Earnings Management and Sustainability

VerifiedAdded on 2020/02/05

|13

|4120

|434

Report

AI Summary

This research paper examines the complex relationship between earnings management and sustainability reporting. It delves into various methods of earnings management, including real activities manipulation and accrual-based adjustments. The paper analyzes how these practices influence the accuracy and reliability of financial information, potentially obscuring a company's true performance and sustainability status. It also explores the implications of earnings management for stakeholders, including investors, creditors, and the environment.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1 ...........................................................................................................................................1

P1 (a) (i) Describe management accounting and how it is differentiate from financial

accounting ..............................................................................................................................1

(ii) Importance of management accounting ...........................................................................2

(b) Examine the types of management accounting system ...................................................2

TASK 2............................................................................................................................................3

P3 (i)Income statement under marginal costing ....................................................................3

(ii) Income statement under absorption costing.....................................................................4

TASK 3............................................................................................................................................5

P4 (i)Different types of budgets and their advantages and disadvantages ............................5

(ii) Process of preparing budgets............................................................................................6

(iii) What are pricing strategics..............................................................................................6

TASK 4 ...........................................................................................................................................7

P5 (i) What is balance scorecard and how it is useful in respond to financial problems.......7

(ii) How balance scorecard can be used to improve financial development of effective

strategies.................................................................................................................................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION ..........................................................................................................................1

TASK 1 ...........................................................................................................................................1

P1 (a) (i) Describe management accounting and how it is differentiate from financial

accounting ..............................................................................................................................1

(ii) Importance of management accounting ...........................................................................2

(b) Examine the types of management accounting system ...................................................2

TASK 2............................................................................................................................................3

P3 (i)Income statement under marginal costing ....................................................................3

(ii) Income statement under absorption costing.....................................................................4

TASK 3............................................................................................................................................5

P4 (i)Different types of budgets and their advantages and disadvantages ............................5

(ii) Process of preparing budgets............................................................................................6

(iii) What are pricing strategics..............................................................................................6

TASK 4 ...........................................................................................................................................7

P5 (i) What is balance scorecard and how it is useful in respond to financial problems.......7

(ii) How balance scorecard can be used to improve financial development of effective

strategies.................................................................................................................................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is an activity of interpretation, analysing, communicating,

identifying and measuring in order to achieve organisational goals. This is also known as cost

accounting. It is the process managing financial reports and accounts that is able to provide

accurate and correct information and data. Managerial accounting is also helpful in making short

term or as well as day to day organisational operational. It provides annual budgets and income

& balance sheet statement, so that mangers can easily analysis their financial position and

performance in capital market (Briciu, Groza and Ganfalean, 2009). Basically these reports are

useful in showing sales revenue,capital expenditure,amount of order in hand, accounts receivable

and accounts payable, the statement are useful of internal analysis of the business organisation.

Managers can easily assessed their internal and external issues by which the behaviour of the

employees are effected. Management accounting and financial accpunti9ng bothy are the

essential tool of a commercial industries.

TASK 1

P1 (a) (i) Describe management accounting and how it is differentiate from financial accounting

Management accounting is the combination of finance, management and accounting by

which business techniques and skills added real value to any organisation. Management

accountant uses content of all types, not only just financial but also it inform and lead company's

strategy and able to drive sustainable growth (Zang, 2011). It works in all types of business

sectors, public as well as private sectors. It is helpful in managers in order to take financial and

non financial decision, and gives proper knowledge of how much money can be spent on sales

and how much its revenue.

Distinguish between management accounting and financial accounting:-

Management accounting is helpful in providing day to day or short term financial

decision, and its is relates with only internal environment. Although financial accounting

provides long term and annually year plans and strategics and it relates with external as

well as internal environment of Imda Tech limited.

Management accounting collate content regarding sales revenue, outstanding debts and

cash flow that produces timely reports and statements to inform about the daily activities

to the mangers (Michalski, 2012.). Financial accounting is accommodating in preparing

1

Management accounting is an activity of interpretation, analysing, communicating,

identifying and measuring in order to achieve organisational goals. This is also known as cost

accounting. It is the process managing financial reports and accounts that is able to provide

accurate and correct information and data. Managerial accounting is also helpful in making short

term or as well as day to day organisational operational. It provides annual budgets and income

& balance sheet statement, so that mangers can easily analysis their financial position and

performance in capital market (Briciu, Groza and Ganfalean, 2009). Basically these reports are

useful in showing sales revenue,capital expenditure,amount of order in hand, accounts receivable

and accounts payable, the statement are useful of internal analysis of the business organisation.

Managers can easily assessed their internal and external issues by which the behaviour of the

employees are effected. Management accounting and financial accpunti9ng bothy are the

essential tool of a commercial industries.

TASK 1

P1 (a) (i) Describe management accounting and how it is differentiate from financial accounting

Management accounting is the combination of finance, management and accounting by

which business techniques and skills added real value to any organisation. Management

accountant uses content of all types, not only just financial but also it inform and lead company's

strategy and able to drive sustainable growth (Zang, 2011). It works in all types of business

sectors, public as well as private sectors. It is helpful in managers in order to take financial and

non financial decision, and gives proper knowledge of how much money can be spent on sales

and how much its revenue.

Distinguish between management accounting and financial accounting:-

Management accounting is helpful in providing day to day or short term financial

decision, and its is relates with only internal environment. Although financial accounting

provides long term and annually year plans and strategics and it relates with external as

well as internal environment of Imda Tech limited.

Management accounting collate content regarding sales revenue, outstanding debts and

cash flow that produces timely reports and statements to inform about the daily activities

to the mangers (Michalski, 2012.). Financial accounting is accommodating in preparing

1

reports that are generally based on past experience, by using this managers can easily

take financial decisions for the future.

Management accounting is combines both financial and non financial information content

to draw a complete image of the organisation. It can be utilize to drive business success.

Financial management is the process of financial data only that can be used by other

functions of the organisation for example :- department managers.

(ii) Importance of management accounting

Management accounting is helpful to managers to assessed the internal and the external

environment of the organisation, that helps to identifies the issues and challenges of the

organisation. It reduces the chance risk and uncertainty by evaluate the market competitors. It is

fornicating of products as well as company financial profile in capital market (Bebbington,

Unerman and O'Dwyer, 2014). It gives accurate and aggregate information about divisions,

plants, products, operations, tasks and individual activities.

(b) Examine the types of management accounting system

The types of management accounting are as follows:- Cost accounting system – Cost accounting system is also called costing system. It is a

procedure to collecting, classifying, analysing, evaluating and allocating the various

methods control of costs and course of action. It main aim is to give suggestion to the

management regarding cost of the product and services, and tries to spent less money in

manufacturing process (Dechow, Myers and Shakespeare, 2010). It is usually used in

financial accounting, but it is primary element that can be used by mangers of Imda Tech

limited, in order to facilitate decision making process. All the kind of business such as

trading, manufacturing, and service requires the cost accounting that helps into track their

business. Inventory management system :- The system is helpful manages the overall inventory of

the company. It gives accurate advices to mangers, how much stock is to be keep in

business, how much is going to bes usages in production. It main goals to reduces

wastages and making production profitable. It focusses on how to provide good quality

products to the customers by reducing cost of production. Job costing system :- Job costing system is the part of cost accounting system. It is

assigning production costs for and individual products or services or may the bunch of

2

take financial decisions for the future.

Management accounting is combines both financial and non financial information content

to draw a complete image of the organisation. It can be utilize to drive business success.

Financial management is the process of financial data only that can be used by other

functions of the organisation for example :- department managers.

(ii) Importance of management accounting

Management accounting is helpful to managers to assessed the internal and the external

environment of the organisation, that helps to identifies the issues and challenges of the

organisation. It reduces the chance risk and uncertainty by evaluate the market competitors. It is

fornicating of products as well as company financial profile in capital market (Bebbington,

Unerman and O'Dwyer, 2014). It gives accurate and aggregate information about divisions,

plants, products, operations, tasks and individual activities.

(b) Examine the types of management accounting system

The types of management accounting are as follows:- Cost accounting system – Cost accounting system is also called costing system. It is a

procedure to collecting, classifying, analysing, evaluating and allocating the various

methods control of costs and course of action. It main aim is to give suggestion to the

management regarding cost of the product and services, and tries to spent less money in

manufacturing process (Dechow, Myers and Shakespeare, 2010). It is usually used in

financial accounting, but it is primary element that can be used by mangers of Imda Tech

limited, in order to facilitate decision making process. All the kind of business such as

trading, manufacturing, and service requires the cost accounting that helps into track their

business. Inventory management system :- The system is helpful manages the overall inventory of

the company. It gives accurate advices to mangers, how much stock is to be keep in

business, how much is going to bes usages in production. It main goals to reduces

wastages and making production profitable. It focusses on how to provide good quality

products to the customers by reducing cost of production. Job costing system :- Job costing system is the part of cost accounting system. It is

assigning production costs for and individual products or services or may the bunch of

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

products. Usually it can be only used when the manufacturing products are totally

different from each other (Gunny, 2010). It accumulated cost at small unit of business

organisation, and demands a appreciable amount of costing precision. It is allocation of

labour, material and overhead.

Price optimising system :- Price optimising system is relates with mathematical analysis

of the company, it is helpful in knowing how customer reacts to different prices of the

product.

M1

Management accounting is helpful in assessment of overall organisational financial

policies and strategics, so that the mangers can take decisions in day to day operations and for

short term decisions. It provides the internal as well as external analysis of the company in order

to figure out the problems and issues that are faced by internal environment (Cohen and Zarowin,

2010). Thus it can be only useful for the internal uses only and accommodating to change the

behaviour of the employees.

D1

Management accounting system and reporting is based on managerial decisions of the

company. By using this, any company can develops their financial plans and their strategics.

They provides annual reports and income statements in terms of balance sheet on the end of

financial year, that includes sales, net profit, purchases and gross profit (Hillier, Grinblatt and

Titman, 2011).

TASK 2

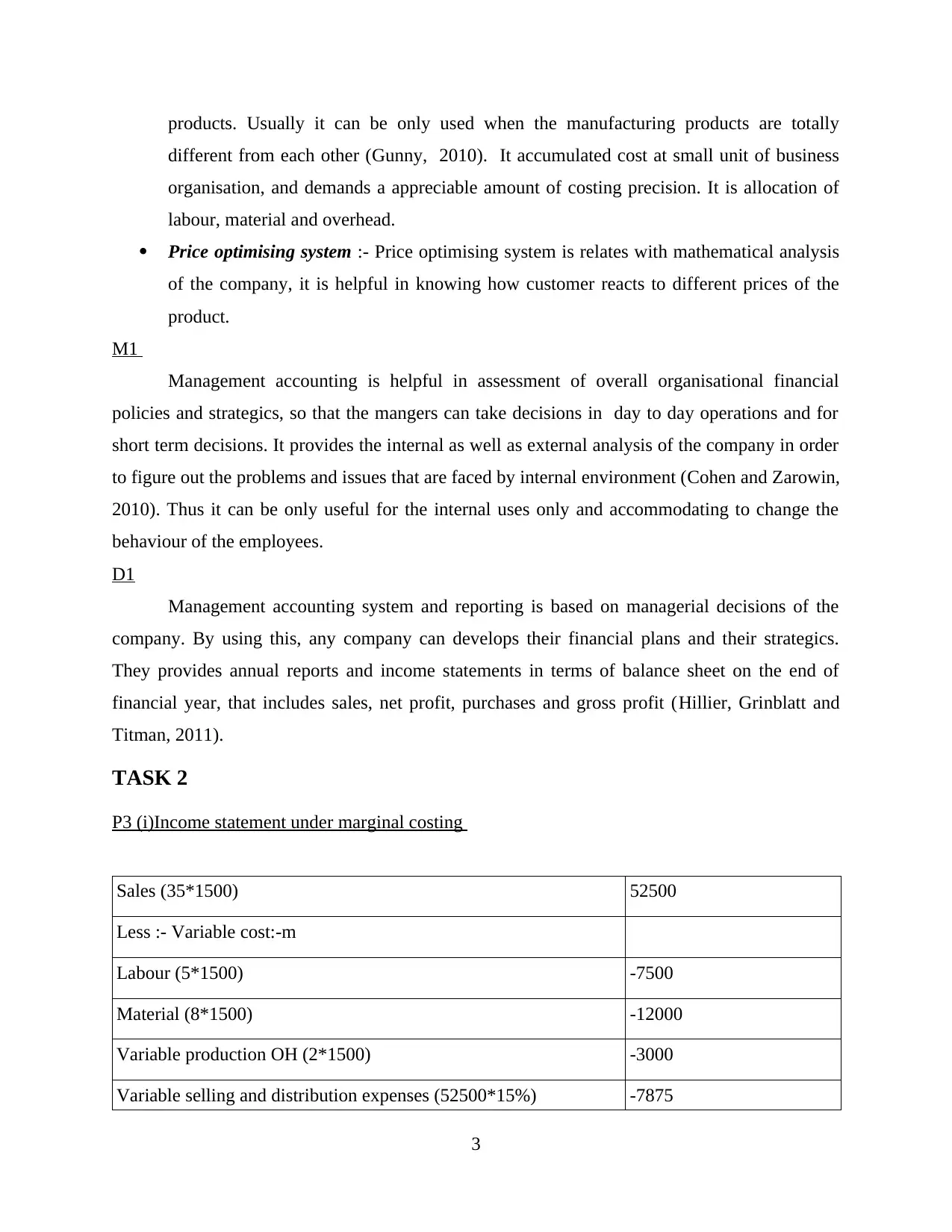

P3 (i)Income statement under marginal costing

Sales (35*1500) 52500

Less :- Variable cost:-m

Labour (5*1500) -7500

Material (8*1500) -12000

Variable production OH (2*1500) -3000

Variable selling and distribution expenses (52500*15%) -7875

3

different from each other (Gunny, 2010). It accumulated cost at small unit of business

organisation, and demands a appreciable amount of costing precision. It is allocation of

labour, material and overhead.

Price optimising system :- Price optimising system is relates with mathematical analysis

of the company, it is helpful in knowing how customer reacts to different prices of the

product.

M1

Management accounting is helpful in assessment of overall organisational financial

policies and strategics, so that the mangers can take decisions in day to day operations and for

short term decisions. It provides the internal as well as external analysis of the company in order

to figure out the problems and issues that are faced by internal environment (Cohen and Zarowin,

2010). Thus it can be only useful for the internal uses only and accommodating to change the

behaviour of the employees.

D1

Management accounting system and reporting is based on managerial decisions of the

company. By using this, any company can develops their financial plans and their strategics.

They provides annual reports and income statements in terms of balance sheet on the end of

financial year, that includes sales, net profit, purchases and gross profit (Hillier, Grinblatt and

Titman, 2011).

TASK 2

P3 (i)Income statement under marginal costing

Sales (35*1500) 52500

Less :- Variable cost:-m

Labour (5*1500) -7500

Material (8*1500) -12000

Variable production OH (2*1500) -3000

Variable selling and distribution expenses (52500*15%) -7875

3

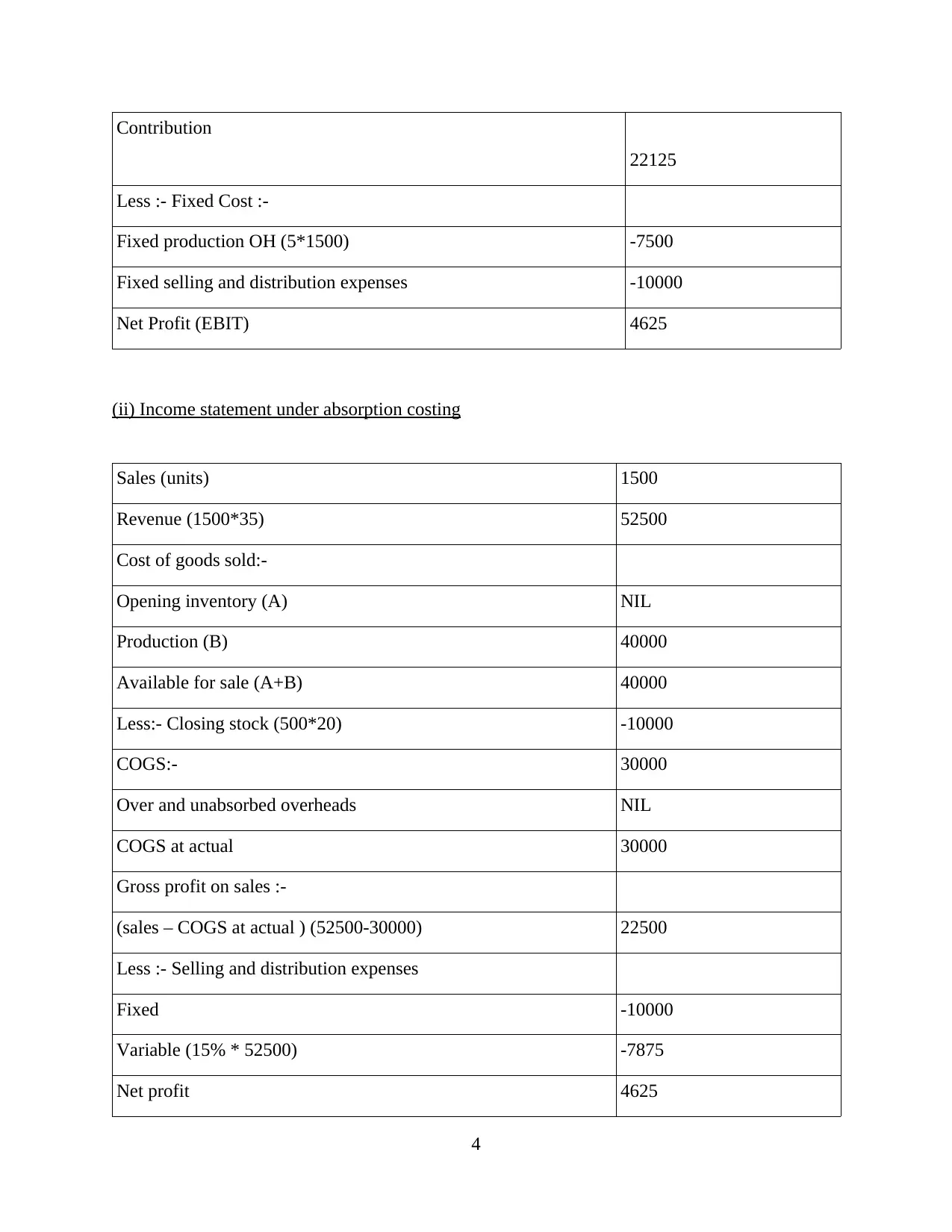

Contribution

22125

Less :- Fixed Cost :-

Fixed production OH (5*1500) -7500

Fixed selling and distribution expenses -10000

Net Profit (EBIT) 4625

(ii) Income statement under absorption costing

Sales (units) 1500

Revenue (1500*35) 52500

Cost of goods sold:-

Opening inventory (A) NIL

Production (B) 40000

Available for sale (A+B) 40000

Less:- Closing stock (500*20) -10000

COGS:- 30000

Over and unabsorbed overheads NIL

COGS at actual 30000

Gross profit on sales :-

(sales – COGS at actual ) (52500-30000) 22500

Less :- Selling and distribution expenses

Fixed -10000

Variable (15% * 52500) -7875

Net profit 4625

4

22125

Less :- Fixed Cost :-

Fixed production OH (5*1500) -7500

Fixed selling and distribution expenses -10000

Net Profit (EBIT) 4625

(ii) Income statement under absorption costing

Sales (units) 1500

Revenue (1500*35) 52500

Cost of goods sold:-

Opening inventory (A) NIL

Production (B) 40000

Available for sale (A+B) 40000

Less:- Closing stock (500*20) -10000

COGS:- 30000

Over and unabsorbed overheads NIL

COGS at actual 30000

Gross profit on sales :-

(sales – COGS at actual ) (52500-30000) 22500

Less :- Selling and distribution expenses

Fixed -10000

Variable (15% * 52500) -7875

Net profit 4625

4

M2

The tools and techniques of management accounting system, are helpful to figure out the

problems and challenges with external market. It gives an the overall analysis of capital market,

so that organisation makes their product capable in order to competition from another products.

They are helpful to compete with new entrants or competitors to the business organisation and

gives a new changes in the capital of business organisation (Burritt and Schaltegger, 2010). It is

makes easier to decide, how much money spent an dhow much profitable it is for organisational,

they are able to forecasting the company's financial position and its performance in external

market.

D2

Financial data and information are capable to analysis the economic conditions of the

business. It gives an flexible flow to the financial accounting, and make able to managers so that

they can use them in proper way. It makes communication effective and change the behaviour of

the employees in order to develop their performance. These data and information generally based

on past experience and gives effective suggestions to the mangers and make able those financial

decisions, so that they be can be easily implement in business organisation (Chandra, 2011).

With the help of accurate information and data, established flexibility in business decisions and

also manages the cash inflow and outflow of the Imda tech limited.

TASK 3

P4 (i)Different types of budgets and their advantages and disadvantages

An budgets is the financial statements if company's economic activities, it is an income

and expenditure estimate for a set time of period. There are many types of budgets, different

organization, choose them according to their choice and business type. There are mentioned

below main types of budgets, such are as :- Master budget :- It is an aggregate of organisation's individual budget, that is designed

to be a present the actual image of the company, for example :- its financial heath and

activities. This types of budgets is a combination of such factors like :- income streams,

assets, sales and operating expenses, these streams allows businesses to determines their

goals and analysis their performance and master budgets are rarely used in big and larger

5

The tools and techniques of management accounting system, are helpful to figure out the

problems and challenges with external market. It gives an the overall analysis of capital market,

so that organisation makes their product capable in order to competition from another products.

They are helpful to compete with new entrants or competitors to the business organisation and

gives a new changes in the capital of business organisation (Burritt and Schaltegger, 2010). It is

makes easier to decide, how much money spent an dhow much profitable it is for organisational,

they are able to forecasting the company's financial position and its performance in external

market.

D2

Financial data and information are capable to analysis the economic conditions of the

business. It gives an flexible flow to the financial accounting, and make able to managers so that

they can use them in proper way. It makes communication effective and change the behaviour of

the employees in order to develop their performance. These data and information generally based

on past experience and gives effective suggestions to the mangers and make able those financial

decisions, so that they be can be easily implement in business organisation (Chandra, 2011).

With the help of accurate information and data, established flexibility in business decisions and

also manages the cash inflow and outflow of the Imda tech limited.

TASK 3

P4 (i)Different types of budgets and their advantages and disadvantages

An budgets is the financial statements if company's economic activities, it is an income

and expenditure estimate for a set time of period. There are many types of budgets, different

organization, choose them according to their choice and business type. There are mentioned

below main types of budgets, such are as :- Master budget :- It is an aggregate of organisation's individual budget, that is designed

to be a present the actual image of the company, for example :- its financial heath and

activities. This types of budgets is a combination of such factors like :- income streams,

assets, sales and operating expenses, these streams allows businesses to determines their

goals and analysis their performance and master budgets are rarely used in big and larger

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation in order to keep aligned individual manages (Schaltegger and Burritt,

2010). Operational budget :- Operational budgets are helpful in forecasting the financial

conditions f the company. It is an evaluation of projected income & expenses for the

specific course of action for set time period. It creates accurate shape of the organisation,

and it must account for factors such as labour cost, production, sales, material cost and

overhead or manufacturing cost. They are generally create don monthly or weekly basis.

Financial budget :- Financial budget is helpful in presents company's strategics and

policies, it also effects on short term as well as long term decisions of the company, that

is related with assets, income, expenses and cash flow. Financial budget put an impact

on operations and decision making process of the company.

(ii) Process of preparing budgets

Every company has create their own budgets that involves their income and expenses. In

order to create an effective budget Imda Tech limited have to put certain steps, such are as :-

Firstly company has update the overall information regarding sales and production so that it can

easily reduces wastage and further expenses. After that managers have to analyse that how much

funds they have fr the budget making process. In several companies, budget committees

assessed the various plans and policies deposited by different organisational units in order to

find out the possibilities of plans in the whole interest of the company and to compute what kind

of resources are available and also they can fairy allocated between the various groups of the

organisation. After that managers have to communicate the budget among all over the

employees, it is necessary that the prepare budgets is a also fulfils their demands. If their is any

to change and modification in final budget, that is should be made by the managers in order to

obtained their coordination and cooperation for the budgets. Because budgeting requires

effectual communication so that employees can easily convince to the departmental manger

about any changes (Renz, 2016). The final budget is ready to implement in organisation and

adopted as the strategy of activities for the future coming financial period. The different service

units in a commercial enterprise are requisite to provide the essential materials, facilities, labour

and other resources that are able to carry out the budget.

6

2010). Operational budget :- Operational budgets are helpful in forecasting the financial

conditions f the company. It is an evaluation of projected income & expenses for the

specific course of action for set time period. It creates accurate shape of the organisation,

and it must account for factors such as labour cost, production, sales, material cost and

overhead or manufacturing cost. They are generally create don monthly or weekly basis.

Financial budget :- Financial budget is helpful in presents company's strategics and

policies, it also effects on short term as well as long term decisions of the company, that

is related with assets, income, expenses and cash flow. Financial budget put an impact

on operations and decision making process of the company.

(ii) Process of preparing budgets

Every company has create their own budgets that involves their income and expenses. In

order to create an effective budget Imda Tech limited have to put certain steps, such are as :-

Firstly company has update the overall information regarding sales and production so that it can

easily reduces wastage and further expenses. After that managers have to analyse that how much

funds they have fr the budget making process. In several companies, budget committees

assessed the various plans and policies deposited by different organisational units in order to

find out the possibilities of plans in the whole interest of the company and to compute what kind

of resources are available and also they can fairy allocated between the various groups of the

organisation. After that managers have to communicate the budget among all over the

employees, it is necessary that the prepare budgets is a also fulfils their demands. If their is any

to change and modification in final budget, that is should be made by the managers in order to

obtained their coordination and cooperation for the budgets. Because budgeting requires

effectual communication so that employees can easily convince to the departmental manger

about any changes (Renz, 2016). The final budget is ready to implement in organisation and

adopted as the strategy of activities for the future coming financial period. The different service

units in a commercial enterprise are requisite to provide the essential materials, facilities, labour

and other resources that are able to carry out the budget.

6

(iii) What are pricing strategics

Pricing strategics are those that can used as a variety when selling any goods or service.

The prices can be change in order to increases profit and develop the growth of the company.

Price of the product is always depends on its demands and needs of the product in market. If the

products is demand able, so its prices are automatically increases and if product is not in demand,

so its prices are automatically decreases. Pricing is the one of highly demanded or vital element

in the marketing mix theory (Bodie, 2013). The business decision on prices is always impacts on

customer decisions in order to choose their product or not. It develops competition among

companies for same product.

M3

Planning is necessary for every organisation, it gives strengths and many opportunities to

it. Without any planning no one business will be succeed and cannot achieves its targets.

Planning is the pre determination of company's goals and aims, and it also describes that where a

company is and where is wants to go. It means it is future scenario of the company, that is relates

with policies and strategics. In management accounting, planning helps in assessment of

financial conditions of the company , it involves income and balance sheet statemented or profit

or loss statement as well also.

D3

Planning tools and techniques are helpful in decision making process of the company. They are

able to provide managers an effective and sufficient solution of the problem. These techniques

are able to analyse the overall evaluation of internal and external market, that impact on

employees behaviour. These planning tools are able to provide organisation, its capabilities, so

that it can easily compete with new entrants of the external market. It can easily identifies the

issues and challenges, after that make appropriate solution so that they cannot effect

organisational success and its growth. Planing tools are always based on financial situation of the

business enterprise.

TASK 4

P5 (i) What is balance scorecard and how it is useful in respond to financial problems

Balance scorecard is a strategic planning that is used by managers in order to align

business activities and functions. It is helpful to managing the organisation better at every level

7

Pricing strategics are those that can used as a variety when selling any goods or service.

The prices can be change in order to increases profit and develop the growth of the company.

Price of the product is always depends on its demands and needs of the product in market. If the

products is demand able, so its prices are automatically increases and if product is not in demand,

so its prices are automatically decreases. Pricing is the one of highly demanded or vital element

in the marketing mix theory (Bodie, 2013). The business decision on prices is always impacts on

customer decisions in order to choose their product or not. It develops competition among

companies for same product.

M3

Planning is necessary for every organisation, it gives strengths and many opportunities to

it. Without any planning no one business will be succeed and cannot achieves its targets.

Planning is the pre determination of company's goals and aims, and it also describes that where a

company is and where is wants to go. It means it is future scenario of the company, that is relates

with policies and strategics. In management accounting, planning helps in assessment of

financial conditions of the company , it involves income and balance sheet statemented or profit

or loss statement as well also.

D3

Planning tools and techniques are helpful in decision making process of the company. They are

able to provide managers an effective and sufficient solution of the problem. These techniques

are able to analyse the overall evaluation of internal and external market, that impact on

employees behaviour. These planning tools are able to provide organisation, its capabilities, so

that it can easily compete with new entrants of the external market. It can easily identifies the

issues and challenges, after that make appropriate solution so that they cannot effect

organisational success and its growth. Planing tools are always based on financial situation of the

business enterprise.

TASK 4

P5 (i) What is balance scorecard and how it is useful in respond to financial problems

Balance scorecard is a strategic planning that is used by managers in order to align

business activities and functions. It is helpful to managing the organisation better at every level

7

to achieve its goals and objectives. Balance scorecard is a company's mission statement as well

as a strategic plan. It focus on how day to day activities can support missions or vision of

business organisation. Along with this, managers can be used it to evaluate financial condition

of business organisation and level of customer satisfaction. In Imda Tech Ltd, balance scorecards

are pertain as a performance management tool which can measure employees performance and

their productivity. It is a semi-structured report which is developed by various automation tools

and designing methods.

Use of balance scorecards : -

The main use of that it is helpful in order to provide feedbacks and reviews to business

organisation. It is helpful to attain goals, initiatives, objectives, targets and measurements of

firm. Managers of Imda Tech are using Balance scorecards because it aids in implementing

strategies and policies to see where value is added in their firm. Balance scorecards also helps in

aligning key performance measurements at every level of company. It is capable to provide a

comprehensive picture of business operations to managers as they can analyse market image of

their business organisation (Zang, 2011). Balance scorecards also helpful in increases creativity

and innovation for managers as they can easily understand business goals. The methodology

supports to facilitates communication among managers and employees as they can easily

cooperation and coordination in business functions.

Importance of balance scorecards in financial perspective: -

The balanced scorecards also can be used in financial performance measures, i.e. return

on investments, net income; because IMDA tech and all another business organisations are use

them. Along with this, BSC also helps managers to implement financial strategic objectives and

to evaluate the processes in order to achieve them. Financial perspective is recognized for the

importance of short term financial results which are obtain from the analysis of financial targets

for companies in competitive market.

It is the most essential work of balance scorecards to improve financial services of

business organisation by regulating effective strategies and policies. There are four legs of

balance scorecards that can be used in information collection and evaluation. Below mentioned

four perspectives of balance scorecard: -

Customer's perspective – Balance scorecards can be used to know the level of customer's

satisfaction. In today's scenario it is the mission of many firms to focus on customers

8

as a strategic plan. It focus on how day to day activities can support missions or vision of

business organisation. Along with this, managers can be used it to evaluate financial condition

of business organisation and level of customer satisfaction. In Imda Tech Ltd, balance scorecards

are pertain as a performance management tool which can measure employees performance and

their productivity. It is a semi-structured report which is developed by various automation tools

and designing methods.

Use of balance scorecards : -

The main use of that it is helpful in order to provide feedbacks and reviews to business

organisation. It is helpful to attain goals, initiatives, objectives, targets and measurements of

firm. Managers of Imda Tech are using Balance scorecards because it aids in implementing

strategies and policies to see where value is added in their firm. Balance scorecards also helps in

aligning key performance measurements at every level of company. It is capable to provide a

comprehensive picture of business operations to managers as they can analyse market image of

their business organisation (Zang, 2011). Balance scorecards also helpful in increases creativity

and innovation for managers as they can easily understand business goals. The methodology

supports to facilitates communication among managers and employees as they can easily

cooperation and coordination in business functions.

Importance of balance scorecards in financial perspective: -

The balanced scorecards also can be used in financial performance measures, i.e. return

on investments, net income; because IMDA tech and all another business organisations are use

them. Along with this, BSC also helps managers to implement financial strategic objectives and

to evaluate the processes in order to achieve them. Financial perspective is recognized for the

importance of short term financial results which are obtain from the analysis of financial targets

for companies in competitive market.

It is the most essential work of balance scorecards to improve financial services of

business organisation by regulating effective strategies and policies. There are four legs of

balance scorecards that can be used in information collection and evaluation. Below mentioned

four perspectives of balance scorecard: -

Customer's perspective – Balance scorecards can be used to know the level of customer's

satisfaction. In today's scenario it is the mission of many firms to focus on customers

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

needs and wants. It is essential to deliver quality products and services to buyers in order

to accomplish goals and objectives (Zadek, Evans and Pruzan, 2013). Consumers provide

reviews and feedbacks if their needs are being met with goods and services that are

offered by firm.

Financial perspective – Managers are used balance scorecards in order to get financial

data and information. Typically financial objectives have to do with growth, profitability

and shareholder value. Financial perspective is helpful to measure company's strategy

that is executed for bottom line improvement.

Internal business perspective – Managers have to focus on internal critical operation and

activities that are enable to fulfil customers needs and wants. If managers wants excellent

customers satisfaction as they need to develop their current process and actions. In

context of balance scorecards, internal perspective includes- employees skills, production

cycle time, quality & quantity of products.

Innovation and learning perspective – Balance scorecards are accommodating to generate

new ideas and innovation through which managers can improvise their existing strategies

and policies (Schaltegger and Burritt, 2010). If Imda Tech is using innovative tools and

techniques, it helps in developing their productivity. Apart from this, learning perspective

required to provide training and development assistance to employees as they can

increases their skills and knowledge.

M4

Financial problems and issues are the main components by which organisational success

can be effective. With the help of management accounting, managerial accountants can easily get

rid of all those problems and issues. Because management accounting is a source of financial

success and its growth. It gives accurate and relevant financial information to the managers, by

using that leaders can easily analyse the future conditions of the market. It deals with financial

and non – financial aspects of accounting in order to develop organisation's profit and its profit

as well. Management accounting is the cure of all financial problems in order to keep all

financial information and contents.

CONCLUSION

From the above mentioned report is based upon management accounting, that means how

companies can manges their financial data and information in order to improve their financial

9

to accomplish goals and objectives (Zadek, Evans and Pruzan, 2013). Consumers provide

reviews and feedbacks if their needs are being met with goods and services that are

offered by firm.

Financial perspective – Managers are used balance scorecards in order to get financial

data and information. Typically financial objectives have to do with growth, profitability

and shareholder value. Financial perspective is helpful to measure company's strategy

that is executed for bottom line improvement.

Internal business perspective – Managers have to focus on internal critical operation and

activities that are enable to fulfil customers needs and wants. If managers wants excellent

customers satisfaction as they need to develop their current process and actions. In

context of balance scorecards, internal perspective includes- employees skills, production

cycle time, quality & quantity of products.

Innovation and learning perspective – Balance scorecards are accommodating to generate

new ideas and innovation through which managers can improvise their existing strategies

and policies (Schaltegger and Burritt, 2010). If Imda Tech is using innovative tools and

techniques, it helps in developing their productivity. Apart from this, learning perspective

required to provide training and development assistance to employees as they can

increases their skills and knowledge.

M4

Financial problems and issues are the main components by which organisational success

can be effective. With the help of management accounting, managerial accountants can easily get

rid of all those problems and issues. Because management accounting is a source of financial

success and its growth. It gives accurate and relevant financial information to the managers, by

using that leaders can easily analyse the future conditions of the market. It deals with financial

and non – financial aspects of accounting in order to develop organisation's profit and its profit

as well. Management accounting is the cure of all financial problems in order to keep all

financial information and contents.

CONCLUSION

From the above mentioned report is based upon management accounting, that means how

companies can manges their financial data and information in order to improve their financial

9

stability and growth. In the report is also has be concluded that how financial accounting keep

income and expenses or balance sheet statements of the company. On the other hands, budgets

are also useful in making financial decisions or making any strategics and policies that can be

increase their sales revenue. There five types of budgets :- operational, master, financial budgets,

that can be choose by the organisation that fulfils their all financial needs.

REFERENCES

Books and Journal

Badertscher, B.A., 2011. Overvaluation and the choice of alternative earnings management

mechanisms. The Accounting Review. 86(5). pp.1491-1518.

Bebbington, J., Unerman, J. and O'Dwyer, B., 2014. Sustainability accounting and

accountability. Routledge.

Bodie, Z., 2013. Investments. McGraw-Hill.

Briciu, S., Groza, C. and Ganfalean, I., 2009. International Financial Reporting Standard (Ifrs)

Will Support Managemnet Accounting System For Small And Medium Entreprise

(Sme)?. Annales Universitatis Apulensis: Series Oeconomica. 11(1). p.308.

Burritt, R.L. and Schaltegger, S., 2010. Sustainability accounting and reporting: fad or trend?.

Accounting, Auditing & Accountability Journal. 23(7). pp.829-846.

Chandra, P., 2011. Financial management. Tata McGraw-Hill Education.

Cohen, D.A. and Zarowin, P., 2010. Accrual-based and real earnings management activities

around seasoned equity offerings. Journal of Accounting and Economics. 50(1). pp.2-

19.

10

income and expenses or balance sheet statements of the company. On the other hands, budgets

are also useful in making financial decisions or making any strategics and policies that can be

increase their sales revenue. There five types of budgets :- operational, master, financial budgets,

that can be choose by the organisation that fulfils their all financial needs.

REFERENCES

Books and Journal

Badertscher, B.A., 2011. Overvaluation and the choice of alternative earnings management

mechanisms. The Accounting Review. 86(5). pp.1491-1518.

Bebbington, J., Unerman, J. and O'Dwyer, B., 2014. Sustainability accounting and

accountability. Routledge.

Bodie, Z., 2013. Investments. McGraw-Hill.

Briciu, S., Groza, C. and Ganfalean, I., 2009. International Financial Reporting Standard (Ifrs)

Will Support Managemnet Accounting System For Small And Medium Entreprise

(Sme)?. Annales Universitatis Apulensis: Series Oeconomica. 11(1). p.308.

Burritt, R.L. and Schaltegger, S., 2010. Sustainability accounting and reporting: fad or trend?.

Accounting, Auditing & Accountability Journal. 23(7). pp.829-846.

Chandra, P., 2011. Financial management. Tata McGraw-Hill Education.

Cohen, D.A. and Zarowin, P., 2010. Accrual-based and real earnings management activities

around seasoned equity offerings. Journal of Accounting and Economics. 50(1). pp.2-

19.

10

Dechow, P.M., Myers, L.A. and Shakespeare, C., 2010. Fair value accounting and gains from

asset securitizations: A convenient earnings management tool with compensation side-

benefits. Journal of accounting and economics. 49(1). pp.2-25.

Easterby-Smith, M., Thorpe, R. and Jackson, P.R., 2012. Management research. Sage.

Gunny, K.A., 2010. The relation between earnings management using real activities

manipulation and future performance: Evidence from meeting earnings benchmarks.

Contemporary Accounting Research. 27(3). pp.855-888.

Hillier, D., Grinblatt, M. and Titman, S., 2011. Financial markets and corporate strategy.

McGraw Hill.

Michalski, G., 2012. Accounts receivable management in nonprofit organizations. Zeszyty

Teoretyczne Rachunkowości. (68). pp.83-96.

Myers, M.D., 2013. Qualitative research in business and management. Sage.

Renz, D.O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Schaltegger, S. and Burritt, R.L., 2010. Sustainability accounting for companies: Catchphrase or

decision support for business leaders?. Journal of World Business. 45(4). pp.375-384.

Zadek, S., Evans, R. and Pruzan, P., 2013. Building corporate accountability: Emerging practice

in social and ethical accounting and auditing. Routledge.

Zang, A.Y., 2011. Evidence on the trade-off between real activities manipulation and accrual-

based earnings management. The Accounting Review. 87(2). pp.675-703.

Online

WHAT IS MANAGEMENT ACCOUNTING?. 2017. [Online]. Available through:

<http://www.cgma.org/aboutcgma/whatiscgma.html>. [Accessed on 24th April 2017].

What Are Financial Management Objectives?. 2017. [Online]. Availabe

through:<http://smallbusiness.chron.com/financial-management-objectives-4725.html>.

[Accessed on 24th April 2017].

11

asset securitizations: A convenient earnings management tool with compensation side-

benefits. Journal of accounting and economics. 49(1). pp.2-25.

Easterby-Smith, M., Thorpe, R. and Jackson, P.R., 2012. Management research. Sage.

Gunny, K.A., 2010. The relation between earnings management using real activities

manipulation and future performance: Evidence from meeting earnings benchmarks.

Contemporary Accounting Research. 27(3). pp.855-888.

Hillier, D., Grinblatt, M. and Titman, S., 2011. Financial markets and corporate strategy.

McGraw Hill.

Michalski, G., 2012. Accounts receivable management in nonprofit organizations. Zeszyty

Teoretyczne Rachunkowości. (68). pp.83-96.

Myers, M.D., 2013. Qualitative research in business and management. Sage.

Renz, D.O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Schaltegger, S. and Burritt, R.L., 2010. Sustainability accounting for companies: Catchphrase or

decision support for business leaders?. Journal of World Business. 45(4). pp.375-384.

Zadek, S., Evans, R. and Pruzan, P., 2013. Building corporate accountability: Emerging practice

in social and ethical accounting and auditing. Routledge.

Zang, A.Y., 2011. Evidence on the trade-off between real activities manipulation and accrual-

based earnings management. The Accounting Review. 87(2). pp.675-703.

Online

WHAT IS MANAGEMENT ACCOUNTING?. 2017. [Online]. Available through:

<http://www.cgma.org/aboutcgma/whatiscgma.html>. [Accessed on 24th April 2017].

What Are Financial Management Objectives?. 2017. [Online]. Availabe

through:<http://smallbusiness.chron.com/financial-management-objectives-4725.html>.

[Accessed on 24th April 2017].

11

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.