Financial Accounting Principles: Ledger, Statement, and BRS Analysis

VerifiedAdded on 2021/01/02

|28

|3576

|127

Report

AI Summary

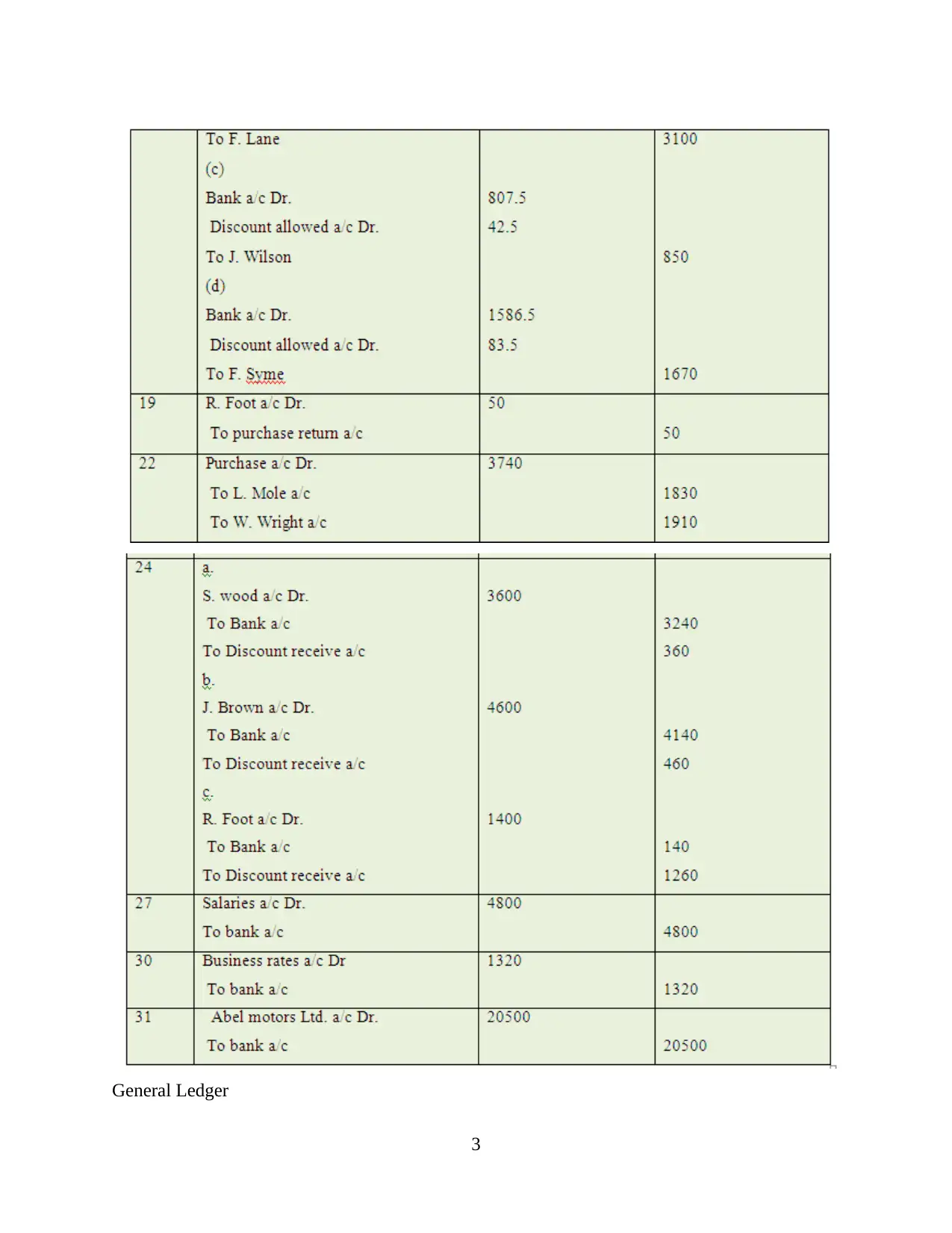

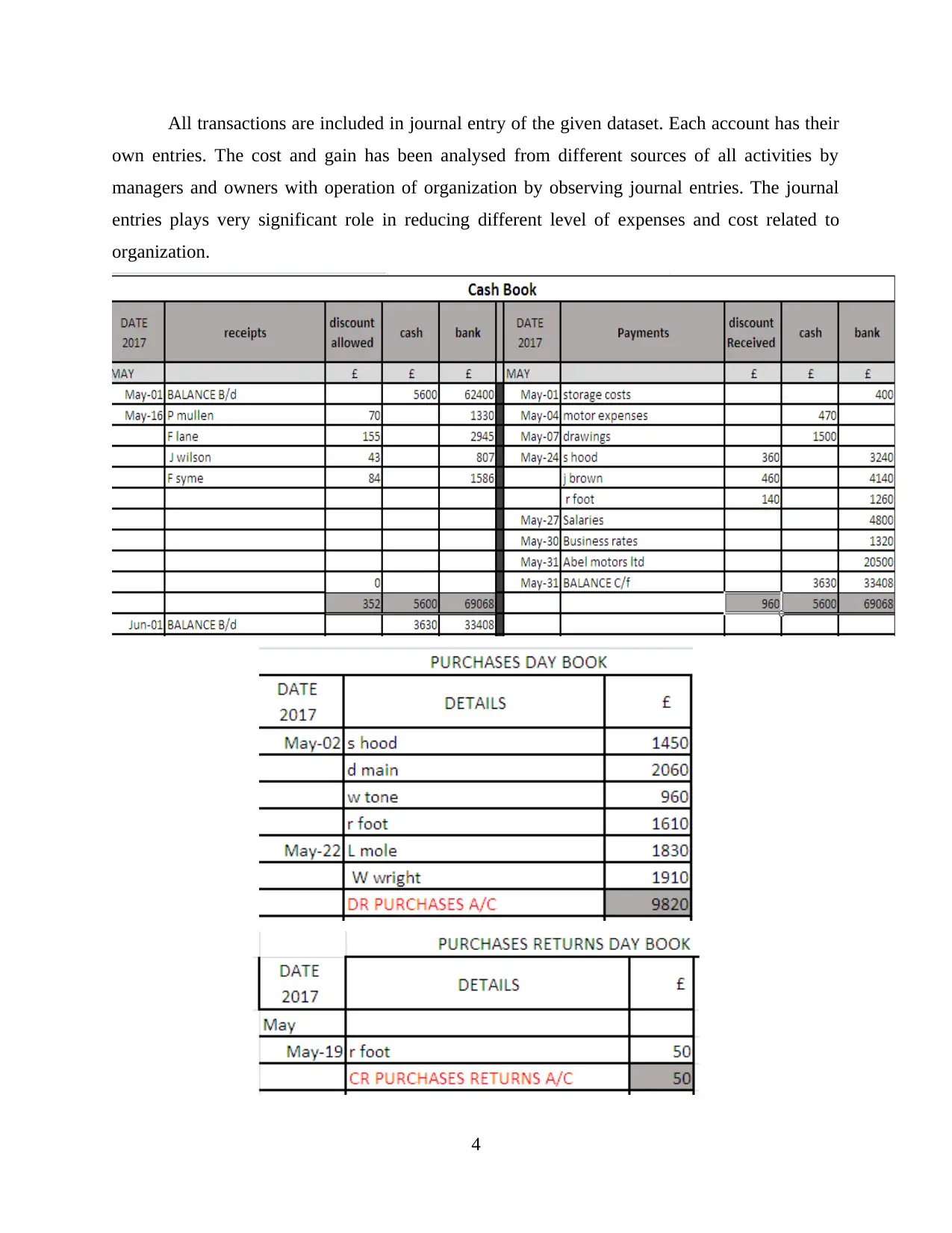

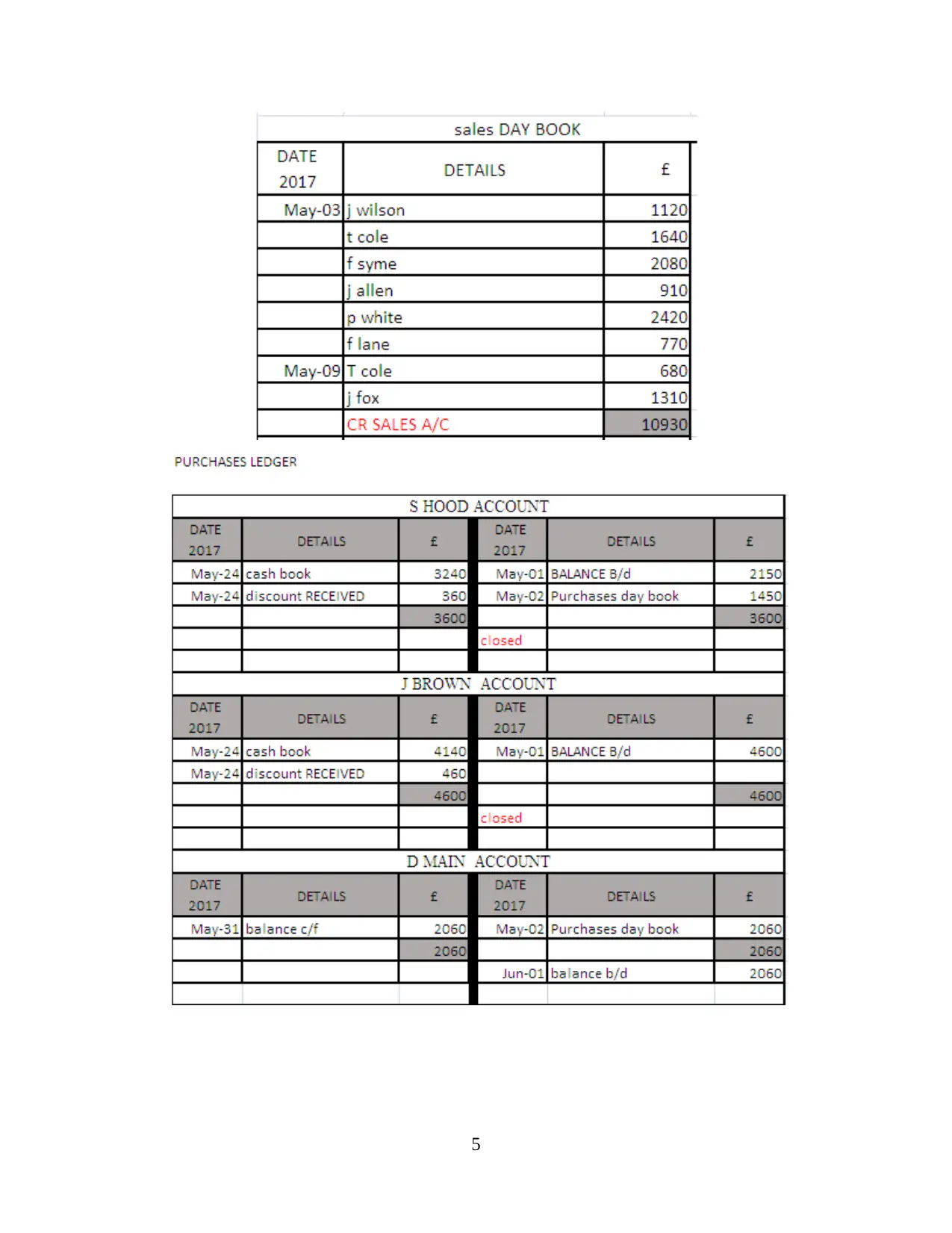

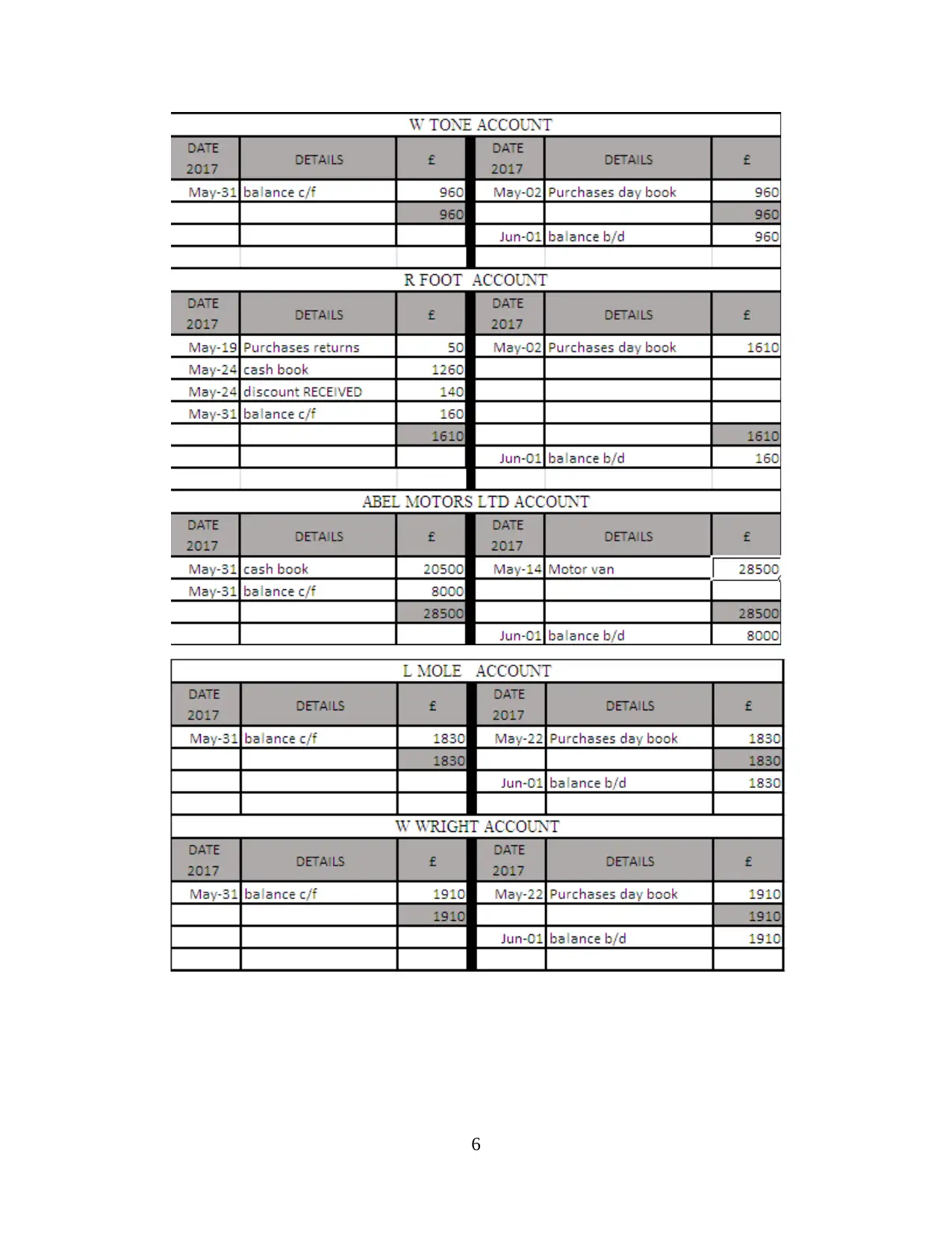

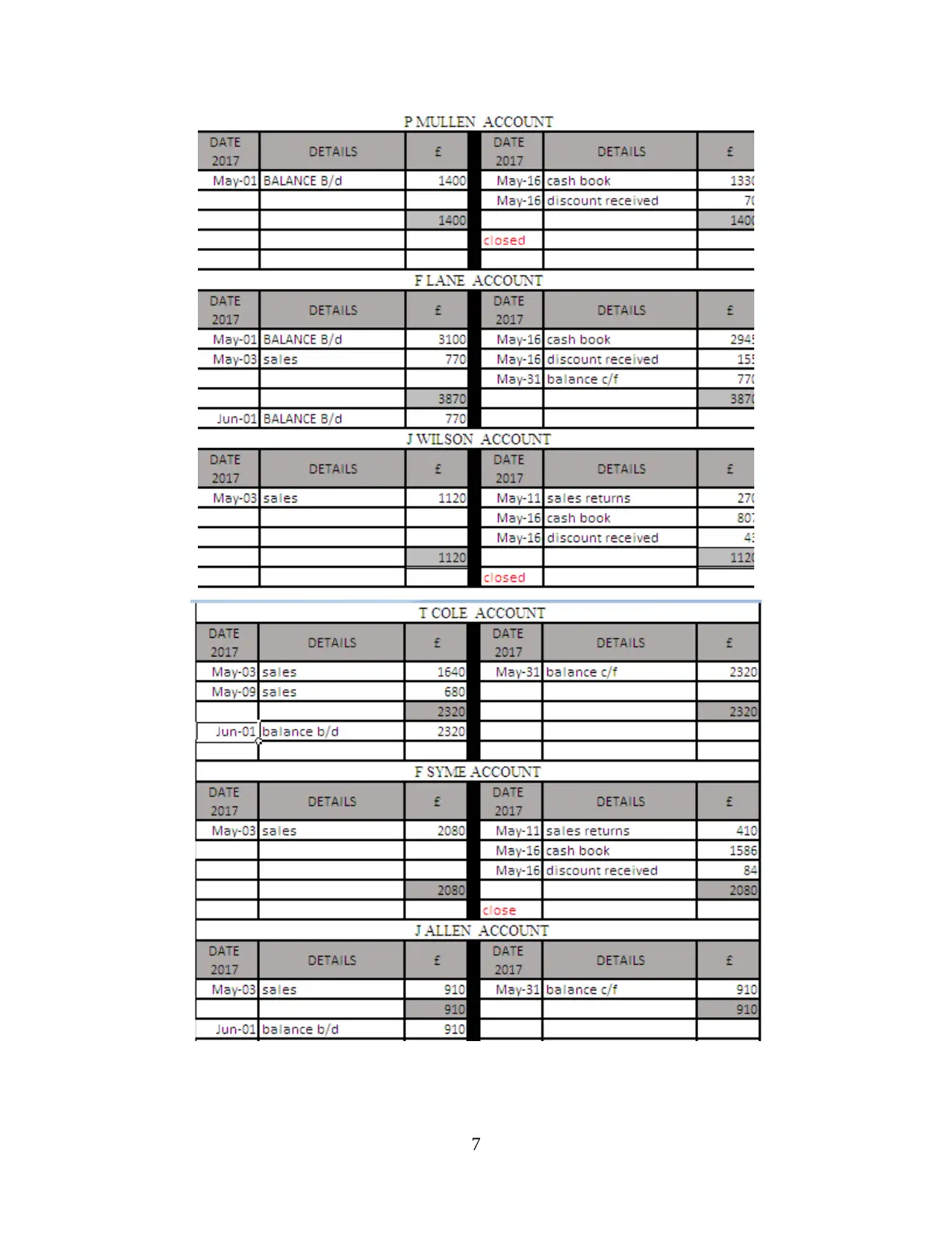

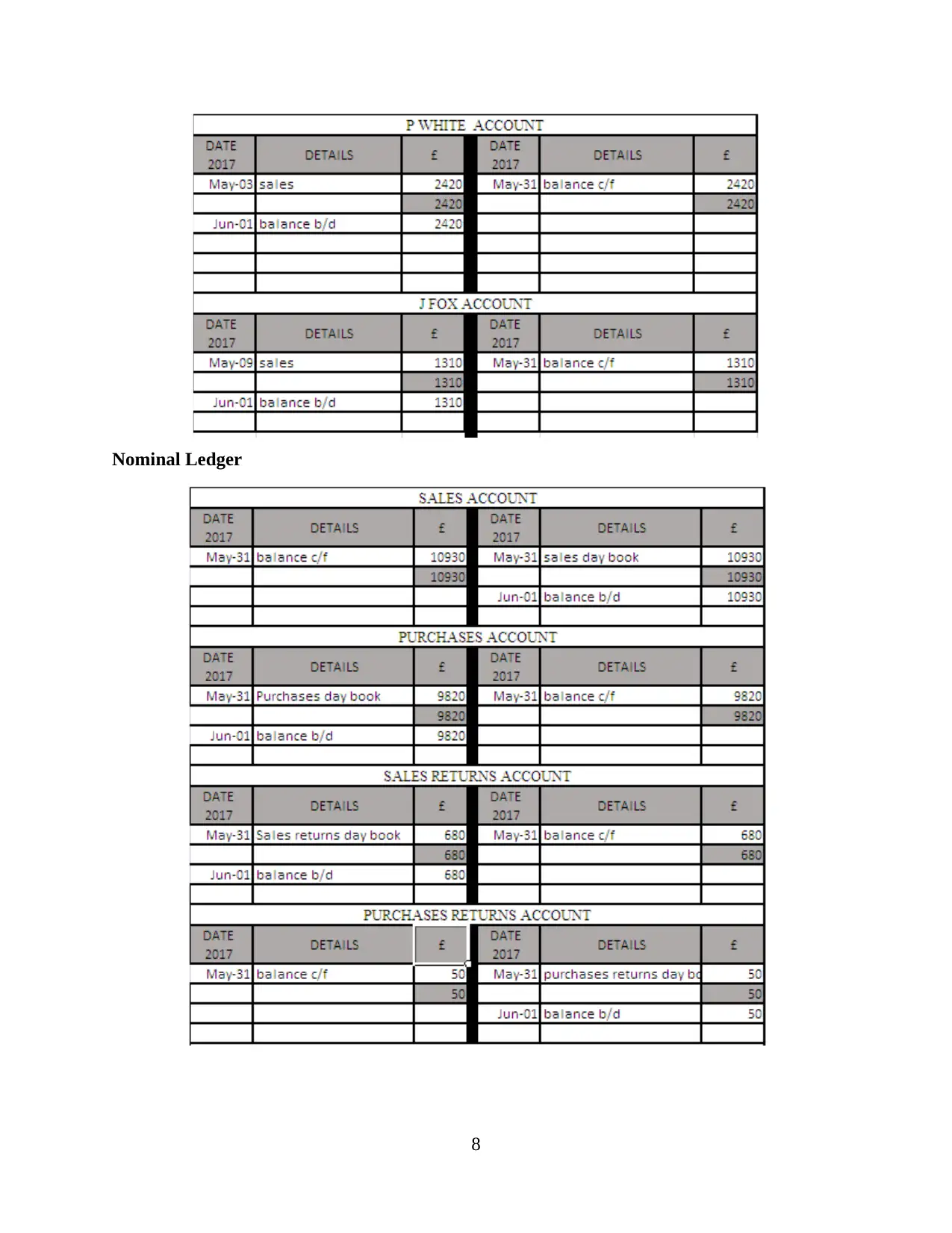

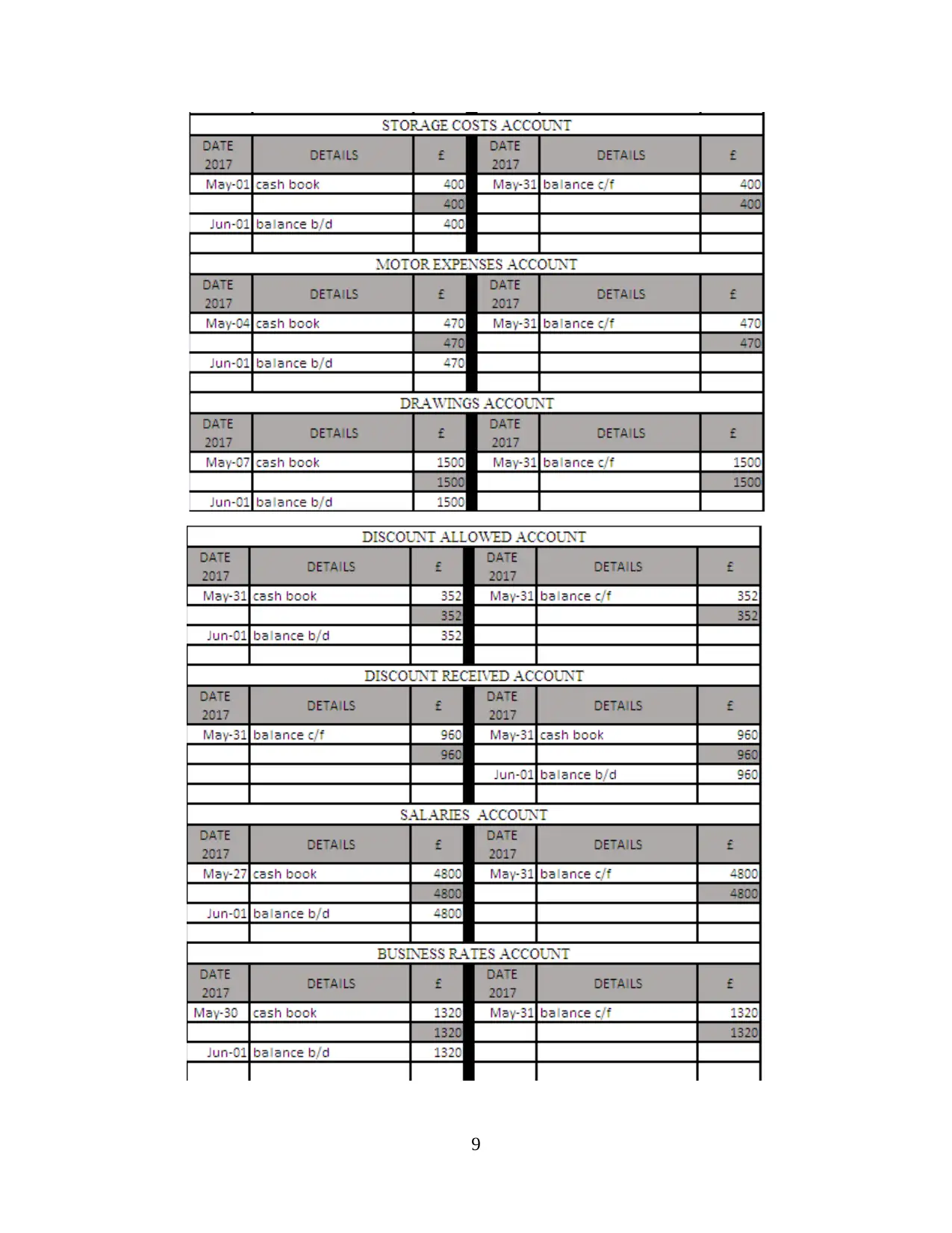

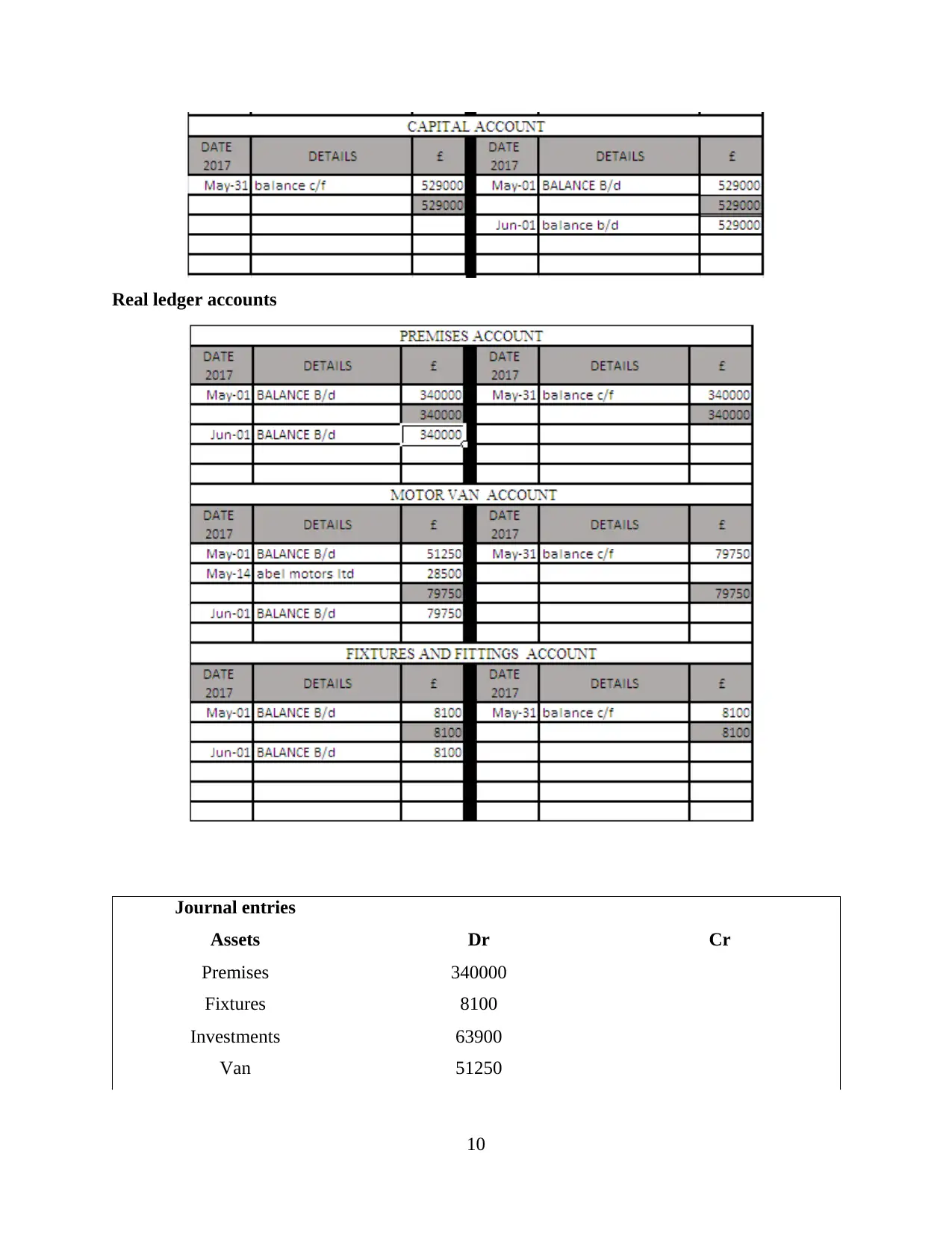

This report delves into the core principles of financial accounting, beginning with the application of the double-entry bookkeeping system to create general ledgers for sales and purchase transactions. It then proceeds to the construction of trial balances using the balance-off rule, followed by the preparation of final accounts, incorporating adjustments for depreciation and prepayments. The report further analyzes financial statements and includes a detailed examination of bank reconciliation statements (BRS). It also covers the framing of sales and purchase ledgers for a specific period, the evaluation of control accounts, and an explanation of suspense accounts, including their features, trial balance, journal entries, and a differentiation from clearing accounts. Furthermore, the report explores the different kinds of accounts and the construction of reconciliation methods, and it concludes by generating adequate accounting methods for measuring the financial performance of a business.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.