UG221 Financial Accounting: Consolidated Statements & Performance

VerifiedAdded on 2023/06/14

|13

|4056

|397

Report

AI Summary

This financial accounting report focuses on consolidated financial statements and the financial performance of Patrick Financial Services. It includes the preparation of a consolidated statement of financial position for the Pee group, calculation of goodwill and non-controlling interest. The report assesses Patrick Financial Services' profitability, growth, and credit management using financial data, comparing performance across financial years. It also discusses the importance of reliability, relevance, and comparability in financial reporting, emphasizing adherence to accounting standards and policies for accurate and useful financial information. Desklib offers this and many other solved assignments to help students.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................4

Question 1 A................................................................................................................................4

b. Making financial information useful through required level of reliability, relevance and

comparability...............................................................................................................................6

Question 2........................................................................................................................................8

(a).................................................................................................................................................8

B.................................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................4

Question 1 A................................................................................................................................4

b. Making financial information useful through required level of reliability, relevance and

comparability...............................................................................................................................6

Question 2........................................................................................................................................8

(a).................................................................................................................................................8

B.................................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial accounting is a practice of recording to the financial transaction of the business.

This project will emphasis over the consolidated financial statement of the company. Further the

performance of business will monitor. Professional ethics of accountant will also disclose in this

report.

MAIN BODY

Question 1 A

Particulars Amount

Non – current assets

Property plant & equipment (160000 + 50000) 210000

Goodwill 20000

230000

Current assets (30000 + 10000) 40000

TOTAL ASSETS 270000

Equity & liabilities

Ordinary shares at £ 1 each 100000

Retained profits 158000

Non – controlling interest 12000

TOTAL OF EQUITY & LIABILITIES 270000

Working notes:

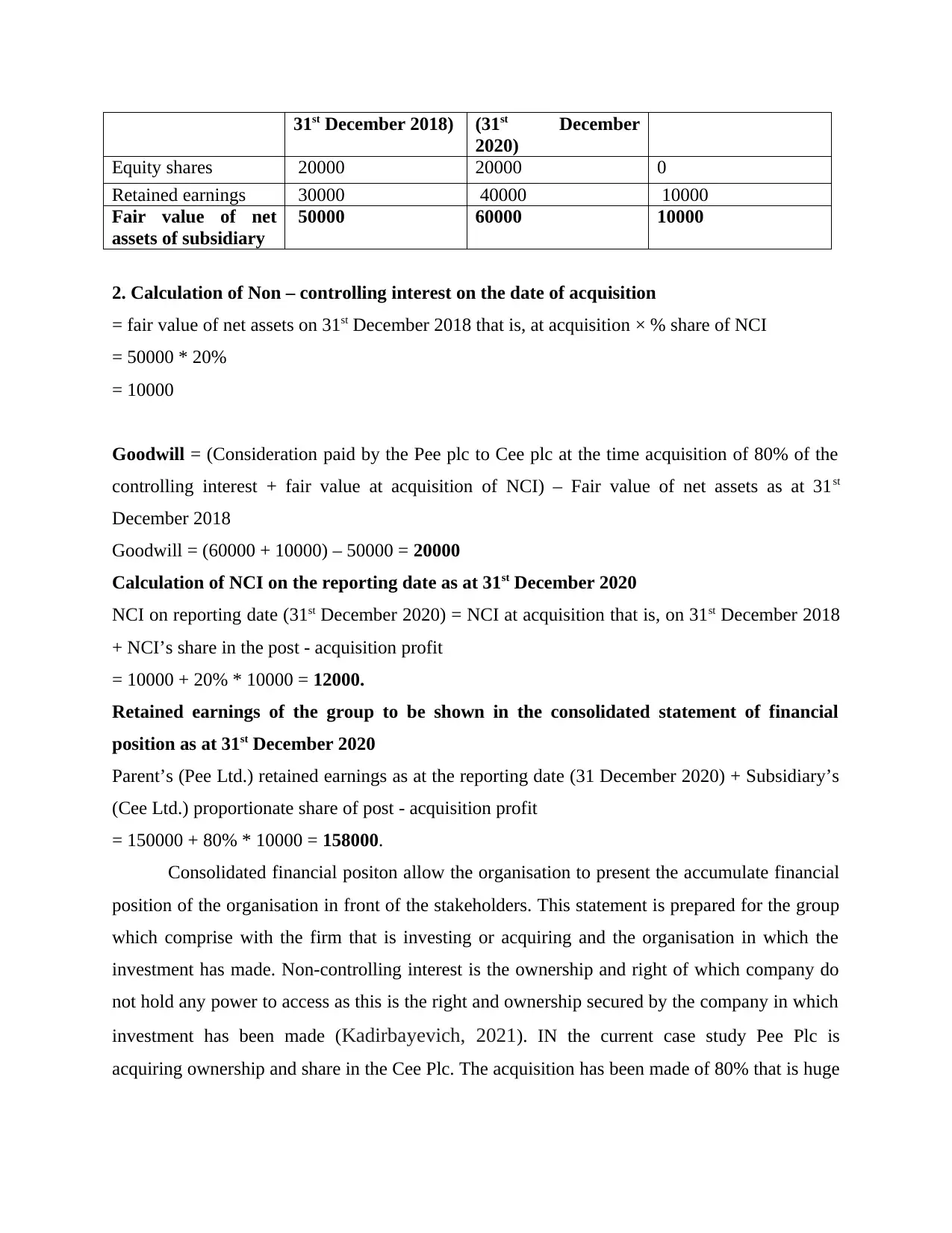

1. Calculation of Net assets for the Subsidiary Co. i.e., Cee plc

Particulars At acquisition (as at At Reporting date Post - acquisition

Financial accounting is a practice of recording to the financial transaction of the business.

This project will emphasis over the consolidated financial statement of the company. Further the

performance of business will monitor. Professional ethics of accountant will also disclose in this

report.

MAIN BODY

Question 1 A

Particulars Amount

Non – current assets

Property plant & equipment (160000 + 50000) 210000

Goodwill 20000

230000

Current assets (30000 + 10000) 40000

TOTAL ASSETS 270000

Equity & liabilities

Ordinary shares at £ 1 each 100000

Retained profits 158000

Non – controlling interest 12000

TOTAL OF EQUITY & LIABILITIES 270000

Working notes:

1. Calculation of Net assets for the Subsidiary Co. i.e., Cee plc

Particulars At acquisition (as at At Reporting date Post - acquisition

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

31st December 2018) (31st December

2020)

Equity shares 20000 20000 0

Retained earnings 30000 40000 10000

Fair value of net

assets of subsidiary

50000 60000 10000

2. Calculation of Non – controlling interest on the date of acquisition

= fair value of net assets on 31st December 2018 that is, at acquisition × % share of NCI

= 50000 * 20%

= 10000

Goodwill = (Consideration paid by the Pee plc to Cee plc at the time acquisition of 80% of the

controlling interest + fair value at acquisition of NCI) – Fair value of net assets as at 31st

December 2018

Goodwill = (60000 + 10000) – 50000 = 20000

Calculation of NCI on the reporting date as at 31st December 2020

NCI on reporting date (31st December 2020) = NCI at acquisition that is, on 31st December 2018

+ NCI’s share in the post - acquisition profit

= 10000 + 20% * 10000 = 12000.

Retained earnings of the group to be shown in the consolidated statement of financial

position as at 31st December 2020

Parent’s (Pee Ltd.) retained earnings as at the reporting date (31 December 2020) + Subsidiary’s

(Cee Ltd.) proportionate share of post - acquisition profit

= 150000 + 80% * 10000 = 158000.

Consolidated financial positon allow the organisation to present the accumulate financial

position of the organisation in front of the stakeholders. This statement is prepared for the group

which comprise with the firm that is investing or acquiring and the organisation in which the

investment has made. Non-controlling interest is the ownership and right of which company do

not hold any power to access as this is the right and ownership secured by the company in which

investment has been made (Kadirbayevich, 2021). IN the current case study Pee Plc is

acquiring ownership and share in the Cee Plc. The acquisition has been made of 80% that is huge

2020)

Equity shares 20000 20000 0

Retained earnings 30000 40000 10000

Fair value of net

assets of subsidiary

50000 60000 10000

2. Calculation of Non – controlling interest on the date of acquisition

= fair value of net assets on 31st December 2018 that is, at acquisition × % share of NCI

= 50000 * 20%

= 10000

Goodwill = (Consideration paid by the Pee plc to Cee plc at the time acquisition of 80% of the

controlling interest + fair value at acquisition of NCI) – Fair value of net assets as at 31st

December 2018

Goodwill = (60000 + 10000) – 50000 = 20000

Calculation of NCI on the reporting date as at 31st December 2020

NCI on reporting date (31st December 2020) = NCI at acquisition that is, on 31st December 2018

+ NCI’s share in the post - acquisition profit

= 10000 + 20% * 10000 = 12000.

Retained earnings of the group to be shown in the consolidated statement of financial

position as at 31st December 2020

Parent’s (Pee Ltd.) retained earnings as at the reporting date (31 December 2020) + Subsidiary’s

(Cee Ltd.) proportionate share of post - acquisition profit

= 150000 + 80% * 10000 = 158000.

Consolidated financial positon allow the organisation to present the accumulate financial

position of the organisation in front of the stakeholders. This statement is prepared for the group

which comprise with the firm that is investing or acquiring and the organisation in which the

investment has made. Non-controlling interest is the ownership and right of which company do

not hold any power to access as this is the right and ownership secured by the company in which

investment has been made (Kadirbayevich, 2021). IN the current case study Pee Plc is

acquiring ownership and share in the Cee Plc. The acquisition has been made of 80% that is huge

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in numbers. This denote the fact that company grant the access of 80% of ownership claim in the

Cee Plc.

Non-controlling interest: refer to lack of ownership a decision making right. This is a right that

is not controllable by the firm acquired ownership in other organisation. The non-controlling

interest belong to such organisation that hold the ownership claim or investment in company less

than 50% which do not provide any significant right to make any decision of the company. As

per the generally accepted accounting principle (GAAP), NCI should be a part of liability section

of balance sheet. This will denote the ownership claim by any other firm. This further present in

the liability side of balance sheet showing the fact that the percentage or number of equity hold

by any other firm (Pisanello, 2021). The transaction related to the NCI is conducted as per the

IAS 27.

Consolidated statement of financial position: is a financial record that is combined financial

record of all the firm invested in the business. This is total and individual proportion of share

owning by every individual firm in the business (Oroh, Kalangi and Rondonuwu, 2022). Both

the company’s parent as well subsidiary claiming the interest in the firm are reflected in this

consolidated financial statement. The single statement is prepared by adding all the treatment

related to parent company and the firm to which the organisation has acquired. In the current

case single statement is prepared of both Pee Plc and Cee Plc in the form of consolidated

financial statement. The statement reflects to the overall financial position of the organisation

comprising all the parent and subsidiary firm’s involved in the ownership of business. This

statement is preparing by the group as a whole reflecting the overall financial situation of the

company as a whole.

b. Making financial information useful through required level of reliability, relevance and

comparability

It is necessary to ensure that financial statement must reflect sufficient quantity & quality

of financial information, so that reader's expectations can be satisfied in reasonable manner.

There are certain qualitative characteristics of financial statements through which financial

information provided by it can be made useful such as reliability, relevance and comparability

which will be explained in the next section of this report (Ebaid, 2021).

Relevance: The financial information can be said to be relevant if it has the ability of influencing

economic decisions made by the users of such information by assisting them in the evaluation of

Cee Plc.

Non-controlling interest: refer to lack of ownership a decision making right. This is a right that

is not controllable by the firm acquired ownership in other organisation. The non-controlling

interest belong to such organisation that hold the ownership claim or investment in company less

than 50% which do not provide any significant right to make any decision of the company. As

per the generally accepted accounting principle (GAAP), NCI should be a part of liability section

of balance sheet. This will denote the ownership claim by any other firm. This further present in

the liability side of balance sheet showing the fact that the percentage or number of equity hold

by any other firm (Pisanello, 2021). The transaction related to the NCI is conducted as per the

IAS 27.

Consolidated statement of financial position: is a financial record that is combined financial

record of all the firm invested in the business. This is total and individual proportion of share

owning by every individual firm in the business (Oroh, Kalangi and Rondonuwu, 2022). Both

the company’s parent as well subsidiary claiming the interest in the firm are reflected in this

consolidated financial statement. The single statement is prepared by adding all the treatment

related to parent company and the firm to which the organisation has acquired. In the current

case single statement is prepared of both Pee Plc and Cee Plc in the form of consolidated

financial statement. The statement reflects to the overall financial position of the organisation

comprising all the parent and subsidiary firm’s involved in the ownership of business. This

statement is preparing by the group as a whole reflecting the overall financial situation of the

company as a whole.

b. Making financial information useful through required level of reliability, relevance and

comparability

It is necessary to ensure that financial statement must reflect sufficient quantity & quality

of financial information, so that reader's expectations can be satisfied in reasonable manner.

There are certain qualitative characteristics of financial statements through which financial

information provided by it can be made useful such as reliability, relevance and comparability

which will be explained in the next section of this report (Ebaid, 2021).

Relevance: The financial information can be said to be relevant if it has the ability of influencing

economic decisions made by the users of such information by assisting them in the evaluation of

present, past and future events taking place within the business. Therefore, it is must that there

exists both confirmatory and predictive value within information. If information assists its users

in evaluating present, past and future of events, then it is said to have predictive value. The

ability of financial statements increases in terms of predicting future events with the way past

information is being presented within it. Therefore, with the required and appropriate

presentation of information, user's need of making decision can be satisfied, so that they can

predict future trends of the company's performance & position that is, predictive value through

correcting those predictions made in the past that is, confirmatory value. To enhance relevancy

of financial information, the transactions associated with disposed of and new acquired business

are stated separately from that information related to continuing operations of the business

(Wahab, Ali and Abduzahre, 2019). Accordingly, a diligent user can identify changes taking

place in financial position and performance that has resulted from normal activities, so that

prediction of future activities can be done accurately. In addition to this, relevance can be

ensured through stating recent and understandable information and provision of information in

timely manner is must, so that higher relevancy can be ensured to enhance its usefulness for

decision-making.

Reliability: To make financial information useful, it is required to be reliable. The information is

said to be reliable when there it is free from material or deliberate error to facilitate dependency

of users on it. Reliability can be ensured, if financial statements offer required level of

trustworthiness within the information provided by it (Chiyad and Mahmoud, 2019). This

characteristic of financial statement is helpful in ensuring that the information provided by it is

trustful, so that investors and creditors can make decisions such as whether to invest or lend to

the company or not. It can be ensured that the financial statement is reliable when the financial

statements get verified with some authorized body. If three attributes that is neutrality,

faithfulness and verifiability are there while presenting financial statements, then its reliability

could be confirmed. Verifiability implies that the auditor or any other investigator land at the

same outcome after measuring and evaluating financial performance of the business. In addition

to this, presenting true & fair view of the business position and taking into account unfavourable

events while preparing & presenting financial statements ensures that the financial information is

faithful and neutral respectively. Accordingly, by confirming reliability of financial information,

it becomes useful for investors and creditors in making decisions.

exists both confirmatory and predictive value within information. If information assists its users

in evaluating present, past and future of events, then it is said to have predictive value. The

ability of financial statements increases in terms of predicting future events with the way past

information is being presented within it. Therefore, with the required and appropriate

presentation of information, user's need of making decision can be satisfied, so that they can

predict future trends of the company's performance & position that is, predictive value through

correcting those predictions made in the past that is, confirmatory value. To enhance relevancy

of financial information, the transactions associated with disposed of and new acquired business

are stated separately from that information related to continuing operations of the business

(Wahab, Ali and Abduzahre, 2019). Accordingly, a diligent user can identify changes taking

place in financial position and performance that has resulted from normal activities, so that

prediction of future activities can be done accurately. In addition to this, relevance can be

ensured through stating recent and understandable information and provision of information in

timely manner is must, so that higher relevancy can be ensured to enhance its usefulness for

decision-making.

Reliability: To make financial information useful, it is required to be reliable. The information is

said to be reliable when there it is free from material or deliberate error to facilitate dependency

of users on it. Reliability can be ensured, if financial statements offer required level of

trustworthiness within the information provided by it (Chiyad and Mahmoud, 2019). This

characteristic of financial statement is helpful in ensuring that the information provided by it is

trustful, so that investors and creditors can make decisions such as whether to invest or lend to

the company or not. It can be ensured that the financial statement is reliable when the financial

statements get verified with some authorized body. If three attributes that is neutrality,

faithfulness and verifiability are there while presenting financial statements, then its reliability

could be confirmed. Verifiability implies that the auditor or any other investigator land at the

same outcome after measuring and evaluating financial performance of the business. In addition

to this, presenting true & fair view of the business position and taking into account unfavourable

events while preparing & presenting financial statements ensures that the financial information is

faithful and neutral respectively. Accordingly, by confirming reliability of financial information,

it becomes useful for investors and creditors in making decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Comparability: It is that qualitative feature of accounting information which satisfies that

policies & accounting standards are applied in consistency from one year to another (Al-Hashimi

and Mahdi, 2019). In this financial statements indicating business financial performance and

position becomes comparable from one year to another which allows its users to draw

meaningful conclusions and useful insights regarding company's performance trends over time.

Also, with the help of applying policies and accounting standards in consistency with other firms

in industry, financial performance of one firm can be compared with another firm's performance

and thus investors can make decisions regarding where to invest and creditors can make

decisions about to whom they should lend their money. In addition to this, if any changes

took place in following certain accounting policies or standards, then it must be disclosed within

the notes to account such policy changes and its impact on the financial performance and

position of a concern (Al-Dmour, Abbod and Al-Balqa, 2018). In this way, users can be able to

compare financial information of various periods and of other companies as well. It can be said

that by achieving consistency in preparing financial statements, it can be ensured that financial

information is comparable and can be used for analysing performance trends and predicting

future events in performance as well.

Question 2

(a)

(in) Comment on financial performance of Patrick Financial services using financial data

Financial performance of the Patrick Financial Service Company is based on the certain

criteria and aspects. The overall performance of the venture is totally based on the certain aspect

that can demonstrate as the profits, growth and credit management. All these are the fundamental

basis to demonstrate the performance of the venture in the respective target market. All these

aspects critically demonstrate to the overall performance of organisation in respective financial

year.

Profitability

Appendix 1 of the Financial Statement reflect the fact that the performance of the

organisation in term of profitability is similar to what company has achieved in the earlier

financial year. IN the previous financial year, the net profit margin of the Patrick Financial

Service was 20% (180 / 900 * 100(which is similar to the current financial year in which also

organisation could go through to the 20% profit margin (187 / 945 * 100). Profitability is one of

policies & accounting standards are applied in consistency from one year to another (Al-Hashimi

and Mahdi, 2019). In this financial statements indicating business financial performance and

position becomes comparable from one year to another which allows its users to draw

meaningful conclusions and useful insights regarding company's performance trends over time.

Also, with the help of applying policies and accounting standards in consistency with other firms

in industry, financial performance of one firm can be compared with another firm's performance

and thus investors can make decisions regarding where to invest and creditors can make

decisions about to whom they should lend their money. In addition to this, if any changes

took place in following certain accounting policies or standards, then it must be disclosed within

the notes to account such policy changes and its impact on the financial performance and

position of a concern (Al-Dmour, Abbod and Al-Balqa, 2018). In this way, users can be able to

compare financial information of various periods and of other companies as well. It can be said

that by achieving consistency in preparing financial statements, it can be ensured that financial

information is comparable and can be used for analysing performance trends and predicting

future events in performance as well.

Question 2

(a)

(in) Comment on financial performance of Patrick Financial services using financial data

Financial performance of the Patrick Financial Service Company is based on the certain

criteria and aspects. The overall performance of the venture is totally based on the certain aspect

that can demonstrate as the profits, growth and credit management. All these are the fundamental

basis to demonstrate the performance of the venture in the respective target market. All these

aspects critically demonstrate to the overall performance of organisation in respective financial

year.

Profitability

Appendix 1 of the Financial Statement reflect the fact that the performance of the

organisation in term of profitability is similar to what company has achieved in the earlier

financial year. IN the previous financial year, the net profit margin of the Patrick Financial

Service was 20% (180 / 900 * 100(which is similar to the current financial year in which also

organisation could go through to the 20% profit margin (187 / 945 * 100). Profitability is one of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the most significant factor or element that reflect about the performance business could achieve

in the market. 20% is a good and healthy rate in term of net profits. Company could not increase

this share of profits irrespective to the fact that organisation could increase its sale in the current

financial year (Dalwai and Salehi, 2021). Every organisation always aims to increase the share

of profits in the market. In the upcoming financial year company should also focus over

increasing the profit margin along with the sales of the business. The same amount of profits

demonstrates the feature or the fact that company hold this ability to sustain the profit margin

which further empower to the organisation for taking up the competitive advantage. Other

expenses can be controlled by the venture in process to boost the net profit margin of the

business.

Growth

Patrick Financial Services could address the sales growth of 5% (945 – 900 / 900 * 100)

in compare to the earlier financial year. Further the growth rate identify in net profits are 3.88%

(187 – 180 / 180 * 100). These values are clearly showing the fact that company has been

capable to increase its profitability along with sales of the company. Increasing sales of the

venture is a positive indicator and sign for the organisation. Every organisation aims to boost the

sales of the company in order to maximise the overall performance of the venture in respective

financial year. Increase sales ratio is a very productive and positive sign and indicate for the

company to entertain more favourable performance margin of the venture in compare to the

earlier financial years (Tanko and et.al., 2021). Growth is always the primary objective and

aim associated with the business. Even if the net profit margin of company remains the same the

increasing sales provide the opportunity to the organisation to maximise the overall growth and

development of the venture in respective target market.

Credit Management

Credit management of the Patrick Company is better in compare top the earlier financial

year. The average collection period from debtor could go down to 18 from 22. Industry average

on the other hand is 30 which reflect that company is doing far better job in this area (Dao,

2021). The credit management of the organisation is improving which is a positive sign or

indicator for the company.

ii) Financial performance indicators are useful for showing past financial performance or success

of the business. It can never be guaranteed that whatever financial performance was there in the

in the market. 20% is a good and healthy rate in term of net profits. Company could not increase

this share of profits irrespective to the fact that organisation could increase its sale in the current

financial year (Dalwai and Salehi, 2021). Every organisation always aims to increase the share

of profits in the market. In the upcoming financial year company should also focus over

increasing the profit margin along with the sales of the business. The same amount of profits

demonstrates the feature or the fact that company hold this ability to sustain the profit margin

which further empower to the organisation for taking up the competitive advantage. Other

expenses can be controlled by the venture in process to boost the net profit margin of the

business.

Growth

Patrick Financial Services could address the sales growth of 5% (945 – 900 / 900 * 100)

in compare to the earlier financial year. Further the growth rate identify in net profits are 3.88%

(187 – 180 / 180 * 100). These values are clearly showing the fact that company has been

capable to increase its profitability along with sales of the company. Increasing sales of the

venture is a positive indicator and sign for the organisation. Every organisation aims to boost the

sales of the company in order to maximise the overall performance of the venture in respective

financial year. Increase sales ratio is a very productive and positive sign and indicate for the

company to entertain more favourable performance margin of the venture in compare to the

earlier financial years (Tanko and et.al., 2021). Growth is always the primary objective and

aim associated with the business. Even if the net profit margin of company remains the same the

increasing sales provide the opportunity to the organisation to maximise the overall growth and

development of the venture in respective target market.

Credit Management

Credit management of the Patrick Company is better in compare top the earlier financial

year. The average collection period from debtor could go down to 18 from 22. Industry average

on the other hand is 30 which reflect that company is doing far better job in this area (Dao,

2021). The credit management of the organisation is improving which is a positive sign or

indicator for the company.

ii) Financial performance indicators are useful for showing past financial performance or success

of the business. It can never be guaranteed that whatever financial performance was there in the

past would remain the same in future or there will be the similar trends in performance that was

present in the past. There are many circumstances that could take place in upcoming year which

lead to losses for the company such as higher costs and losing clients. This may affect the

profitability of the business and accordingly, there would be poor performance in the future as

against good performance in past many years.

On the other hand, non-financial performance indicators are often regarded as measures

of future performance. For instance, if there is a greater quality of company's product, then in the

years to come there are higher probability of getting more clients, retaining the existing client

base along with raising price of product or service which provides additional revenue and profit

margins to the company respectively (Maletič, Gomišček and Maletič, 2021). Non-financial

measures of company's performance are indicated within balanced scorecard which have various

particulars within which different non-financial measures of performance are mentioned to

indicate non-financial performance of the business. For example, internal business processes

show internal efficiency of business, customer knowledge shows how business is dealing with its

customer's needs and expectations and learning and growth shows the patterns in business

developments.

Therefore, measuring of success and performance of the business through non-financial

means in more likely to exhibit future success or failure of the business.

(iii) Comment on performance of Patrick Financial service using non-financial data

The appendix 2 provided the financial position of the company in balance scorecard

format that is non-financial by nature. This comprise with internal business process, customer

knowledge and learning or growth of the company.

Internal business process

The error rate in job done in the current year is more than the previous year rate.

Company could achieve the error rate of 16% in current financial year as compare to the

previous financial year that was 10%. This ratio demonstrates the fact that the percentage of

mistake made by the staff in the current financial year is more than the [previous financial year

(Kumar and Gupta, 2021). The average job completion time in the previous financial year was

10 weeks which could further reduce to 7 weeks in the current financial year. This clearly

reflecting the fact that completion time of the job could go down in the current financial year as

compare to the earlier financial year. The difference can easily be seen.

present in the past. There are many circumstances that could take place in upcoming year which

lead to losses for the company such as higher costs and losing clients. This may affect the

profitability of the business and accordingly, there would be poor performance in the future as

against good performance in past many years.

On the other hand, non-financial performance indicators are often regarded as measures

of future performance. For instance, if there is a greater quality of company's product, then in the

years to come there are higher probability of getting more clients, retaining the existing client

base along with raising price of product or service which provides additional revenue and profit

margins to the company respectively (Maletič, Gomišček and Maletič, 2021). Non-financial

measures of company's performance are indicated within balanced scorecard which have various

particulars within which different non-financial measures of performance are mentioned to

indicate non-financial performance of the business. For example, internal business processes

show internal efficiency of business, customer knowledge shows how business is dealing with its

customer's needs and expectations and learning and growth shows the patterns in business

developments.

Therefore, measuring of success and performance of the business through non-financial

means in more likely to exhibit future success or failure of the business.

(iii) Comment on performance of Patrick Financial service using non-financial data

The appendix 2 provided the financial position of the company in balance scorecard

format that is non-financial by nature. This comprise with internal business process, customer

knowledge and learning or growth of the company.

Internal business process

The error rate in job done in the current year is more than the previous year rate.

Company could achieve the error rate of 16% in current financial year as compare to the

previous financial year that was 10%. This ratio demonstrates the fact that the percentage of

mistake made by the staff in the current financial year is more than the [previous financial year

(Kumar and Gupta, 2021). The average job completion time in the previous financial year was

10 weeks which could further reduce to 7 weeks in the current financial year. This clearly

reflecting the fact that completion time of the job could go down in the current financial year as

compare to the earlier financial year. The difference can easily be seen.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Customer knowledge

The customer knowledge data of the company indicate the total number of customers and

market share in the current financial year. This ratio clearly shows the fact that total customer

own by the business in the current time is less than the previous financial year. On the contrary

note average fees or amount of revenue from the customer has increased in the current financial

year (Chulpanovna, Botiraliyevna and Turgunovich, 2021). This clearly reflecting to the fact

that even if the company is able to collect better revenue still the customer retention is less in the

Patrick Company. The current year leads could also decrease with 14%. The fees have increased

to 77 in the existing financial year.

Learning and growth

The total revenue of the organisation from the non-core work has been decreased in the

current financial year in compare to the earlier financial year. Employee retention of organisation

is bad. On the contrary note the revenue of the industry from the non-core work has increased.

B

Professional ethics refer to the individual behaviour of the accountant in context to

industry standard. These are the personal as well corporate standards of the behaviour associated

with the individual Professionally the standards do feel that professional should come up with all

norms and industry standard that can guide the person to approach the professional role and

responsibility in the most effective manner. In accounting business professional ethics should be

prioritised as standards of accounting professional must maintain in order to approach the

working objectives as an accountant. Professional ethics can disclose in the following points.

Integrity

Integrity is among the major professional this that need to followed by the accountant.

This ethics believe that and accountant need to be honest and straightforward in context to its

individual professional responsibilities. This ethics allows the accountant to fulfil all its role and

responsibilities in the most effective manner.

Objectivity

Accountant should not allow elements like conflict of interest, biasness and undue

influence while performing the role and responsibility as an accountant (Nguyen and et.al.,

2021). This ethic allows the professional to provide the best and most authentic services that can

support the professional role and responsibility of an accountant.

The customer knowledge data of the company indicate the total number of customers and

market share in the current financial year. This ratio clearly shows the fact that total customer

own by the business in the current time is less than the previous financial year. On the contrary

note average fees or amount of revenue from the customer has increased in the current financial

year (Chulpanovna, Botiraliyevna and Turgunovich, 2021). This clearly reflecting to the fact

that even if the company is able to collect better revenue still the customer retention is less in the

Patrick Company. The current year leads could also decrease with 14%. The fees have increased

to 77 in the existing financial year.

Learning and growth

The total revenue of the organisation from the non-core work has been decreased in the

current financial year in compare to the earlier financial year. Employee retention of organisation

is bad. On the contrary note the revenue of the industry from the non-core work has increased.

B

Professional ethics refer to the individual behaviour of the accountant in context to

industry standard. These are the personal as well corporate standards of the behaviour associated

with the individual Professionally the standards do feel that professional should come up with all

norms and industry standard that can guide the person to approach the professional role and

responsibility in the most effective manner. In accounting business professional ethics should be

prioritised as standards of accounting professional must maintain in order to approach the

working objectives as an accountant. Professional ethics can disclose in the following points.

Integrity

Integrity is among the major professional this that need to followed by the accountant.

This ethics believe that and accountant need to be honest and straightforward in context to its

individual professional responsibilities. This ethics allows the accountant to fulfil all its role and

responsibilities in the most effective manner.

Objectivity

Accountant should not allow elements like conflict of interest, biasness and undue

influence while performing the role and responsibility as an accountant (Nguyen and et.al.,

2021). This ethic allows the professional to provide the best and most authentic services that can

support the professional role and responsibility of an accountant.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Professional competence & due care

This is necessary that accountant must be aware with current developments, techniques

and legislation that can offer the accountant role mitigate role and responsibility. All the

applicable rules and regulations that legislatively apply on the job role of accountant must be

known by the professional.

Confidentiality

Accountant get to know the complete financial details of the organisation. This is the

professional ethics of the professional not to share any confidential information of business with

any other individual (Prayoga and Afrizal, 2021). Also the accountant must not use this

information for individual interest.

Professional behaviour

The accountant must act professionally while performing the individual role and

responsibility as an accountant.

CONCLUSION

Patrick Company has the potential to perform better in the market. Commercial

performance of organisation can monitor with support of internal business process, customer

knowledge and learning & growth. Professional ethics of an accountant involve various

principles that comprise with integrity, objectivity, professional competence & due care,

confidentiality and professional behaviour. All these are the core ethical principles and values

related to the accountant.

This is necessary that accountant must be aware with current developments, techniques

and legislation that can offer the accountant role mitigate role and responsibility. All the

applicable rules and regulations that legislatively apply on the job role of accountant must be

known by the professional.

Confidentiality

Accountant get to know the complete financial details of the organisation. This is the

professional ethics of the professional not to share any confidential information of business with

any other individual (Prayoga and Afrizal, 2021). Also the accountant must not use this

information for individual interest.

Professional behaviour

The accountant must act professionally while performing the individual role and

responsibility as an accountant.

CONCLUSION

Patrick Company has the potential to perform better in the market. Commercial

performance of organisation can monitor with support of internal business process, customer

knowledge and learning & growth. Professional ethics of an accountant involve various

principles that comprise with integrity, objectivity, professional competence & due care,

confidentiality and professional behaviour. All these are the core ethical principles and values

related to the accountant.

REFERENCES

Books and Journal

Al-Dmour, A., Abbod, M. and Al-Balqa, N., 2018. The impact of the quality of financial

reporting on non-financial business performance and the role of organizations

demographic'attributes (type, size and experience).

Al-Hashimi, A. M. and Mahdi, H. T. B., 2019. The Impact of Creative Accounting on the

Qualitative Characteristics of Accounting Information according to the Joint Project–

Exploratory Study. Journal of University of Babylon for Pure and Applied

Sciences, 27(5), pp.222-245.

Chiyad, A. F. and Mahmoud, M. T., 2019. The impact of the qualitative characteristics of

accounting information in improving the quality of financial reports, Study in a sample

of private banks operating in the Iraqi market. Economic Sciences, 14(55).

Chulpanovna, K. Z., Botiraliyevna, Y. M. and Turgunovich, M. A., 2021. SOCIETY

INTERESTS, PROFESSIONAL COMPETENCE AND ETHICAL

REQUIREMENTS FOR PROFESSIONAL ACCOUNTANTS. World

Economics and Finance Bulletin. 4. pp.3-5.

Dalwai, T. and Salehi, M., 2021. Business strategy, intellectual capital, firm performance,

and bankruptcy risk: evidence from Oman's non-financial sector

companies. Asian Review of Accounting.

Dao, B., 2021. Impact of corporate governance on firm performance and earnings

management a study on vietnamese non-financial companies. Asian Economic

and Financial Review. 10(5). pp.480-501.

Ebaid, I. E. S., 2021. Does IFRS implementation improve qualitative characteristics of

accounting information: evidence from Saudi commercial banks. Journal of Advanced

Research in Economics and Administrative Sciences, 2(1), pp.17-27.

Kadirbayevich, P. A., 2021. PREPARATION OF CONSOLIDATED FINANCIAL

STATEMENTS OF HOLDING COMPANIES IN ACCORDANCE WITH

INTERNATIONAL FINANCIAL REPORTING STANDARDS. Web of

Scientist: International Scientific Research Journal. 2(05). pp.492-496.

Books and Journal

Al-Dmour, A., Abbod, M. and Al-Balqa, N., 2018. The impact of the quality of financial

reporting on non-financial business performance and the role of organizations

demographic'attributes (type, size and experience).

Al-Hashimi, A. M. and Mahdi, H. T. B., 2019. The Impact of Creative Accounting on the

Qualitative Characteristics of Accounting Information according to the Joint Project–

Exploratory Study. Journal of University of Babylon for Pure and Applied

Sciences, 27(5), pp.222-245.

Chiyad, A. F. and Mahmoud, M. T., 2019. The impact of the qualitative characteristics of

accounting information in improving the quality of financial reports, Study in a sample

of private banks operating in the Iraqi market. Economic Sciences, 14(55).

Chulpanovna, K. Z., Botiraliyevna, Y. M. and Turgunovich, M. A., 2021. SOCIETY

INTERESTS, PROFESSIONAL COMPETENCE AND ETHICAL

REQUIREMENTS FOR PROFESSIONAL ACCOUNTANTS. World

Economics and Finance Bulletin. 4. pp.3-5.

Dalwai, T. and Salehi, M., 2021. Business strategy, intellectual capital, firm performance,

and bankruptcy risk: evidence from Oman's non-financial sector

companies. Asian Review of Accounting.

Dao, B., 2021. Impact of corporate governance on firm performance and earnings

management a study on vietnamese non-financial companies. Asian Economic

and Financial Review. 10(5). pp.480-501.

Ebaid, I. E. S., 2021. Does IFRS implementation improve qualitative characteristics of

accounting information: evidence from Saudi commercial banks. Journal of Advanced

Research in Economics and Administrative Sciences, 2(1), pp.17-27.

Kadirbayevich, P. A., 2021. PREPARATION OF CONSOLIDATED FINANCIAL

STATEMENTS OF HOLDING COMPANIES IN ACCORDANCE WITH

INTERNATIONAL FINANCIAL REPORTING STANDARDS. Web of

Scientist: International Scientific Research Journal. 2(05). pp.492-496.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.