Financial Accounting & Reporting - DOC

Added on 2020-09-08

37 Pages3749 Words61 Views

Financial Accounting

TABLE OF CONTENTSINTRODUCTION...........................................................................................................................1A. Prepare a report for accounting regulations for firm to the Line manager........................11. Discussing financial accounting.........................................................................................12. Outlining financial accounting regulations........................................................................23. Discussing various principles and rules for accounting.....................................................34. Discussing concepts of material disclosure as well as consistency....................................4CLIENT 1........................................................................................................................................41. Producing journal account for organisation.......................................................................4..........................................................................................................................................................6..........................................................................................................................................................6..........................................................................................................................................................72. Preparation of ledger accounts from the journal entries.....................................................7..........................................................................................................................................................9........................................................................................................................................................10........................................................................................................................................................11........................................................................................................................................................11........................................................................................................................................................12........................................................................................................................................................13........................................................................................................................................................14........................................................................................................................................................15........................................................................................................................................................16........................................................................................................................................................16........................................................................................................................................................17........................................................................................................................................................17........................................................................................................................................................183. Extraction of Trial balance of organisation......................................................................18M1. Analyse purchase and sale transactions to compile a trial balance...............................19D1. Presentation of trial balance while considering accounting principles..........................19CLIENT 2......................................................................................................................................20A Profit and loss statement for company.............................................................................20

B. Preparation of balance sheet for Peter Piper company....................................................21CLIENT 3......................................................................................................................................23A. Income statement for Raintree Ltd..................................................................................23B. Financial position of company.........................................................................................24C. Discussing principles and concepts of accounting..........................................................25D. Outlining importance of measuring and presenting depreciation in the financials ofbusiness and providing methods of deprecation...................................................................26M2 Providing analysis of P&L, balance sheet and cash flow statements............................26D2 Applying calculations in construction of the final accounts..........................................27CLIENT 4......................................................................................................................................27A. Preparing the bank statement...........................................................................................27B Outlining the causes of recording bank statements..........................................................27C. Cash books.......................................................................................................................27M3 Reconciliation process and outlining various terms......................................................28D3 Producing BRS in consideration of accounting tools.....................................................28CLIENT 5......................................................................................................................................28A Producing the sales and purchase ledger account for Henderson organisation................28B. Defining control account.................................................................................................29CLIENT 6......................................................................................................................................29A Illustrating suspense account and highlighting main features..........................................29B. Preparing trial balance.....................................................................................................30C. Producing journal entries.................................................................................................31D. Distinguishing clearing and suspense account................................................................32M4 Providing types of accounts and reconciliation.............................................................32D4 Preparing adequate accounting methods........................................................................33CONCLUSION..............................................................................................................................33REFERENCES..............................................................................................................................34

INTRODUCTIONFinancial accounting is required to be prepared by the company so that true and fairfinancial information may be provided to users of accounting information. The enclosed reportdeals with various companies by which financial statements are prepared with much ease.Moreover, accounting principles guides accountants to be efficient preparing accurate financialinformation. A. Prepare a report for accounting regulations for firm to the Line managerTo: Line ManagerFrom: Junior accountantSubject: Different accounting terms and which are relevant with such accounting regulations.Sir,The accounting principles are useful for organisation as they guide accountants toprepare accurate financial statements such as balance sheets, Profit & Loss account and cashflow statements as well. They are reliable source fop information to external as well as internalusers for making certain better and effective decisions in the best possible way. In addition tothis, budgeting and forecasting are also powerful tool for the business to flourish in the market.Various accounting techniques helps company to prepare accurate and meaningful financialstatements. 1. Discussing financial accountingFinancial accounting is the branch of accounting which deals with recording of dailymonetary transactions of business in that way which in turn may be interpreted and analysed byusers of accounting information. Management is benefited by such information which isprepared with the help of financial accounting. As such, better and effective decisions may betaken in the most profitable manner. Various financial statements such as balance sheets, Profit& Loss account and cash flow statements are prepared by accountants which are useful forexternal as well as internal stakeholders' of the company. The main motive of such financialstatements is to provide and disclose the liquidity, profitability and efficiency of organisation.This in turn helps investors and creditors to make enhanced decisions whether to priovide fundsto company to not.1

Illustration 1: Types of financial statementsSource: (Zeff, 2016)The above diagram shows several kinds of financial statements which are produced byorganisation. This information eases tax payment liability of the firm and as a result, taxationauthorities are enhanced by fair and true information provided by financial statements. 2. Outlining financial accounting regulationsVarious operational activities takes place in company and as such, every record ismaintained which is the primary requirement of organisation. In addition to this, financialaccounting regulations are required to be fulfil by company so that it may be able to providelegal framework of accounting principles and as a result, fair and true financial statements areproduced for users of accounting information to make effective and better decisions. In relationto this, UK's corporate reporting and governance regulator has provided FRC which regulatesfinancial reporting of organisations, government departments and other units as well. Thisprovides to have an effective financial information and auditing of financial accounts preparedso that trade may be improved in the country and in turn economy may be benefited in the bestpossible manner (Dutta and Patatoukas, 2016). The various legal frameworks governed by professional bodies are as follows :FRC : This board is a company limited by guarantee and this regulates high corporategovernance and also for foster investment in UK. The FRC (Financial Reporting Council) isresponsible for promoting healthy corporate governance so that overall economy may bebenefited in the best possible manner. IASB : The main motive of such information is to provide guidelines and adequate informationto accountants so that financial statements may be prepared nicely and as such must exhibit trueinformation by adopting various accounting principles and concepts. Thus, IASB (International2

Accounting Standards Board) helps in providing legal framework for adeqaute financialdisclosure of final accounts. The guidelines are universally accepted and also helps in attractingthe international investors. IFRS : This professional body provides framework which is relevant for organisation so thatappropriate financial statements may be prepared and essential information may be pass on tousers of accounting information (Grant, 2016). 3. Discussing various principles and rules for accountingThere are several principles and rules for accounting which has been provided by GAAP(Generally Accepted Accounting Principles) that guides accounting professionals whilefacilitating accounting information. The various rules and principles are as follows:Monetary unit assumption : The currency which is universally accepted is US dollar and assuch, business transactions may be made by this currency as it has stable rate in the worldwidemarket. Economic assumptions: Company will often make assumptions regarding economicenvironment for a certain period in order to analyse and predict how this will affect onupcoming project of organisation. The various entities in the market may be tallied so thatassumptions may be made for future period.Cost principle : Cost principle states that requirement of costs for various departments in theorganisation may be analysed so that budget can be prepared and as such, expenditures can becontrolled in the most efficient way. Expenses are to be budgeted to meet the traderequirements.Full disclosure principles : Business records each and every transaction of day to day activitiesof different departments and as such, the financial statements are produced. These statementsmust be audited and compile in single statements so that information may be reliable.Moreover, final accounts of the business must be fully disclosed at the end of every financialperiod which exhibits fair information of the performance of company (Loughran andMcDonald, 2016). Going concern Principles : This principle states that business will continue for longer periodand as such, financial statements are prepared by the organisation. The business will not closewithin short period. As a result, disclosure of final accounts are produced. Business will3

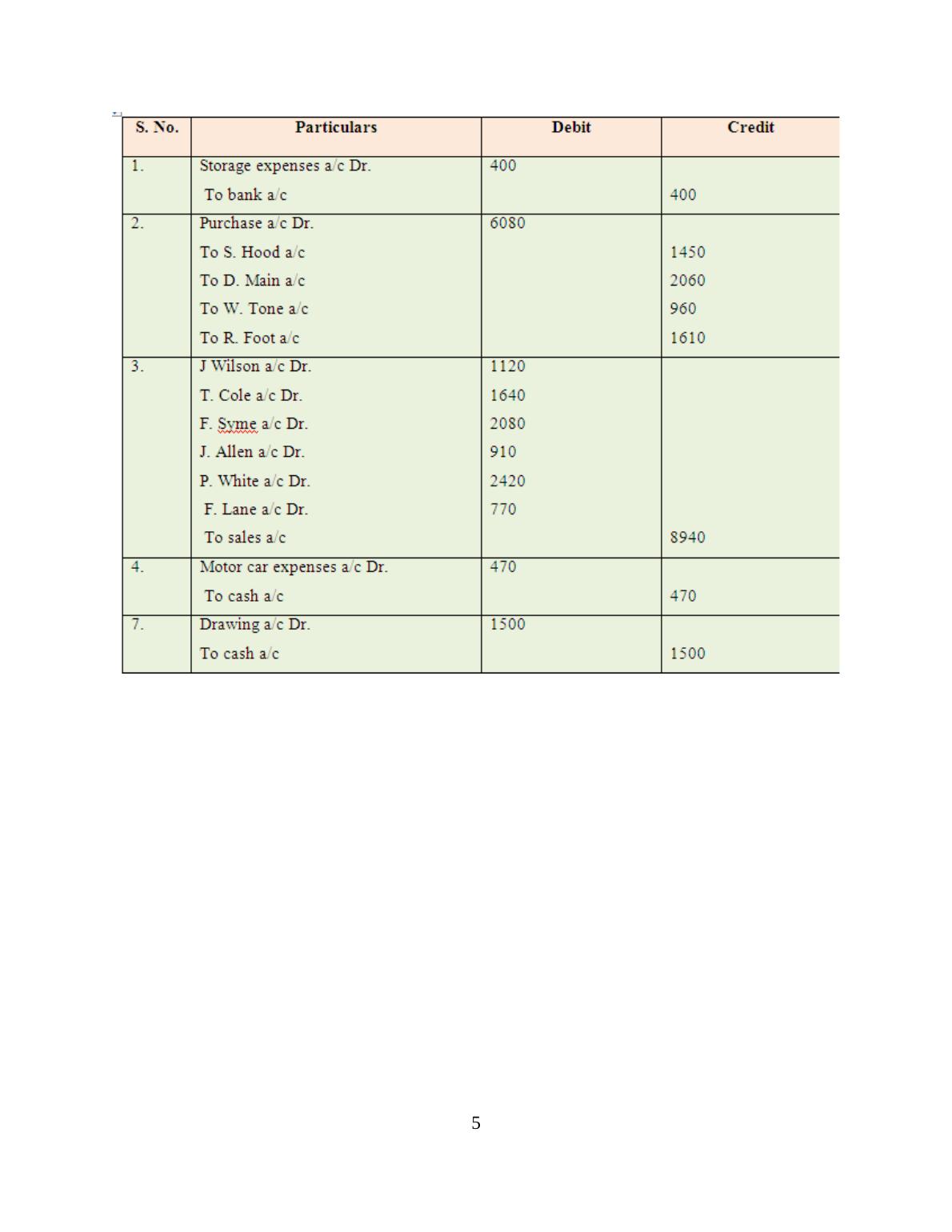

function in the market for longer period and will not be shut down in short time. Materiality: This principle states that only material items which takes place in the business maybe recorded as a business transaction. Company must disclosed the information which mightaffect the decision of the user of the financial information. The information which does notinfluence decision of user of accounting information must be ignored and should not bedisclosed in financial statements. 4. Discussing concepts of material disclosure as well as consistencyConsistency : This principle states that company should follow same accounting principles infuture periods so that reliability may be achieved easily (Pratt, 2016). This states that if frequentchanges are made in the accounting principles, then reliability is lost and financial statementsdoes not reflect accurate results. As a result, consistent accounting policies must be used byorganisation. Example, if company follows diminishing method for depreciation, then sameshould be followed in future periods as well. Material disclosure :This states that material items are needed to be monitored by accountingprofessionals while analysing profitability and efficiency of company to meet severalobjectives. All material items must be disclosed which influences economic decisions of usersof accounting information. CLIENT 11. Producing journal account for organisationFirst of all, balance sheet and income statement to be analysed which is presented byAlexandra and thereafter, journal entries will be presented. This helps to ascertain accurate andsummarized data set in the best possible way. 4

5

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Assignment on Financial Accounting pdflg...

|47

|5713

|177

Financial Accounting Principles: Assignmentlg...

|40

|3645

|142

Importance of Accounting in Preparation of Financial Statements - Reportlg...

|34

|4240

|26

Accounting Principles and Ruleslg...

|39

|4332

|322

Financial Accounting & Principles Assignmentlg...

|37

|2902

|88

UNIT 10 Financial Accounting : Assignmentlg...

|46

|4321

|262