balance

sheet, bank reconciliation statement etc.

PART A

BUSINESS REPORT

1.Define Financial accounting

Finance accounting is the most common form of accounting that deals with the

preparation of financial statements of the company such as balance sheet, profit and loss

statement and cash flow statement. The financial accounting process starts with the recording,

classifying and summarising the financial transactions of the business. These transactions are

recorded in the journal of the companies, then they are posted into ledger and then trial balance is

formulated. After the proper recording of all the transactions the financial managers prepare the

financials of the company. The duty of the financial managers is to prepare these financial

statements with reliable and accurate information so that the users of the financial statements can

entrust on the statements in taking important decisions regarding the investing in company's

projects. And therefore it is the responsibility of the financial managers of the company to

prepare the financials using information which is reliable such that the statements reflect the true

and fair view of the company (Rankin, and et. al. 2012)

Financial accounting in the companies uses certain pre-determined standards that are

formulated by the regulatory bodies such as IASB and FASB. Various companies use different

accounting standards as suitable to the accountants and owners of the companies. The companies

Financial accounting is the process of accounting which deals with recording and

summarising of financial transactions which helps in the formulating the financial strategies and

plans. The finance related accounting is the process of recording the transactions in such a

manner that is understandable for the managers and other users of the organisations. The main

purpose is to bring the financial stability in the business. The information’s related to financial

accounting is presented in financial statements such as profit and loss account, balance sheet and

cash flow statement which are prepared in this report ( Motherly and Burney, 2013.) This report

includes two broad parts, one consists of business report that includes rules and principles and

another one includes statements of financial position such as profit and loss statement, balance

sheet, bank reconciliation statement etc.

PART A

BUSINESS REPORT

1.Define Financial accounting

Finance accounting is the most common form of accounting that deals with the

preparation of financial statements of the company such as balance sheet, profit and loss

statement and cash flow statement. The financial accounting process starts with the recording,

classifying and summarising the financial transactions of the business. These transactions are

recorded in the journal of the companies, then they are posted into ledger and then trial balance is

formulated. After the proper recording of all the transactions the financial managers prepare the

financials of the company. The duty of the financial managers is to prepare these financial

statements with reliable and accurate information so that the users of the financial statements can

entrust on the statements in taking important decisions regarding the investing in company's

projects. And therefore it is the responsibility of the financial managers of the company to

prepare the financials using information which is reliable such that the statements reflect the true

and fair view of the company (Rankin, and et. al. 2012)

Financial accounting in the companies uses certain pre-determined standards that are

formulated by the regulatory bodies such as IASB and FASB. Various companies use different

accounting standards as suitable to the accountants and owners of the companies. The companies

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in US generally uses US-GAAP standards in preparing their financial statements, the IFRS

financial reporting standards are also recognized in the companies all over the world and are

adopted by many big companies. The main purpose behind the adoption of these standards are

that these standards ensure that the prepared financial statements of the company are reliable and

that it shows the true and fair view of the companies because of certain regulations of doing

accounting imposed by the bodies.

2. Regulations relating to financial accounting

Financial accounting deals with the preparations of financial statements and its most

important objective is to prepare those financial with utmost care and using reliable information

such that it shows the correct financial position and health of the company. For solving the

purpose, there are various regulations that are imposed by the regulatory bodies that are created

for this purpose only. The most famous regulatory bodies in the world are FASB and IASB, most

of the companies uses the financial reporting standards that are offered by these bodies. The

name of accounting standards that are prepared by these bodies are US-GAAP (FASB) and IFRS

(by IASB). The reporting standards provided by these informs the managers and accountants that

they should keep a record of the financial transactions of the company. Using reporting standards

provided by regulatory bodies declines the chances of abuse and discrepancies in the recording

of the financial transactions. Every user of financial statements require that the statements are

reliable, accurate, fair, true, understandable and comparable information about the financial

position and health of the companies. The principles and accounting standards are different in

every country but the source of regulation is same in every country (Norton, 2012)

3. Various accounting rules and principles applicable in the organisation

Accounting rules:

Debit the receiver and credit the giver: This rule of accounting is applicable in all the

personal accounts that are dealing with the business directly or indirectly. The personal

accounts of the company include individuals that can be natural or legal body. If the

person receives anything from the organisation, then his account is debited in the

company's account. And if the person provides anything to the company then his account

is credited in the company's account.

Credit what goes out and debit what comes in: This accounting rule is applicable on

the real accounts of the company, the real accounts of company includes fixed assets of

financial reporting standards are also recognized in the companies all over the world and are

adopted by many big companies. The main purpose behind the adoption of these standards are

that these standards ensure that the prepared financial statements of the company are reliable and

that it shows the true and fair view of the companies because of certain regulations of doing

accounting imposed by the bodies.

2. Regulations relating to financial accounting

Financial accounting deals with the preparations of financial statements and its most

important objective is to prepare those financial with utmost care and using reliable information

such that it shows the correct financial position and health of the company. For solving the

purpose, there are various regulations that are imposed by the regulatory bodies that are created

for this purpose only. The most famous regulatory bodies in the world are FASB and IASB, most

of the companies uses the financial reporting standards that are offered by these bodies. The

name of accounting standards that are prepared by these bodies are US-GAAP (FASB) and IFRS

(by IASB). The reporting standards provided by these informs the managers and accountants that

they should keep a record of the financial transactions of the company. Using reporting standards

provided by regulatory bodies declines the chances of abuse and discrepancies in the recording

of the financial transactions. Every user of financial statements require that the statements are

reliable, accurate, fair, true, understandable and comparable information about the financial

position and health of the companies. The principles and accounting standards are different in

every country but the source of regulation is same in every country (Norton, 2012)

3. Various accounting rules and principles applicable in the organisation

Accounting rules:

Debit the receiver and credit the giver: This rule of accounting is applicable in all the

personal accounts that are dealing with the business directly or indirectly. The personal

accounts of the company include individuals that can be natural or legal body. If the

person receives anything from the organisation, then his account is debited in the

company's account. And if the person provides anything to the company then his account

is credited in the company's account.

Credit what goes out and debit what comes in: This accounting rule is applicable on

the real accounts of the company, the real accounts of company includes fixed assets of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the company. When the company purchases the assets the real account of asset is debited

in the company account and when the company discards the asset, that account is credited

in the company's books according to the rule.

Credit all incomes and gains and debit all losses and expenses: this accounting rule is

applicable on all the nominal accounts of the company. Nominal accounts include the

expenses, losses, income and gains of the company. Let’s take an example of salaries

account, when the company pays salaries to its employees the salaries account is debited

and the bank account is credited according to the rule of debit all expense and losses.

( Chea, 2011)

Accounting principle:

Going concern principle: this principle states and assumes that the company will

continue to do its operation for the coming future period and attain the objectives with the

view that company will continue to exist and it will not shut down in near future. In cases

when the accountant of company feels that it will not exist in future then he has to inform

to all the stakeholders of the company.

Matching Principle: This accounting principle needs organisation to follow accrual

accounting system, as per accounting principles, accountant must try to match revenues

according to its expenses.

Revenue recognition principles: This kind of accounting principle simply said that the

organisation must need to implement accrual basis of accounting instead of cash basis

accounting that simply means that the organisation must need to identify the income

when product is sold and not if the amount is achieved from consumers and within the

same time goes with the expenditure (Wilson, and et. al. 2010)

4. Conventions and concepts related to the material disclosure and consistency:

Material Disclosure: This can be rightly said that the accounting conventions simply

suggest that the accounting must concentrates on the recording of transactions that are important

and whole of the abnormal things is ignored. However, this is crucial as normal minutes’

transactions overburden the accounts of the organisation. There is various pre-determined

formula for opting material transactions or events, this decision is entirely relied upon skills and

knowledge of the accountant to judge about the transactions are crucial to be recorded in books

of accounts and which are not. (Brown, 2011). This must be adopted that transactions which is

in the company account and when the company discards the asset, that account is credited

in the company's books according to the rule.

Credit all incomes and gains and debit all losses and expenses: this accounting rule is

applicable on all the nominal accounts of the company. Nominal accounts include the

expenses, losses, income and gains of the company. Let’s take an example of salaries

account, when the company pays salaries to its employees the salaries account is debited

and the bank account is credited according to the rule of debit all expense and losses.

( Chea, 2011)

Accounting principle:

Going concern principle: this principle states and assumes that the company will

continue to do its operation for the coming future period and attain the objectives with the

view that company will continue to exist and it will not shut down in near future. In cases

when the accountant of company feels that it will not exist in future then he has to inform

to all the stakeholders of the company.

Matching Principle: This accounting principle needs organisation to follow accrual

accounting system, as per accounting principles, accountant must try to match revenues

according to its expenses.

Revenue recognition principles: This kind of accounting principle simply said that the

organisation must need to implement accrual basis of accounting instead of cash basis

accounting that simply means that the organisation must need to identify the income

when product is sold and not if the amount is achieved from consumers and within the

same time goes with the expenditure (Wilson, and et. al. 2010)

4. Conventions and concepts related to the material disclosure and consistency:

Material Disclosure: This can be rightly said that the accounting conventions simply

suggest that the accounting must concentrates on the recording of transactions that are important

and whole of the abnormal things is ignored. However, this is crucial as normal minutes’

transactions overburden the accounts of the organisation. There is various pre-determined

formula for opting material transactions or events, this decision is entirely relied upon skills and

knowledge of the accountant to judge about the transactions are crucial to be recorded in books

of accounts and which are not. (Brown, 2011). This must be adopted that transactions which is

material for one organisation might be immaterial for other one, and items that are material in

existing year could be immaterial for the another one, and items that are material in the existing

year could be immaterial in the next year.

Consistency: This consistency convention of accounts implies that the accounting practices

that are applicable in the existing yeas which must remain unchanged for diverse periods. This

simply says that the rules and policies which considered by the business must remain stable for

the organisation for the longer period and must also varied in case of changes the policies as the

urgent needs, organisation must need to have adequate steps in using of those changes.

Stakeholders and various employees who needs consistency in the policies henceforth they could

be convenient in working with the organisation (Balakrishnan and Cohen, 2011).

PART B

CLIENT 1

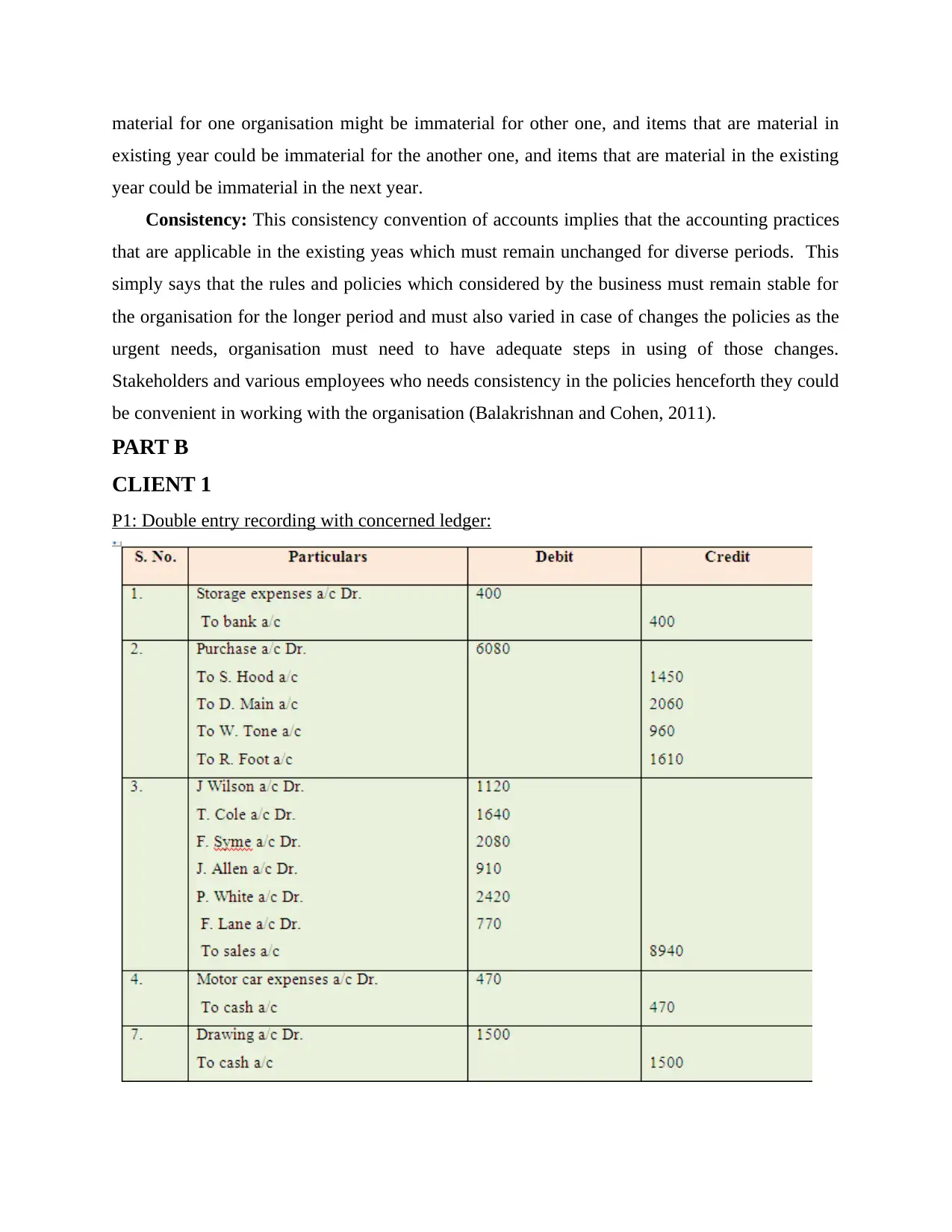

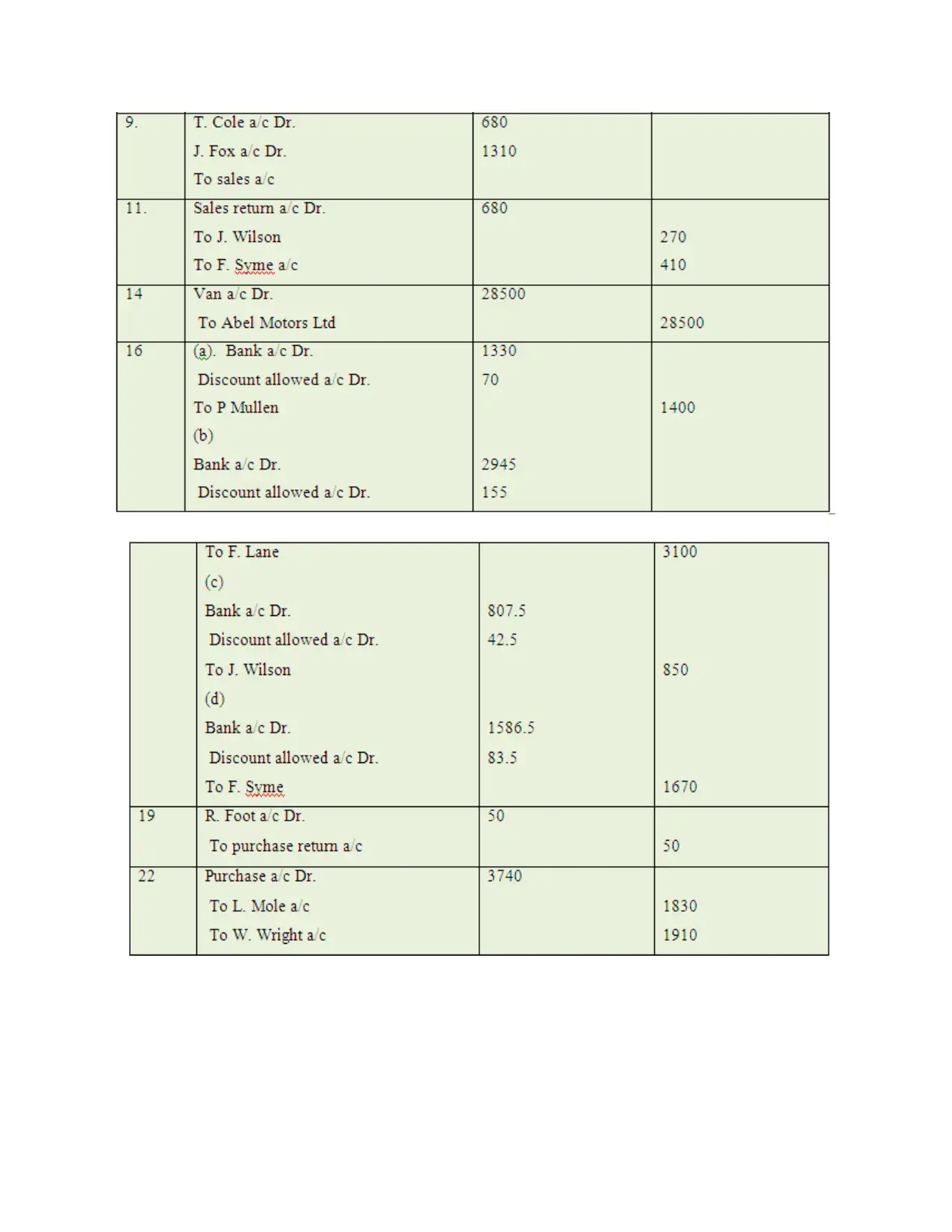

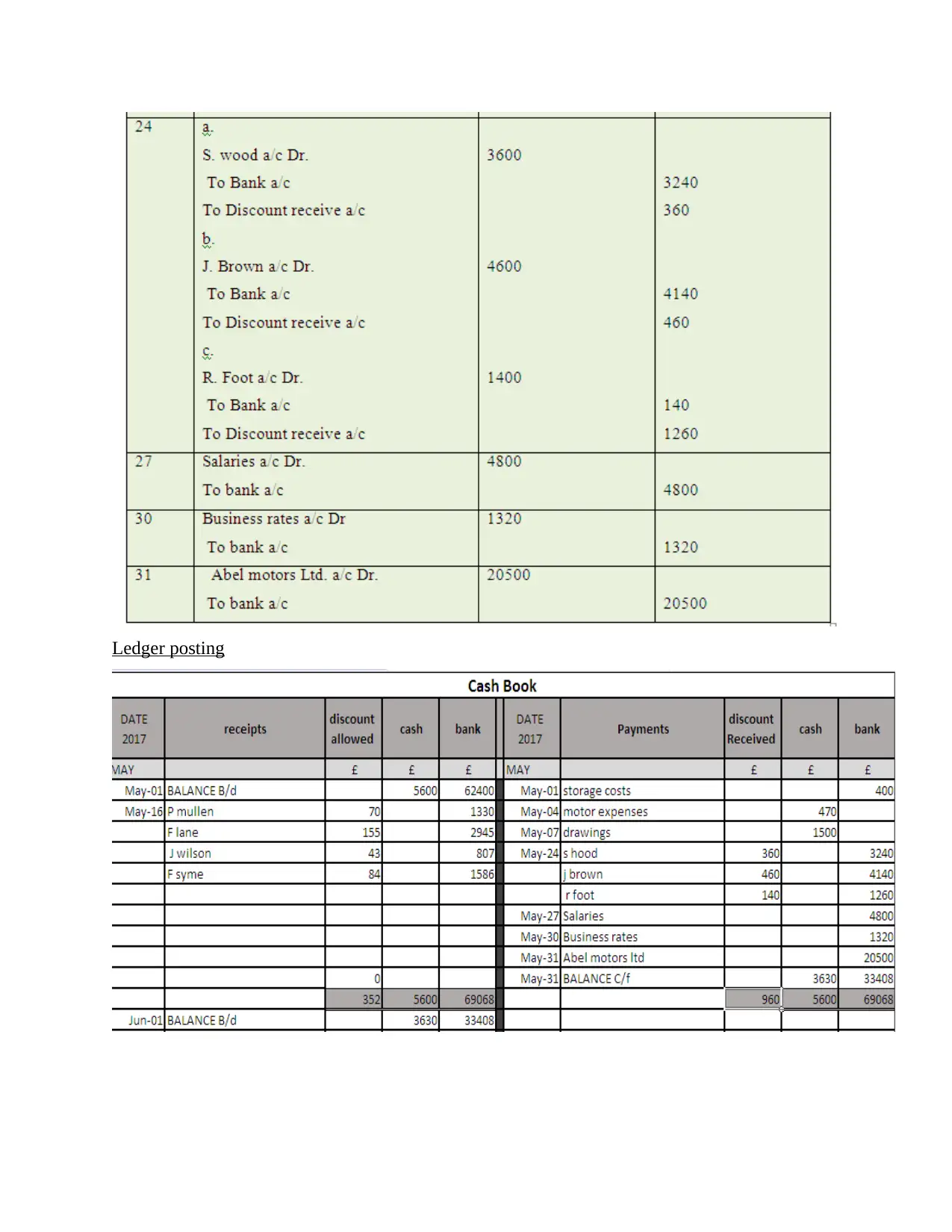

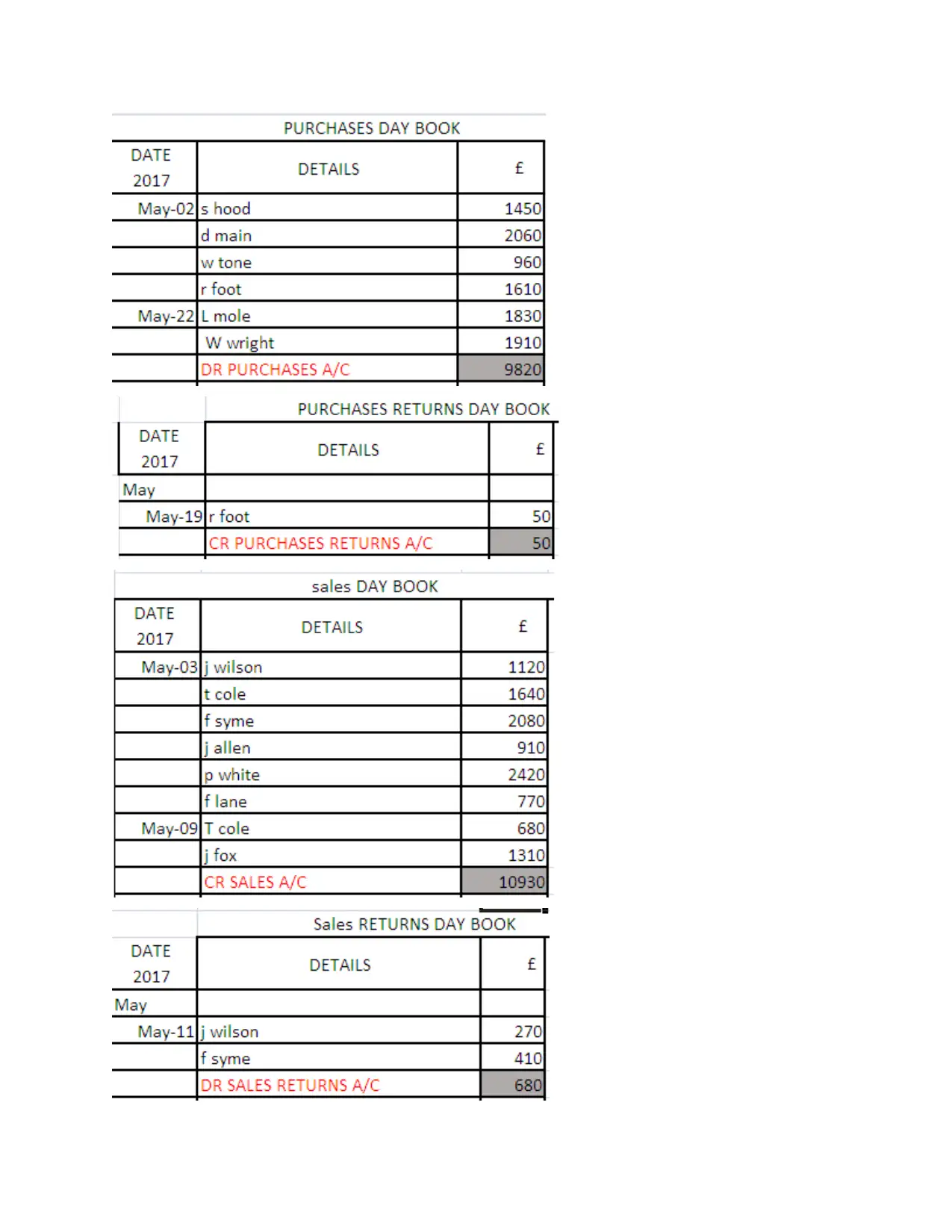

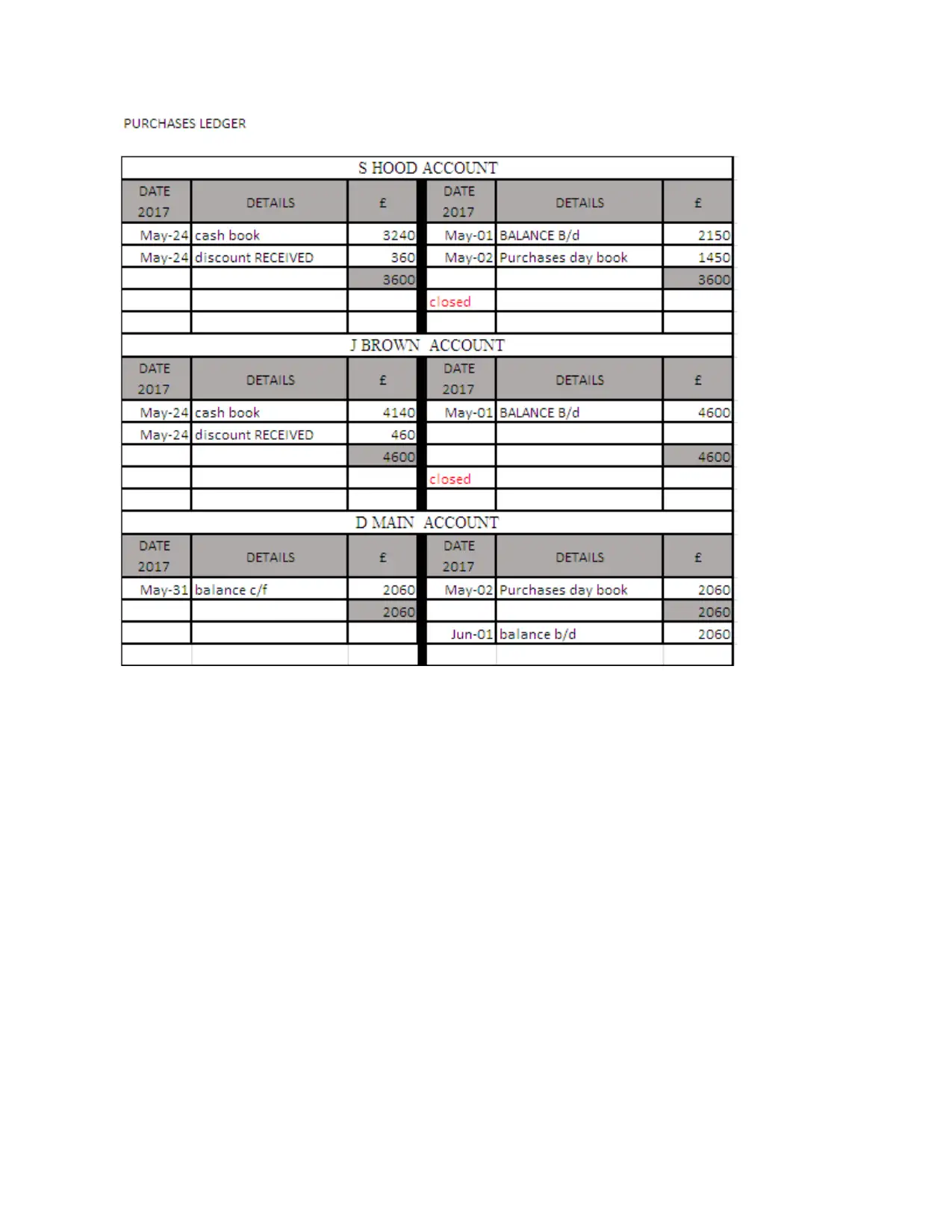

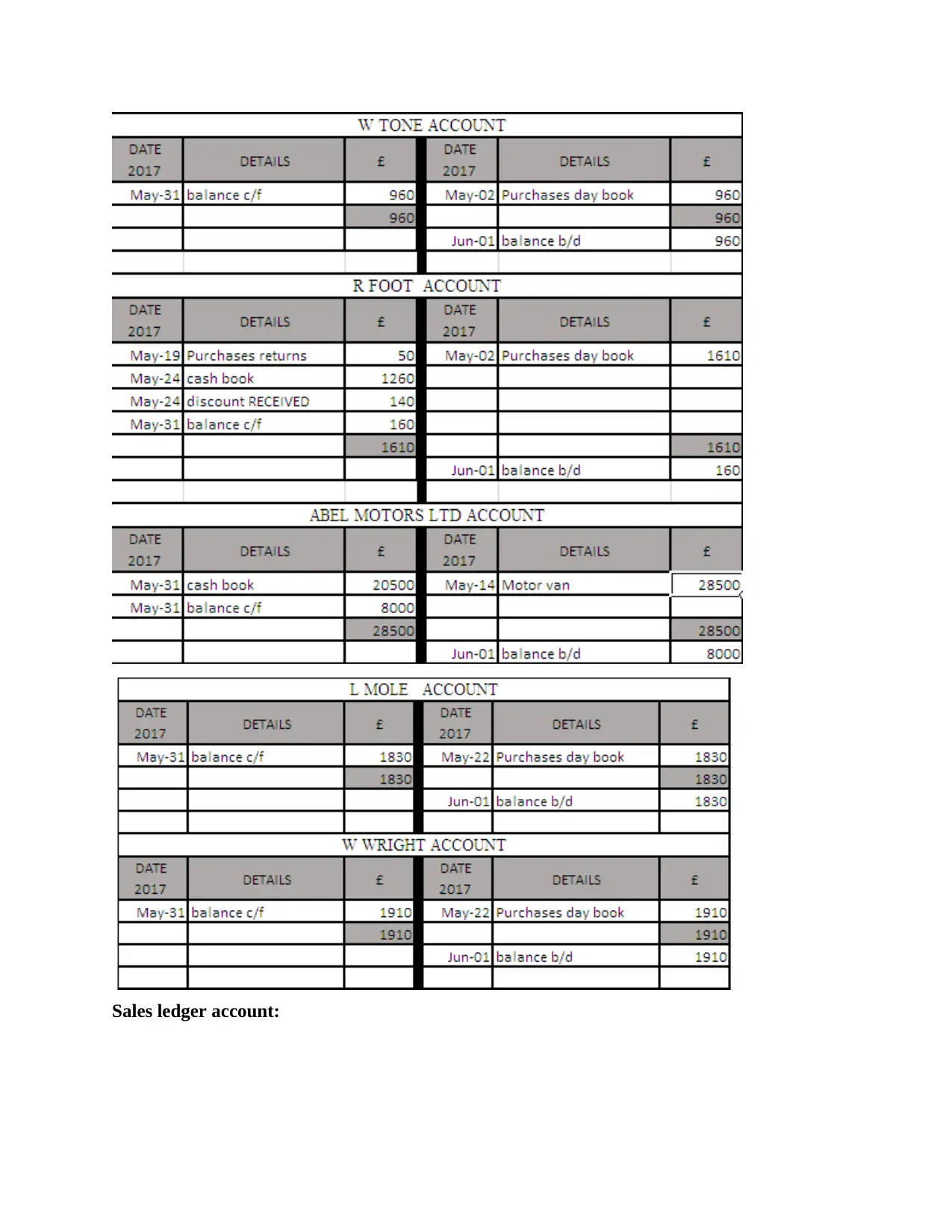

P1: Double entry recording with concerned ledger:

existing year could be immaterial for the another one, and items that are material in the existing

year could be immaterial in the next year.

Consistency: This consistency convention of accounts implies that the accounting practices

that are applicable in the existing yeas which must remain unchanged for diverse periods. This

simply says that the rules and policies which considered by the business must remain stable for

the organisation for the longer period and must also varied in case of changes the policies as the

urgent needs, organisation must need to have adequate steps in using of those changes.

Stakeholders and various employees who needs consistency in the policies henceforth they could

be convenient in working with the organisation (Balakrishnan and Cohen, 2011).

PART B

CLIENT 1

P1: Double entry recording with concerned ledger:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ledger posting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

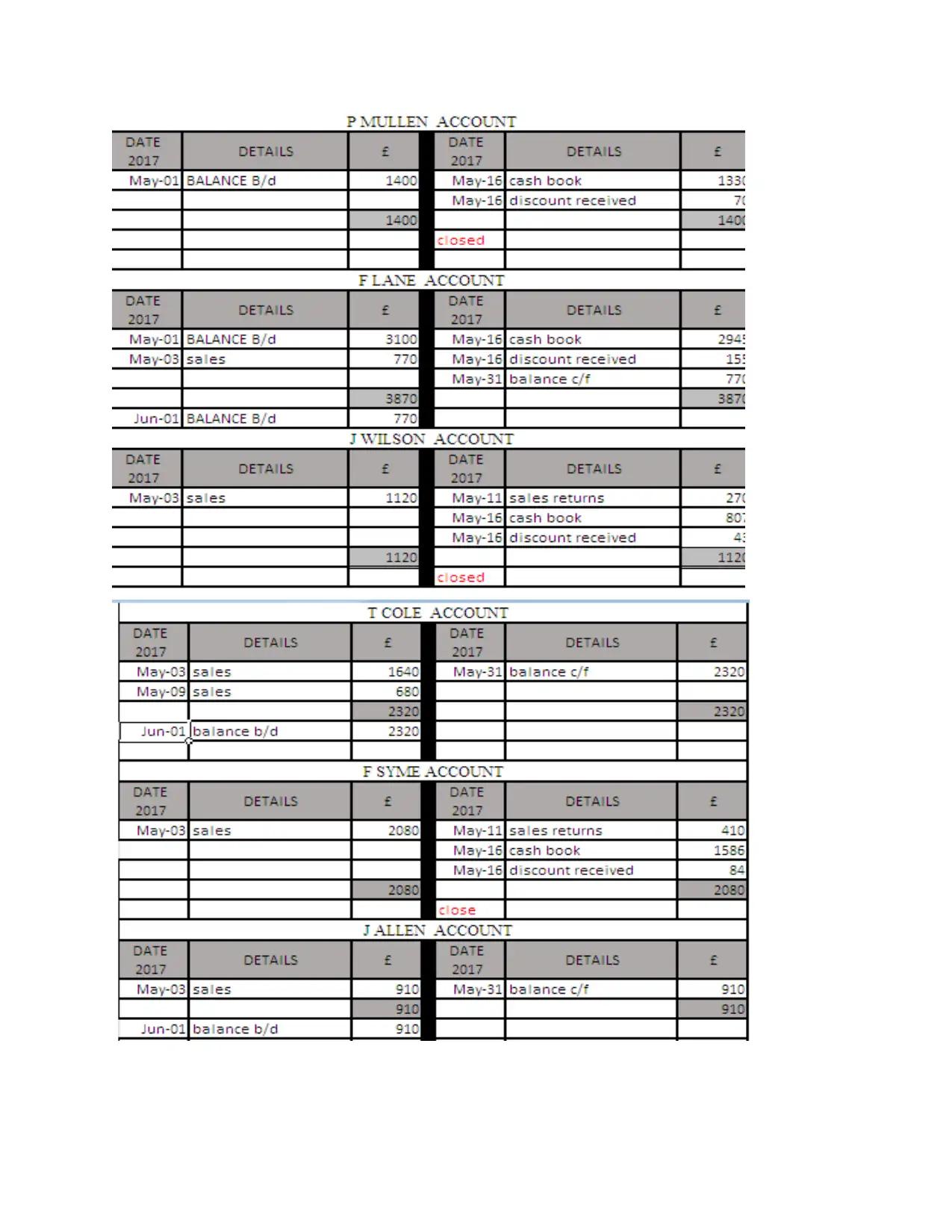

Sales ledger account:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.