Financial Accounting: Reconciliation, Control Accounts and Variances

VerifiedAdded on 2023/01/12

|21

|4301

|64

Report

AI Summary

This financial accounting report provides a detailed exploration of key concepts and methods. It begins with an introduction to financial accounting, emphasizing its role in preparing financial statements for internal and external stakeholders. The report then delves into double-entry bookkeeping, trial balances, and relevant accounting regulations. It differentiates between financial reports and financial statements and explains the accounts for sole traders, partnerships, and limited companies, highlighting their differences. The report also covers the reconciliation process, tools, and techniques used for checking general ledger accounts, as well as the importance of correctly entered figures and variances. Control accounts, suspense accounts, and their uses in financial accounting are explained, along with the processes for reconciling these accounts. Several case studies are included to illustrate the application of these concepts. The report concludes with an overview of financial accounting principles, including the preparation of final accounts, bank reconciliation statements, and control accounts.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

INFORMATION BOOKLET..........................................................................................................1

Double entry book–keeping and trial balance and regulations....................................................1

Difference between the financial reports and financial statements.............................................2

Explanation of the accounts for sole trader, partnership and limited company and their

differences....................................................................................................................................2

Explanation of the reconciliation process and tools & techniques used for checking general

ledger accounts. Explanation on variances and importance of the correctly entered figures......4

Explanation of the control accounts and their use in financial accounting.................................5

Description of process for reconciling control accounts and need to reconcile the accounts.....6

Explanation on purpose of suspense accounts and their difference from the control accounts...7

Case Study 1................................................................................................................................7

Case Study 2................................................................................................................................7

Case Study 3................................................................................................................................8

Case Study 4................................................................................................................................8

Case Study 5..............................................................................................................................11

ACCOUNTING.............................................................................................................................12

Final accounts of sole trader, partnership and company............................................................12

Bank Reconciliation Statement..................................................................................................15

Control Account.........................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

INFORMATION BOOKLET..........................................................................................................1

Double entry book–keeping and trial balance and regulations....................................................1

Difference between the financial reports and financial statements.............................................2

Explanation of the accounts for sole trader, partnership and limited company and their

differences....................................................................................................................................2

Explanation of the reconciliation process and tools & techniques used for checking general

ledger accounts. Explanation on variances and importance of the correctly entered figures......4

Explanation of the control accounts and their use in financial accounting.................................5

Description of process for reconciling control accounts and need to reconcile the accounts.....6

Explanation on purpose of suspense accounts and their difference from the control accounts...7

Case Study 1................................................................................................................................7

Case Study 2................................................................................................................................7

Case Study 3................................................................................................................................8

Case Study 4................................................................................................................................8

Case Study 5..............................................................................................................................11

ACCOUNTING.............................................................................................................................12

Final accounts of sole trader, partnership and company............................................................12

Bank Reconciliation Statement..................................................................................................15

Control Account.........................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUTION

Financial accounting refers to process of preparing the financial statements which represents

the financial position and performance of the company. These financial information is useful for

both the internal management and stakeholders of the company such as creditors, investors,

suppliers and customers. Financial accounting is different from managerial accounting that

prepares financial records for the internal management of the company. Financial statements

prepared by the company are income statement, balance sheet and cash flow statements. They

are prepared by the company as per the applicable accounting standards. Present report will be

revealing about the concepts and methods of financial accounting. It will provide explanation on

double entry book keeping, financial reports and the financial statements. It will also provide

about the sole traders, partnership and limited company form of doing business. Report will

address the reconciliation process and techniques used for checking the balances of general

ledger and the use of control accounts in financial accounting. The concepts will be explained

with the help of examples and case studies. Study will enhance the understanding of financial

accounting concepts and techniques.

INFORMATION BOOKLET

Double entry book–keeping and trial balance and regulations.

Book keeping or double entry system

means that every transaction of the business

affects minimum two accounts. It is to be

recorded in at least two accounts.. It was

established for giving equal effects to the

debit and credit side of the balances. Double

entry requires the accounting equation to be

in balance i.e. assets = owner’s equity +

liabilities. This requires the balance in assets

side should be equal to the balance in

liabilities and equity side.

Trial balance is statement prepared in

double entry system containing the debits

and credit balances of all the ledger

accounts. Trial balance is prepared after

closing the ledger accounts for balancing the

debits and credit side of all the accounts of

business. Trial balance is prepared by the

business for ensuring that entries recorded

for the financial transactions in the ledger

accounts and are balanced at the end. The

debit and credit side of the trial balance

should be equal. In a double entry system

trial balance is used for the preparation of

financial statements. Balance of the accounts

in trial balance is transferred to the

respective financial statements which are

income statement and balance sheet

1

Financial accounting refers to process of preparing the financial statements which represents

the financial position and performance of the company. These financial information is useful for

both the internal management and stakeholders of the company such as creditors, investors,

suppliers and customers. Financial accounting is different from managerial accounting that

prepares financial records for the internal management of the company. Financial statements

prepared by the company are income statement, balance sheet and cash flow statements. They

are prepared by the company as per the applicable accounting standards. Present report will be

revealing about the concepts and methods of financial accounting. It will provide explanation on

double entry book keeping, financial reports and the financial statements. It will also provide

about the sole traders, partnership and limited company form of doing business. Report will

address the reconciliation process and techniques used for checking the balances of general

ledger and the use of control accounts in financial accounting. The concepts will be explained

with the help of examples and case studies. Study will enhance the understanding of financial

accounting concepts and techniques.

INFORMATION BOOKLET

Double entry book–keeping and trial balance and regulations.

Book keeping or double entry system

means that every transaction of the business

affects minimum two accounts. It is to be

recorded in at least two accounts.. It was

established for giving equal effects to the

debit and credit side of the balances. Double

entry requires the accounting equation to be

in balance i.e. assets = owner’s equity +

liabilities. This requires the balance in assets

side should be equal to the balance in

liabilities and equity side.

Trial balance is statement prepared in

double entry system containing the debits

and credit balances of all the ledger

accounts. Trial balance is prepared after

closing the ledger accounts for balancing the

debits and credit side of all the accounts of

business. Trial balance is prepared by the

business for ensuring that entries recorded

for the financial transactions in the ledger

accounts and are balanced at the end. The

debit and credit side of the trial balance

should be equal. In a double entry system

trial balance is used for the preparation of

financial statements. Balance of the accounts

in trial balance is transferred to the

respective financial statements which are

income statement and balance sheet

1

You're viewing a preview

Unlock full access by subscribing today!

(Schroeder, Clark and Cathey, 2019).

Balance of income and expenses are

transferred in the profit or loss statement for

identifying the profitability and balances of

assets, liabilities and capital accounts are

transferred to the balance sheet for

representing the financial position of

company.

Transactions under double entry

system are governed by the accounting

standards issued by the accounting bodies.

Companies are required to comply with the

accounting standards and frameworks for

the preparation of financial statements.

Companies are required to comply with the

reporting frameworks for representing the

financial position and performance of firm

.

Difference between the financial reports and financial statements.

Financial reports and financial

statements are terms often used

interchangeably but there is difference

between the two. It could be said that

financial statements are the financial reports

where financial reports could not be said

financial statements.

Financial Reports

Financial report provides

information for the distribution to public. It

is the report on monitory matters. In other

words, financial report covers the

transaction having financial effects. For

running business financial reports provide

important information relevant for decision

making to outside and inside users (No,

2018). These bank statements, report of aged

debtors. Some of the financial reports are

made only for the internal management for

framing effective corporate strategies and

some are for external users.

Financial Statements

Financial statements on the other are

the part of financial reports. Financial

statements have more increased usage as

compared with the other financial reports.

Financial statements refer to complete set of

general purpose financial statements or

special purpose financial statements.

Financial statements include income

statement, balance sheet and cash flow

statement. Income statements provide the

performance of company during the year,

balance sheet reflects the position and the

cash flow statement provide the flow of

money inside and outside the entity. These

financial statements are governed by the

accounting boards that require the

2

Balance of income and expenses are

transferred in the profit or loss statement for

identifying the profitability and balances of

assets, liabilities and capital accounts are

transferred to the balance sheet for

representing the financial position of

company.

Transactions under double entry

system are governed by the accounting

standards issued by the accounting bodies.

Companies are required to comply with the

accounting standards and frameworks for

the preparation of financial statements.

Companies are required to comply with the

reporting frameworks for representing the

financial position and performance of firm

.

Difference between the financial reports and financial statements.

Financial reports and financial

statements are terms often used

interchangeably but there is difference

between the two. It could be said that

financial statements are the financial reports

where financial reports could not be said

financial statements.

Financial Reports

Financial report provides

information for the distribution to public. It

is the report on monitory matters. In other

words, financial report covers the

transaction having financial effects. For

running business financial reports provide

important information relevant for decision

making to outside and inside users (No,

2018). These bank statements, report of aged

debtors. Some of the financial reports are

made only for the internal management for

framing effective corporate strategies and

some are for external users.

Financial Statements

Financial statements on the other are

the part of financial reports. Financial

statements have more increased usage as

compared with the other financial reports.

Financial statements refer to complete set of

general purpose financial statements or

special purpose financial statements.

Financial statements include income

statement, balance sheet and cash flow

statement. Income statements provide the

performance of company during the year,

balance sheet reflects the position and the

cash flow statement provide the flow of

money inside and outside the entity. These

financial statements are governed by the

accounting boards that require the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statements to be presented in the prescribed

format.

Explanation of the accounts for sole trader, partnership and limited company and their

differences.

Sole Trader

Sole trader is a form of business

where the owner is self employed and runs

the business as individual. In sole trader

business owner is solely responsible for the

debts and obligations of the business. Sole

trader has an unlimited liability over the

business. Sole trader is not required to

prepare accounts as per the required

accounting standards. They are not required

to comply with the regulations for

preparation of financial records. There is no

prescribed format for the sole trade to

prepare its accounts. Accounts of sole trader

are prepared as per the requirement of

owners. Sole trader enjoy the whole profits

unlike the partnership and limited company.

Partnership

Partnership refers to form of

business in which 2 or more people come

together for carrying out the business.

Partners pool resources in partnership for

starting the business. Partnership is formed

on oral or written agreements on mutual

agreements of the partners. Profit and losses

are shared in the partnership firm in the ratio

agreed between them in agreements.

Partnership firms are required to prepare

accounts as per the partnership act (Robson,

Young and Power, 2017). They are not

required to prepare the financial statement as

per the accounting standards for reporting to

the public. Liability of the partners is

unlimited in the unlimited partnership and

limited in the limited partnership firm to the

extent of their contribution in the business.

In a partnership business tax is charged on

the individual income of partners and not

over the partnership firms.

Limited Company

Limited company is the organisation

set up for running a business. Unlike the

sole trader and partnership finance of the

business are separate from the personal

finances. A company is a separate legal

entity different from its owners. Company is

required to comply with all the regulations.

Companies are required to prepare financial

statements as per the accounting standards

given by the accounting bodies. For

preparation of financial statements all the

reporting framework and governing

principles are followed by the management.

Accounts of companies are audited for

3

format.

Explanation of the accounts for sole trader, partnership and limited company and their

differences.

Sole Trader

Sole trader is a form of business

where the owner is self employed and runs

the business as individual. In sole trader

business owner is solely responsible for the

debts and obligations of the business. Sole

trader has an unlimited liability over the

business. Sole trader is not required to

prepare accounts as per the required

accounting standards. They are not required

to comply with the regulations for

preparation of financial records. There is no

prescribed format for the sole trade to

prepare its accounts. Accounts of sole trader

are prepared as per the requirement of

owners. Sole trader enjoy the whole profits

unlike the partnership and limited company.

Partnership

Partnership refers to form of

business in which 2 or more people come

together for carrying out the business.

Partners pool resources in partnership for

starting the business. Partnership is formed

on oral or written agreements on mutual

agreements of the partners. Profit and losses

are shared in the partnership firm in the ratio

agreed between them in agreements.

Partnership firms are required to prepare

accounts as per the partnership act (Robson,

Young and Power, 2017). They are not

required to prepare the financial statement as

per the accounting standards for reporting to

the public. Liability of the partners is

unlimited in the unlimited partnership and

limited in the limited partnership firm to the

extent of their contribution in the business.

In a partnership business tax is charged on

the individual income of partners and not

over the partnership firms.

Limited Company

Limited company is the organisation

set up for running a business. Unlike the

sole trader and partnership finance of the

business are separate from the personal

finances. A company is a separate legal

entity different from its owners. Company is

required to comply with all the regulations.

Companies are required to prepare financial

statements as per the accounting standards

given by the accounting bodies. For

preparation of financial statements all the

reporting framework and governing

principles are followed by the management.

Accounts of companies are audited for

3

ensuring that statements are free from errors

and misstatements before they are issued to

the public. Liabilities of company do not

extend to personal assets of owners. Also the

corporation tax is charged over the profits of

company and not like sole trader and

partnership business.

Explanation of the reconciliation process and tools & techniques used for checking general

ledger accounts. Explanation on variances and importance of the correctly entered figures.

Reconciliation is described as

the process of matching the accounts

that are recorded against the monthly

statements from the external sources

like bank statements for identifying

the differences in records. It other

words it is the process which

compares 2 sets of records for

identifying that the recorded figures

are in agreement and correct (Pratt,

2016). Accounts reconciliation is also

performed for ensuring that balances

in the general ledger are accurate,

consistent and complete. Company is

required to analyse the records of

general ledgers to ensure that they ar

correctly recorded and are free from

material misstatements.

Reconciliation process includes

reconciling the accounts of ledger with the

bank statement for ensuring that all the

entries are correctly recorded. There are

cases where the entries are recorded in cash

ledger of company but are not recorded in

the bank statement due to delay or errors. in

the bank reconciliation statement entries

recorded in the bank ledger and not in bank

statements are adjusted and vice versa. The

reconciliation process allows teh company

to identify the errors done on bank side and

identifying the frauds if any committed by

the employees of company. Trial balance is

also prepared for identifying that the balance

sin the ledger accounts are identified when

the balance of debit side is not equal to the

credit side.

Reconciliation should be performed on

regular basis for ensuring the integrity of the

financial records. It helps to uncover the

omission, theft, duplication and the

fraudulent transactions.

Document review is the method

involving review of the existing transactions

and documents for making sure that amount

recorded is actual amount spent. This review

is generally carried out with the help of

software (Narayanaswamy, 2017). For

example for reviewing the receipts and

identifying the discrepancies. It reconciles

the accounts with the actual invoices of the

4

and misstatements before they are issued to

the public. Liabilities of company do not

extend to personal assets of owners. Also the

corporation tax is charged over the profits of

company and not like sole trader and

partnership business.

Explanation of the reconciliation process and tools & techniques used for checking general

ledger accounts. Explanation on variances and importance of the correctly entered figures.

Reconciliation is described as

the process of matching the accounts

that are recorded against the monthly

statements from the external sources

like bank statements for identifying

the differences in records. It other

words it is the process which

compares 2 sets of records for

identifying that the recorded figures

are in agreement and correct (Pratt,

2016). Accounts reconciliation is also

performed for ensuring that balances

in the general ledger are accurate,

consistent and complete. Company is

required to analyse the records of

general ledgers to ensure that they ar

correctly recorded and are free from

material misstatements.

Reconciliation process includes

reconciling the accounts of ledger with the

bank statement for ensuring that all the

entries are correctly recorded. There are

cases where the entries are recorded in cash

ledger of company but are not recorded in

the bank statement due to delay or errors. in

the bank reconciliation statement entries

recorded in the bank ledger and not in bank

statements are adjusted and vice versa. The

reconciliation process allows teh company

to identify the errors done on bank side and

identifying the frauds if any committed by

the employees of company. Trial balance is

also prepared for identifying that the balance

sin the ledger accounts are identified when

the balance of debit side is not equal to the

credit side.

Reconciliation should be performed on

regular basis for ensuring the integrity of the

financial records. It helps to uncover the

omission, theft, duplication and the

fraudulent transactions.

Document review is the method

involving review of the existing transactions

and documents for making sure that amount

recorded is actual amount spent. This review

is generally carried out with the help of

software (Narayanaswamy, 2017). For

example for reviewing the receipts and

identifying the discrepancies. It reconciles

the accounts with the actual invoices of the

4

You're viewing a preview

Unlock full access by subscribing today!

transactions and ensuring that all the

transactions have double effect.

Analytics review use accounts of

previous levels or the historical activities for

estimating amount that should have been

recorded in accounts. It verifies the banks

statements and cash account for identifying

the irregularities, errors in balance sheet or

any fraudulent activities gong in within the

organization.

Variances are the differences between

the actual and budgeted costs or revenues of

the business income and expense. It

represents the amount of variation in the

budgeted and actual figures for reviewing

the steps or process adopted. On the basis

management plans to make more efficient

strategies.

Figures represented in the financial

statement are required to be correct and free

from errors and mistakes. These financial

statements are used by various users for

decision making such as investments and

ventures. As per the statutory compliance

requirements financial statements should

represent the actual performance and

position of the company as stakeholders are

interested in the operations of business.

Explanation of the control accounts and their use in financial accounting.

Control account is often called

controlling account. This is a general

ledger account which summarises &

combines all subsidiary accounts for

the specific type. It is a summary

account which equals sum of

subsidiary account that is used for

simplifying and organising the ledger

accounts. General ledger could have

numbers of accounts from the assets

and liabilities accounts to incomes and

expenses (Hoggett and et.al., 2018).

Every type of account could have

hundred of the smaller accounts that

are known as subsidiary accounts.

Including every single account in

general ledger would be large,

difficult and unorganised to use. This

is the reason why control accounts are

used for summarising the data from

large number of related accounts.

Use of control account in financial

accounting.

General ledger accounts which sums

subsidiary accounts are considered to

control balances which are reported in

ledger. This is essential as subsidiary

accounts are not reported directly in general

ledger. Control accounts dictate what will

appear in general ledger and the things to be

5

transactions have double effect.

Analytics review use accounts of

previous levels or the historical activities for

estimating amount that should have been

recorded in accounts. It verifies the banks

statements and cash account for identifying

the irregularities, errors in balance sheet or

any fraudulent activities gong in within the

organization.

Variances are the differences between

the actual and budgeted costs or revenues of

the business income and expense. It

represents the amount of variation in the

budgeted and actual figures for reviewing

the steps or process adopted. On the basis

management plans to make more efficient

strategies.

Figures represented in the financial

statement are required to be correct and free

from errors and mistakes. These financial

statements are used by various users for

decision making such as investments and

ventures. As per the statutory compliance

requirements financial statements should

represent the actual performance and

position of the company as stakeholders are

interested in the operations of business.

Explanation of the control accounts and their use in financial accounting.

Control account is often called

controlling account. This is a general

ledger account which summarises &

combines all subsidiary accounts for

the specific type. It is a summary

account which equals sum of

subsidiary account that is used for

simplifying and organising the ledger

accounts. General ledger could have

numbers of accounts from the assets

and liabilities accounts to incomes and

expenses (Hoggett and et.al., 2018).

Every type of account could have

hundred of the smaller accounts that

are known as subsidiary accounts.

Including every single account in

general ledger would be large,

difficult and unorganised to use. This

is the reason why control accounts are

used for summarising the data from

large number of related accounts.

Use of control account in financial

accounting.

General ledger accounts which sums

subsidiary accounts are considered to

control balances which are reported in

ledger. This is essential as subsidiary

accounts are not reported directly in general

ledger. Control accounts dictate what will

appear in general ledger and the things to be

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reported in financial statements. For

example, accounts receivable of the

company could have hundreds of customers

with the current account receivable balances.

The balances are recorded separately in

accounts receivable subsidiary accounts

(Atanasov and Black, 2016). Total of the

accounts are carried forward in accounts

receivable control accounts that appears in

financial statements and general ledger. In

this manner ledger has only one accounts

receivables account in place of hundreds.

When any additional information is required

subsidiary accounts & records could be

reviewed. Control accounts clean up ledger

drastically and make it easier for the book

keepers and accountants to use the ledger

accounts.

Control accounts are used mainly for

identifying the errors in subsidiary ledgers

but also have various advantages due to

which it is used. It used for enabling the

accountants for extracting a single trial

balance from general ledger accounts. When

the balances of the trial balance do not

match control accounts whose balance do

not reconcile could be checked for errors

and mistakes (Cascino and et.al., 2019).

They are used for keeping check against the

frauds and helps in speeding up process for

producing the financial information as

balances of control accounts could be used

instead of waiting for individual balance to

be extracted and reconciled. It reduces the

amount of detailed information in general

ledger. Subsidiary ledgers are part of double

entry system where control accounts are

only prepared for information as they are not

part of system.

Description of process for reconciling control accounts and need to reconcile the accounts.

Reconciliation is the working to

ensure that entries in purchases and sales

ledger are agreeing with entries in control

accounts. Totals in each should exactly be

same, and if not it reflects the error either in

control account or memorandum account.

Discrepancies should be corrected and

investigated. For reconciliations balances of

payable or receivables control accounts are

reconciled with balances as per list of

payable or receivable ledger.

Steps for reconciling the control account

balances with ledger balances are

Step 1 – Adjusting the errors of control

accounts payable or receivable control

accounts by recording credits or debits.

Step 2 – Adjusting errors of payable

receivable ledger in list of the payable/

6

example, accounts receivable of the

company could have hundreds of customers

with the current account receivable balances.

The balances are recorded separately in

accounts receivable subsidiary accounts

(Atanasov and Black, 2016). Total of the

accounts are carried forward in accounts

receivable control accounts that appears in

financial statements and general ledger. In

this manner ledger has only one accounts

receivables account in place of hundreds.

When any additional information is required

subsidiary accounts & records could be

reviewed. Control accounts clean up ledger

drastically and make it easier for the book

keepers and accountants to use the ledger

accounts.

Control accounts are used mainly for

identifying the errors in subsidiary ledgers

but also have various advantages due to

which it is used. It used for enabling the

accountants for extracting a single trial

balance from general ledger accounts. When

the balances of the trial balance do not

match control accounts whose balance do

not reconcile could be checked for errors

and mistakes (Cascino and et.al., 2019).

They are used for keeping check against the

frauds and helps in speeding up process for

producing the financial information as

balances of control accounts could be used

instead of waiting for individual balance to

be extracted and reconciled. It reduces the

amount of detailed information in general

ledger. Subsidiary ledgers are part of double

entry system where control accounts are

only prepared for information as they are not

part of system.

Description of process for reconciling control accounts and need to reconcile the accounts.

Reconciliation is the working to

ensure that entries in purchases and sales

ledger are agreeing with entries in control

accounts. Totals in each should exactly be

same, and if not it reflects the error either in

control account or memorandum account.

Discrepancies should be corrected and

investigated. For reconciliations balances of

payable or receivables control accounts are

reconciled with balances as per list of

payable or receivable ledger.

Steps for reconciling the control account

balances with ledger balances are

Step 1 – Adjusting the errors of control

accounts payable or receivable control

accounts by recording credits or debits.

Step 2 – Adjusting errors of payable

receivable ledger in list of the payable/

6

receivable ledger balance by making the

additions or deductions as required.

After the above adjustments are made

balances of payable/ receivable control

accounts should reconcile with sum of the

list of payable / receivables ledger balances.

Need to Reconcile the financial

statements.

Reconciliation of the control

accounts is essential for identifying that the

balances of relevant ledger accounts match

with the totals of their respective control

account balances. This is carried to ensure

that the control accounts prepared from the

subsidiary ledger account balance are free

from errors and misstatements. Financial

statements prepared from the trial balances

should represent true and actual financial

figures. It should be free from any errors or

material misstatements that could impact the

decisions of users of the financial statements

(Biddle, Ma and Song, 2019). On

reconciliation errors are identified if

balances do not match it helps in

establishing reliability of the information

provided by the financial statements.

Reconciliation process has made the

accounting easier and reliable.

Explanation on purpose of suspense accounts and their difference from the control accounts.

Suspense account is general

ledger account where the amounts are

recorded temporarily. Suspense

accounts are used by the accountants

if appropriate ledger account for

recording the transaction could not be

determined at time of recording. When

the appropriate accounts are identified

the amounts are transferred from

suspense account. Entry in the

suspense account could be credit or

debit. Using suspense account for

recording transaction is more

appropriate rather than not recording

the transactions until there is sufficient

information available for creating the

entry in correct accounts. This may

cause larger transactions as

unrecorded till the end of reporting

period that will result in the inaccurate

financial results.

On the other control accounts are

prepared from the accounts that have already

been recorded. Control accounts are not

prepared for recording any transaction as

appropriate account was not identifiable

instead they are summarised account of all

the subsidiary ledger accounts that already

been correctly recorded by the companies.

Control accounts are different from each

other (Hanif and Mukherjee, 2018).

Suspense account is prepared for

7

additions or deductions as required.

After the above adjustments are made

balances of payable/ receivable control

accounts should reconcile with sum of the

list of payable / receivables ledger balances.

Need to Reconcile the financial

statements.

Reconciliation of the control

accounts is essential for identifying that the

balances of relevant ledger accounts match

with the totals of their respective control

account balances. This is carried to ensure

that the control accounts prepared from the

subsidiary ledger account balance are free

from errors and misstatements. Financial

statements prepared from the trial balances

should represent true and actual financial

figures. It should be free from any errors or

material misstatements that could impact the

decisions of users of the financial statements

(Biddle, Ma and Song, 2019). On

reconciliation errors are identified if

balances do not match it helps in

establishing reliability of the information

provided by the financial statements.

Reconciliation process has made the

accounting easier and reliable.

Explanation on purpose of suspense accounts and their difference from the control accounts.

Suspense account is general

ledger account where the amounts are

recorded temporarily. Suspense

accounts are used by the accountants

if appropriate ledger account for

recording the transaction could not be

determined at time of recording. When

the appropriate accounts are identified

the amounts are transferred from

suspense account. Entry in the

suspense account could be credit or

debit. Using suspense account for

recording transaction is more

appropriate rather than not recording

the transactions until there is sufficient

information available for creating the

entry in correct accounts. This may

cause larger transactions as

unrecorded till the end of reporting

period that will result in the inaccurate

financial results.

On the other control accounts are

prepared from the accounts that have already

been recorded. Control accounts are not

prepared for recording any transaction as

appropriate account was not identifiable

instead they are summarised account of all

the subsidiary ledger accounts that already

been correctly recorded by the companies.

Control accounts are different from each

other (Hanif and Mukherjee, 2018).

Suspense account is prepared for

7

You're viewing a preview

Unlock full access by subscribing today!

temporarily recording the accounting

transaction where the control accounts are

prepared for simplifying the control

accounts. Both control account and suspense

account are essential to be created by the

company for accurately representing the

financial statements.

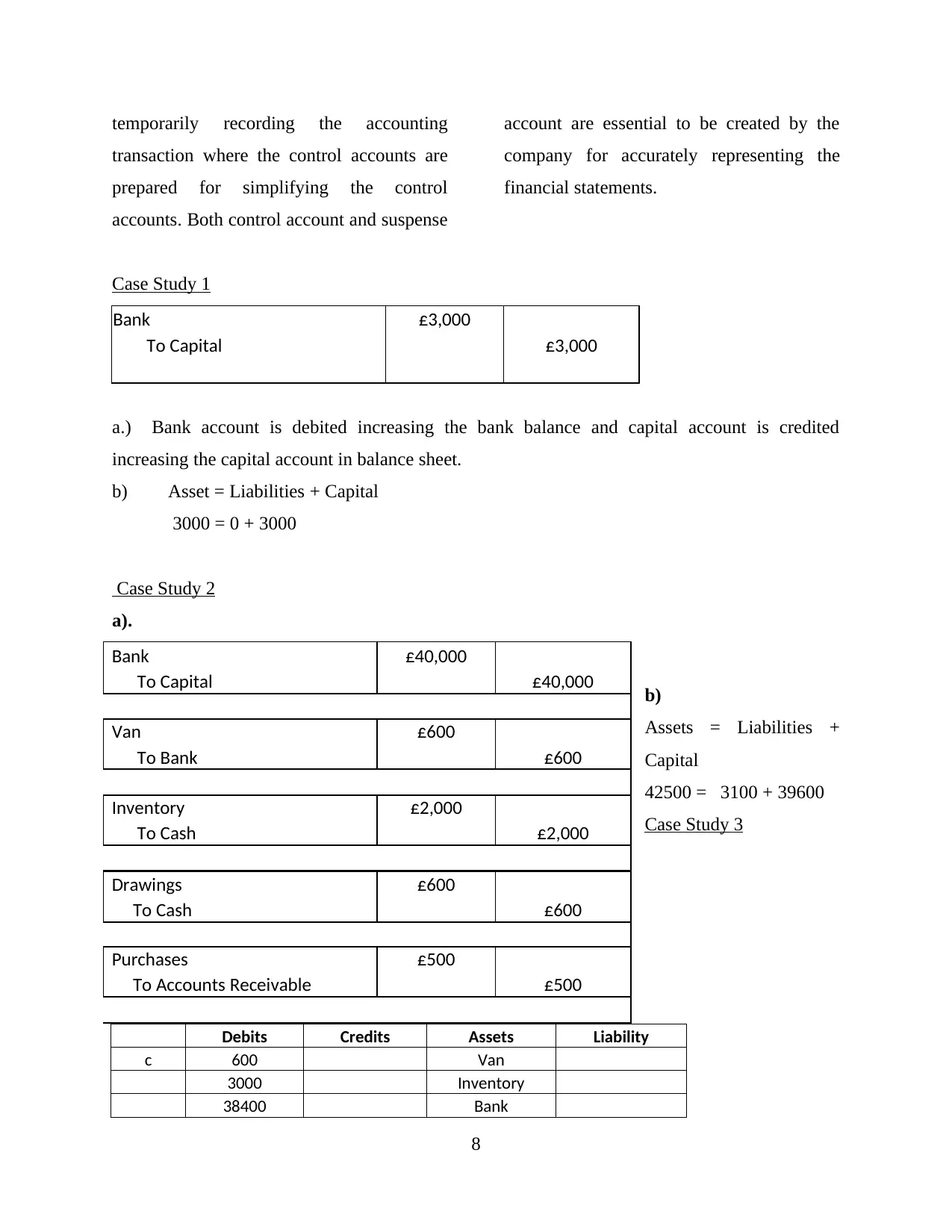

Case Study 1

Bank £3,000

To Capital £3,000

a.) Bank account is debited increasing the bank balance and capital account is credited

increasing the capital account in balance sheet.

b) Asset = Liabilities + Capital

3000 = 0 + 3000

Case Study 2

a).

b)

Assets = Liabilities +

Capital

42500 = 3100 + 39600

Case Study 3

Debits Credits Assets Liability

c 600 Van

3000 Inventory

38400 Bank

8

Bank £40,000

To Capital £40,000

Van £600

To Bank £600

Inventory £2,000

To Cash £2,000

Drawings £600

To Cash £600

Purchases £500

To Accounts Receivable £500

transaction where the control accounts are

prepared for simplifying the control

accounts. Both control account and suspense

account are essential to be created by the

company for accurately representing the

financial statements.

Case Study 1

Bank £3,000

To Capital £3,000

a.) Bank account is debited increasing the bank balance and capital account is credited

increasing the capital account in balance sheet.

b) Asset = Liabilities + Capital

3000 = 0 + 3000

Case Study 2

a).

b)

Assets = Liabilities +

Capital

42500 = 3100 + 39600

Case Study 3

Debits Credits Assets Liability

c 600 Van

3000 Inventory

38400 Bank

8

Bank £40,000

To Capital £40,000

Van £600

To Bank £600

Inventory £2,000

To Cash £2,000

Drawings £600

To Cash £600

Purchases £500

To Accounts Receivable £500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d 40000 Assets

e 600 600 -600 -600

f 600 Van

3000 Inventory

39400 Capital

g 39400 0 Assets

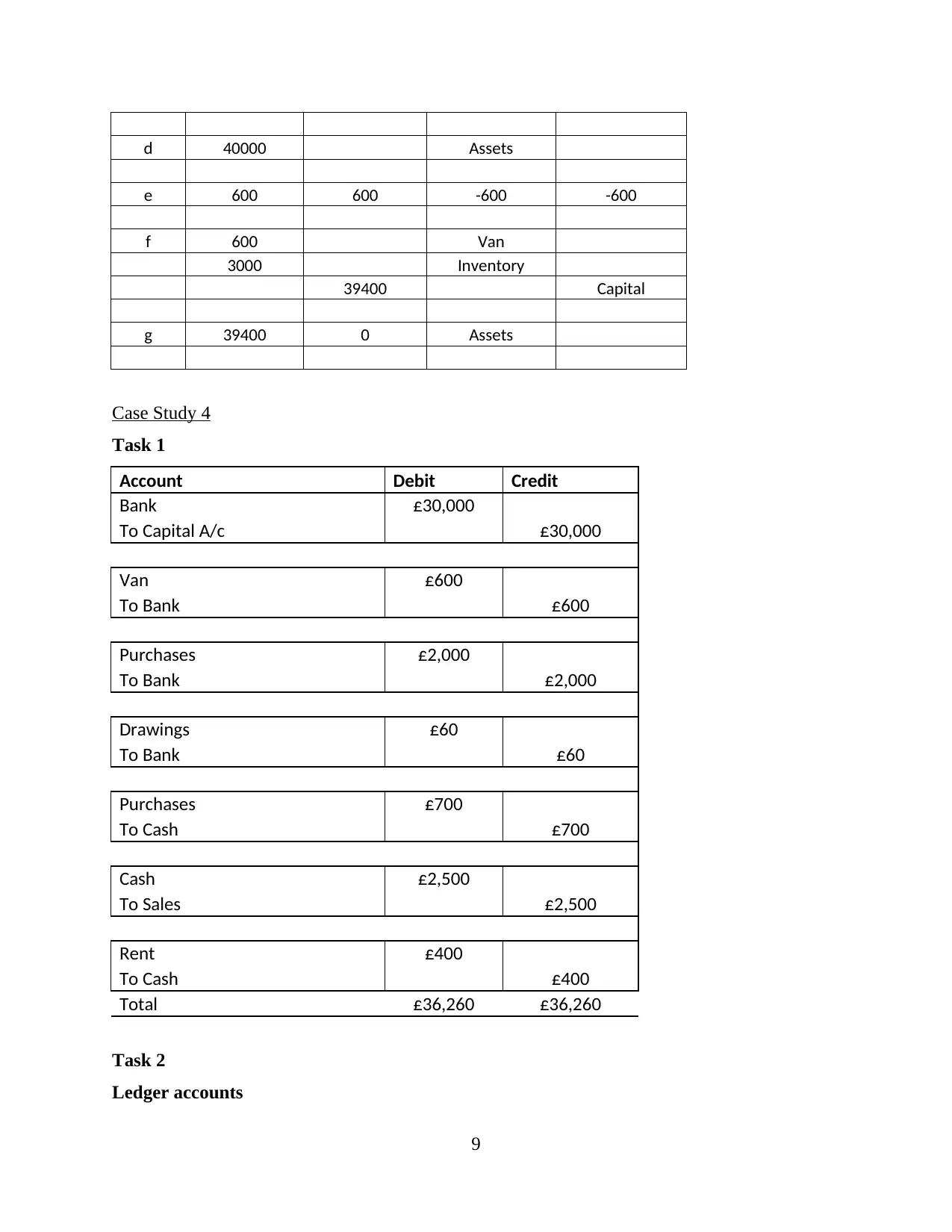

Case Study 4

Task 1

Account Debit Credit

Bank £30,000

To Capital A/c £30,000

Van £600

To Bank £600

Purchases £2,000

To Bank £2,000

Drawings £60

To Bank £60

Purchases £700

To Cash £700

Cash £2,500

To Sales £2,500

Rent £400

To Cash £400

Total £36,260 £36,260

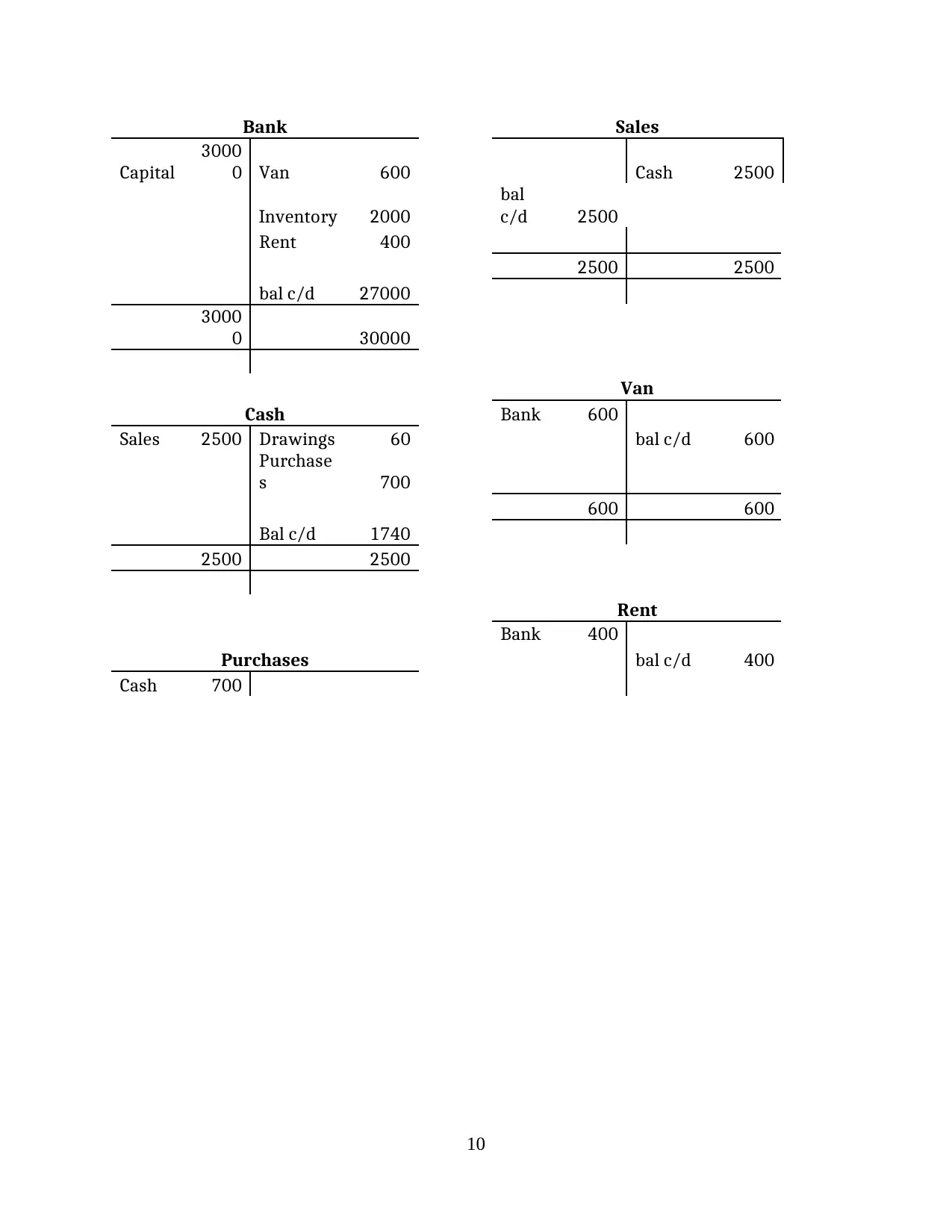

Task 2

Ledger accounts

9

e 600 600 -600 -600

f 600 Van

3000 Inventory

39400 Capital

g 39400 0 Assets

Case Study 4

Task 1

Account Debit Credit

Bank £30,000

To Capital A/c £30,000

Van £600

To Bank £600

Purchases £2,000

To Bank £2,000

Drawings £60

To Bank £60

Purchases £700

To Cash £700

Cash £2,500

To Sales £2,500

Rent £400

To Cash £400

Total £36,260 £36,260

Task 2

Ledger accounts

9

Bank Sales

Capital

3000

0 Van 600 Cash 2500

Inventory 2000

bal

c/d 2500

Rent 400

2500 2500

bal c/d 27000

3000

0 30000

Van

Cash Bank 600

Sales 2500 Drawings 60 bal c/d 600

Purchase

s 700

600 600

Bal c/d 1740

2500 2500

Rent

Bank 400

Purchases bal c/d 400

Cash 700

10

Capital

3000

0 Van 600 Cash 2500

Inventory 2000

bal

c/d 2500

Rent 400

2500 2500

bal c/d 27000

3000

0 30000

Van

Cash Bank 600

Sales 2500 Drawings 60 bal c/d 600

Purchase

s 700

600 600

Bal c/d 1740

2500 2500

Rent

Bank 400

Purchases bal c/d 400

Cash 700

10

You're viewing a preview

Unlock full access by subscribing today!

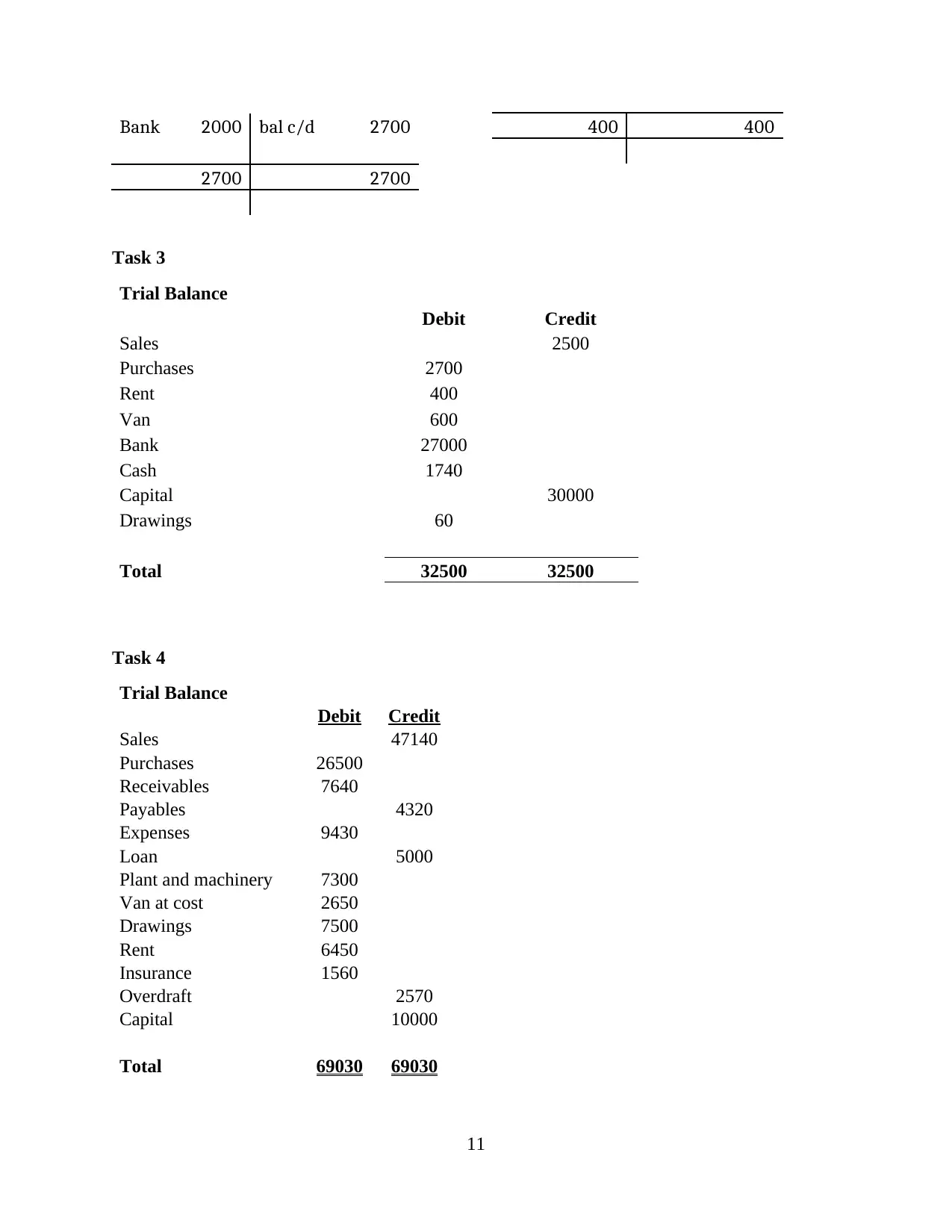

Bank 2000 bal c/d 2700 400 400

2700 2700

Task 3

Trial Balance

Debit Credit

Sales 2500

Purchases 2700

Rent 400

Van 600

Bank 27000

Cash 1740

Capital 30000

Drawings 60

Total 32500 32500

Task 4

Trial Balance

Debit Credit

Sales 47140

Purchases 26500

Receivables 7640

Payables 4320

Expenses 9430

Loan 5000

Plant and machinery 7300

Van at cost 2650

Drawings 7500

Rent 6450

Insurance 1560

Overdraft 2570

Capital 10000

Total 69030 69030

11

2700 2700

Task 3

Trial Balance

Debit Credit

Sales 2500

Purchases 2700

Rent 400

Van 600

Bank 27000

Cash 1740

Capital 30000

Drawings 60

Total 32500 32500

Task 4

Trial Balance

Debit Credit

Sales 47140

Purchases 26500

Receivables 7640

Payables 4320

Expenses 9430

Loan 5000

Plant and machinery 7300

Van at cost 2650

Drawings 7500

Rent 6450

Insurance 1560

Overdraft 2570

Capital 10000

Total 69030 69030

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

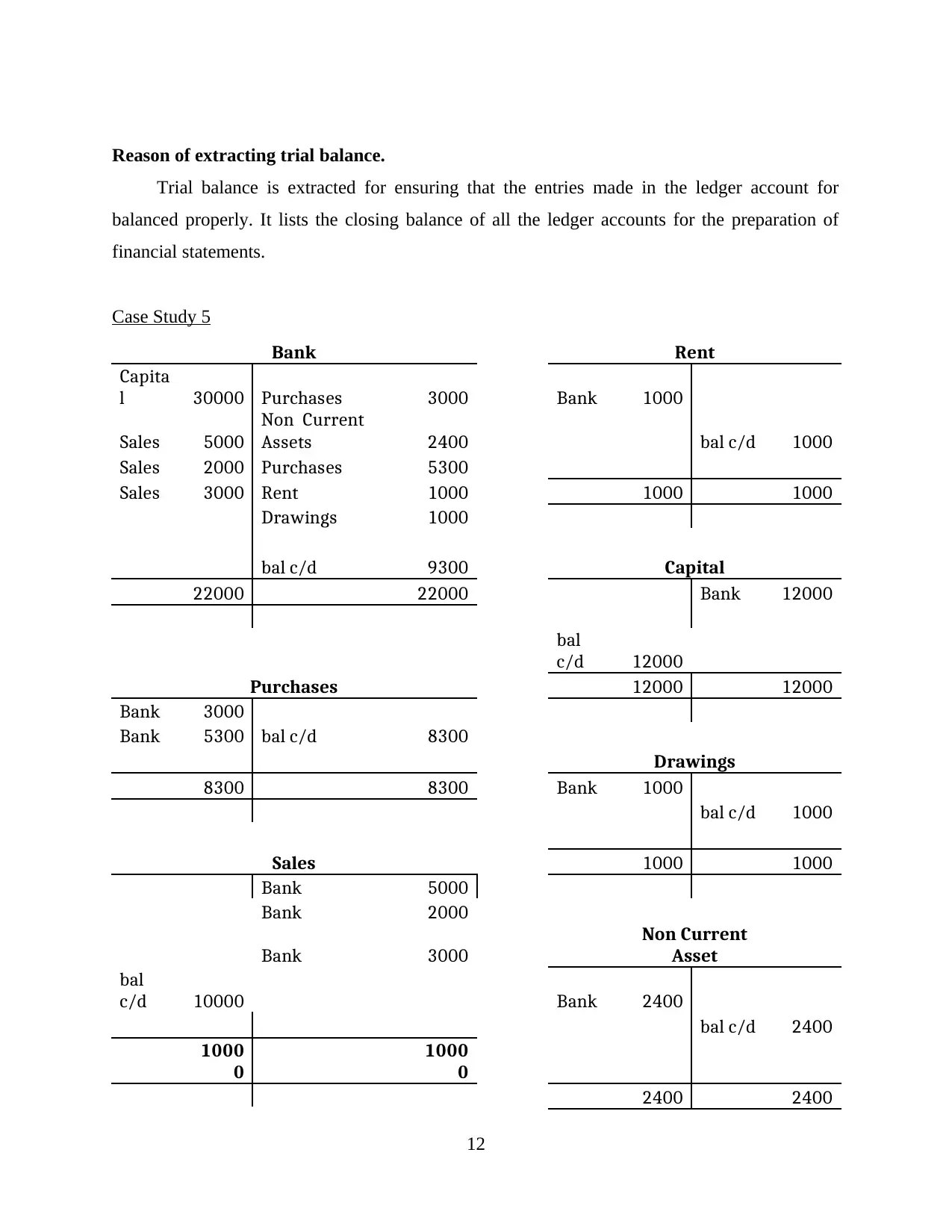

Reason of extracting trial balance.

Trial balance is extracted for ensuring that the entries made in the ledger account for

balanced properly. It lists the closing balance of all the ledger accounts for the preparation of

financial statements.

Case Study 5

Bank Rent

Capita

l 30000 Purchases 3000 Bank 1000

Sales 5000

Non Current

Assets 2400 bal c/d 1000

Sales 2000 Purchases 5300

Sales 3000 Rent 1000 1000 1000

Drawings 1000

bal c/d 9300 Capital

22000 22000 Bank 12000

bal

c/d 12000

Purchases 12000 12000

Bank 3000

Bank 5300 bal c/d 8300

Drawings

8300 8300 Bank 1000

bal c/d 1000

Sales 1000 1000

Bank 5000

Bank 2000

Bank 3000

Non Current

Asset

bal

c/d 10000 Bank 2400

bal c/d 2400

1000

0

1000

0

2400 2400

12

Trial balance is extracted for ensuring that the entries made in the ledger account for

balanced properly. It lists the closing balance of all the ledger accounts for the preparation of

financial statements.

Case Study 5

Bank Rent

Capita

l 30000 Purchases 3000 Bank 1000

Sales 5000

Non Current

Assets 2400 bal c/d 1000

Sales 2000 Purchases 5300

Sales 3000 Rent 1000 1000 1000

Drawings 1000

bal c/d 9300 Capital

22000 22000 Bank 12000

bal

c/d 12000

Purchases 12000 12000

Bank 3000

Bank 5300 bal c/d 8300

Drawings

8300 8300 Bank 1000

bal c/d 1000

Sales 1000 1000

Bank 5000

Bank 2000

Bank 3000

Non Current

Asset

bal

c/d 10000 Bank 2400

bal c/d 2400

1000

0

1000

0

2400 2400

12

Trial Balance

Trial Balance

Debit Credit

Bank 9300

Sales 10000

Purchases 8300

Non Current Assets 2400

Drawings 1000

Rent 1000

Capital 12000

Total 22000 22000

Question : Purpose of book double entry ?

Double entry system requires that every transaction of the business entered in debit should

be equal to amounts entered in the credit.

ACCOUNTING

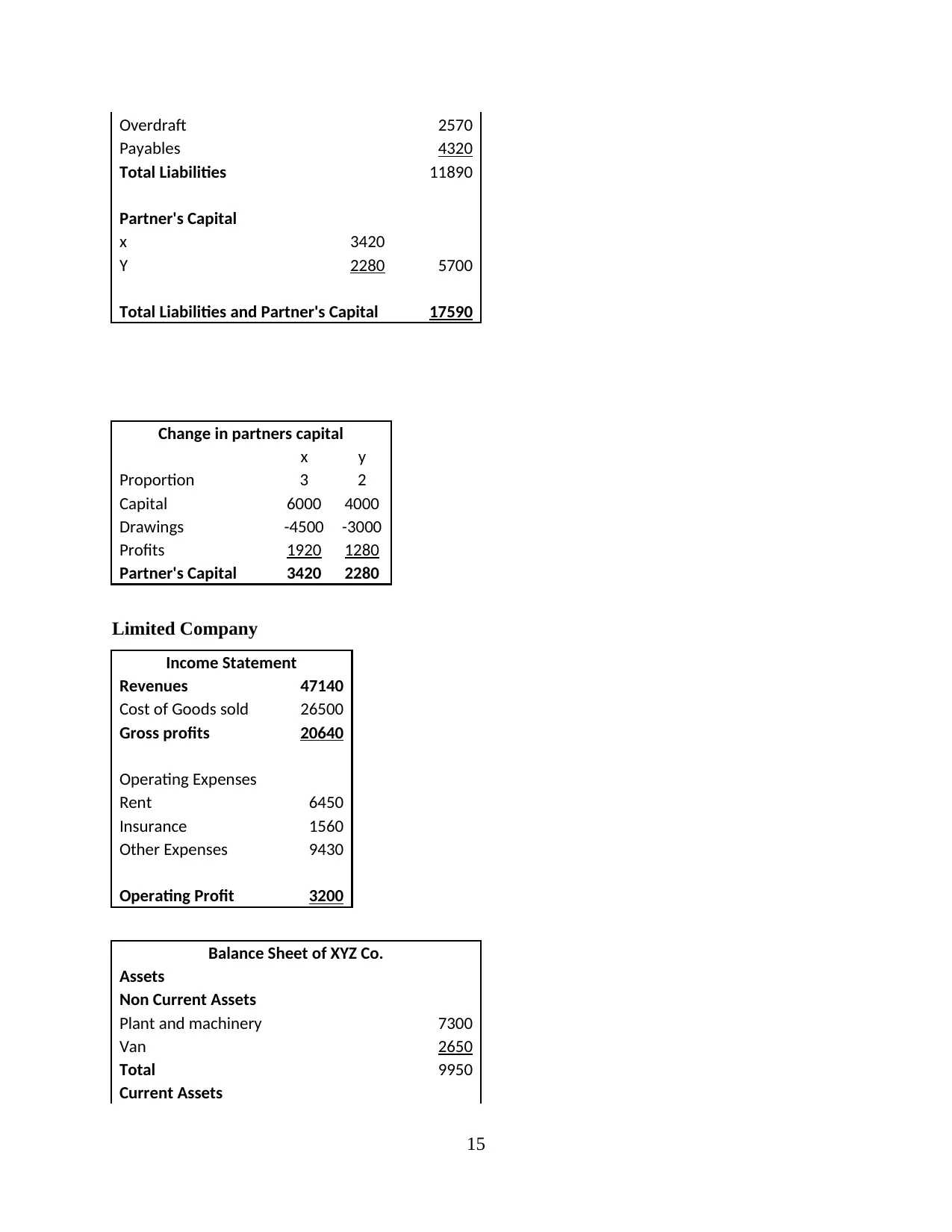

Final accounts of sole trader, partnership and company

Sole Trader

Income Statement

Sales 47140

Cost of Goods sold 26500

Gross profits 20640

Expenses

Rent 6450

Insurance 1560

Other Expenses 9430

Net Profit 3200

Balance Sheet

Assets

13

Trial Balance

Debit Credit

Bank 9300

Sales 10000

Purchases 8300

Non Current Assets 2400

Drawings 1000

Rent 1000

Capital 12000

Total 22000 22000

Question : Purpose of book double entry ?

Double entry system requires that every transaction of the business entered in debit should

be equal to amounts entered in the credit.

ACCOUNTING

Final accounts of sole trader, partnership and company

Sole Trader

Income Statement

Sales 47140

Cost of Goods sold 26500

Gross profits 20640

Expenses

Rent 6450

Insurance 1560

Other Expenses 9430

Net Profit 3200

Balance Sheet

Assets

13

You're viewing a preview

Unlock full access by subscribing today!

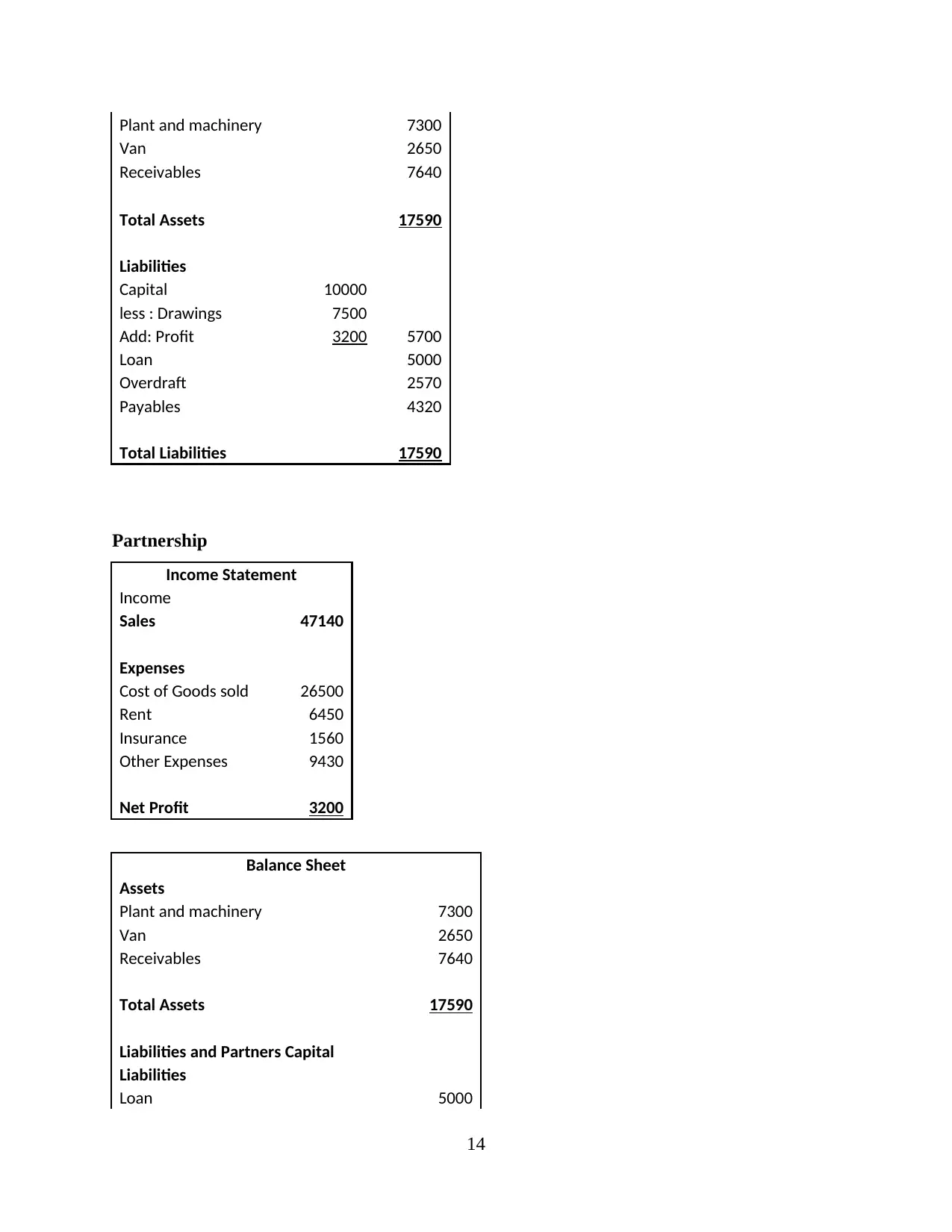

Plant and machinery 7300

Van 2650

Receivables 7640

Total Assets 17590

Liabilities

Capital 10000

less : Drawings 7500

Add: Profit 3200 5700

Loan 5000

Overdraft 2570

Payables 4320

Total Liabilities 17590

Partnership

Income Statement

Income

Sales 47140

Expenses

Cost of Goods sold 26500

Rent 6450

Insurance 1560

Other Expenses 9430

Net Profit 3200

Balance Sheet

Assets

Plant and machinery 7300

Van 2650

Receivables 7640

Total Assets 17590

Liabilities and Partners Capital

Liabilities

Loan 5000

14

Van 2650

Receivables 7640

Total Assets 17590

Liabilities

Capital 10000

less : Drawings 7500

Add: Profit 3200 5700

Loan 5000

Overdraft 2570

Payables 4320

Total Liabilities 17590

Partnership

Income Statement

Income

Sales 47140

Expenses

Cost of Goods sold 26500

Rent 6450

Insurance 1560

Other Expenses 9430

Net Profit 3200

Balance Sheet

Assets

Plant and machinery 7300

Van 2650

Receivables 7640

Total Assets 17590

Liabilities and Partners Capital

Liabilities

Loan 5000

14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Overdraft 2570

Payables 4320

Total Liabilities 11890

Partner's Capital

x 3420

Y 2280 5700

Total Liabilities and Partner's Capital 17590

Change in partners capital

x y

Proportion 3 2

Capital 6000 4000

Drawings -4500 -3000

Profits 1920 1280

Partner's Capital 3420 2280

Limited Company

Income Statement

Revenues 47140

Cost of Goods sold 26500

Gross profits 20640

Operating Expenses

Rent 6450

Insurance 1560

Other Expenses 9430

Operating Profit 3200

Balance Sheet of XYZ Co.

Assets

Non Current Assets

Plant and machinery 7300

Van 2650

Total 9950

Current Assets

15

Payables 4320

Total Liabilities 11890

Partner's Capital

x 3420

Y 2280 5700

Total Liabilities and Partner's Capital 17590

Change in partners capital

x y

Proportion 3 2

Capital 6000 4000

Drawings -4500 -3000

Profits 1920 1280

Partner's Capital 3420 2280

Limited Company

Income Statement

Revenues 47140

Cost of Goods sold 26500

Gross profits 20640

Operating Expenses

Rent 6450

Insurance 1560

Other Expenses 9430

Operating Profit 3200

Balance Sheet of XYZ Co.

Assets

Non Current Assets

Plant and machinery 7300

Van 2650

Total 9950

Current Assets

15

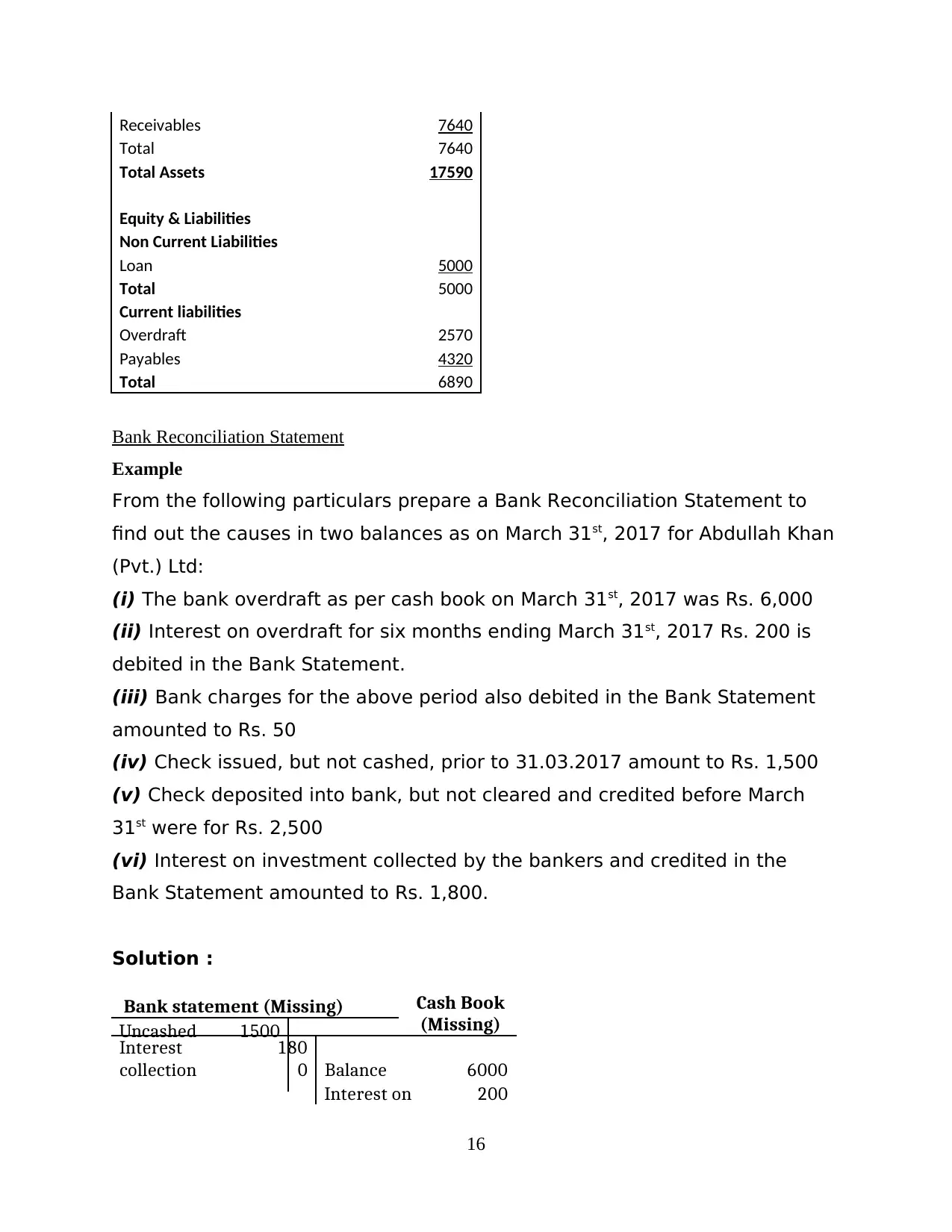

Receivables 7640

Total 7640

Total Assets 17590

Equity & Liabilities

Non Current Liabilities

Loan 5000

Total 5000

Current liabilities

Overdraft 2570

Payables 4320

Total 6890

Bank Reconciliation Statement

Example

From the following particulars prepare a Bank Reconciliation Statement to

find out the causes in two balances as on March 31st, 2017 for Abdullah Khan

(Pvt.) Ltd:

(i) The bank overdraft as per cash book on March 31st, 2017 was Rs. 6,000

(ii) Interest on overdraft for six months ending March 31st, 2017 Rs. 200 is

debited in the Bank Statement.

(iii) Bank charges for the above period also debited in the Bank Statement

amounted to Rs. 50

(iv) Check issued, but not cashed, prior to 31.03.2017 amount to Rs. 1,500

(v) Check deposited into bank, but not cleared and credited before March

31st were for Rs. 2,500

(vi) Interest on investment collected by the bankers and credited in the

Bank Statement amounted to Rs. 1,800.

Solution :

Cash Book

(Missing)

Interest

collection

180

0 Balance 6000

Interest on 200

16

Bank statement (Missing)

Uncashed 1500

Total 7640

Total Assets 17590

Equity & Liabilities

Non Current Liabilities

Loan 5000

Total 5000

Current liabilities

Overdraft 2570

Payables 4320

Total 6890

Bank Reconciliation Statement

Example

From the following particulars prepare a Bank Reconciliation Statement to

find out the causes in two balances as on March 31st, 2017 for Abdullah Khan

(Pvt.) Ltd:

(i) The bank overdraft as per cash book on March 31st, 2017 was Rs. 6,000

(ii) Interest on overdraft for six months ending March 31st, 2017 Rs. 200 is

debited in the Bank Statement.

(iii) Bank charges for the above period also debited in the Bank Statement

amounted to Rs. 50

(iv) Check issued, but not cashed, prior to 31.03.2017 amount to Rs. 1,500

(v) Check deposited into bank, but not cleared and credited before March

31st were for Rs. 2,500

(vi) Interest on investment collected by the bankers and credited in the

Bank Statement amounted to Rs. 1,800.

Solution :

Cash Book

(Missing)

Interest

collection

180

0 Balance 6000

Interest on 200

16

Bank statement (Missing)

Uncashed 1500

You're viewing a preview

Unlock full access by subscribing today!

O/d

Bank charges 50

Bank Reconciliation Statement

Bank Reconciliation Statement

Bank o/d as per cash book (Cr.) 6000

Add :

Interest on o/d 200

Bank Charges 50

Uncredited 2500 2750

8750

Less:

Interest collected on investment 1800

Uncashed cheque 1500 3300

Balance as per bank statement (Dr) 5450

Control Account

Example :

1. Accounts Receivable Account 7640

2. Receivables ledger control account 8540

3. Discount allowed not entered in control account but recorded in individual

ledger account of 100

4. Bad debts of 350 not recorded in control account.

5. Sales day book under casted by 550

6. On listing debit balance is incorrectly treated as credit of 1250

8. Collection from supplier treated in control account but not in receivables

individual account of 250.

Solution :

Receivables Control

account

Balanc

e

854

0

Sales 550

Discount

allowed 100

Bad Debts 350

bal c/d 8640

909 9090

17

Bank charges 50

Bank Reconciliation Statement

Bank Reconciliation Statement

Bank o/d as per cash book (Cr.) 6000

Add :

Interest on o/d 200

Bank Charges 50

Uncredited 2500 2750

8750

Less:

Interest collected on investment 1800

Uncashed cheque 1500 3300

Balance as per bank statement (Dr) 5450

Control Account

Example :

1. Accounts Receivable Account 7640

2. Receivables ledger control account 8540

3. Discount allowed not entered in control account but recorded in individual

ledger account of 100

4. Bad debts of 350 not recorded in control account.

5. Sales day book under casted by 550

6. On listing debit balance is incorrectly treated as credit of 1250

8. Collection from supplier treated in control account but not in receivables

individual account of 250.

Solution :

Receivables Control

account

Balanc

e

854

0

Sales 550

Discount

allowed 100

Bad Debts 350

bal c/d 8640

909 9090

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0

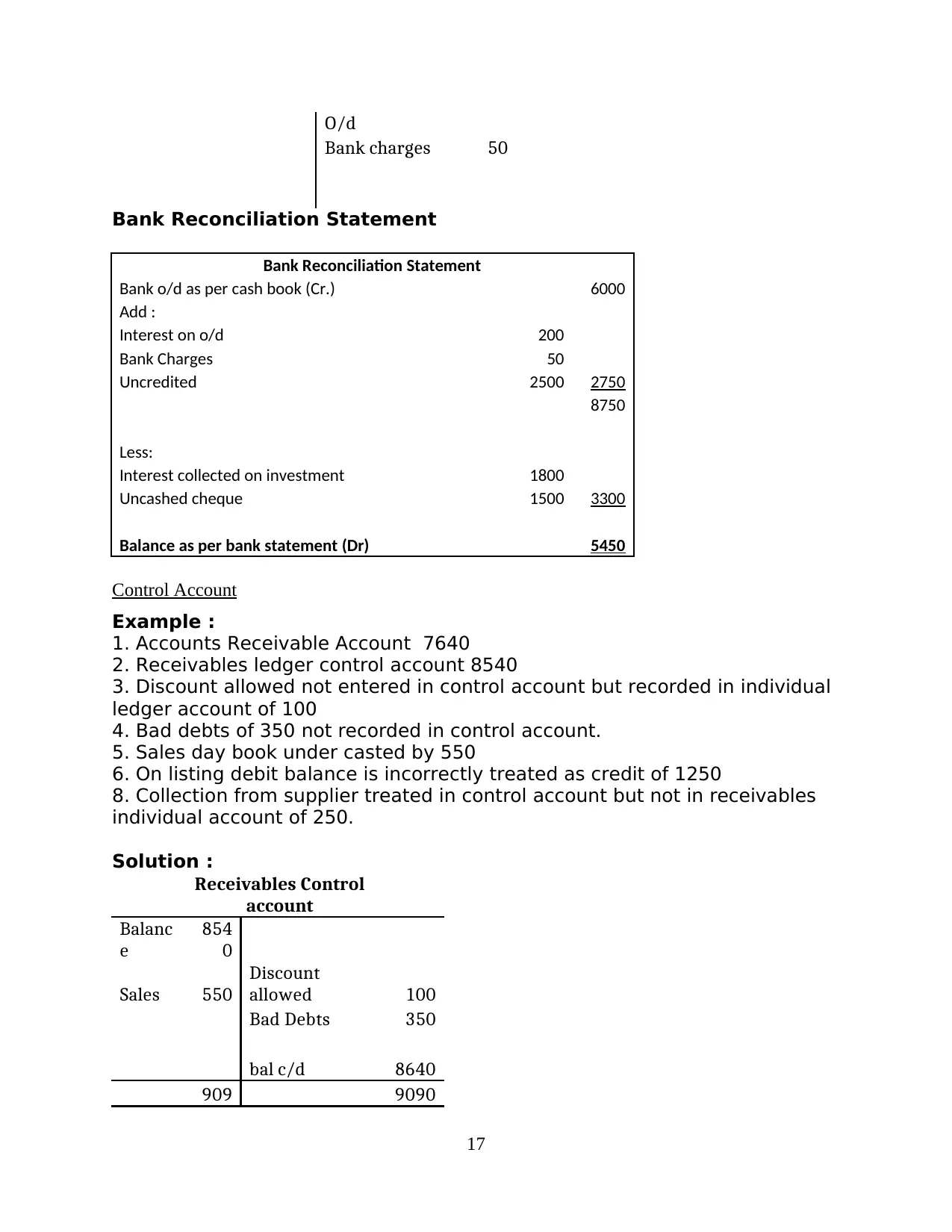

Reconciliation of control

account balance

Balance as extracted 7640

Debit balance incorrectly

recorded 1250

Cash collection -250

Net total agreeing with the

control account 8640

CONCLUSION

From the above report it could be concluded that the financial accounting plays a critical

role in the success of the organisation. it enables the company to appropriately record its

financial transactions for preparing the financial statements of company. Financial statements of

the company are required to be prepared in accordance with the applicable standards and

complying with the financial reporting frameworks.

18

Reconciliation of control

account balance

Balance as extracted 7640

Debit balance incorrectly

recorded 1250

Cash collection -250

Net total agreeing with the

control account 8640

CONCLUSION

From the above report it could be concluded that the financial accounting plays a critical

role in the success of the organisation. it enables the company to appropriately record its

financial transactions for preparing the financial statements of company. Financial statements of

the company are required to be prepared in accordance with the applicable standards and

complying with the financial reporting frameworks.

18

REFERENCES

Books and Journals

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

No, A.S., 2018. Conceptual framework for financial reporting. Norwalk, CT: FASB.

Robson, K., Young, J. and Power, M., 2017. Themed section on financial accounting as social

and organizational practice: exploring the work of financial reporting. Accounting,

Organizations and Society.56.pp.35-37.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Hoggett, J. and et.al., 2018. Financial accounting. Wiley.

Cascino, S. and et.al., 2019. The usefulness of financial accounting information: Evidence from

the field. Available at SSRN 3008083.

Biddle, G.C., Ma, M.L. and Song, F.M., 2019. Accounting conservatism and bankruptcy

risk. Available at SSRN 1621272.

Hanif, M. and Mukherjee, A., 2018. Financial Accounting-I. McGraw-Hill Education.

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate finance and

accounting research. Critical Finance Review.5.pp.207-304.

19

Books and Journals

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

No, A.S., 2018. Conceptual framework for financial reporting. Norwalk, CT: FASB.

Robson, K., Young, J. and Power, M., 2017. Themed section on financial accounting as social

and organizational practice: exploring the work of financial reporting. Accounting,

Organizations and Society.56.pp.35-37.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Hoggett, J. and et.al., 2018. Financial accounting. Wiley.

Cascino, S. and et.al., 2019. The usefulness of financial accounting information: Evidence from

the field. Available at SSRN 3008083.

Biddle, G.C., Ma, M.L. and Song, F.M., 2019. Accounting conservatism and bankruptcy

risk. Available at SSRN 1621272.

Hanif, M. and Mukherjee, A., 2018. Financial Accounting-I. McGraw-Hill Education.

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate finance and

accounting research. Critical Finance Review.5.pp.207-304.

19

You're viewing a preview

Unlock full access by subscribing today!

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.