Evaluation of Reporting Entity and Physical Capital Maintenance in Financial Reporting

VerifiedAdded on 2022/11/14

|16

|4108

|67

AI Summary

This report evaluates the concept of reporting entity and physical maintenance and their relevance in the financial reporting. It discusses the characteristics of a reporting entity and their application on government organizations. It also explains the concept of physical capital maintenance and its impact on increasing the decision usefulness of financial information. Lastly, it reviews the quality of AASB 137 disclosures in financial reports of Woolworth and Origin Energy.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Abstract

This report has carried out an evaluation of the concept of reporting entity and physical

maintenance and their relevance in the financial reporting. The different characteristics evaluated

of a reporting entity has inferred that public sector bodies can also be classified as a reporting

entity on the basis of the dependency of the users on the financial information provided by them.

Also, the concept of physical capital maintenance provided by IFRS for determining the profit

helps in enhanced economic-decision making of the users by providing actual profitability

position of a company generated from its capital base. In addition to this, the adoption of AASB

standard 137 is very essential or providing effective disclosure regarding the type of provision

and contingent assets and liabilities by the ASX listed entities.

2

This report has carried out an evaluation of the concept of reporting entity and physical

maintenance and their relevance in the financial reporting. The different characteristics evaluated

of a reporting entity has inferred that public sector bodies can also be classified as a reporting

entity on the basis of the dependency of the users on the financial information provided by them.

Also, the concept of physical capital maintenance provided by IFRS for determining the profit

helps in enhanced economic-decision making of the users by providing actual profitability

position of a company generated from its capital base. In addition to this, the adoption of AASB

standard 137 is very essential or providing effective disclosure regarding the type of provision

and contingent assets and liabilities by the ASX listed entities.

2

Contents

Introduction.................................................................................................................................................4

Part 1: Characteristics of a Reporting Entity and their Application on the Government Organizations......4

Part 2: Concept of Physical Capital Maintenance and its Impact on Increasing the Decision Usefulness of

Financial Information..................................................................................................................................6

Part 3: Quality of AASB 137 disclosures in financial reports of Woolworth and Origin Energy...................8

Provisions................................................................................................................................................8

Contingent Liabilities.............................................................................................................................13

Conclusion and Recommendation.............................................................................................................13

References.................................................................................................................................................15

3

Introduction.................................................................................................................................................4

Part 1: Characteristics of a Reporting Entity and their Application on the Government Organizations......4

Part 2: Concept of Physical Capital Maintenance and its Impact on Increasing the Decision Usefulness of

Financial Information..................................................................................................................................6

Part 3: Quality of AASB 137 disclosures in financial reports of Woolworth and Origin Energy...................8

Provisions................................................................................................................................................8

Contingent Liabilities.............................................................................................................................13

Conclusion and Recommendation.............................................................................................................13

References.................................................................................................................................................15

3

Introduction

This report is carried for the purpose of examining the various concepts and issues related

with the financial accounting and reporting. In this context, it primarily presents a discussion

about the concept and characteristics of a reporting entity as provided within the Statement of

Accounting Concept 1 (SAC1). Also, the application of the identified characteristics on

government organizations for classifying themselves as reporting entities have also been

conducted within the report. This is followed by discussing the concept of physical capital

maintenance and impact of it on the decision usefulness of financial information. Lastly, it

presents a review of the latest annual reports of two selected ASX listed entities that are

Woolworths Group and Origin Energy. The analysis is mainly carried out for comparing and

analyzing the disclosures related to provisions, contingent liabilities and assets as per the AASB

137 within their financial statements. The analysis is mainly intended to examine the compliance

of both the firms with the relevant accounting standards and thus ensuring quality financial

information presented to the end-users.

Part 1: Characteristics of a Reporting Entity and their Application on the

Government Organizations

The Statement of Accounting Concepts (SAC 1) provided by the AASB (Australian

Accounting Standards Board) has provided the definition of a reporting entity. The main purpose

of the statement is to provide a definition and explanation of a reporting entity and also to

provide a benchmark for the quality of financial reporting required by such entities. It has

outlines the various circumstances under which an economic entity should be classified as a

reporting entity. As per the standard, a reporting entity can be regarded as an entity that is

expected to develop and present its general purpose financial reports (GPFR) to the end-users.

Thus, it can be expected from a reporting entity that there are users who are dependent on its

financial information presented for making significant decisions by developing an understanding

of its financial position (Statement of Accounting Concepts, 2011). The different characteristics

of a reporting entity as outlined by the statement can be stated as follows:

As per the concept, a reporting entity need to be recognized by the presence of the users

and their relevant information needs to make significant economic decisions

4

This report is carried for the purpose of examining the various concepts and issues related

with the financial accounting and reporting. In this context, it primarily presents a discussion

about the concept and characteristics of a reporting entity as provided within the Statement of

Accounting Concept 1 (SAC1). Also, the application of the identified characteristics on

government organizations for classifying themselves as reporting entities have also been

conducted within the report. This is followed by discussing the concept of physical capital

maintenance and impact of it on the decision usefulness of financial information. Lastly, it

presents a review of the latest annual reports of two selected ASX listed entities that are

Woolworths Group and Origin Energy. The analysis is mainly carried out for comparing and

analyzing the disclosures related to provisions, contingent liabilities and assets as per the AASB

137 within their financial statements. The analysis is mainly intended to examine the compliance

of both the firms with the relevant accounting standards and thus ensuring quality financial

information presented to the end-users.

Part 1: Characteristics of a Reporting Entity and their Application on the

Government Organizations

The Statement of Accounting Concepts (SAC 1) provided by the AASB (Australian

Accounting Standards Board) has provided the definition of a reporting entity. The main purpose

of the statement is to provide a definition and explanation of a reporting entity and also to

provide a benchmark for the quality of financial reporting required by such entities. It has

outlines the various circumstances under which an economic entity should be classified as a

reporting entity. As per the standard, a reporting entity can be regarded as an entity that is

expected to develop and present its general purpose financial reports (GPFR) to the end-users.

Thus, it can be expected from a reporting entity that there are users who are dependent on its

financial information presented for making significant decisions by developing an understanding

of its financial position (Statement of Accounting Concepts, 2011). The different characteristics

of a reporting entity as outlined by the statement can be stated as follows:

As per the concept, a reporting entity need to be recognized by the presence of the users

and their relevant information needs to make significant economic decisions

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

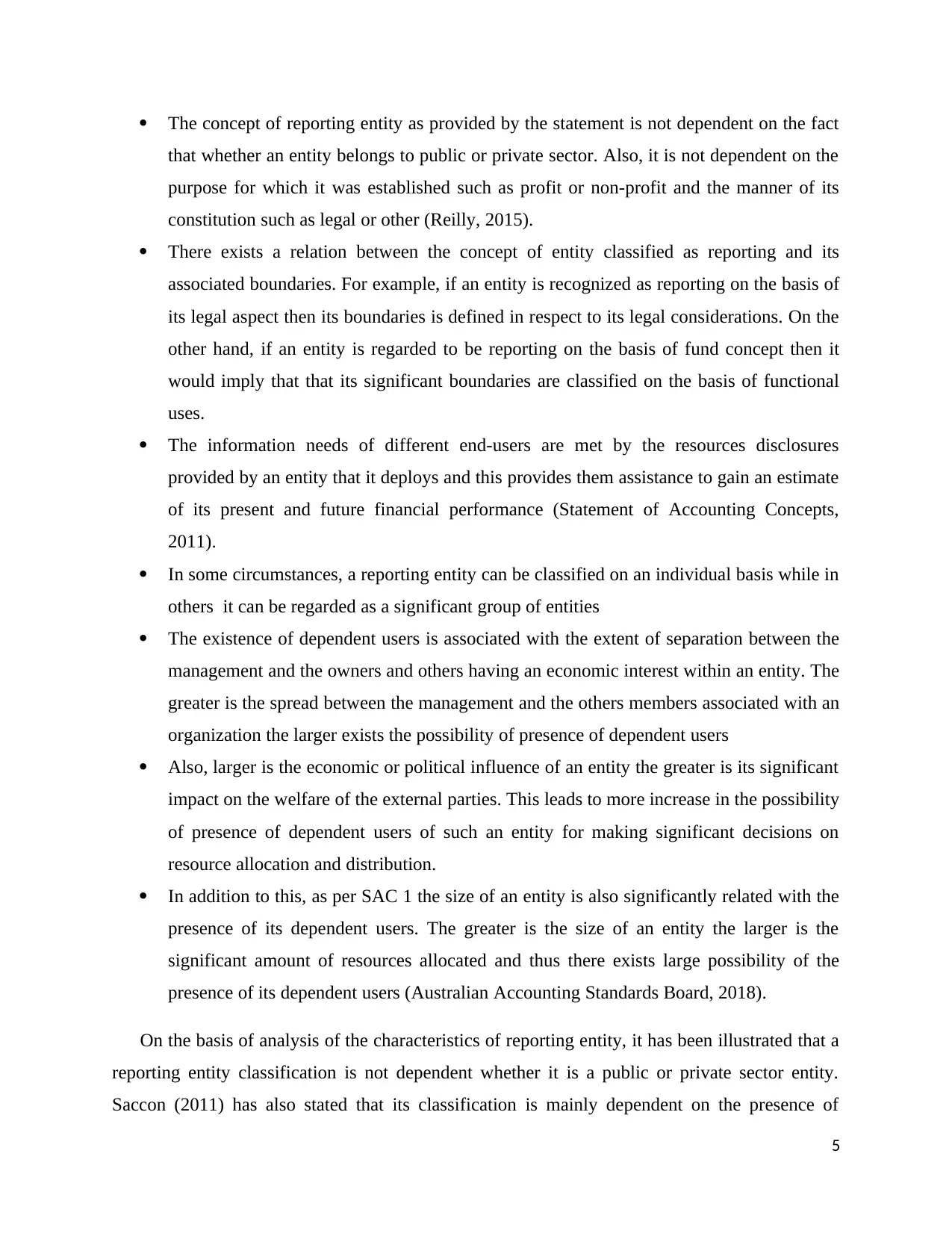

The concept of reporting entity as provided by the statement is not dependent on the fact

that whether an entity belongs to public or private sector. Also, it is not dependent on the

purpose for which it was established such as profit or non-profit and the manner of its

constitution such as legal or other (Reilly, 2015).

There exists a relation between the concept of entity classified as reporting and its

associated boundaries. For example, if an entity is recognized as reporting on the basis of

its legal aspect then its boundaries is defined in respect to its legal considerations. On the

other hand, if an entity is regarded to be reporting on the basis of fund concept then it

would imply that that its significant boundaries are classified on the basis of functional

uses.

The information needs of different end-users are met by the resources disclosures

provided by an entity that it deploys and this provides them assistance to gain an estimate

of its present and future financial performance (Statement of Accounting Concepts,

2011).

In some circumstances, a reporting entity can be classified on an individual basis while in

others it can be regarded as a significant group of entities

The existence of dependent users is associated with the extent of separation between the

management and the owners and others having an economic interest within an entity. The

greater is the spread between the management and the others members associated with an

organization the larger exists the possibility of presence of dependent users

Also, larger is the economic or political influence of an entity the greater is its significant

impact on the welfare of the external parties. This leads to more increase in the possibility

of presence of dependent users of such an entity for making significant decisions on

resource allocation and distribution.

In addition to this, as per SAC 1 the size of an entity is also significantly related with the

presence of its dependent users. The greater is the size of an entity the larger is the

significant amount of resources allocated and thus there exists large possibility of the

presence of its dependent users (Australian Accounting Standards Board, 2018).

On the basis of analysis of the characteristics of reporting entity, it has been illustrated that a

reporting entity classification is not dependent whether it is a public or private sector entity.

Saccon (2011) has also stated that its classification is mainly dependent on the presence of

5

that whether an entity belongs to public or private sector. Also, it is not dependent on the

purpose for which it was established such as profit or non-profit and the manner of its

constitution such as legal or other (Reilly, 2015).

There exists a relation between the concept of entity classified as reporting and its

associated boundaries. For example, if an entity is recognized as reporting on the basis of

its legal aspect then its boundaries is defined in respect to its legal considerations. On the

other hand, if an entity is regarded to be reporting on the basis of fund concept then it

would imply that that its significant boundaries are classified on the basis of functional

uses.

The information needs of different end-users are met by the resources disclosures

provided by an entity that it deploys and this provides them assistance to gain an estimate

of its present and future financial performance (Statement of Accounting Concepts,

2011).

In some circumstances, a reporting entity can be classified on an individual basis while in

others it can be regarded as a significant group of entities

The existence of dependent users is associated with the extent of separation between the

management and the owners and others having an economic interest within an entity. The

greater is the spread between the management and the others members associated with an

organization the larger exists the possibility of presence of dependent users

Also, larger is the economic or political influence of an entity the greater is its significant

impact on the welfare of the external parties. This leads to more increase in the possibility

of presence of dependent users of such an entity for making significant decisions on

resource allocation and distribution.

In addition to this, as per SAC 1 the size of an entity is also significantly related with the

presence of its dependent users. The greater is the size of an entity the larger is the

significant amount of resources allocated and thus there exists large possibility of the

presence of its dependent users (Australian Accounting Standards Board, 2018).

On the basis of analysis of the characteristics of reporting entity, it has been illustrated that a

reporting entity classification is not dependent whether it is a public or private sector entity.

Saccon (2011) has also stated that its classification is mainly dependent on the presence of

5

dependent users for such an entity due to which it is required to develop and disclose the GPFR.

There exist dependent users for the government organizations as illustrated by the characteristics

of a reporting entity discussed above. For example, there should be wide separation between the

management and the ownership for the presence of dependent users and this is present within a

government organization. The management people within a government organization are elected

by the parties having an economic interest that is general public (Saccon, 2011).

As such, it becomes their large responsibility for disclosing the significant information to the

external users. In addition to this, the public sector organizations have a large economic or

political influence and thus there exist large users of it that are dependent on the information

disclosed within its general purpose financial reports (Guerreiro, , Rodrigues and Craig, 2014).

Also, the public-sector entities are larger in size and thus own extensive resources and therefore

it needs to present information to the users for assisting their decision-making. Thus, it can be

said on the basis of different characteristics of a rpeoirting entity that public sector bodies

whether functioning at a federal, state or local level can be identified as reporting entity due to

presence of dependent users requiring financial information for making significant decisions and

ensuring their accountability (Statement of Accounting Concepts, 2011).

Part 2: Concept of Physical Capital Maintenance and its Impact on

Increasing the Decision Usefulness of Financial Information

Jianu and Gusatu (2011) has stated that the concept of capital maintenance in the

accounting is based on the principle that the income realized by an entity should be recognized

only after meeting all the significant costs of capital. The conceptual framework of accounting

has identified the two concepts of capital that a company needs to adopt for assessing its capital

base. In this context, the concept of physical capital maintenance concept has stated that capital

of an entity can be regarded as its production capacity that is it is mainly based on the outputs

units produced. Thus, as per the concept, an entity is said to have realized a profit when its

physical production capacity at the end of the reporting period exceeds as compared to the

beginning of the period (Australian Accounting Standards Board, 2018). The concept of physical

maintenance is not related with recognizing the significant cost that is associated with

maintaining the tangible assets such as equipments but it mainly emphasize on the ability of a

business entity to sustain the cash flows in the future context. This refers to maintaining the

6

There exist dependent users for the government organizations as illustrated by the characteristics

of a reporting entity discussed above. For example, there should be wide separation between the

management and the ownership for the presence of dependent users and this is present within a

government organization. The management people within a government organization are elected

by the parties having an economic interest that is general public (Saccon, 2011).

As such, it becomes their large responsibility for disclosing the significant information to the

external users. In addition to this, the public sector organizations have a large economic or

political influence and thus there exist large users of it that are dependent on the information

disclosed within its general purpose financial reports (Guerreiro, , Rodrigues and Craig, 2014).

Also, the public-sector entities are larger in size and thus own extensive resources and therefore

it needs to present information to the users for assisting their decision-making. Thus, it can be

said on the basis of different characteristics of a rpeoirting entity that public sector bodies

whether functioning at a federal, state or local level can be identified as reporting entity due to

presence of dependent users requiring financial information for making significant decisions and

ensuring their accountability (Statement of Accounting Concepts, 2011).

Part 2: Concept of Physical Capital Maintenance and its Impact on

Increasing the Decision Usefulness of Financial Information

Jianu and Gusatu (2011) has stated that the concept of capital maintenance in the

accounting is based on the principle that the income realized by an entity should be recognized

only after meeting all the significant costs of capital. The conceptual framework of accounting

has identified the two concepts of capital that a company needs to adopt for assessing its capital

base. In this context, the concept of physical capital maintenance concept has stated that capital

of an entity can be regarded as its production capacity that is it is mainly based on the outputs

units produced. Thus, as per the concept, an entity is said to have realized a profit when its

physical production capacity at the end of the reporting period exceeds as compared to the

beginning of the period (Australian Accounting Standards Board, 2018). The concept of physical

maintenance is not related with recognizing the significant cost that is associated with

maintaining the tangible assets such as equipments but it mainly emphasize on the ability of a

business entity to sustain the cash flows in the future context. This refers to maintaining the

6

access of a business entity to income generating assets in use within its business infrastructure.

The profit of an entity under the concept is recognized only if its operating capacity at the end of

an accounting period is greater than at the beginning by exclusion of any capital contributions or

distributions from the shareholders (Jianu and Gusatu, 2011).

As per the views of Collins, Pasewark and Riley (2012), it can be said that physical

maintenance concept provided by the IFRS is very useful for determination of the real profits of

an entity. However, the valuation of capital based on the concept is regarded to be largely

difficult because it does not take into account any of the monetary valuation but is only

conducted by analysis of the significant physical characteristics of the tangible assets. It is

mainly based on the evaluation of operating capacity of an entity that requires assessing the

productive assets and the assets that are required for producing the expected amount of goods

and services and maintaining the same operating capacity. The concept is significantly different

from the financial concept of maintaining capital as per which profit is recognized of the net

assets base at the end of a reporting period is higher than at the beginning of the accounting

period. The selection of accounting concept by a business entity to assess its capital base is

determined on the basis of the potential needs of the end-users of the financial report (Collins,

Pasewark and Riley, 2012).

According to Nowak (2013), the physical capital maintenance concept is mainly used if

the end-users need significant information about the operational capability of en entity. It adopts

the use of current cost base for measuring the value of assets and liabilities and requires the

development and presentation of an additional financial statement, that is, capital maintenance

adjustment, separable form the income statement. The concept is regarded to be highly useful for

providing the actual profitability position of a company as it does not take into consideration the

amount of capital contributed by the shareholders,. It only provides an assessment of the

enhancement in the physical productive capacity of an entity and the profit released directly

represents the increase in the capital over the respective period. The price changes impacting the

assets and liabilities of a company are regarded as changes in measuring the physical productive

capacity. Therefore, the economic users such as investors, creditors and other stakeholders can

determine the actual operational effectiveness of a company and its ability to utilize its capital

7

The profit of an entity under the concept is recognized only if its operating capacity at the end of

an accounting period is greater than at the beginning by exclusion of any capital contributions or

distributions from the shareholders (Jianu and Gusatu, 2011).

As per the views of Collins, Pasewark and Riley (2012), it can be said that physical

maintenance concept provided by the IFRS is very useful for determination of the real profits of

an entity. However, the valuation of capital based on the concept is regarded to be largely

difficult because it does not take into account any of the monetary valuation but is only

conducted by analysis of the significant physical characteristics of the tangible assets. It is

mainly based on the evaluation of operating capacity of an entity that requires assessing the

productive assets and the assets that are required for producing the expected amount of goods

and services and maintaining the same operating capacity. The concept is significantly different

from the financial concept of maintaining capital as per which profit is recognized of the net

assets base at the end of a reporting period is higher than at the beginning of the accounting

period. The selection of accounting concept by a business entity to assess its capital base is

determined on the basis of the potential needs of the end-users of the financial report (Collins,

Pasewark and Riley, 2012).

According to Nowak (2013), the physical capital maintenance concept is mainly used if

the end-users need significant information about the operational capability of en entity. It adopts

the use of current cost base for measuring the value of assets and liabilities and requires the

development and presentation of an additional financial statement, that is, capital maintenance

adjustment, separable form the income statement. The concept is regarded to be highly useful for

providing the actual profitability position of a company as it does not take into consideration the

amount of capital contributed by the shareholders,. It only provides an assessment of the

enhancement in the physical productive capacity of an entity and the profit released directly

represents the increase in the capital over the respective period. The price changes impacting the

assets and liabilities of a company are regarded as changes in measuring the physical productive

capacity. Therefore, the economic users such as investors, creditors and other stakeholders can

determine the actual operational effectiveness of a company and its ability to utilize its capital

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

base for generating profit. This helps in better economic decision-making by assessing the actual

profit realized from the capital base of a company (Nowak, 2013).

Part 3: Quality of AASB 137 disclosures in financial reports of

Woolworth and Origin Energy

AASB 137 refers to Australian accounting standard on Provisions, contingent liabilities

and contingent assets. AASB 137 was derived from IAS 37 and some paragraphs have been

added to improve the quality of reporting by Australian companies. The main objective of AASB

137 is to make sure that companies should have applied recognition criteria and basis of

measurement for provisions, contingent liabilities and contingent assets. This standard provides

relevant disclosures to be made by Australian companies to enable users to have knowledge of

nature, timing and amount of provision, contingent liability and contingent assets (AASB

Standard: AASB 137, 2014).

The two Australian companies selected to make a review of their quality of disclosure in

relation to AASB 137 are Woolworth and Origin Energy. Woolworth belongs to consumer

staples industry while Origin Energy is related to energy industry. Both of these companies are

regarded as reporting entity as SAC 1 and there are required to make full disclosure of

provisions, contingent liabilities and contingent assets as provided in AASB 137. Annual reports

of year 2018 have been selected for both companies to perform the review.

Provisions

Provisions refer to liability recognized in balance sheet as there is certainty of occurrence

of event but timing and amount cannot be defined. The main difference between provisions and

contingent liabilities is that provisions are recognized but contingent liabilities are not as their

existence is dependent upon the occurrence or non occurrence of uncertain future act and whose

control does not lies with the company. Recognition of provision is based truly on three criteria

such there must be present obligation because of past act, there is requirement to settle the

obligation using the resources (economic outflow of resources) and lastly reliable estimate can

be made to predict the amount of provision(AASB Standard: AASB 137, 2014).

Disclosures set out in AASB 137 in relation to provisions must be strictly followed while

recognizing each class of provisions. Woolworth has recognized three classes of provisions and

8

profit realized from the capital base of a company (Nowak, 2013).

Part 3: Quality of AASB 137 disclosures in financial reports of

Woolworth and Origin Energy

AASB 137 refers to Australian accounting standard on Provisions, contingent liabilities

and contingent assets. AASB 137 was derived from IAS 37 and some paragraphs have been

added to improve the quality of reporting by Australian companies. The main objective of AASB

137 is to make sure that companies should have applied recognition criteria and basis of

measurement for provisions, contingent liabilities and contingent assets. This standard provides

relevant disclosures to be made by Australian companies to enable users to have knowledge of

nature, timing and amount of provision, contingent liability and contingent assets (AASB

Standard: AASB 137, 2014).

The two Australian companies selected to make a review of their quality of disclosure in

relation to AASB 137 are Woolworth and Origin Energy. Woolworth belongs to consumer

staples industry while Origin Energy is related to energy industry. Both of these companies are

regarded as reporting entity as SAC 1 and there are required to make full disclosure of

provisions, contingent liabilities and contingent assets as provided in AASB 137. Annual reports

of year 2018 have been selected for both companies to perform the review.

Provisions

Provisions refer to liability recognized in balance sheet as there is certainty of occurrence

of event but timing and amount cannot be defined. The main difference between provisions and

contingent liabilities is that provisions are recognized but contingent liabilities are not as their

existence is dependent upon the occurrence or non occurrence of uncertain future act and whose

control does not lies with the company. Recognition of provision is based truly on three criteria

such there must be present obligation because of past act, there is requirement to settle the

obligation using the resources (economic outflow of resources) and lastly reliable estimate can

be made to predict the amount of provision(AASB Standard: AASB 137, 2014).

Disclosures set out in AASB 137 in relation to provisions must be strictly followed while

recognizing each class of provisions. Woolworth has recognized three classes of provisions and

8

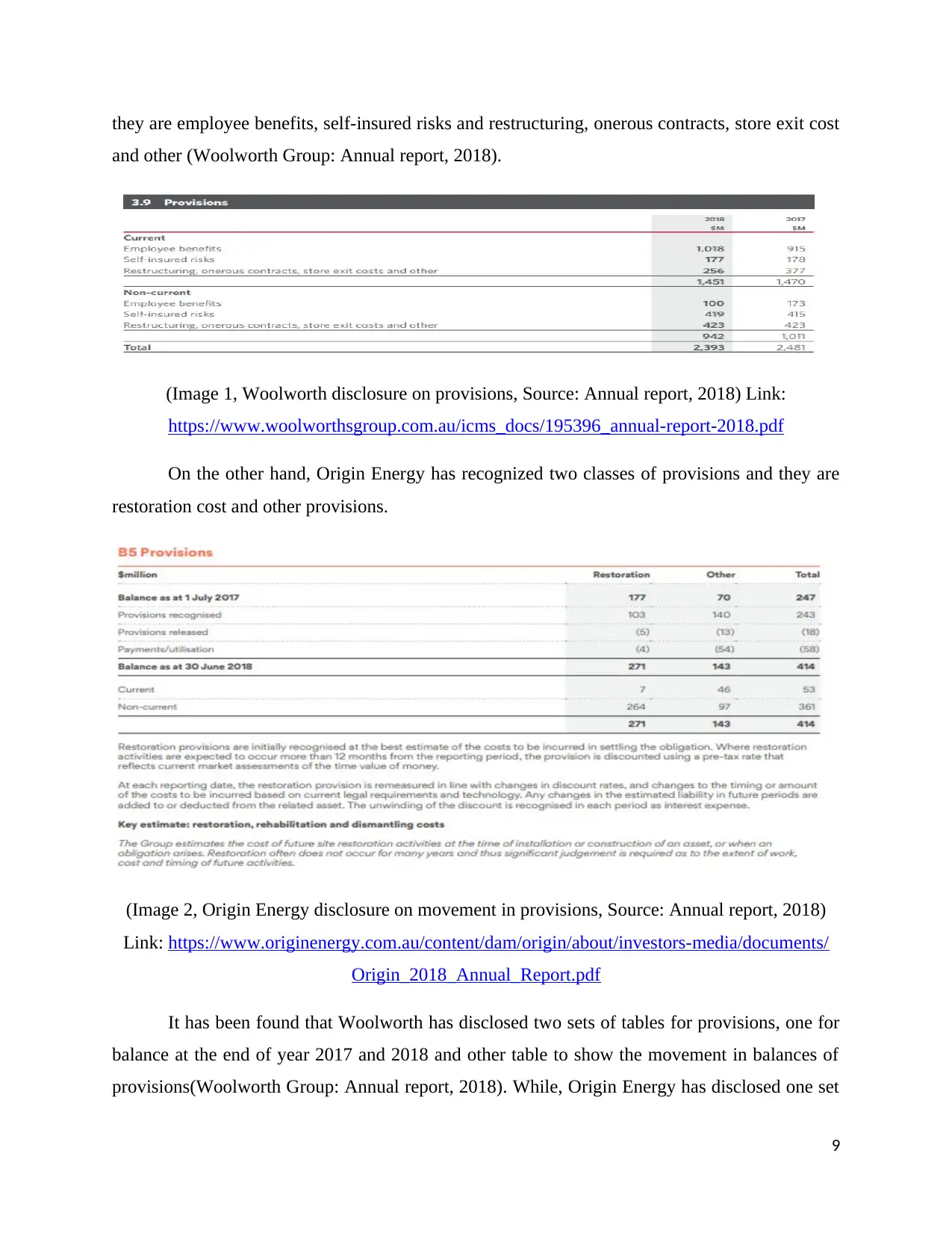

they are employee benefits, self-insured risks and restructuring, onerous contracts, store exit cost

and other (Woolworth Group: Annual report, 2018).

(Image 1, Woolworth disclosure on provisions, Source: Annual report, 2018) Link:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

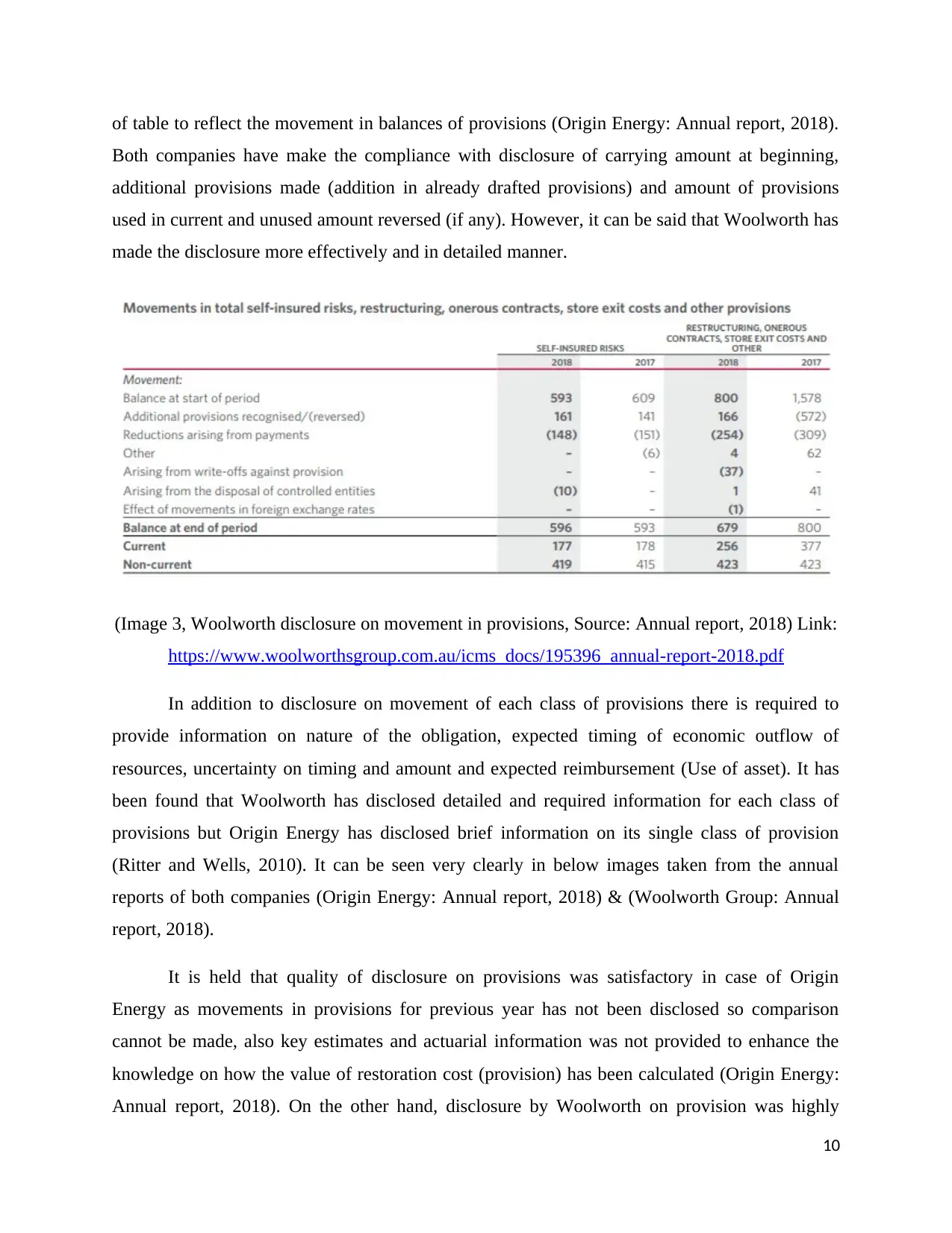

On the other hand, Origin Energy has recognized two classes of provisions and they are

restoration cost and other provisions.

(Image 2, Origin Energy disclosure on movement in provisions, Source: Annual report, 2018)

Link: https://www.originenergy.com.au/content/dam/origin/about/investors-media/documents/

Origin_2018_Annual_Report.pdf

It has been found that Woolworth has disclosed two sets of tables for provisions, one for

balance at the end of year 2017 and 2018 and other table to show the movement in balances of

provisions(Woolworth Group: Annual report, 2018). While, Origin Energy has disclosed one set

9

and other (Woolworth Group: Annual report, 2018).

(Image 1, Woolworth disclosure on provisions, Source: Annual report, 2018) Link:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

On the other hand, Origin Energy has recognized two classes of provisions and they are

restoration cost and other provisions.

(Image 2, Origin Energy disclosure on movement in provisions, Source: Annual report, 2018)

Link: https://www.originenergy.com.au/content/dam/origin/about/investors-media/documents/

Origin_2018_Annual_Report.pdf

It has been found that Woolworth has disclosed two sets of tables for provisions, one for

balance at the end of year 2017 and 2018 and other table to show the movement in balances of

provisions(Woolworth Group: Annual report, 2018). While, Origin Energy has disclosed one set

9

of table to reflect the movement in balances of provisions (Origin Energy: Annual report, 2018).

Both companies have make the compliance with disclosure of carrying amount at beginning,

additional provisions made (addition in already drafted provisions) and amount of provisions

used in current and unused amount reversed (if any). However, it can be said that Woolworth has

made the disclosure more effectively and in detailed manner.

(Image 3, Woolworth disclosure on movement in provisions, Source: Annual report, 2018) Link:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

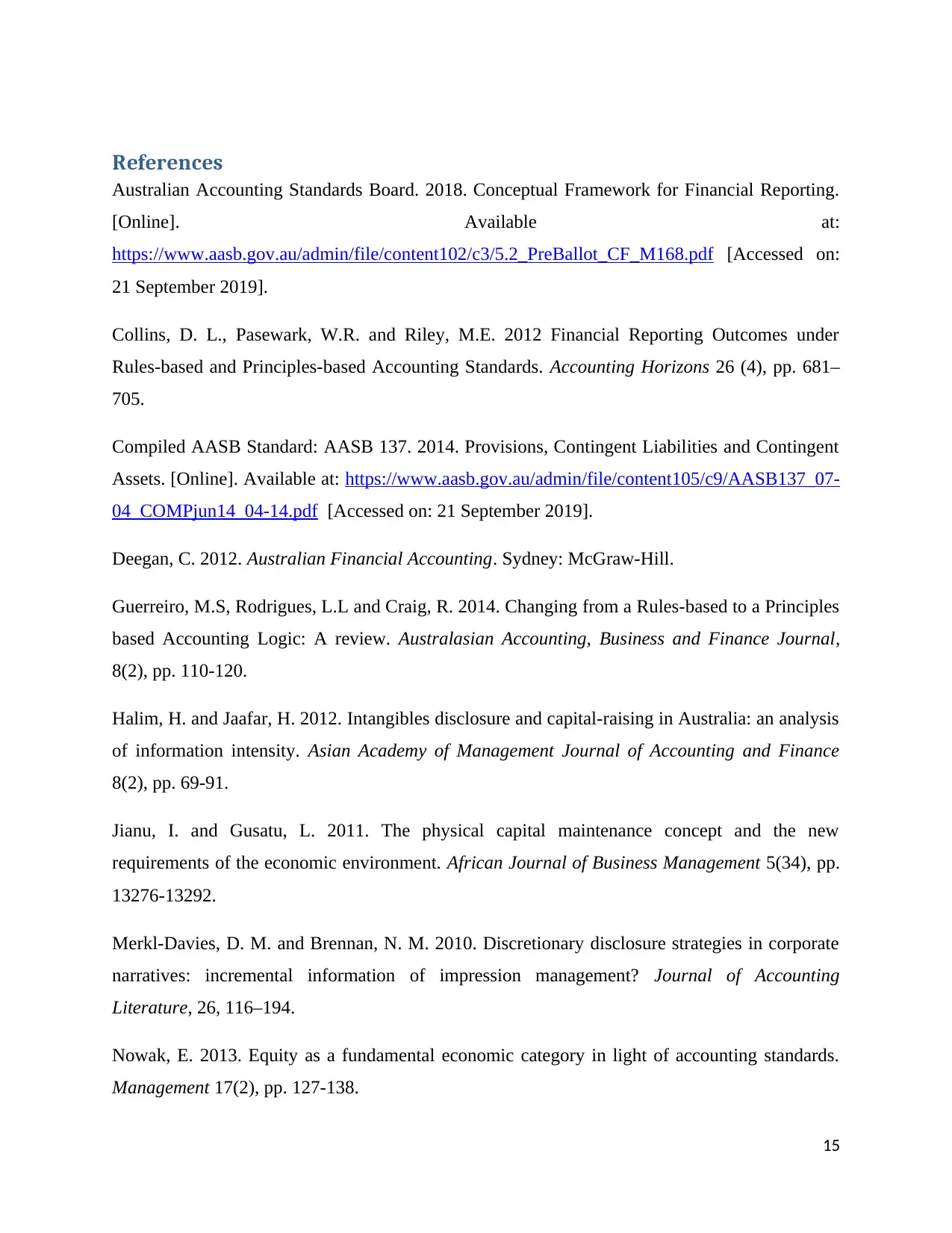

In addition to disclosure on movement of each class of provisions there is required to

provide information on nature of the obligation, expected timing of economic outflow of

resources, uncertainty on timing and amount and expected reimbursement (Use of asset). It has

been found that Woolworth has disclosed detailed and required information for each class of

provisions but Origin Energy has disclosed brief information on its single class of provision

(Ritter and Wells, 2010). It can be seen very clearly in below images taken from the annual

reports of both companies (Origin Energy: Annual report, 2018) & (Woolworth Group: Annual

report, 2018).

It is held that quality of disclosure on provisions was satisfactory in case of Origin

Energy as movements in provisions for previous year has not been disclosed so comparison

cannot be made, also key estimates and actuarial information was not provided to enhance the

knowledge on how the value of restoration cost (provision) has been calculated (Origin Energy:

Annual report, 2018). On the other hand, disclosure by Woolworth on provision was highly

10

Both companies have make the compliance with disclosure of carrying amount at beginning,

additional provisions made (addition in already drafted provisions) and amount of provisions

used in current and unused amount reversed (if any). However, it can be said that Woolworth has

made the disclosure more effectively and in detailed manner.

(Image 3, Woolworth disclosure on movement in provisions, Source: Annual report, 2018) Link:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

In addition to disclosure on movement of each class of provisions there is required to

provide information on nature of the obligation, expected timing of economic outflow of

resources, uncertainty on timing and amount and expected reimbursement (Use of asset). It has

been found that Woolworth has disclosed detailed and required information for each class of

provisions but Origin Energy has disclosed brief information on its single class of provision

(Ritter and Wells, 2010). It can be seen very clearly in below images taken from the annual

reports of both companies (Origin Energy: Annual report, 2018) & (Woolworth Group: Annual

report, 2018).

It is held that quality of disclosure on provisions was satisfactory in case of Origin

Energy as movements in provisions for previous year has not been disclosed so comparison

cannot be made, also key estimates and actuarial information was not provided to enhance the

knowledge on how the value of restoration cost (provision) has been calculated (Origin Energy:

Annual report, 2018). On the other hand, disclosure by Woolworth on provision was highly

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

satisfactory as all requirement of AASB 137 plus other information used to enhance user

decision process have been provided for each class of provision (Woolworth Group: Annual

report, 2018).

According to Merkl-Davies and Brennan (2010), it is mandatory for every company to

fulfill the minimum requirement of AASB 137 and disclose information such as nature, timing,

movement, valuation measurement and uncertainties related to each class of provisions. This

information is important to make useful decision and help users to know the future liabilities

pertinent with company (Deegan, 2012). However, mere disclosure on measurement basis

without providing key estimates decreases the quality of disclosure and lead to lack of

understanding on how provisions have been measured and there use to settle future liabilities. So,

it can be said that Woolworth has provided enhanced disclosure while Origin Energy has stick to

minimum disclosure required of AASB 137 (Origin Energy: Annual report, 2018).

11

decision process have been provided for each class of provision (Woolworth Group: Annual

report, 2018).

According to Merkl-Davies and Brennan (2010), it is mandatory for every company to

fulfill the minimum requirement of AASB 137 and disclose information such as nature, timing,

movement, valuation measurement and uncertainties related to each class of provisions. This

information is important to make useful decision and help users to know the future liabilities

pertinent with company (Deegan, 2012). However, mere disclosure on measurement basis

without providing key estimates decreases the quality of disclosure and lead to lack of

understanding on how provisions have been measured and there use to settle future liabilities. So,

it can be said that Woolworth has provided enhanced disclosure while Origin Energy has stick to

minimum disclosure required of AASB 137 (Origin Energy: Annual report, 2018).

11

(Image 4, Woolworth disclosure on nature, measurement and timing of each class of provisions,

Source: Annual report, 2018) Link:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

(Image 4, Woolworth disclosure on nature, measurement and timing of each class of provisions,

Source: Annual report, 2018) Link:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

(Image 5, Origin Energy disclosure on nature, measurement and timing of each class of

provisions, Source: Annual report, 2018) Link:

https://www.originenergy.com.au/content/dam/origin/about/investors-media/documents/

Origin_2018_Annual_Report.pdf

12

Source: Annual report, 2018) Link:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

(Image 4, Woolworth disclosure on nature, measurement and timing of each class of provisions,

Source: Annual report, 2018) Link:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

(Image 5, Origin Energy disclosure on nature, measurement and timing of each class of

provisions, Source: Annual report, 2018) Link:

https://www.originenergy.com.au/content/dam/origin/about/investors-media/documents/

Origin_2018_Annual_Report.pdf

12

Contingent Liabilities

Contingent liabilities is similar to provisions as it arises due to past events and its

occurrence is dependent upon the occurrence or non occurrence of future act which is uncertain

and not in control of entity. The only difference between provisions and contingent liability is

that under liabilities that can measured with sufficient reliability is termed as provisions and

when it is measured without sufficient reliability it is termed as contingent liabilities(AASB

Standard: AASB 137, 2014).

Woolworth and Origin Energy have recognized the contingent liabilities in notes to

accounts as provided by AASB 137. According to AASB 137, disclosure requirement of

contingent liabilities is limited as compared to provisions but it cannot be avoided Compiled

(AASB Standard: AASB 137, 2014). Woolworth has disclosed the liabilities against the

guarantees as a part of contingent liabilities because the probability of making the payment for

the guarantees provided has been considered remote. Woolworth discloses two types of

guarantees and it has not provided any information on how it is measured but independent

actuarial advice is used on whether guarantee should be recognized as contingent or

not(Woolworth Group: Annual report, 2018). On the other hand, Origin Energy has disclosed

detailed information on measurement and timing for each class of contingent liabilities (Origin

Energy: Annual report, 2018).

According to Halim and Jaafar (2012), information on contingent liabilities provides

useful information to user on future liabilities that can be occurred if any defined event takes

place. So, it is necessary to provide information on how each class of contingent liabilities

requires the outflow of economic resources when particular take place. There is also requirement

to disclosure percentage of probability of each event so that economic outflow can be measured.

Conclusion and Recommendation

The overall discussion held within the report has lead to developing a better

understanding of the concept and characteristics of a reporting entity. The different

characteristics of a reporting entity has inferred that government organizations also fulfils the

criteria of a reporting entity and hence need to adequately develop and present their general

13

Contingent liabilities is similar to provisions as it arises due to past events and its

occurrence is dependent upon the occurrence or non occurrence of future act which is uncertain

and not in control of entity. The only difference between provisions and contingent liability is

that under liabilities that can measured with sufficient reliability is termed as provisions and

when it is measured without sufficient reliability it is termed as contingent liabilities(AASB

Standard: AASB 137, 2014).

Woolworth and Origin Energy have recognized the contingent liabilities in notes to

accounts as provided by AASB 137. According to AASB 137, disclosure requirement of

contingent liabilities is limited as compared to provisions but it cannot be avoided Compiled

(AASB Standard: AASB 137, 2014). Woolworth has disclosed the liabilities against the

guarantees as a part of contingent liabilities because the probability of making the payment for

the guarantees provided has been considered remote. Woolworth discloses two types of

guarantees and it has not provided any information on how it is measured but independent

actuarial advice is used on whether guarantee should be recognized as contingent or

not(Woolworth Group: Annual report, 2018). On the other hand, Origin Energy has disclosed

detailed information on measurement and timing for each class of contingent liabilities (Origin

Energy: Annual report, 2018).

According to Halim and Jaafar (2012), information on contingent liabilities provides

useful information to user on future liabilities that can be occurred if any defined event takes

place. So, it is necessary to provide information on how each class of contingent liabilities

requires the outflow of economic resources when particular take place. There is also requirement

to disclosure percentage of probability of each event so that economic outflow can be measured.

Conclusion and Recommendation

The overall discussion held within the report has lead to developing a better

understanding of the concept and characteristics of a reporting entity. The different

characteristics of a reporting entity has inferred that government organizations also fulfils the

criteria of a reporting entity and hence need to adequately develop and present their general

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

purpose financial reports. In addition to this, the concept of physical capital maintenance is

useful in enhanced decision-making of a business entity by providing real profit position of an

entity. This is because it helps in assessing the actual profitability position of a company by

excluding the capital contributed from the shareholders. Also, the analysis of the AASB

standards 137 on the basis of examining the annual reports of two selected companies, that are,

Woolworths and Origin Energy, have inferred that it is highly necessary for the companies to

implement the use of the standard for providing adequate information in relation to the

provisions and contingent liabilities and assets. It has also been recommended form the analysis

held that ASX listed entities need to sufficiently disclose the information about each class of its

provisions and contingent assets and liabilities for improving the reliability and relevance to

financial information before the end-users.

14

useful in enhanced decision-making of a business entity by providing real profit position of an

entity. This is because it helps in assessing the actual profitability position of a company by

excluding the capital contributed from the shareholders. Also, the analysis of the AASB

standards 137 on the basis of examining the annual reports of two selected companies, that are,

Woolworths and Origin Energy, have inferred that it is highly necessary for the companies to

implement the use of the standard for providing adequate information in relation to the

provisions and contingent liabilities and assets. It has also been recommended form the analysis

held that ASX listed entities need to sufficiently disclose the information about each class of its

provisions and contingent assets and liabilities for improving the reliability and relevance to

financial information before the end-users.

14

References

Australian Accounting Standards Board. 2018. Conceptual Framework for Financial Reporting.

[Online]. Available at:

https://www.aasb.gov.au/admin/file/content102/c3/5.2_PreBallot_CF_M168.pdf [Accessed on:

21 September 2019].

Collins, D. L., Pasewark, W.R. and Riley, M.E. 2012 Financial Reporting Outcomes under

Rules-based and Principles-based Accounting Standards. Accounting Horizons 26 (4), pp. 681–

705.

Compiled AASB Standard: AASB 137. 2014. Provisions, Contingent Liabilities and Contingent

Assets. [Online]. Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB137_07-

04_COMPjun14_04-14.pdf [Accessed on: 21 September 2019].

Deegan, C. 2012. Australian Financial Accounting. Sydney: McGraw-Hill.

Guerreiro, M.S, Rodrigues, L.L and Craig, R. 2014. Changing from a Rules-based to a Principles

based Accounting Logic: A review. Australasian Accounting, Business and Finance Journal,

8(2), pp. 110-120.

Halim, H. and Jaafar, H. 2012. Intangibles disclosure and capital-raising in Australia: an analysis

of information intensity. Asian Academy of Management Journal of Accounting and Finance

8(2), pp. 69-91.

Jianu, I. and Gusatu, L. 2011. The physical capital maintenance concept and the new

requirements of the economic environment. African Journal of Business Management 5(34), pp.

13276-13292.

Merkl-Davies, D. M. and Brennan, N. M. 2010. Discretionary disclosure strategies in corporate

narratives: incremental information of impression management? Journal of Accounting

Literature, 26, 116–194.

Nowak, E. 2013. Equity as a fundamental economic category in light of accounting standards.

Management 17(2), pp. 127-138.

15

Australian Accounting Standards Board. 2018. Conceptual Framework for Financial Reporting.

[Online]. Available at:

https://www.aasb.gov.au/admin/file/content102/c3/5.2_PreBallot_CF_M168.pdf [Accessed on:

21 September 2019].

Collins, D. L., Pasewark, W.R. and Riley, M.E. 2012 Financial Reporting Outcomes under

Rules-based and Principles-based Accounting Standards. Accounting Horizons 26 (4), pp. 681–

705.

Compiled AASB Standard: AASB 137. 2014. Provisions, Contingent Liabilities and Contingent

Assets. [Online]. Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB137_07-

04_COMPjun14_04-14.pdf [Accessed on: 21 September 2019].

Deegan, C. 2012. Australian Financial Accounting. Sydney: McGraw-Hill.

Guerreiro, M.S, Rodrigues, L.L and Craig, R. 2014. Changing from a Rules-based to a Principles

based Accounting Logic: A review. Australasian Accounting, Business and Finance Journal,

8(2), pp. 110-120.

Halim, H. and Jaafar, H. 2012. Intangibles disclosure and capital-raising in Australia: an analysis

of information intensity. Asian Academy of Management Journal of Accounting and Finance

8(2), pp. 69-91.

Jianu, I. and Gusatu, L. 2011. The physical capital maintenance concept and the new

requirements of the economic environment. African Journal of Business Management 5(34), pp.

13276-13292.

Merkl-Davies, D. M. and Brennan, N. M. 2010. Discretionary disclosure strategies in corporate

narratives: incremental information of impression management? Journal of Accounting

Literature, 26, 116–194.

Nowak, E. 2013. Equity as a fundamental economic category in light of accounting standards.

Management 17(2), pp. 127-138.

15

Origin Energy: Annual report. 2018. [Online]. Available at:

https://www.originenergy.com.au/content/dam/origin/about/investors-media/documents/

Origin_2018_Annual_Report.pdf [Accessed on: 21 September 2019].

Reilly, K. 2015. Reporting Entities, Non-Reporting Entities and the Reduced Disclosure Regime.

Australian Accounting Review.

Ritter, A. and Wells, P. 2010. Identifiable intangible asset disclosures, stock prices and future

earnings. Accounting and Finance 46, 843–863.

Saccon, C. 2011. The Reporting Entity Concept in Australia: An Exploration of the Impact and

Comparison to International Standards. [Online]. Available at:

http://dspace.unive.it/bitstream/handle/10579/11964/866274-1226868.pdf?sequence=2

[Accessed on: 21 September 2019].

Statement of Accounting Concepts. 2011. Definition of a Reporting Entity. [Online]. Available

at: https://www.aasb.gov.au/admin/file/content102/c3/SAC1_8-90_2001V.pdf [Accessed on: 21

September 2019].

Woolworth Group: Annual report. 2018. [Online]. Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf [Accessed on:

21 September 2019].

16

https://www.originenergy.com.au/content/dam/origin/about/investors-media/documents/

Origin_2018_Annual_Report.pdf [Accessed on: 21 September 2019].

Reilly, K. 2015. Reporting Entities, Non-Reporting Entities and the Reduced Disclosure Regime.

Australian Accounting Review.

Ritter, A. and Wells, P. 2010. Identifiable intangible asset disclosures, stock prices and future

earnings. Accounting and Finance 46, 843–863.

Saccon, C. 2011. The Reporting Entity Concept in Australia: An Exploration of the Impact and

Comparison to International Standards. [Online]. Available at:

http://dspace.unive.it/bitstream/handle/10579/11964/866274-1226868.pdf?sequence=2

[Accessed on: 21 September 2019].

Statement of Accounting Concepts. 2011. Definition of a Reporting Entity. [Online]. Available

at: https://www.aasb.gov.au/admin/file/content102/c3/SAC1_8-90_2001V.pdf [Accessed on: 21

September 2019].

Woolworth Group: Annual report. 2018. [Online]. Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf [Accessed on:

21 September 2019].

16

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.