Financial Accounting: Types of Business Transactions, Financial Statements vs Financial Reports, Users of Financial Reporting

VerifiedAdded on 2023/01/10

|18

|4507

|73

AI Summary

This document provides an introduction to financial accounting, covering topics such as types of business transactions, the difference between financial statements and financial reports, and the users of financial reporting. It includes explanations, examples, and ledger accounts for better understanding. The subject is Financial Accounting, and the course code is not mentioned. The document type is an assignment, and the assignment type is not mentioned. The college/university is not mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Scenario 1........................................................................................................................................1

Question 1....................................................................................................................................1

What are the different types of business transaction...................................................................1

Question 2....................................................................................................................................3

Question 3....................................................................................................................................7

Explain the difference between financial statement and financial report, why these reports are

required and who are the different users......................................................................................7

Question 4....................................................................................................................................8

Explain different fundamental principles of accounting.............................................................8

Question 5....................................................................................................................................9

Scenario 2......................................................................................................................................10

Question 1..................................................................................................................................10

What is meant by bank reconciliation and why is it required? How is this achieved? Why is

this necessary.............................................................................................................................10

Question 2..................................................................................................................................11

What are control accounts? Explain the role of control accounts in financial management.....11

Question 3..................................................................................................................................12

Suspense account and the reasons for drafting suspense accounts............................................12

Question 4..................................................................................................................................12

(a) Required to prepare updated cash book and bank reconciliation statement.........................12

(b) Explain the following terms.................................................................................................13

Question 5..................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

MAIN BODY..................................................................................................................................1

Scenario 1........................................................................................................................................1

Question 1....................................................................................................................................1

What are the different types of business transaction...................................................................1

Question 2....................................................................................................................................3

Question 3....................................................................................................................................7

Explain the difference between financial statement and financial report, why these reports are

required and who are the different users......................................................................................7

Question 4....................................................................................................................................8

Explain different fundamental principles of accounting.............................................................8

Question 5....................................................................................................................................9

Scenario 2......................................................................................................................................10

Question 1..................................................................................................................................10

What is meant by bank reconciliation and why is it required? How is this achieved? Why is

this necessary.............................................................................................................................10

Question 2..................................................................................................................................11

What are control accounts? Explain the role of control accounts in financial management.....11

Question 3..................................................................................................................................12

Suspense account and the reasons for drafting suspense accounts............................................12

Question 4..................................................................................................................................12

(a) Required to prepare updated cash book and bank reconciliation statement.........................12

(b) Explain the following terms.................................................................................................13

Question 5..................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Financial accounting is a specialist accounting division that maintains records of cash

activities within a business (Chan, 2015). The transactions are recorded, summarized, and

statement of revenue or financial statement, such as a statement of cash flows or a balance sheet,

utilizing standardized guidance. For the better understanding of financial accounts, Brightstar

Financial Company selected which is UK based small accountancy firm. This report is

determined by different task of recording business transactions in terms of journals, ledger, trial

balance and producing final accounts with different business types. Additionally, this report

needed a bank reconciliation to recognise whether or not bank statements are correct.

MAIN BODY

Scenario 1

Question 1

What are the different types of business transaction

There are several types of business transactions which applied in single and double entry

bookkeeping. Basically it has four major types which are as follow:

Sales: This sale is performed by business in which they sell their products & services to

some other entity and give the money back to the customer or may buy items on credit. Both

selling transactions reported in account books and then further it is analyzed for reporting

purposes to render journals and other records. Purchasers will debit in this transaction, and sales

accounts will be credited.

Purchase: Where any items are bought by an agency or person, this activity falls under

transactions (Drexler, Fischer and Schoar, 2014). If the company buys something and the

payment will be documented as the purchase account debit and the individual or creditor to

whom people purchased would be credited. Such practice is often performed in cash or on the

basis of credit. Further this transaction recorded in the books of accounts for reporting purpose.

Receipts: When a company is paying for providing goods or services to another entity,

these fees apply to other companies or persons. Further such sales are registered in newspapers

where dealers are charged to trade receivables as debit and cash or credit payment.

1

Financial accounting is a specialist accounting division that maintains records of cash

activities within a business (Chan, 2015). The transactions are recorded, summarized, and

statement of revenue or financial statement, such as a statement of cash flows or a balance sheet,

utilizing standardized guidance. For the better understanding of financial accounts, Brightstar

Financial Company selected which is UK based small accountancy firm. This report is

determined by different task of recording business transactions in terms of journals, ledger, trial

balance and producing final accounts with different business types. Additionally, this report

needed a bank reconciliation to recognise whether or not bank statements are correct.

MAIN BODY

Scenario 1

Question 1

What are the different types of business transaction

There are several types of business transactions which applied in single and double entry

bookkeeping. Basically it has four major types which are as follow:

Sales: This sale is performed by business in which they sell their products & services to

some other entity and give the money back to the customer or may buy items on credit. Both

selling transactions reported in account books and then further it is analyzed for reporting

purposes to render journals and other records. Purchasers will debit in this transaction, and sales

accounts will be credited.

Purchase: Where any items are bought by an agency or person, this activity falls under

transactions (Drexler, Fischer and Schoar, 2014). If the company buys something and the

payment will be documented as the purchase account debit and the individual or creditor to

whom people purchased would be credited. Such practice is often performed in cash or on the

basis of credit. Further this transaction recorded in the books of accounts for reporting purpose.

Receipts: When a company is paying for providing goods or services to another entity,

these fees apply to other companies or persons. Further such sales are registered in newspapers

where dealers are charged to trade receivables as debit and cash or credit payment.

1

Payments: This contains business activities where organizations have to spend on other

parties in credit or cash terms. These would be recorded in accounting records and are further

prepared for reporting purposes by journals. Expenditures are debit and earnings paid to another

group.

Single-entry book keeping: If the company is very short and simple with little operational

activities. This truly is like having that own personal chequebook. Company is using single-entry

bookkeeping in order to maintain a list of purchases such as currency, tax-deductible

expenditures and taxable income. Single-entry bookkeeping, as in the check ledger, is defined by

the fact that only one record is made on each activity. Entries are reported in one column as

either a positive or a negative number. They should simply maintain a two-column register in

single-entry book keeping, one column for income and one for expenditures. It is still considered

single-entry, even though for each transaction, there is only one line.

Double-entry book keeping: Many corporations, including the bulk of small firms, use

dual-entry bookkeeping for the financial requirements (Jiang, Wang and Xie, 2015). Two

features of book keeping with double entry where each account has two columns and that each

sale is in two books. With each sale, two transactions are rendered as a deduction in one account

and a add-up in another. If the business needs to spend on creditor, one example of a double-

entry transaction would be. The volume the company owes the creditor would cut the

cash account balance where debit the cash account. Instead, the double-entry eliminates the

money that the company actually charges to the borrower account because it has earned the

amount of credit that the company is expanding and account will be credited.

Trial balance and its importance:

A Ledger will be formed by multiple entries in different accounts. It is Trial Balance to

take all the ledger balances and show them in a single worksheet as on a given date. Group

reviews its transactions at the month-end and classifies them into separate groups. They are now

making a sheet and splitting the groups into effective / non effective.

The importance of a trial balance is to ensure adequate accounting of all transactions

recorded into the ledger accounts of a company. Within every general ledger account a trial

balance reports the starting balance. The actual number of the debit and credit balances in each

accounting entry should match with each other.

2

parties in credit or cash terms. These would be recorded in accounting records and are further

prepared for reporting purposes by journals. Expenditures are debit and earnings paid to another

group.

Single-entry book keeping: If the company is very short and simple with little operational

activities. This truly is like having that own personal chequebook. Company is using single-entry

bookkeeping in order to maintain a list of purchases such as currency, tax-deductible

expenditures and taxable income. Single-entry bookkeeping, as in the check ledger, is defined by

the fact that only one record is made on each activity. Entries are reported in one column as

either a positive or a negative number. They should simply maintain a two-column register in

single-entry book keeping, one column for income and one for expenditures. It is still considered

single-entry, even though for each transaction, there is only one line.

Double-entry book keeping: Many corporations, including the bulk of small firms, use

dual-entry bookkeeping for the financial requirements (Jiang, Wang and Xie, 2015). Two

features of book keeping with double entry where each account has two columns and that each

sale is in two books. With each sale, two transactions are rendered as a deduction in one account

and a add-up in another. If the business needs to spend on creditor, one example of a double-

entry transaction would be. The volume the company owes the creditor would cut the

cash account balance where debit the cash account. Instead, the double-entry eliminates the

money that the company actually charges to the borrower account because it has earned the

amount of credit that the company is expanding and account will be credited.

Trial balance and its importance:

A Ledger will be formed by multiple entries in different accounts. It is Trial Balance to

take all the ledger balances and show them in a single worksheet as on a given date. Group

reviews its transactions at the month-end and classifies them into separate groups. They are now

making a sheet and splitting the groups into effective / non effective.

The importance of a trial balance is to ensure adequate accounting of all transactions

recorded into the ledger accounts of a company. Within every general ledger account a trial

balance reports the starting balance. The actual number of the debit and credit balances in each

accounting entry should match with each other.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

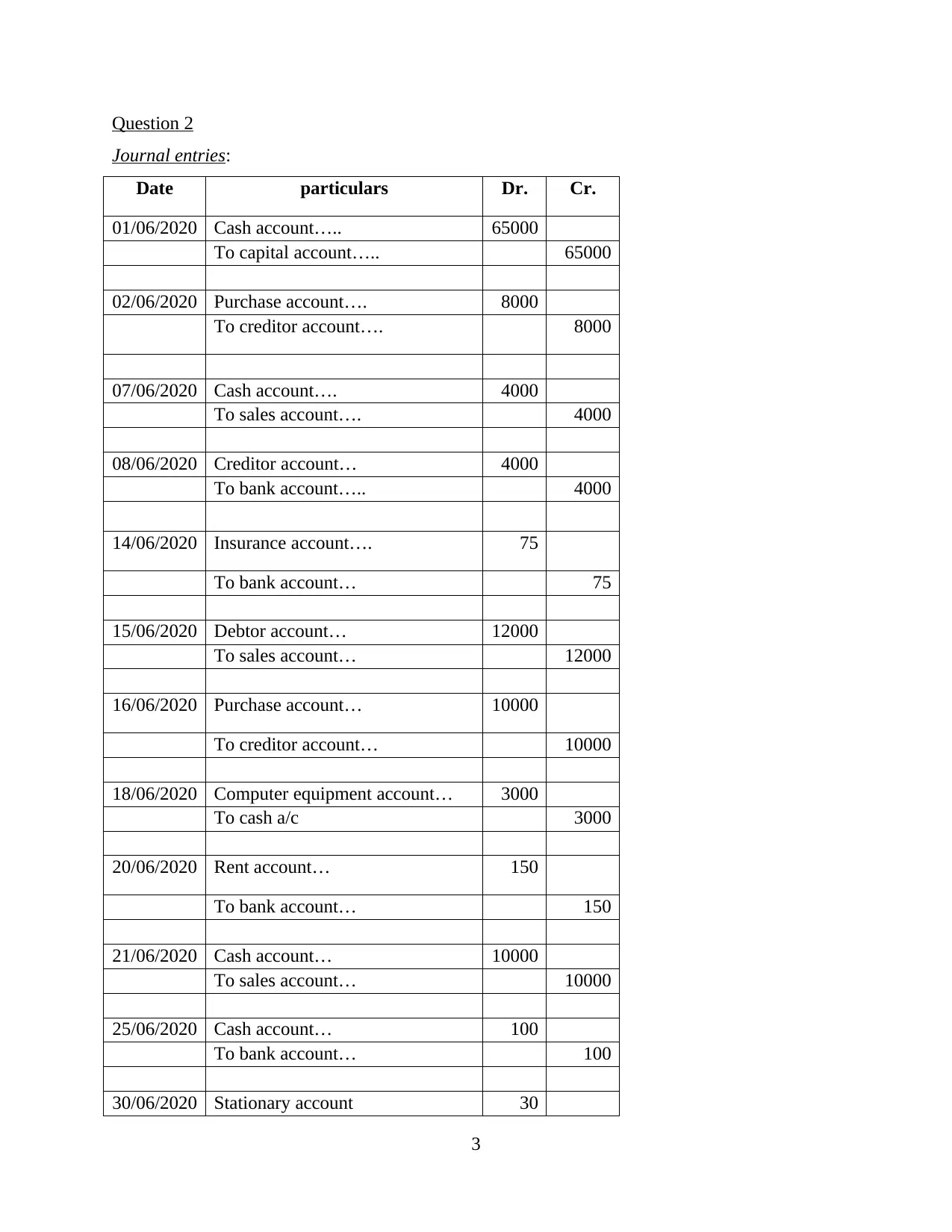

Question 2

Journal entries:

Date particulars Dr. Cr.

01/06/2020 Cash account….. 65000

To capital account….. 65000

02/06/2020 Purchase account…. 8000

To creditor account…. 8000

07/06/2020 Cash account…. 4000

To sales account…. 4000

08/06/2020 Creditor account… 4000

To bank account….. 4000

14/06/2020 Insurance account…. 75

To bank account… 75

15/06/2020 Debtor account… 12000

To sales account… 12000

16/06/2020 Purchase account… 10000

To creditor account… 10000

18/06/2020 Computer equipment account… 3000

To cash a/c 3000

20/06/2020 Rent account… 150

To bank account… 150

21/06/2020 Cash account… 10000

To sales account… 10000

25/06/2020 Cash account… 100

To bank account… 100

30/06/2020 Stationary account 30

3

Journal entries:

Date particulars Dr. Cr.

01/06/2020 Cash account….. 65000

To capital account….. 65000

02/06/2020 Purchase account…. 8000

To creditor account…. 8000

07/06/2020 Cash account…. 4000

To sales account…. 4000

08/06/2020 Creditor account… 4000

To bank account….. 4000

14/06/2020 Insurance account…. 75

To bank account… 75

15/06/2020 Debtor account… 12000

To sales account… 12000

16/06/2020 Purchase account… 10000

To creditor account… 10000

18/06/2020 Computer equipment account… 3000

To cash a/c 3000

20/06/2020 Rent account… 150

To bank account… 150

21/06/2020 Cash account… 10000

To sales account… 10000

25/06/2020 Cash account… 100

To bank account… 100

30/06/2020 Stationary account 30

3

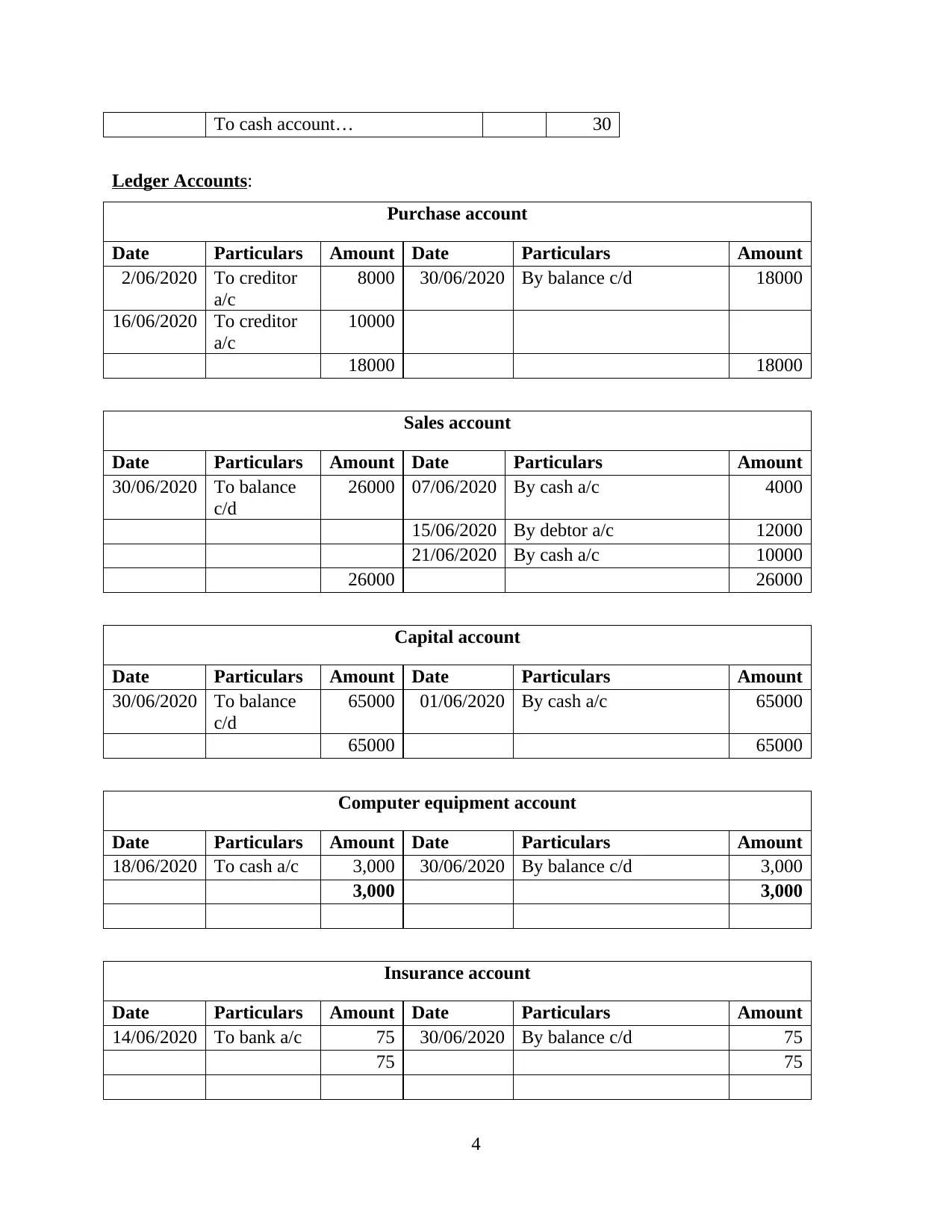

To cash account… 30

Ledger Accounts:

Purchase account

Date Particulars Amount Date Particulars Amount

2/06/2020 To creditor

a/c

8000 30/06/2020 By balance c/d 18000

16/06/2020 To creditor

a/c

10000

18000 18000

Sales account

Date Particulars Amount Date Particulars Amount

30/06/2020 To balance

c/d

26000 07/06/2020 By cash a/c 4000

15/06/2020 By debtor a/c 12000

21/06/2020 By cash a/c 10000

26000 26000

Capital account

Date Particulars Amount Date Particulars Amount

30/06/2020 To balance

c/d

65000 01/06/2020 By cash a/c 65000

65000 65000

Computer equipment account

Date Particulars Amount Date Particulars Amount

18/06/2020 To cash a/c 3,000 30/06/2020 By balance c/d 3,000

3,000 3,000

Insurance account

Date Particulars Amount Date Particulars Amount

14/06/2020 To bank a/c 75 30/06/2020 By balance c/d 75

75 75

4

Ledger Accounts:

Purchase account

Date Particulars Amount Date Particulars Amount

2/06/2020 To creditor

a/c

8000 30/06/2020 By balance c/d 18000

16/06/2020 To creditor

a/c

10000

18000 18000

Sales account

Date Particulars Amount Date Particulars Amount

30/06/2020 To balance

c/d

26000 07/06/2020 By cash a/c 4000

15/06/2020 By debtor a/c 12000

21/06/2020 By cash a/c 10000

26000 26000

Capital account

Date Particulars Amount Date Particulars Amount

30/06/2020 To balance

c/d

65000 01/06/2020 By cash a/c 65000

65000 65000

Computer equipment account

Date Particulars Amount Date Particulars Amount

18/06/2020 To cash a/c 3,000 30/06/2020 By balance c/d 3,000

3,000 3,000

Insurance account

Date Particulars Amount Date Particulars Amount

14/06/2020 To bank a/c 75 30/06/2020 By balance c/d 75

75 75

4

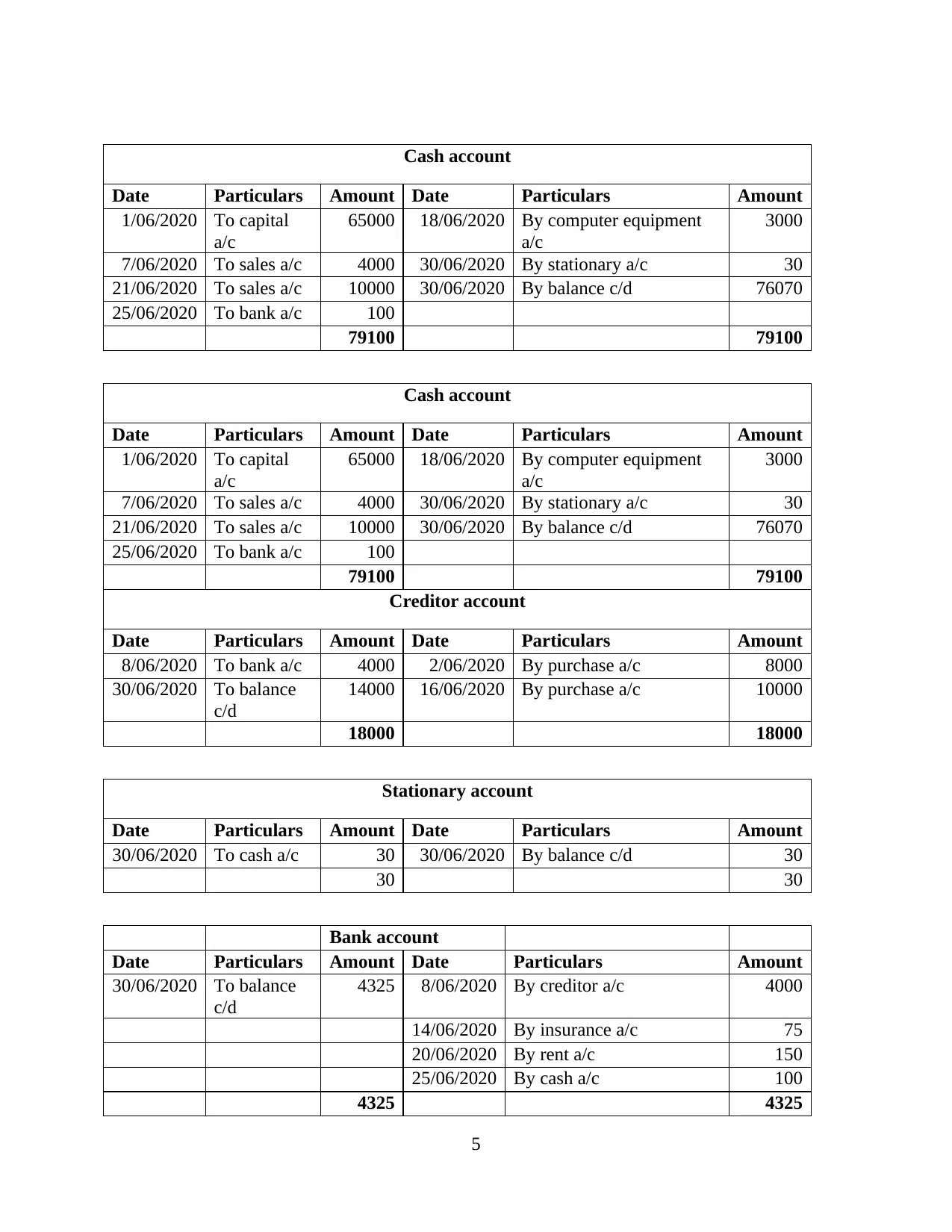

Cash account

Date Particulars Amount Date Particulars Amount

1/06/2020 To capital

a/c

65000 18/06/2020 By computer equipment

a/c

3000

7/06/2020 To sales a/c 4000 30/06/2020 By stationary a/c 30

21/06/2020 To sales a/c 10000 30/06/2020 By balance c/d 76070

25/06/2020 To bank a/c 100

79100 79100

Cash account

Date Particulars Amount Date Particulars Amount

1/06/2020 To capital

a/c

65000 18/06/2020 By computer equipment

a/c

3000

7/06/2020 To sales a/c 4000 30/06/2020 By stationary a/c 30

21/06/2020 To sales a/c 10000 30/06/2020 By balance c/d 76070

25/06/2020 To bank a/c 100

79100 79100

Creditor account

Date Particulars Amount Date Particulars Amount

8/06/2020 To bank a/c 4000 2/06/2020 By purchase a/c 8000

30/06/2020 To balance

c/d

14000 16/06/2020 By purchase a/c 10000

18000 18000

Stationary account

Date Particulars Amount Date Particulars Amount

30/06/2020 To cash a/c 30 30/06/2020 By balance c/d 30

30 30

Bank account

Date Particulars Amount Date Particulars Amount

30/06/2020 To balance

c/d

4325 8/06/2020 By creditor a/c 4000

14/06/2020 By insurance a/c 75

20/06/2020 By rent a/c 150

25/06/2020 By cash a/c 100

4325 4325

5

Date Particulars Amount Date Particulars Amount

1/06/2020 To capital

a/c

65000 18/06/2020 By computer equipment

a/c

3000

7/06/2020 To sales a/c 4000 30/06/2020 By stationary a/c 30

21/06/2020 To sales a/c 10000 30/06/2020 By balance c/d 76070

25/06/2020 To bank a/c 100

79100 79100

Cash account

Date Particulars Amount Date Particulars Amount

1/06/2020 To capital

a/c

65000 18/06/2020 By computer equipment

a/c

3000

7/06/2020 To sales a/c 4000 30/06/2020 By stationary a/c 30

21/06/2020 To sales a/c 10000 30/06/2020 By balance c/d 76070

25/06/2020 To bank a/c 100

79100 79100

Creditor account

Date Particulars Amount Date Particulars Amount

8/06/2020 To bank a/c 4000 2/06/2020 By purchase a/c 8000

30/06/2020 To balance

c/d

14000 16/06/2020 By purchase a/c 10000

18000 18000

Stationary account

Date Particulars Amount Date Particulars Amount

30/06/2020 To cash a/c 30 30/06/2020 By balance c/d 30

30 30

Bank account

Date Particulars Amount Date Particulars Amount

30/06/2020 To balance

c/d

4325 8/06/2020 By creditor a/c 4000

14/06/2020 By insurance a/c 75

20/06/2020 By rent a/c 150

25/06/2020 By cash a/c 100

4325 4325

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

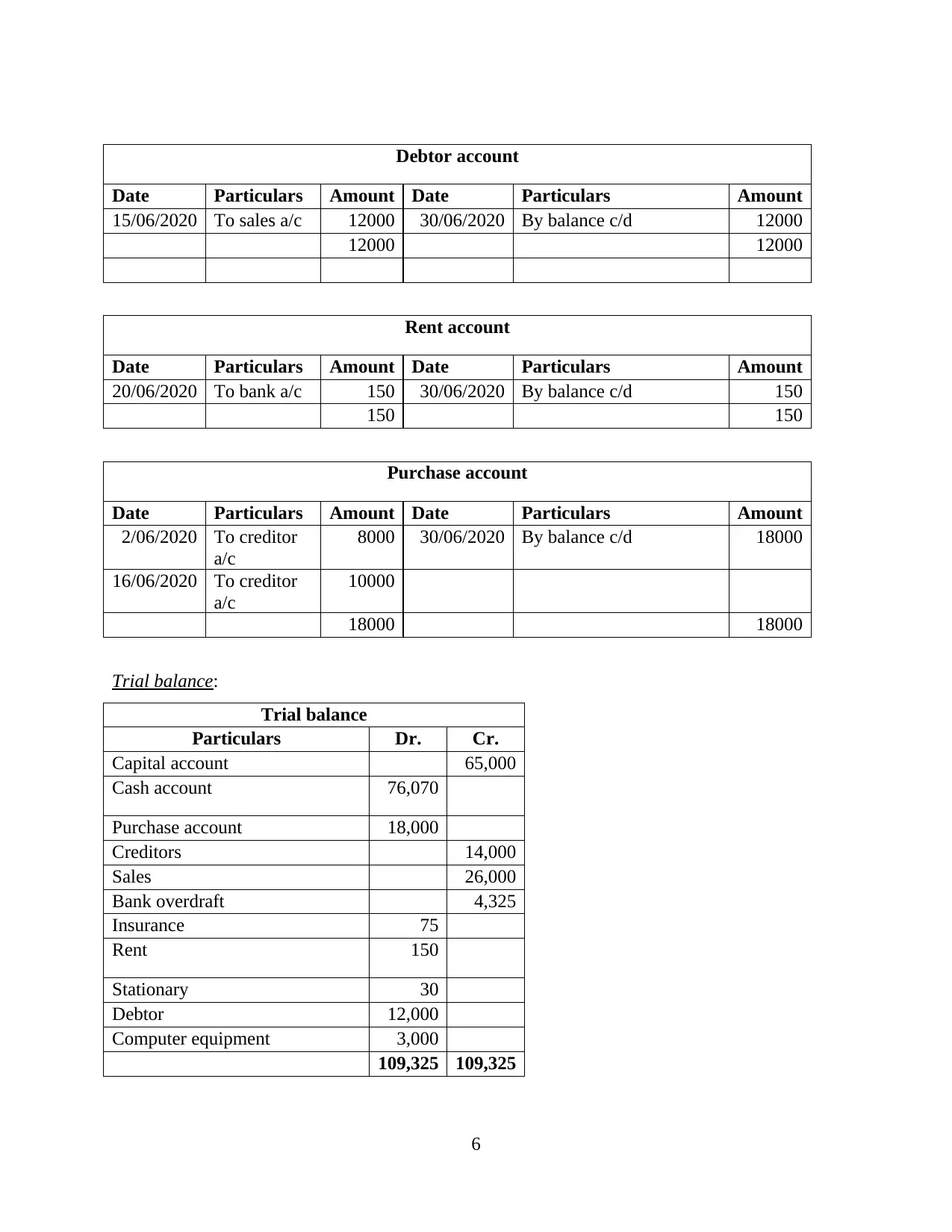

Debtor account

Date Particulars Amount Date Particulars Amount

15/06/2020 To sales a/c 12000 30/06/2020 By balance c/d 12000

12000 12000

Rent account

Date Particulars Amount Date Particulars Amount

20/06/2020 To bank a/c 150 30/06/2020 By balance c/d 150

150 150

Purchase account

Date Particulars Amount Date Particulars Amount

2/06/2020 To creditor

a/c

8000 30/06/2020 By balance c/d 18000

16/06/2020 To creditor

a/c

10000

18000 18000

Trial balance:

Trial balance

Particulars Dr. Cr.

Capital account 65,000

Cash account 76,070

Purchase account 18,000

Creditors 14,000

Sales 26,000

Bank overdraft 4,325

Insurance 75

Rent 150

Stationary 30

Debtor 12,000

Computer equipment 3,000

109,325 109,325

6

Date Particulars Amount Date Particulars Amount

15/06/2020 To sales a/c 12000 30/06/2020 By balance c/d 12000

12000 12000

Rent account

Date Particulars Amount Date Particulars Amount

20/06/2020 To bank a/c 150 30/06/2020 By balance c/d 150

150 150

Purchase account

Date Particulars Amount Date Particulars Amount

2/06/2020 To creditor

a/c

8000 30/06/2020 By balance c/d 18000

16/06/2020 To creditor

a/c

10000

18000 18000

Trial balance:

Trial balance

Particulars Dr. Cr.

Capital account 65,000

Cash account 76,070

Purchase account 18,000

Creditors 14,000

Sales 26,000

Bank overdraft 4,325

Insurance 75

Rent 150

Stationary 30

Debtor 12,000

Computer equipment 3,000

109,325 109,325

6

Question 3

Explain the difference between financial statement and financial report, why these reports are

required and who are the different users

Financial statements and the reports are also used as interchangeably. But there are some

variations in financial statement and reports and the annual statements (Kaplan and Atkinson,

2015). Reporting is being used to support the decision-making information. Financial reporting is

more structured. They also use disclosures to express the financial health to third party agencies.

For each fiscal cycle, file the annual statements. In the financial reporting includes the ratios

analysis which are used to identify the company’s financial performance in terms of profitability,

liquidity and efficiency. In contrast, financial statement includes the balance sheet, profit and

loss account, cash flow, fund flow statement etc.

The financial reporting is required to give organizations some in-depth analysis to

evaluate performance of the business. The reports help in valuing businesses, trying to predict

cash flows and planning investments. The accounts in the records demonstrate the financial

implications of the decisions made by the company. These records are for internal use, and some

are used by external parties. The financial reports of the company are also looked at by creditors,

lenders and government officials (Barron, Chung and Yong, 2016). To order to ensure

consistency, they can need to enforce compliance restrictions on financial reporting to other

agencies. Use a systematic approach for each report they preparing. This way, data from

several reports can be easily compared.

There are several users of financial reporting in context of Brightstar Financial Company

and those are discussed below:

Owner: shareholders and owners require financial knowledge to assist them determine

what to do with their assets such as retain, purchase, or sell more.

Management: Management can involve owners and managers. However, in

small companies strategy is typically composed of hired professionals who have been given the

responsibility of managing the organization or a side of the economy. They act as closed source

agents.

Employees: These people are keen on the sustainability and survival of the business. They

are all about the company can pay salaries as well as provide benefits for employees. They could

7

Explain the difference between financial statement and financial report, why these reports are

required and who are the different users

Financial statements and the reports are also used as interchangeably. But there are some

variations in financial statement and reports and the annual statements (Kaplan and Atkinson,

2015). Reporting is being used to support the decision-making information. Financial reporting is

more structured. They also use disclosures to express the financial health to third party agencies.

For each fiscal cycle, file the annual statements. In the financial reporting includes the ratios

analysis which are used to identify the company’s financial performance in terms of profitability,

liquidity and efficiency. In contrast, financial statement includes the balance sheet, profit and

loss account, cash flow, fund flow statement etc.

The financial reporting is required to give organizations some in-depth analysis to

evaluate performance of the business. The reports help in valuing businesses, trying to predict

cash flows and planning investments. The accounts in the records demonstrate the financial

implications of the decisions made by the company. These records are for internal use, and some

are used by external parties. The financial reports of the company are also looked at by creditors,

lenders and government officials (Barron, Chung and Yong, 2016). To order to ensure

consistency, they can need to enforce compliance restrictions on financial reporting to other

agencies. Use a systematic approach for each report they preparing. This way, data from

several reports can be easily compared.

There are several users of financial reporting in context of Brightstar Financial Company

and those are discussed below:

Owner: shareholders and owners require financial knowledge to assist them determine

what to do with their assets such as retain, purchase, or sell more.

Management: Management can involve owners and managers. However, in

small companies strategy is typically composed of hired professionals who have been given the

responsibility of managing the organization or a side of the economy. They act as closed source

agents.

Employees: These people are keen on the sustainability and survival of the business. They

are all about the company can pay salaries as well as provide benefits for employees. They could

7

also be involved in the financial status and results to determine opportunities for business growth

and job advancement.

Customers: When there has been a long-term participation or agreement between the firm

and its customers, consumers become involved in the company's ability to precede its presence

and retain operational stability (Edwards, Schwab and Shevlin, 2015). This need is also increased

in cases where even the clients rely on the entity.

Investors: Potential investors require financial reporting to assess the performance and

profitability possibility of the enterprise. Similarly, small business owners need monetary

information in order to determine if the project is worth and whether it should continue, enhance

or drop.

Above discussed users of financial reporting is limited, there are more left who required

such information to made their decisions. They can be internal as well as external users of

financial information. Similarly, Brightstar company prepare financial reporting for the use of its

users.

Question 4

Explain different fundamental principles of accounting

There are several fundamental principles which are very essential to followed by the

financial firms to maintain their accounts and record transactions according to the principles.

Some of them are as follow:

Monetary transactions: Accounting wants to monitor all the values in terms of the actual

monetary unit (Kim and Zhang, 2016). This is impossible to provide for such products as the

barter scheme. Consequently, assigning meanings to objects and products is an problem because

it is arbitrary. Accounting has however recommended rules for dealing with about the same.

Going concern: This concept means that the firm would continue doing its life as normal

until the give up of the next accounting cycle and that the opposite is not reported. Regardless of

the concept of going concern, companies may run on credit, account for payments payable and

receivable they expect to earn or reimburse in the lifetime, and incur depreciation if the system is

being used for generations to follow.

Principle of conservatism: Professionals are shown to be inherently very progressive.

They would like to stay positive, and prepare themselves for the worst. This is seen in the rules

which they generated for their career. Another of the central aspects of accounting is the

8

and job advancement.

Customers: When there has been a long-term participation or agreement between the firm

and its customers, consumers become involved in the company's ability to precede its presence

and retain operational stability (Edwards, Schwab and Shevlin, 2015). This need is also increased

in cases where even the clients rely on the entity.

Investors: Potential investors require financial reporting to assess the performance and

profitability possibility of the enterprise. Similarly, small business owners need monetary

information in order to determine if the project is worth and whether it should continue, enhance

or drop.

Above discussed users of financial reporting is limited, there are more left who required

such information to made their decisions. They can be internal as well as external users of

financial information. Similarly, Brightstar company prepare financial reporting for the use of its

users.

Question 4

Explain different fundamental principles of accounting

There are several fundamental principles which are very essential to followed by the

financial firms to maintain their accounts and record transactions according to the principles.

Some of them are as follow:

Monetary transactions: Accounting wants to monitor all the values in terms of the actual

monetary unit (Kim and Zhang, 2016). This is impossible to provide for such products as the

barter scheme. Consequently, assigning meanings to objects and products is an problem because

it is arbitrary. Accounting has however recommended rules for dealing with about the same.

Going concern: This concept means that the firm would continue doing its life as normal

until the give up of the next accounting cycle and that the opposite is not reported. Regardless of

the concept of going concern, companies may run on credit, account for payments payable and

receivable they expect to earn or reimburse in the lifetime, and incur depreciation if the system is

being used for generations to follow.

Principle of conservatism: Professionals are shown to be inherently very progressive.

They would like to stay positive, and prepare themselves for the worst. This is seen in the rules

which they generated for their career. Another of the central aspects of accounting is the

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

consistency theory. Due to this theory, where the quantity of planned outflows and inflows is in

doubt, the company must claim the least possible income and the maximum possible expense.

Cost principle: Cost principle is directly relevant to the conservatism principle (Lara,

Osma and Penalva, 2016). The cost theory suggests that individuals should report anything at

cost price on the financial reports. Appreciate typically properties such as land and houses,

money, etc. Nevertheless, the accounting professionals do not require the company's financial

statements to show this recognition until it is understood. Accountants assume that something is

just an belief about the market value. They could not pay on the level of views, since all of those

exist. But someone has compensated for it, the selling price of something that is a reality, but the

same could be authenticated. Accounting thus operates on the theory of expense, and hence on

facts.

Question 5

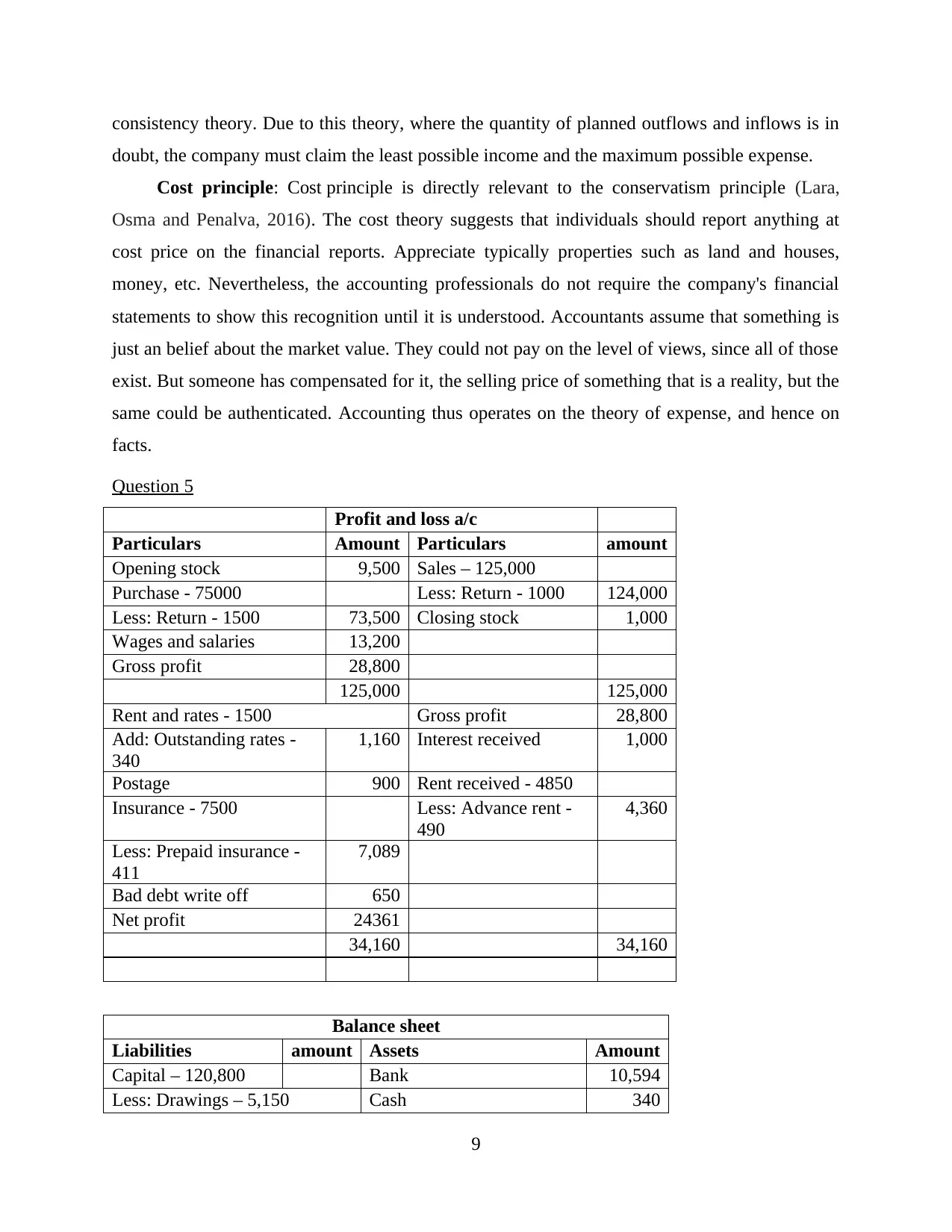

Profit and loss a/c

Particulars Amount Particulars amount

Opening stock 9,500 Sales – 125,000

Purchase - 75000 Less: Return - 1000 124,000

Less: Return - 1500 73,500 Closing stock 1,000

Wages and salaries 13,200

Gross profit 28,800

125,000 125,000

Rent and rates - 1500 Gross profit 28,800

Add: Outstanding rates -

340

1,160 Interest received 1,000

Postage 900 Rent received - 4850

Insurance - 7500 Less: Advance rent -

490

4,360

Less: Prepaid insurance -

411

7,089

Bad debt write off 650

Net profit 24361

34,160 34,160

Balance sheet

Liabilities amount Assets Amount

Capital – 120,800 Bank 10,594

Less: Drawings – 5,150 Cash 340

9

doubt, the company must claim the least possible income and the maximum possible expense.

Cost principle: Cost principle is directly relevant to the conservatism principle (Lara,

Osma and Penalva, 2016). The cost theory suggests that individuals should report anything at

cost price on the financial reports. Appreciate typically properties such as land and houses,

money, etc. Nevertheless, the accounting professionals do not require the company's financial

statements to show this recognition until it is understood. Accountants assume that something is

just an belief about the market value. They could not pay on the level of views, since all of those

exist. But someone has compensated for it, the selling price of something that is a reality, but the

same could be authenticated. Accounting thus operates on the theory of expense, and hence on

facts.

Question 5

Profit and loss a/c

Particulars Amount Particulars amount

Opening stock 9,500 Sales – 125,000

Purchase - 75000 Less: Return - 1000 124,000

Less: Return - 1500 73,500 Closing stock 1,000

Wages and salaries 13,200

Gross profit 28,800

125,000 125,000

Rent and rates - 1500 Gross profit 28,800

Add: Outstanding rates -

340

1,160 Interest received 1,000

Postage 900 Rent received - 4850

Insurance - 7500 Less: Advance rent -

490

4,360

Less: Prepaid insurance -

411

7,089

Bad debt write off 650

Net profit 24361

34,160 34,160

Balance sheet

Liabilities amount Assets Amount

Capital – 120,800 Bank 10,594

Less: Drawings – 5,150 Cash 340

9

Add: Net profit -

24361

140,011 Prepaid insurance 411

Provision for bad

debts

934 Advance rent 490

Debtor - 12500

Creditor 3,900 Less: Bad debt write off -

934

11,850

Outstanding rates 340 Motor van at WDV - 19600

Less: Dep - 5000 14,600

Loan 100,000

Closing stock 1,000

145,185 145,185

Scenario 2

Question 1

What is meant by bank reconciliation and why is it required? How is this achieved? Why is this

necessary

Bank reconciliation statements facilitate the processing of transfers and depositing cash

deposits into the accounts (Mussari, 2014). In order to accept appropriate changes or

clarifications, the reconciliation statement allows finding variations between the bank account

balance and the book balance. It is a method of comparing the balances for a cash account in an

organization's financial documents to the related facts on a bank statement. A financial audit with

all bank accounts will be performed at regular intervals, to ensure that the cash records of a

business are accurate.

Bank reconciliation is required to compare company's records with the bank's records, and

if there are the certain differences for cash transactions among these two record sets. The closing

balance of the cash report edition is recognized as the book balance, although the bank's portion

is referred to as the money balance. Contrast between the three balances sheets are extremely

common, which company should chase down and modify in their own records. When these

dissimilarities were to be ignored, there would ultimately be significant differences between the

quantity of funds users think people have and the quantity that the bank says they actually have

in an account. Overdrawn bank account, cash inflows and outflows, and overdraft fees might be

the result. For certain instances, the bank can also chose to cut off your bank account.

10

24361

140,011 Prepaid insurance 411

Provision for bad

debts

934 Advance rent 490

Debtor - 12500

Creditor 3,900 Less: Bad debt write off -

934

11,850

Outstanding rates 340 Motor van at WDV - 19600

Less: Dep - 5000 14,600

Loan 100,000

Closing stock 1,000

145,185 145,185

Scenario 2

Question 1

What is meant by bank reconciliation and why is it required? How is this achieved? Why is this

necessary

Bank reconciliation statements facilitate the processing of transfers and depositing cash

deposits into the accounts (Mussari, 2014). In order to accept appropriate changes or

clarifications, the reconciliation statement allows finding variations between the bank account

balance and the book balance. It is a method of comparing the balances for a cash account in an

organization's financial documents to the related facts on a bank statement. A financial audit with

all bank accounts will be performed at regular intervals, to ensure that the cash records of a

business are accurate.

Bank reconciliation is required to compare company's records with the bank's records, and

if there are the certain differences for cash transactions among these two record sets. The closing

balance of the cash report edition is recognized as the book balance, although the bank's portion

is referred to as the money balance. Contrast between the three balances sheets are extremely

common, which company should chase down and modify in their own records. When these

dissimilarities were to be ignored, there would ultimately be significant differences between the

quantity of funds users think people have and the quantity that the bank says they actually have

in an account. Overdrawn bank account, cash inflows and outflows, and overdraft fees might be

the result. For certain instances, the bank can also chose to cut off your bank account.

10

Bank reconciliation can be achieved through comparing their internal account information

and needs to balance to their monthly bank statement to resolve their accounts (Raiborn and

Sivitanides, 2015). Check each transaction separately, make sure that now the quantities match

perfectly, and recognize any differences that require further investigation. The procedure can be

as structured or casual as you wish, and some companies are making a declaration of bank

reconciliation to show that they periodically reconcile accounts. If company don't finish the

process on a monthly basis, they can do so regularly, on a quarterly basis or on every other time

they choose. It is necessary to identify to check the balance and evaluate that it is same or not. If

they find any difference, so they need to give justification for it or find out the reason.

Question 2

What are control accounts? Explain the role of control accounts in financial management

Control account is often considered a controlling account which is a general ledger account

that describes all the subsidiary account balances for a particular type and integrates them

together (Trotman and Carson, 2018). In other words, it is a descriptive account that is equivalent

to the subordinate account total which is used to ease the general ledger that coordinates it.

Control accounts plays several roles in financial management which is automatically

beneficial for the organization and those are mentioned below:

Provides a check-up system for early detection of mistakes and fraud.

Eliminate shapeless information from general ledger.

Large businesses may establish accounting departments for particular places.

Trial balance figures, instead of individual accounts give a summary of total.

Reduce the likelihood of forgery even though control account documents and subsidiary

ledger are maintained individually by different personnel.

Question 3

Suspense account and the reasons for drafting suspense accounts

Suspense recorded in the general section in which company records unclear entries which

still require for further analysis to determine everyone’s implementation strategies or destination.

Throughout the investment context, a suspense account is a account in which a shareholder parks

his money temporarily till they can implement that money to until capital spending.

Reasons of preparing suspense accounts:

11

and needs to balance to their monthly bank statement to resolve their accounts (Raiborn and

Sivitanides, 2015). Check each transaction separately, make sure that now the quantities match

perfectly, and recognize any differences that require further investigation. The procedure can be

as structured or casual as you wish, and some companies are making a declaration of bank

reconciliation to show that they periodically reconcile accounts. If company don't finish the

process on a monthly basis, they can do so regularly, on a quarterly basis or on every other time

they choose. It is necessary to identify to check the balance and evaluate that it is same or not. If

they find any difference, so they need to give justification for it or find out the reason.

Question 2

What are control accounts? Explain the role of control accounts in financial management

Control account is often considered a controlling account which is a general ledger account

that describes all the subsidiary account balances for a particular type and integrates them

together (Trotman and Carson, 2018). In other words, it is a descriptive account that is equivalent

to the subordinate account total which is used to ease the general ledger that coordinates it.

Control accounts plays several roles in financial management which is automatically

beneficial for the organization and those are mentioned below:

Provides a check-up system for early detection of mistakes and fraud.

Eliminate shapeless information from general ledger.

Large businesses may establish accounting departments for particular places.

Trial balance figures, instead of individual accounts give a summary of total.

Reduce the likelihood of forgery even though control account documents and subsidiary

ledger are maintained individually by different personnel.

Question 3

Suspense account and the reasons for drafting suspense accounts

Suspense recorded in the general section in which company records unclear entries which

still require for further analysis to determine everyone’s implementation strategies or destination.

Throughout the investment context, a suspense account is a account in which a shareholder parks

his money temporarily till they can implement that money to until capital spending.

Reasons of preparing suspense accounts:

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

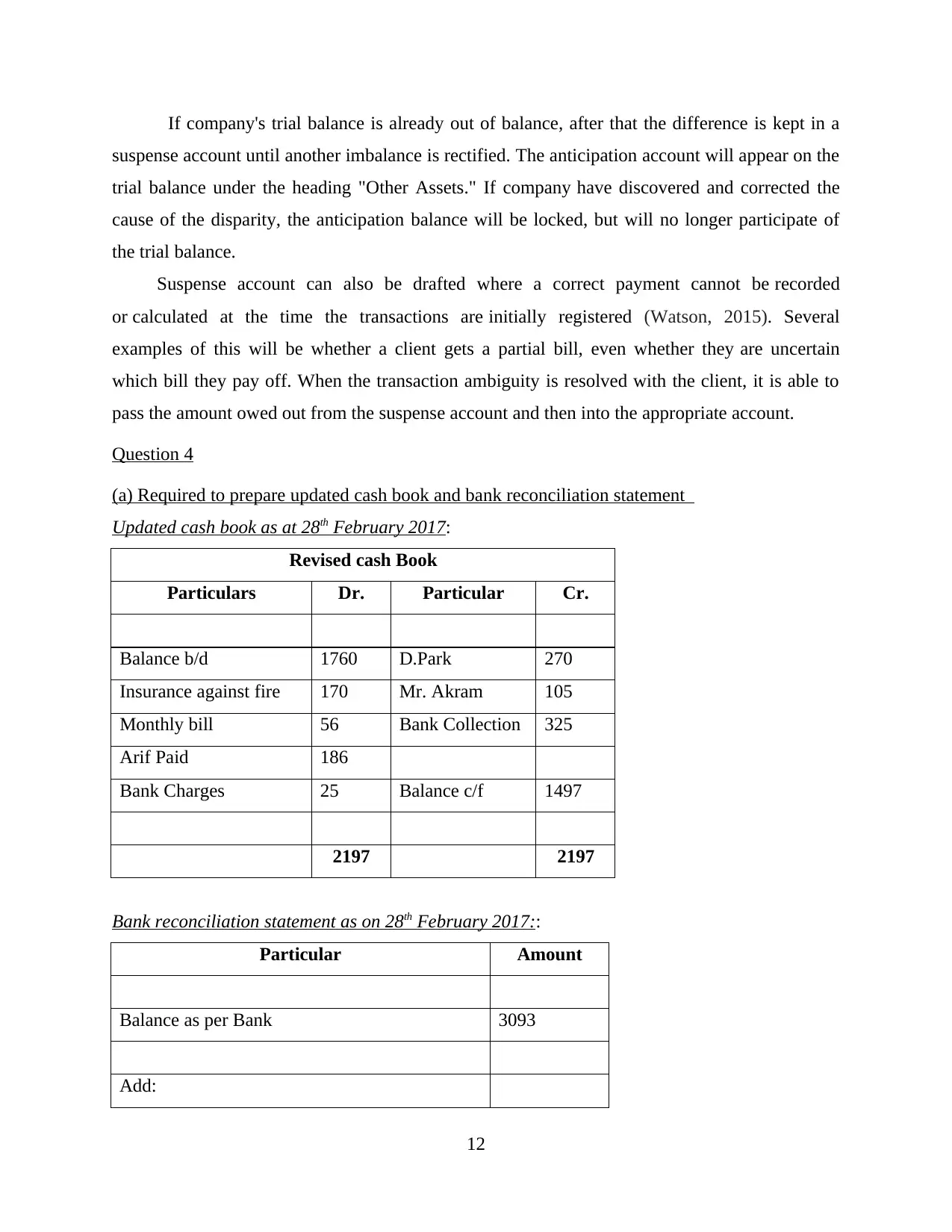

If company's trial balance is already out of balance, after that the difference is kept in a

suspense account until another imbalance is rectified. The anticipation account will appear on the

trial balance under the heading "Other Assets." If company have discovered and corrected the

cause of the disparity, the anticipation balance will be locked, but will no longer participate of

the trial balance.

Suspense account can also be drafted where a correct payment cannot be recorded

or calculated at the time the transactions are initially registered (Watson, 2015). Several

examples of this will be whether a client gets a partial bill, even whether they are uncertain

which bill they pay off. When the transaction ambiguity is resolved with the client, it is able to

pass the amount owed out from the suspense account and then into the appropriate account.

Question 4

(a) Required to prepare updated cash book and bank reconciliation statement

Updated cash book as at 28th February 2017:

Revised cash Book

Particulars Dr. Particular Cr.

Balance b/d 1760 D.Park 270

Insurance against fire 170 Mr. Akram 105

Monthly bill 56 Bank Collection 325

Arif Paid 186

Bank Charges 25 Balance c/f 1497

2197 2197

Bank reconciliation statement as on 28th February 2017::

Particular Amount

Balance as per Bank 3093

Add:

12

suspense account until another imbalance is rectified. The anticipation account will appear on the

trial balance under the heading "Other Assets." If company have discovered and corrected the

cause of the disparity, the anticipation balance will be locked, but will no longer participate of

the trial balance.

Suspense account can also be drafted where a correct payment cannot be recorded

or calculated at the time the transactions are initially registered (Watson, 2015). Several

examples of this will be whether a client gets a partial bill, even whether they are uncertain

which bill they pay off. When the transaction ambiguity is resolved with the client, it is able to

pass the amount owed out from the suspense account and then into the appropriate account.

Question 4

(a) Required to prepare updated cash book and bank reconciliation statement

Updated cash book as at 28th February 2017:

Revised cash Book

Particulars Dr. Particular Cr.

Balance b/d 1760 D.Park 270

Insurance against fire 170 Mr. Akram 105

Monthly bill 56 Bank Collection 325

Arif Paid 186

Bank Charges 25 Balance c/f 1497

2197 2197

Bank reconciliation statement as on 28th February 2017::

Particular Amount

Balance as per Bank 3093

Add:

12

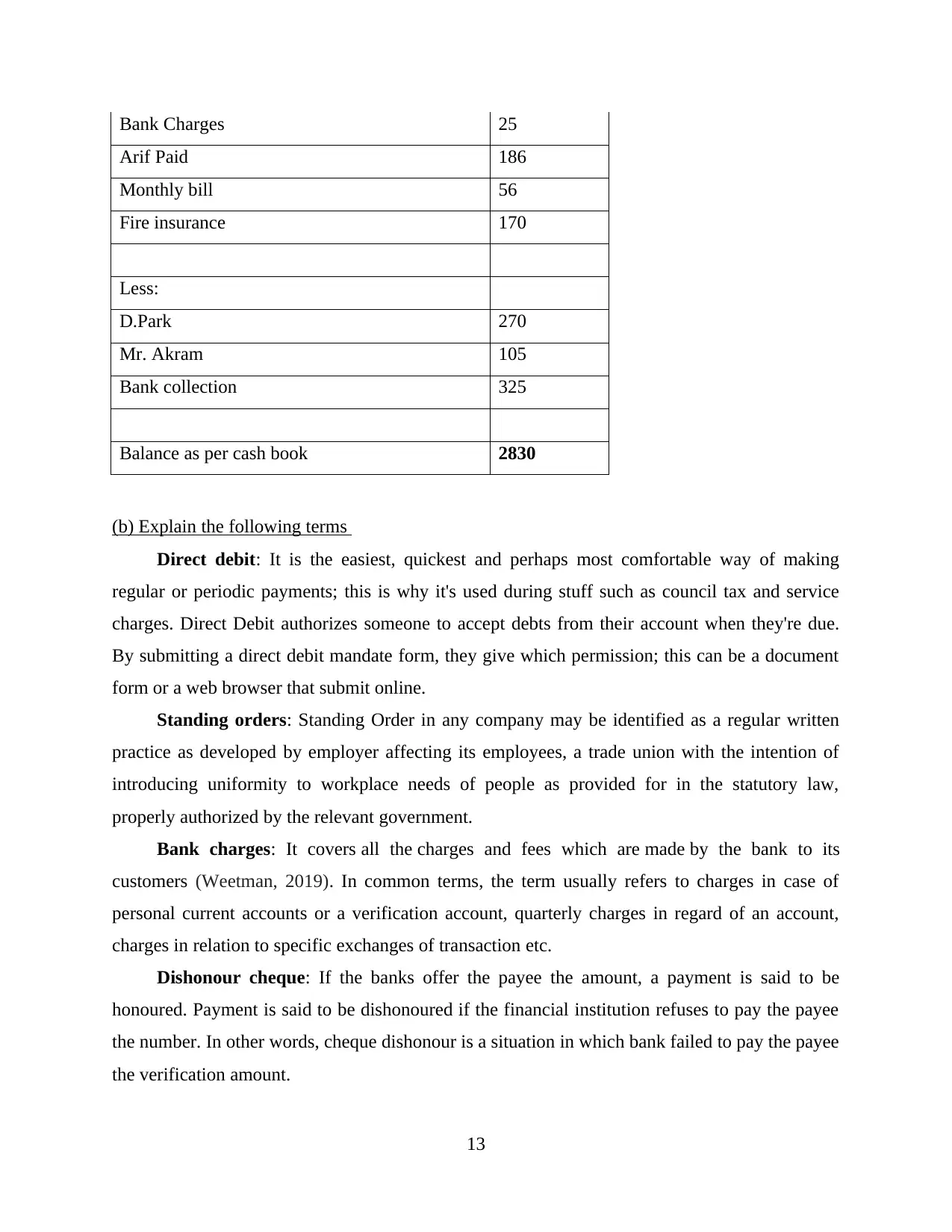

Bank Charges 25

Arif Paid 186

Monthly bill 56

Fire insurance 170

Less:

D.Park 270

Mr. Akram 105

Bank collection 325

Balance as per cash book 2830

(b) Explain the following terms

Direct debit: It is the easiest, quickest and perhaps most comfortable way of making

regular or periodic payments; this is why it's used during stuff such as council tax and service

charges. Direct Debit authorizes someone to accept debts from their account when they're due.

By submitting a direct debit mandate form, they give which permission; this can be a document

form or a web browser that submit online.

Standing orders: Standing Order in any company may be identified as a regular written

practice as developed by employer affecting its employees, a trade union with the intention of

introducing uniformity to workplace needs of people as provided for in the statutory law,

properly authorized by the relevant government.

Bank charges: It covers all the charges and fees which are made by the bank to its

customers (Weetman, 2019). In common terms, the term usually refers to charges in case of

personal current accounts or a verification account, quarterly charges in regard of an account,

charges in relation to specific exchanges of transaction etc.

Dishonour cheque: If the banks offer the payee the amount, a payment is said to be

honoured. Payment is said to be dishonoured if the financial institution refuses to pay the payee

the number. In other words, cheque dishonour is a situation in which bank failed to pay the payee

the verification amount.

13

Arif Paid 186

Monthly bill 56

Fire insurance 170

Less:

D.Park 270

Mr. Akram 105

Bank collection 325

Balance as per cash book 2830

(b) Explain the following terms

Direct debit: It is the easiest, quickest and perhaps most comfortable way of making

regular or periodic payments; this is why it's used during stuff such as council tax and service

charges. Direct Debit authorizes someone to accept debts from their account when they're due.

By submitting a direct debit mandate form, they give which permission; this can be a document

form or a web browser that submit online.

Standing orders: Standing Order in any company may be identified as a regular written

practice as developed by employer affecting its employees, a trade union with the intention of

introducing uniformity to workplace needs of people as provided for in the statutory law,

properly authorized by the relevant government.

Bank charges: It covers all the charges and fees which are made by the bank to its

customers (Weetman, 2019). In common terms, the term usually refers to charges in case of

personal current accounts or a verification account, quarterly charges in regard of an account,

charges in relation to specific exchanges of transaction etc.

Dishonour cheque: If the banks offer the payee the amount, a payment is said to be

honoured. Payment is said to be dishonoured if the financial institution refuses to pay the payee

the number. In other words, cheque dishonour is a situation in which bank failed to pay the payee

the verification amount.

13

Question 5

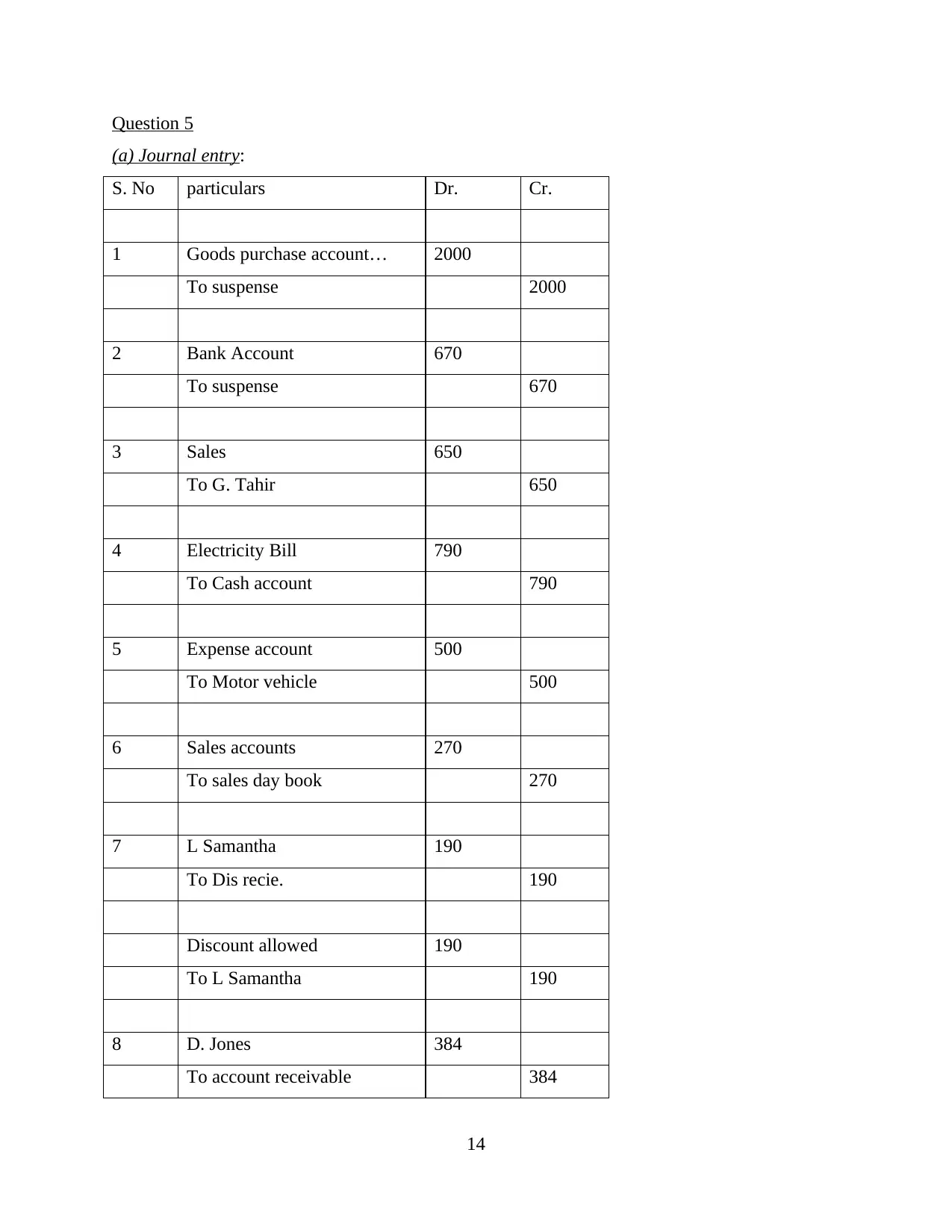

(a) Journal entry:

S. No particulars Dr. Cr.

1 Goods purchase account… 2000

To suspense 2000

2 Bank Account 670

To suspense 670

3 Sales 650

To G. Tahir 650

4 Electricity Bill 790

To Cash account 790

5 Expense account 500

To Motor vehicle 500

6 Sales accounts 270

To sales day book 270

7 L Samantha 190

To Dis recie. 190

Discount allowed 190

To L Samantha 190

8 D. Jones 384

To account receivable 384

14

(a) Journal entry:

S. No particulars Dr. Cr.

1 Goods purchase account… 2000

To suspense 2000

2 Bank Account 670

To suspense 670

3 Sales 650

To G. Tahir 650

4 Electricity Bill 790

To Cash account 790

5 Expense account 500

To Motor vehicle 500

6 Sales accounts 270

To sales day book 270

7 L Samantha 190

To Dis recie. 190

Discount allowed 190

To L Samantha 190

8 D. Jones 384

To account receivable 384

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

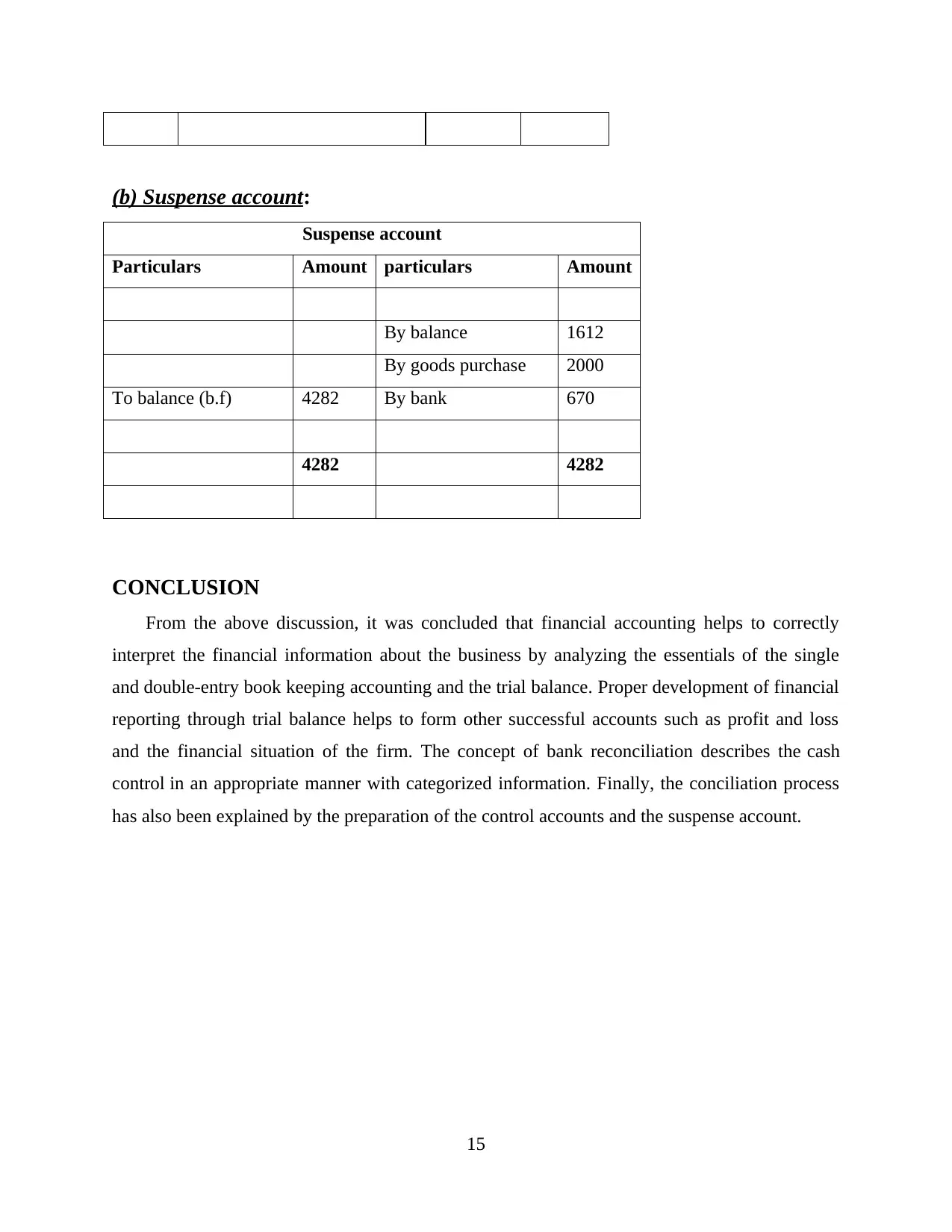

(b) Suspense account:

Suspense account

Particulars Amount particulars Amount

By balance 1612

By goods purchase 2000

To balance (b.f) 4282 By bank 670

4282 4282

CONCLUSION

From the above discussion, it was concluded that financial accounting helps to correctly

interpret the financial information about the business by analyzing the essentials of the single

and double-entry book keeping accounting and the trial balance. Proper development of financial

reporting through trial balance helps to form other successful accounts such as profit and loss

and the financial situation of the firm. The concept of bank reconciliation describes the cash

control in an appropriate manner with categorized information. Finally, the conciliation process

has also been explained by the preparation of the control accounts and the suspense account.

15

Suspense account

Particulars Amount particulars Amount

By balance 1612

By goods purchase 2000

To balance (b.f) 4282 By bank 670

4282 4282

CONCLUSION

From the above discussion, it was concluded that financial accounting helps to correctly

interpret the financial information about the business by analyzing the essentials of the single

and double-entry book keeping accounting and the trial balance. Proper development of financial

reporting through trial balance helps to form other successful accounts such as profit and loss

and the financial situation of the firm. The concept of bank reconciliation describes the cash

control in an appropriate manner with categorized information. Finally, the conciliation process

has also been explained by the preparation of the control accounts and the suspense account.

15

REFERENCES

Books & Journals

Chan, J. L., 2015. New development: China promotes government financial accounting and

management accounting. Public Money & Management. 35(6). pp.451-454.

Drexler, A., Fischer, G. and Schoar, A., 2014. Keeping it simple: Financial literacy and rules of

thumb. American Economic Journal: Applied Economics. 6(2). pp.1-31.

Jiang, J., Wang, I. Y. and Xie, Y., 2015. Does it matter who serves on the Financial Accounting

Standards Board? Bob Herz’s resignation and fair value accounting for loans. Review of

Accounting Studies. 20(1). pp.371-394.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Barron, O. E., Chung, S. G. and Yong, K. O., 2016. The effect of Statement of Financial

Accounting Standards No. 157 Fair Value Measurements on analysts’ information

environment. Journal of accounting and public policy. 35(4). pp.395-416.

Edwards, A., Schwab, C. and Shevlin, T., 2015. Financial constraints and cash tax savings. The

Accounting Review. 91(3). pp.859-881.

Kim, J. B. and Zhang, L., 2016. Accounting conservatism and stock price crash risk: Firm‐level

evidence. Contemporary Accounting Research. 33(1). pp.412-441.

Lara, J. M. G., Osma, B. G. and Penalva, F., 2016. Accounting conservatism and firm investment

efficiency. Journal of Accounting and Economics. 61(1). pp.221-238.

Mussari, R., 2014. EPSAS and the unification of public sector accounting across

Europe. Accounting, Economics and Law. 4(3). pp.299-312.

Raiborn, C. and Sivitanides, M., 2015. Accounting issues related to Bitcoins. Journal of

Corporate Accounting & Finance. 26(2). pp.25-34.

Trotman, K. and Carson, E., 2018. Financial accounting: an integrated approach. Cengage AU.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of Accounting

Literature. 34. pp.1-16.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

16

Books & Journals

Chan, J. L., 2015. New development: China promotes government financial accounting and

management accounting. Public Money & Management. 35(6). pp.451-454.

Drexler, A., Fischer, G. and Schoar, A., 2014. Keeping it simple: Financial literacy and rules of

thumb. American Economic Journal: Applied Economics. 6(2). pp.1-31.

Jiang, J., Wang, I. Y. and Xie, Y., 2015. Does it matter who serves on the Financial Accounting

Standards Board? Bob Herz’s resignation and fair value accounting for loans. Review of

Accounting Studies. 20(1). pp.371-394.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Barron, O. E., Chung, S. G. and Yong, K. O., 2016. The effect of Statement of Financial

Accounting Standards No. 157 Fair Value Measurements on analysts’ information

environment. Journal of accounting and public policy. 35(4). pp.395-416.

Edwards, A., Schwab, C. and Shevlin, T., 2015. Financial constraints and cash tax savings. The

Accounting Review. 91(3). pp.859-881.

Kim, J. B. and Zhang, L., 2016. Accounting conservatism and stock price crash risk: Firm‐level

evidence. Contemporary Accounting Research. 33(1). pp.412-441.

Lara, J. M. G., Osma, B. G. and Penalva, F., 2016. Accounting conservatism and firm investment

efficiency. Journal of Accounting and Economics. 61(1). pp.221-238.

Mussari, R., 2014. EPSAS and the unification of public sector accounting across

Europe. Accounting, Economics and Law. 4(3). pp.299-312.

Raiborn, C. and Sivitanides, M., 2015. Accounting issues related to Bitcoins. Journal of

Corporate Accounting & Finance. 26(2). pp.25-34.

Trotman, K. and Carson, E., 2018. Financial accounting: an integrated approach. Cengage AU.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of Accounting

Literature. 34. pp.1-16.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

16

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.