Financial Accounting Report

VerifiedAdded on 2020/10/22

|21

|5839

|347

AI Summary

This financial accounting report delves into the main motive of financial accounting, which is to communicate the true and fair view of an organization's financial performance and position. It highlights how all accounting functions are linked with reporting financial performance and guided by principles of financial accounting. The report also emphasizes the importance of financial accounting in providing a framework for decision-making activities and determining objectives and goals of a business organization.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

Principles

Principles

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................4

BUSINESS REPORT......................................................................................................................4

1.Financial Accounting and its purpose:................................................................................4

2. Internal and external stakeholder:......................................................................................5

CLIENT 1........................................................................................................................................6

1. Journal Entries and Ledgers in the book of Alexandra Study:...........................................6

2. Trial Balance as at 31st January 2019 in the books of Alexandra Study:........................13

CLIENT 2......................................................................................................................................14

1. Statement of Profit and Loss of Munteanu Ltd. For the year ended 31st December 2018:14

2. Statement of financial position of Munteanu Ltd. As at 31st December 2018:...............15

3. Accounting Concepts: Consistency and Prudency:..........................................................16

4. Purpose of depreciation in formulating accounting statement:........................................16

5. Evaluation of difference between financial statements prepared by the sole trader & the

limited companies ................................................................................................................16

CLIENT 3 .....................................................................................................................................17

1. Purpose of preparation of Bank-reconciliation Statement:..............................................17

2. Reasons for difference between balance of bank column of cash book and bank statements:

..............................................................................................................................................17

3. Imprest:.............................................................................................................................17

4. Bank-reconciliation Statement as at 30 September 2018:................................................17

CLIENT 4......................................................................................................................................18

1. Sales Ledger Control Account in the books of January 2018:.........................................18

2. Purchase Ledger Control Account in the books of January 2018:...................................18

3. Control Account:..............................................................................................................19

CLIENT 5......................................................................................................................................19

1. Suspense account and its main features:..........................................................................19

2. Trial Balance using a control account as balancing figure:..............................................19

3. Journal Entries for corrections:........................................................................................20

CONCLUSION..............................................................................................................................20

INTRODUCTION...........................................................................................................................4

BUSINESS REPORT......................................................................................................................4

1.Financial Accounting and its purpose:................................................................................4

2. Internal and external stakeholder:......................................................................................5

CLIENT 1........................................................................................................................................6

1. Journal Entries and Ledgers in the book of Alexandra Study:...........................................6

2. Trial Balance as at 31st January 2019 in the books of Alexandra Study:........................13

CLIENT 2......................................................................................................................................14

1. Statement of Profit and Loss of Munteanu Ltd. For the year ended 31st December 2018:14

2. Statement of financial position of Munteanu Ltd. As at 31st December 2018:...............15

3. Accounting Concepts: Consistency and Prudency:..........................................................16

4. Purpose of depreciation in formulating accounting statement:........................................16

5. Evaluation of difference between financial statements prepared by the sole trader & the

limited companies ................................................................................................................16

CLIENT 3 .....................................................................................................................................17

1. Purpose of preparation of Bank-reconciliation Statement:..............................................17

2. Reasons for difference between balance of bank column of cash book and bank statements:

..............................................................................................................................................17

3. Imprest:.............................................................................................................................17

4. Bank-reconciliation Statement as at 30 September 2018:................................................17

CLIENT 4......................................................................................................................................18

1. Sales Ledger Control Account in the books of January 2018:.........................................18

2. Purchase Ledger Control Account in the books of January 2018:...................................18

3. Control Account:..............................................................................................................19

CLIENT 5......................................................................................................................................19

1. Suspense account and its main features:..........................................................................19

2. Trial Balance using a control account as balancing figure:..............................................19

3. Journal Entries for corrections:........................................................................................20

CONCLUSION..............................................................................................................................20

REFERENCES .............................................................................................................................22

INTRODUCTION

Financial accounting is an organised course of action including activities such as

recording of accounting transaction, classification, verification, interpreting, summarizing and

communicating or reporting of financial information. Financial accounting provides details and

information regarding availability of existing or potential resources, way of financing and output

through their utilisation. Financial accounting also provides groundwork for Internal and external

stakeholders in order to take significant decisions (Agasisti and Catalano, 2013). In order to

analyse the performance of PURCO company has been taken into account. All activities and

functions of financial accounting are governed or administrated by some rules and guidelines

called as financial accounting principles such as UK GAAP (Generally Accepted Accounting

Principles). This report provides an explanation about definition of financial accounting, purpose

of financial accounting, internal and external stakeholders and brief knowledge about accounting

concepts, purpose of providing depreciation and major methods of depreciation, control accounts

and purpose of bank reconciliation statements.

BUSINESS REPORT

1. Financial Accounting and its purpose:

Financial accounting refers to a systematic process classification of financial and non-

financial transactions, recording of transaction, summarizing them for a better interpretation and

reporting under a formal format to internal and external stakeholders. Financial accounting

processes are structure in a systematic way and ensures compliances of various accounting

principles, policies, rules and regulations (Alver, Alver and Talpas, 2013). Financial accounting

gives a structure for quick assessment of any problems and for taking vital decisions. Following

are the most considerable purpose of financial accounting, as follows:

Financial reporting helps to record all financial transactions as per double entry

system in an organised manner.

It helps to assess the actual position and performance of business organisation.

It assists in projecting anticipated earnings and performance of business organisation.

INTRODUCTION

Financial accounting is an organised course of action including activities such as

recording of accounting transaction, classification, verification, interpreting, summarizing and

communicating or reporting of financial information. Financial accounting provides details and

information regarding availability of existing or potential resources, way of financing and output

through their utilisation. Financial accounting also provides groundwork for Internal and external

stakeholders in order to take significant decisions (Agasisti and Catalano, 2013). In order to

analyse the performance of PURCO company has been taken into account. All activities and

functions of financial accounting are governed or administrated by some rules and guidelines

called as financial accounting principles such as UK GAAP (Generally Accepted Accounting

Principles). This report provides an explanation about definition of financial accounting, purpose

of financial accounting, internal and external stakeholders and brief knowledge about accounting

concepts, purpose of providing depreciation and major methods of depreciation, control accounts

and purpose of bank reconciliation statements.

BUSINESS REPORT

1. Financial Accounting and its purpose:

Financial accounting refers to a systematic process classification of financial and non-

financial transactions, recording of transaction, summarizing them for a better interpretation and

reporting under a formal format to internal and external stakeholders. Financial accounting

processes are structure in a systematic way and ensures compliances of various accounting

principles, policies, rules and regulations (Alver, Alver and Talpas, 2013). Financial accounting

gives a structure for quick assessment of any problems and for taking vital decisions. Following

are the most considerable purpose of financial accounting, as follows:

Financial reporting helps to record all financial transactions as per double entry

system in an organised manner.

It helps to assess the actual position and performance of business organisation.

It assists in projecting anticipated earnings and performance of business organisation.

Financial reporting provides a basis for better decision making to investors and other

stakeholders actual profitability and liquidity situation of business organisation as on

a particular date.

It ensures compliance of statutory requirements, policies, framework, rules and

regulations.

It provides a comparative data and records along with previous years’ data and

competitor’s data and record to evaluate the performance effectively.

It serves as a formal report of financial health of business organisation to top

management and external users of financial information (Barth, 2015).

It helps to classify organisation's various assets and liabilities in order to manage

them efficiently.

2. Internal and external stakeholder:

Stakeholders are person, individual, group, body of individuals or organisation having

direct or indirect interest in organisation's position, performance, objectives or goals and results.

Stakeholder are classified as internal stakeholders and external stakeholders. Internal

stakeholders are person, group or individuals within the business organisation having substantial

interest. Whereas external stakeholders are individuals, persons, group or organisation outside

the business organisation associated with organisation and having direct or indirect interest

(Edwards, 2013).

Internal Stakeholder: In a large business organisation, internal stakeholders are shareholders,

owners, management and employees (Stice and Stice, 2013). Following is a brief discussion

about major internal stakeholders and, possible way through which they are interested in

financial information of organisation, as follows:

Owners and shareholders: They are real stakeholders of entity. Owner and shareholders

are holding major shares of a large business organisation and gain profits in case of

increase in share price. They are highly affected by the performance and financial

position of company.

Employees: Employees are most considerable resources of a business organisation and

always wants to achieve growth within the organisation. Employees are having

sustainable stake in business organisation because their salary and career are dependent

on performance and growth of organisation.

stakeholders actual profitability and liquidity situation of business organisation as on

a particular date.

It ensures compliance of statutory requirements, policies, framework, rules and

regulations.

It provides a comparative data and records along with previous years’ data and

competitor’s data and record to evaluate the performance effectively.

It serves as a formal report of financial health of business organisation to top

management and external users of financial information (Barth, 2015).

It helps to classify organisation's various assets and liabilities in order to manage

them efficiently.

2. Internal and external stakeholder:

Stakeholders are person, individual, group, body of individuals or organisation having

direct or indirect interest in organisation's position, performance, objectives or goals and results.

Stakeholder are classified as internal stakeholders and external stakeholders. Internal

stakeholders are person, group or individuals within the business organisation having substantial

interest. Whereas external stakeholders are individuals, persons, group or organisation outside

the business organisation associated with organisation and having direct or indirect interest

(Edwards, 2013).

Internal Stakeholder: In a large business organisation, internal stakeholders are shareholders,

owners, management and employees (Stice and Stice, 2013). Following is a brief discussion

about major internal stakeholders and, possible way through which they are interested in

financial information of organisation, as follows:

Owners and shareholders: They are real stakeholders of entity. Owner and shareholders

are holding major shares of a large business organisation and gain profits in case of

increase in share price. They are highly affected by the performance and financial

position of company.

Employees: Employees are most considerable resources of a business organisation and

always wants to achieve growth within the organisation. Employees are having

sustainable stake in business organisation because their salary and career are dependent

on performance and growth of organisation.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

External Stakeholder: External stakeholders in case of a large business organisation are its

customers. Suppliers, government, creditors etc. Following is a short explanation about key

external stakeholders and, manner through which they are interested in financial information of

organisation, as follows:

Government: Government collect various taxes on income of business organisation so

government hold stake in profits of entities in form of taxes. Government along with collection

of taxes insures proper compliance of rules and regulation in business organisation.

Suppliers: Suppliers of goods and raw material receives payments from business

organisation and full-fills the demands. They always try to receive payment in scheduled times

and provides credit based on liquidity position of company so suppliers having stake in business

organisation in form of their payments and sales (DRURY, 2013).

Customers: Customers decides an organisation's growth and revenue. They contribute in

business by purchasing and by recommending product of company to others. Customers buy

product or services of organisation by analysing their popularity, quality, performance, growth

and beliefs therefore they are holding stake in form of performance and sustainability of business

organisation.

Investors: Investors are most significant for business organisation because they

contribute in expansion and growth of company by investing their money or other financial

assets in company. They are highly affected by performance and growth of business

organisation. Investors are actual stakeholder of company because they always try to get

maximum return from investment made by in business organisation.

CLIENT 1

1. Journal Entries and Ledgers in the book of Alexandra Study:

SALES DAY BOOK

DATE DETAILS £

2018

03 January

2018 J Wilson 1,200

T Cole 1,650

F Syma 2,100

J Allen 1,020

P White 2,520

F Lane 980

customers. Suppliers, government, creditors etc. Following is a short explanation about key

external stakeholders and, manner through which they are interested in financial information of

organisation, as follows:

Government: Government collect various taxes on income of business organisation so

government hold stake in profits of entities in form of taxes. Government along with collection

of taxes insures proper compliance of rules and regulation in business organisation.

Suppliers: Suppliers of goods and raw material receives payments from business

organisation and full-fills the demands. They always try to receive payment in scheduled times

and provides credit based on liquidity position of company so suppliers having stake in business

organisation in form of their payments and sales (DRURY, 2013).

Customers: Customers decides an organisation's growth and revenue. They contribute in

business by purchasing and by recommending product of company to others. Customers buy

product or services of organisation by analysing their popularity, quality, performance, growth

and beliefs therefore they are holding stake in form of performance and sustainability of business

organisation.

Investors: Investors are most significant for business organisation because they

contribute in expansion and growth of company by investing their money or other financial

assets in company. They are highly affected by performance and growth of business

organisation. Investors are actual stakeholder of company because they always try to get

maximum return from investment made by in business organisation.

CLIENT 1

1. Journal Entries and Ledgers in the book of Alexandra Study:

SALES DAY BOOK

DATE DETAILS £

2018

03 January

2018 J Wilson 1,200

T Cole 1,650

F Syma 2,100

J Allen 1,020

P White 2,520

F Lane 980

09 January

2018 T Cole 680

J FOX 1,310

Credit in sales account in Nominal Ledger 11,460

PURCHASES DAY BOOK

DATE DETAILS £

2018

02 January 2018 S.Hood 1,450

D Main 2,060

W.Tone 960

R Foot 1,610

22 January 2018 L Mole 1,830

W Wright 1,910

Debit Purchases account in Nominal Ledger 9,820

PURCHASES RETURNS DAY BOOK

DATE DETAILS £

2018

19 January 2018 R Foot 50

Credit purchases returns account

in Nominal Ledger 50

SALES RETURNS DAY BOOK

DATE DETAILS £

2018

11 January 2018 J Wilson 270

F Syma 410

2018 T Cole 680

J FOX 1,310

Credit in sales account in Nominal Ledger 11,460

PURCHASES DAY BOOK

DATE DETAILS £

2018

02 January 2018 S.Hood 1,450

D Main 2,060

W.Tone 960

R Foot 1,610

22 January 2018 L Mole 1,830

W Wright 1,910

Debit Purchases account in Nominal Ledger 9,820

PURCHASES RETURNS DAY BOOK

DATE DETAILS £

2018

19 January 2018 R Foot 50

Credit purchases returns account

in Nominal Ledger 50

SALES RETURNS DAY BOOK

DATE DETAILS £

2018

11 January 2018 J Wilson 270

F Syma 410

Debit sales returns account

in Nominal Ledger 680

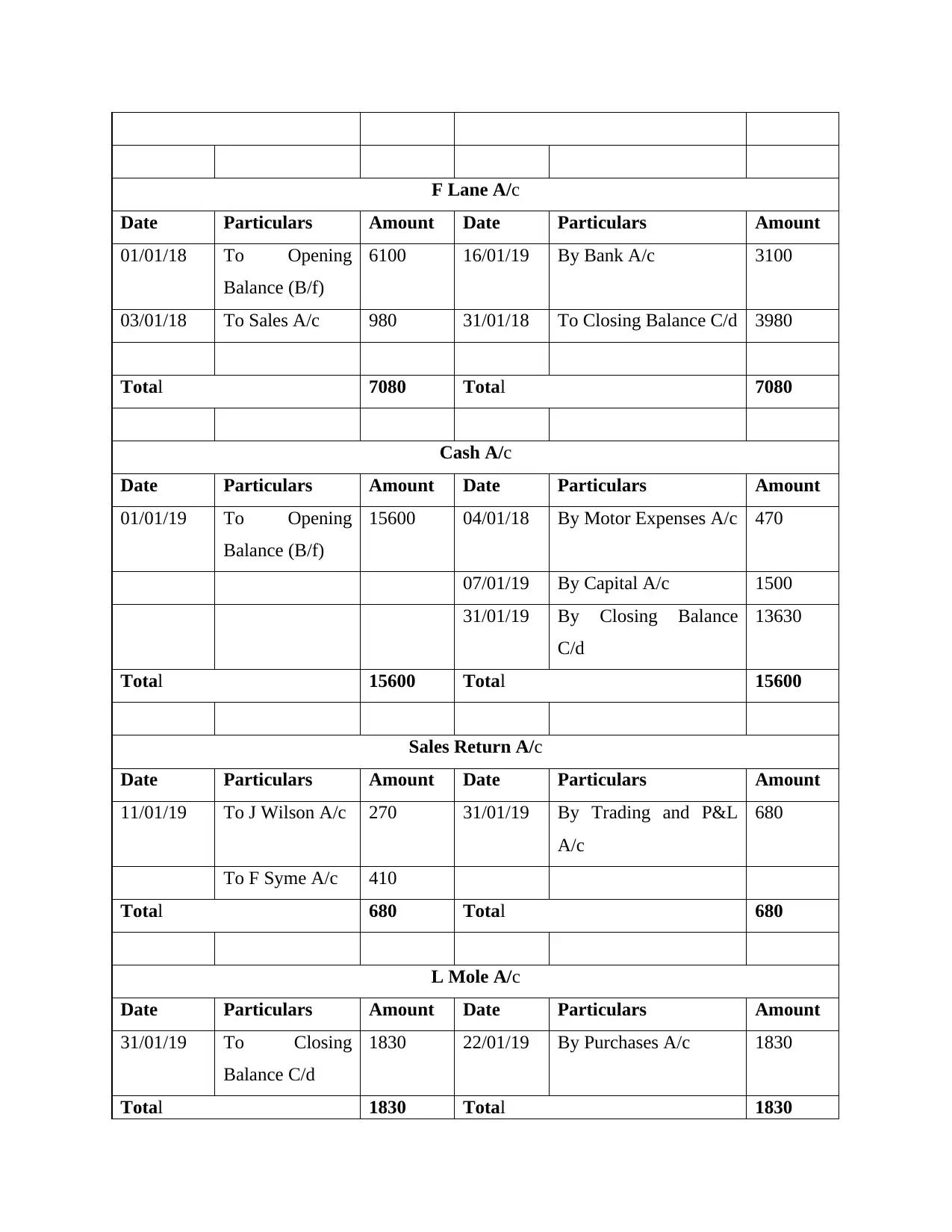

Ledgers

Purchases A/c

Date Particulars Amount Date Particulars Amount

02/01/19 To S Hood A/c 1450 31/01/19 By Trading and P&L

A/c

9820

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

22/01/19 To L Mole A/c 1830

To W Wright

A/c

1910

Total 9820 Total 9820

Bank A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

68400 01/01/19 By Storage cost A/c 450

16/01/19 To P Mullen A/c 1400 24/01/19 By S Hood A/c 3600

To F Lane A/c 3100 By J Brown A/c 4600

To J Wilson A/c 850 By R Foot A/c 1400

To F Syme A/c 1670 27/01/19 By Salaries A/c 4800

30/01/19 By Business Rates A/c 1320

31/01/19 By Closing Balance

C/d

59250

Total 75420 Total 75420

D Main A/c

Date Particulars Amount Date Particulars Amount

in Nominal Ledger 680

Ledgers

Purchases A/c

Date Particulars Amount Date Particulars Amount

02/01/19 To S Hood A/c 1450 31/01/19 By Trading and P&L

A/c

9820

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

22/01/19 To L Mole A/c 1830

To W Wright

A/c

1910

Total 9820 Total 9820

Bank A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

68400 01/01/19 By Storage cost A/c 450

16/01/19 To P Mullen A/c 1400 24/01/19 By S Hood A/c 3600

To F Lane A/c 3100 By J Brown A/c 4600

To J Wilson A/c 850 By R Foot A/c 1400

To F Syme A/c 1670 27/01/19 By Salaries A/c 4800

30/01/19 By Business Rates A/c 1320

31/01/19 By Closing Balance

C/d

59250

Total 75420 Total 75420

D Main A/c

Date Particulars Amount Date Particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

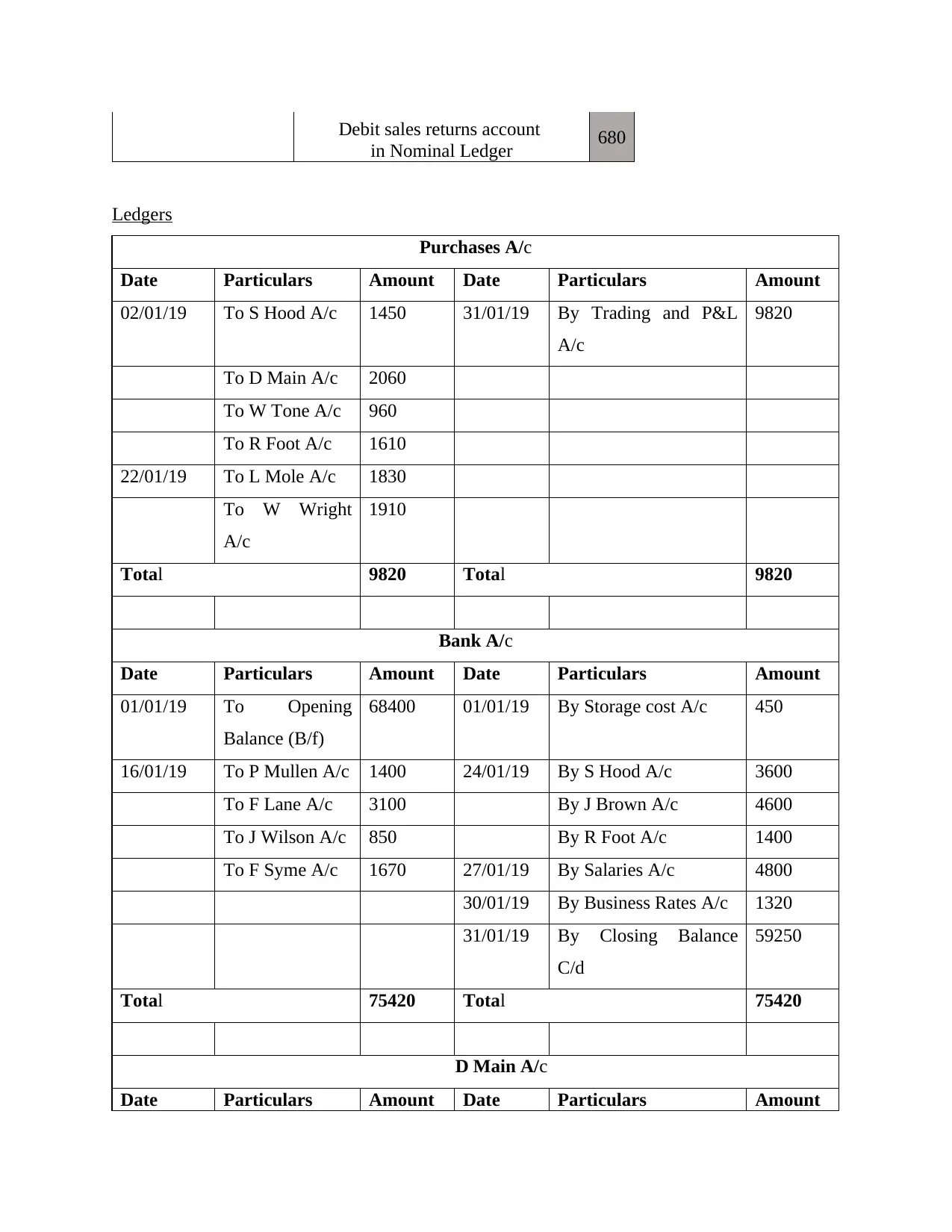

31/01/19 To Closing

Balance A/c

2060 02/01/19 By purchases A/c 2060

Total 2060 Total 2060

By Purchases Return A/c

Date Particulars Amount Date Particulars Amount

31/01/18 To Trading and

P&L A/c

50 19/01/18 By R foot A/c 50

50 50

R Foot A/c

Date Particulars Amount Date Particulars Amount

19/01/18 To Purchase

Return A/c

50 02/01/19 By purchases A/c 1610

24/01/19 To Bank A/c 1400

31/01/19 By Closing

Balance C/d

160

Total 1450 Total 1610

T Cole A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1650 31/01/19 By Closing Balance

C/d

2330

09/01/19 To Sales A/c 680

Total 2330 Total 2330

J Allen A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1020 31/01/19 By Closing Balance

C/d

1020

Total 1020 Total 1020

Balance A/c

2060 02/01/19 By purchases A/c 2060

Total 2060 Total 2060

By Purchases Return A/c

Date Particulars Amount Date Particulars Amount

31/01/18 To Trading and

P&L A/c

50 19/01/18 By R foot A/c 50

50 50

R Foot A/c

Date Particulars Amount Date Particulars Amount

19/01/18 To Purchase

Return A/c

50 02/01/19 By purchases A/c 1610

24/01/19 To Bank A/c 1400

31/01/19 By Closing

Balance C/d

160

Total 1450 Total 1610

T Cole A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1650 31/01/19 By Closing Balance

C/d

2330

09/01/19 To Sales A/c 680

Total 2330 Total 2330

J Allen A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1020 31/01/19 By Closing Balance

C/d

1020

Total 1020 Total 1020

F Lane A/c

Date Particulars Amount Date Particulars Amount

01/01/18 To Opening

Balance (B/f)

6100 16/01/19 By Bank A/c 3100

03/01/18 To Sales A/c 980 31/01/18 To Closing Balance C/d 3980

Total 7080 Total 7080

Cash A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

15600 04/01/18 By Motor Expenses A/c 470

07/01/19 By Capital A/c 1500

31/01/19 By Closing Balance

C/d

13630

Total 15600 Total 15600

Sales Return A/c

Date Particulars Amount Date Particulars Amount

11/01/19 To J Wilson A/c 270 31/01/19 By Trading and P&L

A/c

680

To F Syme A/c 410

Total 680 Total 680

L Mole A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1830 22/01/19 By Purchases A/c 1830

Total 1830 Total 1830

Date Particulars Amount Date Particulars Amount

01/01/18 To Opening

Balance (B/f)

6100 16/01/19 By Bank A/c 3100

03/01/18 To Sales A/c 980 31/01/18 To Closing Balance C/d 3980

Total 7080 Total 7080

Cash A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

15600 04/01/18 By Motor Expenses A/c 470

07/01/19 By Capital A/c 1500

31/01/19 By Closing Balance

C/d

13630

Total 15600 Total 15600

Sales Return A/c

Date Particulars Amount Date Particulars Amount

11/01/19 To J Wilson A/c 270 31/01/19 By Trading and P&L

A/c

680

To F Syme A/c 410

Total 680 Total 680

L Mole A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1830 22/01/19 By Purchases A/c 1830

Total 1830 Total 1830

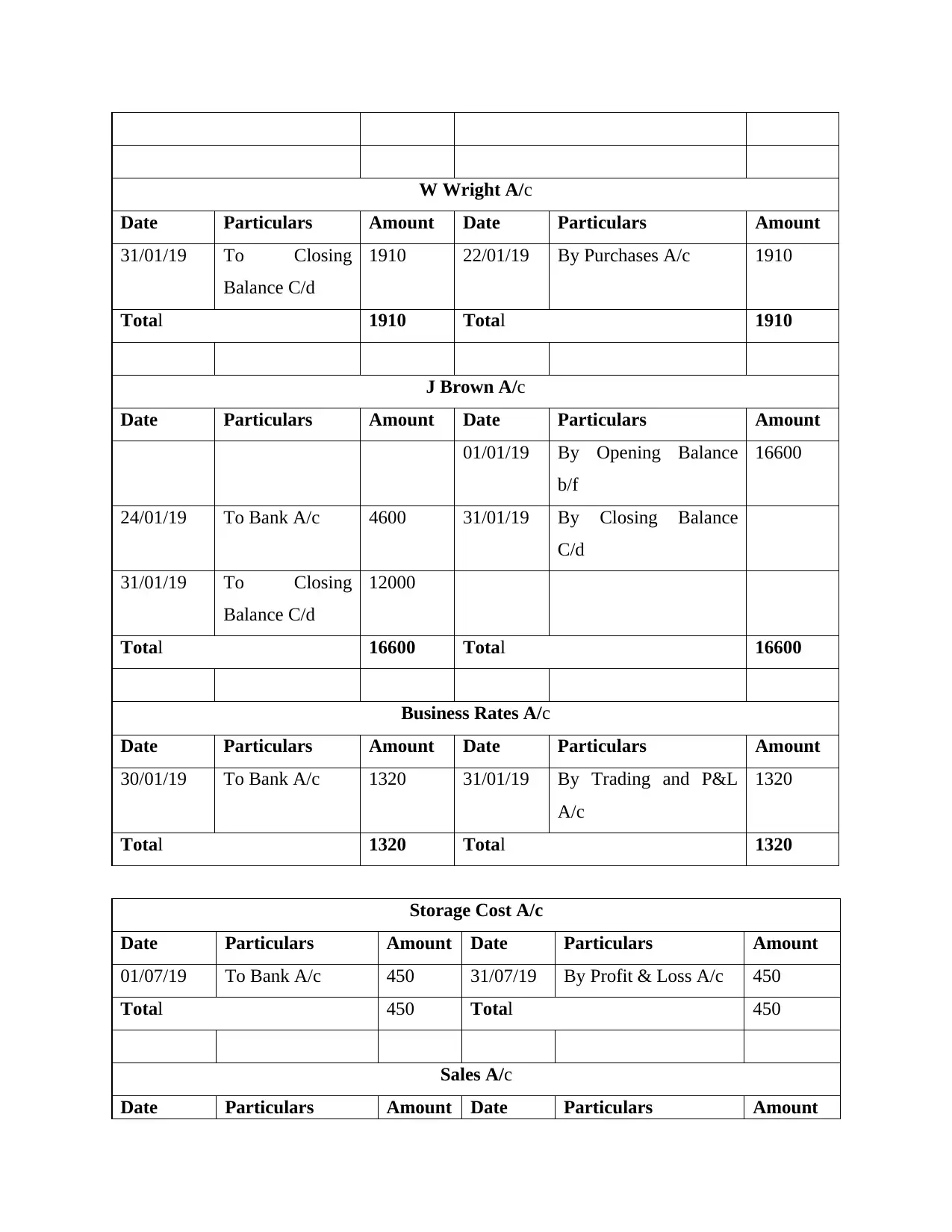

W Wright A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1910 22/01/19 By Purchases A/c 1910

Total 1910 Total 1910

J Brown A/c

Date Particulars Amount Date Particulars Amount

01/01/19 By Opening Balance

b/f

16600

24/01/19 To Bank A/c 4600 31/01/19 By Closing Balance

C/d

31/01/19 To Closing

Balance C/d

12000

Total 16600 Total 16600

Business Rates A/c

Date Particulars Amount Date Particulars Amount

30/01/19 To Bank A/c 1320 31/01/19 By Trading and P&L

A/c

1320

Total 1320 Total 1320

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/19 To Bank A/c 450 31/07/19 By Profit & Loss A/c 450

Total 450 Total 450

Sales A/c

Date Particulars Amount Date Particulars Amount

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1910 22/01/19 By Purchases A/c 1910

Total 1910 Total 1910

J Brown A/c

Date Particulars Amount Date Particulars Amount

01/01/19 By Opening Balance

b/f

16600

24/01/19 To Bank A/c 4600 31/01/19 By Closing Balance

C/d

31/01/19 To Closing

Balance C/d

12000

Total 16600 Total 16600

Business Rates A/c

Date Particulars Amount Date Particulars Amount

30/01/19 To Bank A/c 1320 31/01/19 By Trading and P&L

A/c

1320

Total 1320 Total 1320

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/19 To Bank A/c 450 31/07/19 By Profit & Loss A/c 450

Total 450 Total 450

Sales A/c

Date Particulars Amount Date Particulars Amount

Secure Best Marks with AI Grader

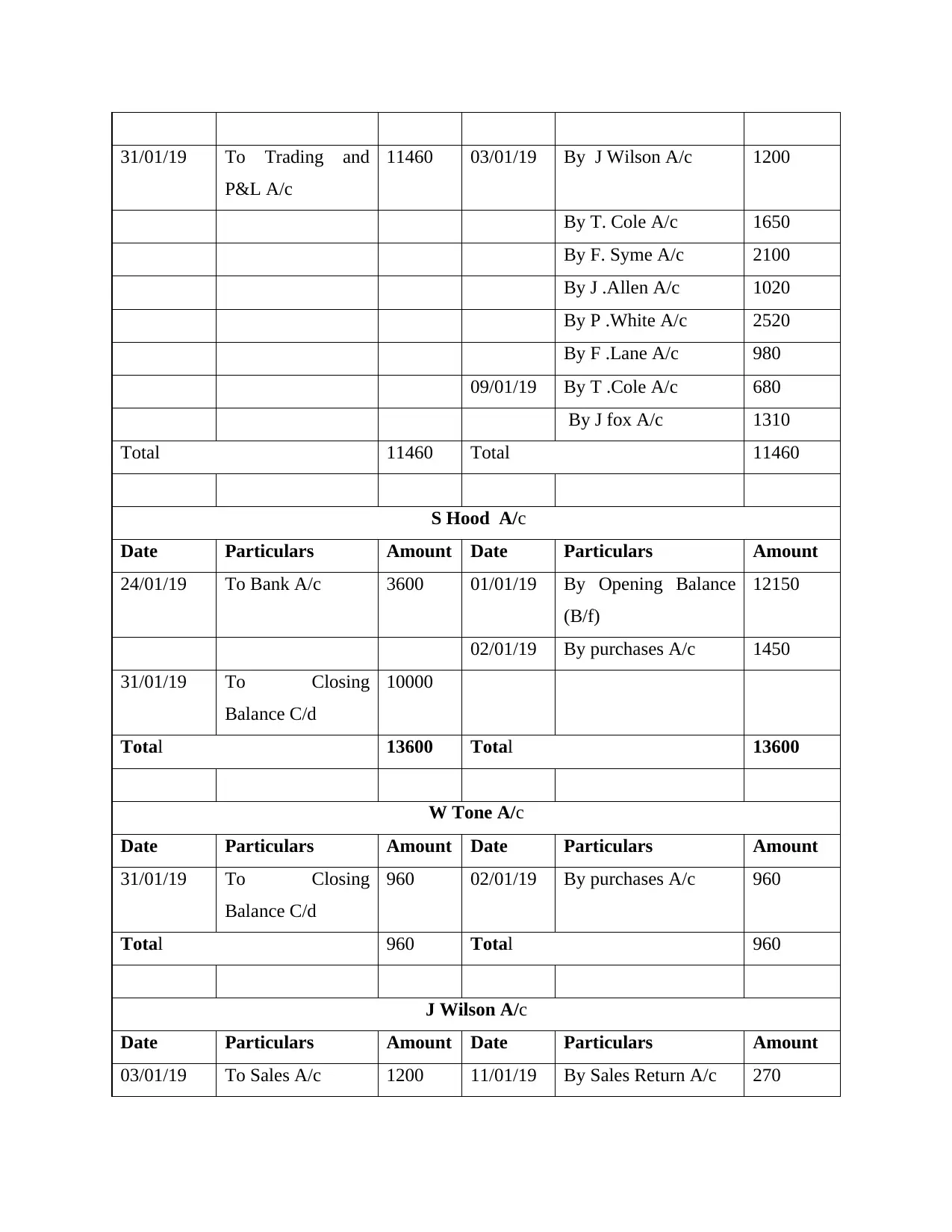

Need help grading? Try our AI Grader for instant feedback on your assignments.

31/01/19 To Trading and

P&L A/c

11460 03/01/19 By J Wilson A/c 1200

By T. Cole A/c 1650

By F. Syme A/c 2100

By J .Allen A/c 1020

By P .White A/c 2520

By F .Lane A/c 980

09/01/19 By T .Cole A/c 680

By J fox A/c 1310

Total 11460 Total 11460

S Hood A/c

Date Particulars Amount Date Particulars Amount

24/01/19 To Bank A/c 3600 01/01/19 By Opening Balance

(B/f)

12150

02/01/19 By purchases A/c 1450

31/01/19 To Closing

Balance C/d

10000

Total 13600 Total 13600

W Tone A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

960 02/01/19 By purchases A/c 960

Total 960 Total 960

J Wilson A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1200 11/01/19 By Sales Return A/c 270

P&L A/c

11460 03/01/19 By J Wilson A/c 1200

By T. Cole A/c 1650

By F. Syme A/c 2100

By J .Allen A/c 1020

By P .White A/c 2520

By F .Lane A/c 980

09/01/19 By T .Cole A/c 680

By J fox A/c 1310

Total 11460 Total 11460

S Hood A/c

Date Particulars Amount Date Particulars Amount

24/01/19 To Bank A/c 3600 01/01/19 By Opening Balance

(B/f)

12150

02/01/19 By purchases A/c 1450

31/01/19 To Closing

Balance C/d

10000

Total 13600 Total 13600

W Tone A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

960 02/01/19 By purchases A/c 960

Total 960 Total 960

J Wilson A/c

Date Particulars Amount Date Particulars Amount

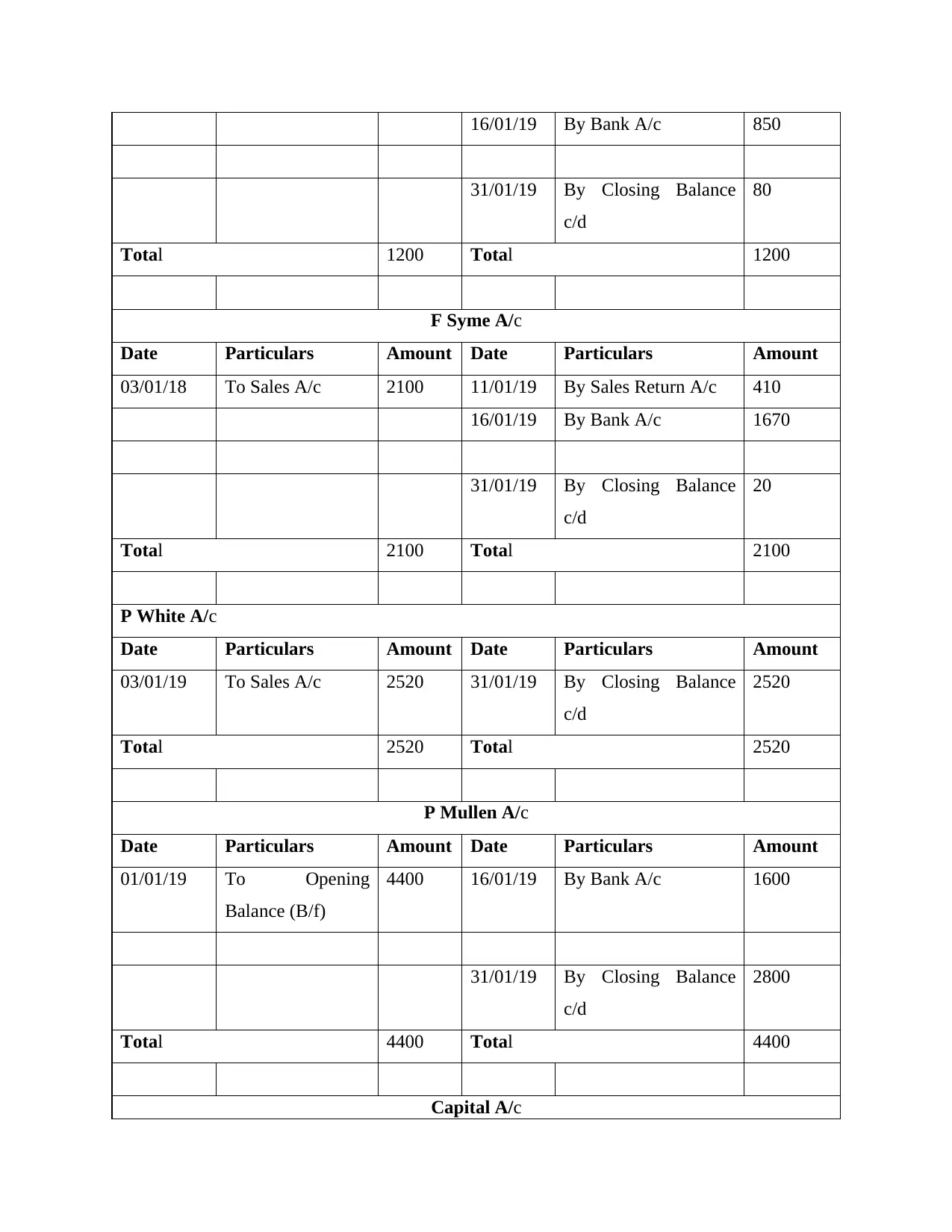

03/01/19 To Sales A/c 1200 11/01/19 By Sales Return A/c 270

16/01/19 By Bank A/c 850

31/01/19 By Closing Balance

c/d

80

Total 1200 Total 1200

F Syme A/c

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/c 2100 11/01/19 By Sales Return A/c 410

16/01/19 By Bank A/c 1670

31/01/19 By Closing Balance

c/d

20

Total 2100 Total 2100

P White A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 2520 31/01/19 By Closing Balance

c/d

2520

Total 2520 Total 2520

P Mullen A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

4400 16/01/19 By Bank A/c 1600

31/01/19 By Closing Balance

c/d

2800

Total 4400 Total 4400

Capital A/c

31/01/19 By Closing Balance

c/d

80

Total 1200 Total 1200

F Syme A/c

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/c 2100 11/01/19 By Sales Return A/c 410

16/01/19 By Bank A/c 1670

31/01/19 By Closing Balance

c/d

20

Total 2100 Total 2100

P White A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 2520 31/01/19 By Closing Balance

c/d

2520

Total 2520 Total 2520

P Mullen A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

4400 16/01/19 By Bank A/c 1600

31/01/19 By Closing Balance

c/d

2800

Total 4400 Total 4400

Capital A/c

Date Particulars Amount Date Particulars Amount

07/01/18 To Cash A/c 1500 01/01/18 By Opening Balance

b/f

389000

31/01/18 To Closing

Balance C/d

387500

Total 389000 Total 389000

J Allen A/c

Date Particulars Amount Date Particulars Amount

09/01/18 To Sales A/c 1310 31/01/18 By Closing Balance

c/d

1310

Total 1310 Total 1310

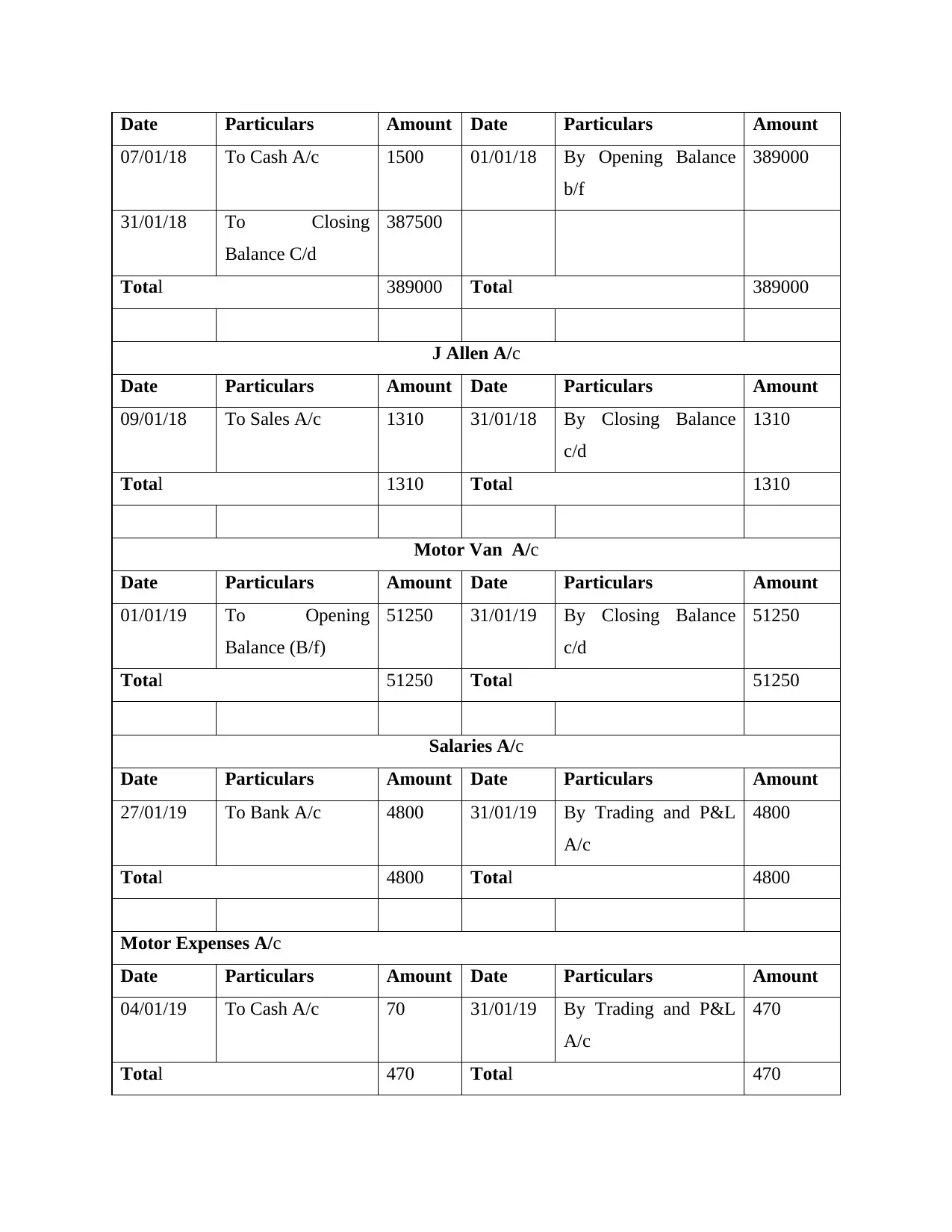

Motor Van A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

51250 31/01/19 By Closing Balance

c/d

51250

Total 51250 Total 51250

Salaries A/c

Date Particulars Amount Date Particulars Amount

27/01/19 To Bank A/c 4800 31/01/19 By Trading and P&L

A/c

4800

Total 4800 Total 4800

Motor Expenses A/c

Date Particulars Amount Date Particulars Amount

04/01/19 To Cash A/c 70 31/01/19 By Trading and P&L

A/c

470

Total 470 Total 470

07/01/18 To Cash A/c 1500 01/01/18 By Opening Balance

b/f

389000

31/01/18 To Closing

Balance C/d

387500

Total 389000 Total 389000

J Allen A/c

Date Particulars Amount Date Particulars Amount

09/01/18 To Sales A/c 1310 31/01/18 By Closing Balance

c/d

1310

Total 1310 Total 1310

Motor Van A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

51250 31/01/19 By Closing Balance

c/d

51250

Total 51250 Total 51250

Salaries A/c

Date Particulars Amount Date Particulars Amount

27/01/19 To Bank A/c 4800 31/01/19 By Trading and P&L

A/c

4800

Total 4800 Total 4800

Motor Expenses A/c

Date Particulars Amount Date Particulars Amount

04/01/19 To Cash A/c 70 31/01/19 By Trading and P&L

A/c

470

Total 470 Total 470

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

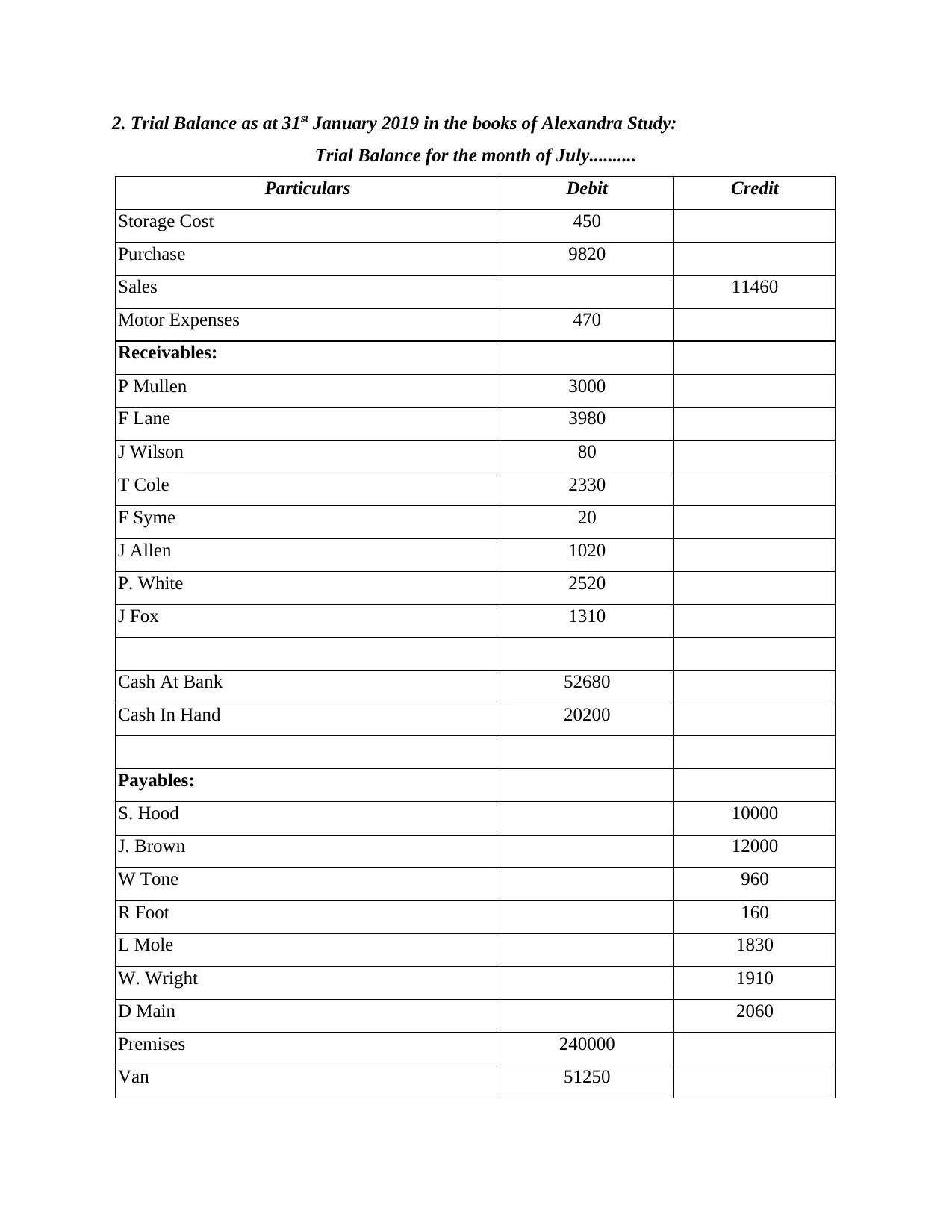

2. Trial Balance as at 31st January 2019 in the books of Alexandra Study:

Trial Balance for the month of July..........

Particulars Debit Credit

Storage Cost 450

Purchase 9820

Sales 11460

Motor Expenses 470

Receivables:

P Mullen 3000

F Lane 3980

J Wilson 80

T Cole 2330

F Syme 20

J Allen 1020

P. White 2520

J Fox 1310

Cash At Bank 52680

Cash In Hand 20200

Payables:

S. Hood 10000

J. Brown 12000

W Tone 960

R Foot 160

L Mole 1830

W. Wright 1910

D Main 2060

Premises 240000

Van 51250

Trial Balance for the month of July..........

Particulars Debit Credit

Storage Cost 450

Purchase 9820

Sales 11460

Motor Expenses 470

Receivables:

P Mullen 3000

F Lane 3980

J Wilson 80

T Cole 2330

F Syme 20

J Allen 1020

P. White 2520

J Fox 1310

Cash At Bank 52680

Cash In Hand 20200

Payables:

S. Hood 10000

J. Brown 12000

W Tone 960

R Foot 160

L Mole 1830

W. Wright 1910

D Main 2060

Premises 240000

Van 51250

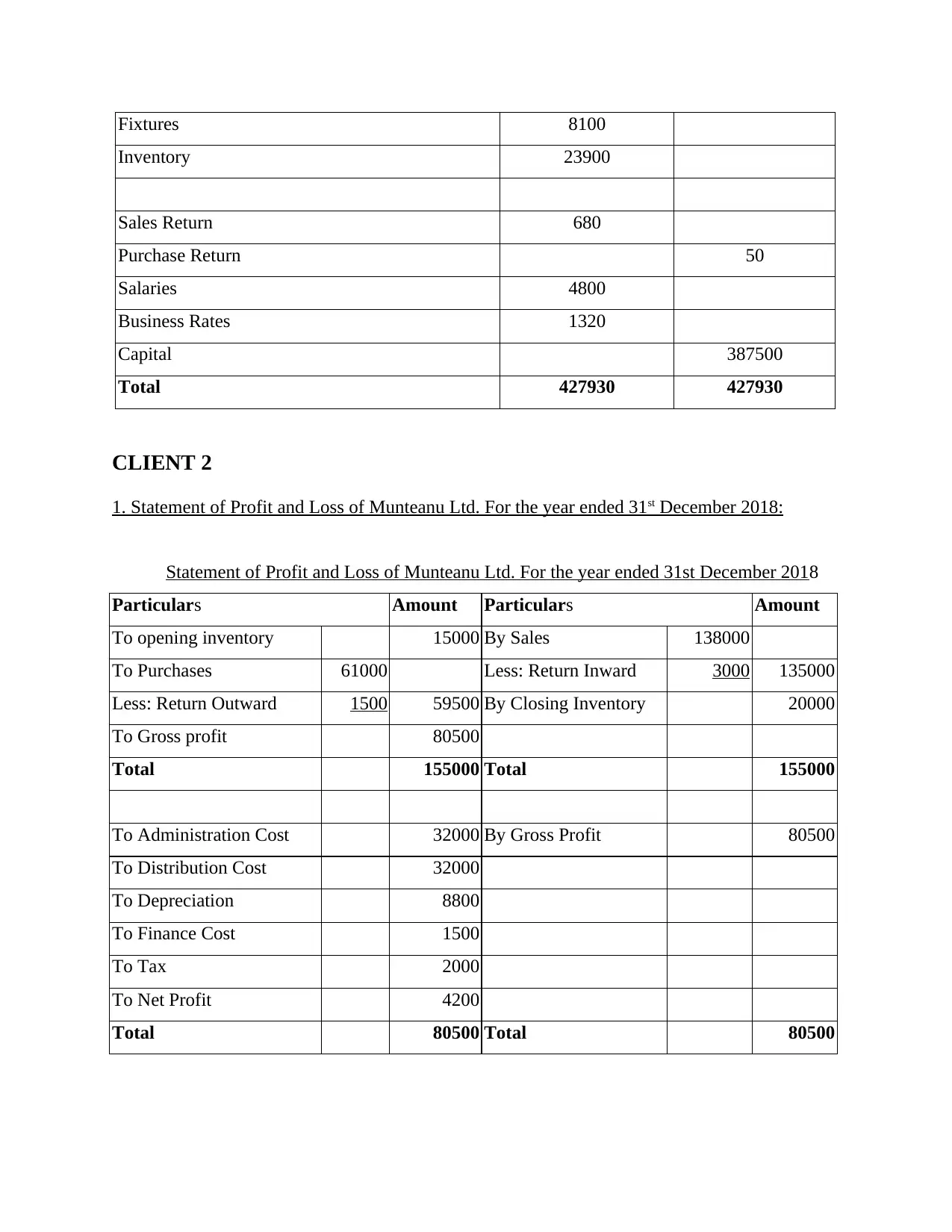

Fixtures 8100

Inventory 23900

Sales Return 680

Purchase Return 50

Salaries 4800

Business Rates 1320

Capital 387500

Total 427930 427930

CLIENT 2

1. Statement of Profit and Loss of Munteanu Ltd. For the year ended 31st December 2018:

Statement of Profit and Loss of Munteanu Ltd. For the year ended 31st December 2018

Particulars Amount Particulars Amount

To opening inventory 15000 By Sales 138000

To Purchases 61000 Less: Return Inward 3000 135000

Less: Return Outward 1500 59500 By Closing Inventory 20000

To Gross profit 80500

Total 155000 Total 155000

To Administration Cost 32000 By Gross Profit 80500

To Distribution Cost 32000

To Depreciation 8800

To Finance Cost 1500

To Tax 2000

To Net Profit 4200

Total 80500 Total 80500

Inventory 23900

Sales Return 680

Purchase Return 50

Salaries 4800

Business Rates 1320

Capital 387500

Total 427930 427930

CLIENT 2

1. Statement of Profit and Loss of Munteanu Ltd. For the year ended 31st December 2018:

Statement of Profit and Loss of Munteanu Ltd. For the year ended 31st December 2018

Particulars Amount Particulars Amount

To opening inventory 15000 By Sales 138000

To Purchases 61000 Less: Return Inward 3000 135000

Less: Return Outward 1500 59500 By Closing Inventory 20000

To Gross profit 80500

Total 155000 Total 155000

To Administration Cost 32000 By Gross Profit 80500

To Distribution Cost 32000

To Depreciation 8800

To Finance Cost 1500

To Tax 2000

To Net Profit 4200

Total 80500 Total 80500

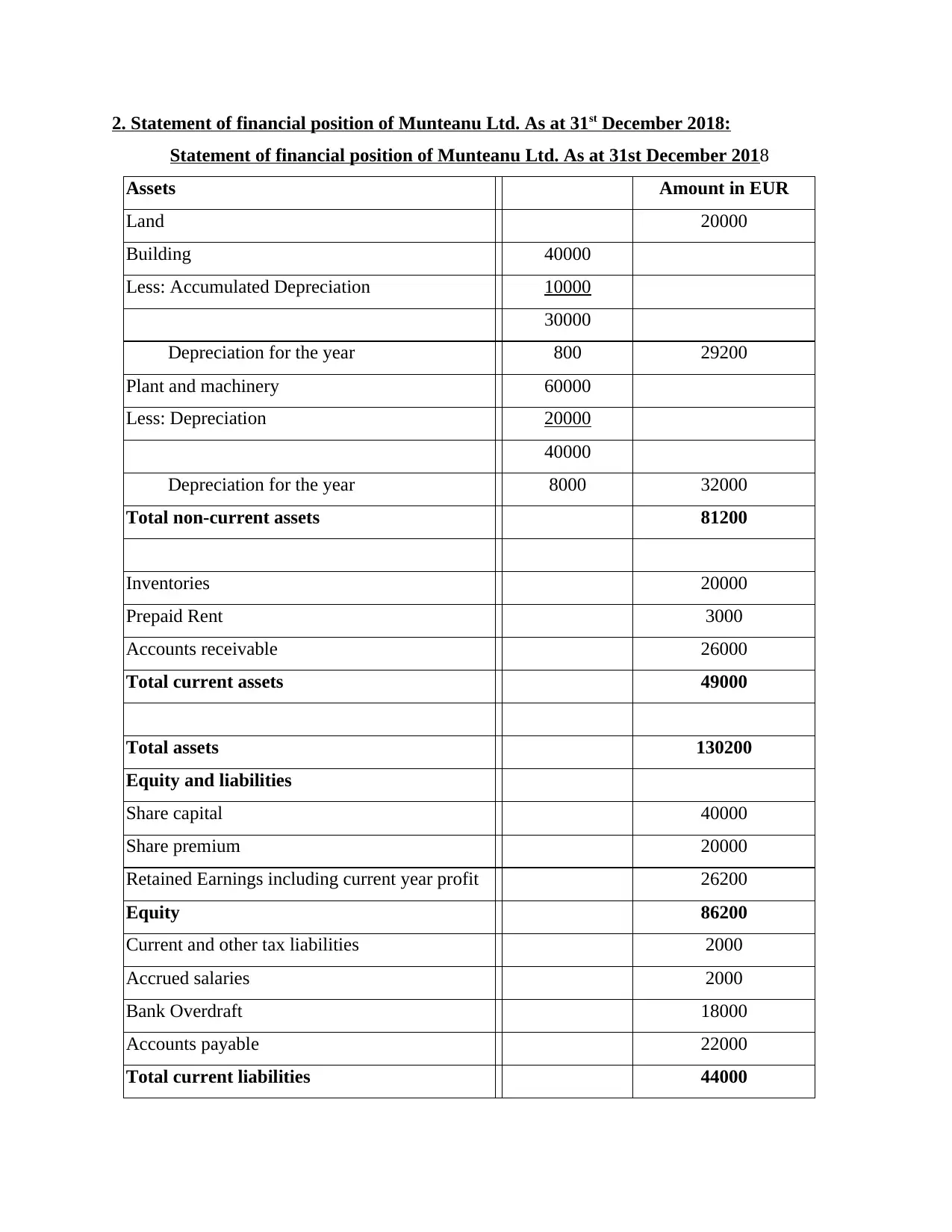

2. Statement of financial position of Munteanu Ltd. As at 31st December 2018:

Statement of financial position of Munteanu Ltd. As at 31st December 2018

Assets Amount in EUR

Land 20000

Building 40000

Less: Accumulated Depreciation 10000

30000

Depreciation for the year 800 29200

Plant and machinery 60000

Less: Depreciation 20000

40000

Depreciation for the year 8000 32000

Total non-current assets 81200

Inventories 20000

Prepaid Rent 3000

Accounts receivable 26000

Total current assets 49000

Total assets 130200

Equity and liabilities

Share capital 40000

Share premium 20000

Retained Earnings including current year profit 26200

Equity 86200

Current and other tax liabilities 2000

Accrued salaries 2000

Bank Overdraft 18000

Accounts payable 22000

Total current liabilities 44000

Statement of financial position of Munteanu Ltd. As at 31st December 2018

Assets Amount in EUR

Land 20000

Building 40000

Less: Accumulated Depreciation 10000

30000

Depreciation for the year 800 29200

Plant and machinery 60000

Less: Depreciation 20000

40000

Depreciation for the year 8000 32000

Total non-current assets 81200

Inventories 20000

Prepaid Rent 3000

Accounts receivable 26000

Total current assets 49000

Total assets 130200

Equity and liabilities

Share capital 40000

Share premium 20000

Retained Earnings including current year profit 26200

Equity 86200

Current and other tax liabilities 2000

Accrued salaries 2000

Bank Overdraft 18000

Accounts payable 22000

Total current liabilities 44000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

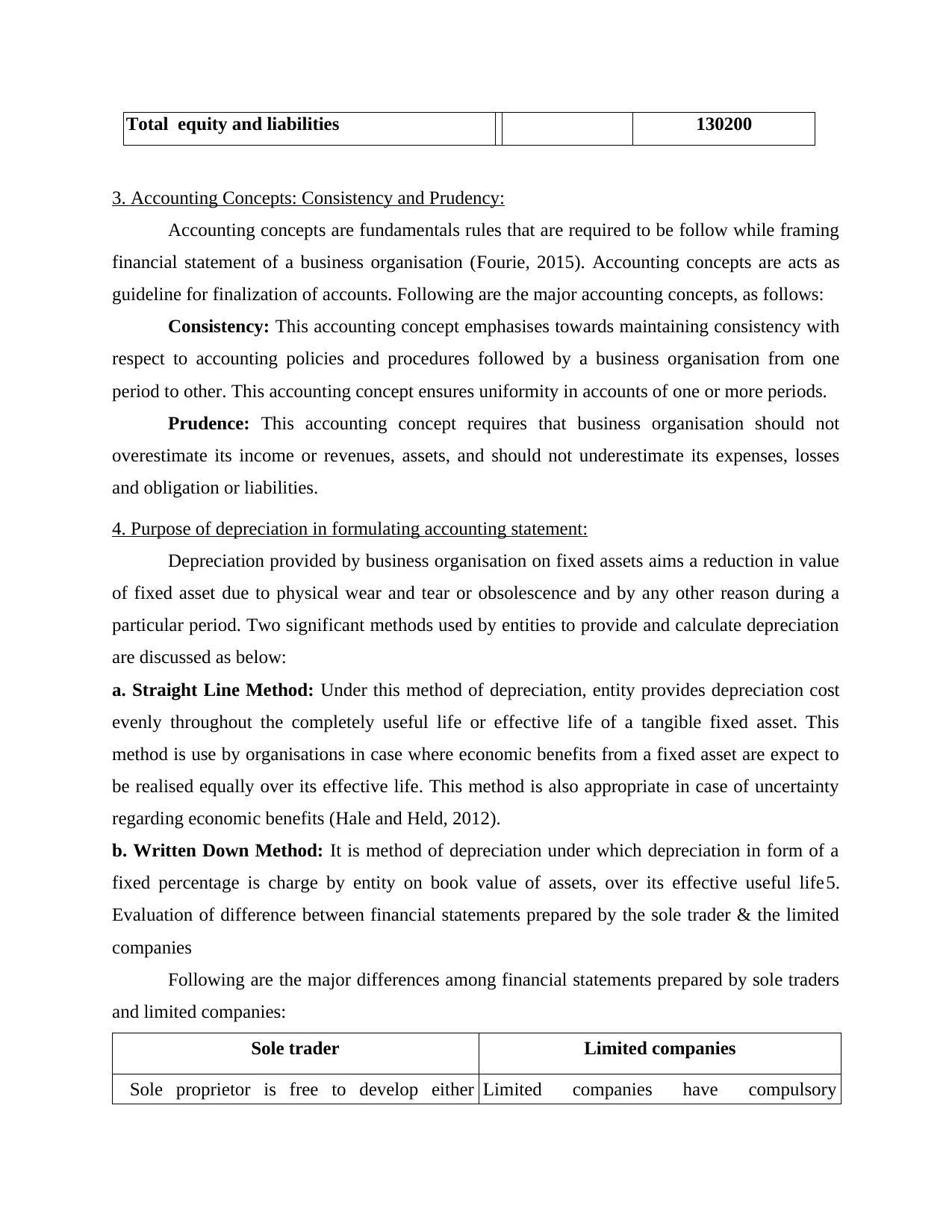

Total equity and liabilities 130200

3. Accounting Concepts: Consistency and Prudency:

Accounting concepts are fundamentals rules that are required to be follow while framing

financial statement of a business organisation (Fourie, 2015). Accounting concepts are acts as

guideline for finalization of accounts. Following are the major accounting concepts, as follows:

Consistency: This accounting concept emphasises towards maintaining consistency with

respect to accounting policies and procedures followed by a business organisation from one

period to other. This accounting concept ensures uniformity in accounts of one or more periods.

Prudence: This accounting concept requires that business organisation should not

overestimate its income or revenues, assets, and should not underestimate its expenses, losses

and obligation or liabilities.

4. Purpose of depreciation in formulating accounting statement:

Depreciation provided by business organisation on fixed assets aims a reduction in value

of fixed asset due to physical wear and tear or obsolescence and by any other reason during a

particular period. Two significant methods used by entities to provide and calculate depreciation

are discussed as below:

a. Straight Line Method: Under this method of depreciation, entity provides depreciation cost

evenly throughout the completely useful life or effective life of a tangible fixed asset. This

method is use by organisations in case where economic benefits from a fixed asset are expect to

be realised equally over its effective life. This method is also appropriate in case of uncertainty

regarding economic benefits (Hale and Held, 2012).

b. Written Down Method: It is method of depreciation under which depreciation in form of a

fixed percentage is charge by entity on book value of assets, over its effective useful life5.

Evaluation of difference between financial statements prepared by the sole trader & the limited

companies

Following are the major differences among financial statements prepared by sole traders

and limited companies:

Sole trader Limited companies

Sole proprietor is free to develop either Limited companies have compulsory

3. Accounting Concepts: Consistency and Prudency:

Accounting concepts are fundamentals rules that are required to be follow while framing

financial statement of a business organisation (Fourie, 2015). Accounting concepts are acts as

guideline for finalization of accounts. Following are the major accounting concepts, as follows:

Consistency: This accounting concept emphasises towards maintaining consistency with

respect to accounting policies and procedures followed by a business organisation from one

period to other. This accounting concept ensures uniformity in accounts of one or more periods.

Prudence: This accounting concept requires that business organisation should not

overestimate its income or revenues, assets, and should not underestimate its expenses, losses

and obligation or liabilities.

4. Purpose of depreciation in formulating accounting statement:

Depreciation provided by business organisation on fixed assets aims a reduction in value

of fixed asset due to physical wear and tear or obsolescence and by any other reason during a

particular period. Two significant methods used by entities to provide and calculate depreciation

are discussed as below:

a. Straight Line Method: Under this method of depreciation, entity provides depreciation cost

evenly throughout the completely useful life or effective life of a tangible fixed asset. This

method is use by organisations in case where economic benefits from a fixed asset are expect to

be realised equally over its effective life. This method is also appropriate in case of uncertainty

regarding economic benefits (Hale and Held, 2012).

b. Written Down Method: It is method of depreciation under which depreciation in form of a

fixed percentage is charge by entity on book value of assets, over its effective useful life5.

Evaluation of difference between financial statements prepared by the sole trader & the limited

companies

Following are the major differences among financial statements prepared by sole traders

and limited companies:

Sole trader Limited companies

Sole proprietor is free to develop either Limited companies have compulsory

horizontal or vertical balance sheet (Hall,

2012).

obligation to prepare vertical balance sheet

only

In this, the financial position of a sole

proprietorship is showing through the amount

of the assets held.

They mainly use their financial information for

making overall decision in relation to the

company profitability.

CLIENT 3

1. Purpose of preparation of Bank-reconciliation Statement:

Every business organisation prepares cashbook in which cash as well as bank transactions

are record. Sometimes difference arises in amount in bank column of cashbook and balance of

bank statement due some common reasons. So in order to reconcile such balance bank-

reconciliation statement is prepared by Burcu organisation. Bank-reconciliation statement is

prepared by entities on monthly basis, annual basis and quarterly basis. However, most of the

entities prepare bank reconciliation statements on monthly basis to avoid any complexity at year-

end (Jonson, 2013).

2. Reasons for difference between balance of bank column of cash book and bank statements:

Most common reasons for difference between balance on the bank statement and the

balance on the books are deposits in transit, errors of books, electronic charges charged by bank

but not yet recorded in books, outstanding charges, check printing charges, bank service charges,

cheque issued but not presented etc.

3. Imprest:

Imprest is a system of accounting in which a fixed amount is reserve by organisation for

payment of day-to-day small amount of expenses. Petty cash book is an example of accounting

under imprest system (Tschopp and Nastanski, 2014).

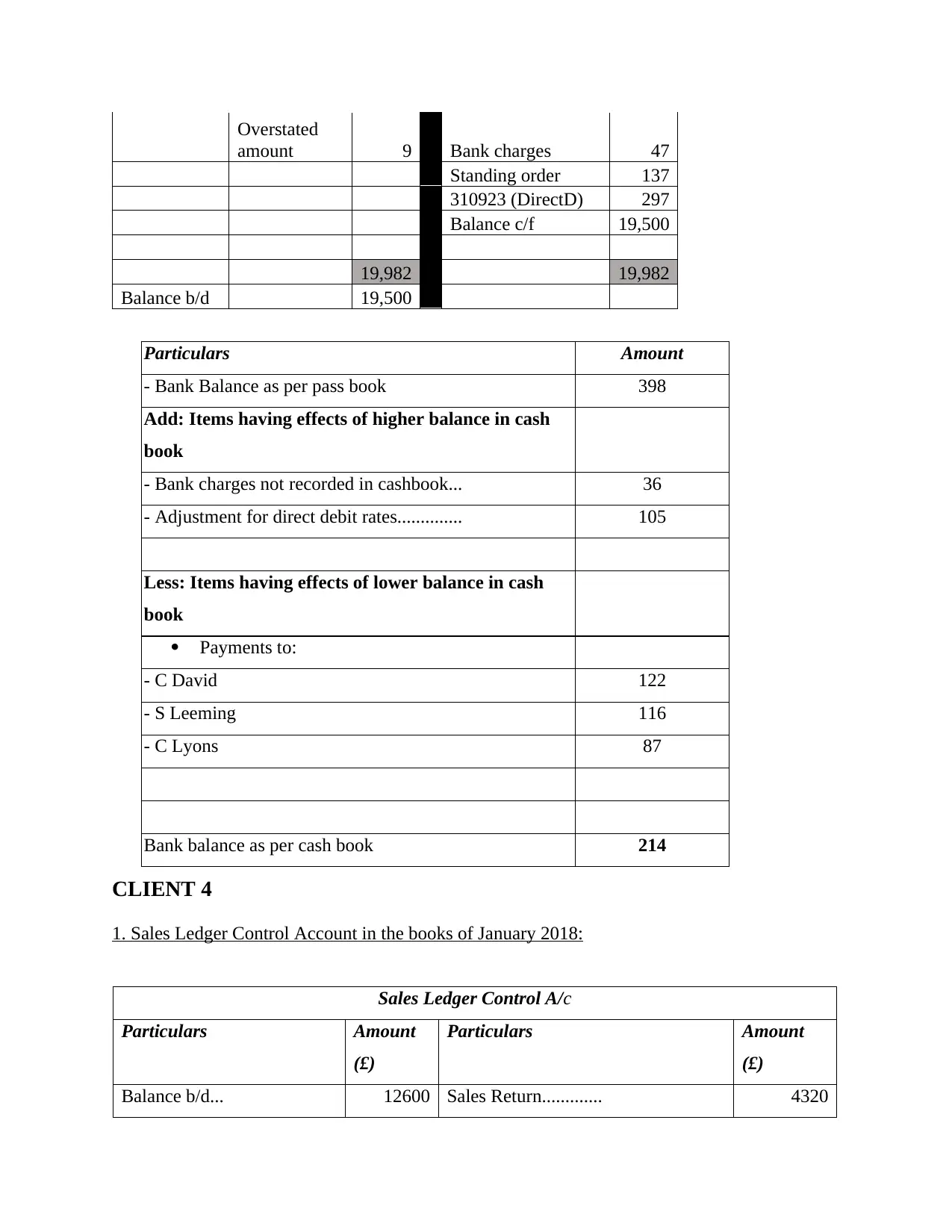

4. Bank-reconciliation Statement as at 30 September 2018:

Dr Corrected Cash Book (Bank) Cr

£ £

31-Dec Balance b/d 19,973

Overstated

amount 1

2012).

obligation to prepare vertical balance sheet

only

In this, the financial position of a sole

proprietorship is showing through the amount

of the assets held.

They mainly use their financial information for

making overall decision in relation to the

company profitability.

CLIENT 3

1. Purpose of preparation of Bank-reconciliation Statement:

Every business organisation prepares cashbook in which cash as well as bank transactions

are record. Sometimes difference arises in amount in bank column of cashbook and balance of

bank statement due some common reasons. So in order to reconcile such balance bank-

reconciliation statement is prepared by Burcu organisation. Bank-reconciliation statement is

prepared by entities on monthly basis, annual basis and quarterly basis. However, most of the

entities prepare bank reconciliation statements on monthly basis to avoid any complexity at year-

end (Jonson, 2013).

2. Reasons for difference between balance of bank column of cash book and bank statements:

Most common reasons for difference between balance on the bank statement and the

balance on the books are deposits in transit, errors of books, electronic charges charged by bank

but not yet recorded in books, outstanding charges, check printing charges, bank service charges,

cheque issued but not presented etc.

3. Imprest:

Imprest is a system of accounting in which a fixed amount is reserve by organisation for

payment of day-to-day small amount of expenses. Petty cash book is an example of accounting

under imprest system (Tschopp and Nastanski, 2014).

4. Bank-reconciliation Statement as at 30 September 2018:

Dr Corrected Cash Book (Bank) Cr

£ £

31-Dec Balance b/d 19,973

Overstated

amount 1

Overstated

amount 9 Bank charges 47

Standing order 137

310923 (DirectD) 297

Balance c/f 19,500

19,982 19,982

Balance b/d 19,500

Particulars Amount

- Bank Balance as per pass book 398

Add: Items having effects of higher balance in cash

book

- Bank charges not recorded in cashbook... 36

- Adjustment for direct debit rates.............. 105

Less: Items having effects of lower balance in cash

book

Payments to:

- C David 122

- S Leeming 116

- C Lyons 87

Bank balance as per cash book 214

CLIENT 4

1. Sales Ledger Control Account in the books of January 2018:

Sales Ledger Control A/c

Particulars Amount

(£)

Particulars Amount

(£)

Balance b/d... 12600 Sales Return............. 4320

amount 9 Bank charges 47

Standing order 137

310923 (DirectD) 297

Balance c/f 19,500

19,982 19,982

Balance b/d 19,500

Particulars Amount

- Bank Balance as per pass book 398

Add: Items having effects of higher balance in cash

book

- Bank charges not recorded in cashbook... 36

- Adjustment for direct debit rates.............. 105

Less: Items having effects of lower balance in cash

book

Payments to:

- C David 122

- S Leeming 116

- C Lyons 87

Bank balance as per cash book 214

CLIENT 4

1. Sales Ledger Control Account in the books of January 2018:

Sales Ledger Control A/c

Particulars Amount

(£)

Particulars Amount

(£)

Balance b/d... 12600 Sales Return............. 4320

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Credit Sales............. 152350 Bad Debts.................. 1600

Discount Allowed............. 1060

Bank/ Cash (Receipt from credit

customers)..................

120610

Set-off (Transfer to purchase

ledger).............

640

Balance c/d................. 36720

Total 164950 Total 164950

Balance b/d 36720

2. Purchase Ledger Control Account in the books of January 2018:

Purchase Ledger Control A/c

Particulars Amount

(£)

Particulars Amount

(£)

Discount Received... 850 Balance b/d............ 11360

Purchase Return.......... 3110 Credit Purchase................... 126500

Bank/ Cash (Payment to

suppliers)..............

91010 Bank (Refund from supplier)............. 500

Set-off (Transfer from sales

ledger)............

640

Balance c/d.......... 42750

Total 138360 Total 138360

Balance b/d 42750

3. Control Account:

A control account is general ledger account that exhibits total amount of balance of

related subsidiary ledgers accounts. Main purpose of control account is to keep all general

ledgers free of any complex headings or details and still to provide accurate balance for

preparing final accounts (Oulasvirta, 2014).

Discount Allowed............. 1060

Bank/ Cash (Receipt from credit

customers)..................

120610

Set-off (Transfer to purchase

ledger).............

640

Balance c/d................. 36720

Total 164950 Total 164950

Balance b/d 36720

2. Purchase Ledger Control Account in the books of January 2018:

Purchase Ledger Control A/c

Particulars Amount

(£)

Particulars Amount

(£)

Discount Received... 850 Balance b/d............ 11360

Purchase Return.......... 3110 Credit Purchase................... 126500

Bank/ Cash (Payment to

suppliers)..............

91010 Bank (Refund from supplier)............. 500

Set-off (Transfer from sales

ledger)............

640

Balance c/d.......... 42750

Total 138360 Total 138360

Balance b/d 42750

3. Control Account:

A control account is general ledger account that exhibits total amount of balance of

related subsidiary ledgers accounts. Main purpose of control account is to keep all general

ledgers free of any complex headings or details and still to provide accurate balance for

preparing final accounts (Oulasvirta, 2014).

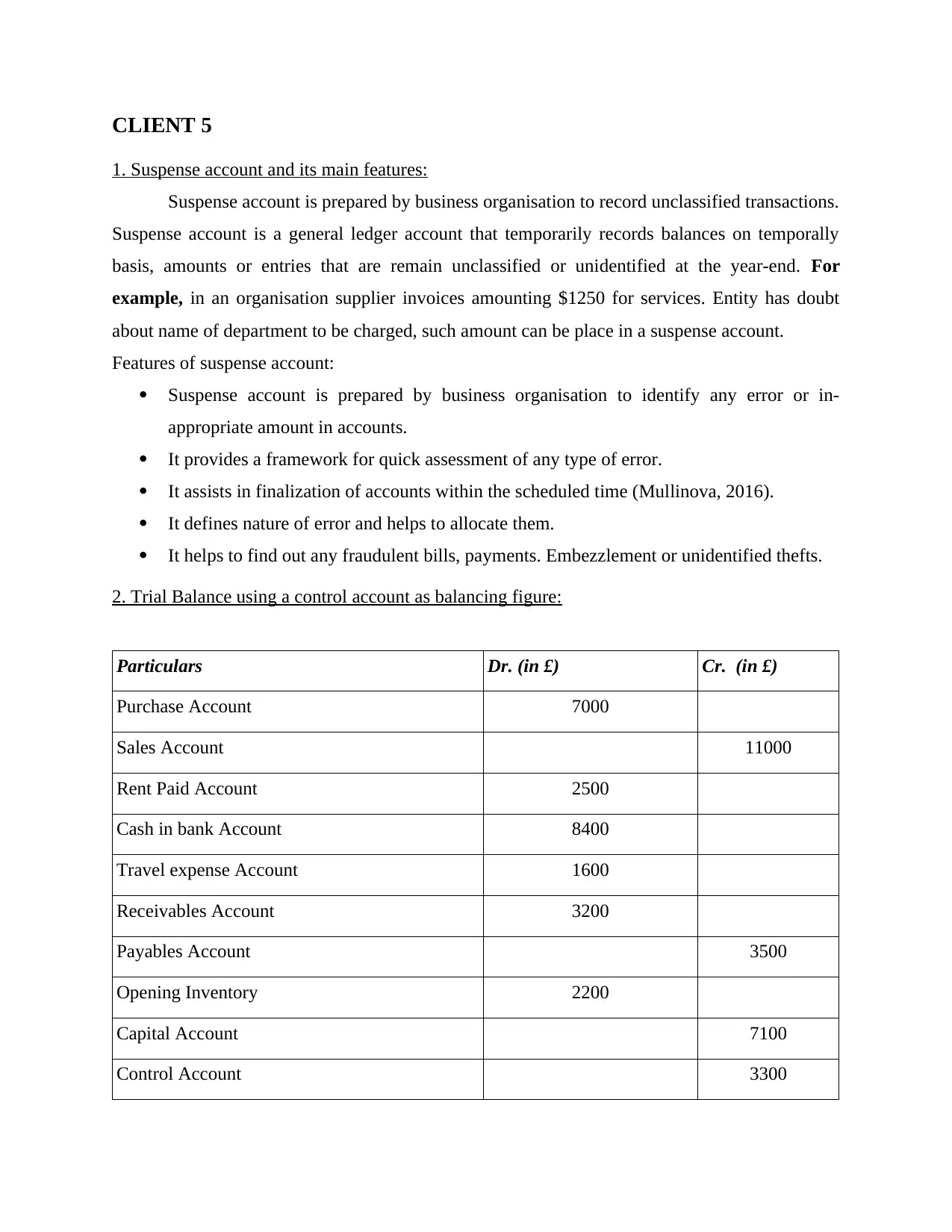

CLIENT 5

1. Suspense account and its main features:

Suspense account is prepared by business organisation to record unclassified transactions.

Suspense account is a general ledger account that temporarily records balances on temporally

basis, amounts or entries that are remain unclassified or unidentified at the year-end. For

example, in an organisation supplier invoices amounting $1250 for services. Entity has doubt

about name of department to be charged, such amount can be place in a suspense account.

Features of suspense account:

Suspense account is prepared by business organisation to identify any error or in-

appropriate amount in accounts.

It provides a framework for quick assessment of any type of error.

It assists in finalization of accounts within the scheduled time (Mullinova, 2016).

It defines nature of error and helps to allocate them.

It helps to find out any fraudulent bills, payments. Embezzlement or unidentified thefts.

2. Trial Balance using a control account as balancing figure:

Particulars Dr. (in £) Cr. (in £)

Purchase Account 7000

Sales Account 11000

Rent Paid Account 2500

Cash in bank Account 8400

Travel expense Account 1600

Receivables Account 3200

Payables Account 3500

Opening Inventory 2200

Capital Account 7100

Control Account 3300

1. Suspense account and its main features:

Suspense account is prepared by business organisation to record unclassified transactions.

Suspense account is a general ledger account that temporarily records balances on temporally

basis, amounts or entries that are remain unclassified or unidentified at the year-end. For

example, in an organisation supplier invoices amounting $1250 for services. Entity has doubt

about name of department to be charged, such amount can be place in a suspense account.

Features of suspense account:

Suspense account is prepared by business organisation to identify any error or in-

appropriate amount in accounts.

It provides a framework for quick assessment of any type of error.

It assists in finalization of accounts within the scheduled time (Mullinova, 2016).

It defines nature of error and helps to allocate them.

It helps to find out any fraudulent bills, payments. Embezzlement or unidentified thefts.

2. Trial Balance using a control account as balancing figure:

Particulars Dr. (in £) Cr. (in £)

Purchase Account 7000

Sales Account 11000

Rent Paid Account 2500

Cash in bank Account 8400

Travel expense Account 1600

Receivables Account 3200

Payables Account 3500

Opening Inventory 2200

Capital Account 7100

Control Account 3300

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.