Financial Accounting: Journal Entries and Financial Statements

VerifiedAdded on 2020/04/15

|13

|1672

|113

Homework Assignment

AI Summary

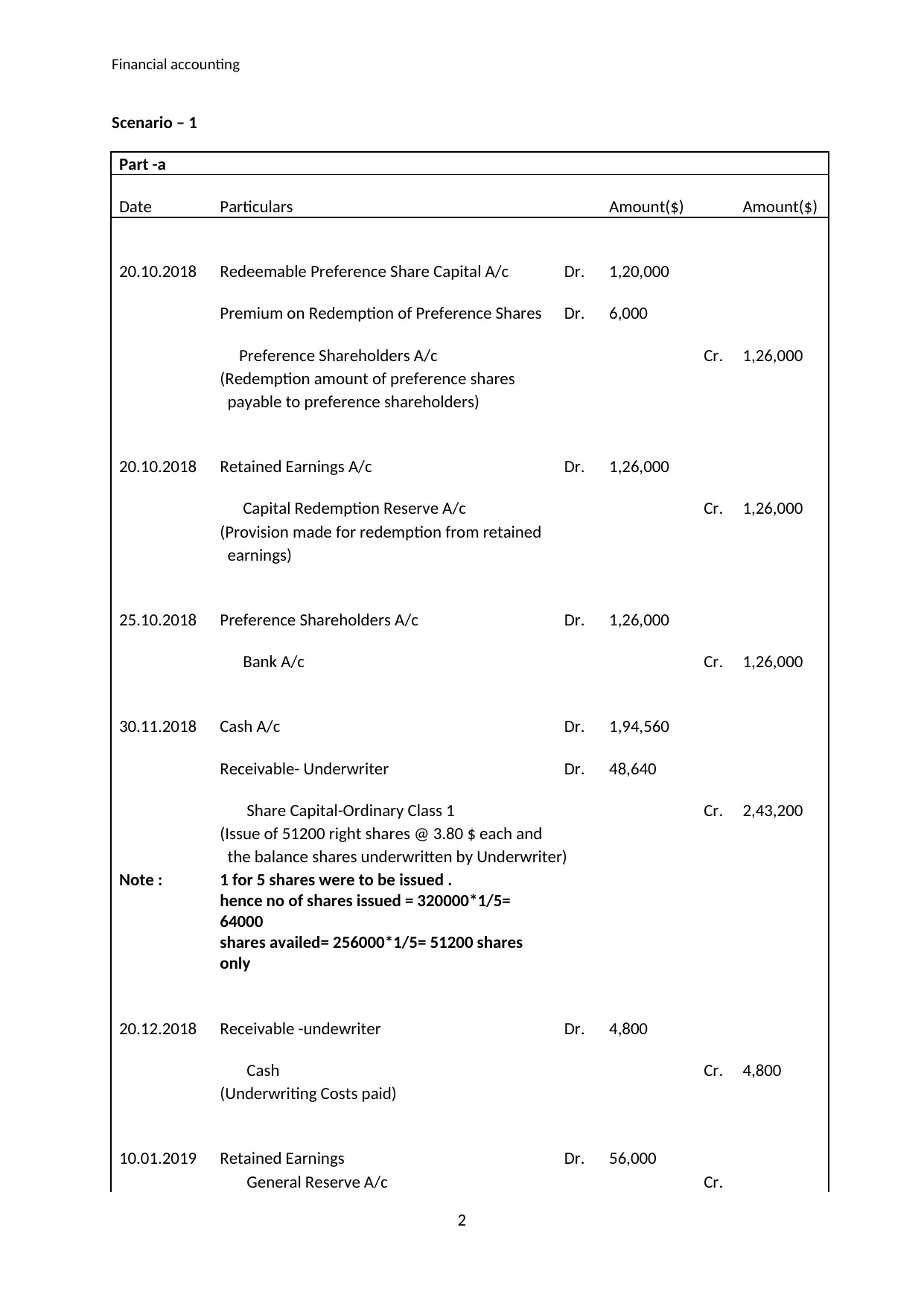

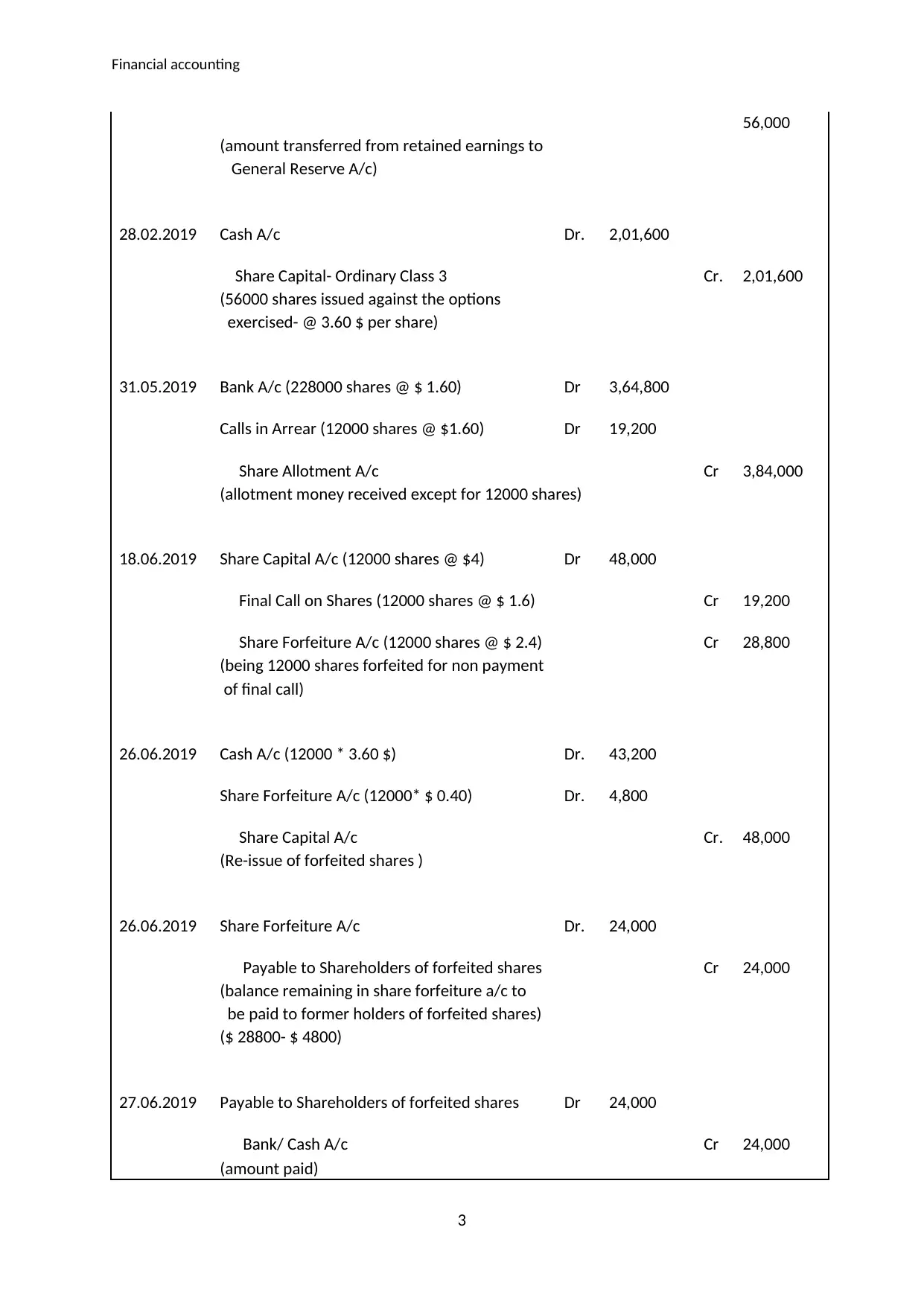

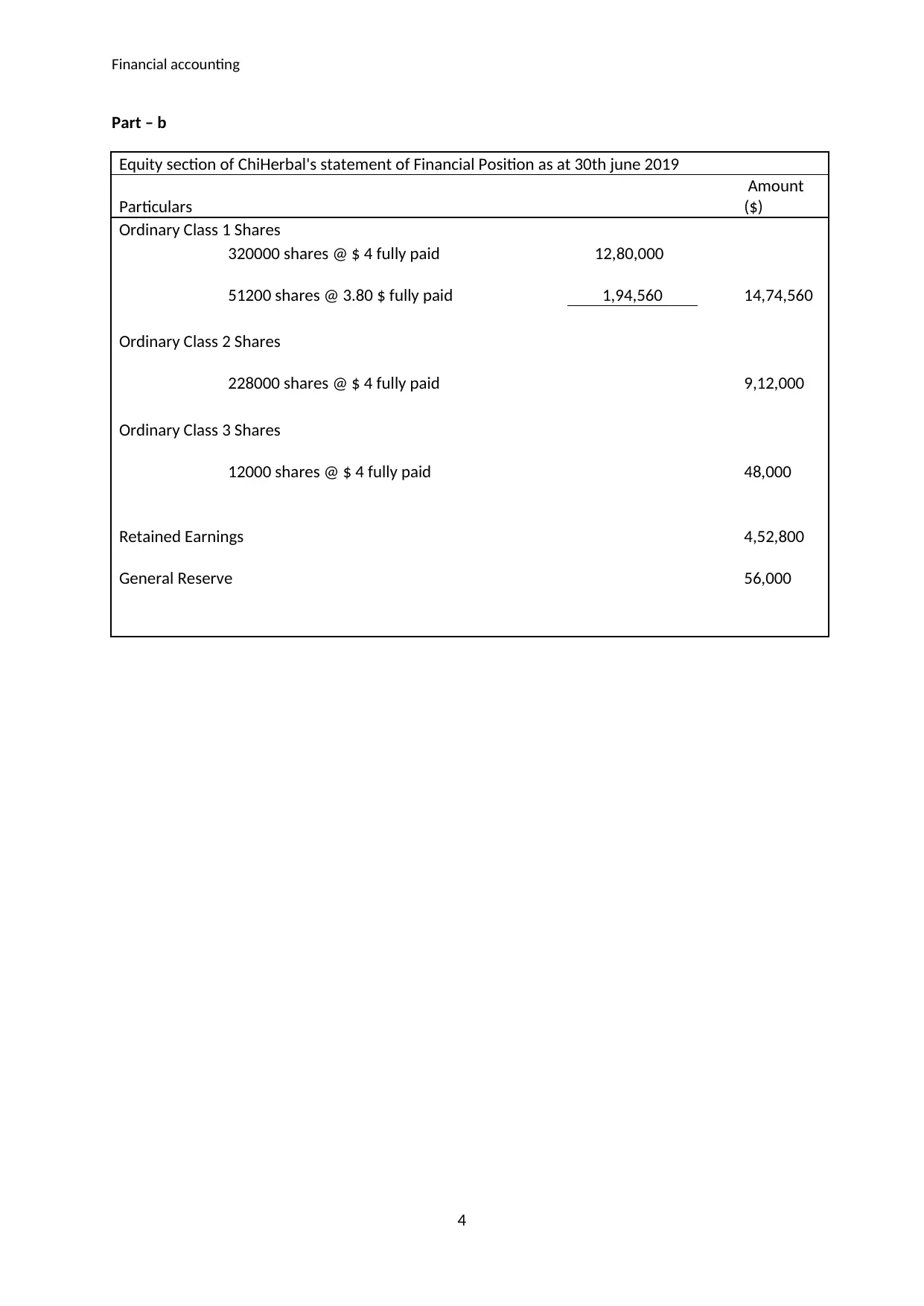

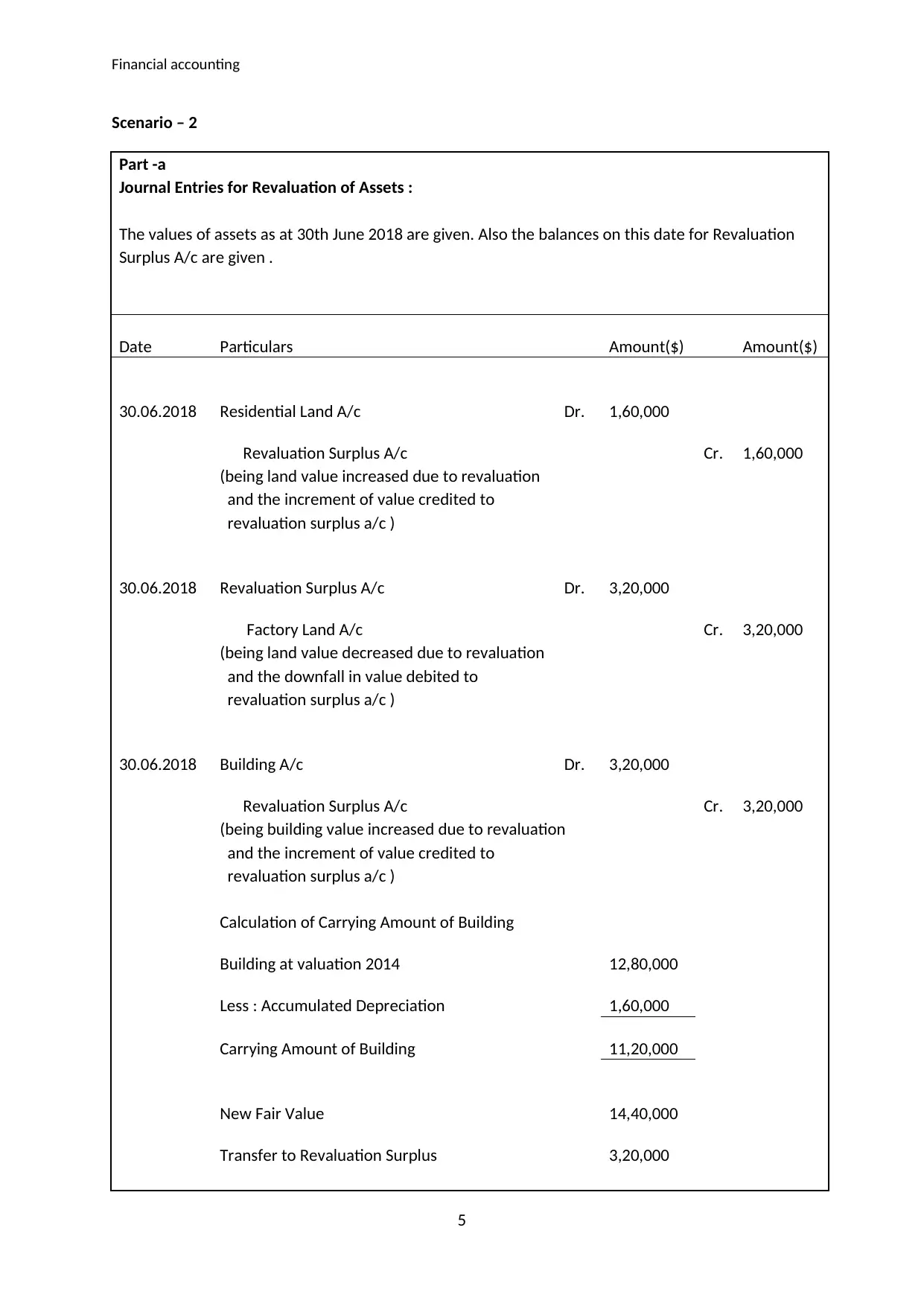

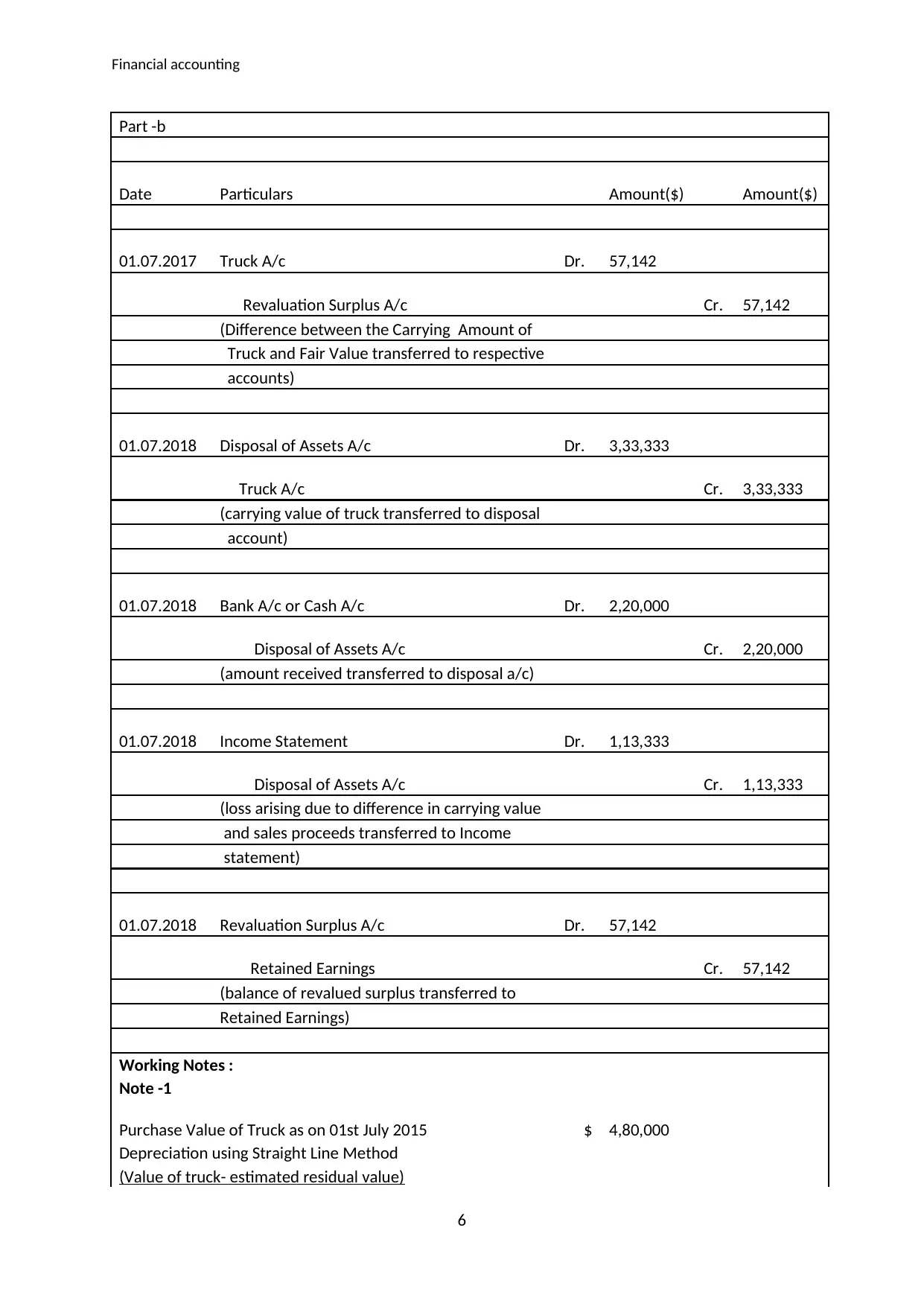

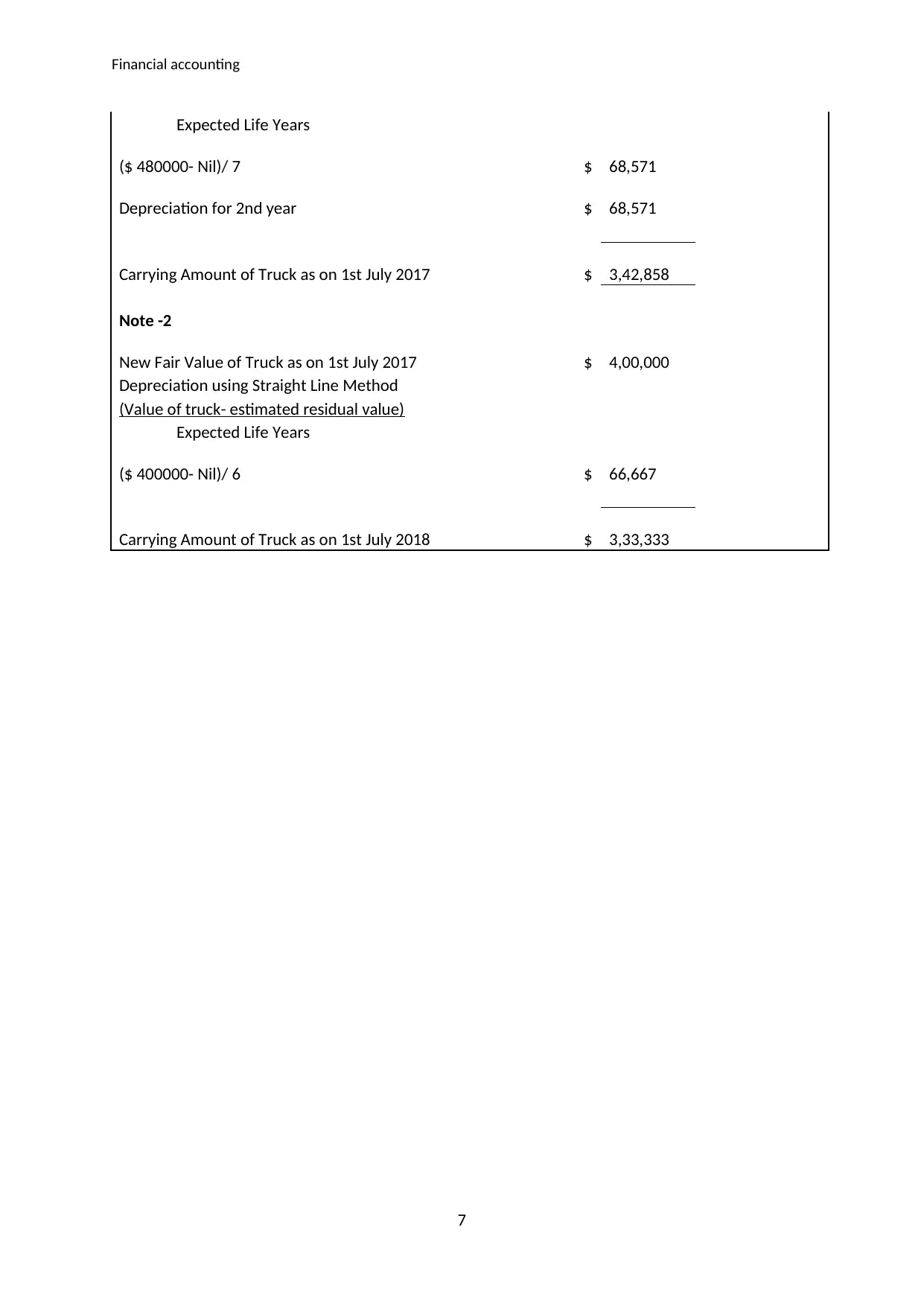

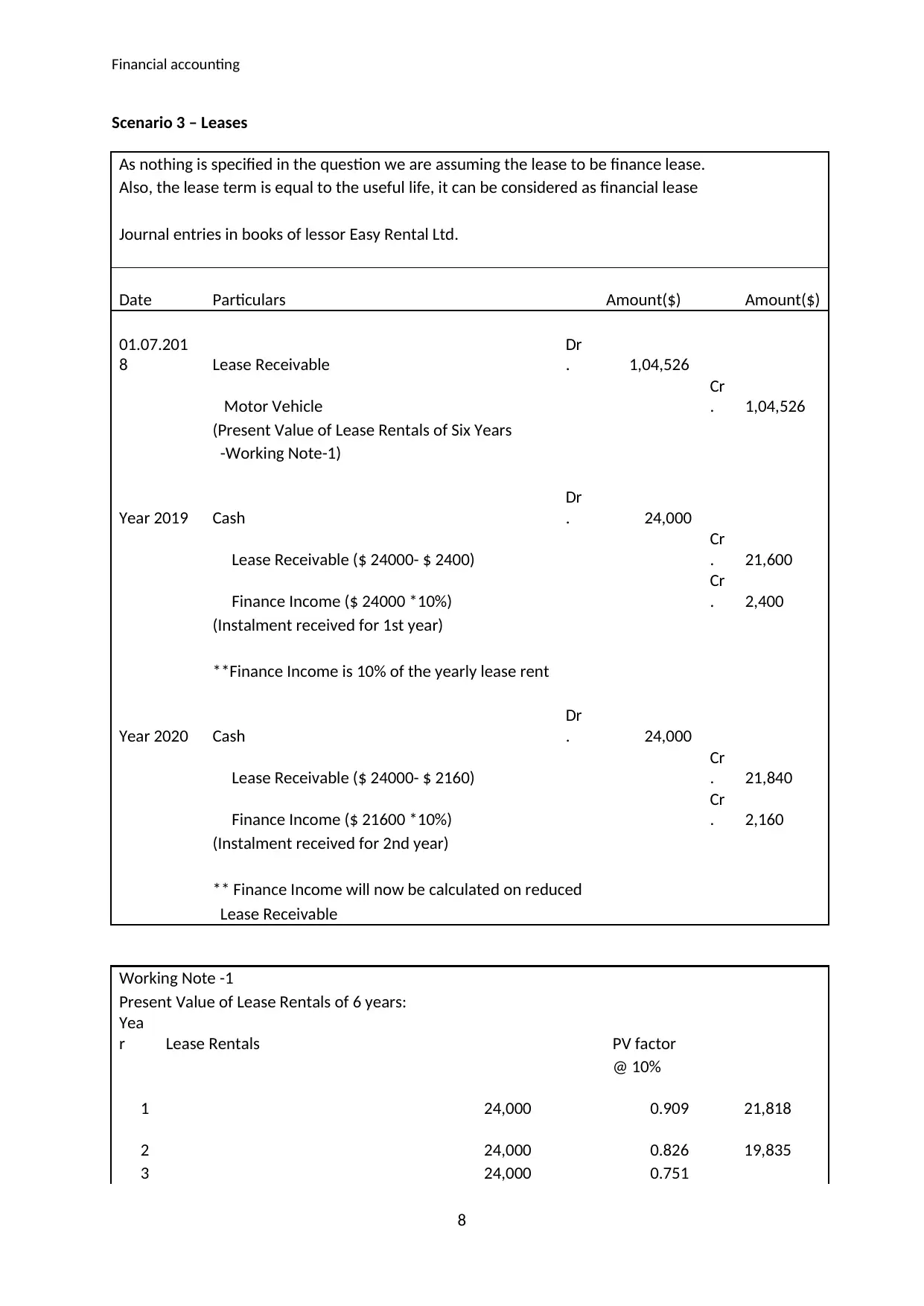

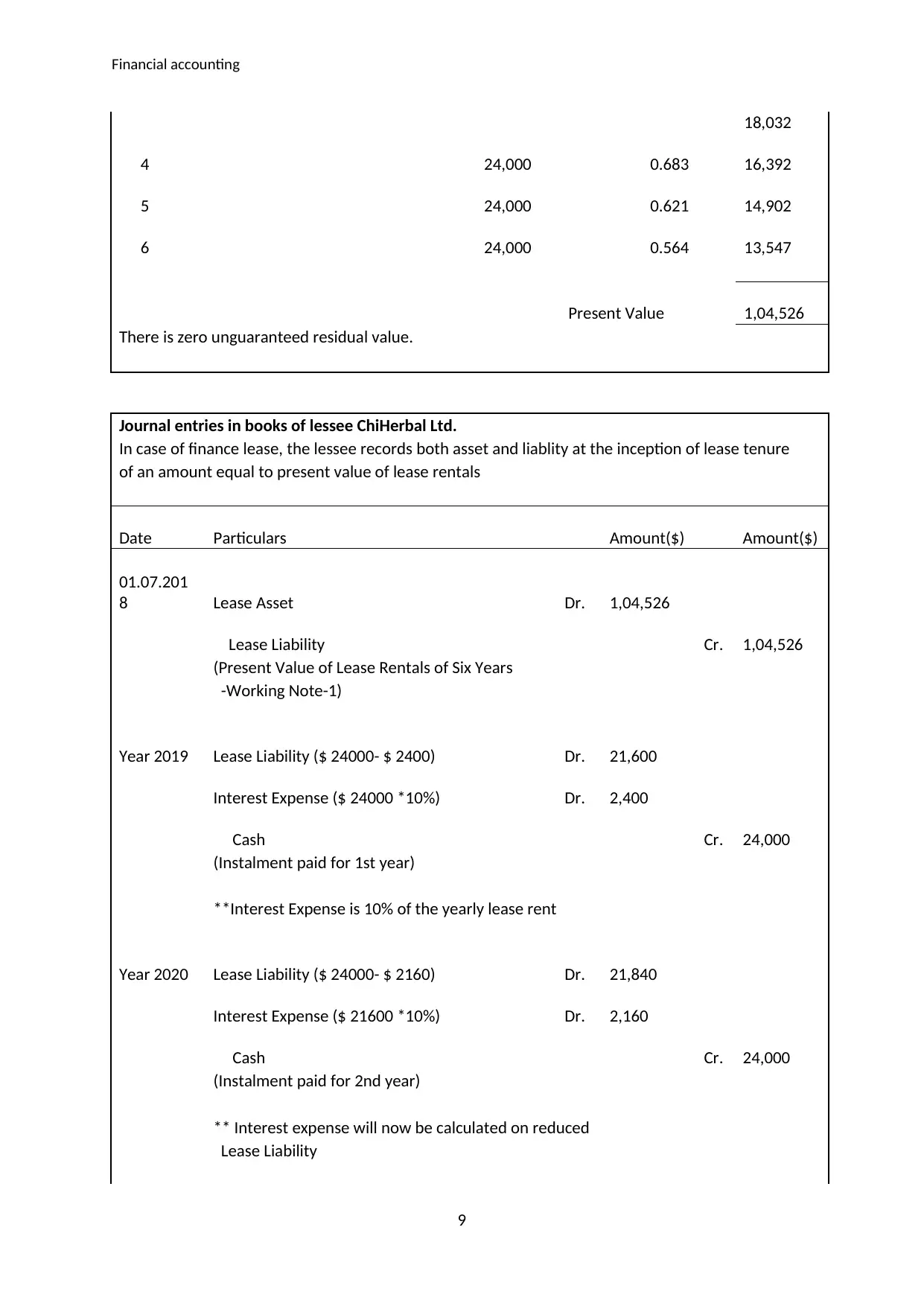

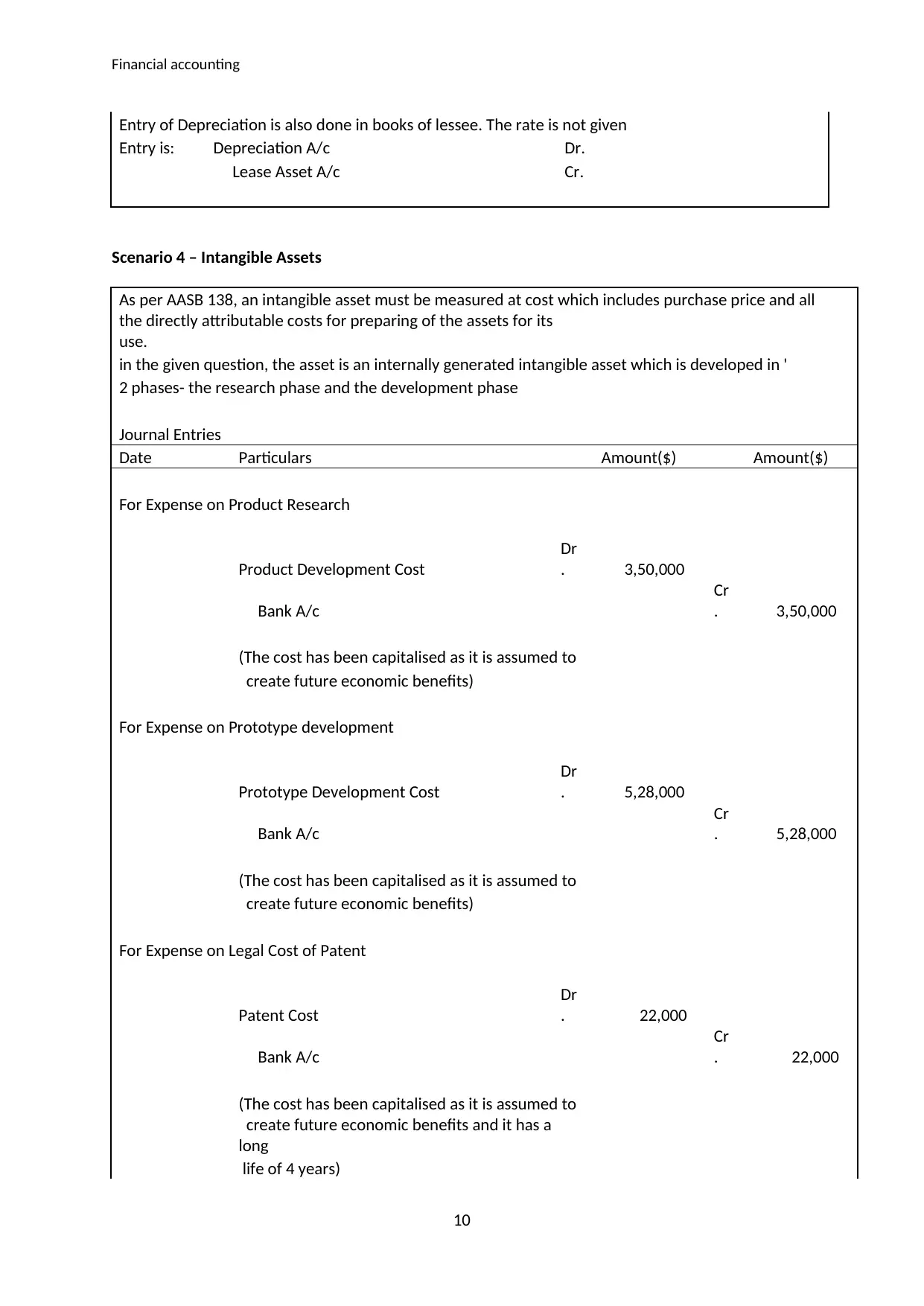

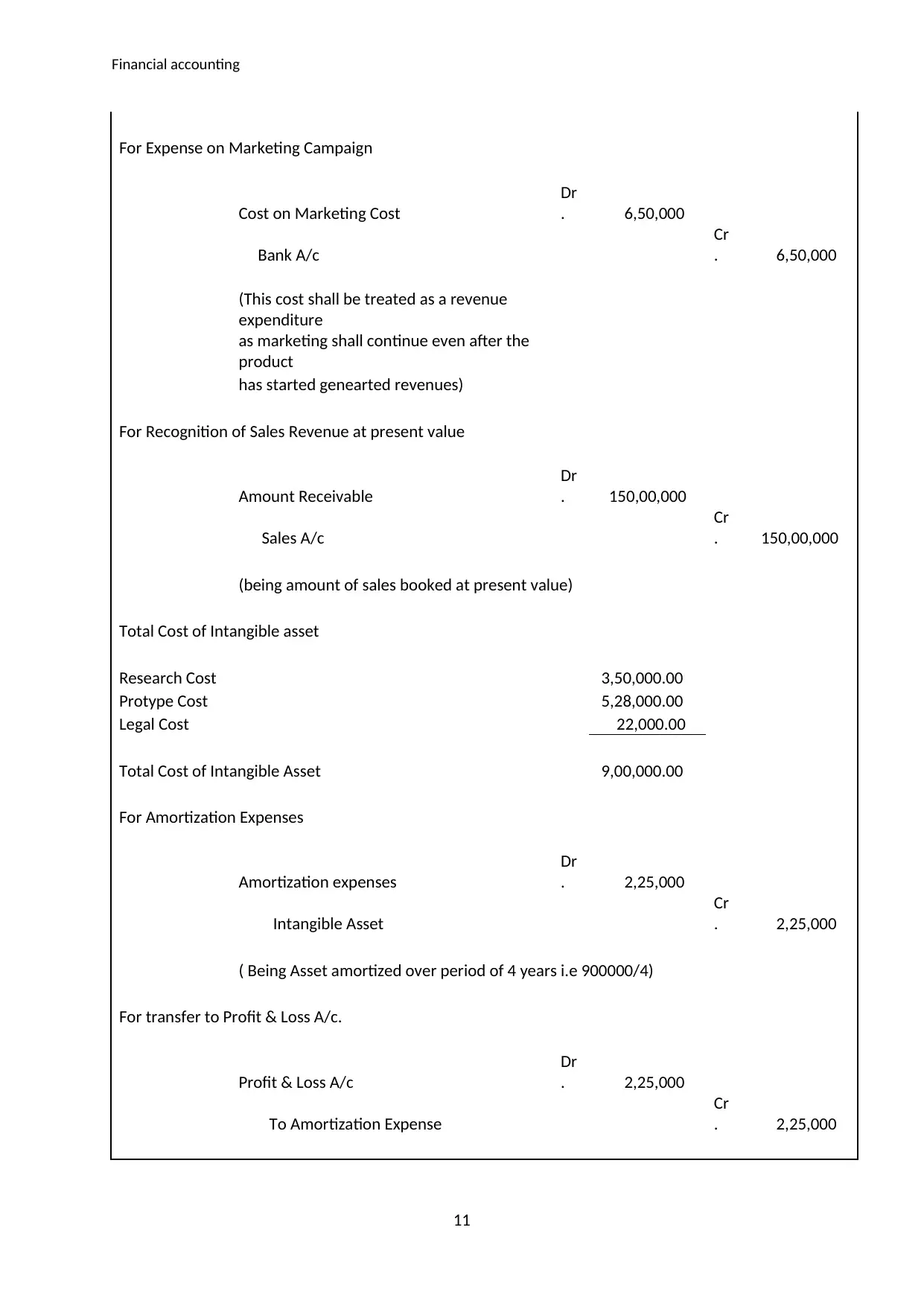

This document provides a comprehensive solution to a financial accounting assignment. It includes detailed journal entries for various scenarios such as redemption of preference shares, right shares, and share forfeitures. It also covers the equity section of a financial position statement. Furthermore, the assignment delves into the revaluation of assets, including land and buildings, alongside the disposal of assets, detailing the relevant journal entries. The solution also addresses finance leases, presenting journal entries for both the lessor and lessee. Lastly, it examines intangible assets, specifically internally generated assets, and includes the associated journal entries for research, development, and amortization expenses. The document also includes working notes and a bibliography.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.