Financial Accounting Report: Principles, Conventions, Client Analysis

VerifiedAdded on 2020/10/04

|28

|5876

|90

Report

AI Summary

This report delves into the core concepts of financial accounting, emphasizing its significance in providing insights into an organization's financial performance. It explores the preparation of financial statements, including the Profit & Loss account, Balance Sheet, and Cash Flow statement, adhering to accounting principles and regulations. The report covers key aspects such as accounting rules, principles (conservatism, cost principle, going concern, monetary unit, full disclosure, matching principle, revenue recognition, materiality, time period assumption, and economic entity assumption), and accounting conventions (materiality and disclosure). It includes practical examples, such as client analyses, showcasing the application of these principles in real-world scenarios. The report also touches on the regulations associated with financial accounting, including the role of IASB. Furthermore, the report provides practical examples through the analysis of six clients' financial transactions, illustrating bookkeeping, ledger accounting, and the double-entry system. Through the analysis of these elements, the report aims to provide a comprehensive understanding of financial accounting and its practical implications.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

1: Financial accounting and its purpose......................................................................................1

2. Regulation associated with financial accounting ...................................................................2

3: Accounting rules and principles..............................................................................................3

4. The conventions and concepts relating to

consistency and material disclosure...........................................................................................5

CLIENT 1........................................................................................................................................6

CLIENT 2......................................................................................................................................14

........................................................................................................................................................16

CLIENT 3......................................................................................................................................16

CLIENT 4......................................................................................................................................18

CLIENT 5......................................................................................................................................20

CLIENT 6......................................................................................................................................22

CONCLUSION..............................................................................................................................24

REFERENCES..............................................................................................................................25

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

1: Financial accounting and its purpose......................................................................................1

2. Regulation associated with financial accounting ...................................................................2

3: Accounting rules and principles..............................................................................................3

4. The conventions and concepts relating to

consistency and material disclosure...........................................................................................5

CLIENT 1........................................................................................................................................6

CLIENT 2......................................................................................................................................14

........................................................................................................................................................16

CLIENT 3......................................................................................................................................16

CLIENT 4......................................................................................................................................18

CLIENT 5......................................................................................................................................20

CLIENT 6......................................................................................................................................22

CONCLUSION..............................................................................................................................24

REFERENCES..............................................................................................................................25

INTRODUCTION

Financial accounting is necessarily requirement of an organisation which enables them in

acquiring knowledge about its actual financial performance or position at current time period

(Zeff, 2016). It can be done through preparing financial accounts such as Profit & Loss a/c,

Balance sheet, Cash Flow statement etc. on specific time period. It is mandatory for all

organisation to prepare such financial reports. The accountants of an organisation are held liable

to follow all such principles and rules associated with preparation of financial reports so that an

accurate and reliable information can be available for the parties outside of an organisation such

as creditors, suppliers, investors etc. The present assignment report is based on the accounting

principles and its role in preparation of financial reports. The project includes brief description of

financial accounting along with its purpose. The project also describes conventions and concepts

related with consistency and material disclosure. In addition, with this, Book-keeping system,

ledger accounting, double entry system etc. are explained under this report. Apart from this

financial reports which includes income & expenditure, balance sheet is also practically

evaluated following all accounting concepts and principles.

BUSINESS REPORT

1: Financial accounting and its purpose

Financial accounting: It is a method of identifying actual financial performance of an

organisation through making of various financial reports. It is mandatory for all organisation to

maintain financial accounts on timely basis as it is more useful for external parties of an

organisation such as investors, creditors, suppliers etc. to make decision regarding giving an

appropriate support in achieving growth and expansion in competitive market.

There are various accounting principle and rules are formulated which need to be comply

by an accountant while preparing financial statements of an organisation (Stice and Stice, 2013).

Therefore, if not allowed then the chances of errors or mistakes are more in financial reports due

to which it may difficult for interested parties to interpret and understand in better manner. Such

financial reports include:

Cash Flow statement: It is a statement prepare with a motive of identifying cash

generation and cash expenditure in business activities on specific time period such as monthly,

quarterly or yearly. Such statement consists of three headings which includes cash flow from

1

Financial accounting is necessarily requirement of an organisation which enables them in

acquiring knowledge about its actual financial performance or position at current time period

(Zeff, 2016). It can be done through preparing financial accounts such as Profit & Loss a/c,

Balance sheet, Cash Flow statement etc. on specific time period. It is mandatory for all

organisation to prepare such financial reports. The accountants of an organisation are held liable

to follow all such principles and rules associated with preparation of financial reports so that an

accurate and reliable information can be available for the parties outside of an organisation such

as creditors, suppliers, investors etc. The present assignment report is based on the accounting

principles and its role in preparation of financial reports. The project includes brief description of

financial accounting along with its purpose. The project also describes conventions and concepts

related with consistency and material disclosure. In addition, with this, Book-keeping system,

ledger accounting, double entry system etc. are explained under this report. Apart from this

financial reports which includes income & expenditure, balance sheet is also practically

evaluated following all accounting concepts and principles.

BUSINESS REPORT

1: Financial accounting and its purpose

Financial accounting: It is a method of identifying actual financial performance of an

organisation through making of various financial reports. It is mandatory for all organisation to

maintain financial accounts on timely basis as it is more useful for external parties of an

organisation such as investors, creditors, suppliers etc. to make decision regarding giving an

appropriate support in achieving growth and expansion in competitive market.

There are various accounting principle and rules are formulated which need to be comply

by an accountant while preparing financial statements of an organisation (Stice and Stice, 2013).

Therefore, if not allowed then the chances of errors or mistakes are more in financial reports due

to which it may difficult for interested parties to interpret and understand in better manner. Such

financial reports include:

Cash Flow statement: It is a statement prepare with a motive of identifying cash

generation and cash expenditure in business activities on specific time period such as monthly,

quarterly or yearly. Such statement consists of three headings which includes cash flow from

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operations, investment and finance. It includes all those transactions which are transacted in

monetary terms.

Income and expenditure account: It is a statement also called as profit and loss a/c

showing all details related with income earned and expenditure incurred in business operations.

It is prepared to ascertain surplus or deficit of income over expenditures for a specific time

period. It is prepared on accrual basis which means all incomes and expenses incurred during an

accounting year whether it has been actually paid and received or not are taken into

consideration (Skogstad and et. al., 2011).

Financial position statement: It has another name called as Balance sheet which shows

the exact financial position of company towards the external parties of an organisation. It is

similar to the basic accounting equation such as Assets= Liabilities + Net assets. Such statement

reflects the basic accounting principles and guidelines which includes cost, matching, and full

disclosure principle. It plays an important role in finding out the investors in market through

representing their actual financial position with their assets and liabilities in figures.

Change in equity statement: Such statement is a reconciliation of the beginning and

ending balances associated with company equity capital during a reporting period. It is more

useful in finding out the fluctuations in equity and share capital of company. As it is not

considered as essential part of monthly financial statement thus it is most likely of all the

financial statements not to be issued (Scott, 2015). The calculation structure of the statement is

under as given:

Beginning equity + Net income – Dividends +/- Other changes

2. Regulation associated with financial accounting

Rules and regulation are very important to follow in every business organisation. So each

accountant is bounded to follow necessary regulation that are made by concern agencies of board

to record every single transaction in correct manner.

IASB- The international accounting standard board is an independent, private sector

body that is develop for the purpose of controlling and management for recording

necessary records. The IABS framework have been approved by the IASC Board in April

1989. Basic purpose of this body is to provide proper guidance and knowledge for

development of new and effective standard that can be further applied in preparing

financial statement.

2

monetary terms.

Income and expenditure account: It is a statement also called as profit and loss a/c

showing all details related with income earned and expenditure incurred in business operations.

It is prepared to ascertain surplus or deficit of income over expenditures for a specific time

period. It is prepared on accrual basis which means all incomes and expenses incurred during an

accounting year whether it has been actually paid and received or not are taken into

consideration (Skogstad and et. al., 2011).

Financial position statement: It has another name called as Balance sheet which shows

the exact financial position of company towards the external parties of an organisation. It is

similar to the basic accounting equation such as Assets= Liabilities + Net assets. Such statement

reflects the basic accounting principles and guidelines which includes cost, matching, and full

disclosure principle. It plays an important role in finding out the investors in market through

representing their actual financial position with their assets and liabilities in figures.

Change in equity statement: Such statement is a reconciliation of the beginning and

ending balances associated with company equity capital during a reporting period. It is more

useful in finding out the fluctuations in equity and share capital of company. As it is not

considered as essential part of monthly financial statement thus it is most likely of all the

financial statements not to be issued (Scott, 2015). The calculation structure of the statement is

under as given:

Beginning equity + Net income – Dividends +/- Other changes

2. Regulation associated with financial accounting

Rules and regulation are very important to follow in every business organisation. So each

accountant is bounded to follow necessary regulation that are made by concern agencies of board

to record every single transaction in correct manner.

IASB- The international accounting standard board is an independent, private sector

body that is develop for the purpose of controlling and management for recording

necessary records. The IABS framework have been approved by the IASC Board in April

1989. Basic purpose of this body is to provide proper guidance and knowledge for

development of new and effective standard that can be further applied in preparing

financial statement.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Some of the basic conceptual framework of IASB are such as:

helps board in developing future international financial reporting standard and review

report.

Helps board of directors in establishing the concepts of regulation, accounting standard,

procedure and method related to the formation of financial statements

helps the national committee in formation of national standard

helps the auditor to give their opinion on the statements whether IFRS standard have

complied while preparing statement.

Help the creditor, investor employee etc. of the statement

3: Accounting rules and principles

Accounting rules: It is such a guidelines formulated by different international bodies

such as FASB and IASB in order to maintain accounting practices in more consistent way that

will bring easiness for interested parties to an organisation to understand in more effective

manner (Simnett and et. al., 2011). It directs an accountant to record all business transactions in

financial reports following all prescribed rules and regulations so that it brings meaningful

information towards external as well as internal parties. Such accounting rules are given as

under:

Debit the receiver, credit the giver: It is the rule which states that when an individual

receives or collects resources called as debtor will be recorded as debit transaction whereas an

individual pays or give something called as creditor will be recorded as credit transaction. This

rule is taken personal accounts into consideration (Oulasvirta, 2014).

Debit all expenses and losses, credit all income and gains: It is the rule which states that

all expenses and losses of company are debiting the transactions in financial statements whereas

income earned and gains by company are required to credit the transaction. In this rule, nominal

account is taken into consideration.

Debit what comes in, credit what goes out: This is the rule which states that if company

acquire any assets then such transaction will be recorded as debit whereas selling or transferring

of assets will be recorded as credit under the financial statements. In this rule, real accounts are

taken into consideration.

3

helps board in developing future international financial reporting standard and review

report.

Helps board of directors in establishing the concepts of regulation, accounting standard,

procedure and method related to the formation of financial statements

helps the national committee in formation of national standard

helps the auditor to give their opinion on the statements whether IFRS standard have

complied while preparing statement.

Help the creditor, investor employee etc. of the statement

3: Accounting rules and principles

Accounting rules: It is such a guidelines formulated by different international bodies

such as FASB and IASB in order to maintain accounting practices in more consistent way that

will bring easiness for interested parties to an organisation to understand in more effective

manner (Simnett and et. al., 2011). It directs an accountant to record all business transactions in

financial reports following all prescribed rules and regulations so that it brings meaningful

information towards external as well as internal parties. Such accounting rules are given as

under:

Debit the receiver, credit the giver: It is the rule which states that when an individual

receives or collects resources called as debtor will be recorded as debit transaction whereas an

individual pays or give something called as creditor will be recorded as credit transaction. This

rule is taken personal accounts into consideration (Oulasvirta, 2014).

Debit all expenses and losses, credit all income and gains: It is the rule which states that

all expenses and losses of company are debiting the transactions in financial statements whereas

income earned and gains by company are required to credit the transaction. In this rule, nominal

account is taken into consideration.

Debit what comes in, credit what goes out: This is the rule which states that if company

acquire any assets then such transaction will be recorded as debit whereas selling or transferring

of assets will be recorded as credit under the financial statements. In this rule, real accounts are

taken into consideration.

3

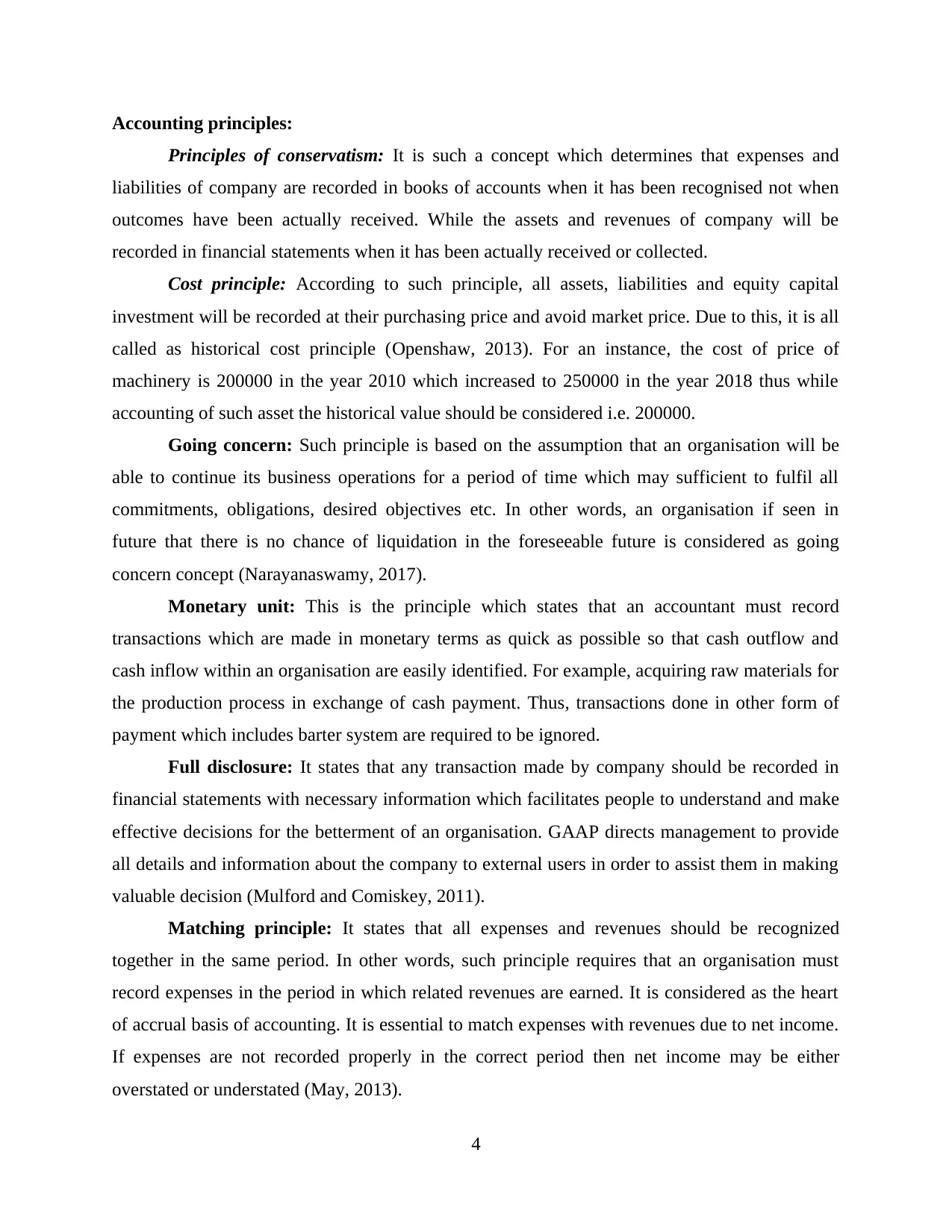

Accounting principles:

Principles of conservatism: It is such a concept which determines that expenses and

liabilities of company are recorded in books of accounts when it has been recognised not when

outcomes have been actually received. While the assets and revenues of company will be

recorded in financial statements when it has been actually received or collected.

Cost principle: According to such principle, all assets, liabilities and equity capital

investment will be recorded at their purchasing price and avoid market price. Due to this, it is all

called as historical cost principle (Openshaw, 2013). For an instance, the cost of price of

machinery is 200000 in the year 2010 which increased to 250000 in the year 2018 thus while

accounting of such asset the historical value should be considered i.e. 200000.

Going concern: Such principle is based on the assumption that an organisation will be

able to continue its business operations for a period of time which may sufficient to fulfil all

commitments, obligations, desired objectives etc. In other words, an organisation if seen in

future that there is no chance of liquidation in the foreseeable future is considered as going

concern concept (Narayanaswamy, 2017).

Monetary unit: This is the principle which states that an accountant must record

transactions which are made in monetary terms as quick as possible so that cash outflow and

cash inflow within an organisation are easily identified. For example, acquiring raw materials for

the production process in exchange of cash payment. Thus, transactions done in other form of

payment which includes barter system are required to be ignored.

Full disclosure: It states that any transaction made by company should be recorded in

financial statements with necessary information which facilitates people to understand and make

effective decisions for the betterment of an organisation. GAAP directs management to provide

all details and information about the company to external users in order to assist them in making

valuable decision (Mulford and Comiskey, 2011).

Matching principle: It states that all expenses and revenues should be recognized

together in the same period. In other words, such principle requires that an organisation must

record expenses in the period in which related revenues are earned. It is considered as the heart

of accrual basis of accounting. It is essential to match expenses with revenues due to net income.

If expenses are not recorded properly in the correct period then net income may be either

overstated or understated (May, 2013).

4

Principles of conservatism: It is such a concept which determines that expenses and

liabilities of company are recorded in books of accounts when it has been recognised not when

outcomes have been actually received. While the assets and revenues of company will be

recorded in financial statements when it has been actually received or collected.

Cost principle: According to such principle, all assets, liabilities and equity capital

investment will be recorded at their purchasing price and avoid market price. Due to this, it is all

called as historical cost principle (Openshaw, 2013). For an instance, the cost of price of

machinery is 200000 in the year 2010 which increased to 250000 in the year 2018 thus while

accounting of such asset the historical value should be considered i.e. 200000.

Going concern: Such principle is based on the assumption that an organisation will be

able to continue its business operations for a period of time which may sufficient to fulfil all

commitments, obligations, desired objectives etc. In other words, an organisation if seen in

future that there is no chance of liquidation in the foreseeable future is considered as going

concern concept (Narayanaswamy, 2017).

Monetary unit: This is the principle which states that an accountant must record

transactions which are made in monetary terms as quick as possible so that cash outflow and

cash inflow within an organisation are easily identified. For example, acquiring raw materials for

the production process in exchange of cash payment. Thus, transactions done in other form of

payment which includes barter system are required to be ignored.

Full disclosure: It states that any transaction made by company should be recorded in

financial statements with necessary information which facilitates people to understand and make

effective decisions for the betterment of an organisation. GAAP directs management to provide

all details and information about the company to external users in order to assist them in making

valuable decision (Mulford and Comiskey, 2011).

Matching principle: It states that all expenses and revenues should be recognized

together in the same period. In other words, such principle requires that an organisation must

record expenses in the period in which related revenues are earned. It is considered as the heart

of accrual basis of accounting. It is essential to match expenses with revenues due to net income.

If expenses are not recorded properly in the correct period then net income may be either

overstated or understated (May, 2013).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

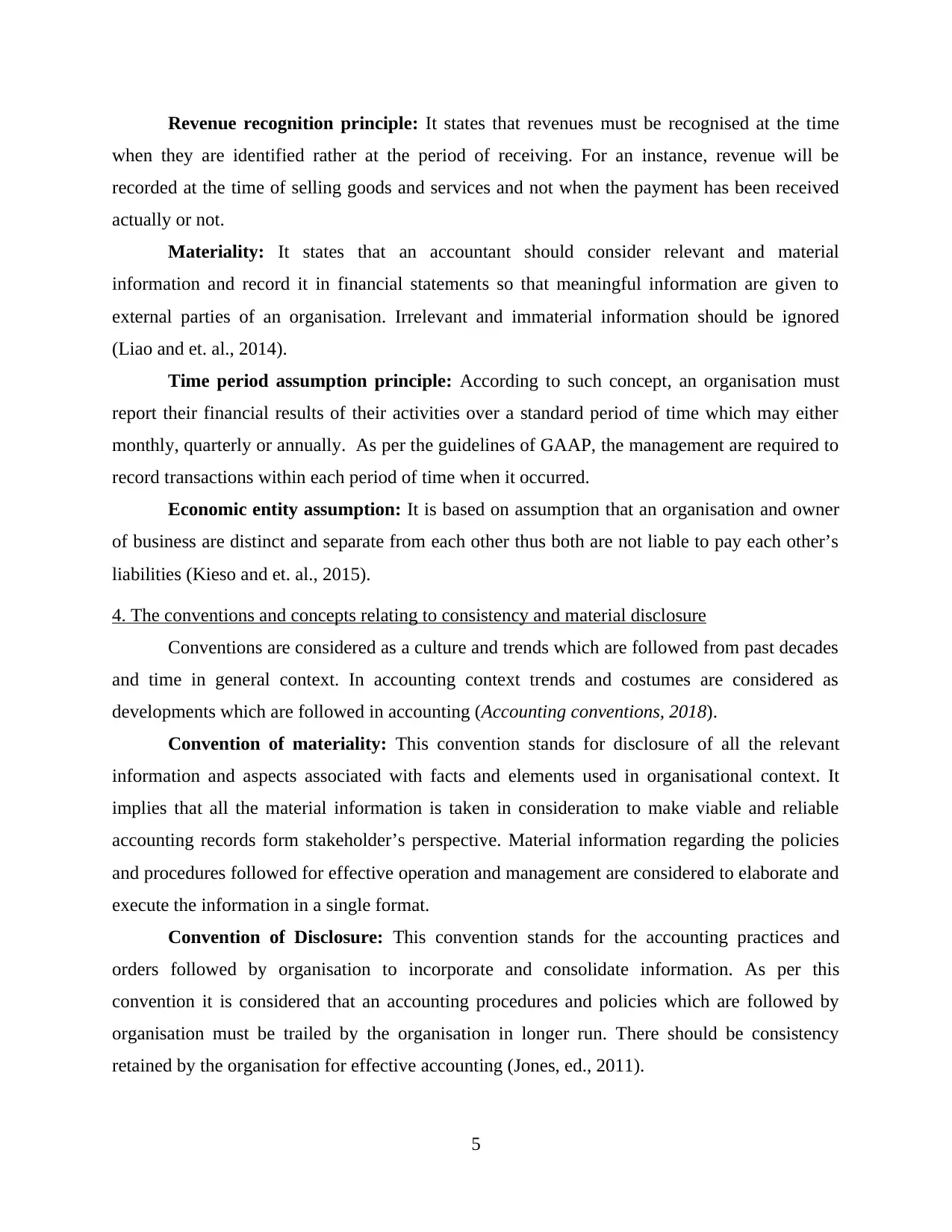

Revenue recognition principle: It states that revenues must be recognised at the time

when they are identified rather at the period of receiving. For an instance, revenue will be

recorded at the time of selling goods and services and not when the payment has been received

actually or not.

Materiality: It states that an accountant should consider relevant and material

information and record it in financial statements so that meaningful information are given to

external parties of an organisation. Irrelevant and immaterial information should be ignored

(Liao and et. al., 2014).

Time period assumption principle: According to such concept, an organisation must

report their financial results of their activities over a standard period of time which may either

monthly, quarterly or annually. As per the guidelines of GAAP, the management are required to

record transactions within each period of time when it occurred.

Economic entity assumption: It is based on assumption that an organisation and owner

of business are distinct and separate from each other thus both are not liable to pay each other’s

liabilities (Kieso and et. al., 2015).

4. The conventions and concepts relating to consistency and material disclosure

Conventions are considered as a culture and trends which are followed from past decades

and time in general context. In accounting context trends and costumes are considered as

developments which are followed in accounting (Accounting conventions, 2018).

Convention of materiality: This convention stands for disclosure of all the relevant

information and aspects associated with facts and elements used in organisational context. It

implies that all the material information is taken in consideration to make viable and reliable

accounting records form stakeholder’s perspective. Material information regarding the policies

and procedures followed for effective operation and management are considered to elaborate and

execute the information in a single format.

Convention of Disclosure: This convention stands for the accounting practices and

orders followed by organisation to incorporate and consolidate information. As per this

convention it is considered that an accounting procedures and policies which are followed by

organisation must be trailed by the organisation in longer run. There should be consistency

retained by the organisation for effective accounting (Jones, ed., 2011).

5

when they are identified rather at the period of receiving. For an instance, revenue will be

recorded at the time of selling goods and services and not when the payment has been received

actually or not.

Materiality: It states that an accountant should consider relevant and material

information and record it in financial statements so that meaningful information are given to

external parties of an organisation. Irrelevant and immaterial information should be ignored

(Liao and et. al., 2014).

Time period assumption principle: According to such concept, an organisation must

report their financial results of their activities over a standard period of time which may either

monthly, quarterly or annually. As per the guidelines of GAAP, the management are required to

record transactions within each period of time when it occurred.

Economic entity assumption: It is based on assumption that an organisation and owner

of business are distinct and separate from each other thus both are not liable to pay each other’s

liabilities (Kieso and et. al., 2015).

4. The conventions and concepts relating to consistency and material disclosure

Conventions are considered as a culture and trends which are followed from past decades

and time in general context. In accounting context trends and costumes are considered as

developments which are followed in accounting (Accounting conventions, 2018).

Convention of materiality: This convention stands for disclosure of all the relevant

information and aspects associated with facts and elements used in organisational context. It

implies that all the material information is taken in consideration to make viable and reliable

accounting records form stakeholder’s perspective. Material information regarding the policies

and procedures followed for effective operation and management are considered to elaborate and

execute the information in a single format.

Convention of Disclosure: This convention stands for the accounting practices and

orders followed by organisation to incorporate and consolidate information. As per this

convention it is considered that an accounting procedures and policies which are followed by

organisation must be trailed by the organisation in longer run. There should be consistency

retained by the organisation for effective accounting (Jones, ed., 2011).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

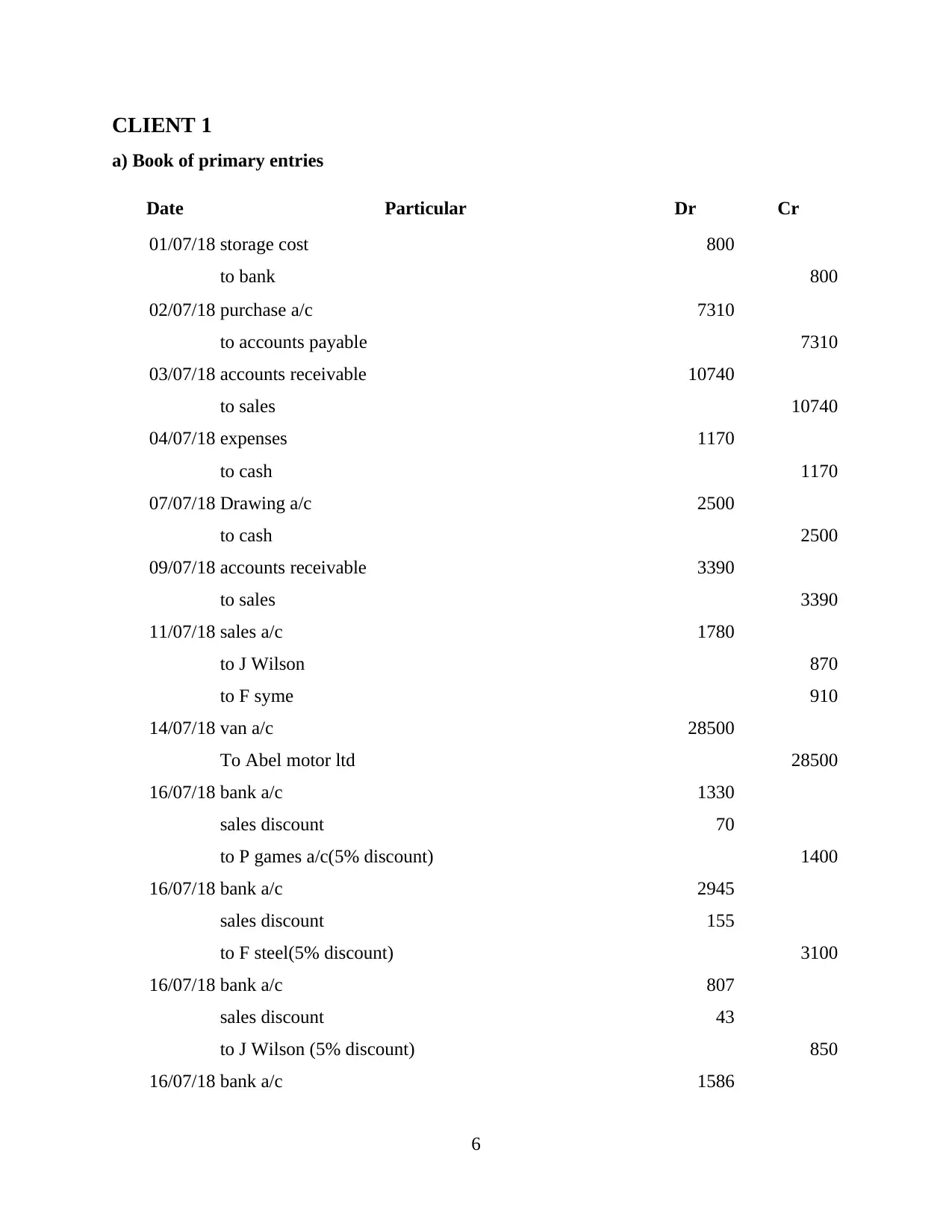

CLIENT 1

a) Book of primary entries

Date Particular Dr Cr

01/07/18 storage cost 800

to bank 800

02/07/18 purchase a/c 7310

to accounts payable 7310

03/07/18 accounts receivable 10740

to sales 10740

04/07/18 expenses 1170

to cash 1170

07/07/18 Drawing a/c 2500

to cash 2500

09/07/18 accounts receivable 3390

to sales 3390

11/07/18 sales a/c 1780

to J Wilson 870

to F syme 910

14/07/18 van a/c 28500

To Abel motor ltd 28500

16/07/18 bank a/c 1330

sales discount 70

to P games a/c(5% discount) 1400

16/07/18 bank a/c 2945

sales discount 155

to F steel(5% discount) 3100

16/07/18 bank a/c 807

sales discount 43

to J Wilson (5% discount) 850

16/07/18 bank a/c 1586

6

a) Book of primary entries

Date Particular Dr Cr

01/07/18 storage cost 800

to bank 800

02/07/18 purchase a/c 7310

to accounts payable 7310

03/07/18 accounts receivable 10740

to sales 10740

04/07/18 expenses 1170

to cash 1170

07/07/18 Drawing a/c 2500

to cash 2500

09/07/18 accounts receivable 3390

to sales 3390

11/07/18 sales a/c 1780

to J Wilson 870

to F syme 910

14/07/18 van a/c 28500

To Abel motor ltd 28500

16/07/18 bank a/c 1330

sales discount 70

to P games a/c(5% discount) 1400

16/07/18 bank a/c 2945

sales discount 155

to F steel(5% discount) 3100

16/07/18 bank a/c 807

sales discount 43

to J Wilson (5% discount) 850

16/07/18 bank a/c 1586

6

sales discount 84

to F syme (5% discount) 1670

19/07/18 R foot 500

to purchase 500

20/07/18 purchase a/c 3740

to accounts payable 3740

24/07/18 S Lyle a/c 3600

to purchase discount(10% discount rec) 360

to bank 3240

24/07/18 J brown 4600

to purchase discount(10% discount rec) 460

to bank 4140

24/07/18 R foot 1400

to purchase discount(10% discount rec) 140

to bank 1260

27/07/18 salary a/c 4800

to bank 4800

30/07/18 business rate a/c 1320

to bank 1320

31/07/18 Abel motor a/c 20500

to bank 20500

b) Ledger posting

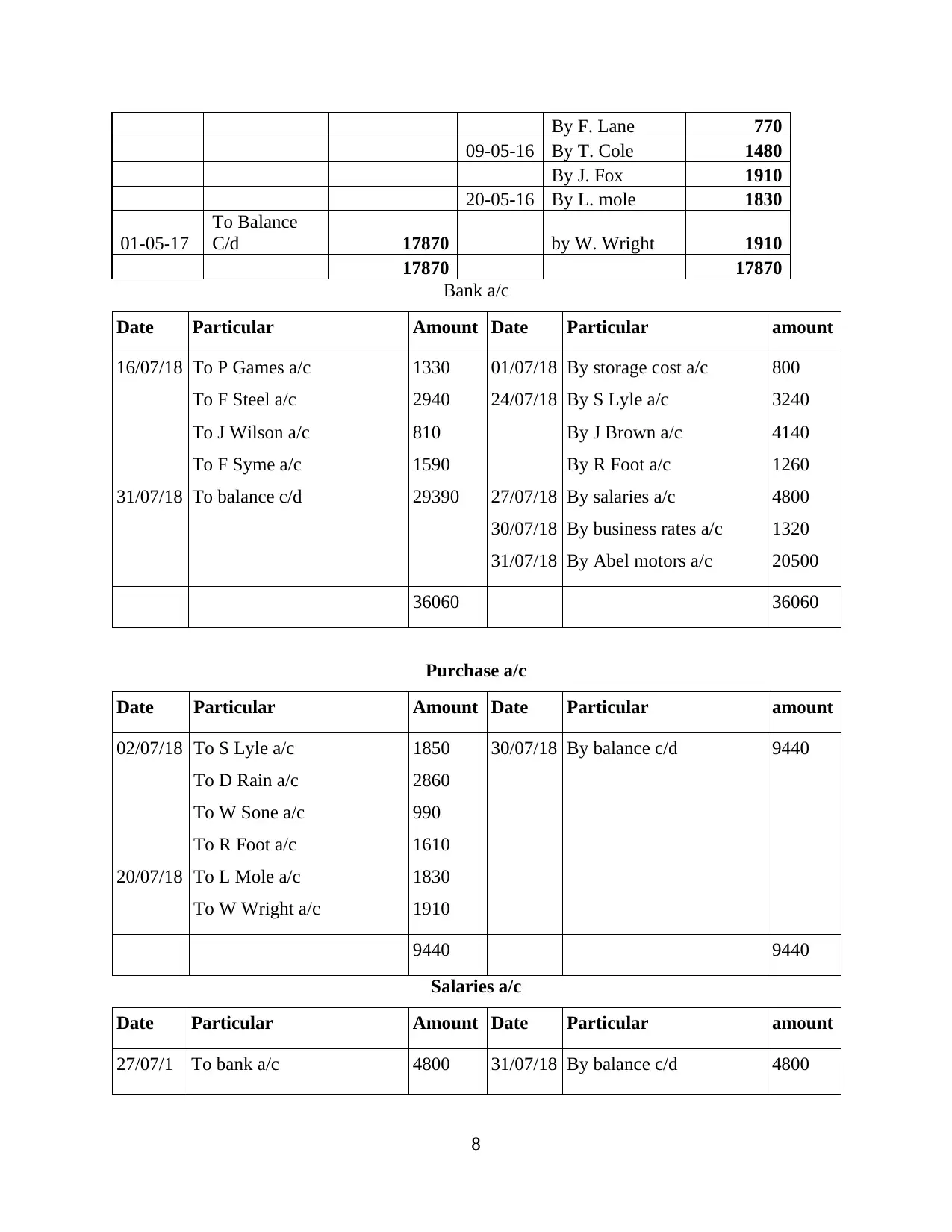

Storage cost

Date Particular Amount Date Particular Amount

01-05-16 To bank 800 01-05-17 By balance c/d 800

800 800

Sales a/c

Date Particular Amount Date Particular Amount

03-05-16 By J. Wilson 1520

By T. Cole 1940

By F. Syme 2980

By J. Allen 1110

By P. White 2420

7

to F syme (5% discount) 1670

19/07/18 R foot 500

to purchase 500

20/07/18 purchase a/c 3740

to accounts payable 3740

24/07/18 S Lyle a/c 3600

to purchase discount(10% discount rec) 360

to bank 3240

24/07/18 J brown 4600

to purchase discount(10% discount rec) 460

to bank 4140

24/07/18 R foot 1400

to purchase discount(10% discount rec) 140

to bank 1260

27/07/18 salary a/c 4800

to bank 4800

30/07/18 business rate a/c 1320

to bank 1320

31/07/18 Abel motor a/c 20500

to bank 20500

b) Ledger posting

Storage cost

Date Particular Amount Date Particular Amount

01-05-16 To bank 800 01-05-17 By balance c/d 800

800 800

Sales a/c

Date Particular Amount Date Particular Amount

03-05-16 By J. Wilson 1520

By T. Cole 1940

By F. Syme 2980

By J. Allen 1110

By P. White 2420

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By F. Lane 770

09-05-16 By T. Cole 1480

By J. Fox 1910

20-05-16 By L. mole 1830

01-05-17

To Balance

C/d 17870 by W. Wright 1910

17870 17870

Bank a/c

Date Particular Amount Date Particular amount

16/07/18

31/07/18

To P Games a/c

To F Steel a/c

To J Wilson a/c

To F Syme a/c

To balance c/d

1330

2940

810

1590

29390

01/07/18

24/07/18

27/07/18

30/07/18

31/07/18

By storage cost a/c

By S Lyle a/c

By J Brown a/c

By R Foot a/c

By salaries a/c

By business rates a/c

By Abel motors a/c

800

3240

4140

1260

4800

1320

20500

36060 36060

Purchase a/c

Date Particular Amount Date Particular amount

02/07/18

20/07/18

To S Lyle a/c

To D Rain a/c

To W Sone a/c

To R Foot a/c

To L Mole a/c

To W Wright a/c

1850

2860

990

1610

1830

1910

30/07/18 By balance c/d 9440

9440 9440

Salaries a/c

Date Particular Amount Date Particular amount

27/07/1 To bank a/c 4800 31/07/18 By balance c/d 4800

8

09-05-16 By T. Cole 1480

By J. Fox 1910

20-05-16 By L. mole 1830

01-05-17

To Balance

C/d 17870 by W. Wright 1910

17870 17870

Bank a/c

Date Particular Amount Date Particular amount

16/07/18

31/07/18

To P Games a/c

To F Steel a/c

To J Wilson a/c

To F Syme a/c

To balance c/d

1330

2940

810

1590

29390

01/07/18

24/07/18

27/07/18

30/07/18

31/07/18

By storage cost a/c

By S Lyle a/c

By J Brown a/c

By R Foot a/c

By salaries a/c

By business rates a/c

By Abel motors a/c

800

3240

4140

1260

4800

1320

20500

36060 36060

Purchase a/c

Date Particular Amount Date Particular amount

02/07/18

20/07/18

To S Lyle a/c

To D Rain a/c

To W Sone a/c

To R Foot a/c

To L Mole a/c

To W Wright a/c

1850

2860

990

1610

1830

1910

30/07/18 By balance c/d 9440

9440 9440

Salaries a/c

Date Particular Amount Date Particular amount

27/07/1 To bank a/c 4800 31/07/18 By balance c/d 4800

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

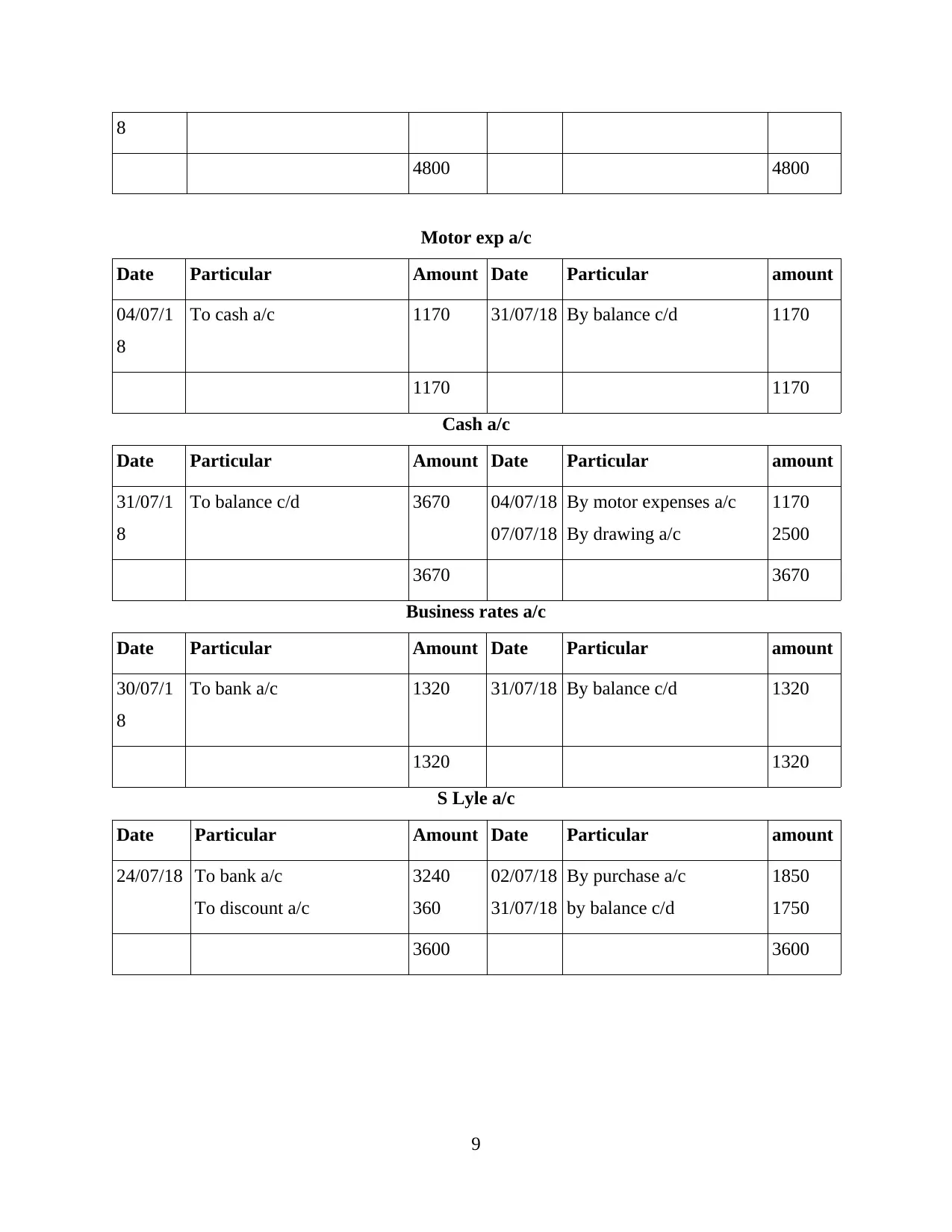

4800 4800

Motor exp a/c

Date Particular Amount Date Particular amount

04/07/1

8

To cash a/c 1170 31/07/18 By balance c/d 1170

1170 1170

Cash a/c

Date Particular Amount Date Particular amount

31/07/1

8

To balance c/d 3670 04/07/18

07/07/18

By motor expenses a/c

By drawing a/c

1170

2500

3670 3670

Business rates a/c

Date Particular Amount Date Particular amount

30/07/1

8

To bank a/c 1320 31/07/18 By balance c/d 1320

1320 1320

S Lyle a/c

Date Particular Amount Date Particular amount

24/07/18 To bank a/c

To discount a/c

3240

360

02/07/18

31/07/18

By purchase a/c

by balance c/d

1850

1750

3600 3600

9

4800 4800

Motor exp a/c

Date Particular Amount Date Particular amount

04/07/1

8

To cash a/c 1170 31/07/18 By balance c/d 1170

1170 1170

Cash a/c

Date Particular Amount Date Particular amount

31/07/1

8

To balance c/d 3670 04/07/18

07/07/18

By motor expenses a/c

By drawing a/c

1170

2500

3670 3670

Business rates a/c

Date Particular Amount Date Particular amount

30/07/1

8

To bank a/c 1320 31/07/18 By balance c/d 1320

1320 1320

S Lyle a/c

Date Particular Amount Date Particular amount

24/07/18 To bank a/c

To discount a/c

3240

360

02/07/18

31/07/18

By purchase a/c

by balance c/d

1850

1750

3600 3600

9

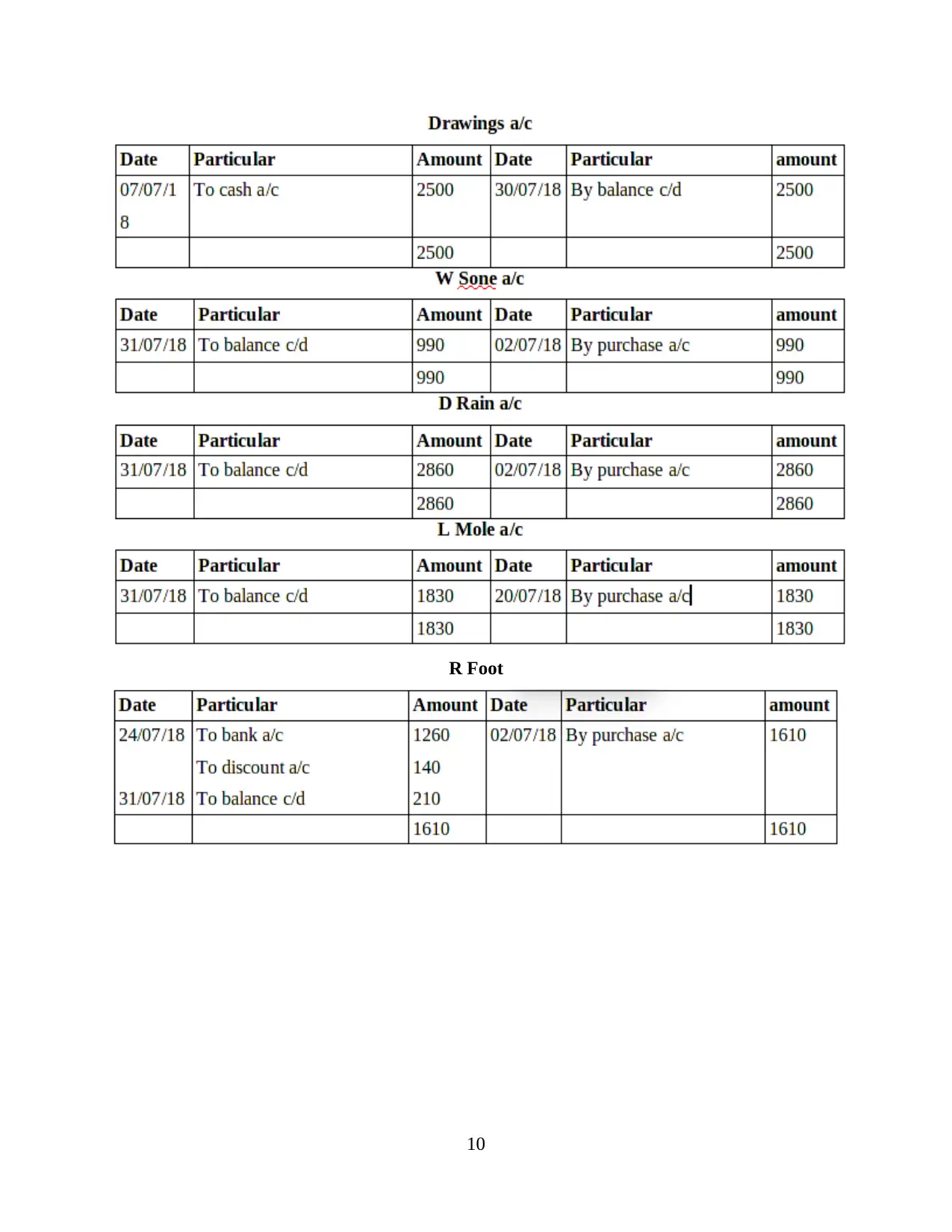

R Foot

10

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.