Financial Accounting Assignment: Trading, Profit & Loss, and Ratios

VerifiedAdded on 2023/01/07

|14

|2890

|75

Homework Assignment

AI Summary

This assignment solution covers key aspects of financial accounting, addressing two main questions. The first question requires the preparation of Bob's trading account, profit and loss account, and statement of financial position, followed by a discussion of the features of information presented in financial statements. The second question delves into ratio analysis, calculating and interpreting various ratios like return on capital employed, gross profit margin, current ratio, and trade payable/receivable ratios. It also includes bank account balancing, account balances over periods, and a trial balance, along with the depreciation calculation using different methods and a discussion on accounting concepts. The solution provides detailed calculations, explanations, and analysis to aid in understanding the financial accounting principles.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

Question 1a).....................................................................................................................................1

(a) Bob’s Trading Account for the year ending 30th April 2019..................................................1

(b) Bob’s Profit and loss Account for the year ending 30th April 2019.......................................1

(c) Bob’s statement of financial position for the year ending 30th April 2019............................1

Question 1b).....................................................................................................................................2

Feature of information of financial statement.............................................................................2

Question 2a).....................................................................................................................................4

Ratio Analysis..............................................................................................................................4

Question 2b).....................................................................................................................................6

(a) Bank account balancing at the end of each month.................................................................6

(b) Accounts balances at the end of two month periods..............................................................7

(c) Trial balance as at 30 April 2018...........................................................................................8

Question 2c).....................................................................................................................................9

(i) Straight Line method at 12.5%..............................................................................................9

(ii) Reducing Balance Method 15%............................................................................................9

(iii) Meaning and significance of the accounting concepts.......................................................10

REFERENCES..............................................................................................................................12

TABLE OF CONTENTS................................................................................................................2

Question 1a).....................................................................................................................................1

(a) Bob’s Trading Account for the year ending 30th April 2019..................................................1

(b) Bob’s Profit and loss Account for the year ending 30th April 2019.......................................1

(c) Bob’s statement of financial position for the year ending 30th April 2019............................1

Question 1b).....................................................................................................................................2

Feature of information of financial statement.............................................................................2

Question 2a).....................................................................................................................................4

Ratio Analysis..............................................................................................................................4

Question 2b).....................................................................................................................................6

(a) Bank account balancing at the end of each month.................................................................6

(b) Accounts balances at the end of two month periods..............................................................7

(c) Trial balance as at 30 April 2018...........................................................................................8

Question 2c).....................................................................................................................................9

(i) Straight Line method at 12.5%..............................................................................................9

(ii) Reducing Balance Method 15%............................................................................................9

(iii) Meaning and significance of the accounting concepts.......................................................10

REFERENCES..............................................................................................................................12

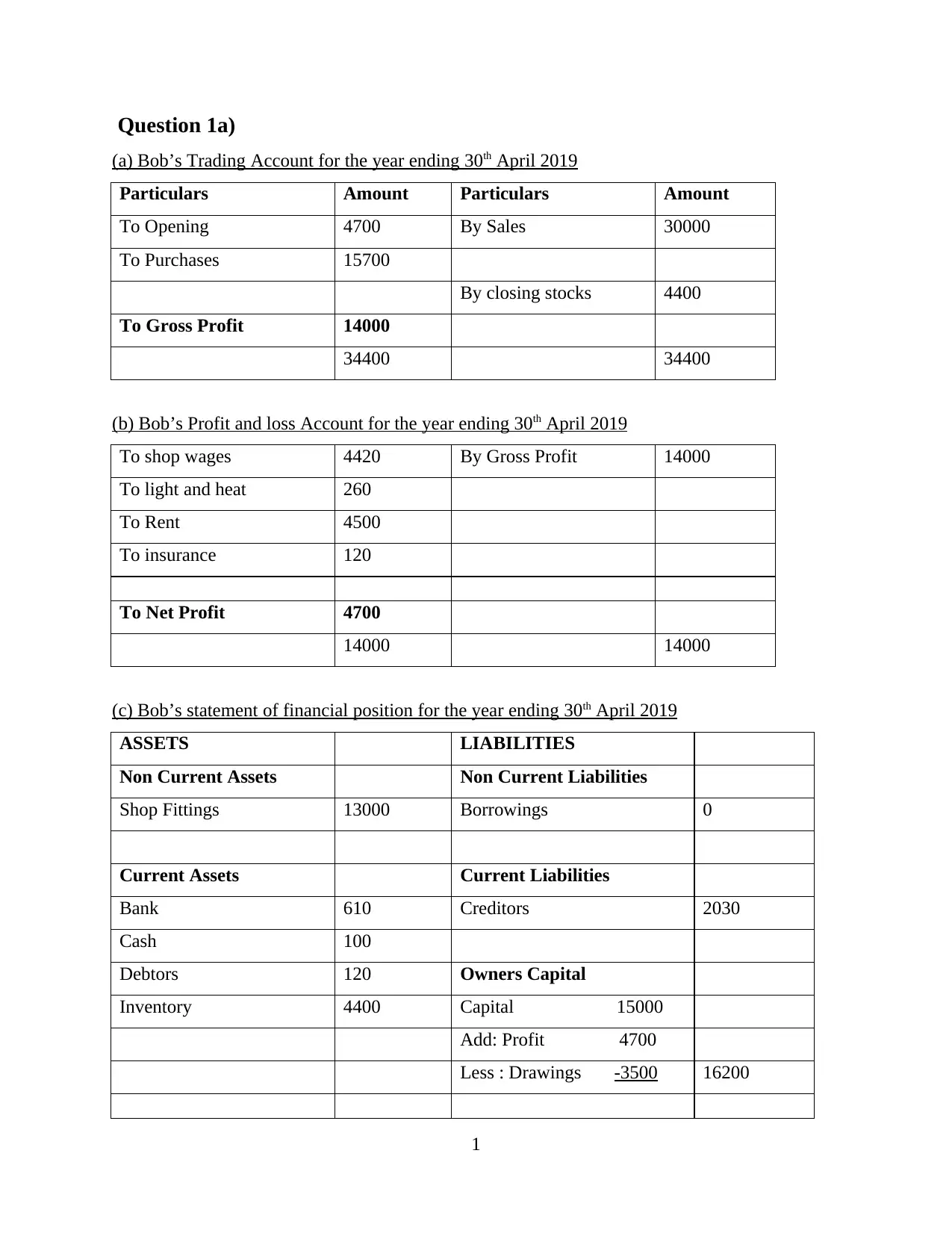

Question 1a)

(a) Bob’s Trading Account for the year ending 30th April 2019

Particulars Amount Particulars Amount

To Opening 4700 By Sales 30000

To Purchases 15700

By closing stocks 4400

To Gross Profit 14000

34400 34400

(b) Bob’s Profit and loss Account for the year ending 30th April 2019

To shop wages 4420 By Gross Profit 14000

To light and heat 260

To Rent 4500

To insurance 120

To Net Profit 4700

14000 14000

(c) Bob’s statement of financial position for the year ending 30th April 2019

ASSETS LIABILITIES

Non Current Assets Non Current Liabilities

Shop Fittings 13000 Borrowings 0

Current Assets Current Liabilities

Bank 610 Creditors 2030

Cash 100

Debtors 120 Owners Capital

Inventory 4400 Capital 15000

Add: Profit 4700

Less : Drawings -3500 16200

1

(a) Bob’s Trading Account for the year ending 30th April 2019

Particulars Amount Particulars Amount

To Opening 4700 By Sales 30000

To Purchases 15700

By closing stocks 4400

To Gross Profit 14000

34400 34400

(b) Bob’s Profit and loss Account for the year ending 30th April 2019

To shop wages 4420 By Gross Profit 14000

To light and heat 260

To Rent 4500

To insurance 120

To Net Profit 4700

14000 14000

(c) Bob’s statement of financial position for the year ending 30th April 2019

ASSETS LIABILITIES

Non Current Assets Non Current Liabilities

Shop Fittings 13000 Borrowings 0

Current Assets Current Liabilities

Bank 610 Creditors 2030

Cash 100

Debtors 120 Owners Capital

Inventory 4400 Capital 15000

Add: Profit 4700

Less : Drawings -3500 16200

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Assets 18230 Total Equity & Liabilities 18230

Question 1b)

Feature of information of financial statement

Financial statements are important for variety of the different parties interested in the

performance of business (Pelekh, Khocha and Holovchak, 2020). Financial Statement generally

contain significant amount of the information about a company financial health. This information

is used by different user to perform variety of different activity. Some of the advantages of

financial information statement are as follows:

Decision making: It is the first feature of information which is performed by the

financial statement information. This sort of the information is generally used by the company

management in the long run. It has been identified that management generally used to analysis

the financial statement of the company on the monthly or the timely basis in the organization.

The main motive of management behind analysing the same in the organization is to find out

variety of the deficit which is presented in the performance of the business across the time. After

that management generally try to find out the solution within the financial statement or from

outside of the same as well. On the basis of variety of different information which is gather from

the financial statement and from outside management generally used to make variety of different

decision in the organization to improve the efficiency of variety of operation. Hence company

management generally uses the financial statement information in taking variety of decision

making.

Valuation of Company: It is another important feature of information presented in the

financial statement of the company. This type of the feature is generally used by the Investor or

the Bank. As investor and Loan provider in the market generally looks at the position of the

business before investing any sort of the money in the organization. Investor and Bank Loan

provider generally looks for the information related to return on the capital and resources and

liability and debtor of the company. On the basis of all the information they generally try to fix

the valuation of the company and on the basis of same they used to decide whether to invest

money into the company or not. Hence Investor generally uses the feature of Valuation of

company feature in the market.

2

Question 1b)

Feature of information of financial statement

Financial statements are important for variety of the different parties interested in the

performance of business (Pelekh, Khocha and Holovchak, 2020). Financial Statement generally

contain significant amount of the information about a company financial health. This information

is used by different user to perform variety of different activity. Some of the advantages of

financial information statement are as follows:

Decision making: It is the first feature of information which is performed by the

financial statement information. This sort of the information is generally used by the company

management in the long run. It has been identified that management generally used to analysis

the financial statement of the company on the monthly or the timely basis in the organization.

The main motive of management behind analysing the same in the organization is to find out

variety of the deficit which is presented in the performance of the business across the time. After

that management generally try to find out the solution within the financial statement or from

outside of the same as well. On the basis of variety of different information which is gather from

the financial statement and from outside management generally used to make variety of different

decision in the organization to improve the efficiency of variety of operation. Hence company

management generally uses the financial statement information in taking variety of decision

making.

Valuation of Company: It is another important feature of information presented in the

financial statement of the company. This type of the feature is generally used by the Investor or

the Bank. As investor and Loan provider in the market generally looks at the position of the

business before investing any sort of the money in the organization. Investor and Bank Loan

provider generally looks for the information related to return on the capital and resources and

liability and debtor of the company. On the basis of all the information they generally try to fix

the valuation of the company and on the basis of same they used to decide whether to invest

money into the company or not. Hence Investor generally uses the feature of Valuation of

company feature in the market.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation: It is another feature of information presented in the financial statement of the

company. This sort of the feature is generally used by the Government of the nation.

Government of the nation is another user of the financial statement of the company. Government

of the nation generally looks to financial statement with the purpose of the fixing it up the

taxation of the company in the long run. Hence they generally looks at the information of the

revenue, liability and resources sell or bought in the financial year. Hence Government is one of

the users of the financial statement of the company and on the basis of the same Government

looks to fix the taxation of the company or the liability of company on to the Government of the

nation.

Budget Formation: Budget formation is also the feature of information presented in the

financial statement of the company (Kutsyk, Shevchuk and Holovatska, 2018). This sort of

information is generally used by the planner or employee in the organization who are having the

responsibility of planning the future activity of the company in the market. They generally looks

at the financial position of the company in the market and on the basis of the same employee in

the organization used to fix the different assumption and permutation in the market and try to

draw the future budget of the company. On the basis of the same company used to carry out

variety of different activity by keeping budget of the company in mind. Hence Employee are

another user of the financial statement information. They generally used to use the same to plan

variety of different activity which need to be carried out by them in the coming future.

Current position of business: It is another feature of information of the financial

statement of the company in the market. It has been identified that these sort of the information is

generally used by the stakeholder of the company in the market. They generally used to consider

the same for understanding the current position of the business. As they are owner of the

company they understand the resources and liability of the company in the market and on the

basis of the same they looks to guide the variety of the information to the management of the

company to improve the position of the company in the market (Lapiţkaia and Leahovcenco,

2020). As stakeholder are the one who used to possess good sort of the information about the

market condition of the company and on the basis of the same they try to fix the position of the

company in the market in a way that they used to present the company in the better way in front

of the other in the market. Hence Stakeholder are the other user in the market which generally

used to consider the information from the financial statement to understand current position and

3

company. This sort of the feature is generally used by the Government of the nation.

Government of the nation is another user of the financial statement of the company. Government

of the nation generally looks to financial statement with the purpose of the fixing it up the

taxation of the company in the long run. Hence they generally looks at the information of the

revenue, liability and resources sell or bought in the financial year. Hence Government is one of

the users of the financial statement of the company and on the basis of the same Government

looks to fix the taxation of the company or the liability of company on to the Government of the

nation.

Budget Formation: Budget formation is also the feature of information presented in the

financial statement of the company (Kutsyk, Shevchuk and Holovatska, 2018). This sort of

information is generally used by the planner or employee in the organization who are having the

responsibility of planning the future activity of the company in the market. They generally looks

at the financial position of the company in the market and on the basis of the same employee in

the organization used to fix the different assumption and permutation in the market and try to

draw the future budget of the company. On the basis of the same company used to carry out

variety of different activity by keeping budget of the company in mind. Hence Employee are

another user of the financial statement information. They generally used to use the same to plan

variety of different activity which need to be carried out by them in the coming future.

Current position of business: It is another feature of information of the financial

statement of the company in the market. It has been identified that these sort of the information is

generally used by the stakeholder of the company in the market. They generally used to consider

the same for understanding the current position of the business. As they are owner of the

company they understand the resources and liability of the company in the market and on the

basis of the same they looks to guide the variety of the information to the management of the

company to improve the position of the company in the market (Lapiţkaia and Leahovcenco,

2020). As stakeholder are the one who used to possess good sort of the information about the

market condition of the company and on the basis of the same they try to fix the position of the

company in the market in a way that they used to present the company in the better way in front

of the other in the market. Hence Stakeholder are the other user in the market which generally

used to consider the information from the financial statement to understand current position and

3

improve the position or the image of the company so that future uncertainty can be managed by

the company in the better way.

Coordinating: It is another feature of the information which is gather from the financial

statement of the company (Duvanskaya and Ol’ga, 2016). As it has been identified that

Company management generally used to see the current position of the company and on the

basis of the same they look to coordinate the position of the company in the way it help them in

coordinating with variety of the future situation which may occur in the market. As it has been

identified that coordinating the current activities with future uncertainty generally help the

company in getting ready for future difficult. Competitor in the market also some time looks into

the financial statement of the company and on the basis of same try to coordinate own activity in

a way that they used to get the competitive advantage in the market as well.

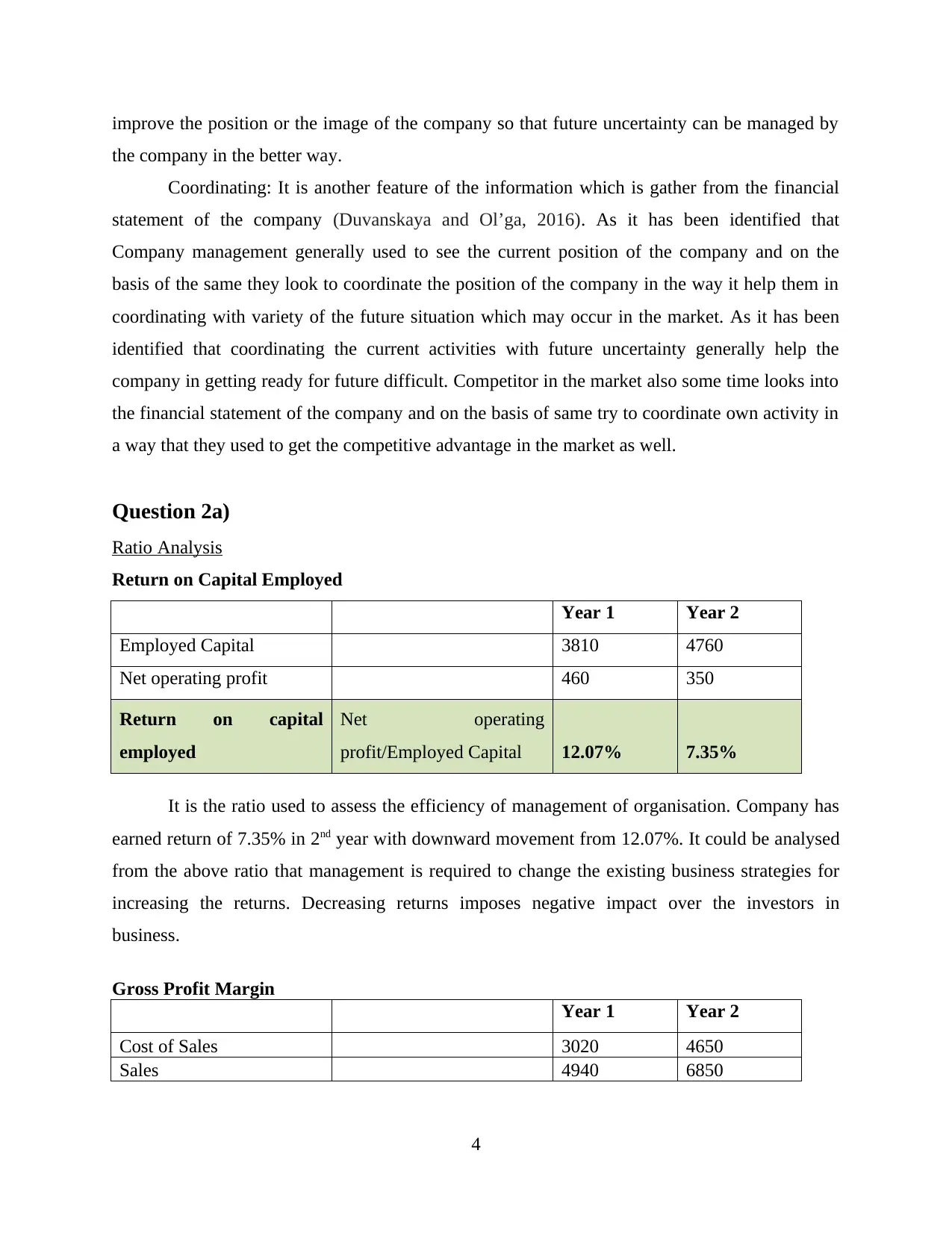

Question 2a)

Ratio Analysis

Return on Capital Employed

Year 1 Year 2

Employed Capital 3810 4760

Net operating profit 460 350

Return on capital

employed

Net operating

profit/Employed Capital 12.07% 7.35%

It is the ratio used to assess the efficiency of management of organisation. Company has

earned return of 7.35% in 2nd year with downward movement from 12.07%. It could be analysed

from the above ratio that management is required to change the existing business strategies for

increasing the returns. Decreasing returns imposes negative impact over the investors in

business.

Gross Profit Margin

Year 1 Year 2

Cost of Sales 3020 4650

Sales 4940 6850

4

the company in the better way.

Coordinating: It is another feature of the information which is gather from the financial

statement of the company (Duvanskaya and Ol’ga, 2016). As it has been identified that

Company management generally used to see the current position of the company and on the

basis of the same they look to coordinate the position of the company in the way it help them in

coordinating with variety of the future situation which may occur in the market. As it has been

identified that coordinating the current activities with future uncertainty generally help the

company in getting ready for future difficult. Competitor in the market also some time looks into

the financial statement of the company and on the basis of same try to coordinate own activity in

a way that they used to get the competitive advantage in the market as well.

Question 2a)

Ratio Analysis

Return on Capital Employed

Year 1 Year 2

Employed Capital 3810 4760

Net operating profit 460 350

Return on capital

employed

Net operating

profit/Employed Capital 12.07% 7.35%

It is the ratio used to assess the efficiency of management of organisation. Company has

earned return of 7.35% in 2nd year with downward movement from 12.07%. It could be analysed

from the above ratio that management is required to change the existing business strategies for

increasing the returns. Decreasing returns imposes negative impact over the investors in

business.

Gross Profit Margin

Year 1 Year 2

Cost of Sales 3020 4650

Sales 4940 6850

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

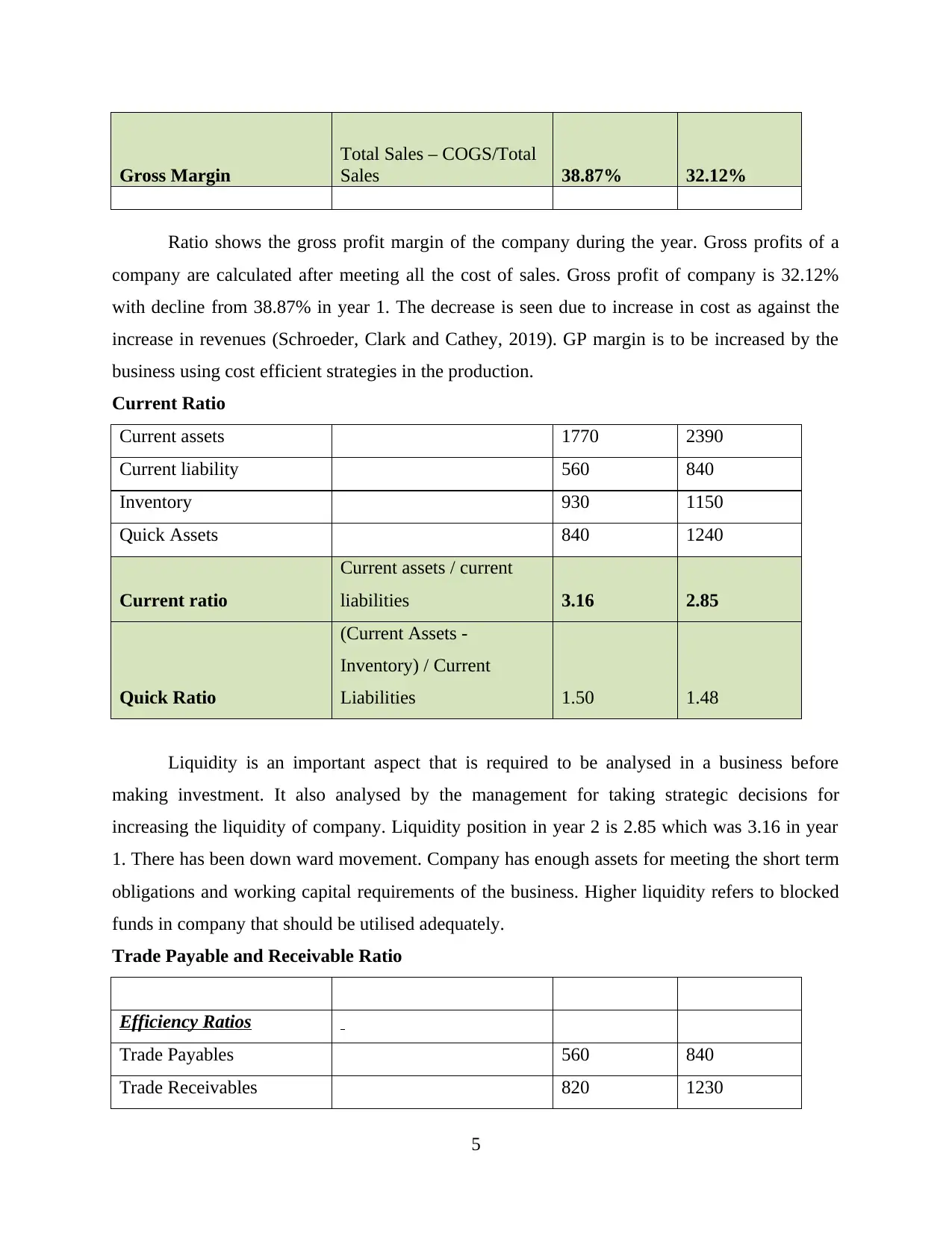

Gross Margin

Total Sales – COGS/Total

Sales 38.87% 32.12%

Ratio shows the gross profit margin of the company during the year. Gross profits of a

company are calculated after meeting all the cost of sales. Gross profit of company is 32.12%

with decline from 38.87% in year 1. The decrease is seen due to increase in cost as against the

increase in revenues (Schroeder, Clark and Cathey, 2019). GP margin is to be increased by the

business using cost efficient strategies in the production.

Current Ratio

Current assets 1770 2390

Current liability 560 840

Inventory 930 1150

Quick Assets 840 1240

Current ratio

Current assets / current

liabilities 3.16 2.85

Quick Ratio

(Current Assets -

Inventory) / Current

Liabilities 1.50 1.48

Liquidity is an important aspect that is required to be analysed in a business before

making investment. It also analysed by the management for taking strategic decisions for

increasing the liquidity of company. Liquidity position in year 2 is 2.85 which was 3.16 in year

1. There has been down ward movement. Company has enough assets for meeting the short term

obligations and working capital requirements of the business. Higher liquidity refers to blocked

funds in company that should be utilised adequately.

Trade Payable and Receivable Ratio

Efficiency Ratios

Trade Payables 560 840

Trade Receivables 820 1230

5

Total Sales – COGS/Total

Sales 38.87% 32.12%

Ratio shows the gross profit margin of the company during the year. Gross profits of a

company are calculated after meeting all the cost of sales. Gross profit of company is 32.12%

with decline from 38.87% in year 1. The decrease is seen due to increase in cost as against the

increase in revenues (Schroeder, Clark and Cathey, 2019). GP margin is to be increased by the

business using cost efficient strategies in the production.

Current Ratio

Current assets 1770 2390

Current liability 560 840

Inventory 930 1150

Quick Assets 840 1240

Current ratio

Current assets / current

liabilities 3.16 2.85

Quick Ratio

(Current Assets -

Inventory) / Current

Liabilities 1.50 1.48

Liquidity is an important aspect that is required to be analysed in a business before

making investment. It also analysed by the management for taking strategic decisions for

increasing the liquidity of company. Liquidity position in year 2 is 2.85 which was 3.16 in year

1. There has been down ward movement. Company has enough assets for meeting the short term

obligations and working capital requirements of the business. Higher liquidity refers to blocked

funds in company that should be utilised adequately.

Trade Payable and Receivable Ratio

Efficiency Ratios

Trade Payables 560 840

Trade Receivables 820 1230

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales 4940 6850

Days 365 365

Trade Payable days

Accounts Payable / Sales

*365 41.38 44.76

Trade Receivable days

Accounts Receivables /

Sales *365 60.59 65.54

Trade payable days of company are 45 that have increased from 41 days in year 1. The

increase in payments days have been made from the last year to manage the cash operating cycle

of the business.

Trade receivable days are 65 that have increased from 61 in year 1. Company has

increased its collection days in year 2 as part of the sales promotional policy (Dutta and

Patatoukas, 2017). Higher credit days enable the company to increase the sales revenue and

managing the cash operating cycle.

Question 2b)

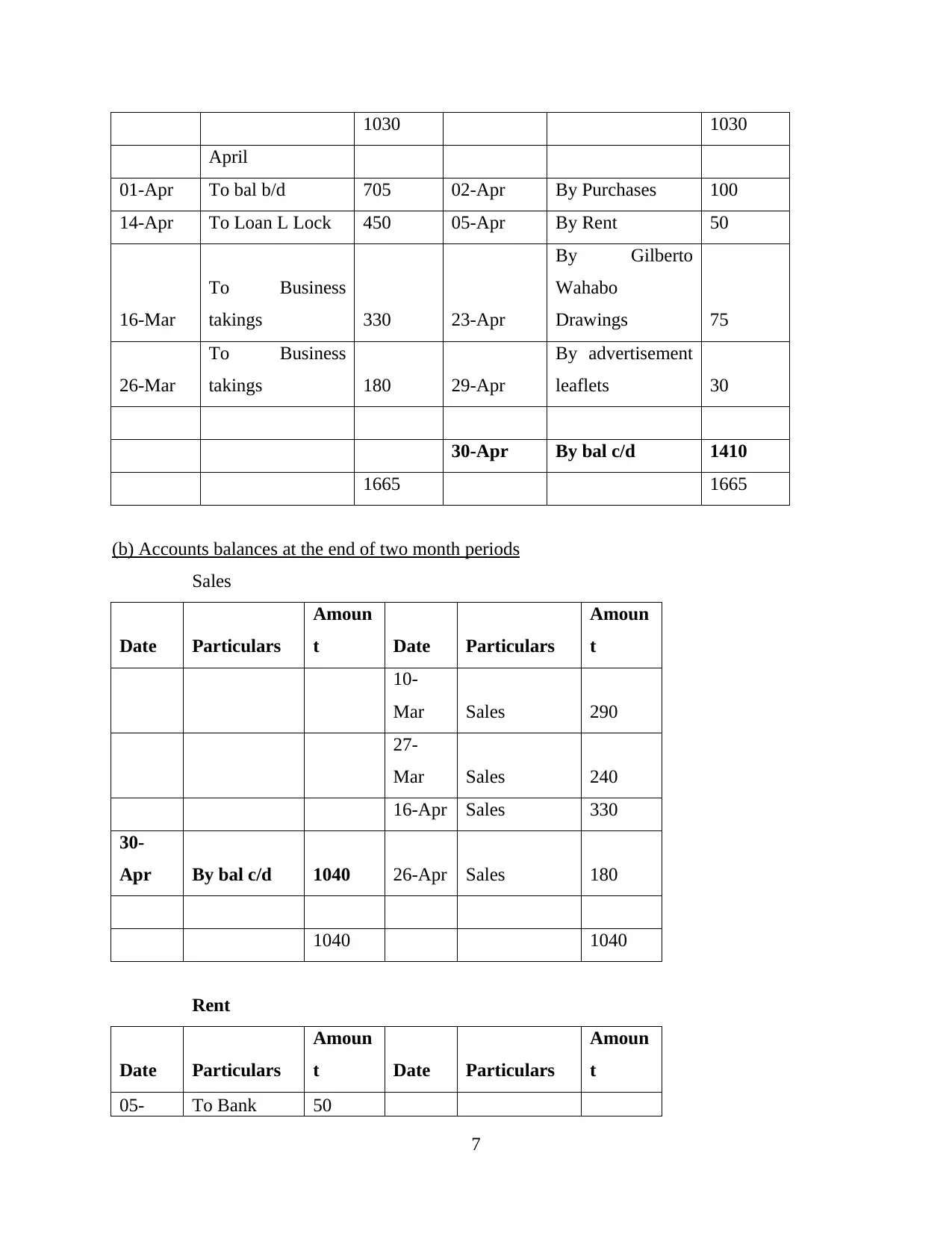

(a) Bank account balancing at the end of each month

Date Particulars Amount Date Particulars Amount

01-Mar To Capital 500

10-Mar

To Business

takings to date 290 01-Mar By Purchases 150

27-Mar

To Business

takings to date 240 05-Mar By Rent 50

22-Mar By Advertising 25

26-Mar

By Gilberto

Wahabo

Drawings 100

31-Mar By bal c/d 705

6

Days 365 365

Trade Payable days

Accounts Payable / Sales

*365 41.38 44.76

Trade Receivable days

Accounts Receivables /

Sales *365 60.59 65.54

Trade payable days of company are 45 that have increased from 41 days in year 1. The

increase in payments days have been made from the last year to manage the cash operating cycle

of the business.

Trade receivable days are 65 that have increased from 61 in year 1. Company has

increased its collection days in year 2 as part of the sales promotional policy (Dutta and

Patatoukas, 2017). Higher credit days enable the company to increase the sales revenue and

managing the cash operating cycle.

Question 2b)

(a) Bank account balancing at the end of each month

Date Particulars Amount Date Particulars Amount

01-Mar To Capital 500

10-Mar

To Business

takings to date 290 01-Mar By Purchases 150

27-Mar

To Business

takings to date 240 05-Mar By Rent 50

22-Mar By Advertising 25

26-Mar

By Gilberto

Wahabo

Drawings 100

31-Mar By bal c/d 705

6

1030 1030

April

01-Apr To bal b/d 705 02-Apr By Purchases 100

14-Apr To Loan L Lock 450 05-Apr By Rent 50

16-Mar

To Business

takings 330 23-Apr

By Gilberto

Wahabo

Drawings 75

26-Mar

To Business

takings 180 29-Apr

By advertisement

leaflets 30

30-Apr By bal c/d 1410

1665 1665

(b) Accounts balances at the end of two month periods

Sales

Date Particulars

Amoun

t Date Particulars

Amoun

t

10-

Mar Sales 290

27-

Mar Sales 240

16-Apr Sales 330

30-

Apr By bal c/d 1040 26-Apr Sales 180

1040 1040

Rent

Date Particulars

Amoun

t Date Particulars

Amoun

t

05- To Bank 50

7

April

01-Apr To bal b/d 705 02-Apr By Purchases 100

14-Apr To Loan L Lock 450 05-Apr By Rent 50

16-Mar

To Business

takings 330 23-Apr

By Gilberto

Wahabo

Drawings 75

26-Mar

To Business

takings 180 29-Apr

By advertisement

leaflets 30

30-Apr By bal c/d 1410

1665 1665

(b) Accounts balances at the end of two month periods

Sales

Date Particulars

Amoun

t Date Particulars

Amoun

t

10-

Mar Sales 290

27-

Mar Sales 240

16-Apr Sales 330

30-

Apr By bal c/d 1040 26-Apr Sales 180

1040 1040

Rent

Date Particulars

Amoun

t Date Particulars

Amoun

t

05- To Bank 50

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

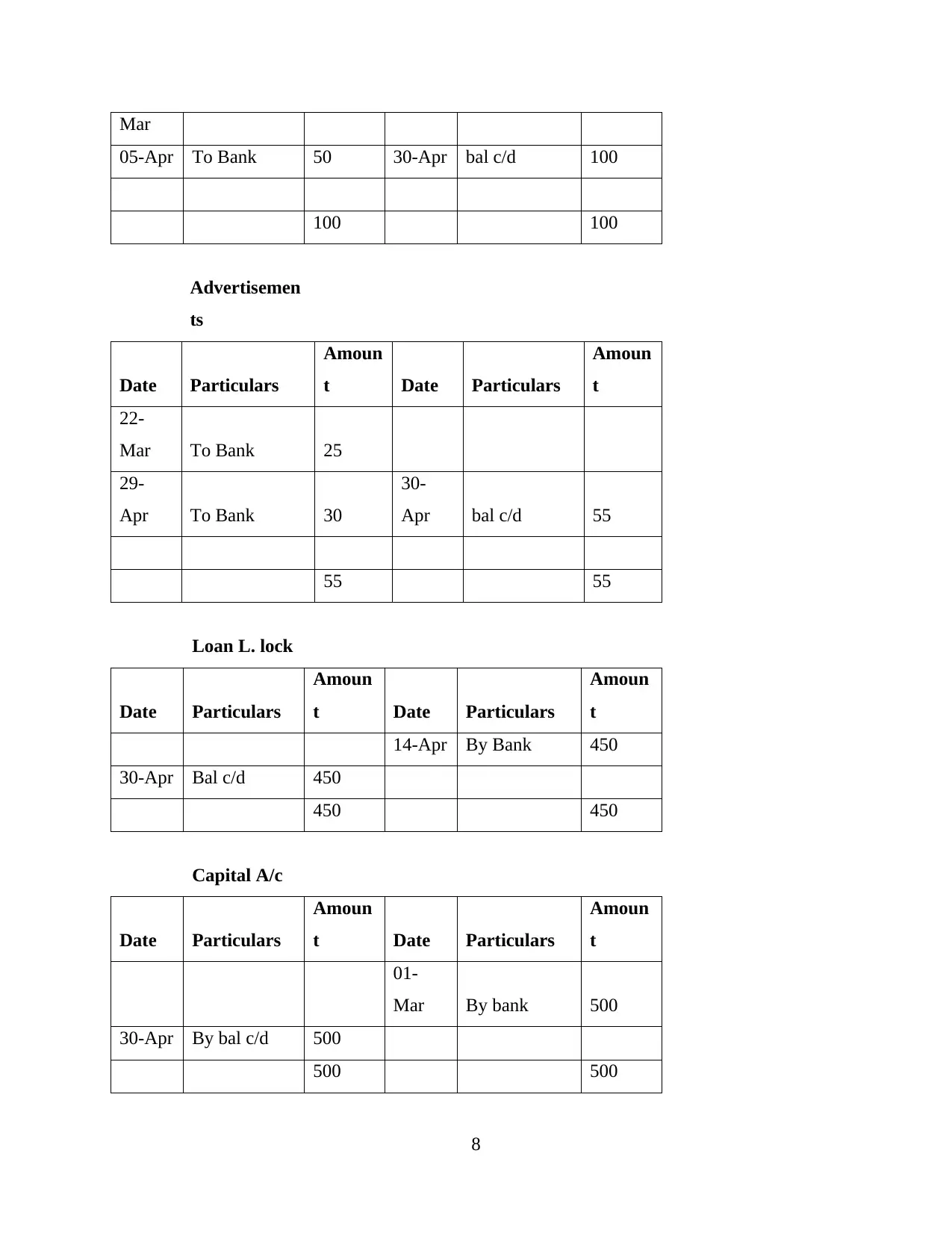

Mar

05-Apr To Bank 50 30-Apr bal c/d 100

100 100

Advertisemen

ts

Date Particulars

Amoun

t Date Particulars

Amoun

t

22-

Mar To Bank 25

29-

Apr To Bank 30

30-

Apr bal c/d 55

55 55

Loan L. lock

Date Particulars

Amoun

t Date Particulars

Amoun

t

14-Apr By Bank 450

30-Apr Bal c/d 450

450 450

Capital A/c

Date Particulars

Amoun

t Date Particulars

Amoun

t

01-

Mar By bank 500

30-Apr By bal c/d 500

500 500

8

05-Apr To Bank 50 30-Apr bal c/d 100

100 100

Advertisemen

ts

Date Particulars

Amoun

t Date Particulars

Amoun

t

22-

Mar To Bank 25

29-

Apr To Bank 30

30-

Apr bal c/d 55

55 55

Loan L. lock

Date Particulars

Amoun

t Date Particulars

Amoun

t

14-Apr By Bank 450

30-Apr Bal c/d 450

450 450

Capital A/c

Date Particulars

Amoun

t Date Particulars

Amoun

t

01-

Mar By bank 500

30-Apr By bal c/d 500

500 500

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

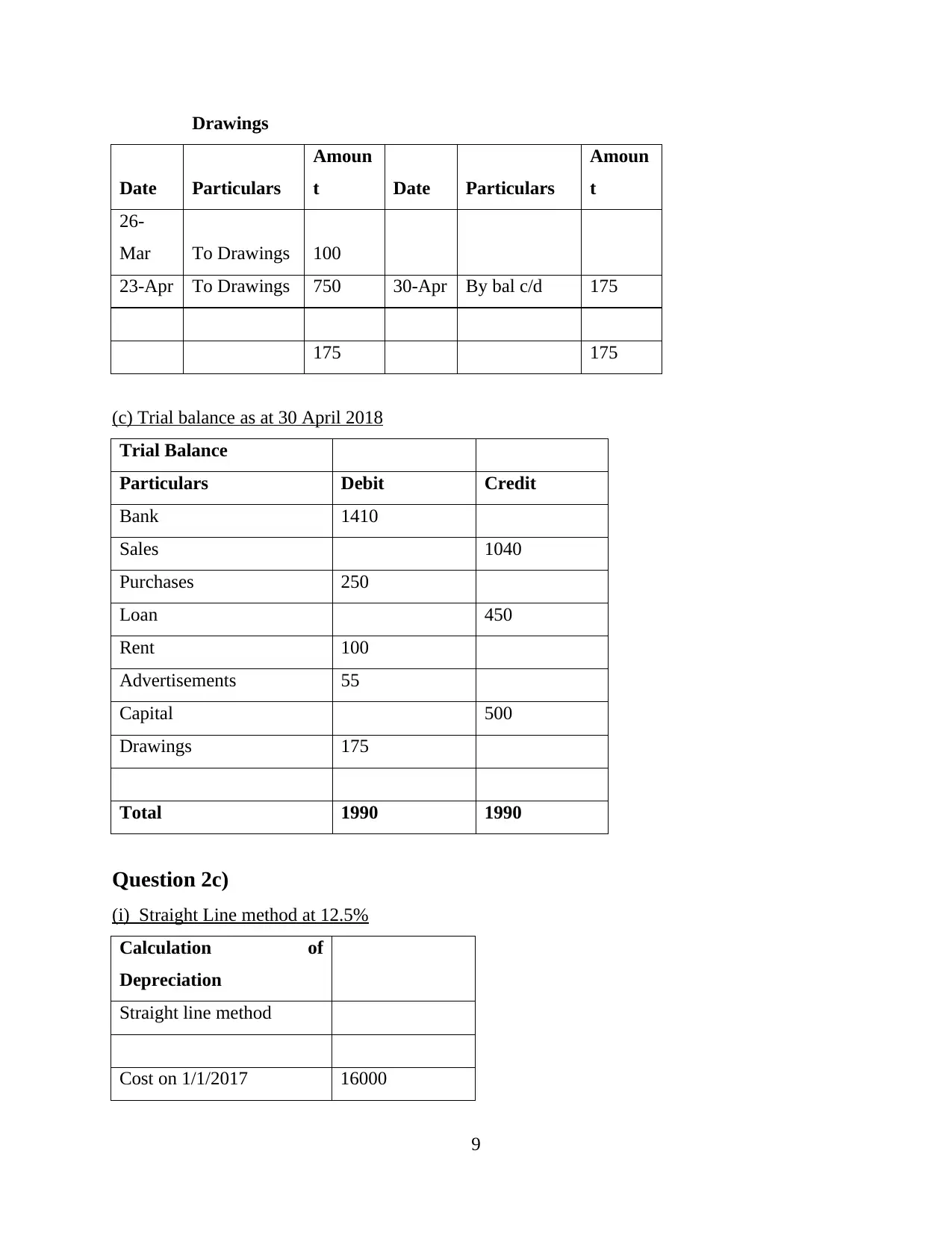

Drawings

Date Particulars

Amoun

t Date Particulars

Amoun

t

26-

Mar To Drawings 100

23-Apr To Drawings 750 30-Apr By bal c/d 175

175 175

(c) Trial balance as at 30 April 2018

Trial Balance

Particulars Debit Credit

Bank 1410

Sales 1040

Purchases 250

Loan 450

Rent 100

Advertisements 55

Capital 500

Drawings 175

Total 1990 1990

Question 2c)

(i) Straight Line method at 12.5%

Calculation of

Depreciation

Straight line method

Cost on 1/1/2017 16000

9

Date Particulars

Amoun

t Date Particulars

Amoun

t

26-

Mar To Drawings 100

23-Apr To Drawings 750 30-Apr By bal c/d 175

175 175

(c) Trial balance as at 30 April 2018

Trial Balance

Particulars Debit Credit

Bank 1410

Sales 1040

Purchases 250

Loan 450

Rent 100

Advertisements 55

Capital 500

Drawings 175

Total 1990 1990

Question 2c)

(i) Straight Line method at 12.5%

Calculation of

Depreciation

Straight line method

Cost on 1/1/2017 16000

9

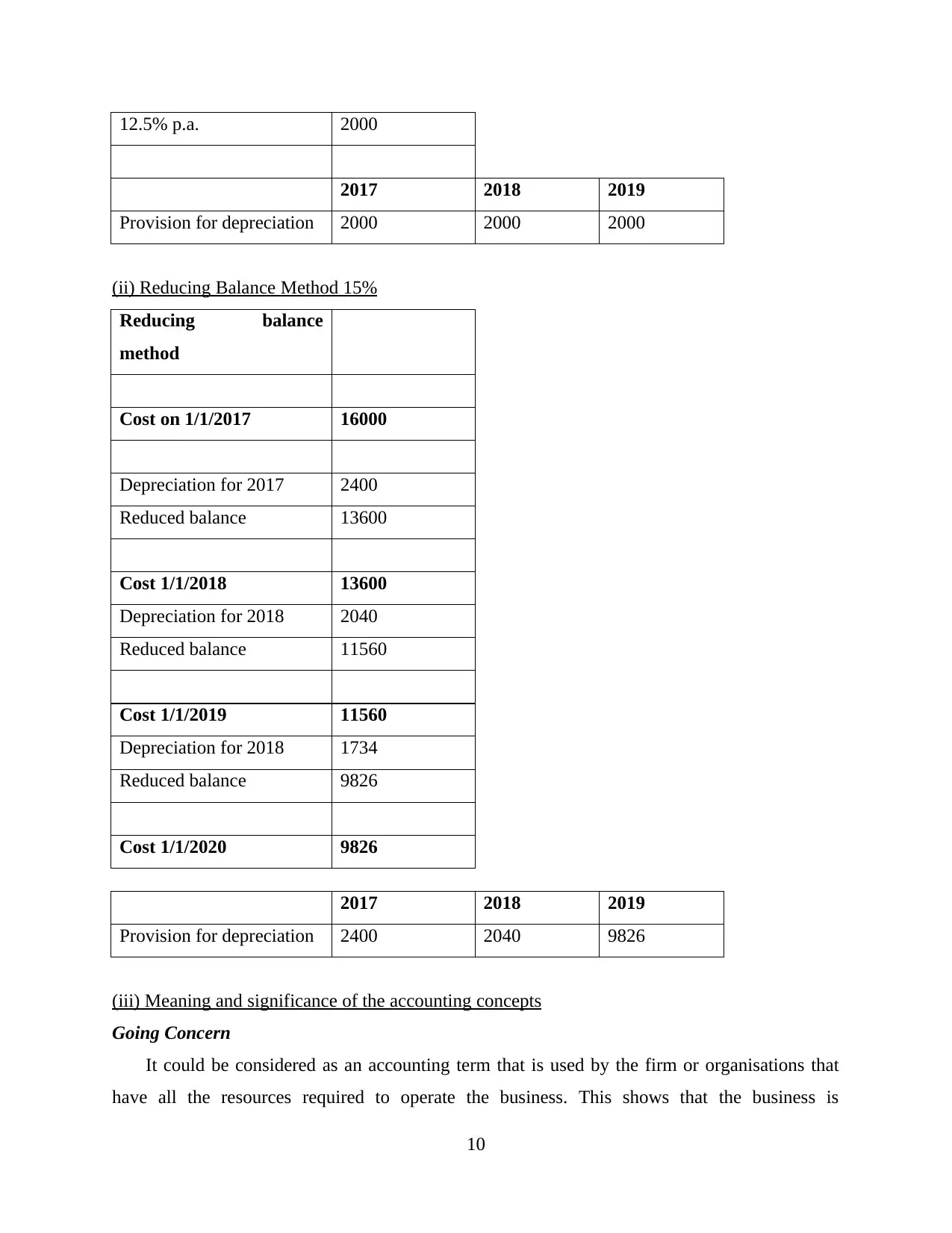

12.5% p.a. 2000

2017 2018 2019

Provision for depreciation 2000 2000 2000

(ii) Reducing Balance Method 15%

Reducing balance

method

Cost on 1/1/2017 16000

Depreciation for 2017 2400

Reduced balance 13600

Cost 1/1/2018 13600

Depreciation for 2018 2040

Reduced balance 11560

Cost 1/1/2019 11560

Depreciation for 2018 1734

Reduced balance 9826

Cost 1/1/2020 9826

2017 2018 2019

Provision for depreciation 2400 2040 9826

(iii) Meaning and significance of the accounting concepts

Going Concern

It could be considered as an accounting term that is used by the firm or organisations that

have all the resources required to operate the business. This shows that the business is

10

2017 2018 2019

Provision for depreciation 2000 2000 2000

(ii) Reducing Balance Method 15%

Reducing balance

method

Cost on 1/1/2017 16000

Depreciation for 2017 2400

Reduced balance 13600

Cost 1/1/2018 13600

Depreciation for 2018 2040

Reduced balance 11560

Cost 1/1/2019 11560

Depreciation for 2018 1734

Reduced balance 9826

Cost 1/1/2020 9826

2017 2018 2019

Provision for depreciation 2400 2040 9826

(iii) Meaning and significance of the accounting concepts

Going Concern

It could be considered as an accounting term that is used by the firm or organisations that

have all the resources required to operate the business. This shows that the business is

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.