Financial Accounting Analysis of Goodwill & Expenses - Pewter Ltd

VerifiedAdded on 2023/06/06

|8

|1863

|92

Report

AI Summary

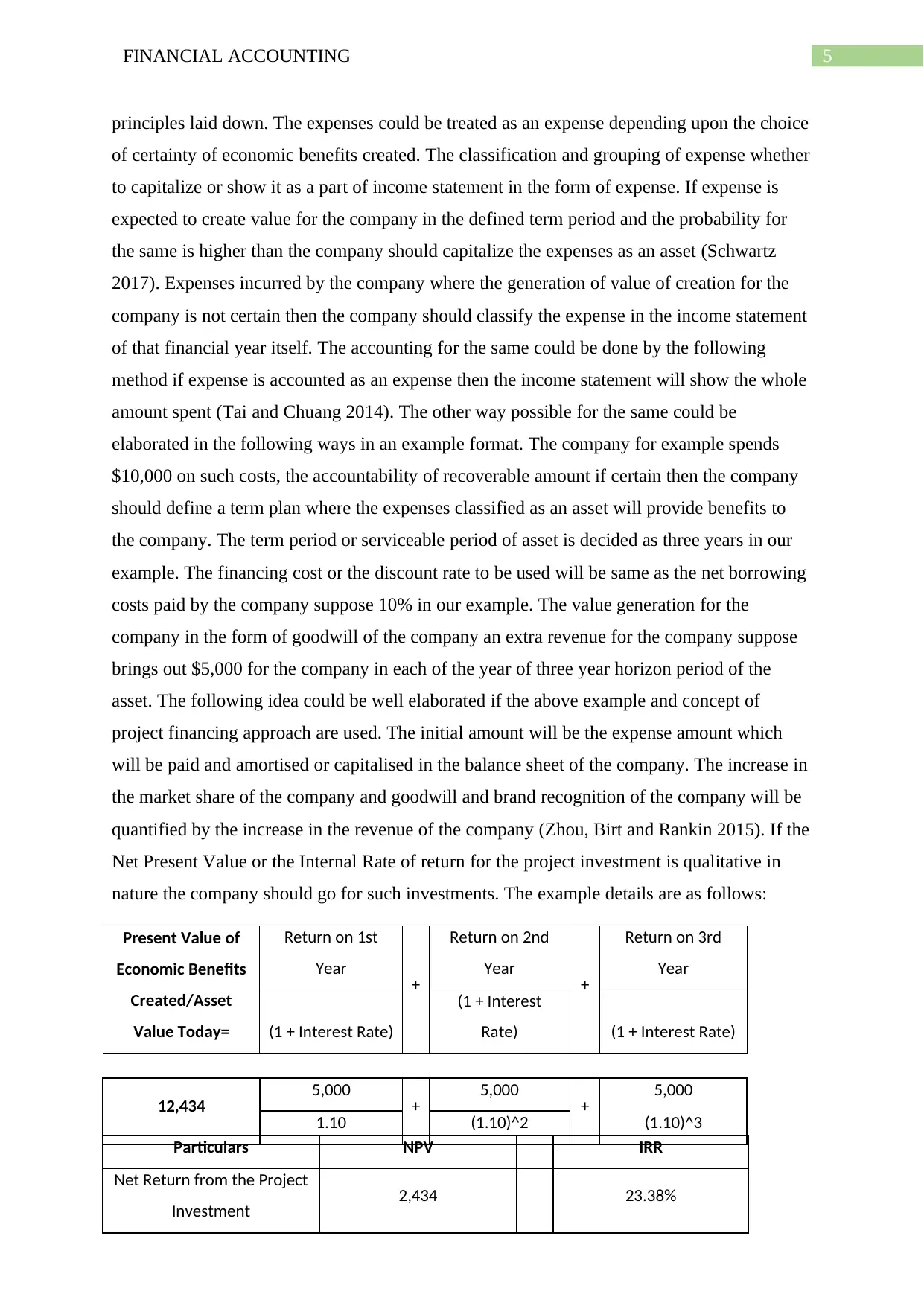

This report addresses accounting queries related to Pewter Ltd, a frozen and canned fishery product company, focusing on goodwill and expense accounting. It discusses the treatment of brand image as an intangible asset under AASB 138 and the accounting for expenses or contingent liabilities under AASB 137, particularly concerning activities related to environmental responsibility. The report details how expenses incurred to enhance brand value and goodwill can be capitalized as intangible assets if they provide economic benefits over time. It also explains the proper accounting treatment for contingent liabilities, emphasizing the importance of cost-benefit analysis and transparent financial reporting. An example is provided to illustrate how expenses can be capitalized and amortized based on the net present value of future benefits. The report concludes by stressing the need for periodic impairment reviews of intangible assets and adherence to financial accounting standards to ensure accurate and reliable financial reporting. Desklib provides access to similar solved assignments and study tools for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.