Financial Accounting: AASB 138 and Ramsay Health Care Limited

VerifiedAdded on 2023/01/06

|10

|2667

|41

AI Summary

This report provides an insight into the relevance and comparison of the accounting policy followed by Ramsay Health Care Limited with AASB 138 in respect to financial accounting of intangible assets.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

This report is on the topic financial accounting in respect to the Ramsay Health Care

Limited. It provides an insight about the relevance and the crucial points which is being stated in

the AASB 138 and drawing comparison between the accounting policy which is being followed

by the company and the policy stated under AASB 138. Based on the finding it is concluded that

the company is following most of the aspects which is being disclosed under AASB 138 and

based on which recommendations is being provided.

This report is on the topic financial accounting in respect to the Ramsay Health Care

Limited. It provides an insight about the relevance and the crucial points which is being stated in

the AASB 138 and drawing comparison between the accounting policy which is being followed

by the company and the policy stated under AASB 138. Based on the finding it is concluded that

the company is following most of the aspects which is being disclosed under AASB 138 and

based on which recommendations is being provided.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................4

Intangible assets under AASB 138.........................................................................................4

Measuring and disclosure as per AASB 138..........................................................................5

Evaluating the practices followed by Ramsay Health Care Limited in respect to intangible

assets.......................................................................................................................................5

Comparing the current policy followed by the company in comparison to the policies

permitted under AASB 138....................................................................................................7

RECOMMENDATION...................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................4

Intangible assets under AASB 138.........................................................................................4

Measuring and disclosure as per AASB 138..........................................................................5

Evaluating the practices followed by Ramsay Health Care Limited in respect to intangible

assets.......................................................................................................................................5

Comparing the current policy followed by the company in comparison to the policies

permitted under AASB 138....................................................................................................7

RECOMMENDATION...................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Every organization is required to follow and disclose the accounting standards it has been

following. For each and every aspect there is an accounting standard which the business entity is

required to comply with. This might be either in regard to disclosing it or the reporting it in the

manner prescribed or state by the law or regulations. In this report, Ramsay Health Care Limited

is taken as an organization. This report provides a complete overview of the accounting standard

which is being followed by the company in respect to measuring and disclosing its intangible

assets.

MAIN BODY

Intangible assets under AASB 138

AASB 138 provides a definition of the intangible assets. This standards also incorporates

IAS 38 in respect to the intangible assets which is being issued by the IASB. This standard

provides information on how to recognize and measure the intangible assets of the organization

and also provides certain requirement in respect to properly disclosing the intangible assets.

Under AASB 138 there are certain factors which are required to be considered for classifying an

asset as an intangible asset (Anwar, Delaney and Winata, 2016). First important aspect is the

identifiability, it involves the identifying the assets as an intangible asset which must be either

distinguished from the business or it must have arisen from the any of the legal document or the

legal rights in respect to it. The second aspect is that the intangible asset must be non-monetary,

in simple words, the value of the asset cannot be determined in fixed or the determinable amount.

The third factor to be considered is that the there must be lack of any physical presence of

the asset in order to consider it as an intangible asset. An asset should be something which

cannot be touched such as copyright, patent and so forth. The next factor is the exerting control

over such assets on account to what occur with it. The level of power to be exercised over the

asset is also dependent upon whether the company is the having power in respect to obtaining the

economic benefits in the future or not. Also, the company should be able to prevent others from

taking advantage of it (Bodle, Cybinski and Monem, 2016). The last and the most vital factor is

the economic benefit in respect to the future. It is very crucial to consider this factor in

determining an asset as intangible. As by identifying the future cash flow will result into getting

more meaningful and useful insight. Also, the organization should be able to determine the future

Every organization is required to follow and disclose the accounting standards it has been

following. For each and every aspect there is an accounting standard which the business entity is

required to comply with. This might be either in regard to disclosing it or the reporting it in the

manner prescribed or state by the law or regulations. In this report, Ramsay Health Care Limited

is taken as an organization. This report provides a complete overview of the accounting standard

which is being followed by the company in respect to measuring and disclosing its intangible

assets.

MAIN BODY

Intangible assets under AASB 138

AASB 138 provides a definition of the intangible assets. This standards also incorporates

IAS 38 in respect to the intangible assets which is being issued by the IASB. This standard

provides information on how to recognize and measure the intangible assets of the organization

and also provides certain requirement in respect to properly disclosing the intangible assets.

Under AASB 138 there are certain factors which are required to be considered for classifying an

asset as an intangible asset (Anwar, Delaney and Winata, 2016). First important aspect is the

identifiability, it involves the identifying the assets as an intangible asset which must be either

distinguished from the business or it must have arisen from the any of the legal document or the

legal rights in respect to it. The second aspect is that the intangible asset must be non-monetary,

in simple words, the value of the asset cannot be determined in fixed or the determinable amount.

The third factor to be considered is that the there must be lack of any physical presence of

the asset in order to consider it as an intangible asset. An asset should be something which

cannot be touched such as copyright, patent and so forth. The next factor is the exerting control

over such assets on account to what occur with it. The level of power to be exercised over the

asset is also dependent upon whether the company is the having power in respect to obtaining the

economic benefits in the future or not. Also, the company should be able to prevent others from

taking advantage of it (Bodle, Cybinski and Monem, 2016). The last and the most vital factor is

the economic benefit in respect to the future. It is very crucial to consider this factor in

determining an asset as intangible. As by identifying the future cash flow will result into getting

more meaningful and useful insight. Also, the organization should be able to determine the future

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

advantages more reliably. These benefits can be derived from the selling of the product or

services and also by saving the cost in association with it.

Measuring and disclosure as per AASB 138

As per the AASB 138, the company is required to initially measure and recognize all the

assets on the basis of its cost. And then after recognizing the assets considering the above stated

factors, the intangible asset can be measured either by cost or with the help of the revaluation

model. Specifics in relation to such models is stated in the AASB 138. This standard also

requires the organization to make disclosure of the assets on the basis of the class and also

distinguishing it from the internally generated intangible assets (Cheung and Lau, 2016).

According to this standard, the internally generated goodwill is not taken as an intangible asset

even though it is generating future economic benefits. Such asset is not considered intangible

assets this is because it is not an identifiable source over which the control can be exerted by the

entity and can be measured at the reliable cost. Also, there are times when there are factors

having an impact over the fair value of the entity, but such cost are not considered and represent

the cost of the intangible assets which is being controlled by the entity.

It is sometimes complex in determining whether an internally generated intangible asset

qualifies for the recognition which is because of the two main problems. First determining when

an identifiable asset will incur future benefits and the second is identifying the cost of the asset

on a reliable basis. For recognising an asset, the generation of the asset is bifurcated into research

phase and the development phase. Under the research phase, no intangible asset is generated and

recognised (Kabir, Su, and Rahman, 2020). Any expenditure which has been incurred on

research will be recognised as an expense. In case of development phase, an intangible asset will

be recognised only if it complies with the certain factors such as technical feasibility, intention to

complete, use or sell it. It also includes how it will generate future economic benefits, measure it

reliably.

Evaluating the practices followed by Ramsay Health Care Limited in respect to intangible assets

Ramsay Health Care Limited has treated goodwill separately from the other intangible

assets. The impairment is identified by determining the recoverable amount on account of the

cash incurring unit which is related to the goodwill. In the situation when the recoverable amount

is lower than the carrying amount then the impairment loss is recognised (Wang, 2019). In case,

that unit is disposed off then the goodwill associated with it is included in the carrying amount of

services and also by saving the cost in association with it.

Measuring and disclosure as per AASB 138

As per the AASB 138, the company is required to initially measure and recognize all the

assets on the basis of its cost. And then after recognizing the assets considering the above stated

factors, the intangible asset can be measured either by cost or with the help of the revaluation

model. Specifics in relation to such models is stated in the AASB 138. This standard also

requires the organization to make disclosure of the assets on the basis of the class and also

distinguishing it from the internally generated intangible assets (Cheung and Lau, 2016).

According to this standard, the internally generated goodwill is not taken as an intangible asset

even though it is generating future economic benefits. Such asset is not considered intangible

assets this is because it is not an identifiable source over which the control can be exerted by the

entity and can be measured at the reliable cost. Also, there are times when there are factors

having an impact over the fair value of the entity, but such cost are not considered and represent

the cost of the intangible assets which is being controlled by the entity.

It is sometimes complex in determining whether an internally generated intangible asset

qualifies for the recognition which is because of the two main problems. First determining when

an identifiable asset will incur future benefits and the second is identifying the cost of the asset

on a reliable basis. For recognising an asset, the generation of the asset is bifurcated into research

phase and the development phase. Under the research phase, no intangible asset is generated and

recognised (Kabir, Su, and Rahman, 2020). Any expenditure which has been incurred on

research will be recognised as an expense. In case of development phase, an intangible asset will

be recognised only if it complies with the certain factors such as technical feasibility, intention to

complete, use or sell it. It also includes how it will generate future economic benefits, measure it

reliably.

Evaluating the practices followed by Ramsay Health Care Limited in respect to intangible assets

Ramsay Health Care Limited has treated goodwill separately from the other intangible

assets. The impairment is identified by determining the recoverable amount on account of the

cash incurring unit which is related to the goodwill. In the situation when the recoverable amount

is lower than the carrying amount then the impairment loss is recognised (Wang, 2019). In case,

that unit is disposed off then the goodwill associated with it is included in the carrying amount of

the business operation at the time of determining the gain or loss on such disposal. The value of

the goodwill is determined under such situation on the basis of the relative values of the

operation.

On account of the intangible assets, the Ramsay Health Care Limited separately measures

the intangible assets initially at the cost. The cost at which the intangible asset is acquired is its

fair value at the time of such acquisition. After the recognition process, the intangible assets are

recognised at the cost reduced by the accumulated amortization or any other impairment losses.

In case of the internally generated intangible assets which excludes the capitalized

developmental costs, is not capitalized and all the expenditure which has been incurred on it is

charged against the profits in the year in which it is incurred (Ramsay Health Care Limited

Annual Report. 2019). The company assesses the useful; life of the assets which is either finite or

indefinite. All the intangible assets of the company having finite life are treated and amortized to

its useful life and along with that the impairment is also assessed if there is an indication that an

any of such asset is impaired. The amortization period and the method in case of finite life is

reviewed at the end of the every financial year.

If there are any changes which is expected in the useful life of the asset or the

consumption pattern on account of the future economic benefits are accounted by making change

in the amortization period or the method whatever is required. This amount of the amortization

expense is recognised in the income statement of the company in respect to the finite. In case of

the indefinite life of the intangible assets is first tested for the impairment which is either done

individually or on the cash generating division which is in consistence with the methodology

used in the goodwill impairment testing. Such type of assets are not amortized (Russell, 2017).

Such intangible assets of the company are reviewed each financial period in order to determine

whether the indefinite life of the assets are continuous to be supportable or not, so that relevant

changes can be made on the same which will result into change in the accounting estimates and

is therefore, accounted on the prospective basis.

the goodwill is determined under such situation on the basis of the relative values of the

operation.

On account of the intangible assets, the Ramsay Health Care Limited separately measures

the intangible assets initially at the cost. The cost at which the intangible asset is acquired is its

fair value at the time of such acquisition. After the recognition process, the intangible assets are

recognised at the cost reduced by the accumulated amortization or any other impairment losses.

In case of the internally generated intangible assets which excludes the capitalized

developmental costs, is not capitalized and all the expenditure which has been incurred on it is

charged against the profits in the year in which it is incurred (Ramsay Health Care Limited

Annual Report. 2019). The company assesses the useful; life of the assets which is either finite or

indefinite. All the intangible assets of the company having finite life are treated and amortized to

its useful life and along with that the impairment is also assessed if there is an indication that an

any of such asset is impaired. The amortization period and the method in case of finite life is

reviewed at the end of the every financial year.

If there are any changes which is expected in the useful life of the asset or the

consumption pattern on account of the future economic benefits are accounted by making change

in the amortization period or the method whatever is required. This amount of the amortization

expense is recognised in the income statement of the company in respect to the finite. In case of

the indefinite life of the intangible assets is first tested for the impairment which is either done

individually or on the cash generating division which is in consistence with the methodology

used in the goodwill impairment testing. Such type of assets are not amortized (Russell, 2017).

Such intangible assets of the company are reviewed each financial period in order to determine

whether the indefinite life of the assets are continuous to be supportable or not, so that relevant

changes can be made on the same which will result into change in the accounting estimates and

is therefore, accounted on the prospective basis.

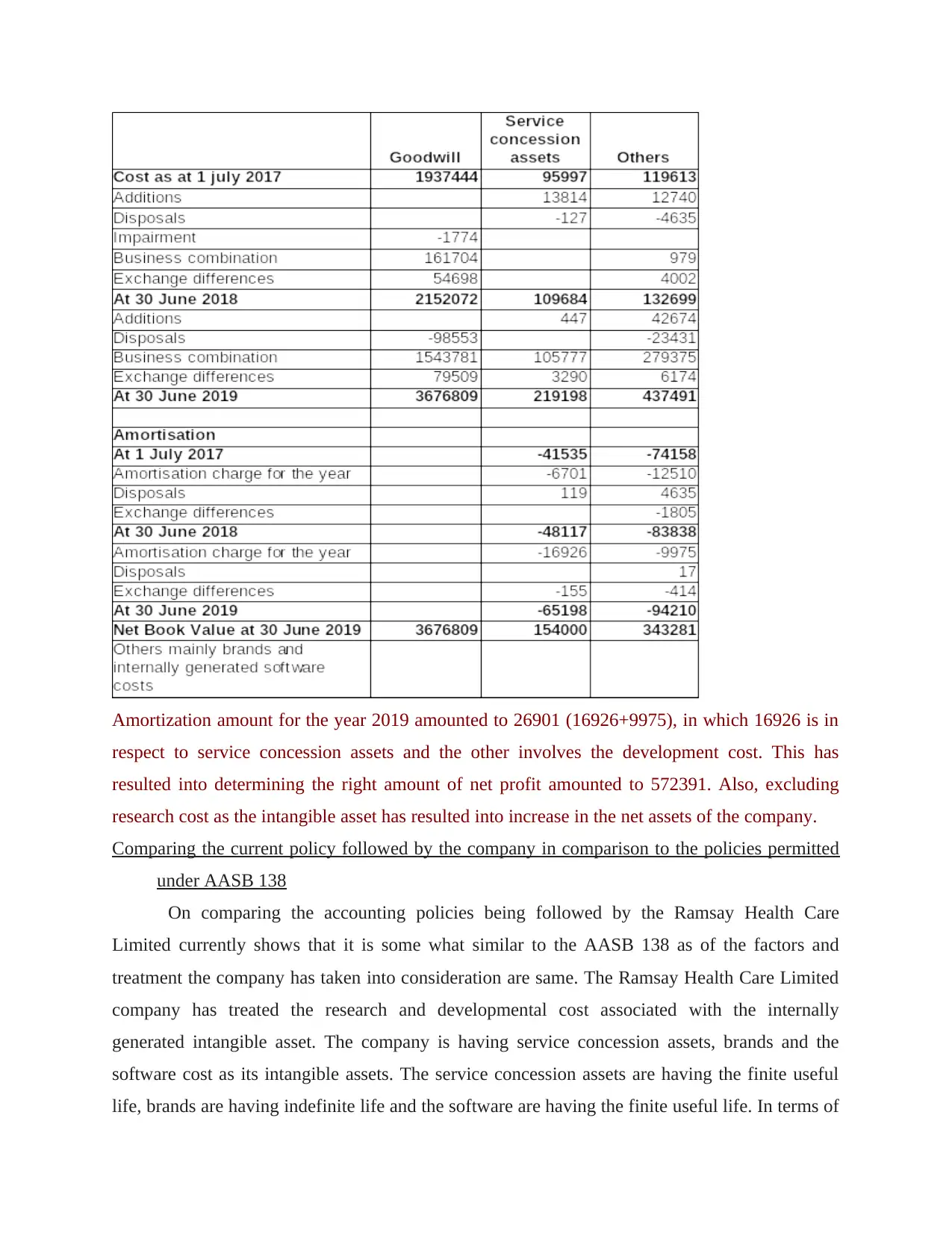

Amortization amount for the year 2019 amounted to 26901 (16926+9975), in which 16926 is in

respect to service concession assets and the other involves the development cost. This has

resulted into determining the right amount of net profit amounted to 572391. Also, excluding

research cost as the intangible asset has resulted into increase in the net assets of the company.

Comparing the current policy followed by the company in comparison to the policies permitted

under AASB 138

On comparing the accounting policies being followed by the Ramsay Health Care

Limited currently shows that it is some what similar to the AASB 138 as of the factors and

treatment the company has taken into consideration are same. The Ramsay Health Care Limited

company has treated the research and developmental cost associated with the internally

generated intangible asset. The company is having service concession assets, brands and the

software cost as its intangible assets. The service concession assets are having the finite useful

life, brands are having indefinite life and the software are having the finite useful life. In terms of

respect to service concession assets and the other involves the development cost. This has

resulted into determining the right amount of net profit amounted to 572391. Also, excluding

research cost as the intangible asset has resulted into increase in the net assets of the company.

Comparing the current policy followed by the company in comparison to the policies permitted

under AASB 138

On comparing the accounting policies being followed by the Ramsay Health Care

Limited currently shows that it is some what similar to the AASB 138 as of the factors and

treatment the company has taken into consideration are same. The Ramsay Health Care Limited

company has treated the research and developmental cost associated with the internally

generated intangible asset. The company is having service concession assets, brands and the

software cost as its intangible assets. The service concession assets are having the finite useful

life, brands are having indefinite life and the software are having the finite useful life. In terms of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

internally generated intangible assets, it mainly includes the brands and the internally created

software cost (Steenkamp and Steenkamp, 2016). This treatment is same as the one stated in the

AASB 138, in the service concession assets, it is amortized over the period of the lease,

amortization is done in the brands and the software cost is also amortized over the specific time

frame in respect to the future benefits associated with it. This has resulted into depicting the right

amount of the profit for the organization which is 572,391. This has resulted into highlighting the

costs which can be amortized and which cannot be and along with that it will help in determining

and identifying the which asset should be recognized as intangible or not.

This is economically feasible for the company as it is helping the company in

determining the right set of assets and bifurcating the same on the basis of tangible and

intangible assets (Su and Wells, 2018). This will assist in meeting with the required changes in

the business environment since it is highlighting the right amount of value of the intangible

assets so that meaningful business decisions can be taken on time which can be turned out to be

beneficial for the company. The Ramsay Health Care Limited is involved in the health care

sector which requires incurring huge amount on its research and development and for treating the

same the accounting standard which is being followed by the company helps in meeting with the

business requirement of the organization.

RECOMMENDATION

Based on the above analysis, there are certain factors which the Ramsay Health Care

Limited should take into account which will help in providing the better and informed business

decisions. Some of the recommendations that the company can implement are described below.

The accountant of the company should be very well aware of the relevant accounting

standards and the implication of it over the business operations and profitability. This will

help in support the organization in determining the significant changes that can be made

to the business which is beneficial for the company.

Also, proper disclosure should be made by the company in respect to the accounting

standards being followed by the company and also how it is being measured by the

company and its implication over the net profits of the company.

The accountant of the company should be aware about the procedure and the steps which

is required to be followed and the factors that is needed to considered which recognizing

an asset as the intangible asset in order to avoid any mistake in the same.

software cost (Steenkamp and Steenkamp, 2016). This treatment is same as the one stated in the

AASB 138, in the service concession assets, it is amortized over the period of the lease,

amortization is done in the brands and the software cost is also amortized over the specific time

frame in respect to the future benefits associated with it. This has resulted into depicting the right

amount of the profit for the organization which is 572,391. This has resulted into highlighting the

costs which can be amortized and which cannot be and along with that it will help in determining

and identifying the which asset should be recognized as intangible or not.

This is economically feasible for the company as it is helping the company in

determining the right set of assets and bifurcating the same on the basis of tangible and

intangible assets (Su and Wells, 2018). This will assist in meeting with the required changes in

the business environment since it is highlighting the right amount of value of the intangible

assets so that meaningful business decisions can be taken on time which can be turned out to be

beneficial for the company. The Ramsay Health Care Limited is involved in the health care

sector which requires incurring huge amount on its research and development and for treating the

same the accounting standard which is being followed by the company helps in meeting with the

business requirement of the organization.

RECOMMENDATION

Based on the above analysis, there are certain factors which the Ramsay Health Care

Limited should take into account which will help in providing the better and informed business

decisions. Some of the recommendations that the company can implement are described below.

The accountant of the company should be very well aware of the relevant accounting

standards and the implication of it over the business operations and profitability. This will

help in support the organization in determining the significant changes that can be made

to the business which is beneficial for the company.

Also, proper disclosure should be made by the company in respect to the accounting

standards being followed by the company and also how it is being measured by the

company and its implication over the net profits of the company.

The accountant of the company should be aware about the procedure and the steps which

is required to be followed and the factors that is needed to considered which recognizing

an asset as the intangible asset in order to avoid any mistake in the same.

AASB 138/ provides a complete set of all the necessary which can be used as the guide

by the organization.

CONCLUSION

It can be summed up from the above that it is very essential for the business organization

in respect to effectively recognizing, measuring and reporting the accounting treatment in the

right and the specific manner which can be understood by the users easily. By implementing the

AASB 138 in respect to the intangible assets will prompt in bringing the new level of

consistency in the financial accounting and reporting. It is a very conservative standard but it

also lacks recognising certain assets as intangible assets which is mainly because of the

restrictions being imposed on the intangible assets which is being generated internally. This

standard provides assistance in identifying the intangible assets. Along with this, the effect of

this on the economic and future benefits of the company is linked and evaluated and determined

how the current policy being followed by the Ramsay Health Care Limited is meaningful for it or

not. At last, certain recommendation is being given which can be taken into account of the

company in effectively managing its intangible assets.

by the organization.

CONCLUSION

It can be summed up from the above that it is very essential for the business organization

in respect to effectively recognizing, measuring and reporting the accounting treatment in the

right and the specific manner which can be understood by the users easily. By implementing the

AASB 138 in respect to the intangible assets will prompt in bringing the new level of

consistency in the financial accounting and reporting. It is a very conservative standard but it

also lacks recognising certain assets as intangible assets which is mainly because of the

restrictions being imposed on the intangible assets which is being generated internally. This

standard provides assistance in identifying the intangible assets. Along with this, the effect of

this on the economic and future benefits of the company is linked and evaluated and determined

how the current policy being followed by the Ramsay Health Care Limited is meaningful for it or

not. At last, certain recommendation is being given which can be taken into account of the

company in effectively managing its intangible assets.

REFERENCES

Books and Journals

Anwar, Y., Delaney, D. and Winata, L., 2016. Intellectual Capital Disclosures-Does Social

Media Make A Difference? Evidence frm Australia and Indonesia.

Bodle, K. A., Cybinski, P. J. and Monem, R., 2016. Effect of IFRS adoption on financial

reporting quality. Accounting Research Journal.

Cheung, E. and Lau, J., 2016. Readability of Notes to the Financial Statements and the Adoption

of IFRS. Australian Accounting Review. 26(2). pp.162-176.

Kabir, H., Su, L. and Rahman, A., 2020. Firm life cycle and the disclosure of estimates and

judgments in goodwill impairment tests: Evidence from Australia. Journal of

Contemporary Accounting & Economics, p.100207.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting &

Finance. 57. pp.211-234.

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions reducing

R&D spending?. Journal of Financial Reporting and Accounting.

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting

Research Journal.

Wang, X., 2019. Compliance Over Time by Australian Firms with IFRS Disclosure

Requirements. Australian Accounting Review. 29(4). pp.679-691.

Online

Ramsay Health Care Limited Annual Report. 2019. [Online]. Available

Through:<https://www.ramsayhealth.com/common/emag/rhc/annualreport2019/RHC-

Annual-Report-2018-2019sml.pdf>.

Books and Journals

Anwar, Y., Delaney, D. and Winata, L., 2016. Intellectual Capital Disclosures-Does Social

Media Make A Difference? Evidence frm Australia and Indonesia.

Bodle, K. A., Cybinski, P. J. and Monem, R., 2016. Effect of IFRS adoption on financial

reporting quality. Accounting Research Journal.

Cheung, E. and Lau, J., 2016. Readability of Notes to the Financial Statements and the Adoption

of IFRS. Australian Accounting Review. 26(2). pp.162-176.

Kabir, H., Su, L. and Rahman, A., 2020. Firm life cycle and the disclosure of estimates and

judgments in goodwill impairment tests: Evidence from Australia. Journal of

Contemporary Accounting & Economics, p.100207.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting &

Finance. 57. pp.211-234.

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions reducing

R&D spending?. Journal of Financial Reporting and Accounting.

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting

Research Journal.

Wang, X., 2019. Compliance Over Time by Australian Firms with IFRS Disclosure

Requirements. Australian Accounting Review. 29(4). pp.679-691.

Online

Ramsay Health Care Limited Annual Report. 2019. [Online]. Available

Through:<https://www.ramsayhealth.com/common/emag/rhc/annualreport2019/RHC-

Annual-Report-2018-2019sml.pdf>.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.