AC4052QA - Financial Analysis: ASOS PLC Performance Evaluation

VerifiedAdded on 2023/06/08

|9

|2652

|283

AI Summary

This coursework provides a comprehensive financial analysis of ASOS PLC for the fiscal years 2020 and 2021. Section A involves calculating and interpreting key financial ratios including profitability, working capital, liquidity, and long-term financing, offering comparative comments on the company's performance. Section B requires preparing financial statements for Giorgio F PLC, including the statement of profit or loss, statement of changes in equity, and statement of financial position. Additionally, it includes a cash budget and profit budget for Grazyna Ltd, a new sports shoe business, for the first six months of 2021. The analysis utilizes provided financial data and assesses the financial health and performance of the companies.

`

AC4052QA Financial Accounting – APR22INTAKE

Assessment Component: Coursework

Weighting: This Coursework contributes 100% to the Overall Module Mark

Word count (1500 words Max): Section A 1200 words(max) and Section B 300 words(max)

Submission: Students to submit to Turnitin via module Weblearn

Deadline: Monday 25 July 2022

INSTRUCTIONS:

This coursework has two sections. Section A has ONE question and Section B has TWO questions.

1. Answer all question

2. Show all working out.

3. It is mandatory to use the template provided

4. You must show all working out. You may use Excel, but you must show the formula for the excel calculations

1

AC4052QA Financial Accounting – APR22INTAKE

Assessment Component: Coursework

Weighting: This Coursework contributes 100% to the Overall Module Mark

Word count (1500 words Max): Section A 1200 words(max) and Section B 300 words(max)

Submission: Students to submit to Turnitin via module Weblearn

Deadline: Monday 25 July 2022

INSTRUCTIONS:

This coursework has two sections. Section A has ONE question and Section B has TWO questions.

1. Answer all question

2. Show all working out.

3. It is mandatory to use the template provided

4. You must show all working out. You may use Excel, but you must show the formula for the excel calculations

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

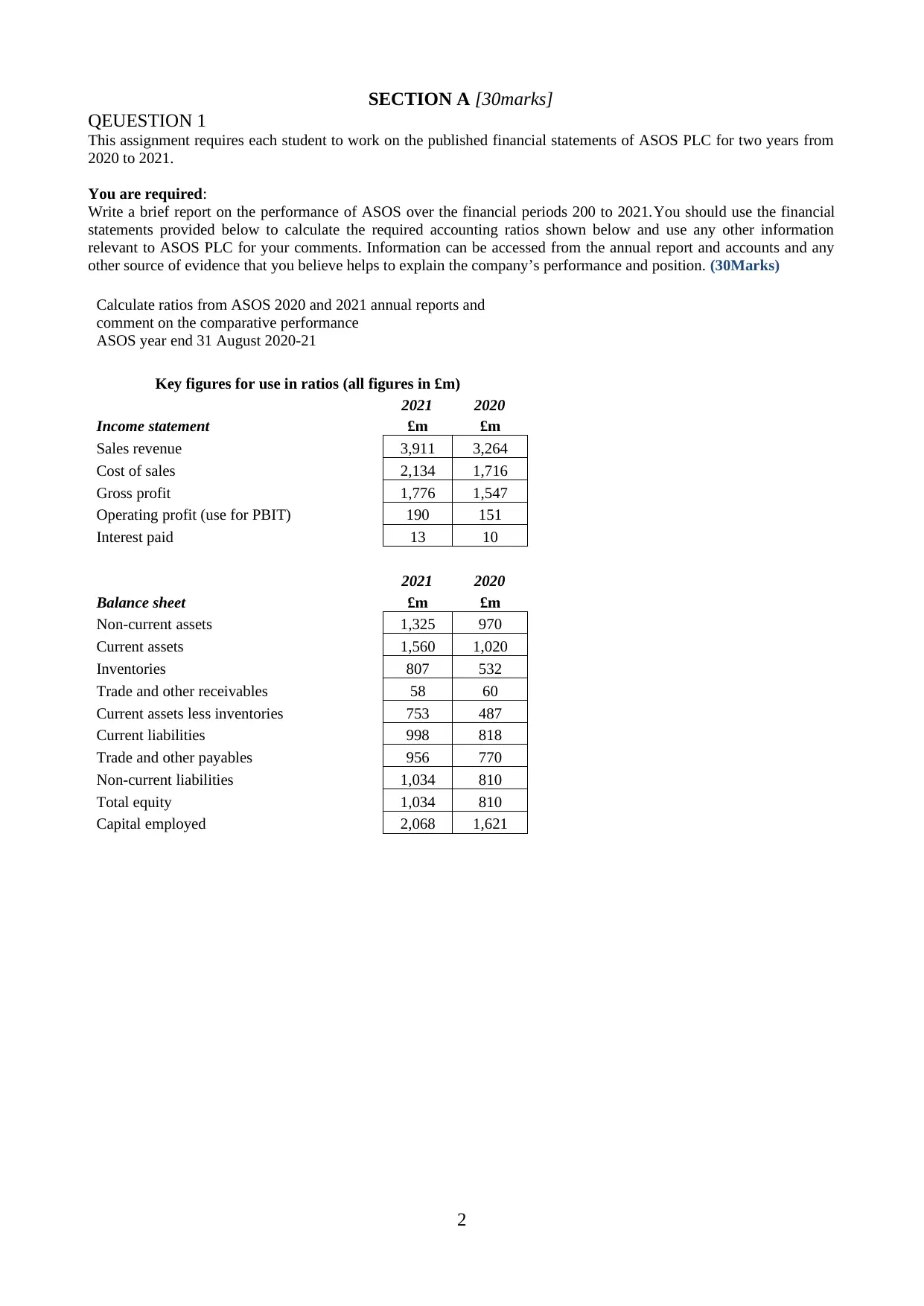

SECTION A [30marks]

QEUESTION 1

This assignment requires each student to work on the published financial statements of ASOS PLC for two years from

2020 to 2021.

You are required:

Write a brief report on the performance of ASOS over the financial periods 200 to 2021.You should use the financial

statements provided below to calculate the required accounting ratios shown below and use any other information

relevant to ASOS PLC for your comments. Information can be accessed from the annual report and accounts and any

other source of evidence that you believe helps to explain the company’s performance and position. (30Marks)

Calculate ratios from ASOS 2020 and 2021 annual reports and

comment on the comparative performance

ASOS year end 31 August 2020-21

Key figures for use in ratios (all figures in £m)

2021 2020

Income statement £m £m

Sales revenue 3,911 3,264

Cost of sales 2,134 1,716

Gross profit 1,776 1,547

Operating profit (use for PBIT) 190 151

Interest paid 13 10

2021 2020

Balance sheet £m £m

Non-current assets 1,325 970

Current assets 1,560 1,020

Inventories 807 532

Trade and other receivables 58 60

Current assets less inventories 753 487

Current liabilities 998 818

Trade and other payables 956 770

Non-current liabilities 1,034 810

Total equity 1,034 810

Capital employed 2,068 1,621

2

QEUESTION 1

This assignment requires each student to work on the published financial statements of ASOS PLC for two years from

2020 to 2021.

You are required:

Write a brief report on the performance of ASOS over the financial periods 200 to 2021.You should use the financial

statements provided below to calculate the required accounting ratios shown below and use any other information

relevant to ASOS PLC for your comments. Information can be accessed from the annual report and accounts and any

other source of evidence that you believe helps to explain the company’s performance and position. (30Marks)

Calculate ratios from ASOS 2020 and 2021 annual reports and

comment on the comparative performance

ASOS year end 31 August 2020-21

Key figures for use in ratios (all figures in £m)

2021 2020

Income statement £m £m

Sales revenue 3,911 3,264

Cost of sales 2,134 1,716

Gross profit 1,776 1,547

Operating profit (use for PBIT) 190 151

Interest paid 13 10

2021 2020

Balance sheet £m £m

Non-current assets 1,325 970

Current assets 1,560 1,020

Inventories 807 532

Trade and other receivables 58 60

Current assets less inventories 753 487

Current liabilities 998 818

Trade and other payables 956 770

Non-current liabilities 1,034 810

Total equity 1,034 810

Capital employed 2,068 1,621

2

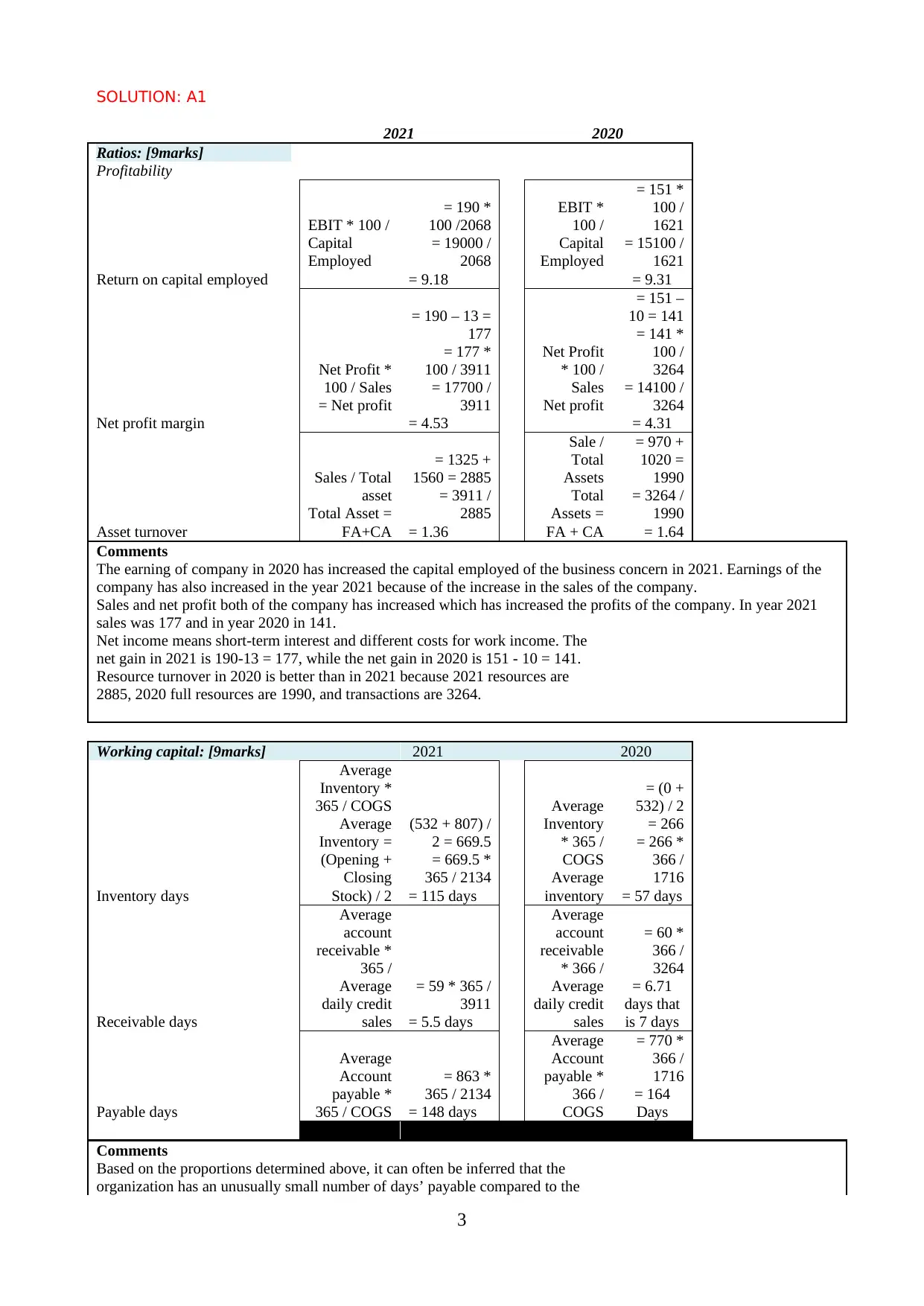

SOLUTION: A1

2021 2020

Ratios: [9marks]

Profitability

Return on capital employed

EBIT * 100 /

Capital

Employed

= 190 *

100 /2068

= 19000 /

2068

= 9.18

EBIT *

100 /

Capital

Employed

= 151 *

100 /

1621

= 15100 /

1621

= 9.31

Net profit margin

Net Profit *

100 / Sales

= Net profit

= 190 – 13 =

177

= 177 *

100 / 3911

= 17700 /

3911

= 4.53

Net Profit

* 100 /

Sales

Net profit

= 151 –

10 = 141

= 141 *

100 /

3264

= 14100 /

3264

= 4.31

Asset turnover

Sales / Total

asset

Total Asset =

FA+CA

= 1325 +

1560 = 2885

= 3911 /

2885

= 1.36

Sale /

Total

Assets

Total

Assets =

FA + CA

= 970 +

1020 =

1990

= 3264 /

1990

= 1.64

Comments

The earning of company in 2020 has increased the capital employed of the business concern in 2021. Earnings of the

company has also increased in the year 2021 because of the increase in the sales of the company.

Sales and net profit both of the company has increased which has increased the profits of the company. In year 2021

sales was 177 and in year 2020 in 141.

Net income means short-term interest and different costs for work income. The

net gain in 2021 is 190-13 = 177, while the net gain in 2020 is 151 - 10 = 141.

Resource turnover in 2020 is better than in 2021 because 2021 resources are

2885, 2020 full resources are 1990, and transactions are 3264.

Working capital: [9marks] 2021 2020

Inventory days

Average

Inventory *

365 / COGS

Average

Inventory =

(Opening +

Closing

Stock) / 2

(532 + 807) /

2 = 669.5

= 669.5 *

365 / 2134

= 115 days

Average

Inventory

* 365 /

COGS

Average

inventory

= (0 +

532) / 2

= 266

= 266 *

366 /

1716

= 57 days

Receivable days

Average

account

receivable *

365 /

Average

daily credit

sales

= 59 * 365 /

3911

= 5.5 days

Average

account

receivable

* 366 /

Average

daily credit

sales

= 60 *

366 /

3264

= 6.71

days that

is 7 days

Payable days

Average

Account

payable *

365 / COGS

= 863 *

365 / 2134

= 148 days

Average

Account

payable *

366 /

COGS

= 770 *

366 /

1716

= 164

Days

Comments

Based on the proportions determined above, it can often be inferred that the

organization has an unusually small number of days’ payable compared to the

3

2021 2020

Ratios: [9marks]

Profitability

Return on capital employed

EBIT * 100 /

Capital

Employed

= 190 *

100 /2068

= 19000 /

2068

= 9.18

EBIT *

100 /

Capital

Employed

= 151 *

100 /

1621

= 15100 /

1621

= 9.31

Net profit margin

Net Profit *

100 / Sales

= Net profit

= 190 – 13 =

177

= 177 *

100 / 3911

= 17700 /

3911

= 4.53

Net Profit

* 100 /

Sales

Net profit

= 151 –

10 = 141

= 141 *

100 /

3264

= 14100 /

3264

= 4.31

Asset turnover

Sales / Total

asset

Total Asset =

FA+CA

= 1325 +

1560 = 2885

= 3911 /

2885

= 1.36

Sale /

Total

Assets

Total

Assets =

FA + CA

= 970 +

1020 =

1990

= 3264 /

1990

= 1.64

Comments

The earning of company in 2020 has increased the capital employed of the business concern in 2021. Earnings of the

company has also increased in the year 2021 because of the increase in the sales of the company.

Sales and net profit both of the company has increased which has increased the profits of the company. In year 2021

sales was 177 and in year 2020 in 141.

Net income means short-term interest and different costs for work income. The

net gain in 2021 is 190-13 = 177, while the net gain in 2020 is 151 - 10 = 141.

Resource turnover in 2020 is better than in 2021 because 2021 resources are

2885, 2020 full resources are 1990, and transactions are 3264.

Working capital: [9marks] 2021 2020

Inventory days

Average

Inventory *

365 / COGS

Average

Inventory =

(Opening +

Closing

Stock) / 2

(532 + 807) /

2 = 669.5

= 669.5 *

365 / 2134

= 115 days

Average

Inventory

* 365 /

COGS

Average

inventory

= (0 +

532) / 2

= 266

= 266 *

366 /

1716

= 57 days

Receivable days

Average

account

receivable *

365 /

Average

daily credit

sales

= 59 * 365 /

3911

= 5.5 days

Average

account

receivable

* 366 /

Average

daily credit

sales

= 60 *

366 /

3264

= 6.71

days that

is 7 days

Payable days

Average

Account

payable *

365 / COGS

= 863 *

365 / 2134

= 148 days

Average

Account

payable *

366 /

COGS

= 770 *

366 /

1716

= 164

Days

Comments

Based on the proportions determined above, it can often be inferred that the

organization has an unusually small number of days’ payable compared to the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization, suggesting that the organization has the option to receive

instalments from its tenants within a very short period of time. Then again, the

organization needs to make this payment to its bank over an extremely long

period of time. The organization needs to pay in instalments over approximately

5 months.

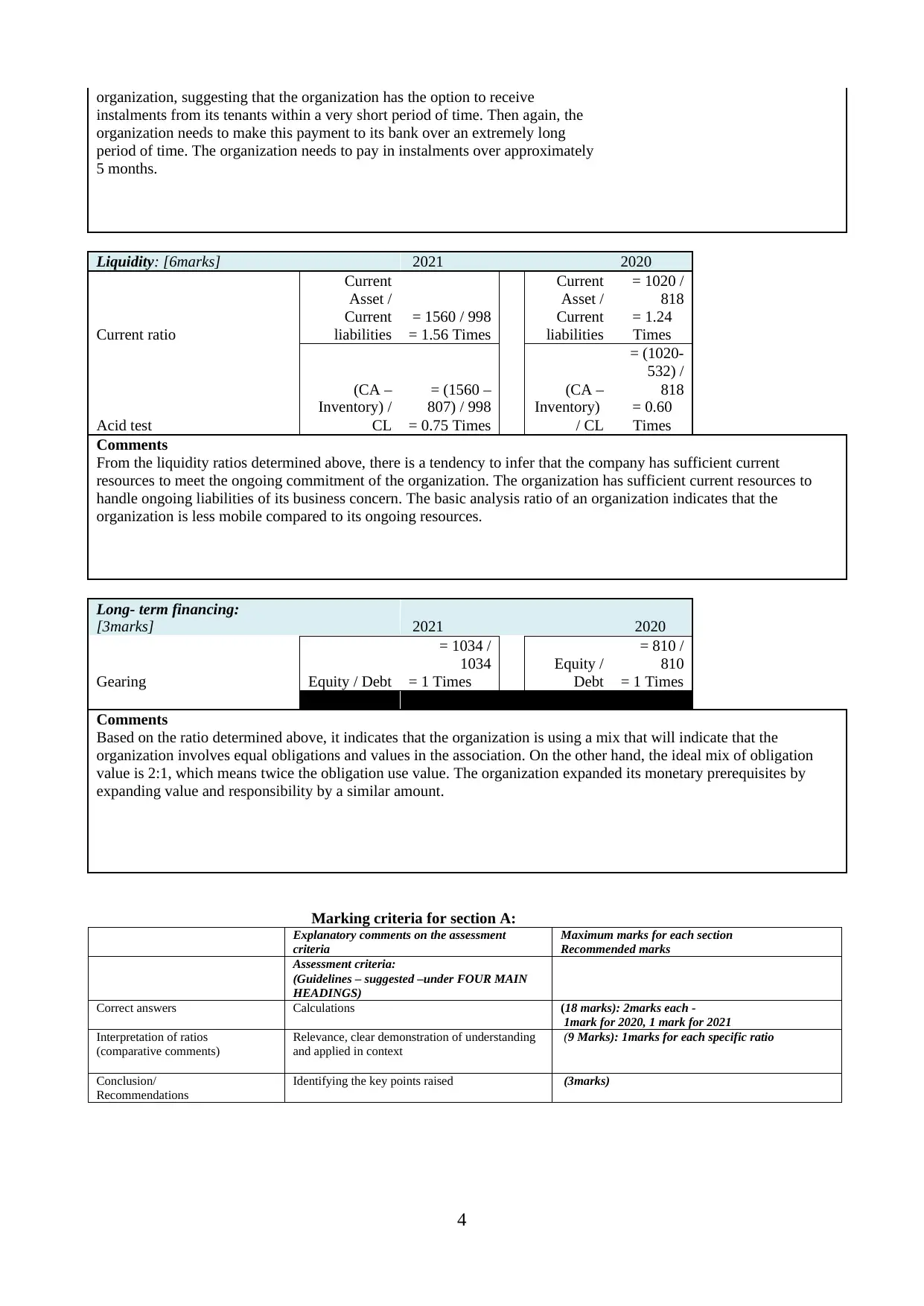

Liquidity: [6marks] 2021 2020

Current ratio

Current

Asset /

Current

liabilities

= 1560 / 998

= 1.56 Times

Current

Asset /

Current

liabilities

= 1020 /

818

= 1.24

Times

Acid test

(CA –

Inventory) /

CL

= (1560 –

807) / 998

= 0.75 Times

(CA –

Inventory)

/ CL

= (1020-

532) /

818

= 0.60

Times

Comments

From the liquidity ratios determined above, there is a tendency to infer that the company has sufficient current

resources to meet the ongoing commitment of the organization. The organization has sufficient current resources to

handle ongoing liabilities of its business concern. The basic analysis ratio of an organization indicates that the

organization is less mobile compared to its ongoing resources.

Long- term financing:

[3marks] 2021 2020

Gearing Equity / Debt

= 1034 /

1034

= 1 Times

Equity /

Debt

= 810 /

810

= 1 Times

Comments

Based on the ratio determined above, it indicates that the organization is using a mix that will indicate that the

organization involves equal obligations and values in the association. On the other hand, the ideal mix of obligation

value is 2:1, which means twice the obligation use value. The organization expanded its monetary prerequisites by

expanding value and responsibility by a similar amount.

Marking criteria for section A:

Explanatory comments on the assessment

criteria

Maximum marks for each section

Recommended marks

Assessment criteria:

(Guidelines – suggested –under FOUR MAIN

HEADINGS)

Correct answers Calculations (18 marks): 2marks each -

1mark for 2020, 1 mark for 2021

Interpretation of ratios

(comparative comments)

Relevance, clear demonstration of understanding

and applied in context

(9 Marks): 1marks for each specific ratio

Conclusion/

Recommendations

Identifying the key points raised (3marks)

4

instalments from its tenants within a very short period of time. Then again, the

organization needs to make this payment to its bank over an extremely long

period of time. The organization needs to pay in instalments over approximately

5 months.

Liquidity: [6marks] 2021 2020

Current ratio

Current

Asset /

Current

liabilities

= 1560 / 998

= 1.56 Times

Current

Asset /

Current

liabilities

= 1020 /

818

= 1.24

Times

Acid test

(CA –

Inventory) /

CL

= (1560 –

807) / 998

= 0.75 Times

(CA –

Inventory)

/ CL

= (1020-

532) /

818

= 0.60

Times

Comments

From the liquidity ratios determined above, there is a tendency to infer that the company has sufficient current

resources to meet the ongoing commitment of the organization. The organization has sufficient current resources to

handle ongoing liabilities of its business concern. The basic analysis ratio of an organization indicates that the

organization is less mobile compared to its ongoing resources.

Long- term financing:

[3marks] 2021 2020

Gearing Equity / Debt

= 1034 /

1034

= 1 Times

Equity /

Debt

= 810 /

810

= 1 Times

Comments

Based on the ratio determined above, it indicates that the organization is using a mix that will indicate that the

organization involves equal obligations and values in the association. On the other hand, the ideal mix of obligation

value is 2:1, which means twice the obligation use value. The organization expanded its monetary prerequisites by

expanding value and responsibility by a similar amount.

Marking criteria for section A:

Explanatory comments on the assessment

criteria

Maximum marks for each section

Recommended marks

Assessment criteria:

(Guidelines – suggested –under FOUR MAIN

HEADINGS)

Correct answers Calculations (18 marks): 2marks each -

1mark for 2020, 1 mark for 2021

Interpretation of ratios

(comparative comments)

Relevance, clear demonstration of understanding

and applied in context

(9 Marks): 1marks for each specific ratio

Conclusion/

Recommendations

Identifying the key points raised (3marks)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SECTION B [70marks]

Question B1 (58marks)

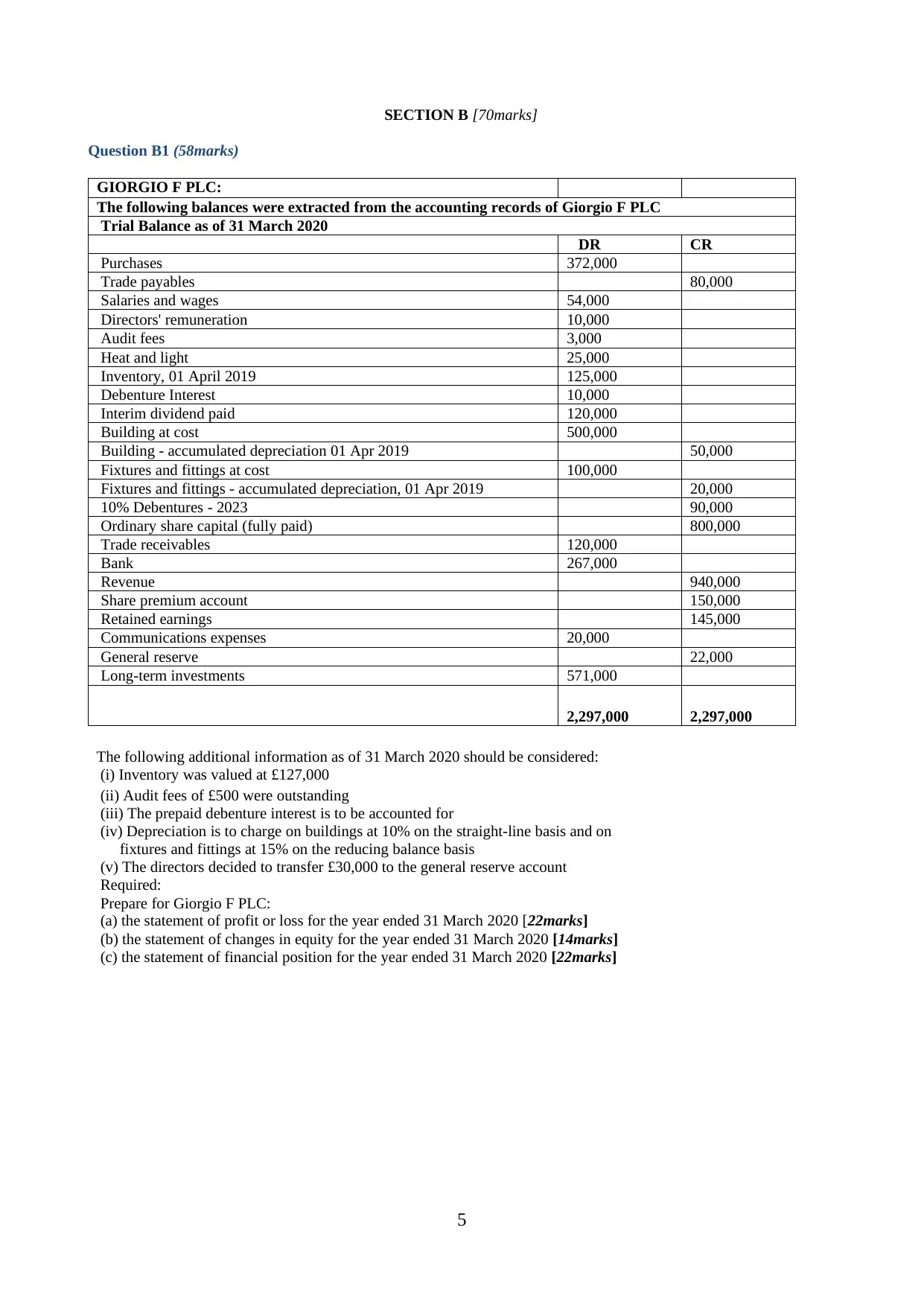

GIORGIO F PLC:

The following balances were extracted from the accounting records of Giorgio F PLC

Trial Balance as of 31 March 2020

DR CR

Purchases 372,000

Trade payables 80,000

Salaries and wages 54,000

Directors' remuneration 10,000

Audit fees 3,000

Heat and light 25,000

Inventory, 01 April 2019 125,000

Debenture Interest 10,000

Interim dividend paid 120,000

Building at cost 500,000

Building - accumulated depreciation 01 Apr 2019 50,000

Fixtures and fittings at cost 100,000

Fixtures and fittings - accumulated depreciation, 01 Apr 2019 20,000

10% Debentures - 2023 90,000

Ordinary share capital (fully paid) 800,000

Trade receivables 120,000

Bank 267,000

Revenue 940,000

Share premium account 150,000

Retained earnings 145,000

Communications expenses 20,000

General reserve 22,000

Long-term investments 571,000

2,297,000 2,297,000

The following additional information as of 31 March 2020 should be considered:

(i) Inventory was valued at £127,000

(ii) Audit fees of £500 were outstanding

(iii) The prepaid debenture interest is to be accounted for

(iv) Depreciation is to charge on buildings at 10% on the straight-line basis and on

fixtures and fittings at 15% on the reducing balance basis

(v) The directors decided to transfer £30,000 to the general reserve account

Required:

Prepare for Giorgio F PLC:

(a) the statement of profit or loss for the year ended 31 March 2020 [22marks]

(b) the statement of changes in equity for the year ended 31 March 2020 [14marks]

(c) the statement of financial position for the year ended 31 March 2020 [22marks]

5

Question B1 (58marks)

GIORGIO F PLC:

The following balances were extracted from the accounting records of Giorgio F PLC

Trial Balance as of 31 March 2020

DR CR

Purchases 372,000

Trade payables 80,000

Salaries and wages 54,000

Directors' remuneration 10,000

Audit fees 3,000

Heat and light 25,000

Inventory, 01 April 2019 125,000

Debenture Interest 10,000

Interim dividend paid 120,000

Building at cost 500,000

Building - accumulated depreciation 01 Apr 2019 50,000

Fixtures and fittings at cost 100,000

Fixtures and fittings - accumulated depreciation, 01 Apr 2019 20,000

10% Debentures - 2023 90,000

Ordinary share capital (fully paid) 800,000

Trade receivables 120,000

Bank 267,000

Revenue 940,000

Share premium account 150,000

Retained earnings 145,000

Communications expenses 20,000

General reserve 22,000

Long-term investments 571,000

2,297,000 2,297,000

The following additional information as of 31 March 2020 should be considered:

(i) Inventory was valued at £127,000

(ii) Audit fees of £500 were outstanding

(iii) The prepaid debenture interest is to be accounted for

(iv) Depreciation is to charge on buildings at 10% on the straight-line basis and on

fixtures and fittings at 15% on the reducing balance basis

(v) The directors decided to transfer £30,000 to the general reserve account

Required:

Prepare for Giorgio F PLC:

(a) the statement of profit or loss for the year ended 31 March 2020 [22marks]

(b) the statement of changes in equity for the year ended 31 March 2020 [14marks]

(c) the statement of financial position for the year ended 31 March 2020 [22marks]

5

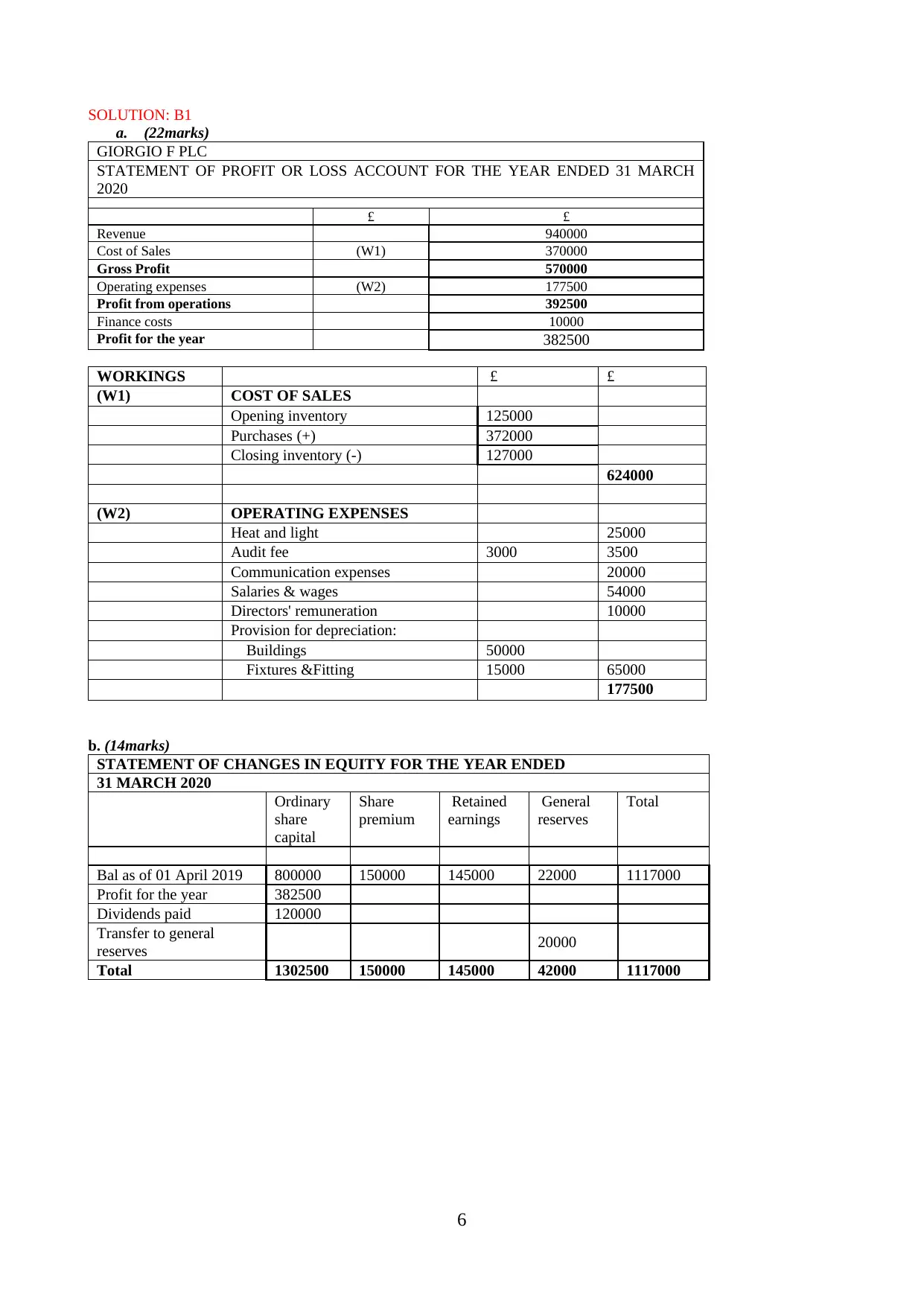

SOLUTION: B1

a. (22marks)

GIORGIO F PLC

STATEMENT OF PROFIT OR LOSS ACCOUNT FOR THE YEAR ENDED 31 MARCH

2020

£ £

Revenue 940000

Cost of Sales (W1) 370000

Gross Profit 570000

Operating expenses (W2) 177500

Profit from operations 392500

Finance costs 10000

Profit for the year 382500

WORKINGS £ £

(W1) COST OF SALES

Opening inventory 125000

Purchases (+) 372000

Closing inventory (-) 127000

624000

(W2) OPERATING EXPENSES

Heat and light 25000

Audit fee 3000 3500

Communication expenses 20000

Salaries & wages 54000

Directors' remuneration 10000

Provision for depreciation:

Buildings 50000

Fixtures &Fitting 15000 65000

177500

b. (14marks)

STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED

31 MARCH 2020

Ordinary

share

capital

Share

premium

Retained

earnings

General

reserves

Total

Bal as of 01 April 2019 800000 150000 145000 22000 1117000

Profit for the year 382500

Dividends paid 120000

Transfer to general

reserves 20000

Total 1302500 150000 145000 42000 1117000

6

a. (22marks)

GIORGIO F PLC

STATEMENT OF PROFIT OR LOSS ACCOUNT FOR THE YEAR ENDED 31 MARCH

2020

£ £

Revenue 940000

Cost of Sales (W1) 370000

Gross Profit 570000

Operating expenses (W2) 177500

Profit from operations 392500

Finance costs 10000

Profit for the year 382500

WORKINGS £ £

(W1) COST OF SALES

Opening inventory 125000

Purchases (+) 372000

Closing inventory (-) 127000

624000

(W2) OPERATING EXPENSES

Heat and light 25000

Audit fee 3000 3500

Communication expenses 20000

Salaries & wages 54000

Directors' remuneration 10000

Provision for depreciation:

Buildings 50000

Fixtures &Fitting 15000 65000

177500

b. (14marks)

STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED

31 MARCH 2020

Ordinary

share

capital

Share

premium

Retained

earnings

General

reserves

Total

Bal as of 01 April 2019 800000 150000 145000 22000 1117000

Profit for the year 382500

Dividends paid 120000

Transfer to general

reserves 20000

Total 1302500 150000 145000 42000 1117000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

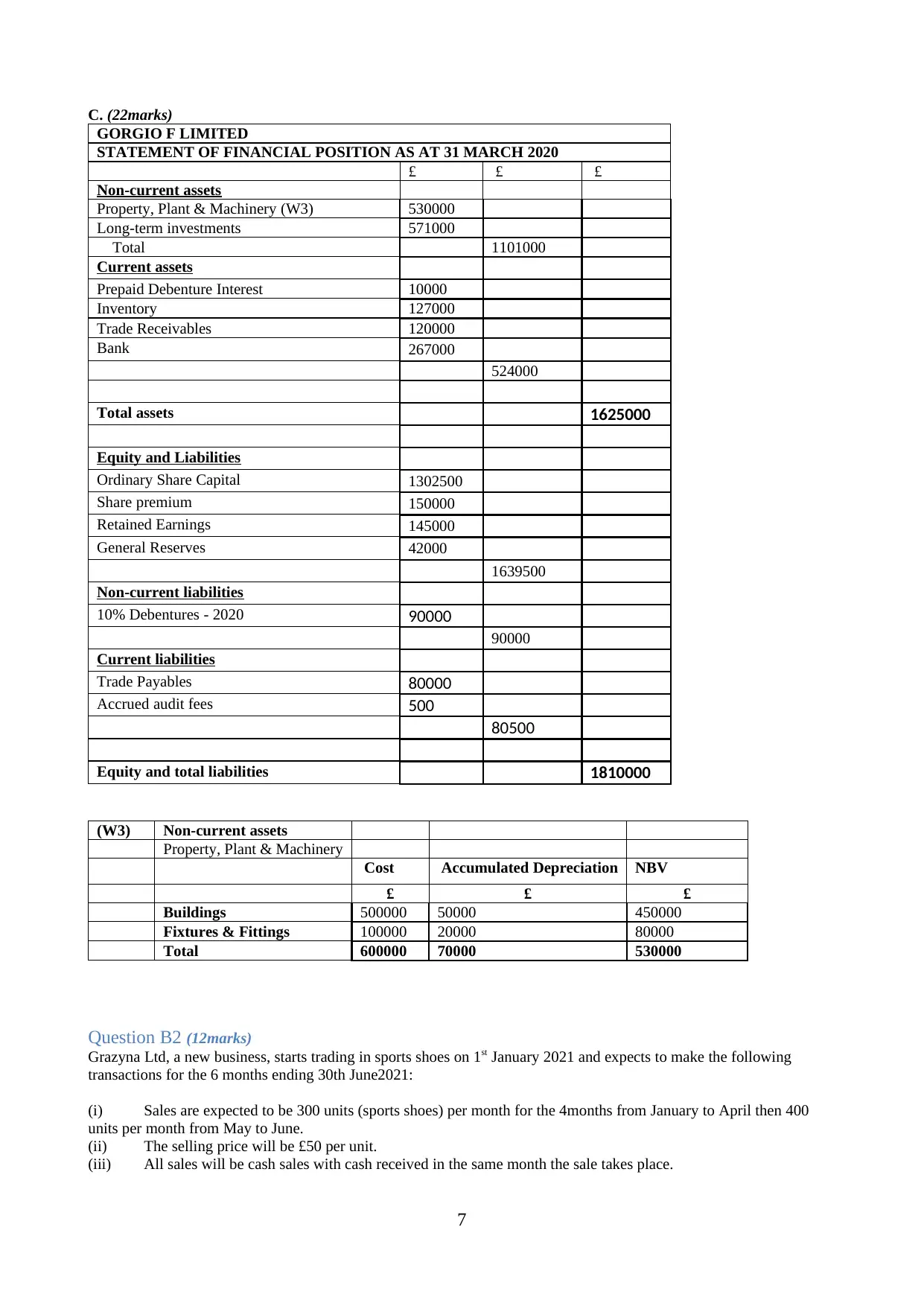

C. (22marks)

GORGIO F LIMITED

STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 2020

£ £ £

Non-current assets

Property, Plant & Machinery (W3) 530000

Long-term investments 571000

Total 1101000

Current assets

Prepaid Debenture Interest 10000

Inventory 127000

Trade Receivables 120000

Bank 267000

524000

Total assets 1625000

Equity and Liabilities

Ordinary Share Capital 1302500

Share premium 150000

Retained Earnings 145000

General Reserves 42000

1639500

Non-current liabilities

10% Debentures - 2020 90000

90000

Current liabilities

Trade Payables 80000

Accrued audit fees 500

80500

Equity and total liabilities 1810000

(W3) Non-current assets

Property, Plant & Machinery

Cost Accumulated Depreciation NBV

£ £ £

Buildings 500000 50000 450000

Fixtures & Fittings 100000 20000 80000

Total 600000 70000 530000

Question B2 (12marks)

Grazyna Ltd, a new business, starts trading in sports shoes on 1st January 2021 and expects to make the following

transactions for the 6 months ending 30th June2021:

(i) Sales are expected to be 300 units (sports shoes) per month for the 4months from January to April then 400

units per month from May to June.

(ii) The selling price will be £50 per unit.

(iii) All sales will be cash sales with cash received in the same month the sale takes place.

7

GORGIO F LIMITED

STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 2020

£ £ £

Non-current assets

Property, Plant & Machinery (W3) 530000

Long-term investments 571000

Total 1101000

Current assets

Prepaid Debenture Interest 10000

Inventory 127000

Trade Receivables 120000

Bank 267000

524000

Total assets 1625000

Equity and Liabilities

Ordinary Share Capital 1302500

Share premium 150000

Retained Earnings 145000

General Reserves 42000

1639500

Non-current liabilities

10% Debentures - 2020 90000

90000

Current liabilities

Trade Payables 80000

Accrued audit fees 500

80500

Equity and total liabilities 1810000

(W3) Non-current assets

Property, Plant & Machinery

Cost Accumulated Depreciation NBV

£ £ £

Buildings 500000 50000 450000

Fixtures & Fittings 100000 20000 80000

Total 600000 70000 530000

Question B2 (12marks)

Grazyna Ltd, a new business, starts trading in sports shoes on 1st January 2021 and expects to make the following

transactions for the 6 months ending 30th June2021:

(i) Sales are expected to be 300 units (sports shoes) per month for the 4months from January to April then 400

units per month from May to June.

(ii) The selling price will be £50 per unit.

(iii) All sales will be cash sales with cash received in the same month the sale takes place.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

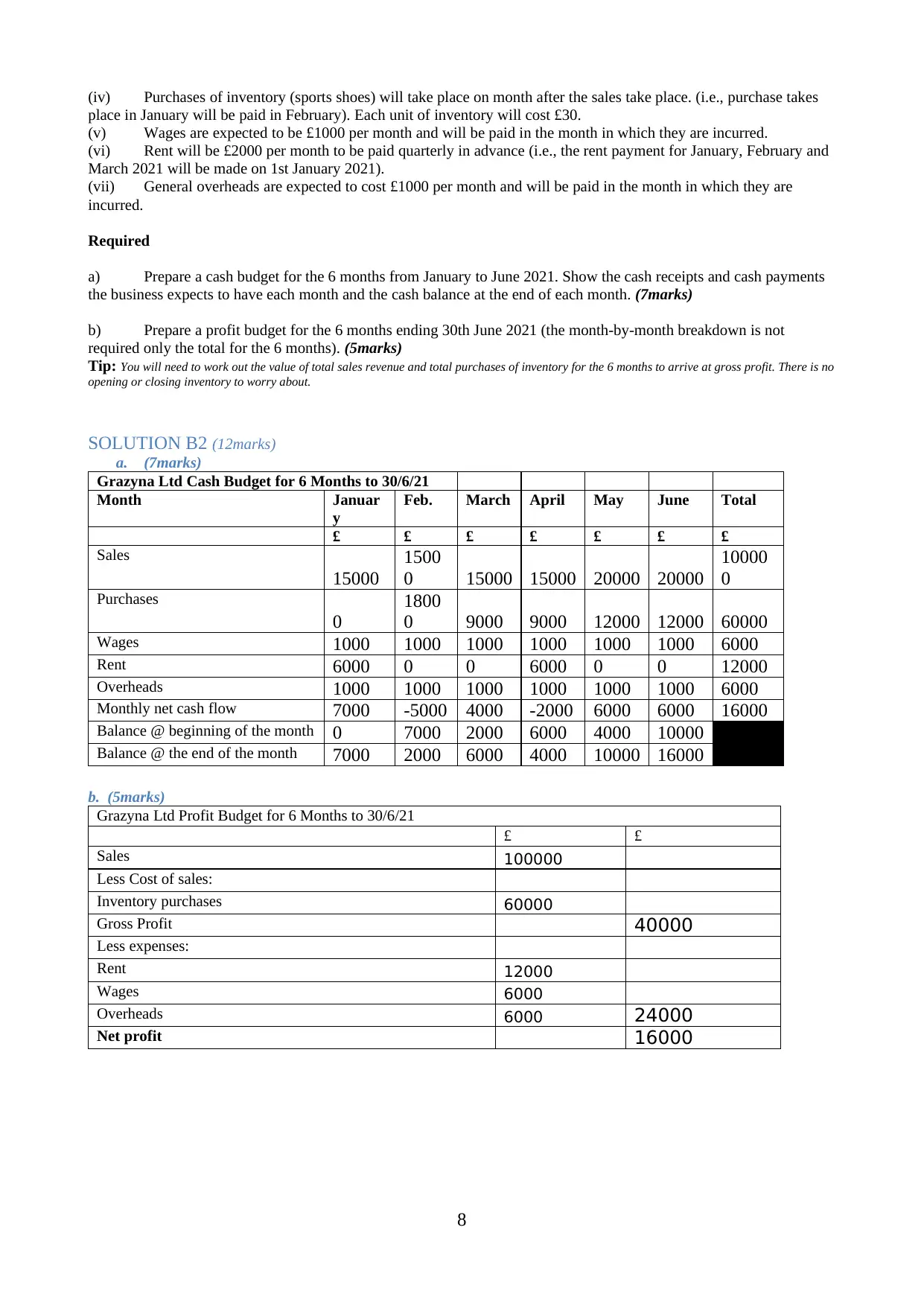

(iv) Purchases of inventory (sports shoes) will take place on month after the sales take place. (i.e., purchase takes

place in January will be paid in February). Each unit of inventory will cost £30.

(v) Wages are expected to be £1000 per month and will be paid in the month in which they are incurred.

(vi) Rent will be £2000 per month to be paid quarterly in advance (i.e., the rent payment for January, February and

March 2021 will be made on 1st January 2021).

(vii) General overheads are expected to cost £1000 per month and will be paid in the month in which they are

incurred.

Required

a) Prepare a cash budget for the 6 months from January to June 2021. Show the cash receipts and cash payments

the business expects to have each month and the cash balance at the end of each month. (7marks)

b) Prepare a profit budget for the 6 months ending 30th June 2021 (the month-by-month breakdown is not

required only the total for the 6 months). (5marks)

Tip: You will need to work out the value of total sales revenue and total purchases of inventory for the 6 months to arrive at gross profit. There is no

opening or closing inventory to worry about.

SOLUTION B2 (12marks)

a. (7marks)

Grazyna Ltd Cash Budget for 6 Months to 30/6/21

Month Januar

y

Feb. March April May June Total

£ £ £ £ £ £ £

Sales

15000

1500

0 15000 15000 20000 20000

10000

0

Purchases

0

1800

0 9000 9000 12000 12000 60000

Wages 1000 1000 1000 1000 1000 1000 6000

Rent 6000 0 0 6000 0 0 12000

Overheads 1000 1000 1000 1000 1000 1000 6000

Monthly net cash flow 7000 -5000 4000 -2000 6000 6000 16000

Balance @ beginning of the month 0 7000 2000 6000 4000 10000

Balance @ the end of the month 7000 2000 6000 4000 10000 16000

b. (5marks)

Grazyna Ltd Profit Budget for 6 Months to 30/6/21

£ £

Sales 100000

Less Cost of sales:

Inventory purchases 60000

Gross Profit 40000

Less expenses:

Rent 12000

Wages 6000

Overheads 6000 24000

Net profit 16000

8

place in January will be paid in February). Each unit of inventory will cost £30.

(v) Wages are expected to be £1000 per month and will be paid in the month in which they are incurred.

(vi) Rent will be £2000 per month to be paid quarterly in advance (i.e., the rent payment for January, February and

March 2021 will be made on 1st January 2021).

(vii) General overheads are expected to cost £1000 per month and will be paid in the month in which they are

incurred.

Required

a) Prepare a cash budget for the 6 months from January to June 2021. Show the cash receipts and cash payments

the business expects to have each month and the cash balance at the end of each month. (7marks)

b) Prepare a profit budget for the 6 months ending 30th June 2021 (the month-by-month breakdown is not

required only the total for the 6 months). (5marks)

Tip: You will need to work out the value of total sales revenue and total purchases of inventory for the 6 months to arrive at gross profit. There is no

opening or closing inventory to worry about.

SOLUTION B2 (12marks)

a. (7marks)

Grazyna Ltd Cash Budget for 6 Months to 30/6/21

Month Januar

y

Feb. March April May June Total

£ £ £ £ £ £ £

Sales

15000

1500

0 15000 15000 20000 20000

10000

0

Purchases

0

1800

0 9000 9000 12000 12000 60000

Wages 1000 1000 1000 1000 1000 1000 6000

Rent 6000 0 0 6000 0 0 12000

Overheads 1000 1000 1000 1000 1000 1000 6000

Monthly net cash flow 7000 -5000 4000 -2000 6000 6000 16000

Balance @ beginning of the month 0 7000 2000 6000 4000 10000

Balance @ the end of the month 7000 2000 6000 4000 10000 16000

b. (5marks)

Grazyna Ltd Profit Budget for 6 Months to 30/6/21

£ £

Sales 100000

Less Cost of sales:

Inventory purchases 60000

Gross Profit 40000

Less expenses:

Rent 12000

Wages 6000

Overheads 6000 24000

Net profit 16000

8

REFERENCES

Almaqtari, F.A. and et.al., 2020. An empirical evaluation of financial reporting quality of the Indian

GAAP and Indian accounting standards. International Journal of Accounting, Auditing

and Performance Evaluation, 16(2-3), pp.200-229.

Arnold, V., 2018. The changing technological environment and the future of behavioural research

in accounting. Accounting & Finance, 58(2), pp.315-339.

Astuti, G.L. and Khotijah, S.A., 2022. Analysis of the Application of PSAK 109 Regarding

Financial Reporting Accounting for Zakat, Infaq/Alms at BAZNAS Tegal Regency. Jurnal

Multidisiplin Madani (MUDIMA), 2(2), pp.737-746.

Conteh, L.J. and Oke, O., 2019. An Examination of the Pass Rates on the CPA Exam: A Suggested

Redesign of the Accounting Curriculum 2013-2017. Journal of Higher Education Theory

& Practice, 19(6).

Dordzhieva, A., Laux, V. and Zheng, R., 2022. Signaling private information via accounting system

design. Journal of Accounting and Economics, p.101494.

Heltzer, W. and Mindak, M., 2021. COVID-19 and the Accounting Profession. Journal of

Accounting, Ethics and Public Policy, 22(2), pp.151-205.

Linsmeier, T. and Wheeler, E., 2020. The debate over subsequent accounting for

goodwill. Available at SSRN 3725007.

Owens, J. and et.al., 2019. The sound of silence: What does a standard unqualified audit opinion

mean under the new going concern financial accounting standard. Available at

SSRN, 3374039.

Pavone, P. and Migliaccio, G., 2021. Profitability of the Italian farming companies and the impact

of financial crisis: a quantitative research using accounting data. International Journal of

Business Performance Management, 22(4), pp.394-425.

Tetteh, L.A. and et.al., 2021. Public sector financial management reforms in Ghana: insights from

institutional theory. Journal of Accounting in Emerging Economies, 11(5), pp.691-713.

9

Almaqtari, F.A. and et.al., 2020. An empirical evaluation of financial reporting quality of the Indian

GAAP and Indian accounting standards. International Journal of Accounting, Auditing

and Performance Evaluation, 16(2-3), pp.200-229.

Arnold, V., 2018. The changing technological environment and the future of behavioural research

in accounting. Accounting & Finance, 58(2), pp.315-339.

Astuti, G.L. and Khotijah, S.A., 2022. Analysis of the Application of PSAK 109 Regarding

Financial Reporting Accounting for Zakat, Infaq/Alms at BAZNAS Tegal Regency. Jurnal

Multidisiplin Madani (MUDIMA), 2(2), pp.737-746.

Conteh, L.J. and Oke, O., 2019. An Examination of the Pass Rates on the CPA Exam: A Suggested

Redesign of the Accounting Curriculum 2013-2017. Journal of Higher Education Theory

& Practice, 19(6).

Dordzhieva, A., Laux, V. and Zheng, R., 2022. Signaling private information via accounting system

design. Journal of Accounting and Economics, p.101494.

Heltzer, W. and Mindak, M., 2021. COVID-19 and the Accounting Profession. Journal of

Accounting, Ethics and Public Policy, 22(2), pp.151-205.

Linsmeier, T. and Wheeler, E., 2020. The debate over subsequent accounting for

goodwill. Available at SSRN 3725007.

Owens, J. and et.al., 2019. The sound of silence: What does a standard unqualified audit opinion

mean under the new going concern financial accounting standard. Available at

SSRN, 3374039.

Pavone, P. and Migliaccio, G., 2021. Profitability of the Italian farming companies and the impact

of financial crisis: a quantitative research using accounting data. International Journal of

Business Performance Management, 22(4), pp.394-425.

Tetteh, L.A. and et.al., 2021. Public sector financial management reforms in Ghana: insights from

institutional theory. Journal of Accounting in Emerging Economies, 11(5), pp.691-713.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.