Financial Accounting Exam - Financial Statements and Analysis

VerifiedAdded on 2022/10/12

|10

|1227

|17

Homework Assignment

AI Summary

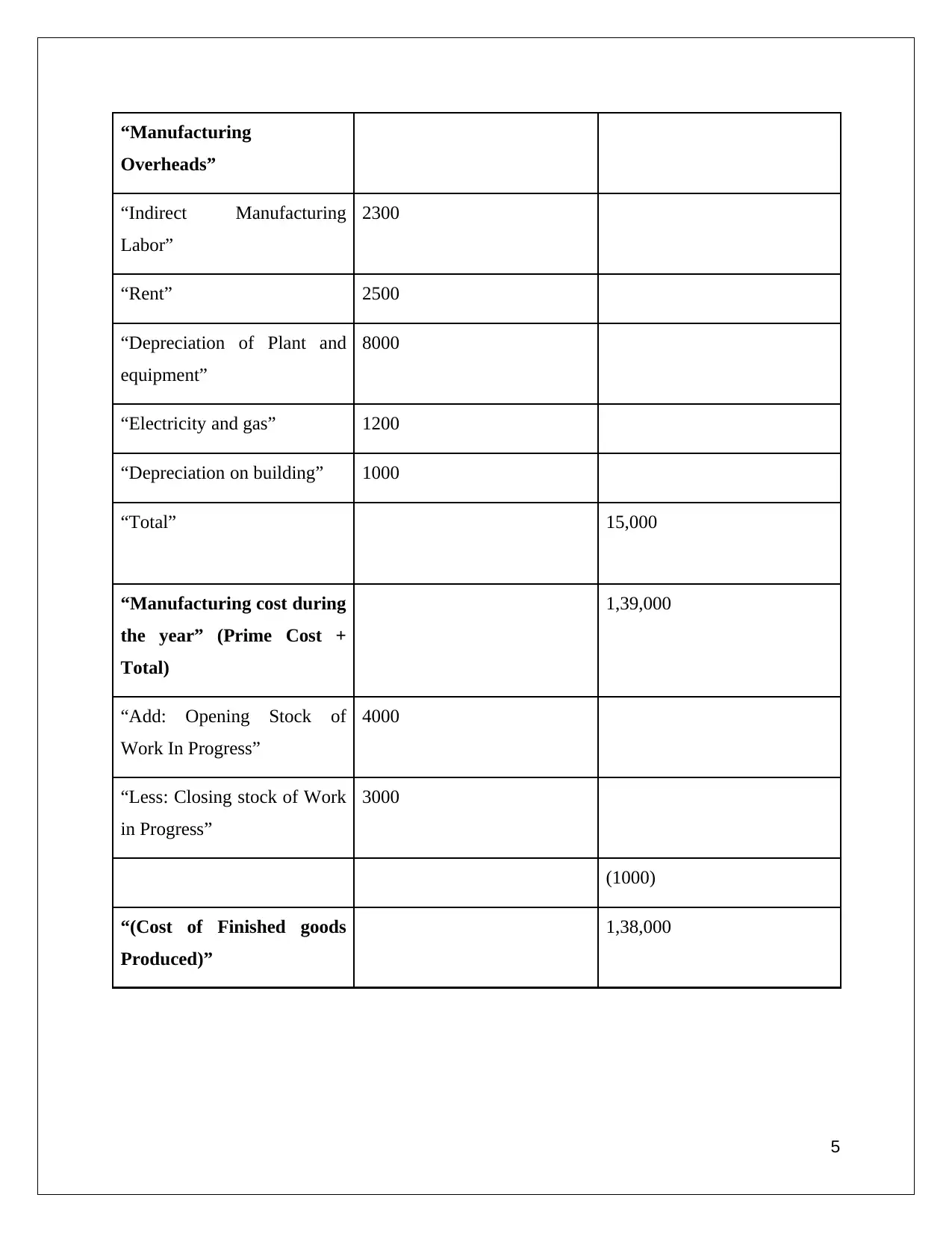

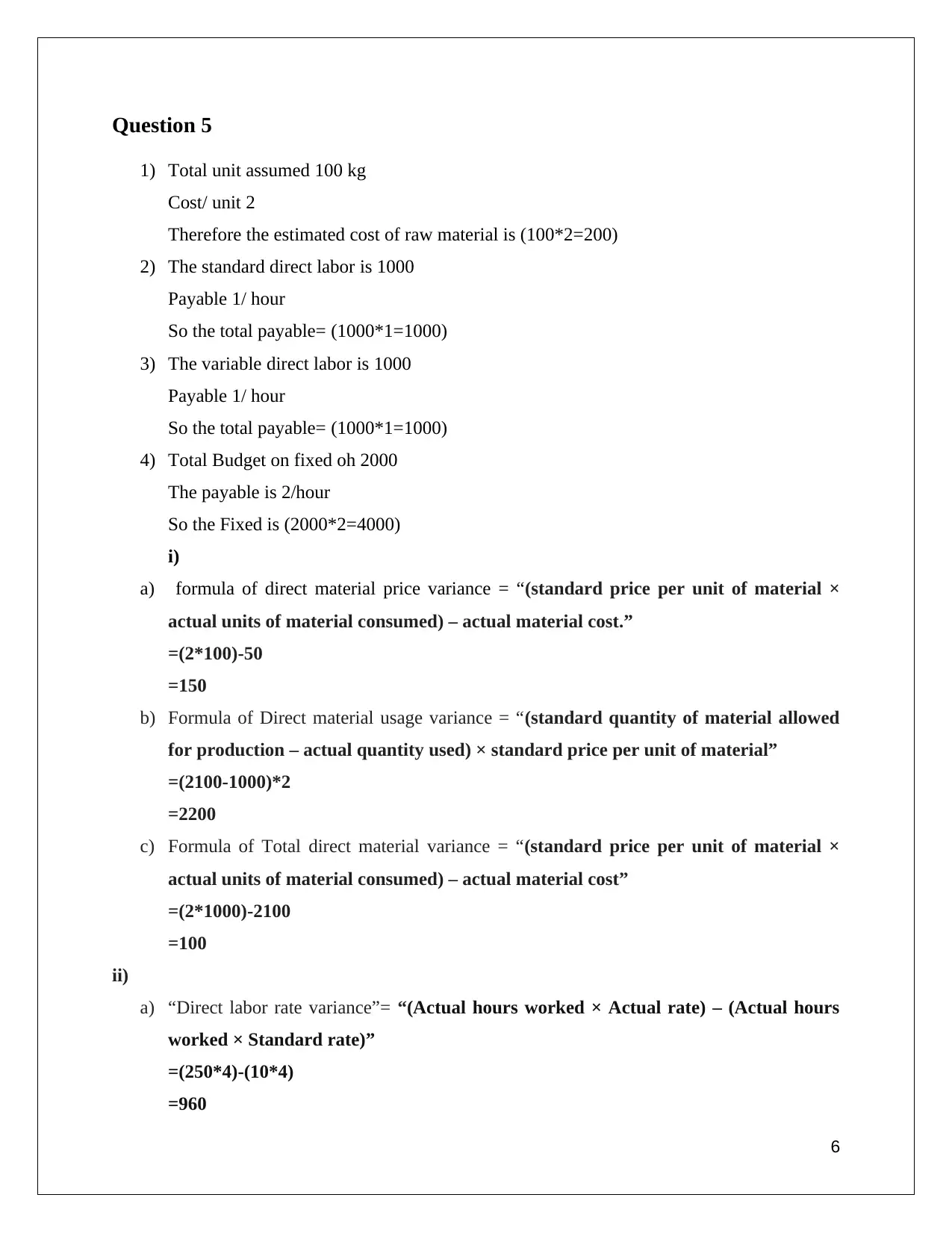

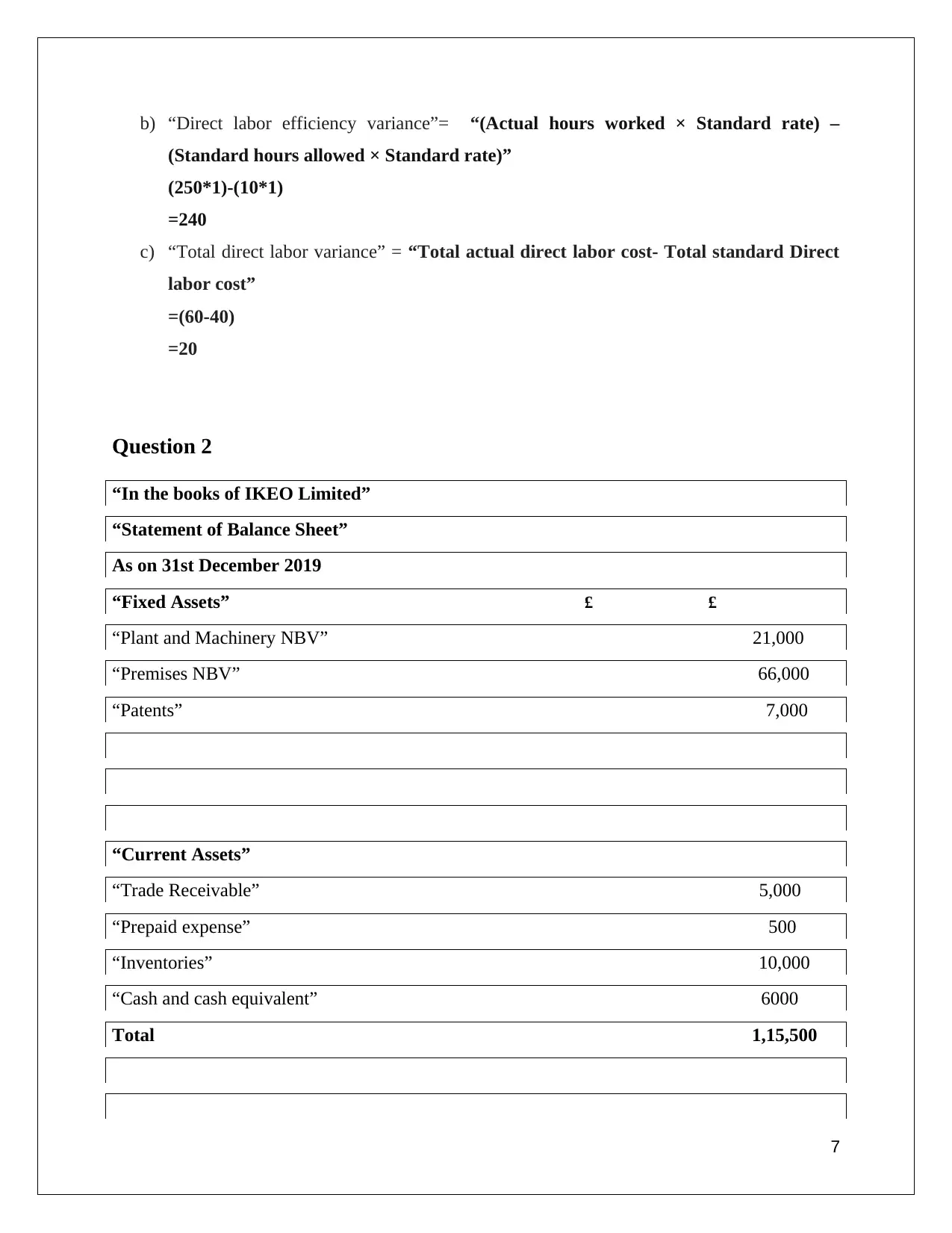

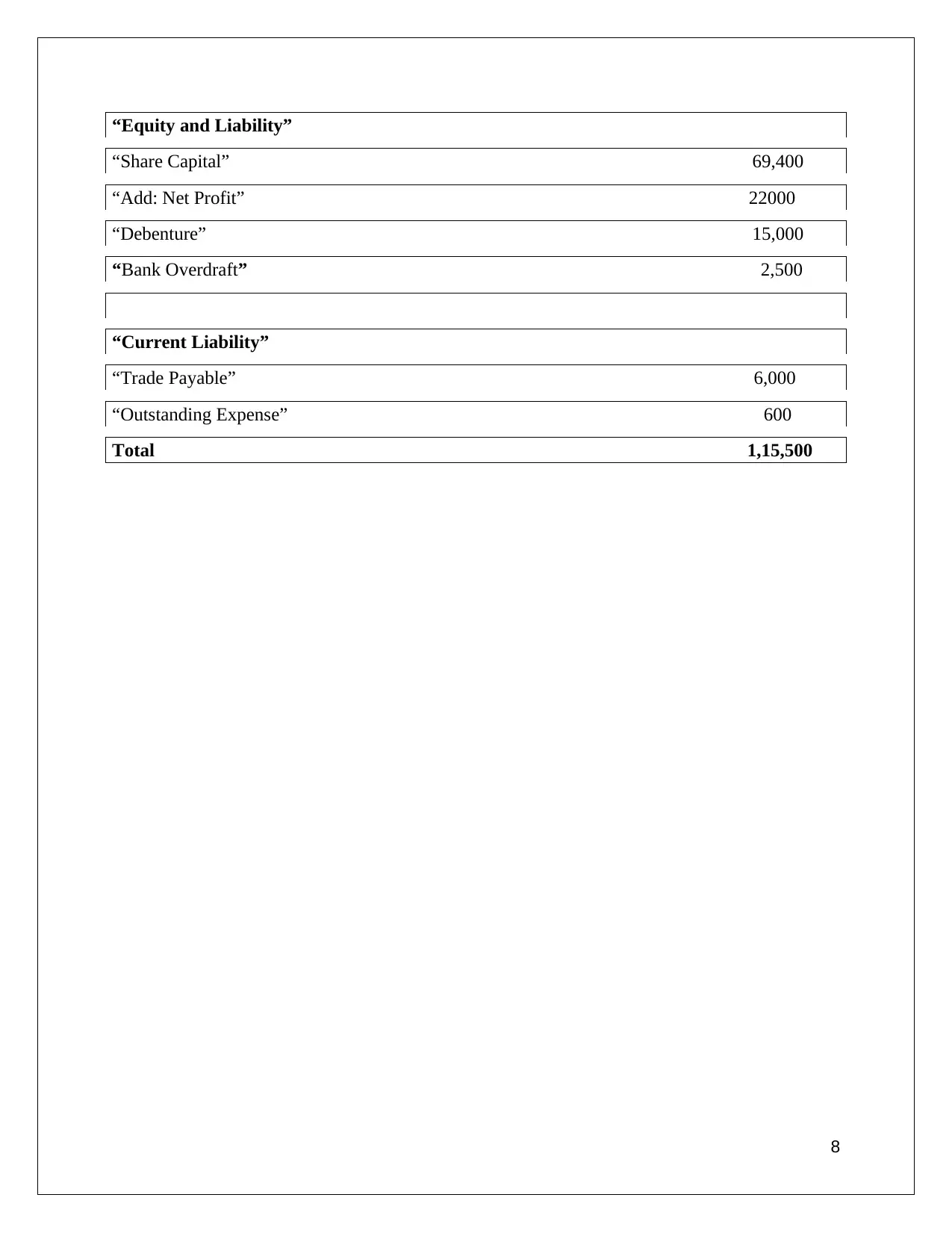

This document presents a comprehensive solution to a financial accounting exam, addressing various aspects of financial reporting and analysis. It includes detailed calculations and explanations for questions related to break-even points under different scenarios, cost of machine and rate of return, and the preparation of manufacturing accounts and balance sheets. The assignment also covers variance analysis for direct materials and direct labor, providing formulas and calculations to determine variances. Furthermore, the solution incorporates the preparation of financial statements, including a balance sheet, and references relevant academic journals and literature. The document serves as a valuable resource for students seeking to understand and solve financial accounting problems, providing a clear and concise approach to complex accounting concepts.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.