Financial Accounting Principle

VerifiedAdded on 2020/12/24

|36

|9395

|326

Project

AI Summary

This project provides a comprehensive guide to financial accounting principles, covering topics such as double-entry bookkeeping, trial balance preparation, financial statement analysis, and bank reconciliation. It explores the importance of accounting concepts, conventions, and regulations in ensuring accurate and reliable financial reporting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL

ACCOUNTING

PRINCIPLE

ACCOUNTING

PRINCIPLE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

BUSINESS REPORT......................................................................................................................1

Financial accounting and its purposes....................................................................................1

The regulations relating to financial accounting....................................................................2

Describe accounting rules and principles...............................................................................3

Explain the convections and concepts relating to consistency and material disclosure.........5

PART B............................................................................................................................................6

CLIENT 1........................................................................................................................................6

P1 Apply the double entry book keeping system of debits and credit and record sales and

purchases transactions in a general ledger..............................................................................6

M1 Analyse the transactions to show the progression from a previous trial balance to the next

one using double entry book keeping...................................................................................21

D1 Apply trial balance figures to show which statement of financial accounts they will end up

..............................................................................................................................................22

CLIENT 2......................................................................................................................................22

P3 Financial accounts from given trial balance figures adjusting, depreciation and preparation

..............................................................................................................................................22

P4 Financial accounts subject to sole traders, partnerships or limited companies...............23

M2 Evaluation of profit and loss account, balance sheet and cash flow statement..............24

D2 Compare the essential features of each financial statement to analyse the differences

between them in terms purpose, structure and content.........................................................24

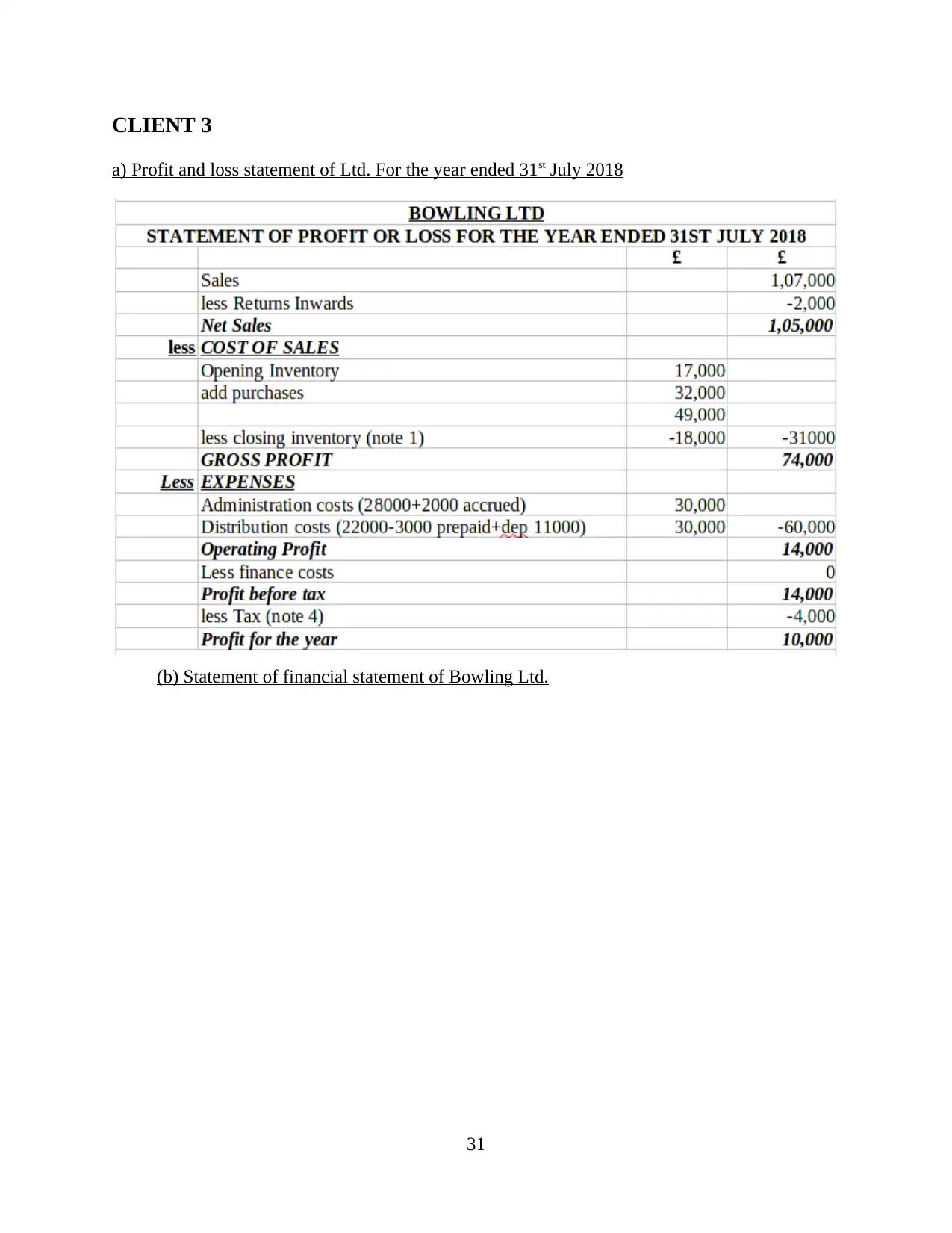

CLIENT 3......................................................................................................................................26

a) Profit and loss statement of Ltd. For the year ended 31st July 2018..............................26

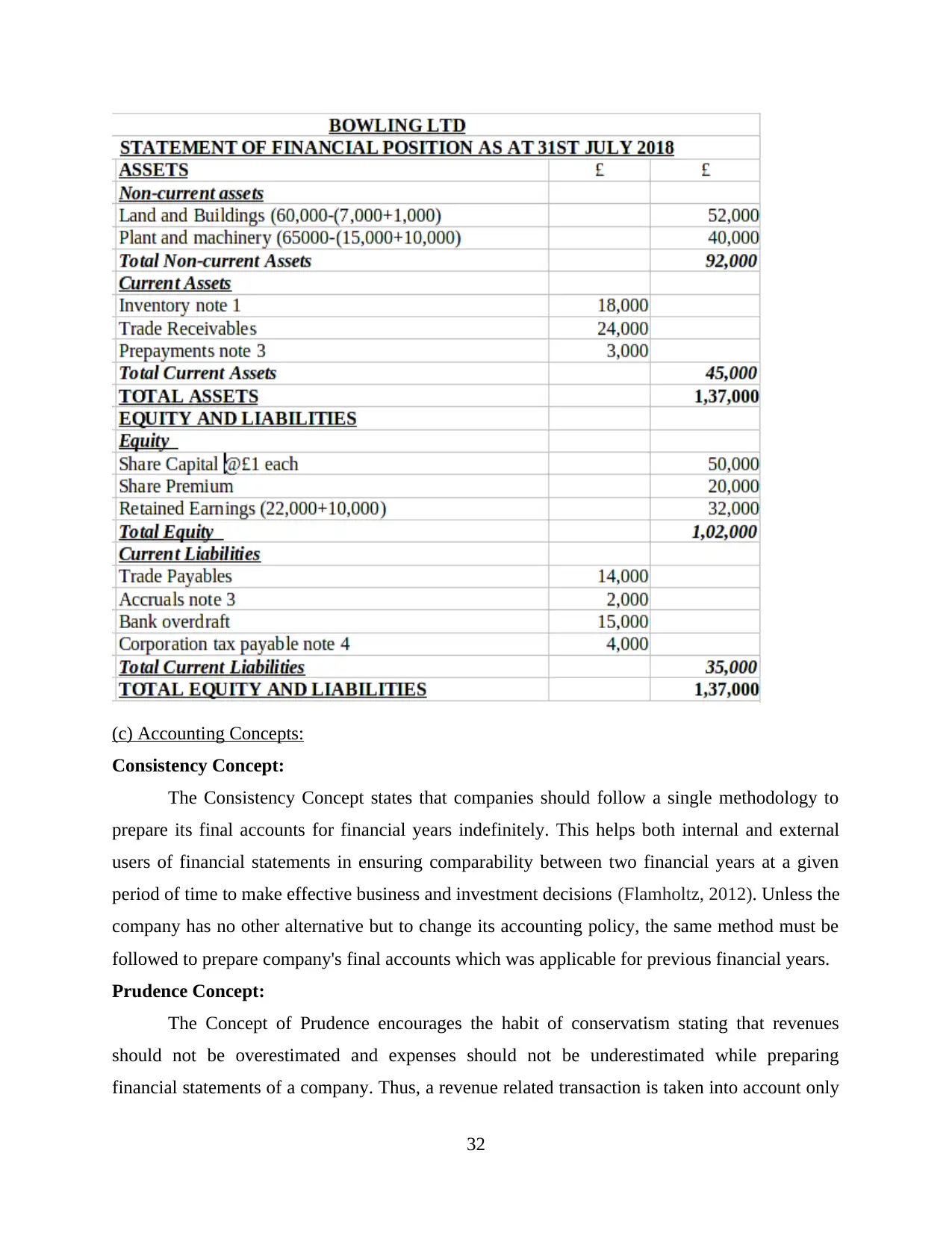

(b) Statement of financial statement of Bowling Ltd...........................................................26

(c) Accounting Concepts:.....................................................................................................27

(d) Purpose of Depreciation in formulating Accounting statements and the methods used for

calculation of Depreciation:.................................................................................................28

CLIENT 4......................................................................................................................................28

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

BUSINESS REPORT......................................................................................................................1

Financial accounting and its purposes....................................................................................1

The regulations relating to financial accounting....................................................................2

Describe accounting rules and principles...............................................................................3

Explain the convections and concepts relating to consistency and material disclosure.........5

PART B............................................................................................................................................6

CLIENT 1........................................................................................................................................6

P1 Apply the double entry book keeping system of debits and credit and record sales and

purchases transactions in a general ledger..............................................................................6

M1 Analyse the transactions to show the progression from a previous trial balance to the next

one using double entry book keeping...................................................................................21

D1 Apply trial balance figures to show which statement of financial accounts they will end up

..............................................................................................................................................22

CLIENT 2......................................................................................................................................22

P3 Financial accounts from given trial balance figures adjusting, depreciation and preparation

..............................................................................................................................................22

P4 Financial accounts subject to sole traders, partnerships or limited companies...............23

M2 Evaluation of profit and loss account, balance sheet and cash flow statement..............24

D2 Compare the essential features of each financial statement to analyse the differences

between them in terms purpose, structure and content.........................................................24

CLIENT 3......................................................................................................................................26

a) Profit and loss statement of Ltd. For the year ended 31st July 2018..............................26

(b) Statement of financial statement of Bowling Ltd...........................................................26

(c) Accounting Concepts:.....................................................................................................27

(d) Purpose of Depreciation in formulating Accounting statements and the methods used for

calculation of Depreciation:.................................................................................................28

CLIENT 4......................................................................................................................................28

P5 Apply the bank reconciliation process to make a number of a reconciliation................28

(a) Need and Importance of Bank Reconciliation Statements:............................................28

M3 Apply the reconciliation process demonstrating the use of deposit in transit................29

D3 Accurate bank reconciliation statement..........................................................................29

CLIENT 5......................................................................................................................................30

(a) Control account...............................................................................................................30

(b) Ledger control accounts..................................................................................................30

CLIENT 6......................................................................................................................................31

P6 Process to be taken to reconcile control accounts and clear suspense account...............31

M4 Understanding of the type of accounts and how and why these accounts need to

reconciled.............................................................................................................................31

CONCLUSION..............................................................................................................................32

REFERENCES..............................................................................................................................33

(a) Need and Importance of Bank Reconciliation Statements:............................................28

M3 Apply the reconciliation process demonstrating the use of deposit in transit................29

D3 Accurate bank reconciliation statement..........................................................................29

CLIENT 5......................................................................................................................................30

(a) Control account...............................................................................................................30

(b) Ledger control accounts..................................................................................................30

CLIENT 6......................................................................................................................................31

P6 Process to be taken to reconcile control accounts and clear suspense account...............31

M4 Understanding of the type of accounts and how and why these accounts need to

reconciled.............................................................................................................................31

CONCLUSION..............................................................................................................................32

REFERENCES..............................................................................................................................33

INTRODUCTION

Financial accounting is the process of recording, summarizing and reporting the

transaction in final report or statement such as cash flow, income statement and balance sheet

(Tassadaq and Malik, 2015). The final reports are prepared through accounting standards that are

followed by every organisation. These standards help to prepare financial statement in

appropriate format and show performance of the company in front of creditors, suppliers and

customers. Purpose of financial accounting is to provide accurate information about company to

existing and potential stakeholders regarding investment decisions. Oktra, a small organization

which based on UK has been chosen for this project.

This project report focused on double entry book keeping system and extract a trial

balance. There is statement of financial accounts according to sole traders, partnership and

limited companies. Creating a bank reconciliation statement, use of suspense account and way in

which it can help to ignore errors in trial balance.

PART A

BUSINESS REPORT

Financial accounting and its purposes

Financial accounting is a specialized branch of accounting that is used by several

companies to record, analyse, monitor and control various transaction of business. With the help

of this the company can track all records and create a detailed summary related to its financial

transactions. In the company when accounts are produced and displayed of financial information

in reports and presented in front of customers, creditor, suppliers of an organisation. Financial

accounting consists of different statements such as trading account to ascertain gross profit/loss,

Income statement account for net profit/net loss, cash flow to know different activities of

business relating to investment, operation and financial and balance sheet for present

performance of company (Maskell, Baggaley and Grasso, 2016). Oktra can attract more

investors by providing them reliable financial information of their organisational operational

activities. It is very essential for Oktra since it provides all the necessary information that is

needed by public for investment purposes. With the help of these statements the investors know

about financial strength of the business and an analysis of weak points that need to be contained.

It provides help to Oktra's top management to take effective and appropriate decisions regarding

1

Financial accounting is the process of recording, summarizing and reporting the

transaction in final report or statement such as cash flow, income statement and balance sheet

(Tassadaq and Malik, 2015). The final reports are prepared through accounting standards that are

followed by every organisation. These standards help to prepare financial statement in

appropriate format and show performance of the company in front of creditors, suppliers and

customers. Purpose of financial accounting is to provide accurate information about company to

existing and potential stakeholders regarding investment decisions. Oktra, a small organization

which based on UK has been chosen for this project.

This project report focused on double entry book keeping system and extract a trial

balance. There is statement of financial accounts according to sole traders, partnership and

limited companies. Creating a bank reconciliation statement, use of suspense account and way in

which it can help to ignore errors in trial balance.

PART A

BUSINESS REPORT

Financial accounting and its purposes

Financial accounting is a specialized branch of accounting that is used by several

companies to record, analyse, monitor and control various transaction of business. With the help

of this the company can track all records and create a detailed summary related to its financial

transactions. In the company when accounts are produced and displayed of financial information

in reports and presented in front of customers, creditor, suppliers of an organisation. Financial

accounting consists of different statements such as trading account to ascertain gross profit/loss,

Income statement account for net profit/net loss, cash flow to know different activities of

business relating to investment, operation and financial and balance sheet for present

performance of company (Maskell, Baggaley and Grasso, 2016). Oktra can attract more

investors by providing them reliable financial information of their organisational operational

activities. It is very essential for Oktra since it provides all the necessary information that is

needed by public for investment purposes. With the help of these statements the investors know

about financial strength of the business and an analysis of weak points that need to be contained.

It provides help to Oktra's top management to take effective and appropriate decisions regarding

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

company in order to achieve their set objectives and goals. Different types of financial

statements are prepared that are important for a business, they are as follows -

Profit and loss statement - The statement of profit and loss is one of the company's core

financial statements that present their profit and loss for a specific time period. There is

calculated net profit and loss after determination of all revenues, incomes and other operating

and non-operating activities. It is an essential part of one of three statements that is used by Oktra

to present their performance. On an income statement, Revenues – Expenses = Net income. The

statement is prepared according to time period and follow operations of company. It is very

important for a business to keep a detailed information of its revenues to pay different expenses

such as taxes, interest, commission etc. (Francis, and et. Al, 2015).

Balance sheet – A balance sheet is a statement of the financial status of a company

which refers to the assets, liabilities and owners’ equity at a specific time. In additional way, it

represents the net worth of a business. With the help of balance sheet the financial position of

Oktra can be provided to its shareholders, customers, suppliers, investors and other external

activities. On a balance sheet, Assets = Liabilities + Stockholders' equity. It is divided into two

sections, left side of the balance sheet outlines all assets and in right side outlines all liabilities

and shareholders' equity.

Cash flow statement – It is a statement which is used to measure all transactions related

to cash that are done by business in a particular financial year. Cash flow statement is divided

into three categories– cash flow from operating activities, cash flow from investing activities and

cash flow from financing activities. It is important to know that cash flow is not the same as net

income because it does not involve actual transfer of money (Collins, Pasewark and Riley, 2012)

.

Purpose of financial accounting -

It is providing financial information about the performance, cash flows and financial

position of the company.

This financial information helps to take investment, credit and taxation decisions

regarding to company.

The regulations relating to financial accounting

For better understanding, different types rules, regulations and principles have been

developed for proper formulation of organization's financial statements. These regulations are

2

statements are prepared that are important for a business, they are as follows -

Profit and loss statement - The statement of profit and loss is one of the company's core

financial statements that present their profit and loss for a specific time period. There is

calculated net profit and loss after determination of all revenues, incomes and other operating

and non-operating activities. It is an essential part of one of three statements that is used by Oktra

to present their performance. On an income statement, Revenues – Expenses = Net income. The

statement is prepared according to time period and follow operations of company. It is very

important for a business to keep a detailed information of its revenues to pay different expenses

such as taxes, interest, commission etc. (Francis, and et. Al, 2015).

Balance sheet – A balance sheet is a statement of the financial status of a company

which refers to the assets, liabilities and owners’ equity at a specific time. In additional way, it

represents the net worth of a business. With the help of balance sheet the financial position of

Oktra can be provided to its shareholders, customers, suppliers, investors and other external

activities. On a balance sheet, Assets = Liabilities + Stockholders' equity. It is divided into two

sections, left side of the balance sheet outlines all assets and in right side outlines all liabilities

and shareholders' equity.

Cash flow statement – It is a statement which is used to measure all transactions related

to cash that are done by business in a particular financial year. Cash flow statement is divided

into three categories– cash flow from operating activities, cash flow from investing activities and

cash flow from financing activities. It is important to know that cash flow is not the same as net

income because it does not involve actual transfer of money (Collins, Pasewark and Riley, 2012)

.

Purpose of financial accounting -

It is providing financial information about the performance, cash flows and financial

position of the company.

This financial information helps to take investment, credit and taxation decisions

regarding to company.

The regulations relating to financial accounting

For better understanding, different types rules, regulations and principles have been

developed for proper formulation of organization's financial statements. These regulations are

2

help to maintain their financial account in an accurate way. All companies including Oktra

follow particular rules and regulations of financial accounting applicable to it. These regulations

provide guidance to investor for analysis of income statements, balance sheet and cash flow

statement. These regulations are introduced by regulatory authority of a country for recording

information in financial statement in appropriate way (Watrin, Pott and Ullmann, 2012). It is

possible to get reliable information from various statement. There are following reliable

regulations -

IFRS – International financial reporting standard was introduced a set of world wide

language. The businesses are using standards for their accounts and mangers apply them to

expand their business globally. There is continuous application of different accounting standards

according to different transactions.

IASB – International accounting standard board is a regularity authority who is liable to

introduce and develop several international financial accounting standards. It has been

introduced by IFRS that are formulated to guide organisations while preparing financial

accounts. At time when organisations are recording transactions in books they follow their rules

and regulations.

IFRS 9 – It is applied in financial accounting instruments for different financial

statements. With the help of this regulation the company can easily measure and identify their

financial assets.

IFRS 10 – It provides a guideline to combined businesses who formulate their financial

statements in consolidated form. It is mainly developed for parent entity which is responsible for

their subsidiaries.

Describe accounting rules and principles

Accounting principles are a set of rules and guidelines followed by companies while

preparing a financial report. The principles of accounting define particular criteria under which

all companies have to maintain their economic transactions in accounting books. There are

following accounting principles -

Business entity concept –

The business entity concept defines that entity of a business are presented as separate

legal entity distinct from its members (Lobo and Zhao, 2013). It means Oktra has a personal

identification on the basis of which it can carry out transactions in its own name, sue or be sued

3

follow particular rules and regulations of financial accounting applicable to it. These regulations

provide guidance to investor for analysis of income statements, balance sheet and cash flow

statement. These regulations are introduced by regulatory authority of a country for recording

information in financial statement in appropriate way (Watrin, Pott and Ullmann, 2012). It is

possible to get reliable information from various statement. There are following reliable

regulations -

IFRS – International financial reporting standard was introduced a set of world wide

language. The businesses are using standards for their accounts and mangers apply them to

expand their business globally. There is continuous application of different accounting standards

according to different transactions.

IASB – International accounting standard board is a regularity authority who is liable to

introduce and develop several international financial accounting standards. It has been

introduced by IFRS that are formulated to guide organisations while preparing financial

accounts. At time when organisations are recording transactions in books they follow their rules

and regulations.

IFRS 9 – It is applied in financial accounting instruments for different financial

statements. With the help of this regulation the company can easily measure and identify their

financial assets.

IFRS 10 – It provides a guideline to combined businesses who formulate their financial

statements in consolidated form. It is mainly developed for parent entity which is responsible for

their subsidiaries.

Describe accounting rules and principles

Accounting principles are a set of rules and guidelines followed by companies while

preparing a financial report. The principles of accounting define particular criteria under which

all companies have to maintain their economic transactions in accounting books. There are

following accounting principles -

Business entity concept –

The business entity concept defines that entity of a business are presented as separate

legal entity distinct from its members (Lobo and Zhao, 2013). It means Oktra has a personal

identification on the basis of which it can carry out transactions in its own name, sue or be sued

3

and open account in bank. If all members leave the company there will be no impact seen on the

existence of Oktra, it will exist regardless.

Dual aspect concept –

According to this concept most of the companies follow this principle to show accurate

amount of particular transaction by recording it twice. If Oktra selects a single entry system it

would lead to irrelevant information since only one aspect of every transaction would be

recorded in its books. Therefore, to avoid this problem, financial accounting assure that every

single transaction has two aspects- debit side and credit side.

Money measurement concept –

The principle of money measurement is based on money value, it means only those

transactions shall be recorded in the books of Oktra that can be measured in money.

Cost principle –

From an accounting point of view, the term cost refers to the amount expended to

acquire an asset for business purposes. According to this principle, amounts are recorded at their

acquisition cost at the time of its purchase or acquisition in a financial year with an appropriation

for depreciation thereafter (Brief and Peasnell, 2013).

Going concern concept –

In this principle of accounting the business has expected to continue for long time as an

entity. This concept does not concern members of the company since it is a separate identity

expected to continue business perpetually.

Financial accounting year –

According to this principle, each business follows a particular financial year to prepare

their accounting books for quarterly, monthly or yearly basis. Generally, accounting period

adopted by companies is 1 April to 31 march as financial year.

Matching principle -

According to this principle, all expenses must be matched with their related revenues

generated in same accounting period. It means expenses and revenues are recorded in books of

same accounting year.

Accounting rules -

4

existence of Oktra, it will exist regardless.

Dual aspect concept –

According to this concept most of the companies follow this principle to show accurate

amount of particular transaction by recording it twice. If Oktra selects a single entry system it

would lead to irrelevant information since only one aspect of every transaction would be

recorded in its books. Therefore, to avoid this problem, financial accounting assure that every

single transaction has two aspects- debit side and credit side.

Money measurement concept –

The principle of money measurement is based on money value, it means only those

transactions shall be recorded in the books of Oktra that can be measured in money.

Cost principle –

From an accounting point of view, the term cost refers to the amount expended to

acquire an asset for business purposes. According to this principle, amounts are recorded at their

acquisition cost at the time of its purchase or acquisition in a financial year with an appropriation

for depreciation thereafter (Brief and Peasnell, 2013).

Going concern concept –

In this principle of accounting the business has expected to continue for long time as an

entity. This concept does not concern members of the company since it is a separate identity

expected to continue business perpetually.

Financial accounting year –

According to this principle, each business follows a particular financial year to prepare

their accounting books for quarterly, monthly or yearly basis. Generally, accounting period

adopted by companies is 1 April to 31 march as financial year.

Matching principle -

According to this principle, all expenses must be matched with their related revenues

generated in same accounting period. It means expenses and revenues are recorded in books of

same accounting year.

Accounting rules -

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For recording transaction in accounting books, we follow 'Three Golden Rules'. Double

entry system is followed to show dual effect of each transaction. The Three Golden Rules relate

to personal account, real account and nominal account. Basic rules are as follows -

1. Debit the receiver and credit the giver : This rule is applicable on Personal Account,

which is related to any individual, company or firm. Since in eyes of law, companies and

firms are legal entities considered as legal person (Nilsson and Stockenstrand, 2015).

This rule means, a person who receives something on behalf of Oktra is called Receiver

and amount is posted in debit column of their account, and same as if any person paid

something on behalf of Oktra is called Giver and amount will be posted in credit column

of their account.

2. Debit what comes in and credit what goes out : This principle is used for Real Account,

which includes all assets of organisation like machinery, building , land etc. And those

assets which come in business through purchase they will be debited in it's account and

anything going from business through sales will be credited in it's account.

3. Debit all expenses and credit all incomes : This principle is used for Nominal Account, it

includes all expenses and all incomes and gains of organisation. In this rule, we debit all

expenses and credit all incomes and gains incurred/received in organisation at the time of

production or sale respectively.

Explain the convections and concepts relating to consistency and material disclosure

Consistency convections – This convection of accounting states that it is used to

maintain a record with the same concept that was followed in previous years. Oktra will continue

to use it in same sequence in financial periods. To show effects in accounting results appropriate

methods should be adopted in case changes are made in accounting policies. Hence, the concept

of consistency assures that policies, method and practices of preparing the financial statements

remains same (Kirsch, 2012). This will help to easily analyse financial information from past

years. For investment decisions, internal and external shareholders analyse financial information

from past activities. Business consistency needs to be maintained for smooth auditing processes.

This concept helps in effortless comparison of financial performance from one period to another.

Material disclosure convention - The Convection of full material disclosure requires

revelation of all information, both favourable and non-favourable regarding to a business

enterprise. These material value are fully disclosed in annual report regarding to debtors and

5

entry system is followed to show dual effect of each transaction. The Three Golden Rules relate

to personal account, real account and nominal account. Basic rules are as follows -

1. Debit the receiver and credit the giver : This rule is applicable on Personal Account,

which is related to any individual, company or firm. Since in eyes of law, companies and

firms are legal entities considered as legal person (Nilsson and Stockenstrand, 2015).

This rule means, a person who receives something on behalf of Oktra is called Receiver

and amount is posted in debit column of their account, and same as if any person paid

something on behalf of Oktra is called Giver and amount will be posted in credit column

of their account.

2. Debit what comes in and credit what goes out : This principle is used for Real Account,

which includes all assets of organisation like machinery, building , land etc. And those

assets which come in business through purchase they will be debited in it's account and

anything going from business through sales will be credited in it's account.

3. Debit all expenses and credit all incomes : This principle is used for Nominal Account, it

includes all expenses and all incomes and gains of organisation. In this rule, we debit all

expenses and credit all incomes and gains incurred/received in organisation at the time of

production or sale respectively.

Explain the convections and concepts relating to consistency and material disclosure

Consistency convections – This convection of accounting states that it is used to

maintain a record with the same concept that was followed in previous years. Oktra will continue

to use it in same sequence in financial periods. To show effects in accounting results appropriate

methods should be adopted in case changes are made in accounting policies. Hence, the concept

of consistency assures that policies, method and practices of preparing the financial statements

remains same (Kirsch, 2012). This will help to easily analyse financial information from past

years. For investment decisions, internal and external shareholders analyse financial information

from past activities. Business consistency needs to be maintained for smooth auditing processes.

This concept helps in effortless comparison of financial performance from one period to another.

Material disclosure convention - The Convection of full material disclosure requires

revelation of all information, both favourable and non-favourable regarding to a business

enterprise. These material value are fully disclosed in annual report regarding to debtors and

5

creditors. IFRS 7 also states that financial information of preceding financial year must be

disclosed in front of its users. Users include both internal and external user. External users

concern suppliers, financial institutions that provide loans for industrial growth, tax authorities

and potential investors and many more. Internal users include top-level managers, middle-level

managers, lower-lever managers and board of directors (Bryer, 2013).

PART B

CLIENT 1

P1 Apply the double entry book keeping system of debits and credit and record sales and

purchases transactions in a general ledger

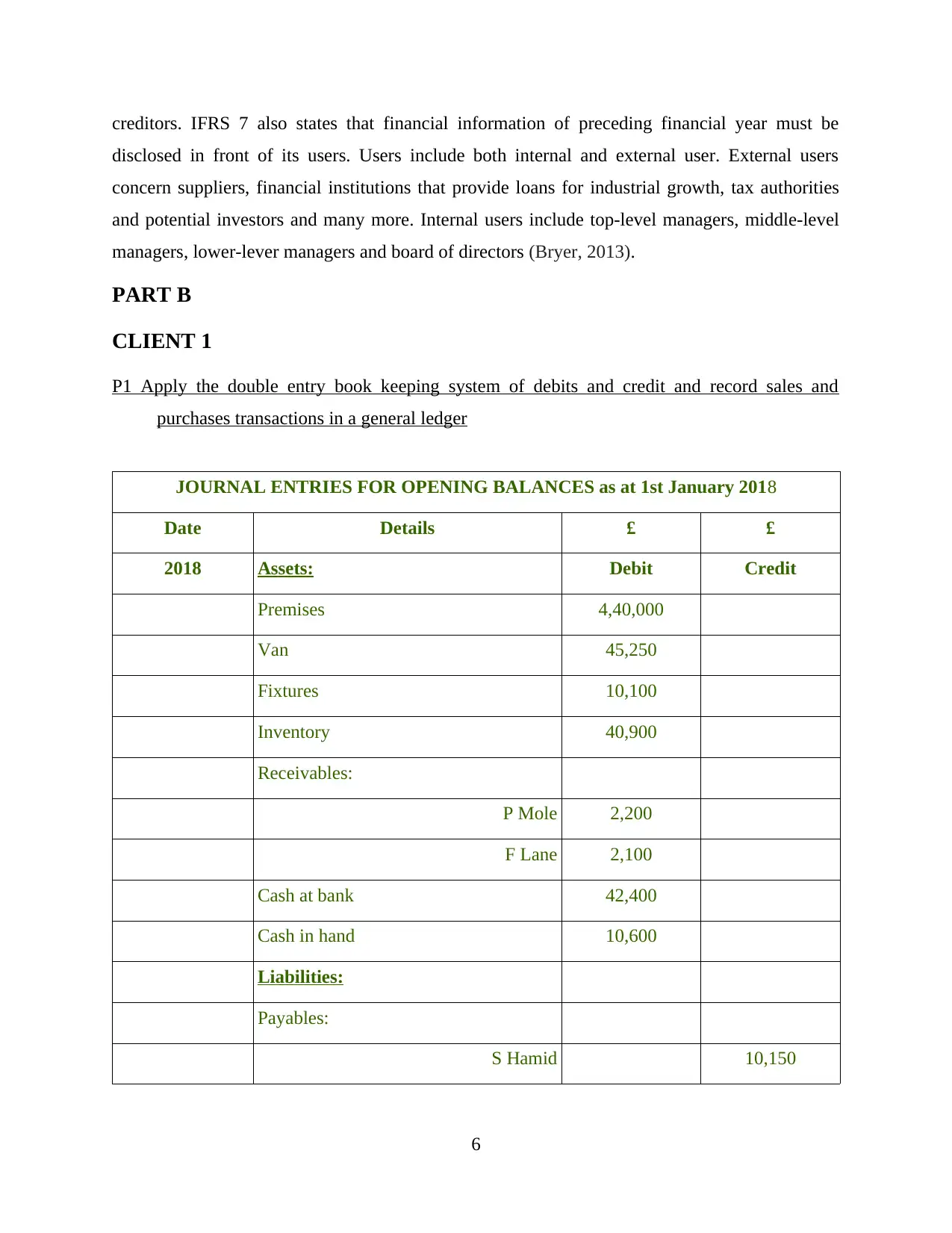

JOURNAL ENTRIES FOR OPENING BALANCES as at 1st January 2018

Date Details £ £

2018 Assets: Debit Credit

Premises 4,40,000

Van 45,250

Fixtures 10,100

Inventory 40,900

Receivables:

P Mole 2,200

F Lane 2,100

Cash at bank 42,400

Cash in hand 10,600

Liabilities:

Payables:

S Hamid 10,150

6

disclosed in front of its users. Users include both internal and external user. External users

concern suppliers, financial institutions that provide loans for industrial growth, tax authorities

and potential investors and many more. Internal users include top-level managers, middle-level

managers, lower-lever managers and board of directors (Bryer, 2013).

PART B

CLIENT 1

P1 Apply the double entry book keeping system of debits and credit and record sales and

purchases transactions in a general ledger

JOURNAL ENTRIES FOR OPENING BALANCES as at 1st January 2018

Date Details £ £

2018 Assets: Debit Credit

Premises 4,40,000

Van 45,250

Fixtures 10,100

Inventory 40,900

Receivables:

P Mole 2,200

F Lane 2,100

Cash at bank 42,400

Cash in hand 10,600

Liabilities:

Payables:

S Hamid 10,150

6

J Brown 9,600

Equity:

Opening capital at 1st January 2018 5,73,800

5,93,550 5,93,550

Date Particulars Debit Credit

01/01/18 Storage cost A/c Dr. 800

To Bank A/c Cr. 800

02/01/18 Purchase A/c Dr. 7680

To S Hamid A/c Cr. 2450

To D Main A/c Cr. 2560

To W Tag A/c Cr. 1060

To R Foot A/c Cr. 1610

03/01/18 J Wilson A/c Dr. 2020

T. Cole A/c Dr. 1840

F. Seema A/c Dr. 2380

J. Allen A/c Dr. 990

P. White A/c Dr. 2820

F. Lane A/c Dr. 1170

To Sales A/c Cr. 11220

04/01/18 Motor Expenses A/c Dr. 670

7

Equity:

Opening capital at 1st January 2018 5,73,800

5,93,550 5,93,550

Date Particulars Debit Credit

01/01/18 Storage cost A/c Dr. 800

To Bank A/c Cr. 800

02/01/18 Purchase A/c Dr. 7680

To S Hamid A/c Cr. 2450

To D Main A/c Cr. 2560

To W Tag A/c Cr. 1060

To R Foot A/c Cr. 1610

03/01/18 J Wilson A/c Dr. 2020

T. Cole A/c Dr. 1840

F. Seema A/c Dr. 2380

J. Allen A/c Dr. 990

P. White A/c Dr. 2820

F. Lane A/c Dr. 1170

To Sales A/c Cr. 11220

04/01/18 Motor Expenses A/c Dr. 670

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

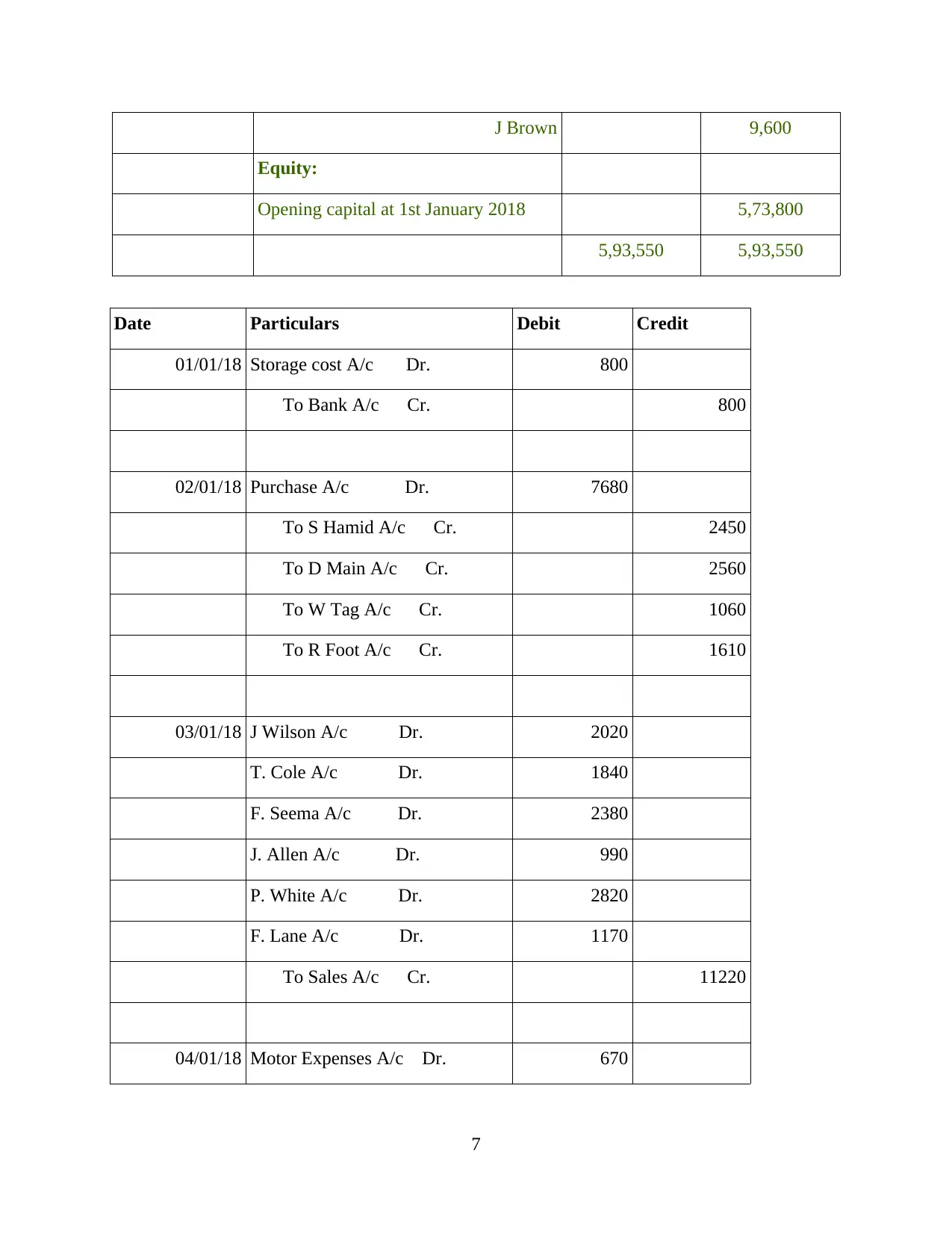

To Cash A/c Cr. 670

07/01/18 Drawings A/c Dr. 2000

To Cash A/c Cr. 2000

09/01/18 T. Cole A/c Dr. 1280

J. Fox A/c Dr. 2310

To Sales A/c Cr. 3590

11/01/18 Sales Return A/c Dr. 680

To J. Wilson A/c Cr. 370

To F. Seema A/c Cr. 310

16/01/18 Bank A/c Dr. 6792

To P. Mole A/c Cr. 1520

To F. Lane A/c Cr. 3040

To J. Wilson A/c Cr. 836

To F. Seema A/c Cr. 1396

16/01/18 Discount allowed Dr. 358

To P.Mole A/c Cr. 80

To F. Lane A/c Cr. 160

To J. Wilson A/c Cr. 44

To F. Seema A/c Cr. 74

8

07/01/18 Drawings A/c Dr. 2000

To Cash A/c Cr. 2000

09/01/18 T. Cole A/c Dr. 1280

J. Fox A/c Dr. 2310

To Sales A/c Cr. 3590

11/01/18 Sales Return A/c Dr. 680

To J. Wilson A/c Cr. 370

To F. Seema A/c Cr. 310

16/01/18 Bank A/c Dr. 6792

To P. Mole A/c Cr. 1520

To F. Lane A/c Cr. 3040

To J. Wilson A/c Cr. 836

To F. Seema A/c Cr. 1396

16/01/18 Discount allowed Dr. 358

To P.Mole A/c Cr. 80

To F. Lane A/c Cr. 160

To J. Wilson A/c Cr. 44

To F. Seema A/c Cr. 74

8

19/01/18 R Foot Dr. 110

To purchase return 110

22/01/18 Purchase A/c Dr. 3140

To L Mole a/c 1330

To W Wright 1810

24/01/18 S Hamid a/c Dr. 2340

J Brown a/c Dr. 2970

R Foot a/c Dr. 1440

To Bank a/c 6750

24/01/18 S Hamid a/c Dr. 260

J Brown a/c Dr. 330

R Foot a/c Dr. 160

To Discount Receivable a/c 750

27/01/18 Salary a/c Dr. 14500

To Bank a/c 14500

30/01/18 Business Exp a/c Dr.. 2220

To Bank a/c 2220

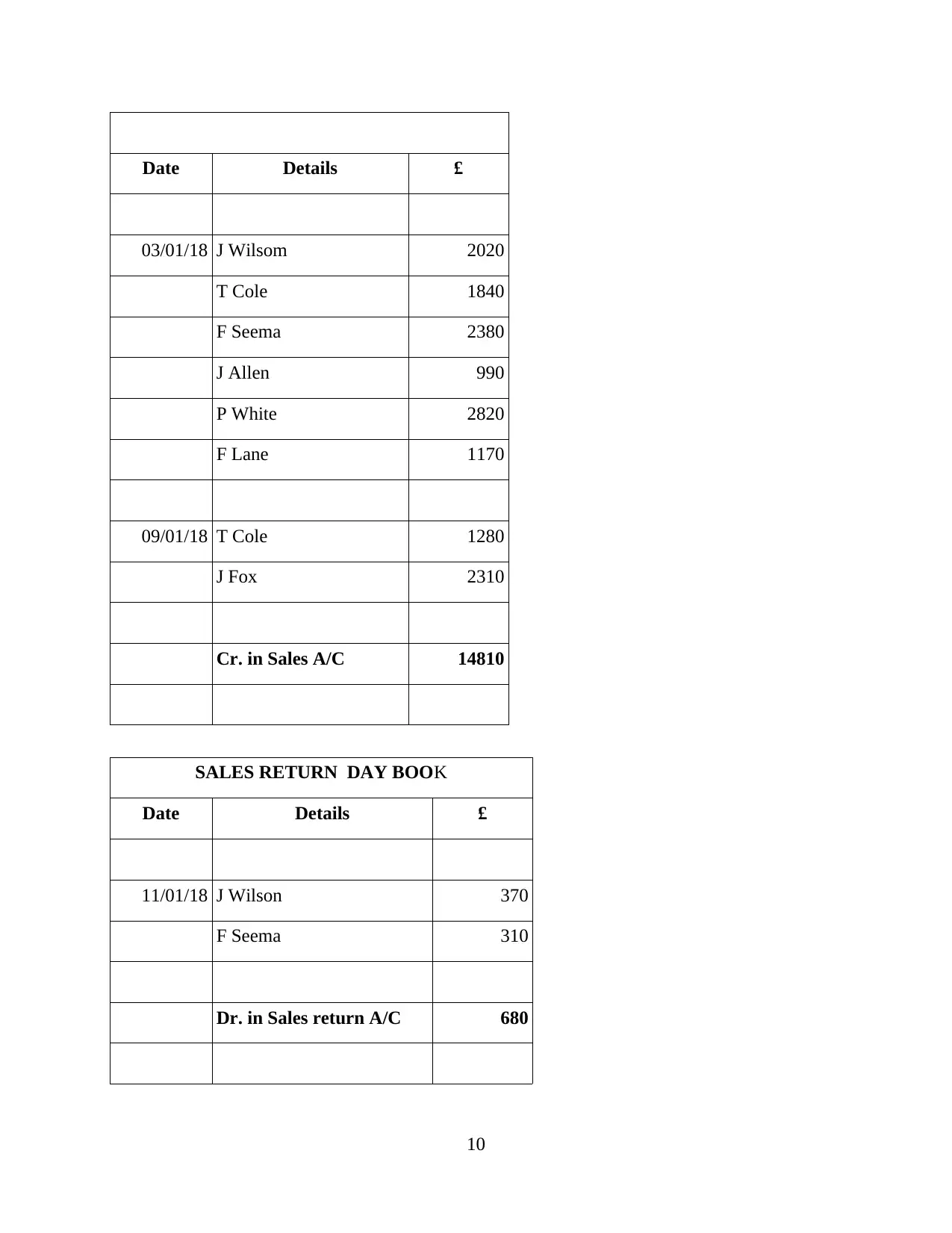

SALES DAY BOOK

9

To purchase return 110

22/01/18 Purchase A/c Dr. 3140

To L Mole a/c 1330

To W Wright 1810

24/01/18 S Hamid a/c Dr. 2340

J Brown a/c Dr. 2970

R Foot a/c Dr. 1440

To Bank a/c 6750

24/01/18 S Hamid a/c Dr. 260

J Brown a/c Dr. 330

R Foot a/c Dr. 160

To Discount Receivable a/c 750

27/01/18 Salary a/c Dr. 14500

To Bank a/c 14500

30/01/18 Business Exp a/c Dr.. 2220

To Bank a/c 2220

SALES DAY BOOK

9

Date Details £

03/01/18 J Wilsom 2020

T Cole 1840

F Seema 2380

J Allen 990

P White 2820

F Lane 1170

09/01/18 T Cole 1280

J Fox 2310

Cr. in Sales A/C 14810

SALES RETURN DAY BOOK

Date Details £

11/01/18 J Wilson 370

F Seema 310

Dr. in Sales return A/C 680

10

03/01/18 J Wilsom 2020

T Cole 1840

F Seema 2380

J Allen 990

P White 2820

F Lane 1170

09/01/18 T Cole 1280

J Fox 2310

Cr. in Sales A/C 14810

SALES RETURN DAY BOOK

Date Details £

11/01/18 J Wilson 370

F Seema 310

Dr. in Sales return A/C 680

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

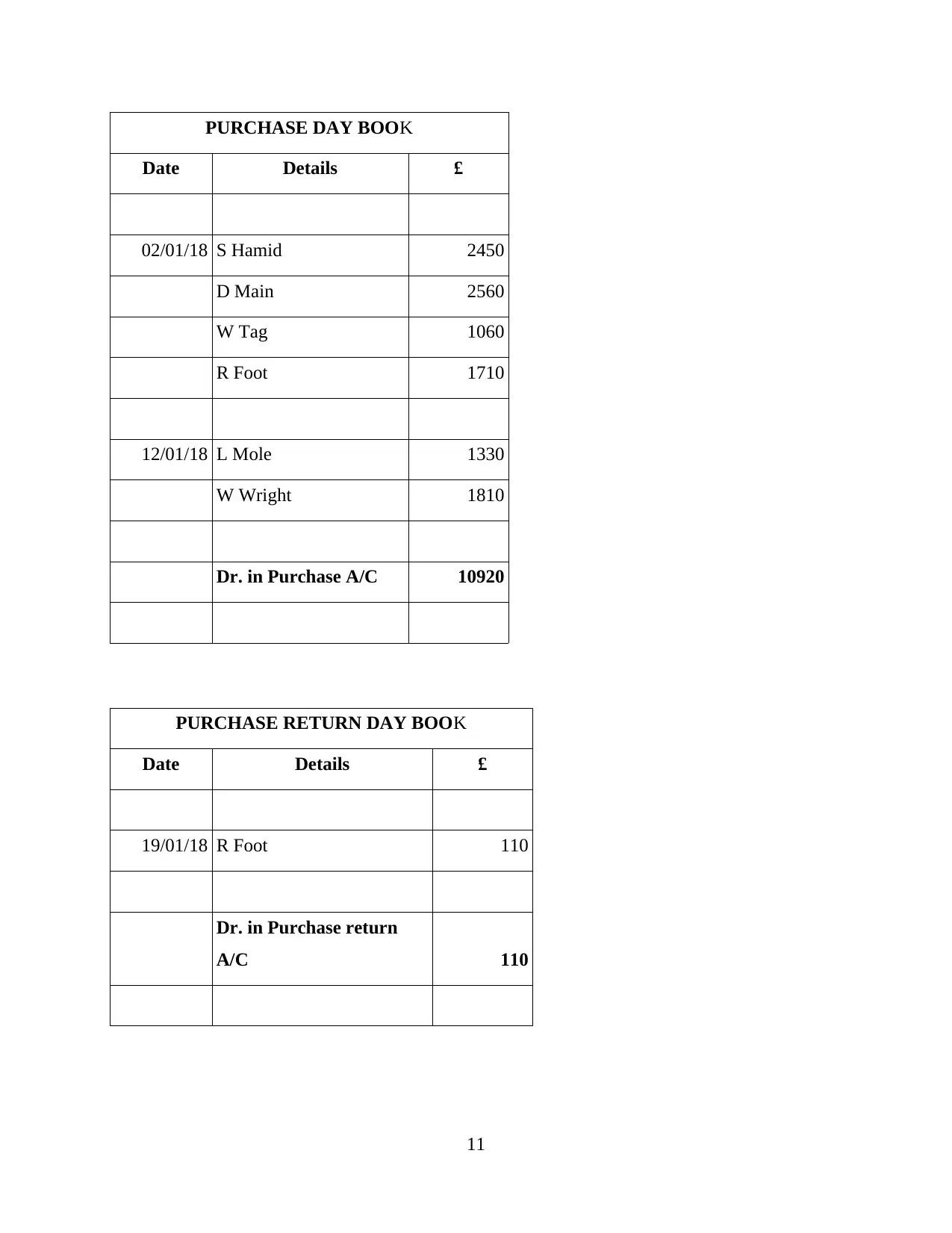

PURCHASE DAY BOOK

Date Details £

02/01/18 S Hamid 2450

D Main 2560

W Tag 1060

R Foot 1710

12/01/18 L Mole 1330

W Wright 1810

Dr. in Purchase A/C 10920

PURCHASE RETURN DAY BOOK

Date Details £

19/01/18 R Foot 110

Dr. in Purchase return

A/C 110

11

Date Details £

02/01/18 S Hamid 2450

D Main 2560

W Tag 1060

R Foot 1710

12/01/18 L Mole 1330

W Wright 1810

Dr. in Purchase A/C 10920

PURCHASE RETURN DAY BOOK

Date Details £

19/01/18 R Foot 110

Dr. in Purchase return

A/C 110

11

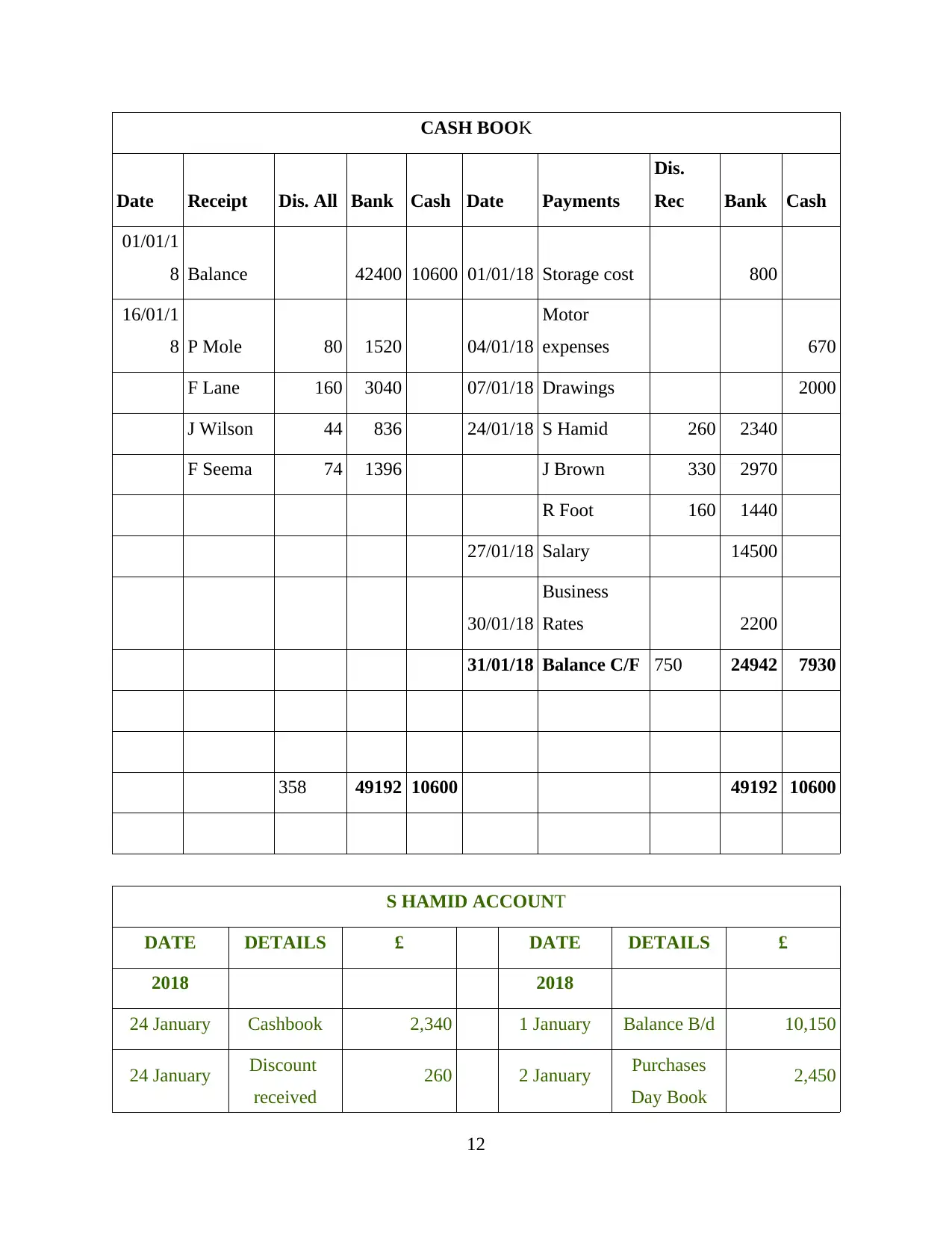

CASH BOOK

Date Receipt Dis. All Bank Cash Date Payments

Dis.

Rec Bank Cash

01/01/1

8 Balance 42400 10600 01/01/18 Storage cost 800

16/01/1

8 P Mole 80 1520 04/01/18

Motor

expenses 670

F Lane 160 3040 07/01/18 Drawings 2000

J Wilson 44 836 24/01/18 S Hamid 260 2340

F Seema 74 1396 J Brown 330 2970

R Foot 160 1440

27/01/18 Salary 14500

30/01/18

Business

Rates 2200

31/01/18 Balance C/F 750 24942 7930

358 49192 10600 49192 10600

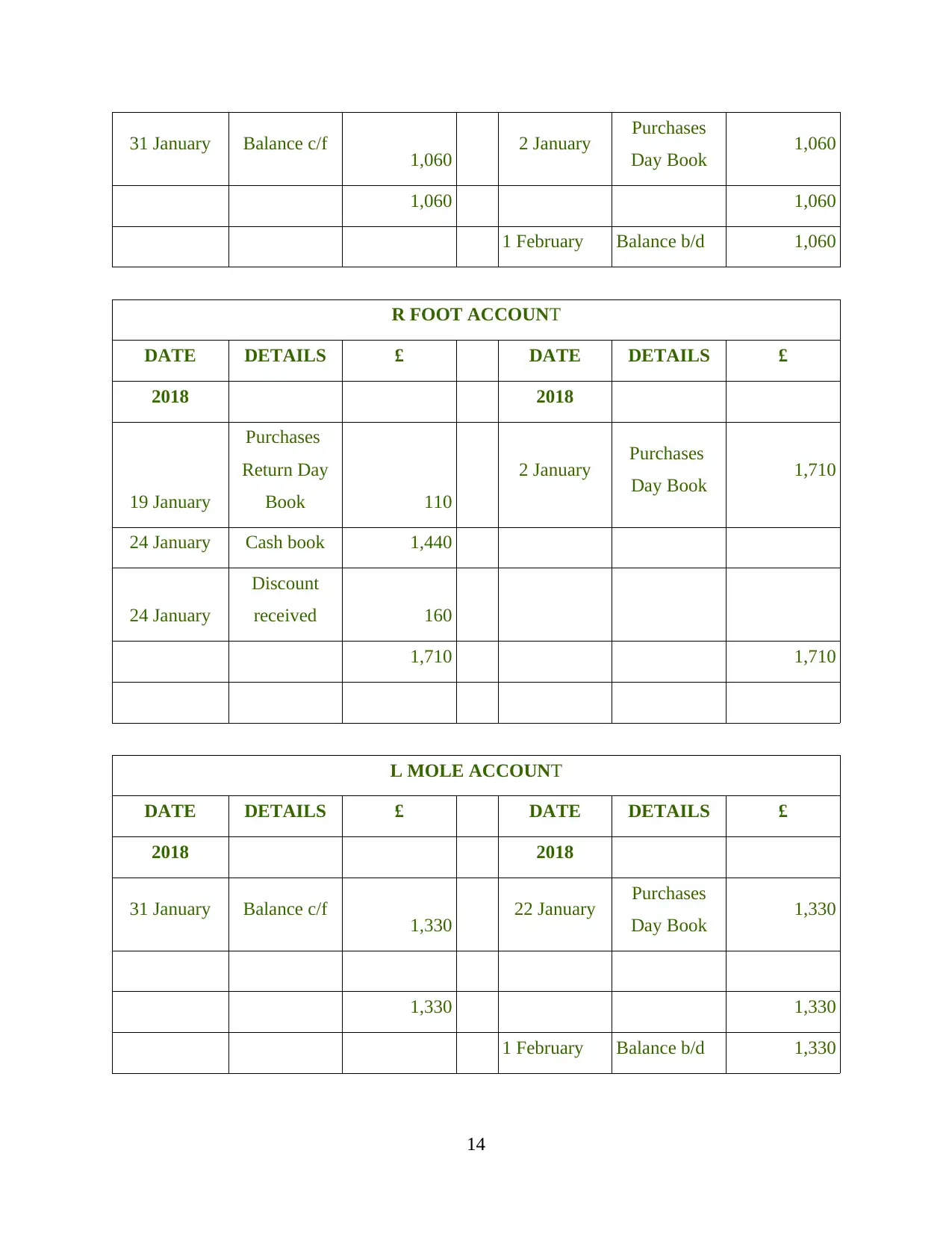

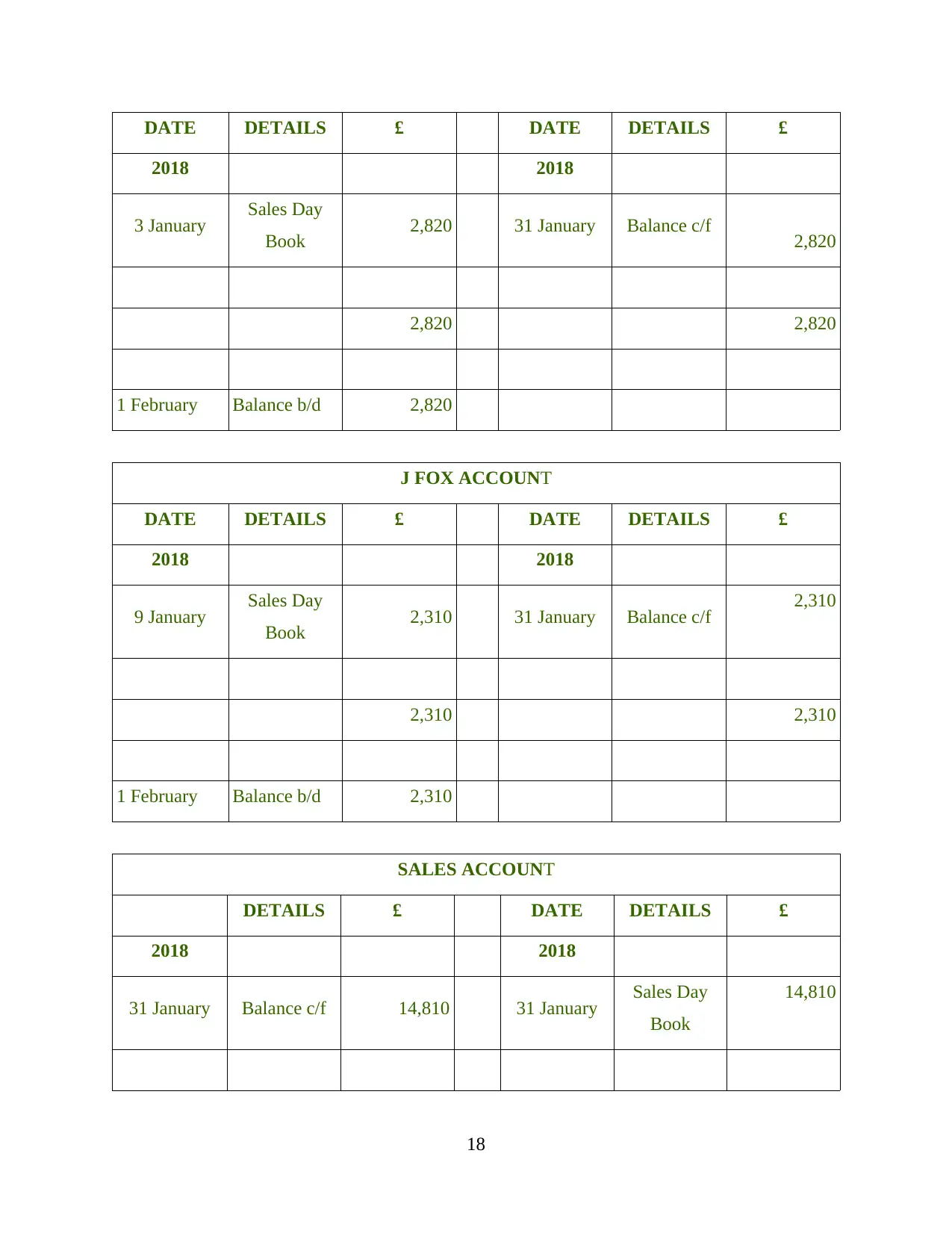

S HAMID ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

24 January Cashbook 2,340 1 January Balance B/d 10,150

24 January Discount

received

260 2 January Purchases

Day Book

2,450

12

Date Receipt Dis. All Bank Cash Date Payments

Dis.

Rec Bank Cash

01/01/1

8 Balance 42400 10600 01/01/18 Storage cost 800

16/01/1

8 P Mole 80 1520 04/01/18

Motor

expenses 670

F Lane 160 3040 07/01/18 Drawings 2000

J Wilson 44 836 24/01/18 S Hamid 260 2340

F Seema 74 1396 J Brown 330 2970

R Foot 160 1440

27/01/18 Salary 14500

30/01/18

Business

Rates 2200

31/01/18 Balance C/F 750 24942 7930

358 49192 10600 49192 10600

S HAMID ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

24 January Cashbook 2,340 1 January Balance B/d 10,150

24 January Discount

received

260 2 January Purchases

Day Book

2,450

12

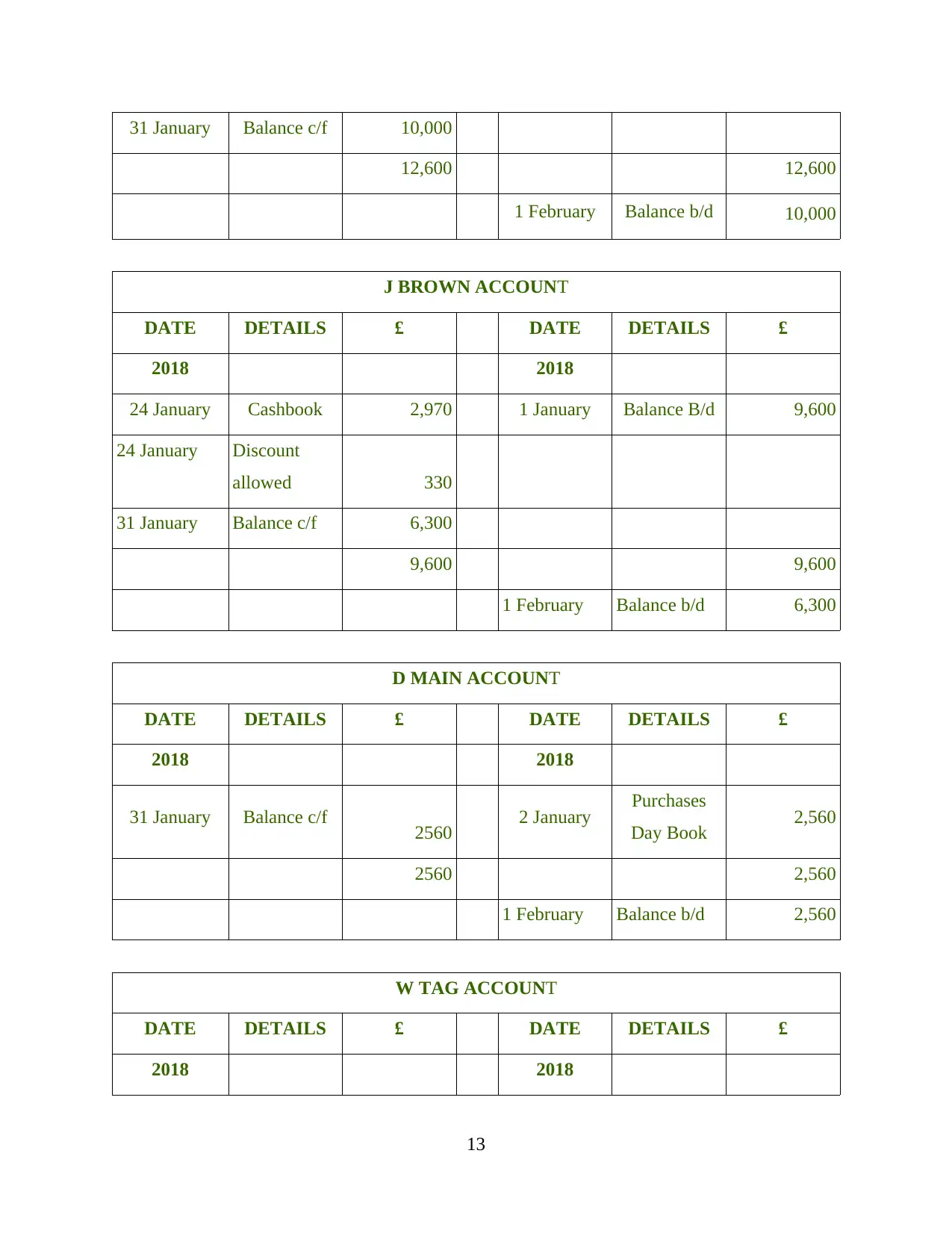

31 January Balance c/f 10,000

12,600 12,600

1 February Balance b/d 10,000

J BROWN ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

24 January Cashbook 2,970 1 January Balance B/d 9,600

24 January Discount

allowed 330

31 January Balance c/f 6,300

9,600 9,600

1 February Balance b/d 6,300

D MAIN ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 2560 2 January Purchases

Day Book 2,560

2560 2,560

1 February Balance b/d 2,560

W TAG ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

13

12,600 12,600

1 February Balance b/d 10,000

J BROWN ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

24 January Cashbook 2,970 1 January Balance B/d 9,600

24 January Discount

allowed 330

31 January Balance c/f 6,300

9,600 9,600

1 February Balance b/d 6,300

D MAIN ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 2560 2 January Purchases

Day Book 2,560

2560 2,560

1 February Balance b/d 2,560

W TAG ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

31 January Balance c/f 1,060 2 January Purchases

Day Book 1,060

1,060 1,060

1 February Balance b/d 1,060

R FOOT ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

19 January

Purchases

Return Day

Book 110

2 January Purchases

Day Book 1,710

24 January Cash book 1,440

24 January

Discount

received 160

1,710 1,710

L MOLE ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 1,330 22 January Purchases

Day Book 1,330

1,330 1,330

1 February Balance b/d 1,330

14

Day Book 1,060

1,060 1,060

1 February Balance b/d 1,060

R FOOT ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

19 January

Purchases

Return Day

Book 110

2 January Purchases

Day Book 1,710

24 January Cash book 1,440

24 January

Discount

received 160

1,710 1,710

L MOLE ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 1,330 22 January Purchases

Day Book 1,330

1,330 1,330

1 February Balance b/d 1,330

14

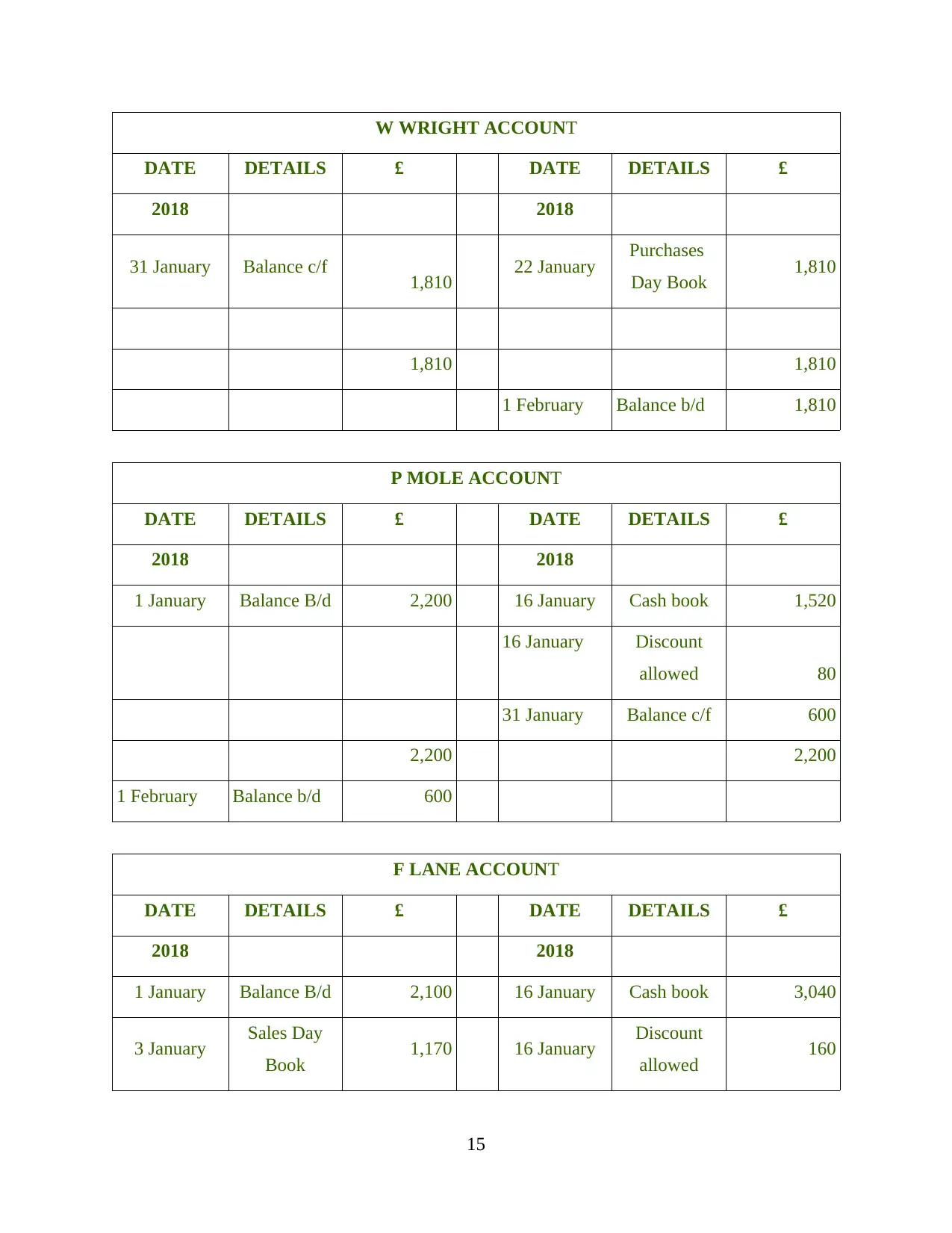

W WRIGHT ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 1,810 22 January Purchases

Day Book 1,810

1,810 1,810

1 February Balance b/d 1,810

P MOLE ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

1 January Balance B/d 2,200 16 January Cash book 1,520

16 January Discount

allowed 80

31 January Balance c/f 600

2,200 2,200

1 February Balance b/d 600

F LANE ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

1 January Balance B/d 2,100 16 January Cash book 3,040

3 January Sales Day

Book 1,170 16 January Discount

allowed 160

15

DATE DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 1,810 22 January Purchases

Day Book 1,810

1,810 1,810

1 February Balance b/d 1,810

P MOLE ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

1 January Balance B/d 2,200 16 January Cash book 1,520

16 January Discount

allowed 80

31 January Balance c/f 600

2,200 2,200

1 February Balance b/d 600

F LANE ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

1 January Balance B/d 2,100 16 January Cash book 3,040

3 January Sales Day

Book 1,170 16 January Discount

allowed 160

15

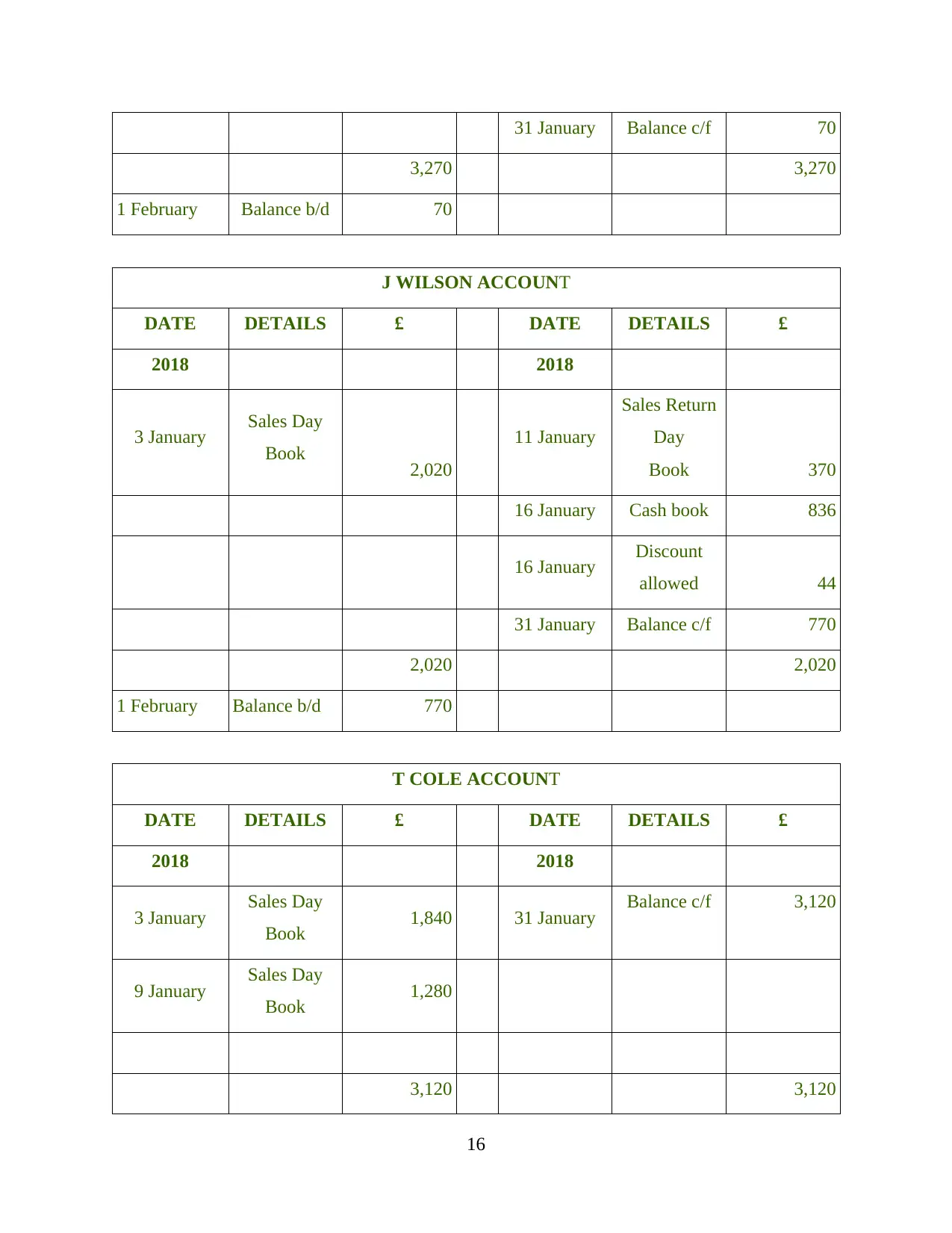

31 January Balance c/f 70

3,270 3,270

1 February Balance b/d 70

J WILSON ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

3 January Sales Day

Book 2,020

11 January

Sales Return

Day

Book 370

16 January Cash book 836

16 January Discount

allowed 44

31 January Balance c/f 770

2,020 2,020

1 February Balance b/d 770

T COLE ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

3 January Sales Day

Book 1,840 31 January Balance c/f 3,120

9 January Sales Day

Book 1,280

3,120 3,120

16

3,270 3,270

1 February Balance b/d 70

J WILSON ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

3 January Sales Day

Book 2,020

11 January

Sales Return

Day

Book 370

16 January Cash book 836

16 January Discount

allowed 44

31 January Balance c/f 770

2,020 2,020

1 February Balance b/d 770

T COLE ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

3 January Sales Day

Book 1,840 31 January Balance c/f 3,120

9 January Sales Day

Book 1,280

3,120 3,120

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

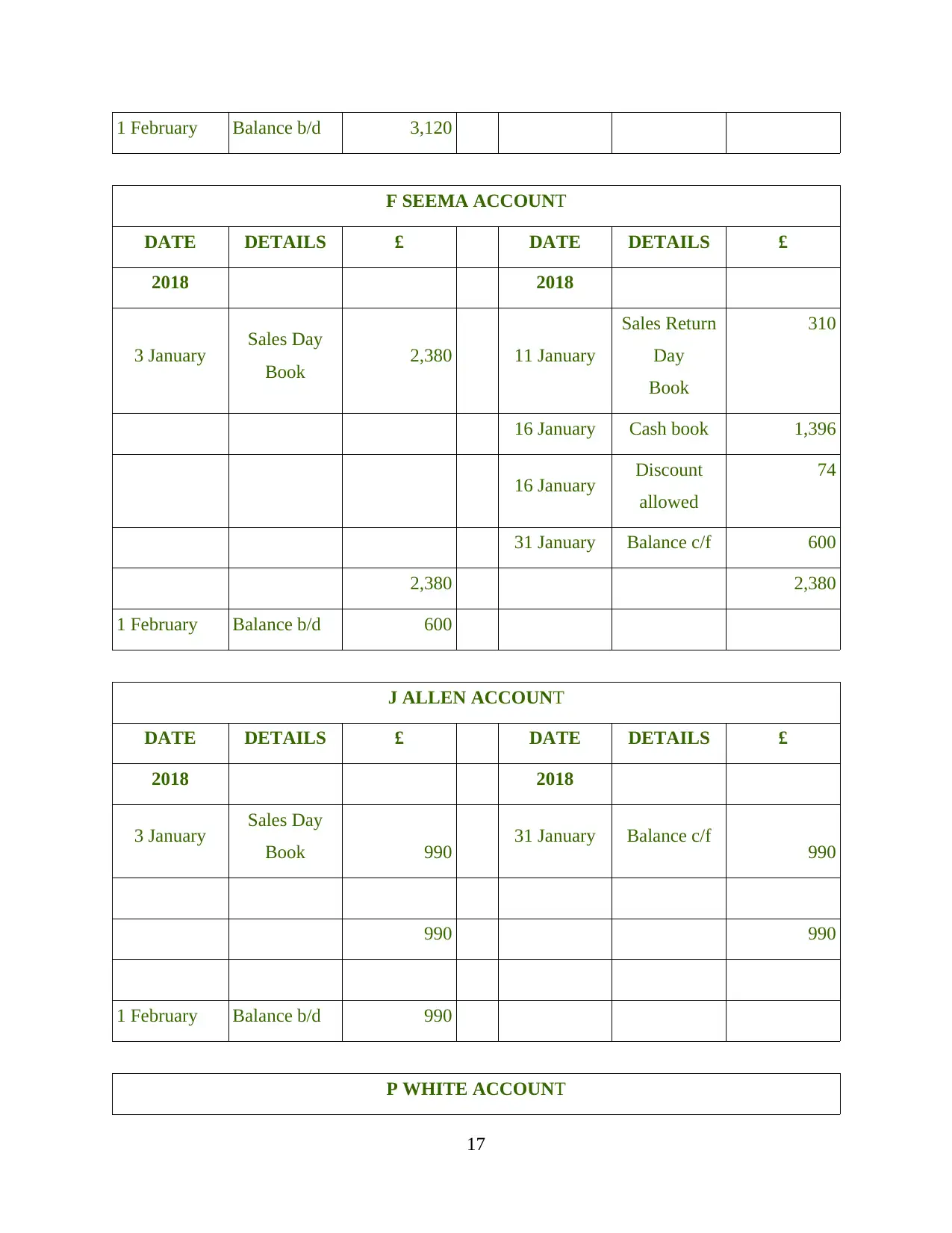

1 February Balance b/d 3,120

F SEEMA ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

3 January Sales Day

Book 2,380 11 January

Sales Return

Day

Book

310

16 January Cash book 1,396

16 January Discount

allowed

74

31 January Balance c/f 600

2,380 2,380

1 February Balance b/d 600

J ALLEN ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

3 January Sales Day

Book 990 31 January Balance c/f 990

990 990

1 February Balance b/d 990

P WHITE ACCOUNT

17

F SEEMA ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

3 January Sales Day

Book 2,380 11 January

Sales Return

Day

Book

310

16 January Cash book 1,396

16 January Discount

allowed

74

31 January Balance c/f 600

2,380 2,380

1 February Balance b/d 600

J ALLEN ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

3 January Sales Day

Book 990 31 January Balance c/f 990

990 990

1 February Balance b/d 990

P WHITE ACCOUNT

17

DATE DETAILS £ DATE DETAILS £

2018 2018

3 January Sales Day

Book 2,820 31 January Balance c/f 2,820

2,820 2,820

1 February Balance b/d 2,820

J FOX ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

9 January Sales Day

Book 2,310 31 January Balance c/f 2,310

2,310 2,310

1 February Balance b/d 2,310

SALES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 14,810 31 January Sales Day

Book

14,810

18

2018 2018

3 January Sales Day

Book 2,820 31 January Balance c/f 2,820

2,820 2,820

1 February Balance b/d 2,820

J FOX ACCOUNT

DATE DETAILS £ DATE DETAILS £

2018 2018

9 January Sales Day

Book 2,310 31 January Balance c/f 2,310

2,310 2,310

1 February Balance b/d 2,310

SALES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 14,810 31 January Sales Day

Book

14,810

18

14,810 14,810

1 February Balance b/d 14,810

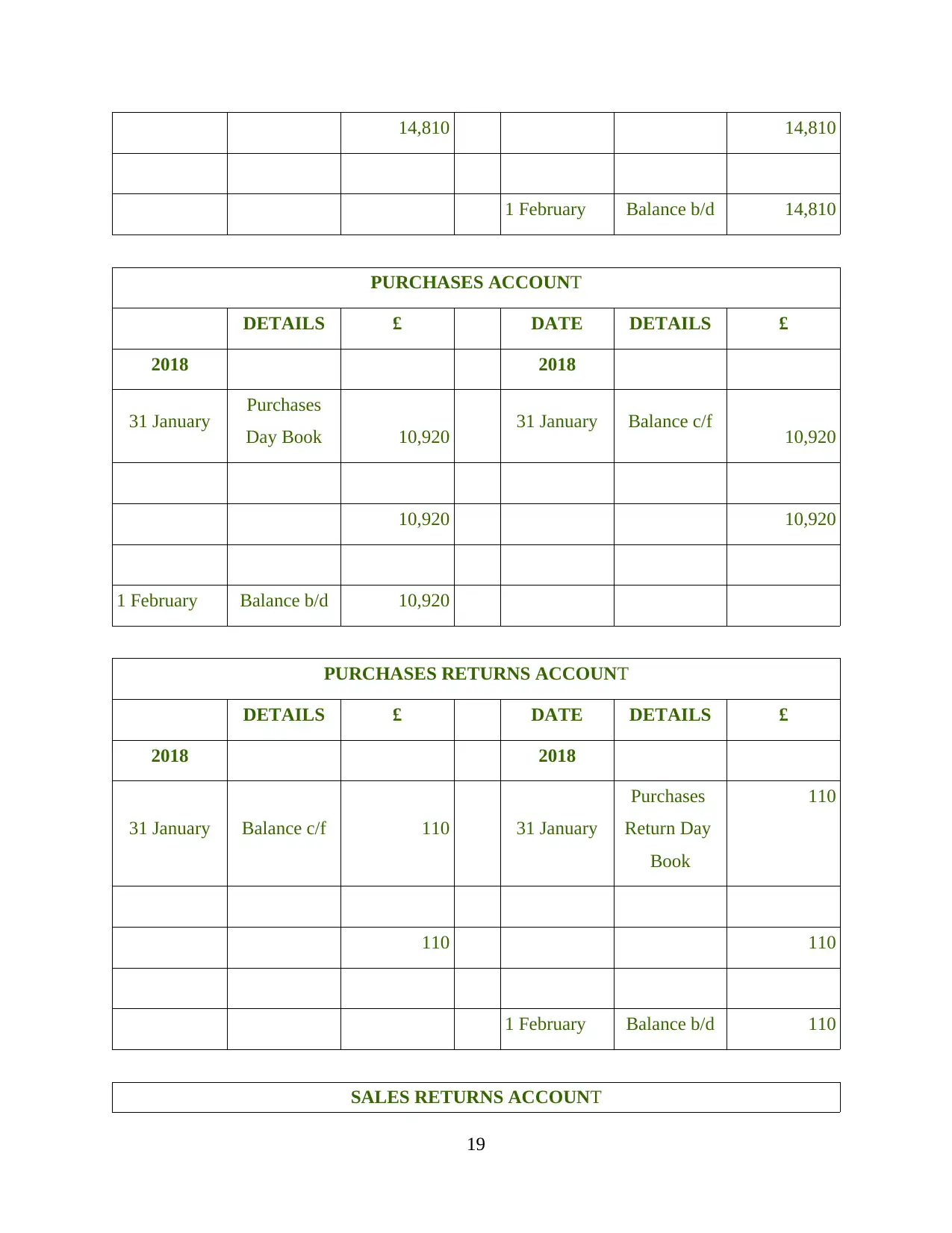

PURCHASES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31 January Purchases

Day Book 10,920 31 January Balance c/f 10,920

10,920 10,920

1 February Balance b/d 10,920

PURCHASES RETURNS ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 110 31 January

Purchases

Return Day

Book

110

110 110

1 February Balance b/d 110

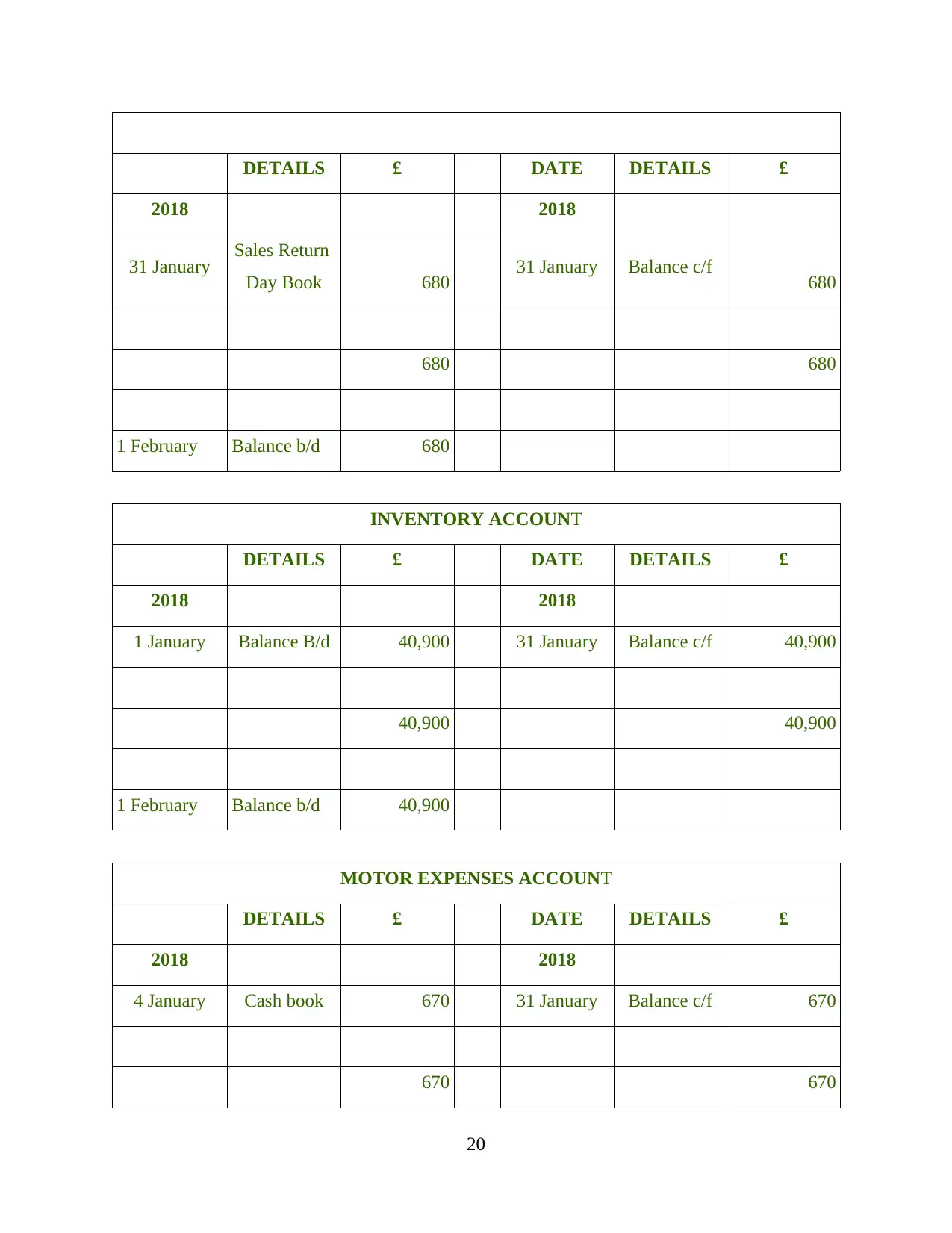

SALES RETURNS ACCOUNT

19

1 February Balance b/d 14,810

PURCHASES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31 January Purchases

Day Book 10,920 31 January Balance c/f 10,920

10,920 10,920

1 February Balance b/d 10,920

PURCHASES RETURNS ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 110 31 January

Purchases

Return Day

Book

110

110 110

1 February Balance b/d 110

SALES RETURNS ACCOUNT

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

DETAILS £ DATE DETAILS £

2018 2018

31 January Sales Return

Day Book 680 31 January Balance c/f 680

680 680

1 February Balance b/d 680

INVENTORY ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

1 January Balance B/d 40,900 31 January Balance c/f 40,900

40,900 40,900

1 February Balance b/d 40,900

MOTOR EXPENSES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

4 January Cash book 670 31 January Balance c/f 670

670 670

20

2018 2018

31 January Sales Return

Day Book 680 31 January Balance c/f 680

680 680

1 February Balance b/d 680

INVENTORY ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

1 January Balance B/d 40,900 31 January Balance c/f 40,900

40,900 40,900

1 February Balance b/d 40,900

MOTOR EXPENSES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

4 January Cash book 670 31 January Balance c/f 670

670 670

20

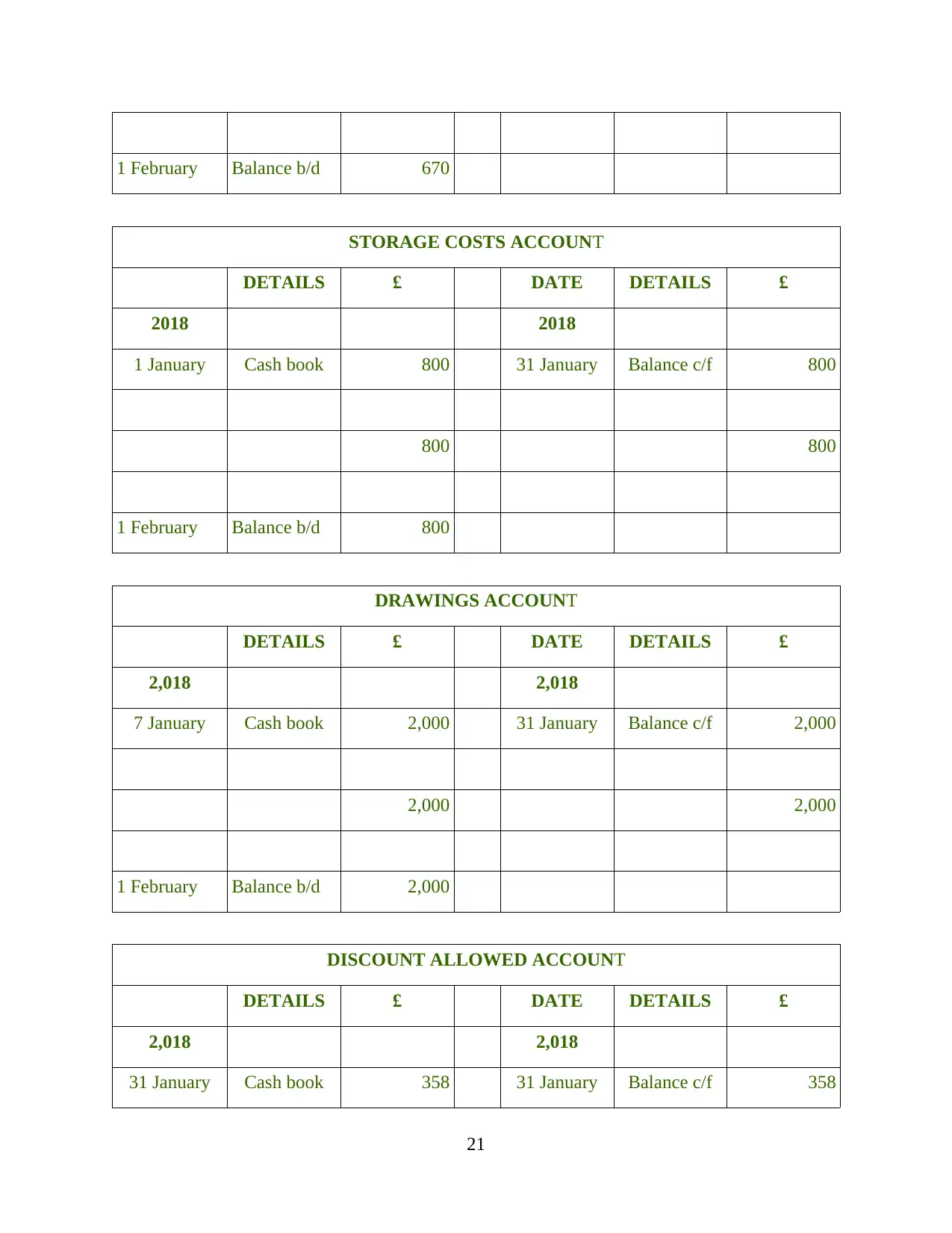

1 February Balance b/d 670

STORAGE COSTS ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

1 January Cash book 800 31 January Balance c/f 800

800 800

1 February Balance b/d 800

DRAWINGS ACCOUNT

DETAILS £ DATE DETAILS £

2,018 2,018

7 January Cash book 2,000 31 January Balance c/f 2,000

2,000 2,000

1 February Balance b/d 2,000

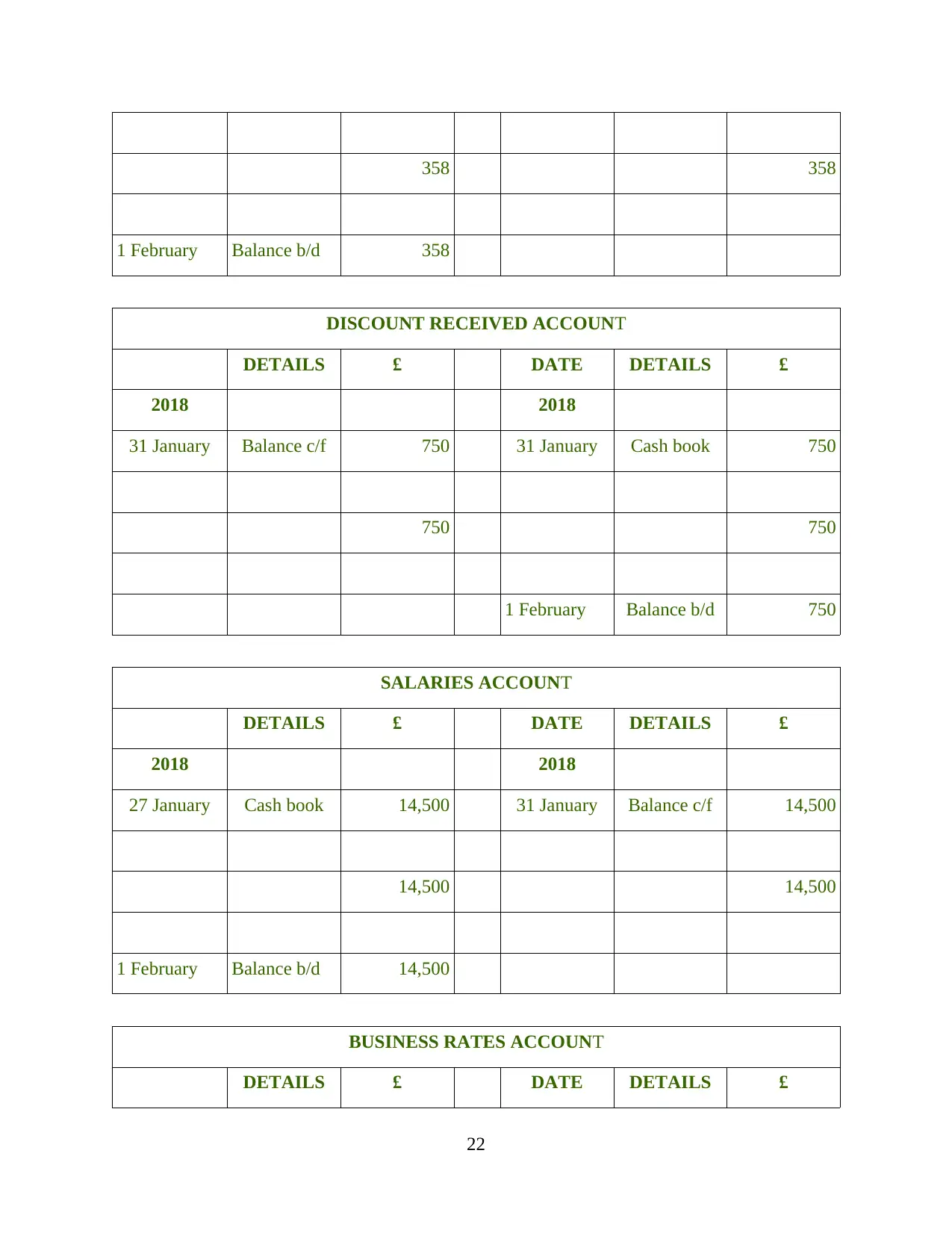

DISCOUNT ALLOWED ACCOUNT

DETAILS £ DATE DETAILS £

2,018 2,018

31 January Cash book 358 31 January Balance c/f 358

21

STORAGE COSTS ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

1 January Cash book 800 31 January Balance c/f 800

800 800

1 February Balance b/d 800

DRAWINGS ACCOUNT

DETAILS £ DATE DETAILS £

2,018 2,018

7 January Cash book 2,000 31 January Balance c/f 2,000

2,000 2,000

1 February Balance b/d 2,000

DISCOUNT ALLOWED ACCOUNT

DETAILS £ DATE DETAILS £

2,018 2,018

31 January Cash book 358 31 January Balance c/f 358

21

358 358

1 February Balance b/d 358

DISCOUNT RECEIVED ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 750 31 January Cash book 750

750 750

1 February Balance b/d 750

SALARIES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

27 January Cash book 14,500 31 January Balance c/f 14,500

14,500 14,500

1 February Balance b/d 14,500

BUSINESS RATES ACCOUNT

DETAILS £ DATE DETAILS £

22

1 February Balance b/d 358

DISCOUNT RECEIVED ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 750 31 January Cash book 750

750 750

1 February Balance b/d 750

SALARIES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

27 January Cash book 14,500 31 January Balance c/f 14,500

14,500 14,500

1 February Balance b/d 14,500

BUSINESS RATES ACCOUNT

DETAILS £ DATE DETAILS £

22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

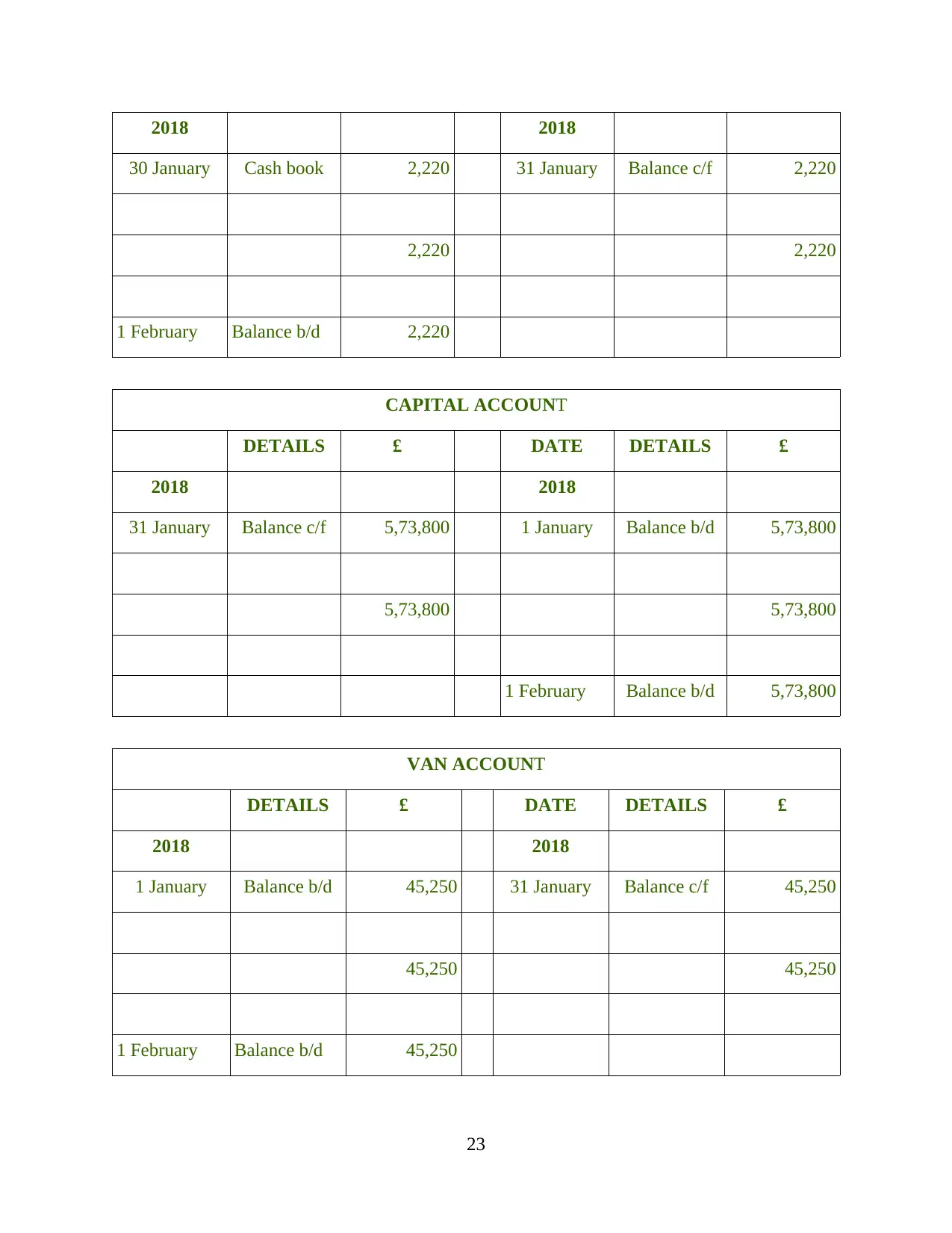

2018 2018

30 January Cash book 2,220 31 January Balance c/f 2,220

2,220 2,220

1 February Balance b/d 2,220

CAPITAL ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 5,73,800 1 January Balance b/d 5,73,800

5,73,800 5,73,800

1 February Balance b/d 5,73,800

VAN ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

1 January Balance b/d 45,250 31 January Balance c/f 45,250

45,250 45,250

1 February Balance b/d 45,250

23

30 January Cash book 2,220 31 January Balance c/f 2,220

2,220 2,220

1 February Balance b/d 2,220

CAPITAL ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31 January Balance c/f 5,73,800 1 January Balance b/d 5,73,800

5,73,800 5,73,800

1 February Balance b/d 5,73,800

VAN ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

1 January Balance b/d 45,250 31 January Balance c/f 45,250

45,250 45,250

1 February Balance b/d 45,250

23

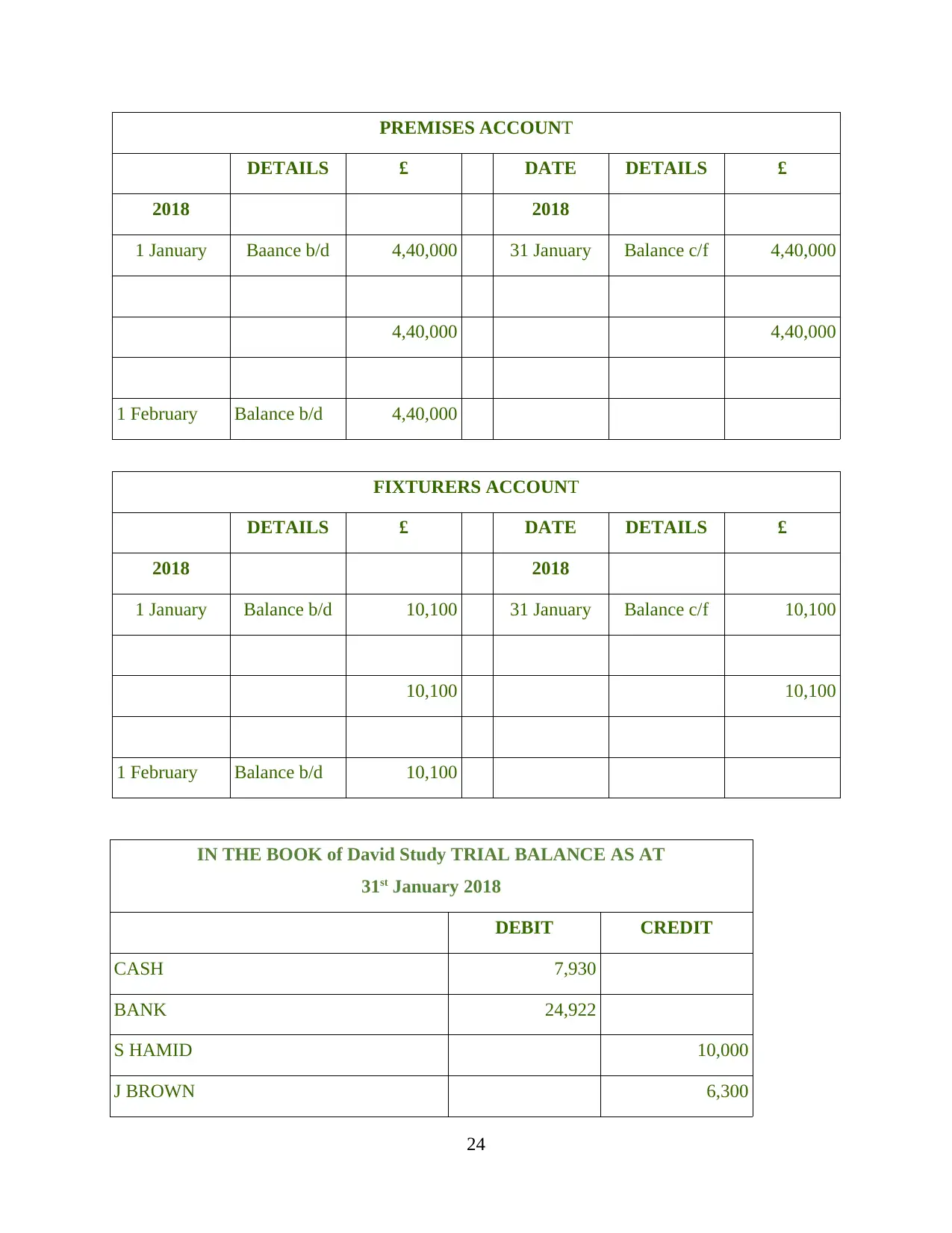

PREMISES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

1 January Baance b/d 4,40,000 31 January Balance c/f 4,40,000

4,40,000 4,40,000

1 February Balance b/d 4,40,000

FIXTURERS ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

1 January Balance b/d 10,100 31 January Balance c/f 10,100

10,100 10,100

1 February Balance b/d 10,100

IN THE BOOK of David Study TRIAL BALANCE AS AT

31st January 2018

DEBIT CREDIT

CASH 7,930

BANK 24,922

S HAMID 10,000

J BROWN 6,300

24

DETAILS £ DATE DETAILS £

2018 2018

1 January Baance b/d 4,40,000 31 January Balance c/f 4,40,000

4,40,000 4,40,000

1 February Balance b/d 4,40,000

FIXTURERS ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

1 January Balance b/d 10,100 31 January Balance c/f 10,100

10,100 10,100

1 February Balance b/d 10,100

IN THE BOOK of David Study TRIAL BALANCE AS AT

31st January 2018

DEBIT CREDIT

CASH 7,930

BANK 24,922

S HAMID 10,000

J BROWN 6,300

24

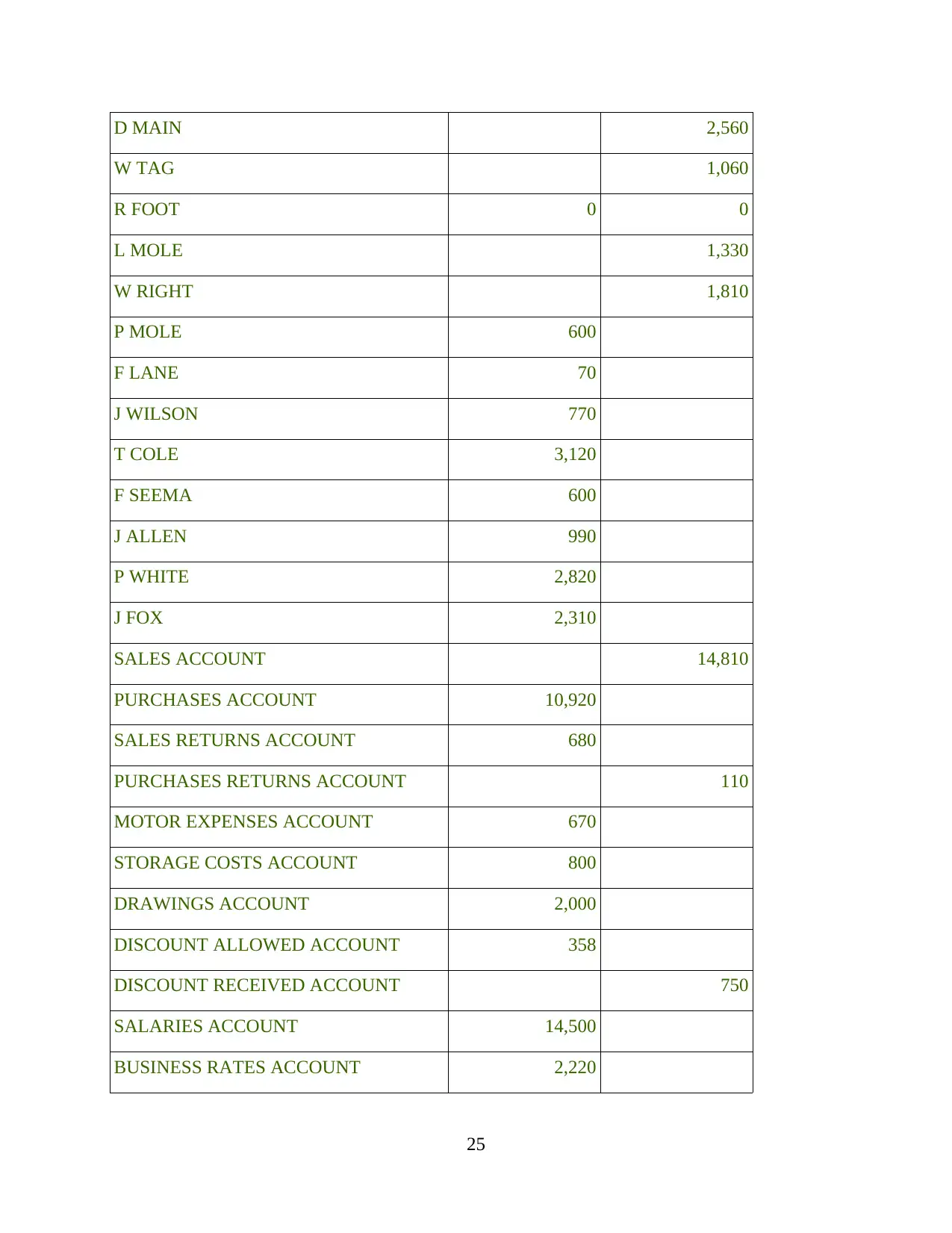

D MAIN 2,560

W TAG 1,060

R FOOT 0 0

L MOLE 1,330

W RIGHT 1,810

P MOLE 600

F LANE 70

J WILSON 770

T COLE 3,120

F SEEMA 600

J ALLEN 990

P WHITE 2,820

J FOX 2,310

SALES ACCOUNT 14,810

PURCHASES ACCOUNT 10,920

SALES RETURNS ACCOUNT 680

PURCHASES RETURNS ACCOUNT 110

MOTOR EXPENSES ACCOUNT 670

STORAGE COSTS ACCOUNT 800

DRAWINGS ACCOUNT 2,000

DISCOUNT ALLOWED ACCOUNT 358

DISCOUNT RECEIVED ACCOUNT 750

SALARIES ACCOUNT 14,500

BUSINESS RATES ACCOUNT 2,220

25

W TAG 1,060

R FOOT 0 0

L MOLE 1,330

W RIGHT 1,810

P MOLE 600

F LANE 70

J WILSON 770

T COLE 3,120

F SEEMA 600

J ALLEN 990

P WHITE 2,820

J FOX 2,310

SALES ACCOUNT 14,810

PURCHASES ACCOUNT 10,920

SALES RETURNS ACCOUNT 680

PURCHASES RETURNS ACCOUNT 110

MOTOR EXPENSES ACCOUNT 670

STORAGE COSTS ACCOUNT 800

DRAWINGS ACCOUNT 2,000

DISCOUNT ALLOWED ACCOUNT 358

DISCOUNT RECEIVED ACCOUNT 750

SALARIES ACCOUNT 14,500

BUSINESS RATES ACCOUNT 2,220

25

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CAPITAL ACCOUNT 573800

INVENTORY ACCOUNT 40900

VAN ACCOUNT 45250

PREMISES ACCOUNT 440000

FIXTURES ACCOUNT 10100

6,12,530 6,12,530

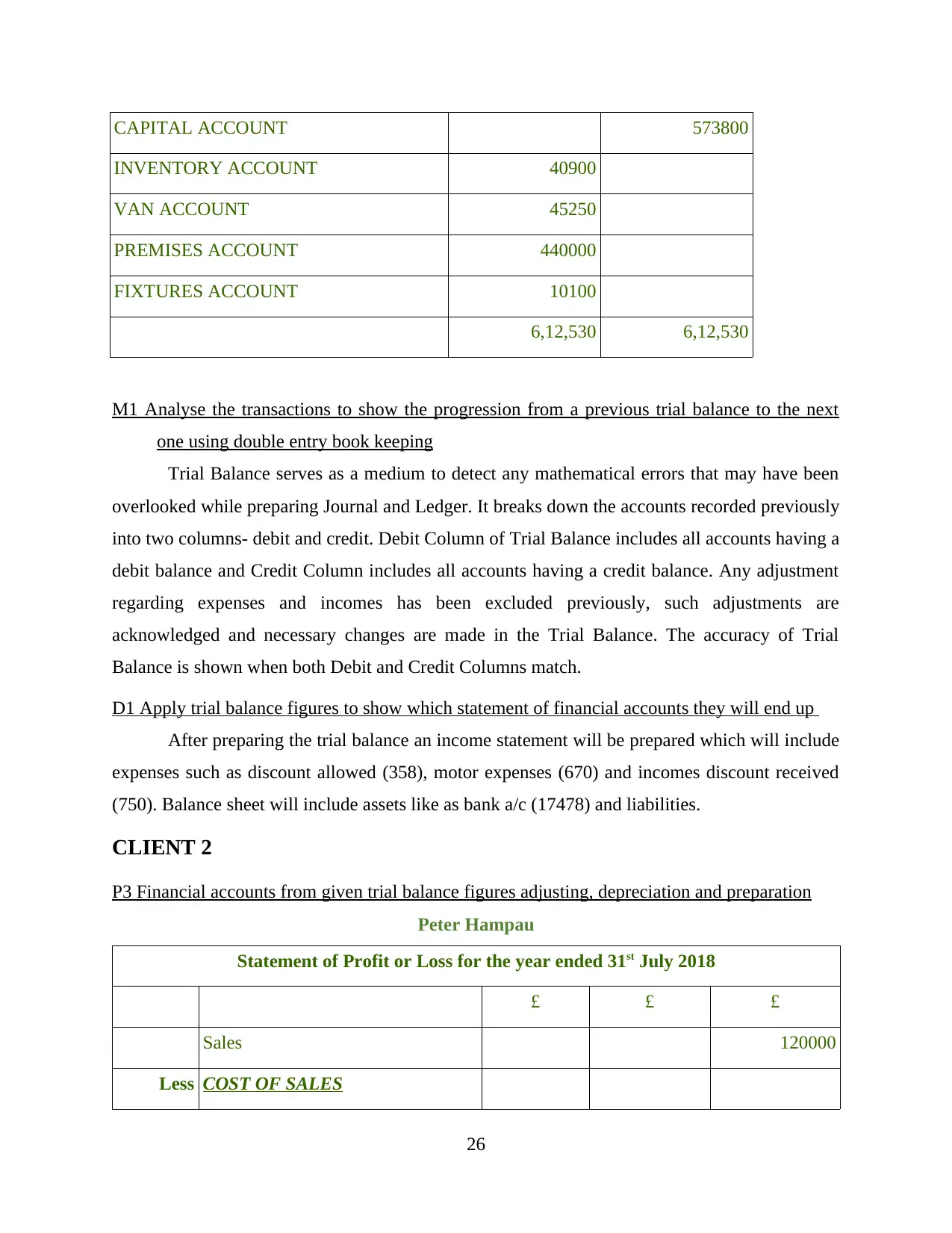

M1 Analyse the transactions to show the progression from a previous trial balance to the next

one using double entry book keeping

Trial Balance serves as a medium to detect any mathematical errors that may have been

overlooked while preparing Journal and Ledger. It breaks down the accounts recorded previously

into two columns- debit and credit. Debit Column of Trial Balance includes all accounts having a

debit balance and Credit Column includes all accounts having a credit balance. Any adjustment

regarding expenses and incomes has been excluded previously, such adjustments are

acknowledged and necessary changes are made in the Trial Balance. The accuracy of Trial

Balance is shown when both Debit and Credit Columns match.

D1 Apply trial balance figures to show which statement of financial accounts they will end up

After preparing the trial balance an income statement will be prepared which will include

expenses such as discount allowed (358), motor expenses (670) and incomes discount received

(750). Balance sheet will include assets like as bank a/c (17478) and liabilities.

CLIENT 2

P3 Financial accounts from given trial balance figures adjusting, depreciation and preparation

Peter Hampau

Statement of Profit or Loss for the year ended 31st July 2018

£ £ £

Sales 120000

Less COST OF SALES

26

INVENTORY ACCOUNT 40900

VAN ACCOUNT 45250

PREMISES ACCOUNT 440000

FIXTURES ACCOUNT 10100

6,12,530 6,12,530

M1 Analyse the transactions to show the progression from a previous trial balance to the next

one using double entry book keeping

Trial Balance serves as a medium to detect any mathematical errors that may have been

overlooked while preparing Journal and Ledger. It breaks down the accounts recorded previously

into two columns- debit and credit. Debit Column of Trial Balance includes all accounts having a

debit balance and Credit Column includes all accounts having a credit balance. Any adjustment

regarding expenses and incomes has been excluded previously, such adjustments are

acknowledged and necessary changes are made in the Trial Balance. The accuracy of Trial

Balance is shown when both Debit and Credit Columns match.

D1 Apply trial balance figures to show which statement of financial accounts they will end up

After preparing the trial balance an income statement will be prepared which will include

expenses such as discount allowed (358), motor expenses (670) and incomes discount received

(750). Balance sheet will include assets like as bank a/c (17478) and liabilities.

CLIENT 2

P3 Financial accounts from given trial balance figures adjusting, depreciation and preparation

Peter Hampau

Statement of Profit or Loss for the year ended 31st July 2018

£ £ £

Sales 120000

Less COST OF SALES

26

Opening inventory 4,500

Add - Purchases 70,000

74,500

Less - Closing inventory 42,640 31,860

GROSS PROFIT 88,140

Less Expenses

Wages and Salaries 16,500

Add amount accrued 1,520 18,020

Motor Expenses 4,580

Admin expenses 1,650

Heating and Lighting 550

Advertising expenses 1,030

Less – Prepaid amount -4,47 583

Depreciation on:

Premises 560

Equipment 1900

Motor Vehicles 600 2820 28203

Operating Profit 59937

Less - Finance cost 0

Profit before tax 59937

Tax 0

Profit for the year 59937

P4 Financial accounts subject to sole traders, partnerships or limited companies

Peter Hampau

27

Add - Purchases 70,000

74,500

Less - Closing inventory 42,640 31,860

GROSS PROFIT 88,140

Less Expenses

Wages and Salaries 16,500

Add amount accrued 1,520 18,020

Motor Expenses 4,580

Admin expenses 1,650

Heating and Lighting 550

Advertising expenses 1,030

Less – Prepaid amount -4,47 583

Depreciation on:

Premises 560

Equipment 1900

Motor Vehicles 600 2820 28203

Operating Profit 59937

Less - Finance cost 0

Profit before tax 59937

Tax 0

Profit for the year 59937

P4 Financial accounts subject to sole traders, partnerships or limited companies

Peter Hampau

27

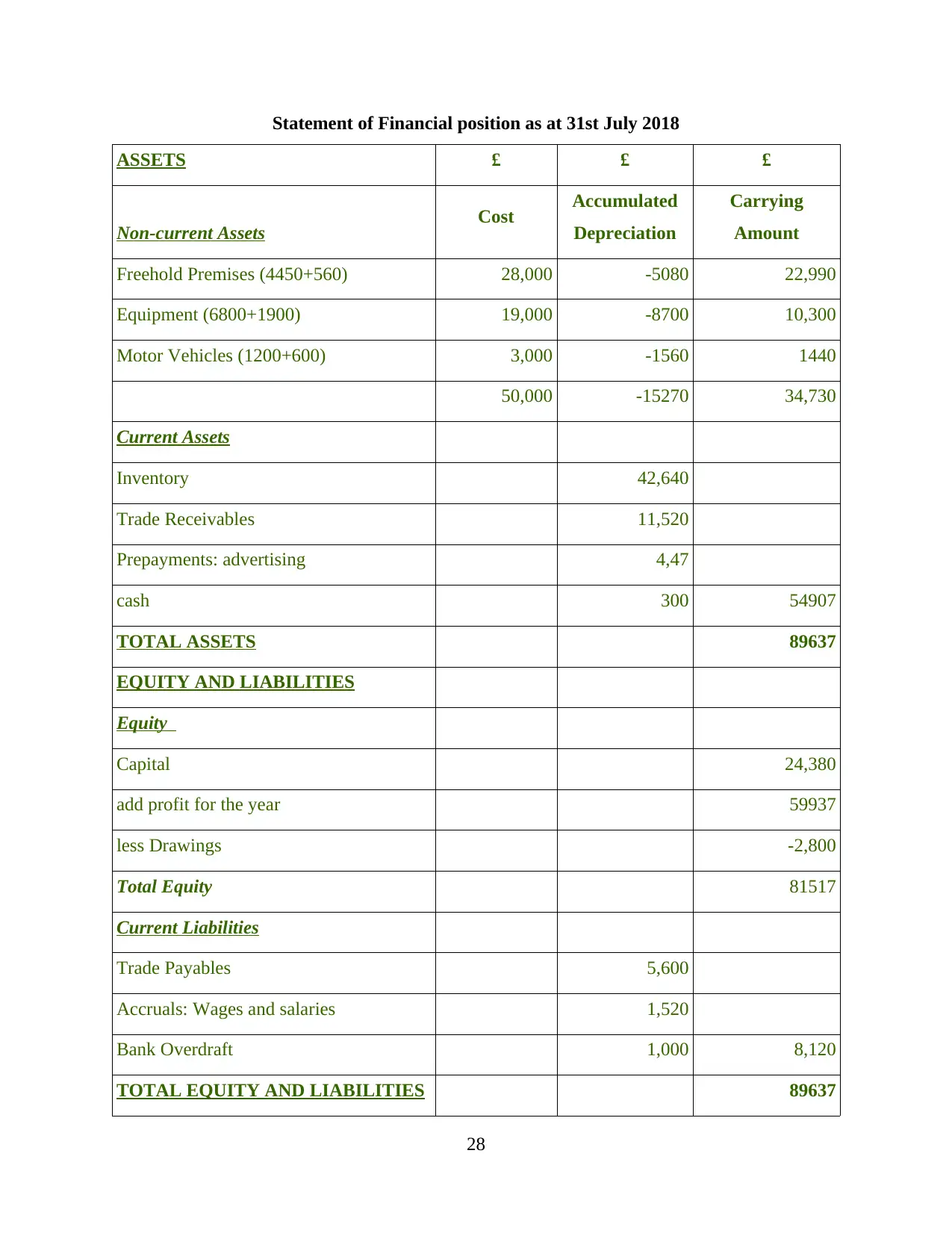

Statement of Financial position as at 31st July 2018

ASSETS £ £ £

Non-current Assets Cost Accumulated

Depreciation

Carrying

Amount

Freehold Premises (4450+560) 28,000 -5080 22,990

Equipment (6800+1900) 19,000 -8700 10,300

Motor Vehicles (1200+600) 3,000 -1560 1440

50,000 -15270 34,730

Current Assets

Inventory 42,640

Trade Receivables 11,520

Prepayments: advertising 4,47

cash 300 54907

TOTAL ASSETS 89637

EQUITY AND LIABILITIES

Equity

Capital 24,380

add profit for the year 59937

less Drawings -2,800

Total Equity 81517

Current Liabilities

Trade Payables 5,600

Accruals: Wages and salaries 1,520

Bank Overdraft 1,000 8,120

TOTAL EQUITY AND LIABILITIES 89637

28

ASSETS £ £ £

Non-current Assets Cost Accumulated

Depreciation

Carrying

Amount

Freehold Premises (4450+560) 28,000 -5080 22,990

Equipment (6800+1900) 19,000 -8700 10,300

Motor Vehicles (1200+600) 3,000 -1560 1440

50,000 -15270 34,730

Current Assets

Inventory 42,640

Trade Receivables 11,520

Prepayments: advertising 4,47

cash 300 54907

TOTAL ASSETS 89637

EQUITY AND LIABILITIES

Equity

Capital 24,380

add profit for the year 59937

less Drawings -2,800

Total Equity 81517

Current Liabilities

Trade Payables 5,600

Accruals: Wages and salaries 1,520

Bank Overdraft 1,000 8,120

TOTAL EQUITY AND LIABILITIES 89637

28

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

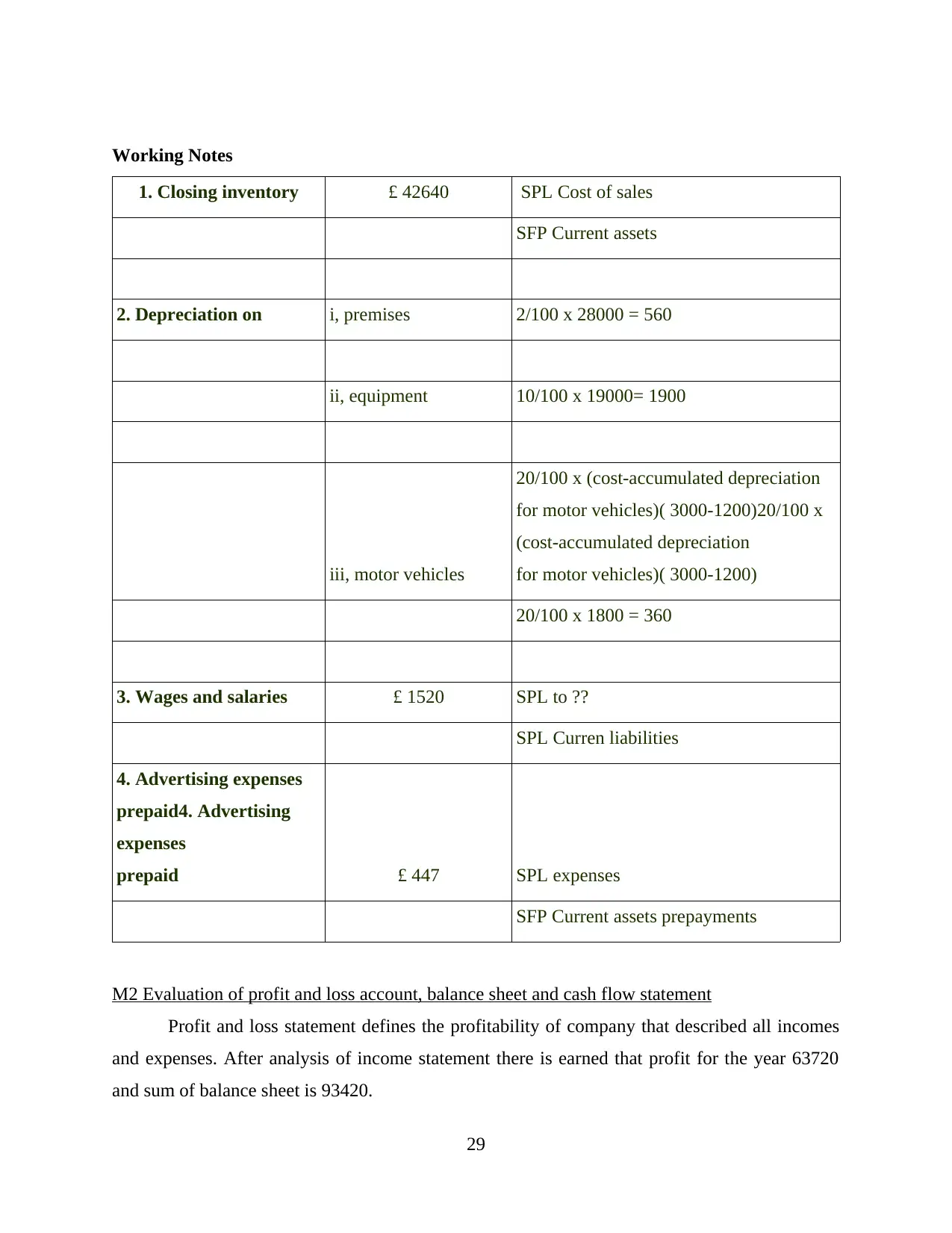

Working Notes

1. Closing inventory £ 42640 SPL Cost of sales

SFP Current assets

2. Depreciation on i, premises 2/100 x 28000 = 560

ii, equipment 10/100 x 19000= 1900

iii, motor vehicles

20/100 x (cost-accumulated depreciation

for motor vehicles)( 3000-1200)20/100 x

(cost-accumulated depreciation

for motor vehicles)( 3000-1200)

20/100 x 1800 = 360

3. Wages and salaries £ 1520 SPL to ??

SPL Curren liabilities

4. Advertising expenses

prepaid4. Advertising

expenses

prepaid £ 447 SPL expenses

SFP Current assets prepayments

M2 Evaluation of profit and loss account, balance sheet and cash flow statement

Profit and loss statement defines the profitability of company that described all incomes

and expenses. After analysis of income statement there is earned that profit for the year 63720

and sum of balance sheet is 93420.

29

1. Closing inventory £ 42640 SPL Cost of sales

SFP Current assets

2. Depreciation on i, premises 2/100 x 28000 = 560

ii, equipment 10/100 x 19000= 1900

iii, motor vehicles

20/100 x (cost-accumulated depreciation

for motor vehicles)( 3000-1200)20/100 x

(cost-accumulated depreciation

for motor vehicles)( 3000-1200)

20/100 x 1800 = 360

3. Wages and salaries £ 1520 SPL to ??

SPL Curren liabilities

4. Advertising expenses

prepaid4. Advertising

expenses

prepaid £ 447 SPL expenses

SFP Current assets prepayments

M2 Evaluation of profit and loss account, balance sheet and cash flow statement

Profit and loss statement defines the profitability of company that described all incomes

and expenses. After analysis of income statement there is earned that profit for the year 63720

and sum of balance sheet is 93420.

29

D2 Compare the essential features of each financial statement to analyse the differences between

them in terms purpose, structure and content

When analysis of financial statement so there is getting different purpose and structure

and content. In financial statement i9ncluding profit and loss statement and financial position of

company. The profit and loss account prepared for achieve net profit and loss and financial

position shows actual performance of company.

30

them in terms purpose, structure and content

When analysis of financial statement so there is getting different purpose and structure

and content. In financial statement i9ncluding profit and loss statement and financial position of

company. The profit and loss account prepared for achieve net profit and loss and financial

position shows actual performance of company.

30

CLIENT 3

a) Profit and loss statement of Ltd. For the year ended 31st July 2018

(b) Statement of financial statement of Bowling Ltd.

31

a) Profit and loss statement of Ltd. For the year ended 31st July 2018

(b) Statement of financial statement of Bowling Ltd.

31

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(c) Accounting Concepts:

Consistency Concept:

The Consistency Concept states that companies should follow a single methodology to

prepare its final accounts for financial years indefinitely. This helps both internal and external

users of financial statements in ensuring comparability between two financial years at a given

period of time to make effective business and investment decisions (Flamholtz, 2012). Unless the

company has no other alternative but to change its accounting policy, the same method must be

followed to prepare company's final accounts which was applicable for previous financial years.

Prudence Concept:

The Concept of Prudence encourages the habit of conservatism stating that revenues

should not be overestimated and expenses should not be underestimated while preparing

financial statements of a company. Thus, a revenue related transaction is taken into account only

32

Consistency Concept:

The Consistency Concept states that companies should follow a single methodology to

prepare its final accounts for financial years indefinitely. This helps both internal and external

users of financial statements in ensuring comparability between two financial years at a given

period of time to make effective business and investment decisions (Flamholtz, 2012). Unless the

company has no other alternative but to change its accounting policy, the same method must be

followed to prepare company's final accounts which was applicable for previous financial years.

Prudence Concept:

The Concept of Prudence encourages the habit of conservatism stating that revenues

should not be overestimated and expenses should not be underestimated while preparing

financial statements of a company. Thus, a revenue related transaction is taken into account only

32

when it is certain and an expense related transaction is taken into account when it is likely to be

incurred. Until and unless a source of revenue is certain, it is not to be recorded. Its main aim is

to represent realistic picture of the operational activities of a company.

(d) Purpose of Depreciation in formulating Accounting statements and the methods used for

calculation of Depreciation:

Depreciation is defined as a process of allocation of costs to the tangible assets such as

machinery, equipment, vehicles, etc. used for business purpose. It acts as reduction in value of

such assets on the grounds of wear and tear, obsolescence over an assets useful life. Purpose of

depreciation is charging an appropriate cost to the capital assets in relation to revenues earned by

them in a year. There are two widely used methods used to calculate depreciation for an asset.

They are as follows-

Straight Line Method:

Straight Line Method involves allocation of equal or fixed amount of depreciation of an

asset over its useful life. This method is usually adopted by Manufacturing industries and in case

of leases. It is calculated as follows- [(Book Value of Asset- Salvage Value)/Useful Life in

years]. Salvage value means the value of the asset at the end of its useful life (Bozkurt, Islamoglu

and Oz, 2013).

Written Down Value Method:

Written Down Value Method involves allocation of an appropriate percentage of

depreciation is charged to the asset over its useful life in proportion to its use. The amount of

depreciation charged over the years goes on diminishing as the asset reaches the end of its useful

life. It is calculated as follows- [{100*[1-((s/c)1 /n)]} where n denotes number of years, s denotes

salvage value and c denotes cost of asset.

CLIENT 4

P5 Apply the bank reconciliation process to make a number of a reconciliation

(a) Need and Importance of Bank Reconciliation Statements:

A Bank Reconciliation Statement is a summarized report prepared by the company that

helps in reconciling differences between Bank balance shown in the books of firm and Bank

Balance stated by firm's Bank Statement. Thus, it is important for Durrell Ltd. to reconcile such

irregularities on monthly basis by preparing a Bank Reconciliation Statement and making

33

incurred. Until and unless a source of revenue is certain, it is not to be recorded. Its main aim is

to represent realistic picture of the operational activities of a company.

(d) Purpose of Depreciation in formulating Accounting statements and the methods used for

calculation of Depreciation:

Depreciation is defined as a process of allocation of costs to the tangible assets such as

machinery, equipment, vehicles, etc. used for business purpose. It acts as reduction in value of

such assets on the grounds of wear and tear, obsolescence over an assets useful life. Purpose of

depreciation is charging an appropriate cost to the capital assets in relation to revenues earned by

them in a year. There are two widely used methods used to calculate depreciation for an asset.

They are as follows-

Straight Line Method:

Straight Line Method involves allocation of equal or fixed amount of depreciation of an

asset over its useful life. This method is usually adopted by Manufacturing industries and in case

of leases. It is calculated as follows- [(Book Value of Asset- Salvage Value)/Useful Life in

years]. Salvage value means the value of the asset at the end of its useful life (Bozkurt, Islamoglu

and Oz, 2013).

Written Down Value Method:

Written Down Value Method involves allocation of an appropriate percentage of

depreciation is charged to the asset over its useful life in proportion to its use. The amount of

depreciation charged over the years goes on diminishing as the asset reaches the end of its useful

life. It is calculated as follows- [{100*[1-((s/c)1 /n)]} where n denotes number of years, s denotes

salvage value and c denotes cost of asset.

CLIENT 4

P5 Apply the bank reconciliation process to make a number of a reconciliation

(a) Need and Importance of Bank Reconciliation Statements:

A Bank Reconciliation Statement is a summarized report prepared by the company that

helps in reconciling differences between Bank balance shown in the books of firm and Bank

Balance stated by firm's Bank Statement. Thus, it is important for Durrell Ltd. to reconcile such

irregularities on monthly basis by preparing a Bank Reconciliation Statement and making

33

1 out of 36

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.