Introduction to Financial Accounting: Income Statement, Statement of Change in Equity, and Balance Sheet

VerifiedAdded on 2023/06/15

|9

|1111

|385

AI Summary

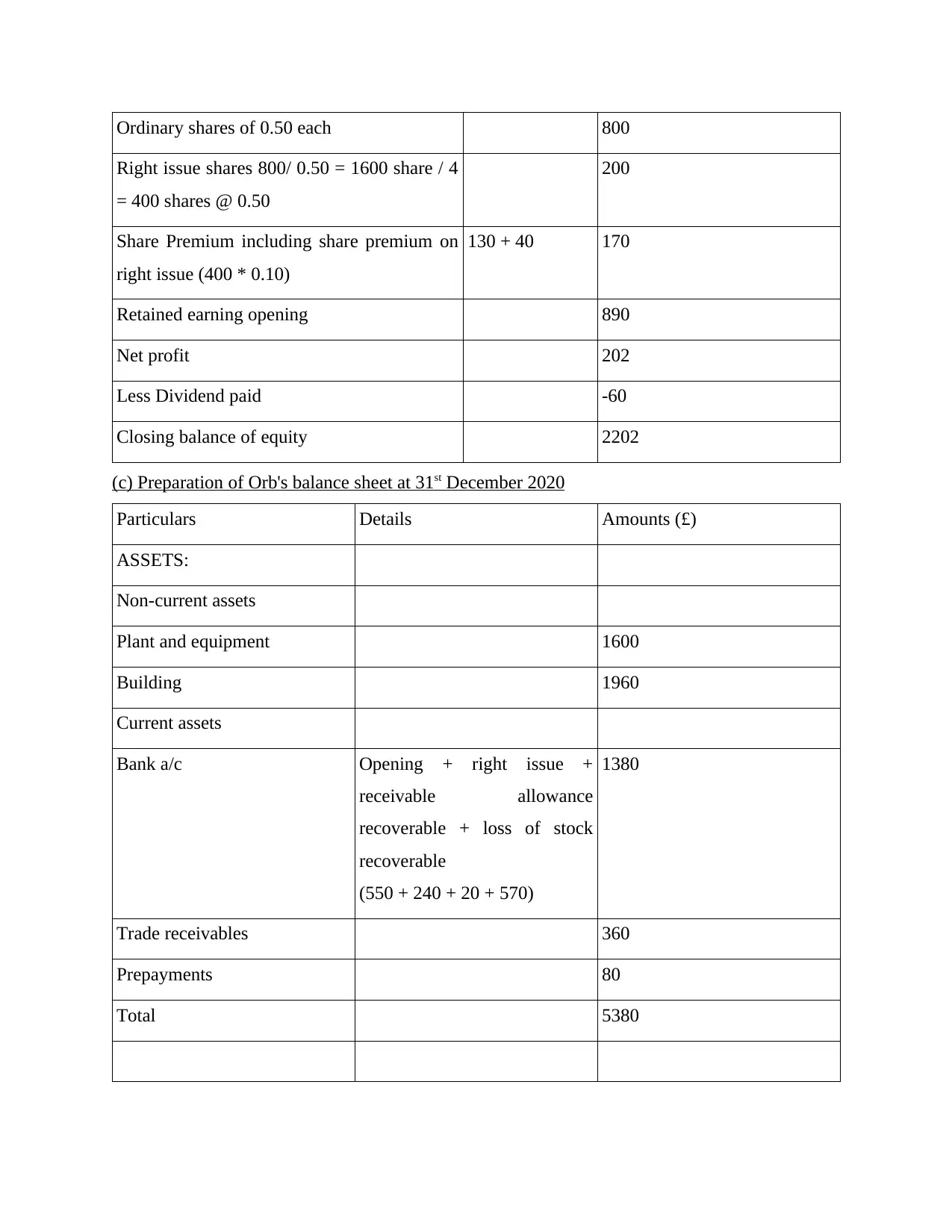

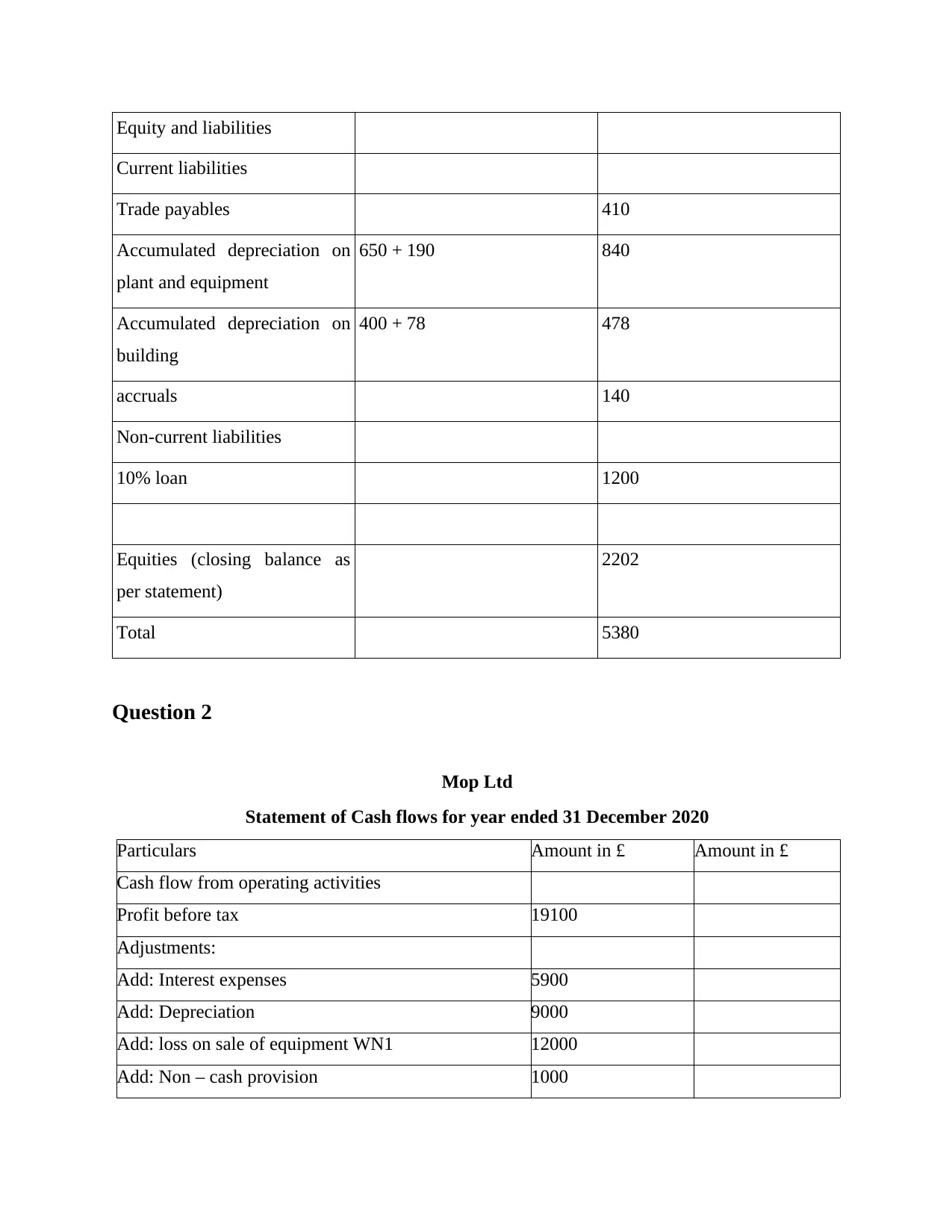

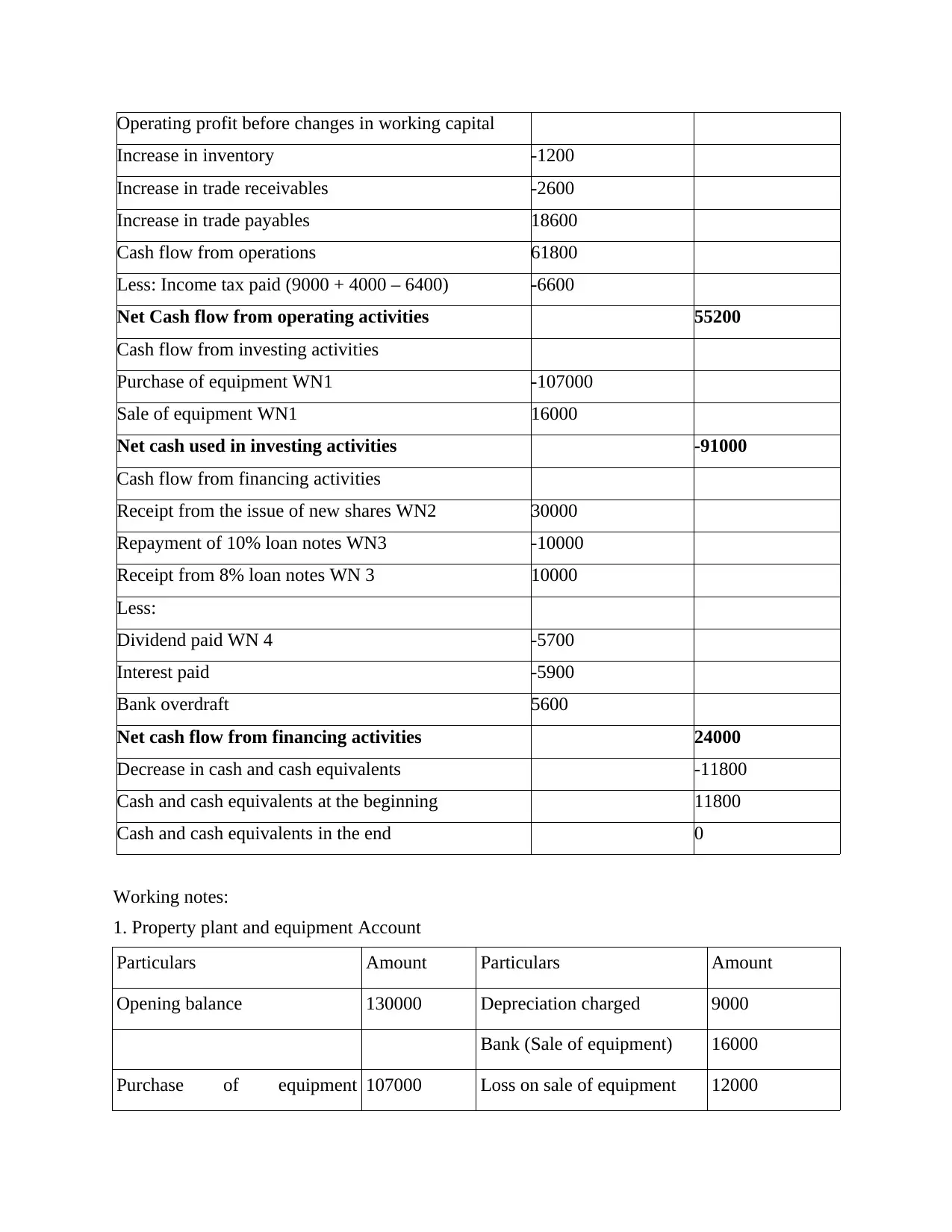

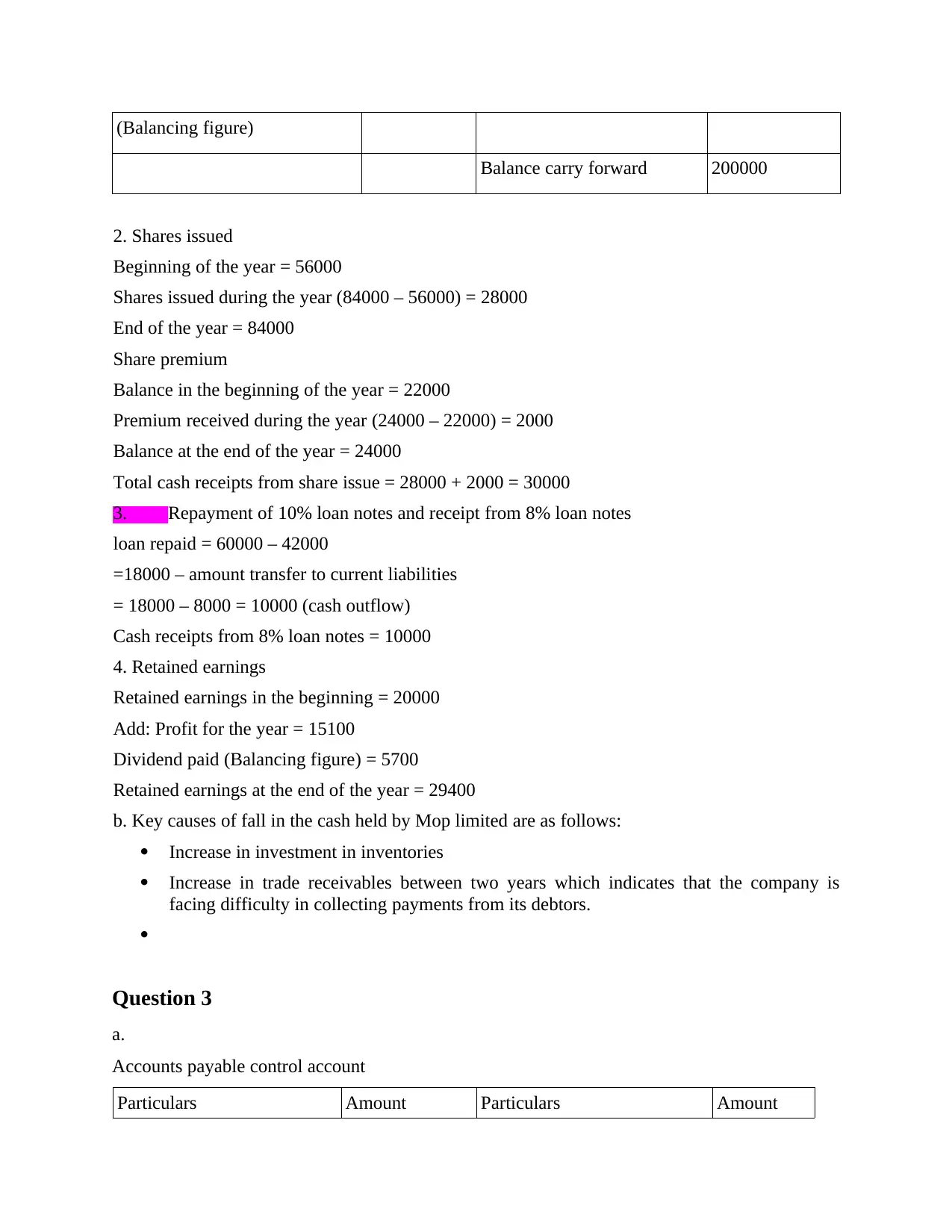

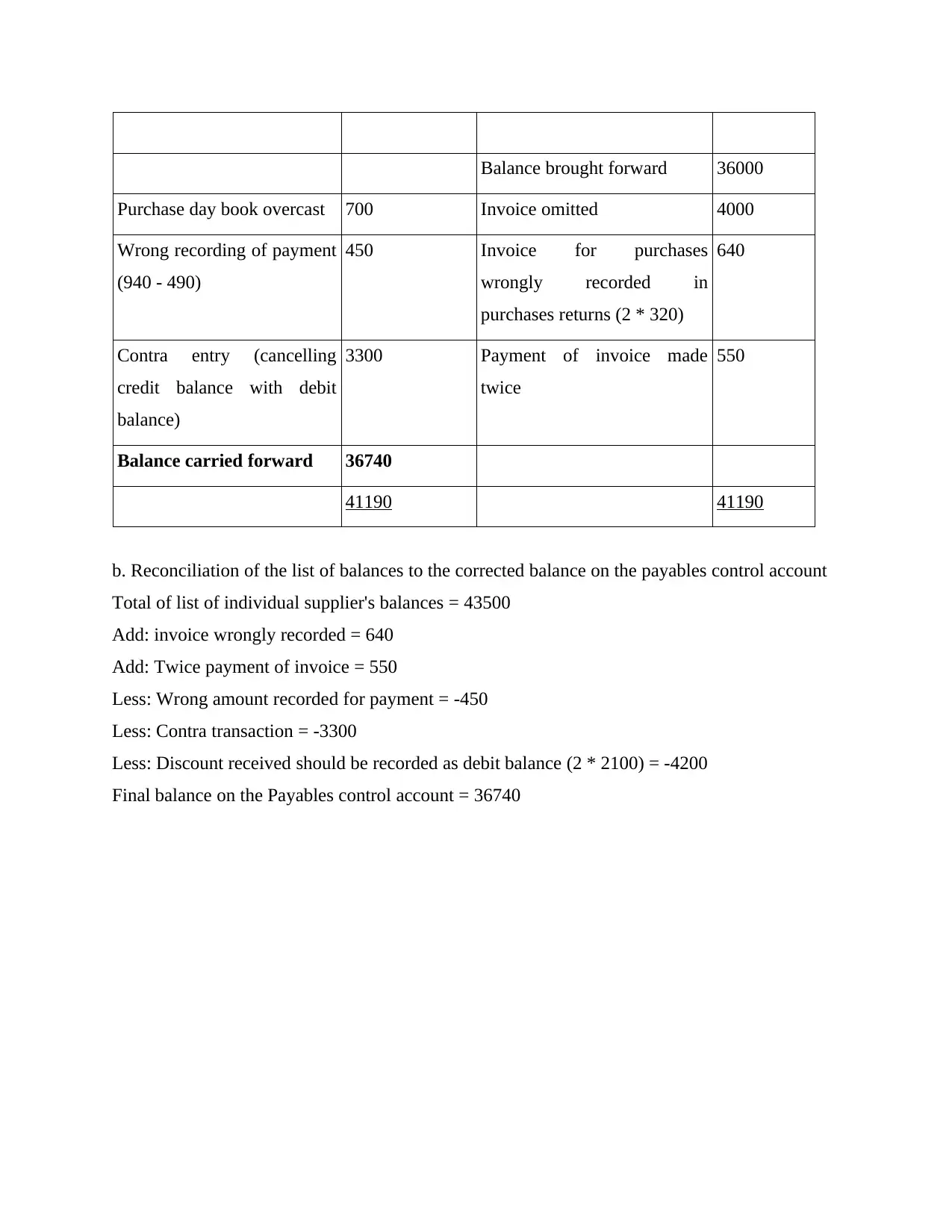

This article covers the preparation of income statement, statement of change in equity, and balance sheet with examples and working notes. It includes solved assignments and essays on financial accounting for students. The article also discusses the key causes of fall in cash held by Mop Limited and the reconciliation of accounts payable control account.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.