University Financial Accounting Assignment: Tax and Reporting Analysis

VerifiedAdded on 2020/05/28

|16

|3325

|87

Homework Assignment

AI Summary

This financial accounting assignment solution addresses various aspects of financial reporting and taxation. Part A focuses on calculating current tax liability, including adjustments for disallowed expenses and tax depreciation, along with the related journal entries. Part B delves into the concept of materiality in accounting, explaining its significance in financial reporting and within the International Integrated Reporting Framework. It also discusses the implications of materiality on financial statements and the importance of disclosing relevant information to investors. Furthermore, the solution examines the statement of cash flows, highlighting issues related to its preparation and the amendments made to IAS 7 to improve the clarity and information provided to financial statement users. The assignment covers detailed calculations, journal entries, and discussions on key accounting principles and standards, including IFRS.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the university:

Authors Note:

Financial Accounting

Name of the Student:

Name of the university:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ACCOUNTING

Table of Contents

Part A.........................................................................................................................................2

Answer to question i...................................................................................................................2

Answer to question ii.................................................................................................................3

Answer to question iii................................................................................................................4

Answer to question iv.................................................................................................................4

Answer to question v..................................................................................................................5

Part B..........................................................................................................................................5

Answer to Question 1.................................................................................................................5

Answer to Question a.............................................................................................................5

Answer to Question b.............................................................................................................6

Answer to Question c.............................................................................................................7

Answer to Question 2.................................................................................................................8

Answer to question a..............................................................................................................8

Answer to Question b...........................................................................................................11

Reference..................................................................................................................................13

Table of Contents

Part A.........................................................................................................................................2

Answer to question i...................................................................................................................2

Answer to question ii.................................................................................................................3

Answer to question iii................................................................................................................4

Answer to question iv.................................................................................................................4

Answer to question v..................................................................................................................5

Part B..........................................................................................................................................5

Answer to Question 1.................................................................................................................5

Answer to Question a.............................................................................................................5

Answer to Question b.............................................................................................................6

Answer to Question c.............................................................................................................7

Answer to Question 2.................................................................................................................8

Answer to question a..............................................................................................................8

Answer to Question b...........................................................................................................11

Reference..................................................................................................................................13

2FINANCIAL ACCOUNTING

Part A

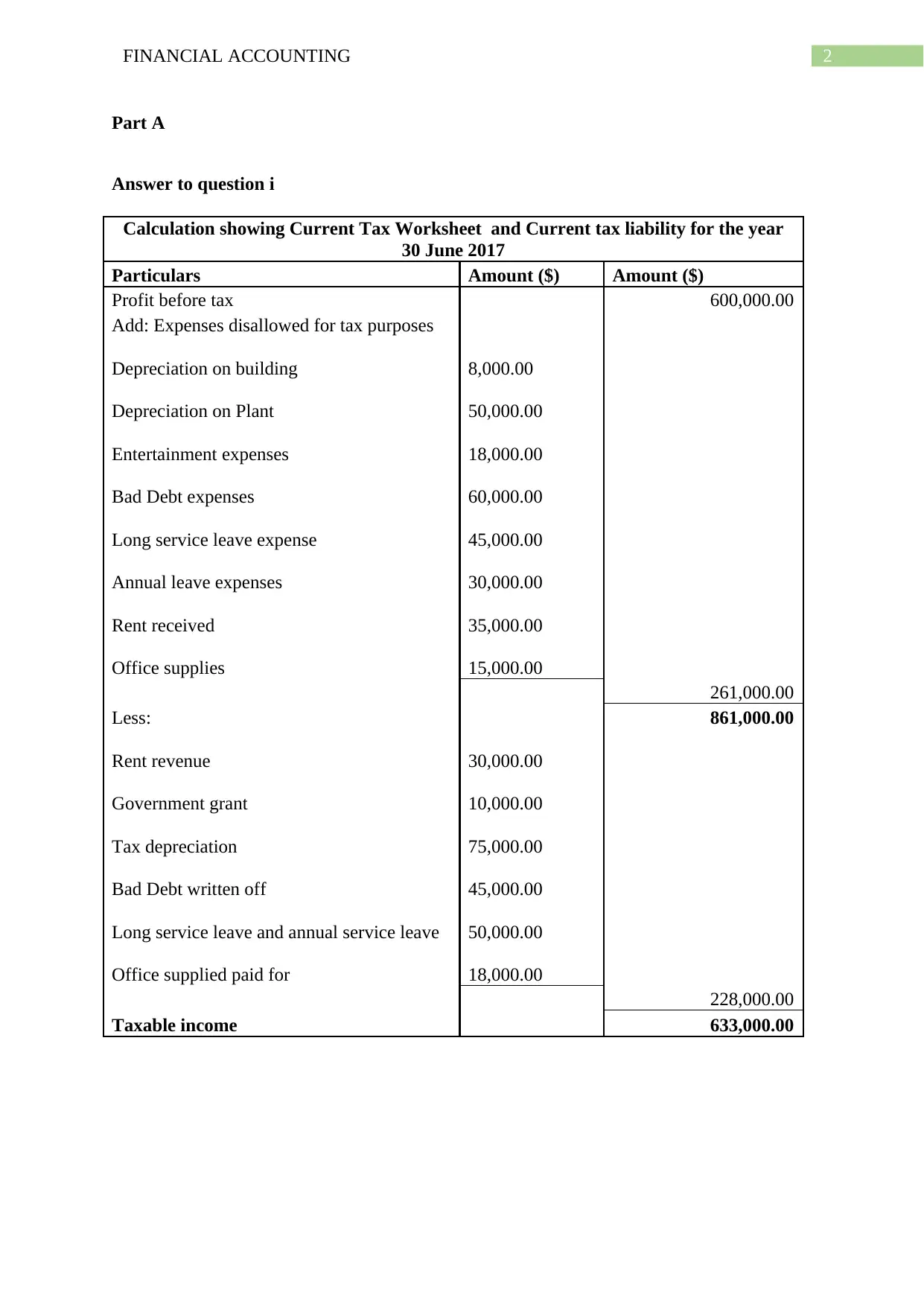

Answer to question i

Calculation showing Current Tax Worksheet and Current tax liability for the year

30 June 2017

Particulars Amount ($) Amount ($)

Profit before tax 600,000.00

Add: Expenses disallowed for tax purposes

Depreciation on building 8,000.00

Depreciation on Plant 50,000.00

Entertainment expenses 18,000.00

Bad Debt expenses 60,000.00

Long service leave expense 45,000.00

Annual leave expenses 30,000.00

Rent received 35,000.00

Office supplies 15,000.00

261,000.00

Less: 861,000.00

Rent revenue 30,000.00

Government grant 10,000.00

Tax depreciation 75,000.00

Bad Debt written off 45,000.00

Long service leave and annual service leave 50,000.00

Office supplied paid for 18,000.00

228,000.00

Taxable income 633,000.00

Part A

Answer to question i

Calculation showing Current Tax Worksheet and Current tax liability for the year

30 June 2017

Particulars Amount ($) Amount ($)

Profit before tax 600,000.00

Add: Expenses disallowed for tax purposes

Depreciation on building 8,000.00

Depreciation on Plant 50,000.00

Entertainment expenses 18,000.00

Bad Debt expenses 60,000.00

Long service leave expense 45,000.00

Annual leave expenses 30,000.00

Rent received 35,000.00

Office supplies 15,000.00

261,000.00

Less: 861,000.00

Rent revenue 30,000.00

Government grant 10,000.00

Tax depreciation 75,000.00

Bad Debt written off 45,000.00

Long service leave and annual service leave 50,000.00

Office supplied paid for 18,000.00

228,000.00

Taxable income 633,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ACCOUNTING

Current tax liability

Particulars Amount ($)

Taxable income 633,000.00

Tax Rate 30%

Current tax liability @30% 189,900.00

Working calculations:

Allowance for Doubtful debt

Particulars Amount Particulars Amount

Account Receivable $45,000.00 Opening balance $40,000.00

Closing balance $55,000.00 Expenses $60,000.00

Total $100,000.00 Total $100,000.00

Rent Received in Advance

Particulars Amount Particulars Amount

Revenue $30,000.00 Opening balance $20,000.00

Closing balance $25,000.00 Cash $35,000.00

Total $55,000.00 Total $55,000.00

Provision for Employee benefit

Particulars Amount Particulars Amount

Cash $50,000.00 Opening balance $75,000.00

LSL Expenses $45,000.00

Closing balance $100,000.00 A/L Expenses $30,000.00

Total $150,000.00 Total $150,000.00

Answer to question ii

Journal entry

Particulars Debit ($) Credit ($)

Income Tax expenses 189,900.00

Current tax Liability 189,900.00

(Being the current tax liability recorded)

Current tax liability

Particulars Amount ($)

Taxable income 633,000.00

Tax Rate 30%

Current tax liability @30% 189,900.00

Working calculations:

Allowance for Doubtful debt

Particulars Amount Particulars Amount

Account Receivable $45,000.00 Opening balance $40,000.00

Closing balance $55,000.00 Expenses $60,000.00

Total $100,000.00 Total $100,000.00

Rent Received in Advance

Particulars Amount Particulars Amount

Revenue $30,000.00 Opening balance $20,000.00

Closing balance $25,000.00 Cash $35,000.00

Total $55,000.00 Total $55,000.00

Provision for Employee benefit

Particulars Amount Particulars Amount

Cash $50,000.00 Opening balance $75,000.00

LSL Expenses $45,000.00

Closing balance $100,000.00 A/L Expenses $30,000.00

Total $150,000.00 Total $150,000.00

Answer to question ii

Journal entry

Particulars Debit ($) Credit ($)

Income Tax expenses 189,900.00

Current tax Liability 189,900.00

(Being the current tax liability recorded)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ACCOUNTING

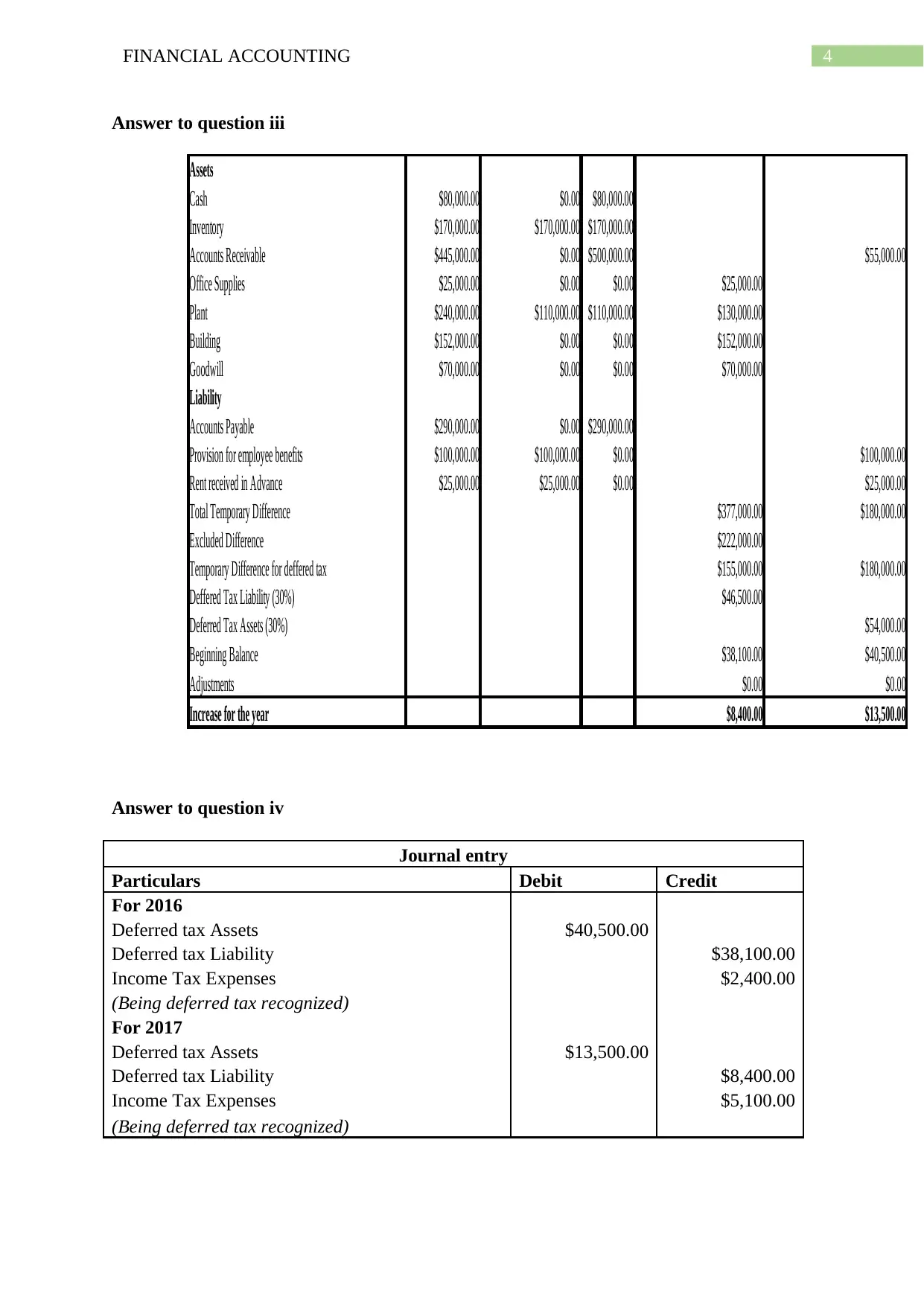

Answer to question iii

Assets

Cash $80,000.00 $0.00 $80,000.00

Inventory $170,000.00 $170,000.00 $170,000.00

Accounts Receivable $445,000.00 $0.00 $500,000.00 $55,000.00

Office Supplies $25,000.00 $0.00 $0.00 $25,000.00

Plant $240,000.00 $110,000.00 $110,000.00 $130,000.00

Building $152,000.00 $0.00 $0.00 $152,000.00

Goodwill $70,000.00 $0.00 $0.00 $70,000.00

Liability

Accounts Payable $290,000.00 $0.00 $290,000.00

Provision for employee benefits $100,000.00 $100,000.00 $0.00 $100,000.00

Rent received in Advance $25,000.00 $25,000.00 $0.00 $25,000.00

Total Temporary Difference $377,000.00 $180,000.00

Excluded Difference $222,000.00

Temporary Difference for deffered tax $155,000.00 $180,000.00

Deffered Tax Liability (30%) $46,500.00

Deferred Tax Assets (30%) $54,000.00

Beginning Balance $38,100.00 $40,500.00

Adjustments $0.00 $0.00

Increase for the year $8,400.00 $13,500.00

Answer to question iv

Journal entry

Particulars Debit Credit

For 2016

Deferred tax Assets $40,500.00

Deferred tax Liability $38,100.00

Income Tax Expenses $2,400.00

(Being deferred tax recognized)

For 2017

Deferred tax Assets $13,500.00

Deferred tax Liability $8,400.00

Income Tax Expenses $5,100.00

(Being deferred tax recognized)

Answer to question iii

Assets

Cash $80,000.00 $0.00 $80,000.00

Inventory $170,000.00 $170,000.00 $170,000.00

Accounts Receivable $445,000.00 $0.00 $500,000.00 $55,000.00

Office Supplies $25,000.00 $0.00 $0.00 $25,000.00

Plant $240,000.00 $110,000.00 $110,000.00 $130,000.00

Building $152,000.00 $0.00 $0.00 $152,000.00

Goodwill $70,000.00 $0.00 $0.00 $70,000.00

Liability

Accounts Payable $290,000.00 $0.00 $290,000.00

Provision for employee benefits $100,000.00 $100,000.00 $0.00 $100,000.00

Rent received in Advance $25,000.00 $25,000.00 $0.00 $25,000.00

Total Temporary Difference $377,000.00 $180,000.00

Excluded Difference $222,000.00

Temporary Difference for deffered tax $155,000.00 $180,000.00

Deffered Tax Liability (30%) $46,500.00

Deferred Tax Assets (30%) $54,000.00

Beginning Balance $38,100.00 $40,500.00

Adjustments $0.00 $0.00

Increase for the year $8,400.00 $13,500.00

Answer to question iv

Journal entry

Particulars Debit Credit

For 2016

Deferred tax Assets $40,500.00

Deferred tax Liability $38,100.00

Income Tax Expenses $2,400.00

(Being deferred tax recognized)

For 2017

Deferred tax Assets $13,500.00

Deferred tax Liability $8,400.00

Income Tax Expenses $5,100.00

(Being deferred tax recognized)

5FINANCIAL ACCOUNTING

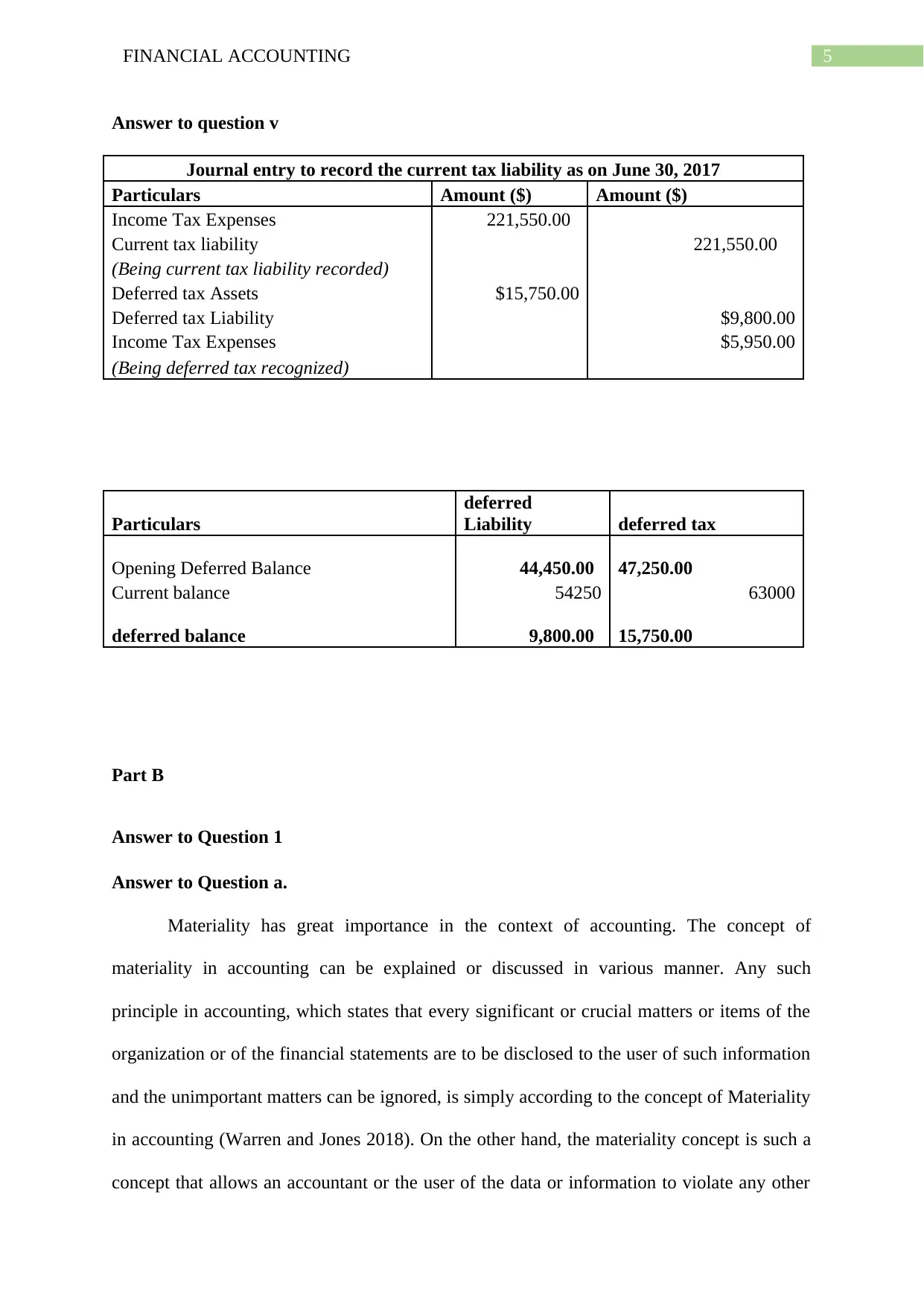

Answer to question v

Journal entry to record the current tax liability as on June 30, 2017

Particulars Amount ($) Amount ($)

Income Tax Expenses 221,550.00

Current tax liability 221,550.00

(Being current tax liability recorded)

Deferred tax Assets $15,750.00

Deferred tax Liability $9,800.00

Income Tax Expenses $5,950.00

(Being deferred tax recognized)

Particulars

deferred

Liability deferred tax

Opening Deferred Balance 44,450.00 47,250.00

Current balance 54250 63000

deferred balance 9,800.00 15,750.00

Part B

Answer to Question 1

Answer to Question a.

Materiality has great importance in the context of accounting. The concept of

materiality in accounting can be explained or discussed in various manner. Any such

principle in accounting, which states that every significant or crucial matters or items of the

organization or of the financial statements are to be disclosed to the user of such information

and the unimportant matters can be ignored, is simply according to the concept of Materiality

in accounting (Warren and Jones 2018). On the other hand, the materiality concept is such a

concept that allows an accountant or the user of the data or information to violate any other

Answer to question v

Journal entry to record the current tax liability as on June 30, 2017

Particulars Amount ($) Amount ($)

Income Tax Expenses 221,550.00

Current tax liability 221,550.00

(Being current tax liability recorded)

Deferred tax Assets $15,750.00

Deferred tax Liability $9,800.00

Income Tax Expenses $5,950.00

(Being deferred tax recognized)

Particulars

deferred

Liability deferred tax

Opening Deferred Balance 44,450.00 47,250.00

Current balance 54250 63000

deferred balance 9,800.00 15,750.00

Part B

Answer to Question 1

Answer to Question a.

Materiality has great importance in the context of accounting. The concept of

materiality in accounting can be explained or discussed in various manner. Any such

principle in accounting, which states that every significant or crucial matters or items of the

organization or of the financial statements are to be disclosed to the user of such information

and the unimportant matters can be ignored, is simply according to the concept of Materiality

in accounting (Warren and Jones 2018). On the other hand, the materiality concept is such a

concept that allows an accountant or the user of the data or information to violate any other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ACCOUNTING

principle of accounting under such circumstances where the amount is so minor that it will

not mislead the reader of the financial report. Thus from the above definition or description of

Materiality it is quite clear that the errors in materiality can always mislead the investors or

decision makers. According to the US GAAP, such items can be considered as material if it

has the potential to influence the decision of the user that is related to his economic condition

or situation (Bushman 2014). The materiality concept varies from firms to firm or from one

company or organization to another. An amount or item of $100 may not be material for a

firm or company that have a very high turnover or which operates in large scale. However, at

the same time this figure of $100 may be of material importance to such firm which have

very small turnover or which operates in small scale and makes minor profits.

After analysing the concept of materiality, it can be observed that there is no distinct

definition or perfect meaning of materiality is given. As it is seen in the above analysis, that

materiality differs from one firm to another depending upon its revenue and scale of

operation. Moreover, it is not properly mentioned under the materiality concept that

specifically which financial or accounting information are to be regarded as material

(Henderson et al. 2015). Due to this reason various financial information, which holds

immense importance, are not disclosed in the statement of financial position. Thus, it is said

that this concept of materiality is reducing the clarity and understanding of financial

statements as very often the users of these statements are deprived of certain material

information to which they are entitled.

Answer to Question b.

The concept of materiality has a very crucial role to play when it comes to the

International Integrated Reporting Framework. Through the concept of materiality, the

determination of matters that are to be included in the IR and hence ensuring conciseness can

principle of accounting under such circumstances where the amount is so minor that it will

not mislead the reader of the financial report. Thus from the above definition or description of

Materiality it is quite clear that the errors in materiality can always mislead the investors or

decision makers. According to the US GAAP, such items can be considered as material if it

has the potential to influence the decision of the user that is related to his economic condition

or situation (Bushman 2014). The materiality concept varies from firms to firm or from one

company or organization to another. An amount or item of $100 may not be material for a

firm or company that have a very high turnover or which operates in large scale. However, at

the same time this figure of $100 may be of material importance to such firm which have

very small turnover or which operates in small scale and makes minor profits.

After analysing the concept of materiality, it can be observed that there is no distinct

definition or perfect meaning of materiality is given. As it is seen in the above analysis, that

materiality differs from one firm to another depending upon its revenue and scale of

operation. Moreover, it is not properly mentioned under the materiality concept that

specifically which financial or accounting information are to be regarded as material

(Henderson et al. 2015). Due to this reason various financial information, which holds

immense importance, are not disclosed in the statement of financial position. Thus, it is said

that this concept of materiality is reducing the clarity and understanding of financial

statements as very often the users of these statements are deprived of certain material

information to which they are entitled.

Answer to Question b.

The concept of materiality has a very crucial role to play when it comes to the

International Integrated Reporting Framework. Through the concept of materiality, the

determination of matters that are to be included in the IR and hence ensuring conciseness can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING

be achieved. The matters or elements where materiality is extremely essential includes the

following:

Through materiality:

Identifications of important matters that are required to be included in the Integrated

Report can be considered. This includes drivers for the values, issues of several stake

or shareholders, internal and external factors, ability of the organization to create

values and company’s present performances (Pratt 2016).

The importance and essentiality of the matters can also be assessed which are based

on the effect’s magnitude and probability of event.

Materiality is also known for prioritising matter that are material according to their

importance and effectiveness.

Materiality also emphasises to disclose several information that are useful for the

investors or other users of financial statements. These includes, the process of

materiality, staffs who are indulges in such process, the governance body, definition

and discussion regarding matters that are material, the performance and goals of the

business or company, uncertainties and control levels over matters that are material

and suggestions for the company (Beatty and Liao 2014).

Answer to Question c.

Initially, in the year 1992, the International Accounting Standard Committee introduced

or issued the IAS 7 – Statement of Cash Flows replacing the IAS 7 – Statement of Changes in

Financial Position. Since then, the statement was amended several times. There are various

issues which are faced by the managers or management regarding the in preparing the cash

flows statement (Macve 2015). Among them, manipulation of information in the cash flow

statement is one of the most serious issue faced by every organization or management. In this

be achieved. The matters or elements where materiality is extremely essential includes the

following:

Through materiality:

Identifications of important matters that are required to be included in the Integrated

Report can be considered. This includes drivers for the values, issues of several stake

or shareholders, internal and external factors, ability of the organization to create

values and company’s present performances (Pratt 2016).

The importance and essentiality of the matters can also be assessed which are based

on the effect’s magnitude and probability of event.

Materiality is also known for prioritising matter that are material according to their

importance and effectiveness.

Materiality also emphasises to disclose several information that are useful for the

investors or other users of financial statements. These includes, the process of

materiality, staffs who are indulges in such process, the governance body, definition

and discussion regarding matters that are material, the performance and goals of the

business or company, uncertainties and control levels over matters that are material

and suggestions for the company (Beatty and Liao 2014).

Answer to Question c.

Initially, in the year 1992, the International Accounting Standard Committee introduced

or issued the IAS 7 – Statement of Cash Flows replacing the IAS 7 – Statement of Changes in

Financial Position. Since then, the statement was amended several times. There are various

issues which are faced by the managers or management regarding the in preparing the cash

flows statement (Macve 2015). Among them, manipulation of information in the cash flow

statement is one of the most serious issue faced by every organization or management. In this

8FINANCIAL ACCOUNTING

regards it can be said that in order to increase the net cash flows, the management of the

organization may opt for making payment to its suppliers lately. Moreover, in order to avoid

in payment of cash, the management may also decides to acquire good based on leasing. Thus

in order to solve out several issues associated with the IAS 7, recently an amendment has

been made to it. The main aim behind implementing changes in IAS 7 is to develop the

potential of the statement so that the user of the financial statements are offered with more

clarity and information regarding the financial status of the company. Firstly, in the

amendments it is clearly mentioned that every organizations are required to provide

disclosures that will assist the user of the financial statements or information in estimating the

difference in the amount of liability which arises out of its financing activities (Chan et al.

2016). Therefore, for the organization to achieve this objective, the IASB must ensure the

following amendments are to be carried out with respect to the liabilities that rises from the

company’s financial activities:

Changes that rises out from obtaining or losing control of other or subsidiary

businesses.

Changes arising from financial cash flows

The impact which are created by the changing rates of foreign exchanges

Changes for values and other changes.

It is also stated in the amendment that by offering a reconciliation between the closing

and the opening balances for those of the liabilities that arises out from financial activities in

the financial statement the requirements of the new disclosures can be fulfilled.

Apart from this, it is also considered as a major disclosure that every company must

mandatorily separate the changes in liabilities arising out from financing activities from that

of the changes that takes place in other liabilities and assets of the company.

regards it can be said that in order to increase the net cash flows, the management of the

organization may opt for making payment to its suppliers lately. Moreover, in order to avoid

in payment of cash, the management may also decides to acquire good based on leasing. Thus

in order to solve out several issues associated with the IAS 7, recently an amendment has

been made to it. The main aim behind implementing changes in IAS 7 is to develop the

potential of the statement so that the user of the financial statements are offered with more

clarity and information regarding the financial status of the company. Firstly, in the

amendments it is clearly mentioned that every organizations are required to provide

disclosures that will assist the user of the financial statements or information in estimating the

difference in the amount of liability which arises out of its financing activities (Chan et al.

2016). Therefore, for the organization to achieve this objective, the IASB must ensure the

following amendments are to be carried out with respect to the liabilities that rises from the

company’s financial activities:

Changes that rises out from obtaining or losing control of other or subsidiary

businesses.

Changes arising from financial cash flows

The impact which are created by the changing rates of foreign exchanges

Changes for values and other changes.

It is also stated in the amendment that by offering a reconciliation between the closing

and the opening balances for those of the liabilities that arises out from financial activities in

the financial statement the requirements of the new disclosures can be fulfilled.

Apart from this, it is also considered as a major disclosure that every company must

mandatorily separate the changes in liabilities arising out from financing activities from that

of the changes that takes place in other liabilities and assets of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ACCOUNTING

Answer to Question 2

Answer to question a

International Financial Reporting Standards has introduced significant changes that

were not required by individual national GAAPs. These changes in the IFRS require the

companies to undertake major changes in the way of their reporting. For example, reporting

on financial instruments and shared based payment were for the first time reported in the

financial statements of the companies due to IFRS requirements or guidelines (Warren 2016).

This results in preparation of more complex financial statements under IFRS as compared to

national GAAPs. The complexity that is encountered while preparing the books of accounts

in accordance with the IFRS is due to the complex nature of rules that lay down the

guidelines for recognition and measurement of transaction and also the increased number of

disclosures required to be given. Though the purpose of IFRS is to bring uniformity and

thereby comparability among the financial statements prepared by different companies, due

to its complexity it often causes problem for the users of financial statements in

understanding them, resulting in inconsistencies in understanding the financial statements by

the users (Barth 2015).

Within the IFRS the way in which financial statements will be made and the way they

should be presented is contained IAS 1 i.e. Presentation of Financial Statements. The

standard suggests the different ways that can be used in presenting and forming the financial

statements. There are also additional information that a country’s legislation makes

compulsory to be disclosed in the financial statements. Therefore, a uniform and optimal

form and way of presentation is yet to evolve internationally. As a result, every organisation

making a transition to IFRS does it in a way that entails minimal changes to be made in the

way of reporting done previously under national GAAP. For e.g. the companies of U.K. have

adopted the practice of recording incomes and expense in a separate statement and changes in

Answer to Question 2

Answer to question a

International Financial Reporting Standards has introduced significant changes that

were not required by individual national GAAPs. These changes in the IFRS require the

companies to undertake major changes in the way of their reporting. For example, reporting

on financial instruments and shared based payment were for the first time reported in the

financial statements of the companies due to IFRS requirements or guidelines (Warren 2016).

This results in preparation of more complex financial statements under IFRS as compared to

national GAAPs. The complexity that is encountered while preparing the books of accounts

in accordance with the IFRS is due to the complex nature of rules that lay down the

guidelines for recognition and measurement of transaction and also the increased number of

disclosures required to be given. Though the purpose of IFRS is to bring uniformity and

thereby comparability among the financial statements prepared by different companies, due

to its complexity it often causes problem for the users of financial statements in

understanding them, resulting in inconsistencies in understanding the financial statements by

the users (Barth 2015).

Within the IFRS the way in which financial statements will be made and the way they

should be presented is contained IAS 1 i.e. Presentation of Financial Statements. The

standard suggests the different ways that can be used in presenting and forming the financial

statements. There are also additional information that a country’s legislation makes

compulsory to be disclosed in the financial statements. Therefore, a uniform and optimal

form and way of presentation is yet to evolve internationally. As a result, every organisation

making a transition to IFRS does it in a way that entails minimal changes to be made in the

way of reporting done previously under national GAAP. For e.g. the companies of U.K. have

adopted the practice of recording incomes and expense in a separate statement and changes in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ACCOUNTING

equity in a separate statement whereas the companies in France have adopted the practice of

making single statement of changes in equity (Lovell 2014).

There also remains the possibility of interpreting the standards in different ways by

the companies due to the absence of clarity or guidance in some of the accounting standards.

For instance there are different methods of recording of assets as prescribed by IAS 39

“Financial Instruments: Recognition and measurement” in the books of accounts i.e. their net

realisable value or fair value.

The standards prescribed in the IFRS are not based upon principles that are consistent.

There are also conceptual inconsistencies present within as well as between the standards.

Certain standards allow the makers of financial statements the use of alternative accounting

treatments and this further adds to the sources of inconsistencies among financial statements.

For e.g. IAS31 dealing with “Interests in joint venture” allows the companies controlled

jointly can record their interest using the proportionate method or equity method. (Callen

2015). The companies may opt for the accounting practice they have been employing

according to the national GAAP. Another e.g. where alternated method of accounting has

been given is IAS 16 ‘plant property and e equipment’. The companies have been given

option either to value their asset using the cost model or the revaluation model. Also there is

very limited information regarding matters related to the industry discussed in IFRS. As a

result the selection of accounting policies is greatly significantly influenced by the

judgements of the management. This has resulted in a degree of inconsistencies and

incomparability among the financial statements of the companies.

Another instance where different accounting treatment can be adopted by different

organisation is of IFRS 1 in which the IFRS allows the companies to enjoy many exemptions

from the requirements of the IFRS. The exemptions availed by the organisations can affect

equity in a separate statement whereas the companies in France have adopted the practice of

making single statement of changes in equity (Lovell 2014).

There also remains the possibility of interpreting the standards in different ways by

the companies due to the absence of clarity or guidance in some of the accounting standards.

For instance there are different methods of recording of assets as prescribed by IAS 39

“Financial Instruments: Recognition and measurement” in the books of accounts i.e. their net

realisable value or fair value.

The standards prescribed in the IFRS are not based upon principles that are consistent.

There are also conceptual inconsistencies present within as well as between the standards.

Certain standards allow the makers of financial statements the use of alternative accounting

treatments and this further adds to the sources of inconsistencies among financial statements.

For e.g. IAS31 dealing with “Interests in joint venture” allows the companies controlled

jointly can record their interest using the proportionate method or equity method. (Callen

2015). The companies may opt for the accounting practice they have been employing

according to the national GAAP. Another e.g. where alternated method of accounting has

been given is IAS 16 ‘plant property and e equipment’. The companies have been given

option either to value their asset using the cost model or the revaluation model. Also there is

very limited information regarding matters related to the industry discussed in IFRS. As a

result the selection of accounting policies is greatly significantly influenced by the

judgements of the management. This has resulted in a degree of inconsistencies and

incomparability among the financial statements of the companies.

Another instance where different accounting treatment can be adopted by different

organisation is of IFRS 1 in which the IFRS allows the companies to enjoy many exemptions

from the requirements of the IFRS. The exemptions availed by the organisations can affect

11FINANCIAL ACCOUNTING

them for years. For e.g. the companies may opt for recognising all the cumulative actuarial

losses and gains with respect to post-employment benefits but, later on decide to choose the

corridor approach. Hence the companies can opt for one time write off all its actuarial losses

thereby influencing the financial statements significantly and affecting its comparability.

Further the company after they have taken the above exemption can make use of other

comprehensive income to record their profits and losses in the period they occurred and

refrain from using the corridor approach. This leads to additional damage to the

comparability.

IAS 18 ‘Revenues’ allow recognition of revenue in alternate ways. There has been no

specific guideline laid down in the standard regarding the arrangements with multiple

deliverables. The standard only says that the transactions should be viewed in respect of their

actual substance than form. But, apart from this there are no clarifications given in the

standard. The process of identification of functional currency under IAS21 is also very

subjective. Because the functional currency of an organisation can be determined by either

the currency in which the commodity produced by the company is being sold or purchased in

the market or the currency that significantly impacts its cost of daily operations , and it is not

necessary that they would be same . This can also lead to inconsistencies.

Answer to Question b

The application of the IFRS system of reporting of financial transaction,

management’s judgement can have greater impact than that was under the national GAAP.

The IFRS uses fair value very extensively. While the management is computing or

considering issues like payments based on shares, retirement pensions, assets which are

intangible being acquired in business acquisitions and the amount by which the assets have

been impaired, the management has to use its own judgements and assumptions in selecting

valuation methods and formulating assumptions (Gumb et al. 2017). These differences in the

them for years. For e.g. the companies may opt for recognising all the cumulative actuarial

losses and gains with respect to post-employment benefits but, later on decide to choose the

corridor approach. Hence the companies can opt for one time write off all its actuarial losses

thereby influencing the financial statements significantly and affecting its comparability.

Further the company after they have taken the above exemption can make use of other

comprehensive income to record their profits and losses in the period they occurred and

refrain from using the corridor approach. This leads to additional damage to the

comparability.

IAS 18 ‘Revenues’ allow recognition of revenue in alternate ways. There has been no

specific guideline laid down in the standard regarding the arrangements with multiple

deliverables. The standard only says that the transactions should be viewed in respect of their

actual substance than form. But, apart from this there are no clarifications given in the

standard. The process of identification of functional currency under IAS21 is also very

subjective. Because the functional currency of an organisation can be determined by either

the currency in which the commodity produced by the company is being sold or purchased in

the market or the currency that significantly impacts its cost of daily operations , and it is not

necessary that they would be same . This can also lead to inconsistencies.

Answer to Question b

The application of the IFRS system of reporting of financial transaction,

management’s judgement can have greater impact than that was under the national GAAP.

The IFRS uses fair value very extensively. While the management is computing or

considering issues like payments based on shares, retirement pensions, assets which are

intangible being acquired in business acquisitions and the amount by which the assets have

been impaired, the management has to use its own judgements and assumptions in selecting

valuation methods and formulating assumptions (Gumb et al. 2017). These differences in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.