Accounting Techniques and Principles

VerifiedAdded on 2020/11/12

|30

|4105

|187

AI Summary

The provided document is a detailed report on accounting techniques and principles. It includes a comprehensive analysis of financial statements such as balance sheets, trial balances, and income statements for different clients. The report also delves into the concepts of suspense accounts and clearing accounts, highlighting their similarities and differences. The document provides references to relevant books and journals, as well as online resources for further learning.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL

ACCOUNTING

PRINCIPLES

ACCOUNTING

PRINCIPLES

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A. The accounting regulations has been reported for organization to the Line manager...........1

1. Explaining Financial Accounting............................................................................................1

2. Regulations of financial accounting .......................................................................................2

3. Accounting rules and principles..............................................................................................3

4. Conventions and concepts with respect to consistency and material disclosures...................3

CLIENT 1........................................................................................................................................5

1. Drafting the journal for Client 1 for the date 1st May 2017...................................................5

2. Presenting the ledger accounts of all Journal entries..............................................................7

..........................................................................................................................................................8

3. The trial balance of client 1...................................................................................................16

CLIENT 2......................................................................................................................................17

A. Peter piper's profit and loss statement for the year ended 31st December 2017..................17

B. Peter piper's Balance sheet for the year ended 31st December 2017...................................17

Client 3...........................................................................................................................................19

A. Rain tree ltd's profit and loss statement for the year ended 30th September 2017..............19

B Raintree Limited Financial position......................................................................................20

C. Identifying different concepts and principles of accounting principles...............................25

C. Significance of measuring and representing depreciation with context of business giving

brief about both methods of business........................................................................................26

CLIENT 4......................................................................................................................................26

A. Aim for framing bank statement .........................................................................................26

B. Identifying the reasons for recording in bank statements.....................................................27

C. Client's cash book ................................................................................................................27

CLIENT 5......................................................................................................................................28

Forming Sales ledger control account and purchase ledger control account for the year 2017

(May) of Henderson..................................................................................................................28

B. Defining the term Control account.......................................................................................28

CLIENT 6......................................................................................................................................29

INTRODUCTION...........................................................................................................................1

A. The accounting regulations has been reported for organization to the Line manager...........1

1. Explaining Financial Accounting............................................................................................1

2. Regulations of financial accounting .......................................................................................2

3. Accounting rules and principles..............................................................................................3

4. Conventions and concepts with respect to consistency and material disclosures...................3

CLIENT 1........................................................................................................................................5

1. Drafting the journal for Client 1 for the date 1st May 2017...................................................5

2. Presenting the ledger accounts of all Journal entries..............................................................7

..........................................................................................................................................................8

3. The trial balance of client 1...................................................................................................16

CLIENT 2......................................................................................................................................17

A. Peter piper's profit and loss statement for the year ended 31st December 2017..................17

B. Peter piper's Balance sheet for the year ended 31st December 2017...................................17

Client 3...........................................................................................................................................19

A. Rain tree ltd's profit and loss statement for the year ended 30th September 2017..............19

B Raintree Limited Financial position......................................................................................20

C. Identifying different concepts and principles of accounting principles...............................25

C. Significance of measuring and representing depreciation with context of business giving

brief about both methods of business........................................................................................26

CLIENT 4......................................................................................................................................26

A. Aim for framing bank statement .........................................................................................26

B. Identifying the reasons for recording in bank statements.....................................................27

C. Client's cash book ................................................................................................................27

CLIENT 5......................................................................................................................................28

Forming Sales ledger control account and purchase ledger control account for the year 2017

(May) of Henderson..................................................................................................................28

B. Defining the term Control account.......................................................................................28

CLIENT 6......................................................................................................................................29

A. Suspense account with its characteristics.............................................................................29

B. Preparing trial balance..........................................................................................................29

C. Journal entries.......................................................................................................................30

D. Difference between Clearing account and Suspense accountant.........................................30

CONCLUSION..............................................................................................................................30

REFERENCES..............................................................................................................................31

B. Preparing trial balance..........................................................................................................29

C. Journal entries.......................................................................................................................30

D. Difference between Clearing account and Suspense accountant.........................................30

CONCLUSION..............................................................................................................................30

REFERENCES..............................................................................................................................31

INTRODUCTION

Financial accounting is considered as very important and essential element of each and

every company. In the present era, different accounting principles, rules and regulations are

followed by every industry and it will be giving great advantage to that specific industry. It gives

brief analysis of funds which are required for performing the various activities related to

business. The present report will be giving brief discussion about different financial regulations,

principles and basic rules for accounting. Further there are six clients which helps in describing

different financial statements such as balance sheet, profit and loss statement, cash flow

statements and so on. There is proper analysis of transactions of purchase and sale for compiling

in trial balance. The clients are giving details about bank reconciliation statement, sales and

purchase ledger account and even there is discussion about suspense account.

A. The accounting regulations has been reported for organization to the Line manager

To: Line Manager

From: Junior Accountant

Subject: Implying the terminology of accounting along with the awareness which is relevant for

regulations of accounting.

Respected Sir,

For improving the activities of transactions which are related to business, there is huge

requirement of analysing the rules, regulations, usage and method of applying different

accounting principles. The operations of the business can be improved by different accounting

techniques and it will directly lead to improve transactional activities. There are different

applications of accounting techniques and its outcome will be very beneficial for allocating

cost, budgeting and forecasting different operational tasks related to the organization or

business.

1. Explaining Financial Accounting

Financial accounting is referred as the most specialized accounting branch which traces

the financial transactions of organization. By using the guidelines which are standards, all the

transactions are summarized, recorded and represented in financial statement or report like

balance or income statement (Hepworth, 2017). The financial statements are issued by company

on daily schedule.

1

Financial accounting is considered as very important and essential element of each and

every company. In the present era, different accounting principles, rules and regulations are

followed by every industry and it will be giving great advantage to that specific industry. It gives

brief analysis of funds which are required for performing the various activities related to

business. The present report will be giving brief discussion about different financial regulations,

principles and basic rules for accounting. Further there are six clients which helps in describing

different financial statements such as balance sheet, profit and loss statement, cash flow

statements and so on. There is proper analysis of transactions of purchase and sale for compiling

in trial balance. The clients are giving details about bank reconciliation statement, sales and

purchase ledger account and even there is discussion about suspense account.

A. The accounting regulations has been reported for organization to the Line manager

To: Line Manager

From: Junior Accountant

Subject: Implying the terminology of accounting along with the awareness which is relevant for

regulations of accounting.

Respected Sir,

For improving the activities of transactions which are related to business, there is huge

requirement of analysing the rules, regulations, usage and method of applying different

accounting principles. The operations of the business can be improved by different accounting

techniques and it will directly lead to improve transactional activities. There are different

applications of accounting techniques and its outcome will be very beneficial for allocating

cost, budgeting and forecasting different operational tasks related to the organization or

business.

1. Explaining Financial Accounting

Financial accounting is referred as the most specialized accounting branch which traces

the financial transactions of organization. By using the guidelines which are standards, all the

transactions are summarized, recorded and represented in financial statement or report like

balance or income statement (Hepworth, 2017). The financial statements are issued by company

on daily schedule.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

There are various types of financial statements which are established for general

objective which are as follows:

Balance sheet

Income statements

Statement of stockholder's equity-trusts-formalities

Statement of cash flows

All the statements are considered as external due to reason that it is used by the persons

who are considered as outsiders. Along with this, all stock holders and even lenders. If the stock

of corporation is traded publicly, then its all financial statements will be circulated and its

information will be with various secondary recipients like investment analysts, customers,

labour organization, employees and competitors. It is very essential to obtain the objective of

financial accounting is not to form the valuation of any of organization. As its main objective is

to give information to others for analysing the valuation of organizations for themselves only.

2. Regulations of financial accounting

Financial accounting consists of different rules and regulations which will be beneficial

for giving a legal framework of accounting. There has been corporate reporting of UK and its

own government regulator as Financial Reporting Council (FRC). It will be giving different

disclosure of financial reporting of all units, government departments and different corporates

(Dung, 2016). In the same series, there are different regulations which are accepted as universal

legal framework like:

IFRS: The information which has been stated by IFRS standards give relevant

framework and forms disclosure of all financial statements which help the organization for

attracting a large number of investors and it will be giving benefit for estimating costs and for

relevant expenses which are caused by operational activities.

FRC: This regulation of financial accounting has been set up by different corporations

of UK by considering accounting standard which are framed for monitoring and executing all

the disclosures related to finance for promoting governance of very high quality.

IASB : The main objective of IASB is to provide adequate information to all the

accounting professionals and guidelines with the perspective of drafting database of financial

and even for providing specific disclosure of all accounts. There has been set up of legal

2

objective which are as follows:

Balance sheet

Income statements

Statement of stockholder's equity-trusts-formalities

Statement of cash flows

All the statements are considered as external due to reason that it is used by the persons

who are considered as outsiders. Along with this, all stock holders and even lenders. If the stock

of corporation is traded publicly, then its all financial statements will be circulated and its

information will be with various secondary recipients like investment analysts, customers,

labour organization, employees and competitors. It is very essential to obtain the objective of

financial accounting is not to form the valuation of any of organization. As its main objective is

to give information to others for analysing the valuation of organizations for themselves only.

2. Regulations of financial accounting

Financial accounting consists of different rules and regulations which will be beneficial

for giving a legal framework of accounting. There has been corporate reporting of UK and its

own government regulator as Financial Reporting Council (FRC). It will be giving different

disclosure of financial reporting of all units, government departments and different corporates

(Dung, 2016). In the same series, there are different regulations which are accepted as universal

legal framework like:

IFRS: The information which has been stated by IFRS standards give relevant

framework and forms disclosure of all financial statements which help the organization for

attracting a large number of investors and it will be giving benefit for estimating costs and for

relevant expenses which are caused by operational activities.

FRC: This regulation of financial accounting has been set up by different corporations

of UK by considering accounting standard which are framed for monitoring and executing all

the disclosures related to finance for promoting governance of very high quality.

IASB : The main objective of IASB is to provide adequate information to all the

accounting professionals and guidelines with the perspective of drafting database of financial

and even for providing specific disclosure of all accounts. There has been set up of legal

2

framework for financial disclosure which is accepted by every one in the world and it also leads

to attract all the investors who are operating internationally.

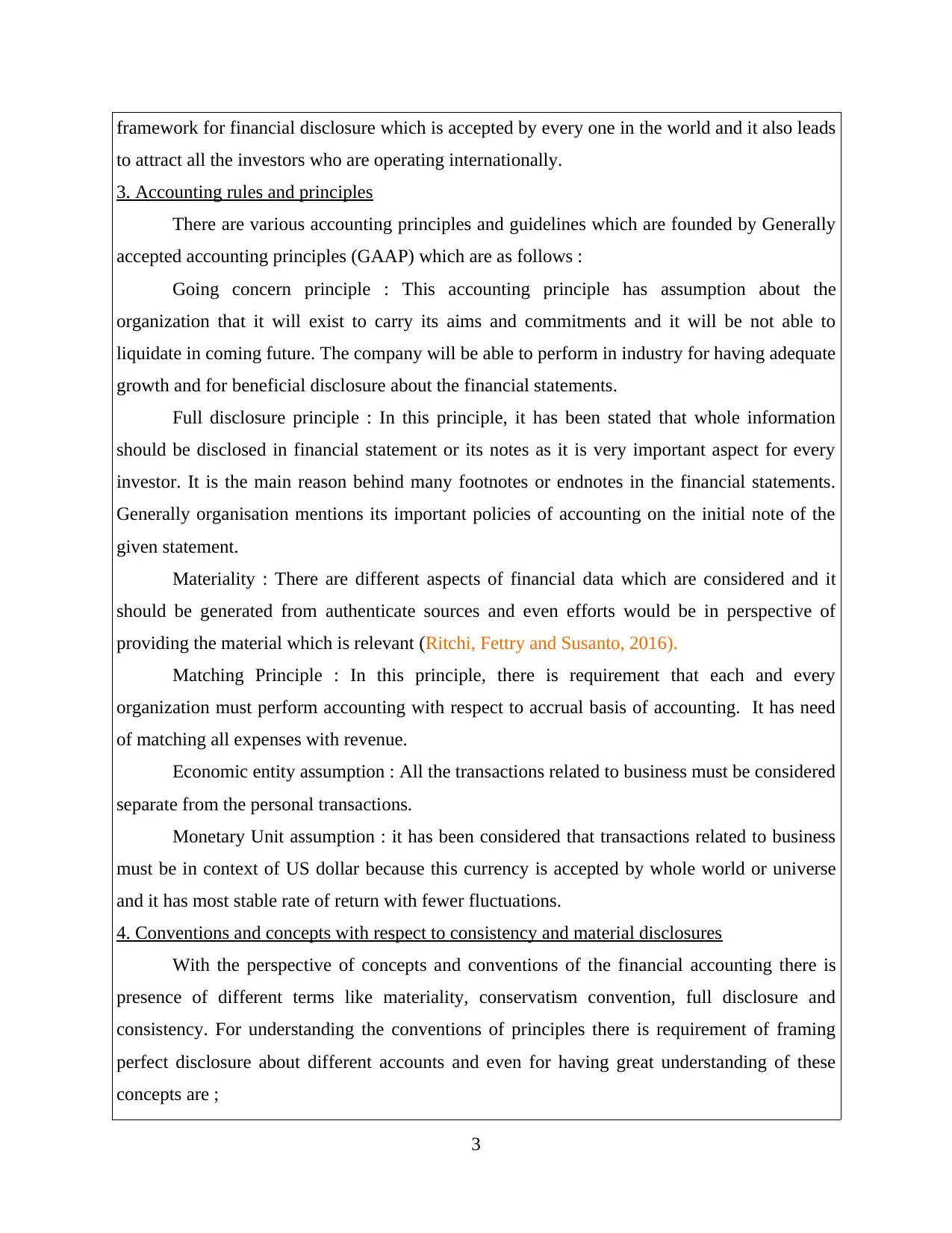

3. Accounting rules and principles

There are various accounting principles and guidelines which are founded by Generally

accepted accounting principles (GAAP) which are as follows :

Going concern principle : This accounting principle has assumption about the

organization that it will exist to carry its aims and commitments and it will be not able to

liquidate in coming future. The company will be able to perform in industry for having adequate

growth and for beneficial disclosure about the financial statements.

Full disclosure principle : In this principle, it has been stated that whole information

should be disclosed in financial statement or its notes as it is very important aspect for every

investor. It is the main reason behind many footnotes or endnotes in the financial statements.

Generally organisation mentions its important policies of accounting on the initial note of the

given statement.

Materiality : There are different aspects of financial data which are considered and it

should be generated from authenticate sources and even efforts would be in perspective of

providing the material which is relevant (Ritchi, Fettry and Susanto, 2016).

Matching Principle : In this principle, there is requirement that each and every

organization must perform accounting with respect to accrual basis of accounting. It has need

of matching all expenses with revenue.

Economic entity assumption : All the transactions related to business must be considered

separate from the personal transactions.

Monetary Unit assumption : it has been considered that transactions related to business

must be in context of US dollar because this currency is accepted by whole world or universe

and it has most stable rate of return with fewer fluctuations.

4. Conventions and concepts with respect to consistency and material disclosures

With the perspective of concepts and conventions of the financial accounting there is

presence of different terms like materiality, conservatism convention, full disclosure and

consistency. For understanding the conventions of principles there is requirement of framing

perfect disclosure about different accounts and even for having great understanding of these

concepts are ;

3

to attract all the investors who are operating internationally.

3. Accounting rules and principles

There are various accounting principles and guidelines which are founded by Generally

accepted accounting principles (GAAP) which are as follows :

Going concern principle : This accounting principle has assumption about the

organization that it will exist to carry its aims and commitments and it will be not able to

liquidate in coming future. The company will be able to perform in industry for having adequate

growth and for beneficial disclosure about the financial statements.

Full disclosure principle : In this principle, it has been stated that whole information

should be disclosed in financial statement or its notes as it is very important aspect for every

investor. It is the main reason behind many footnotes or endnotes in the financial statements.

Generally organisation mentions its important policies of accounting on the initial note of the

given statement.

Materiality : There are different aspects of financial data which are considered and it

should be generated from authenticate sources and even efforts would be in perspective of

providing the material which is relevant (Ritchi, Fettry and Susanto, 2016).

Matching Principle : In this principle, there is requirement that each and every

organization must perform accounting with respect to accrual basis of accounting. It has need

of matching all expenses with revenue.

Economic entity assumption : All the transactions related to business must be considered

separate from the personal transactions.

Monetary Unit assumption : it has been considered that transactions related to business

must be in context of US dollar because this currency is accepted by whole world or universe

and it has most stable rate of return with fewer fluctuations.

4. Conventions and concepts with respect to consistency and material disclosures

With the perspective of concepts and conventions of the financial accounting there is

presence of different terms like materiality, conservatism convention, full disclosure and

consistency. For understanding the conventions of principles there is requirement of framing

perfect disclosure about different accounts and even for having great understanding of these

concepts are ;

3

Material disclosure : There is requirement of disclosing different financial accounts

which includes different material like objects which are required for keeping record of business

professionals by analysing the efficiency and profitability of the organization for accomplishing

the set targets and objectives (Trucco, 2015).

Consistency : In this principle the nature of the organization has been followed and even

trade practices have been formed in market. All the operations related to business will consiste

of perfect consistency and to have great benefit in terms of profit. This principle will lead to

generate more profit and gathering all the returns for long term and giving it back to managers

by providing outcomes which are operational and adequate as well.

4

which includes different material like objects which are required for keeping record of business

professionals by analysing the efficiency and profitability of the organization for accomplishing

the set targets and objectives (Trucco, 2015).

Consistency : In this principle the nature of the organization has been followed and even

trade practices have been formed in market. All the operations related to business will consiste

of perfect consistency and to have great benefit in terms of profit. This principle will lead to

generate more profit and gathering all the returns for long term and giving it back to managers

by providing outcomes which are operational and adequate as well.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

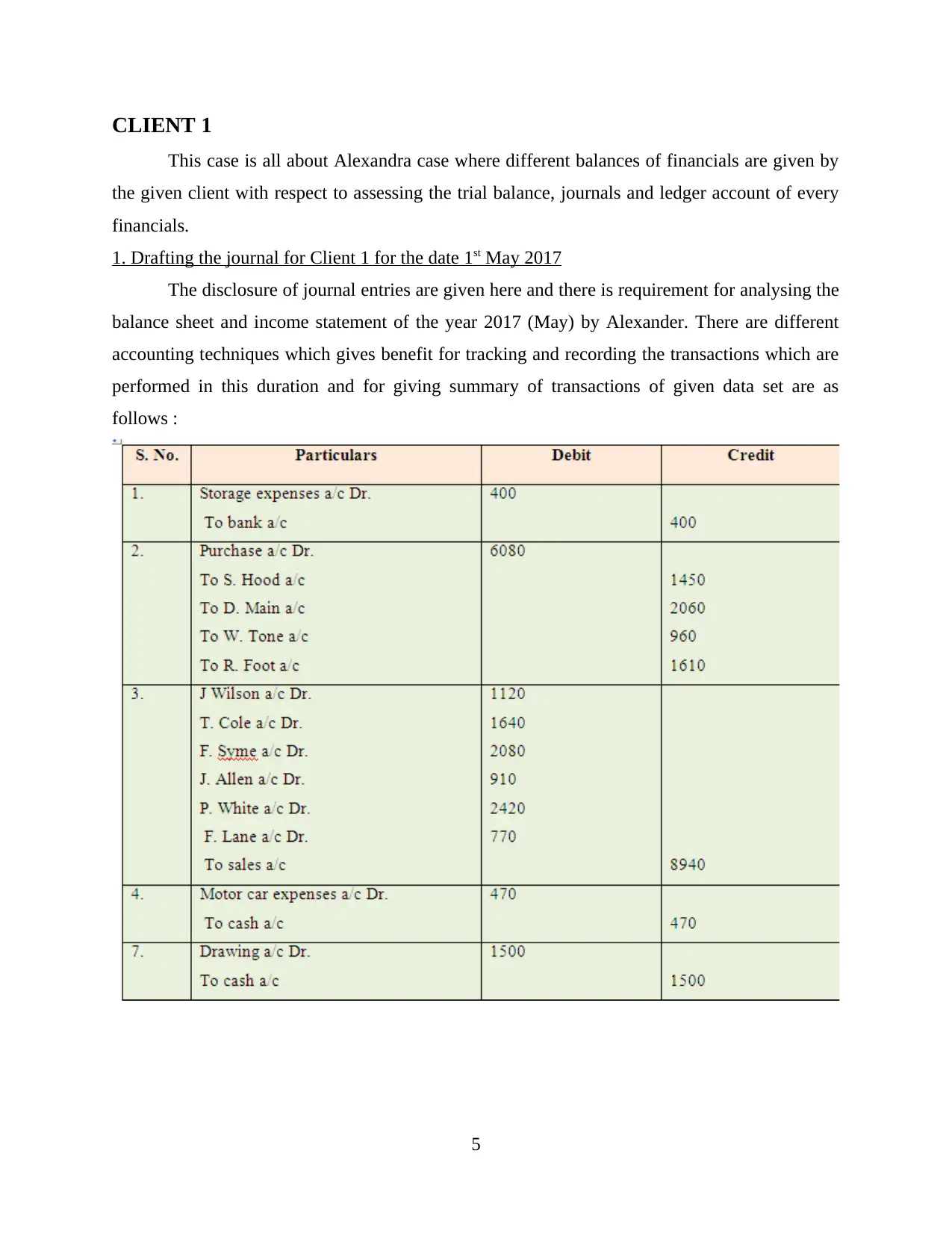

CLIENT 1

This case is all about Alexandra case where different balances of financials are given by

the given client with respect to assessing the trial balance, journals and ledger account of every

financials.

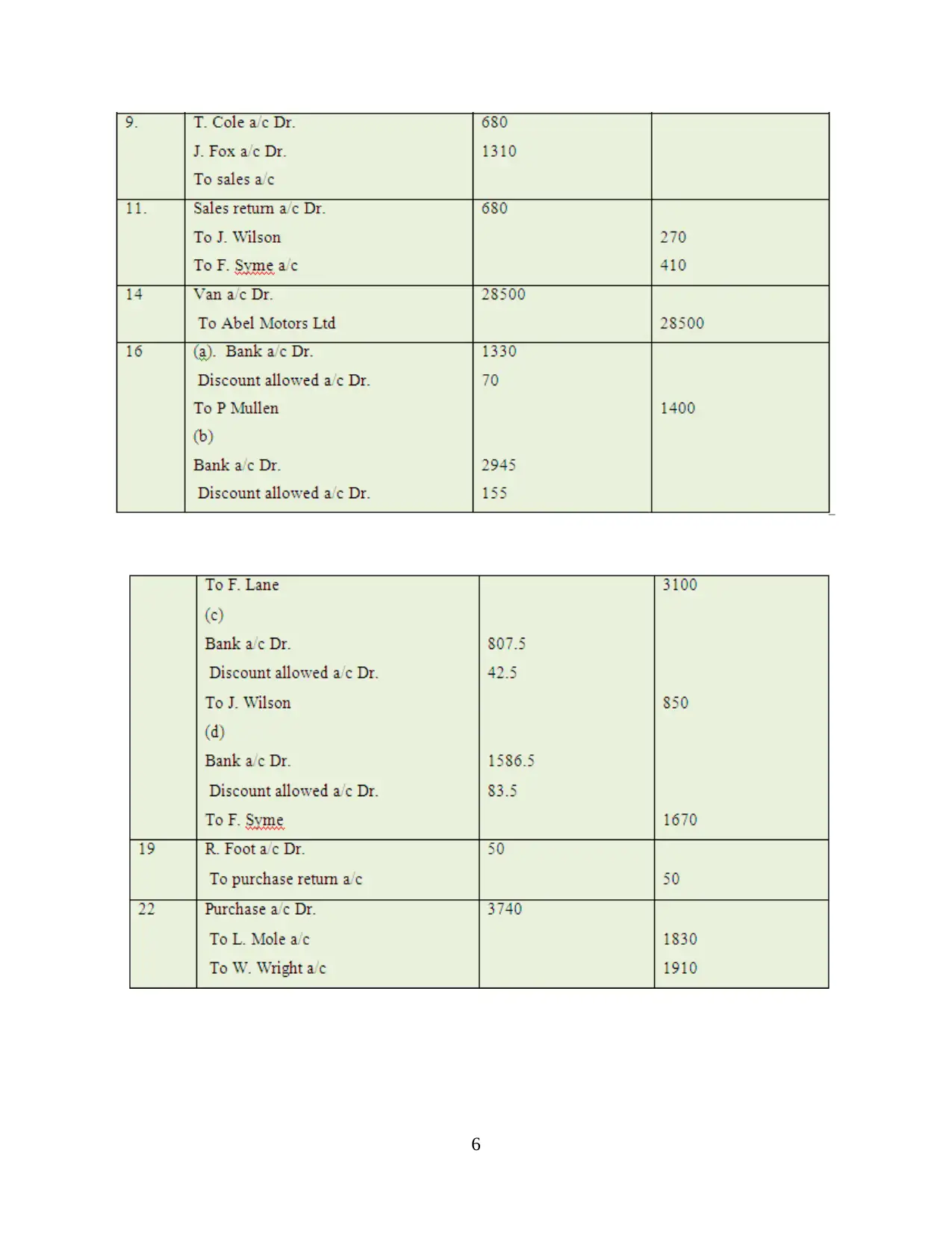

1. Drafting the journal for Client 1 for the date 1st May 2017

The disclosure of journal entries are given here and there is requirement for analysing the

balance sheet and income statement of the year 2017 (May) by Alexander. There are different

accounting techniques which gives benefit for tracking and recording the transactions which are

performed in this duration and for giving summary of transactions of given data set are as

follows :

5

This case is all about Alexandra case where different balances of financials are given by

the given client with respect to assessing the trial balance, journals and ledger account of every

financials.

1. Drafting the journal for Client 1 for the date 1st May 2017

The disclosure of journal entries are given here and there is requirement for analysing the

balance sheet and income statement of the year 2017 (May) by Alexander. There are different

accounting techniques which gives benefit for tracking and recording the transactions which are

performed in this duration and for giving summary of transactions of given data set are as

follows :

5

6

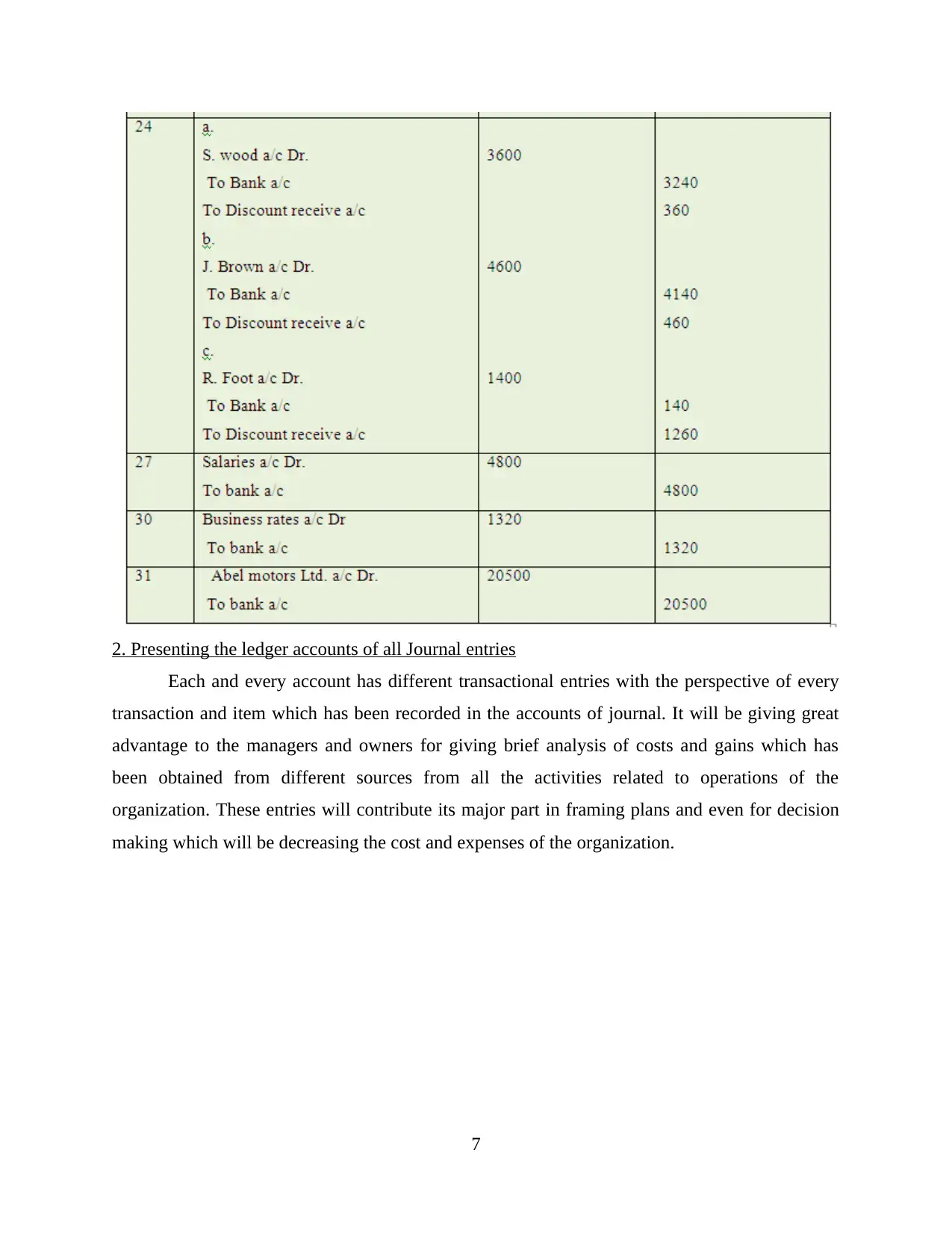

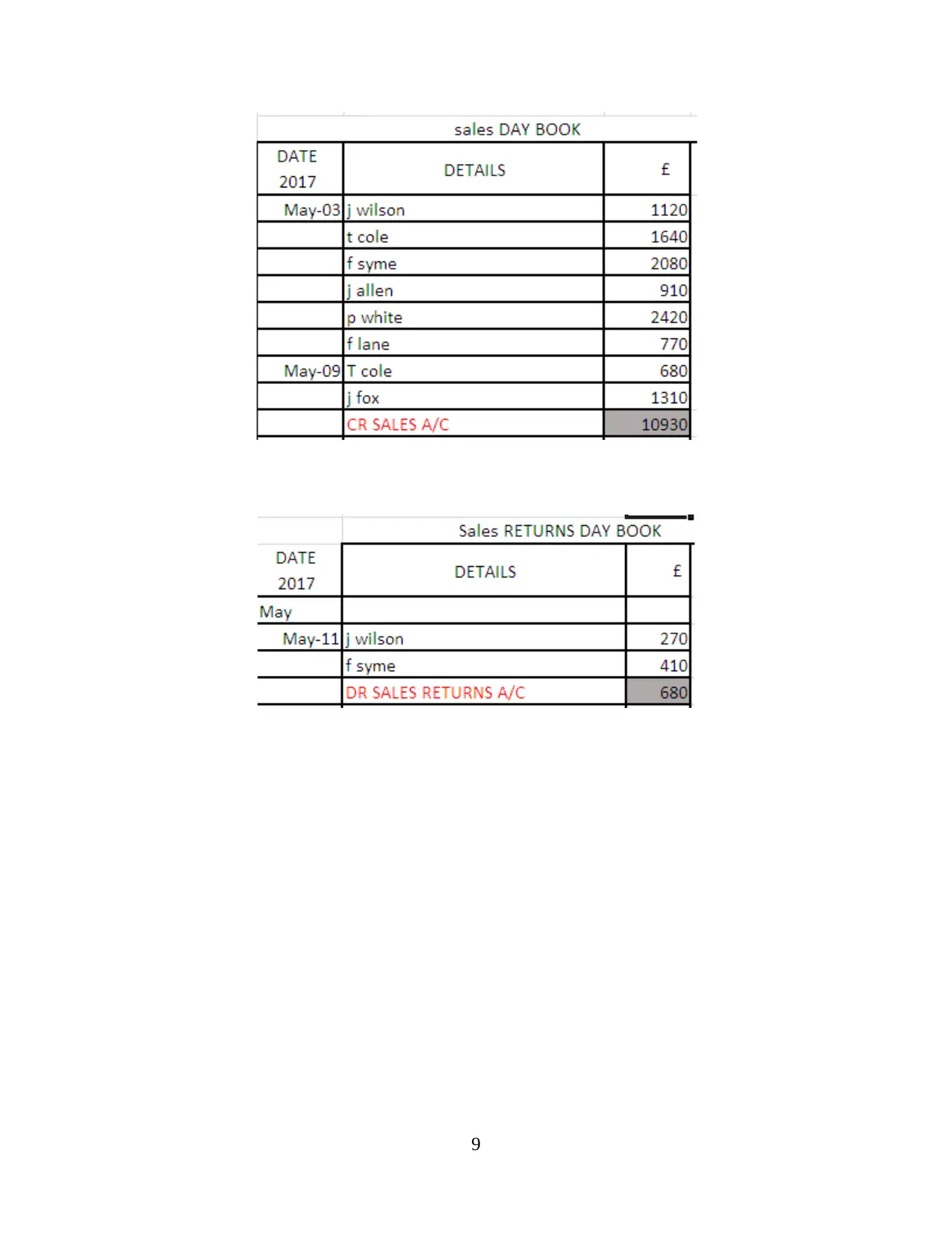

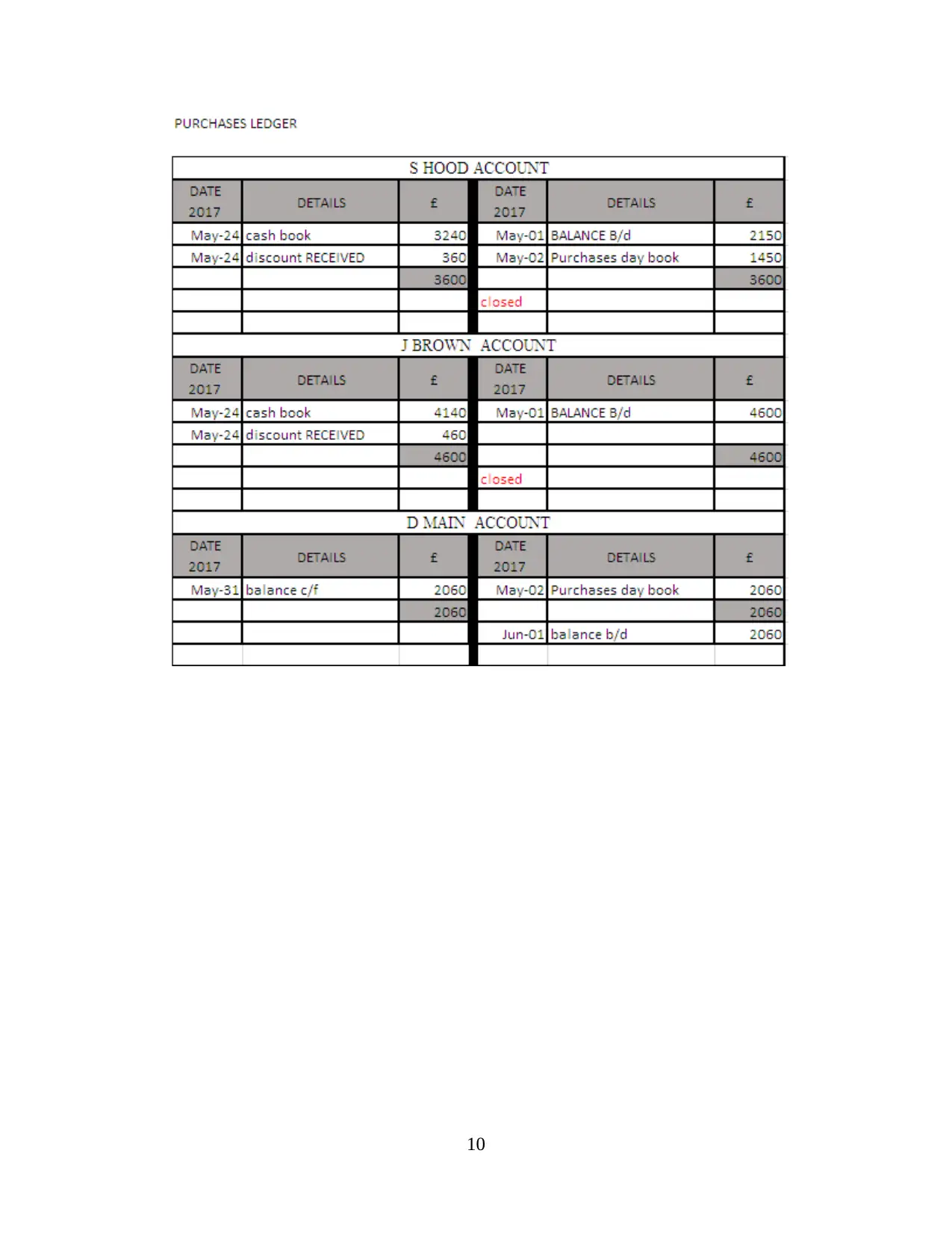

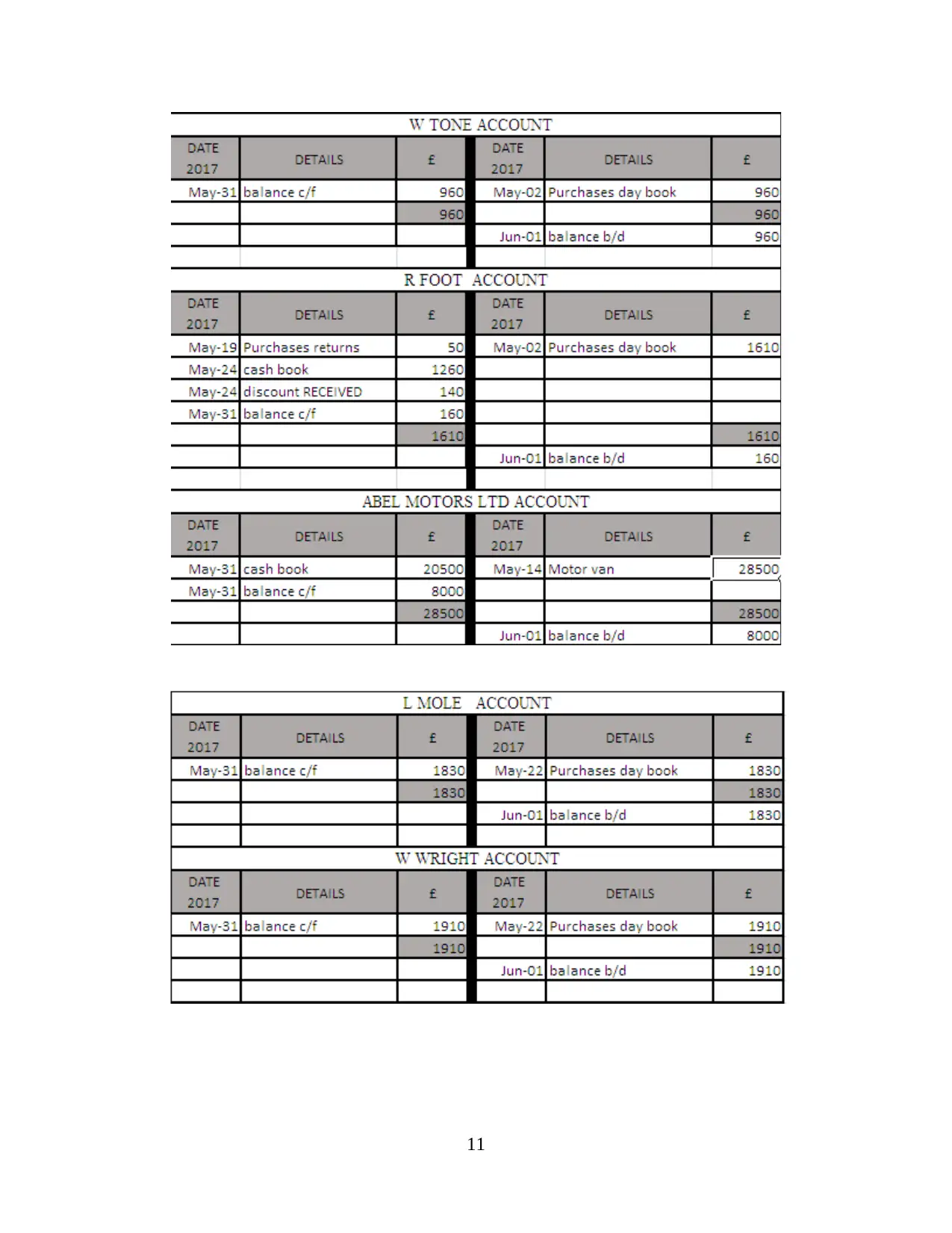

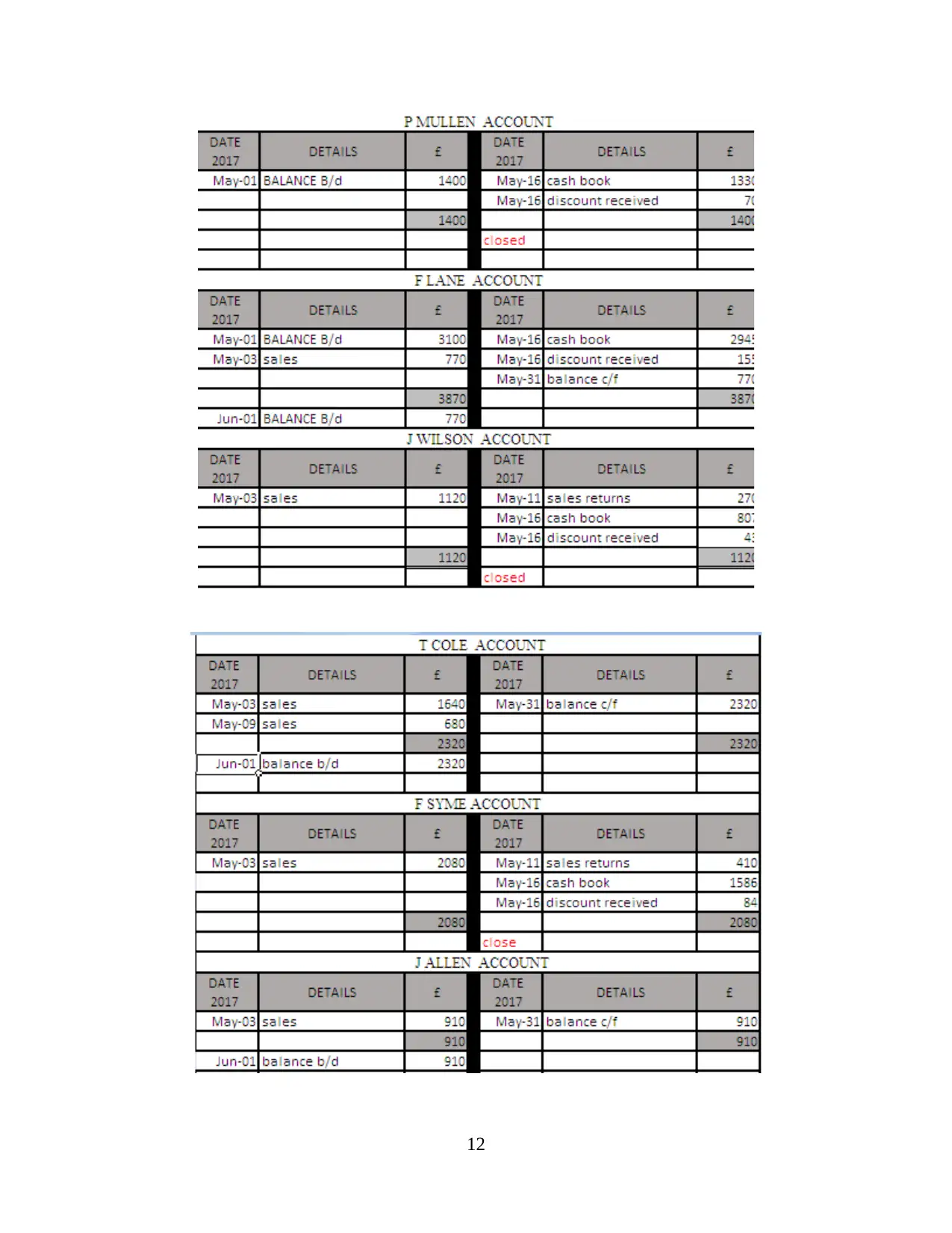

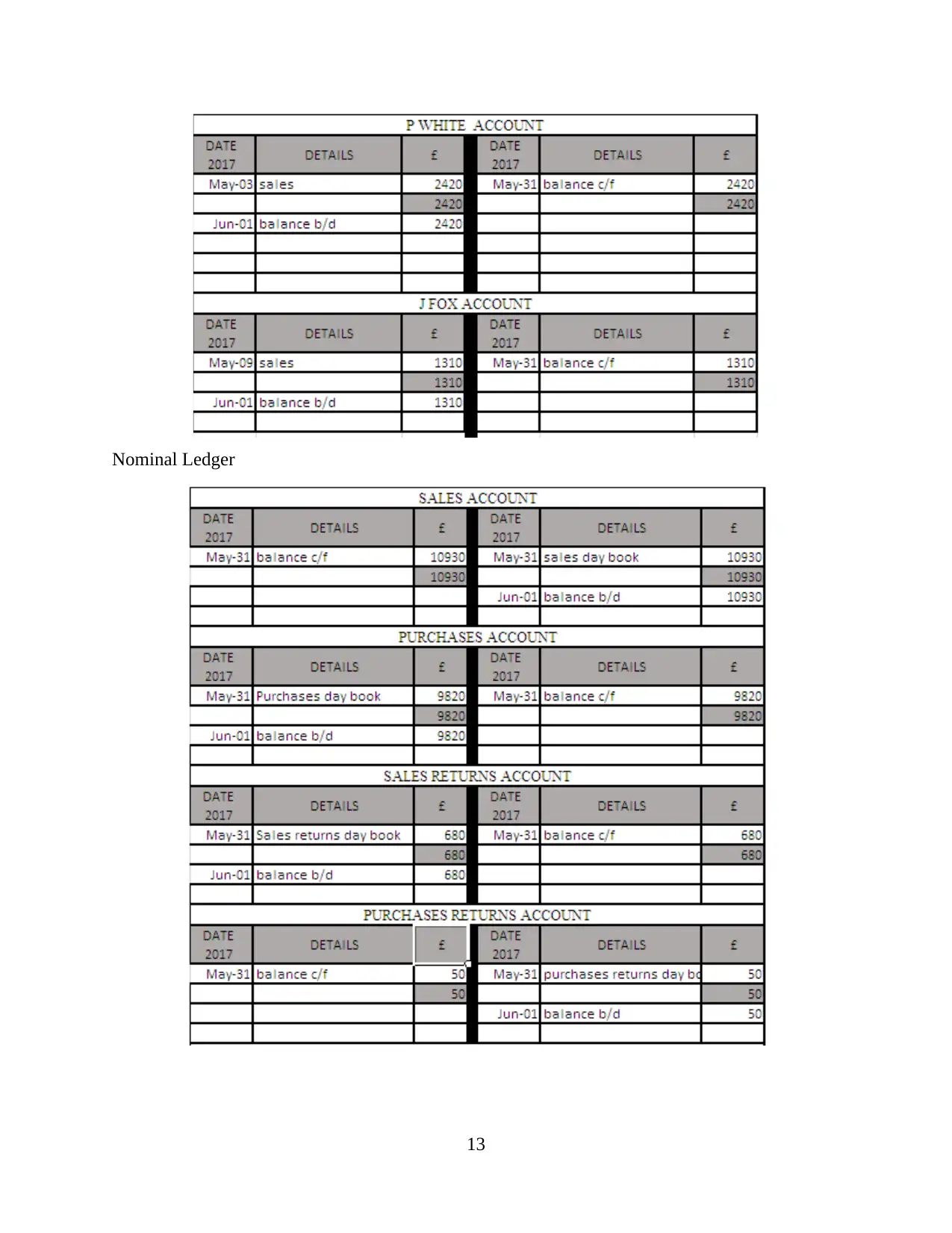

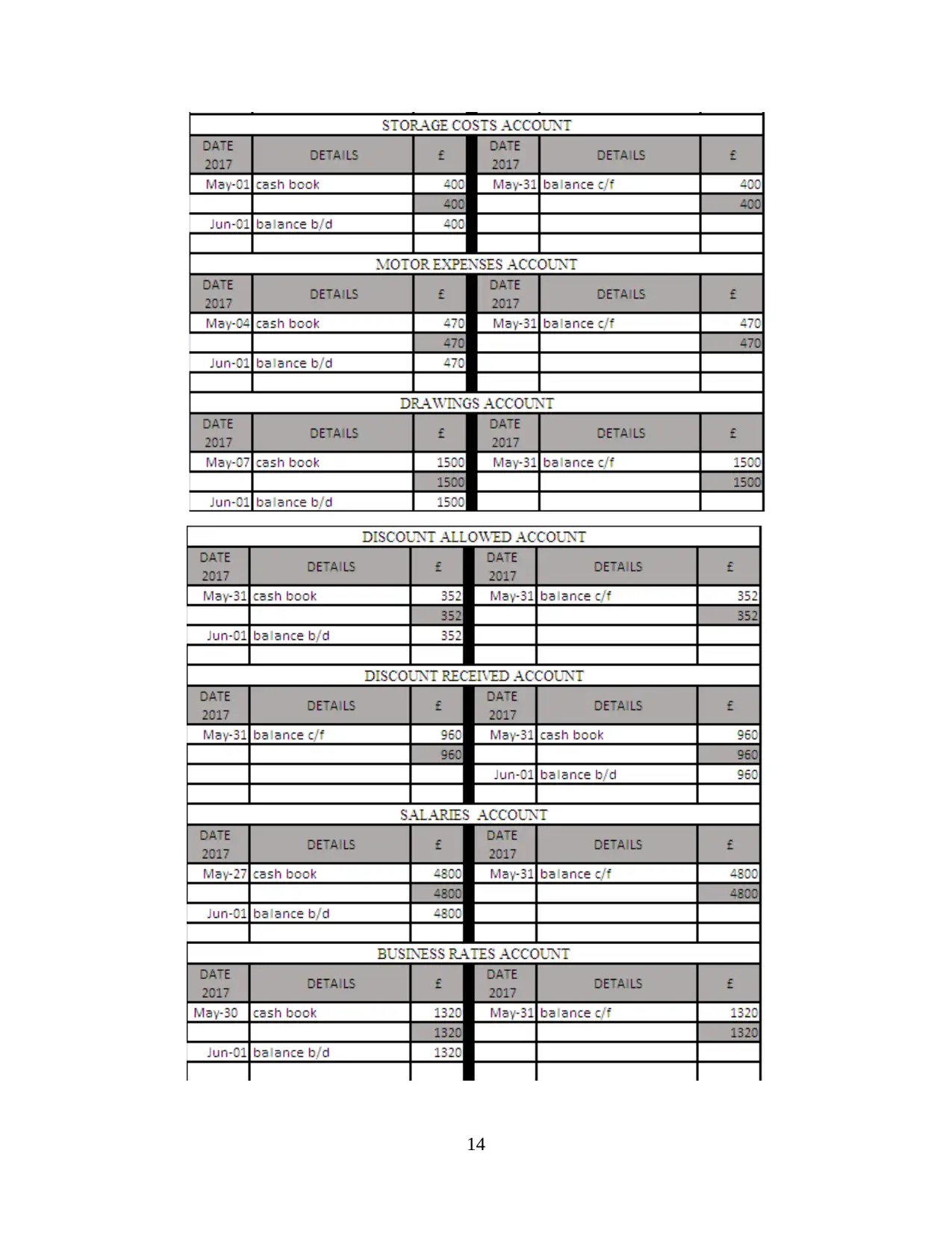

2. Presenting the ledger accounts of all Journal entries

Each and every account has different transactional entries with the perspective of every

transaction and item which has been recorded in the accounts of journal. It will be giving great

advantage to the managers and owners for giving brief analysis of costs and gains which has

been obtained from different sources from all the activities related to operations of the

organization. These entries will contribute its major part in framing plans and even for decision

making which will be decreasing the cost and expenses of the organization.

7

Each and every account has different transactional entries with the perspective of every

transaction and item which has been recorded in the accounts of journal. It will be giving great

advantage to the managers and owners for giving brief analysis of costs and gains which has

been obtained from different sources from all the activities related to operations of the

organization. These entries will contribute its major part in framing plans and even for decision

making which will be decreasing the cost and expenses of the organization.

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

8

9

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

12

Nominal Ledger

13

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

14

Real Ledger accounts

15

15

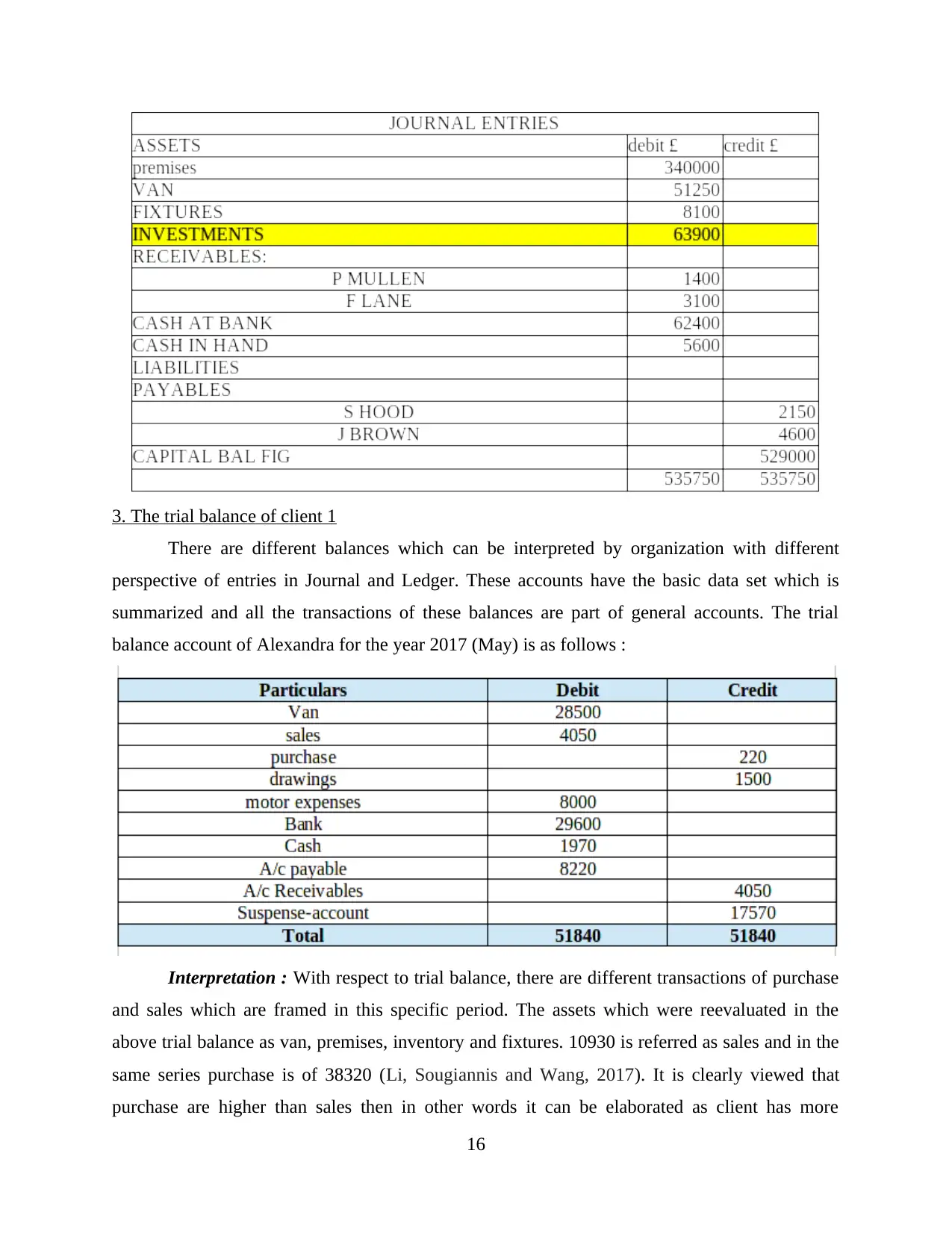

3. The trial balance of client 1

There are different balances which can be interpreted by organization with different

perspective of entries in Journal and Ledger. These accounts have the basic data set which is

summarized and all the transactions of these balances are part of general accounts. The trial

balance account of Alexandra for the year 2017 (May) is as follows :

Interpretation : With respect to trial balance, there are different transactions of purchase

and sales which are framed in this specific period. The assets which were reevaluated in the

above trial balance as van, premises, inventory and fixtures. 10930 is referred as sales and in the

same series purchase is of 38320 (Li, Sougiannis and Wang, 2017). It is clearly viewed that

purchase are higher than sales then in other words it can be elaborated as client has more

16

There are different balances which can be interpreted by organization with different

perspective of entries in Journal and Ledger. These accounts have the basic data set which is

summarized and all the transactions of these balances are part of general accounts. The trial

balance account of Alexandra for the year 2017 (May) is as follows :

Interpretation : With respect to trial balance, there are different transactions of purchase

and sales which are framed in this specific period. The assets which were reevaluated in the

above trial balance as van, premises, inventory and fixtures. 10930 is referred as sales and in the

same series purchase is of 38320 (Li, Sougiannis and Wang, 2017). It is clearly viewed that

purchase are higher than sales then in other words it can be elaborated as client has more

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenses as compare to income. The accounting principles which are directly issued by different

boards and institutions with the context of trial balance which is framed. The transactions are

recorded under the basic framework and format of the trial balance is given by different

principles and concepts of IASB, IFRS and GAAP.

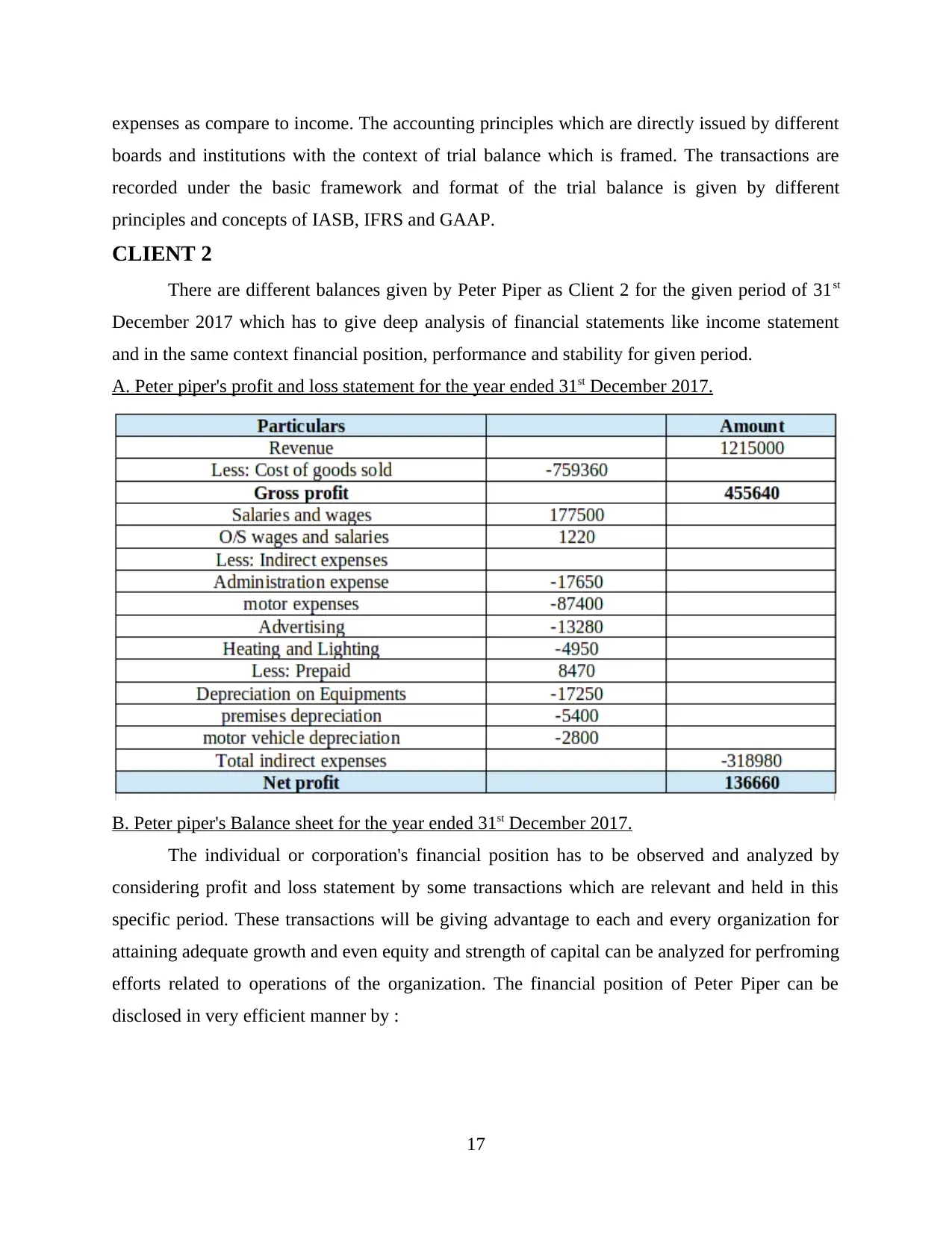

CLIENT 2

There are different balances given by Peter Piper as Client 2 for the given period of 31st

December 2017 which has to give deep analysis of financial statements like income statement

and in the same context financial position, performance and stability for given period.

A. Peter piper's profit and loss statement for the year ended 31st December 2017.

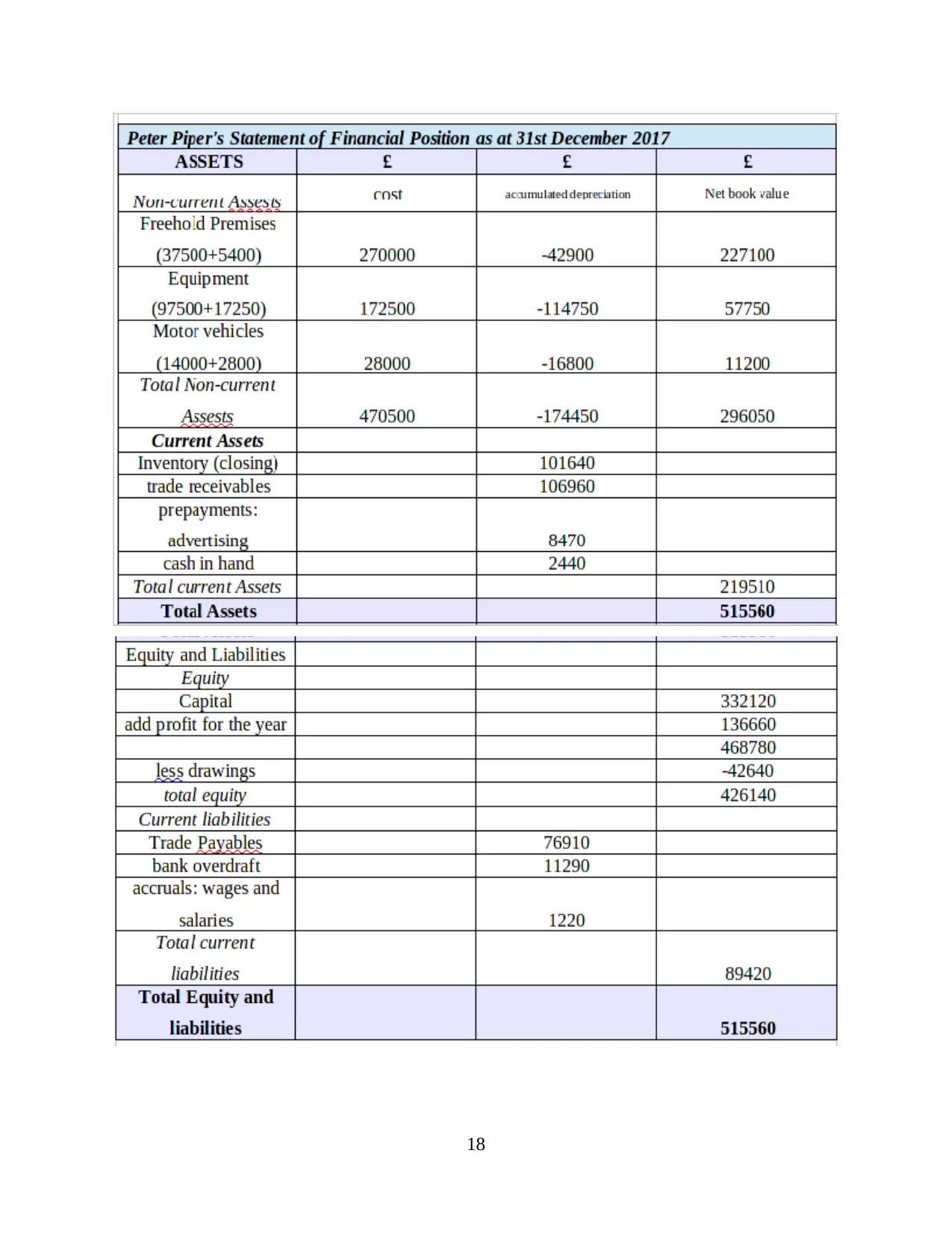

B. Peter piper's Balance sheet for the year ended 31st December 2017.

The individual or corporation's financial position has to be observed and analyzed by

considering profit and loss statement by some transactions which are relevant and held in this

specific period. These transactions will be giving advantage to each and every organization for

attaining adequate growth and even equity and strength of capital can be analyzed for perfroming

efforts related to operations of the organization. The financial position of Peter Piper can be

disclosed in very efficient manner by :

17

boards and institutions with the context of trial balance which is framed. The transactions are

recorded under the basic framework and format of the trial balance is given by different

principles and concepts of IASB, IFRS and GAAP.

CLIENT 2

There are different balances given by Peter Piper as Client 2 for the given period of 31st

December 2017 which has to give deep analysis of financial statements like income statement

and in the same context financial position, performance and stability for given period.

A. Peter piper's profit and loss statement for the year ended 31st December 2017.

B. Peter piper's Balance sheet for the year ended 31st December 2017.

The individual or corporation's financial position has to be observed and analyzed by

considering profit and loss statement by some transactions which are relevant and held in this

specific period. These transactions will be giving advantage to each and every organization for

attaining adequate growth and even equity and strength of capital can be analyzed for perfroming

efforts related to operations of the organization. The financial position of Peter Piper can be

disclosed in very efficient manner by :

17

18

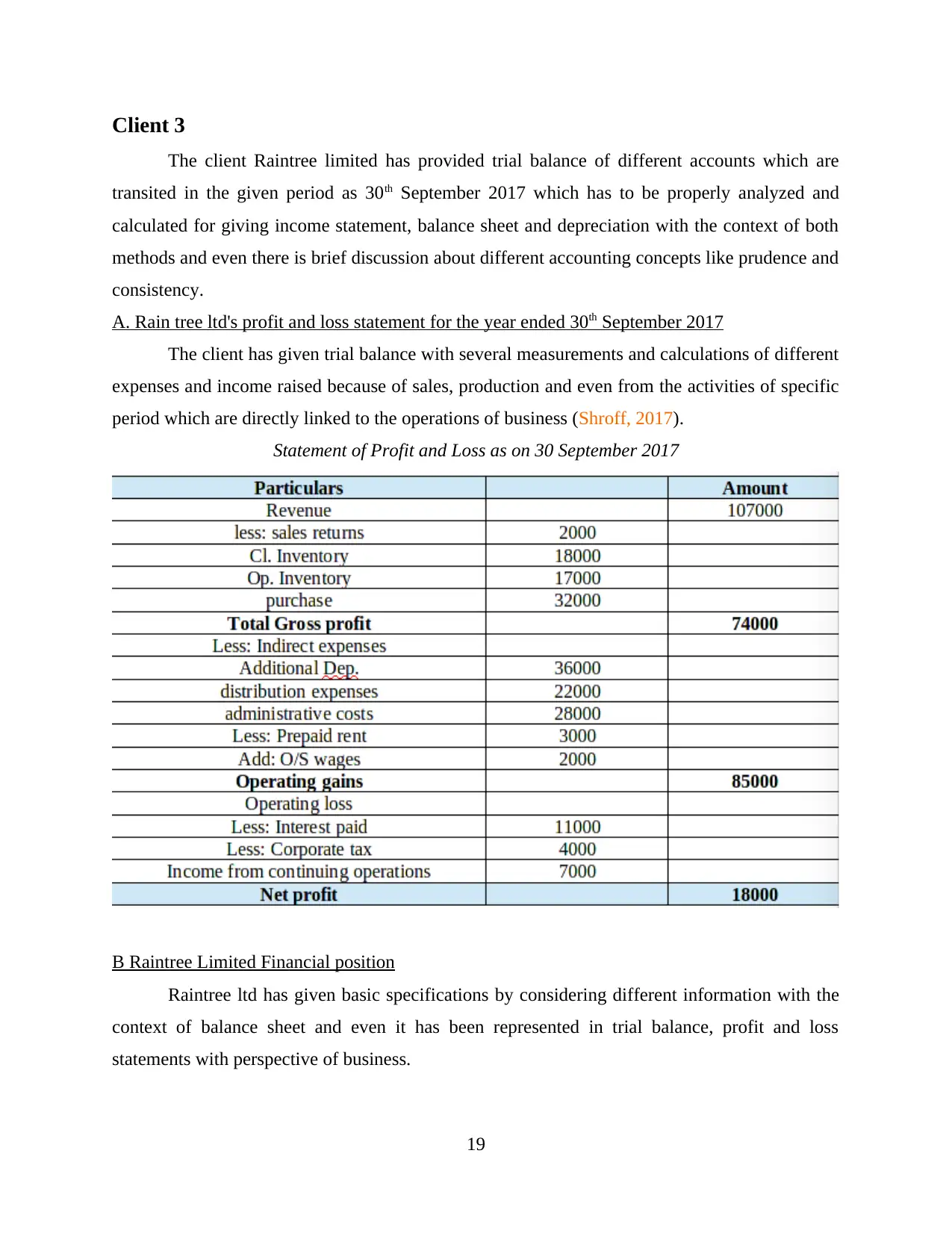

Client 3

The client Raintree limited has provided trial balance of different accounts which are

transited in the given period as 30th September 2017 which has to be properly analyzed and

calculated for giving income statement, balance sheet and depreciation with the context of both

methods and even there is brief discussion about different accounting concepts like prudence and

consistency.

A. Rain tree ltd's profit and loss statement for the year ended 30th September 2017

The client has given trial balance with several measurements and calculations of different

expenses and income raised because of sales, production and even from the activities of specific

period which are directly linked to the operations of business (Shroff, 2017).

Statement of Profit and Loss as on 30 September 2017

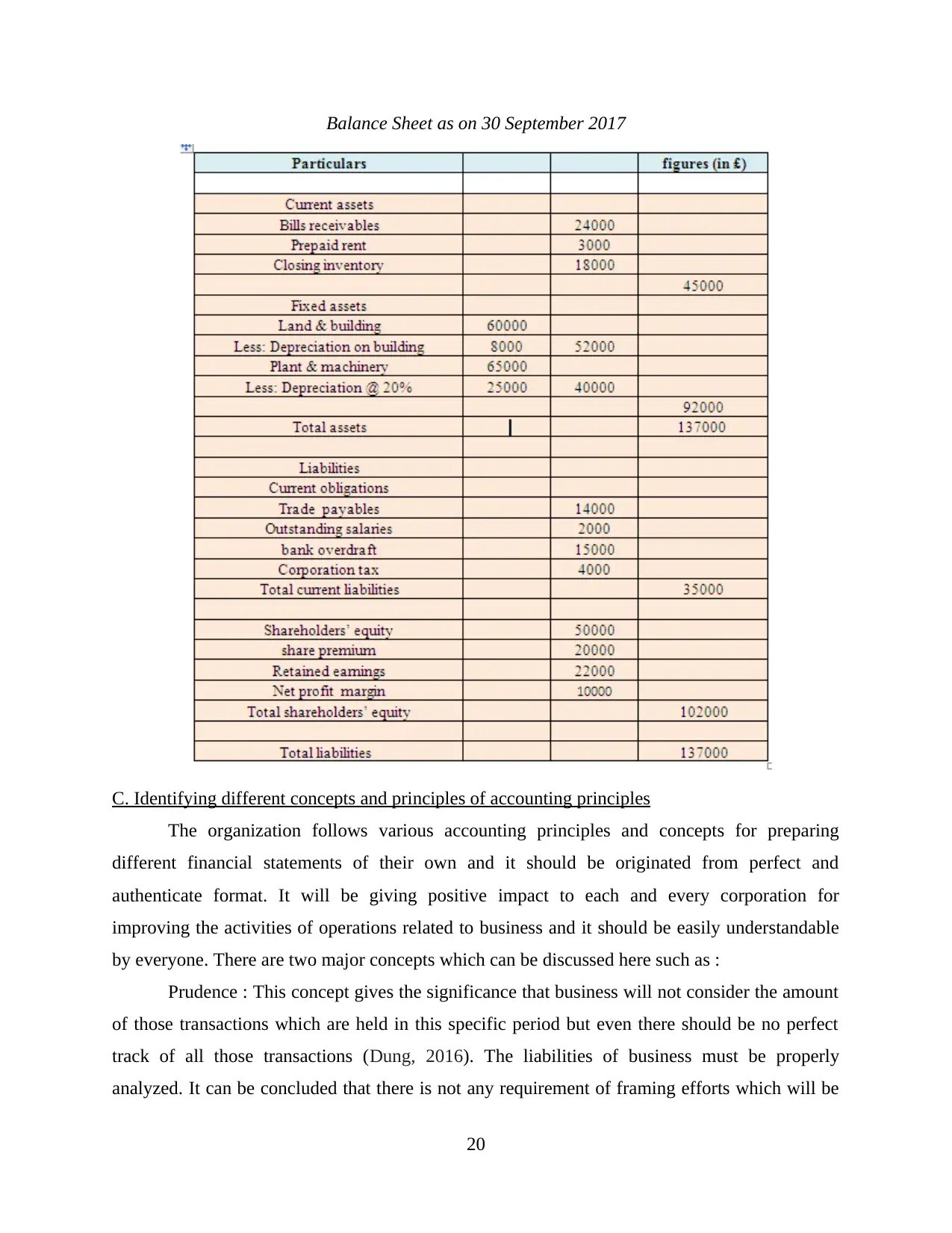

B Raintree Limited Financial position

Raintree ltd has given basic specifications by considering different information with the

context of balance sheet and even it has been represented in trial balance, profit and loss

statements with perspective of business.

19

The client Raintree limited has provided trial balance of different accounts which are

transited in the given period as 30th September 2017 which has to be properly analyzed and

calculated for giving income statement, balance sheet and depreciation with the context of both

methods and even there is brief discussion about different accounting concepts like prudence and

consistency.

A. Rain tree ltd's profit and loss statement for the year ended 30th September 2017

The client has given trial balance with several measurements and calculations of different

expenses and income raised because of sales, production and even from the activities of specific

period which are directly linked to the operations of business (Shroff, 2017).

Statement of Profit and Loss as on 30 September 2017

B Raintree Limited Financial position

Raintree ltd has given basic specifications by considering different information with the

context of balance sheet and even it has been represented in trial balance, profit and loss

statements with perspective of business.

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Balance Sheet as on 30 September 2017

C. Identifying different concepts and principles of accounting principles

The organization follows various accounting principles and concepts for preparing

different financial statements of their own and it should be originated from perfect and

authenticate format. It will be giving positive impact to each and every corporation for

improving the activities of operations related to business and it should be easily understandable

by everyone. There are two major concepts which can be discussed here such as :

Prudence : This concept gives the significance that business will not consider the amount

of those transactions which are held in this specific period but even there should be no perfect

track of all those transactions (Dung, 2016). The liabilities of business must be properly

analyzed. It can be concluded that there is not any requirement of framing efforts which will be

20

C. Identifying different concepts and principles of accounting principles

The organization follows various accounting principles and concepts for preparing

different financial statements of their own and it should be originated from perfect and

authenticate format. It will be giving positive impact to each and every corporation for

improving the activities of operations related to business and it should be easily understandable

by everyone. There are two major concepts which can be discussed here such as :

Prudence : This concept gives the significance that business will not consider the amount

of those transactions which are held in this specific period but even there should be no perfect

track of all those transactions (Dung, 2016). The liabilities of business must be properly

analyzed. It can be concluded that there is not any requirement of framing efforts which will be

20

giving benefit to business and along with this, concepts and principles of these tasks should be

properly understood by business.

Consistency : The operational activities of business should be performed in very

consistent way and along with this, sufficient efforts will be giving the best outcome to the

business. By considering these principles, organization is liable for disclosing the cost which is

predicted on daily basis. These disclosures will help the organization for attaining huge attraction

of stakeholders and even there will be more adequate efforts for improving the future (Sales

Ledger Control account. 2018.).

C. Significance of measuring and representing depreciation with context of business giving brief

about both methods of business.

Depreciation can be defined as fall in value of asset and it will be giving advantage to business

for creating efforts and for representing the asset value in given current time. The main objective

of summing deprecation in these statements is about devaluation of assets with the value of

purchase. The two methods of deprecation are as follows:

Written down method : In this method deprecation has been measured for increase in

proportion with increase in value of charges of depreciation and even for the balance which has

been estimated for completing useful life of all these assets (Küpper and Pedell, 2016).

Straight line method : In this method depreciation has been charged over all the assets on

technique which is default and in this fixed amount of depreciation has been deducted from

assets for remaining period.

With the context of analyzing profit and loss statement of the following business, there is

presence of different transactions which are recorded and then net profit of 10000 has been

generated with sufficient balance. There are different profit and losses which are framed and

recorded and it will be giving outcome as perfect balance.

CLIENT 4

A. Aim for framing bank statement

The main objective of representing the bank statement in the given period for Kendal,

there is presence of different transactions which helps in understanding of expenses and gains

with given specific data set which will lead to understanding of flow of money (Dutta and

Patatoukas, 2016). It will be giving advantage to business for preparing efforts and even for

extracting information for disclosure.

21

properly understood by business.

Consistency : The operational activities of business should be performed in very

consistent way and along with this, sufficient efforts will be giving the best outcome to the

business. By considering these principles, organization is liable for disclosing the cost which is

predicted on daily basis. These disclosures will help the organization for attaining huge attraction

of stakeholders and even there will be more adequate efforts for improving the future (Sales

Ledger Control account. 2018.).

C. Significance of measuring and representing depreciation with context of business giving brief

about both methods of business.

Depreciation can be defined as fall in value of asset and it will be giving advantage to business

for creating efforts and for representing the asset value in given current time. The main objective

of summing deprecation in these statements is about devaluation of assets with the value of

purchase. The two methods of deprecation are as follows:

Written down method : In this method deprecation has been measured for increase in

proportion with increase in value of charges of depreciation and even for the balance which has

been estimated for completing useful life of all these assets (Küpper and Pedell, 2016).

Straight line method : In this method depreciation has been charged over all the assets on

technique which is default and in this fixed amount of depreciation has been deducted from

assets for remaining period.

With the context of analyzing profit and loss statement of the following business, there is

presence of different transactions which are recorded and then net profit of 10000 has been

generated with sufficient balance. There are different profit and losses which are framed and

recorded and it will be giving outcome as perfect balance.

CLIENT 4

A. Aim for framing bank statement

The main objective of representing the bank statement in the given period for Kendal,

there is presence of different transactions which helps in understanding of expenses and gains

with given specific data set which will lead to understanding of flow of money (Dutta and

Patatoukas, 2016). It will be giving advantage to business for preparing efforts and even for

extracting information for disclosure.

21

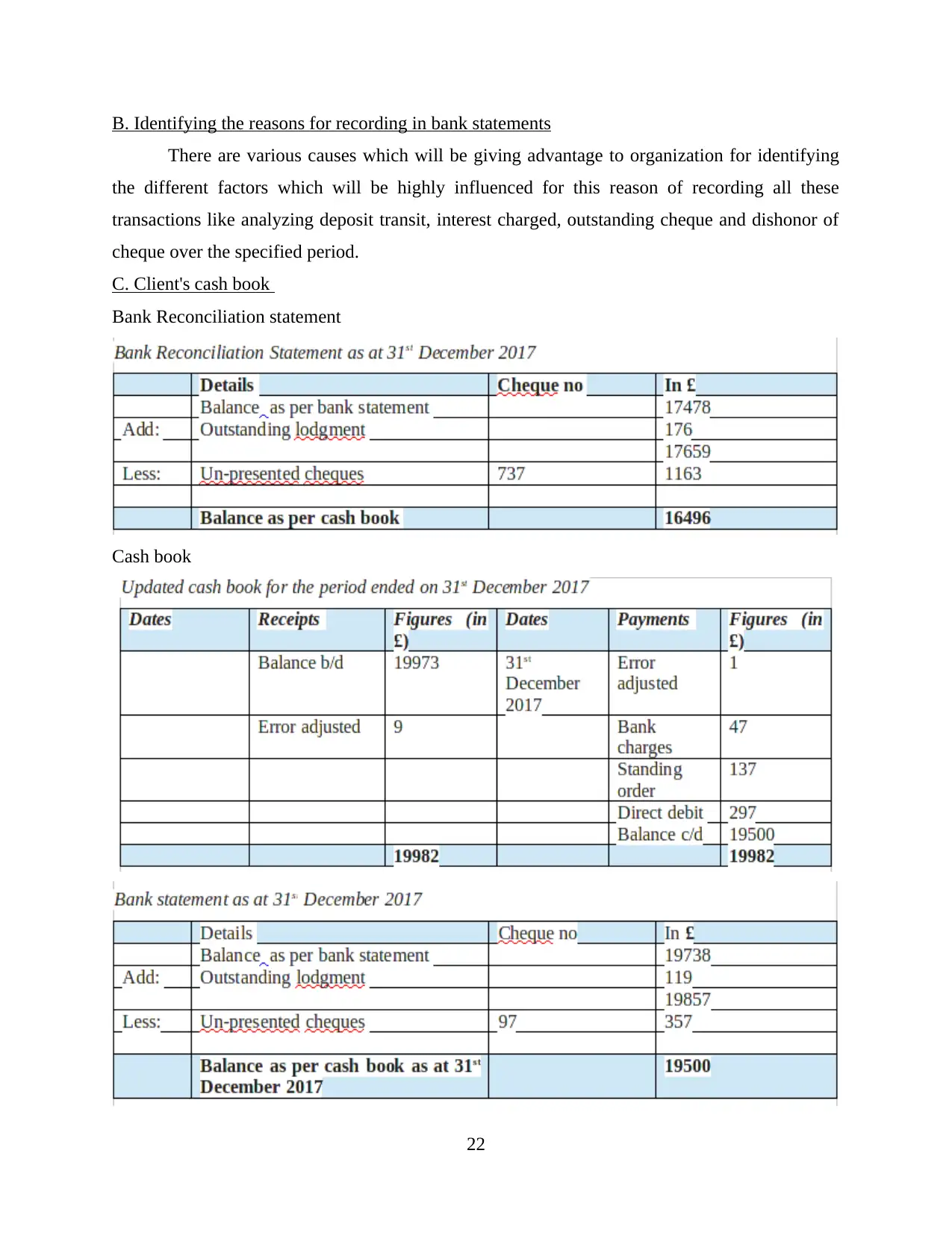

B. Identifying the reasons for recording in bank statements

There are various causes which will be giving advantage to organization for identifying

the different factors which will be highly influenced for this reason of recording all these

transactions like analyzing deposit transit, interest charged, outstanding cheque and dishonor of

cheque over the specified period.

C. Client's cash book

Bank Reconciliation statement

Cash book

22

There are various causes which will be giving advantage to organization for identifying

the different factors which will be highly influenced for this reason of recording all these

transactions like analyzing deposit transit, interest charged, outstanding cheque and dishonor of

cheque over the specified period.

C. Client's cash book

Bank Reconciliation statement

Cash book

22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CLIENT 5

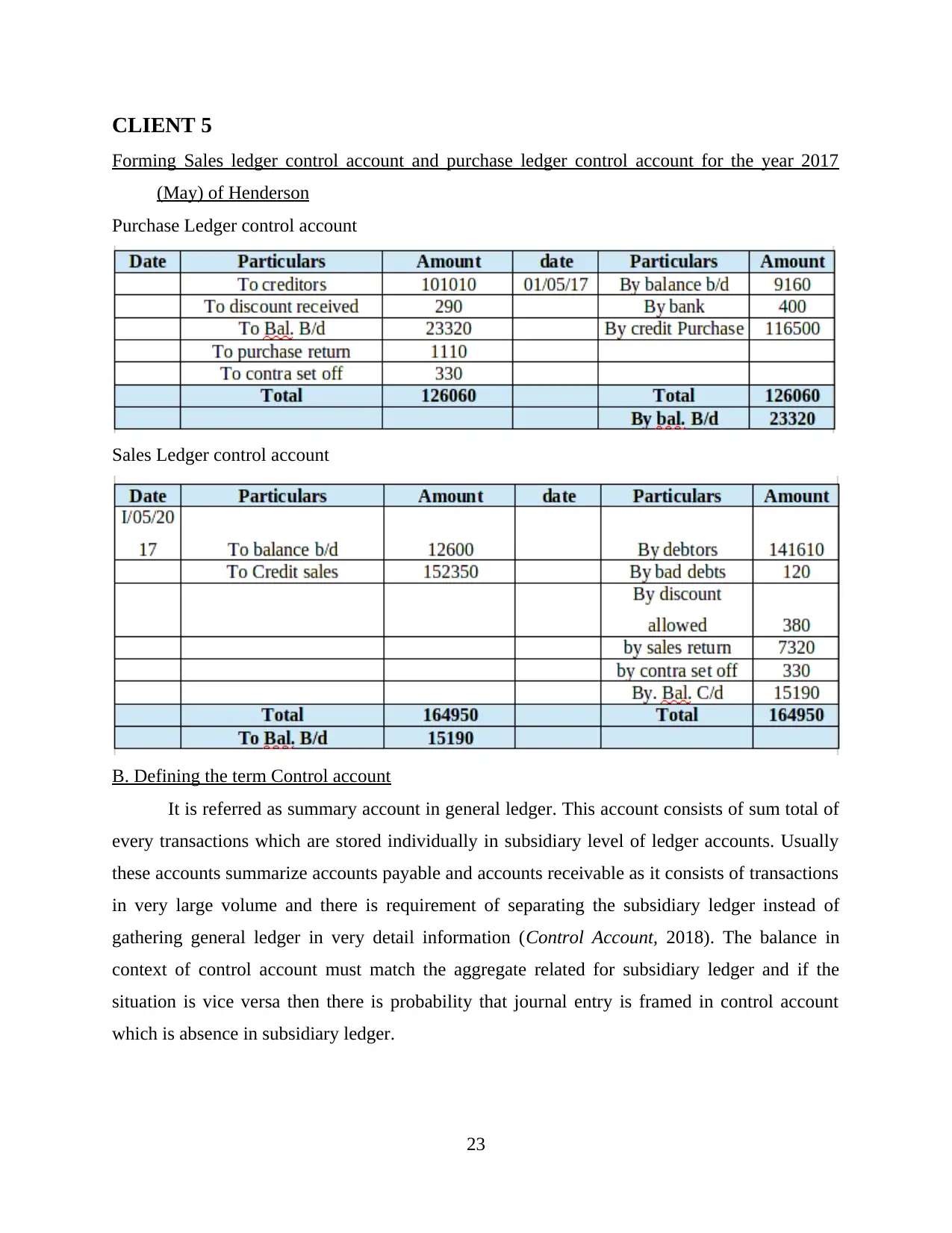

Forming Sales ledger control account and purchase ledger control account for the year 2017

(May) of Henderson

Purchase Ledger control account

Sales Ledger control account

B. Defining the term Control account

It is referred as summary account in general ledger. This account consists of sum total of

every transactions which are stored individually in subsidiary level of ledger accounts. Usually

these accounts summarize accounts payable and accounts receivable as it consists of transactions

in very large volume and there is requirement of separating the subsidiary ledger instead of

gathering general ledger in very detail information (Control Account, 2018). The balance in

context of control account must match the aggregate related for subsidiary ledger and if the

situation is vice versa then there is probability that journal entry is framed in control account

which is absence in subsidiary ledger.

23

Forming Sales ledger control account and purchase ledger control account for the year 2017

(May) of Henderson

Purchase Ledger control account

Sales Ledger control account

B. Defining the term Control account

It is referred as summary account in general ledger. This account consists of sum total of

every transactions which are stored individually in subsidiary level of ledger accounts. Usually

these accounts summarize accounts payable and accounts receivable as it consists of transactions

in very large volume and there is requirement of separating the subsidiary ledger instead of

gathering general ledger in very detail information (Control Account, 2018). The balance in

context of control account must match the aggregate related for subsidiary ledger and if the

situation is vice versa then there is probability that journal entry is framed in control account

which is absence in subsidiary ledger.

23

CLIENT 6

A. Suspense account with its characteristics

Suspense account indicates the account which is prepared for extracting the mistake

which is created in previous year. This nature of this account is temporary and for very less

duration. After finding these problems and resolving issues there will be absence of any single

amount in this account. While preparing this account, it should be always considered that its

duration is very less, as it should be rectified as soon as possible. Its deadline for becoming zero

is before drafting final accounts and these mistakes should be resolved simultaneously.

B. Preparing trial balance

The particular list should be identified with closing balance of the account of ledger at

some given date and it is the most prior step for drafting financial statements. Usually the

preparation of trial balance and all financial statement in the end of accounting period. Basically

there are two sides in trial balance i.e. debit side and credit side. Various assets are included in

debit side and all liabilities, expenses and income consists in credit side (Trial Balance, 2017).

Interpretation : The present statement is considered as a trial balance of the year end.

The particulars side gives the names of account about its extraction. Generally it is applicable for

all the entries which are drafted in right manner and if debit and credit side are not matched then

there is some error in trial balance.

24

A. Suspense account with its characteristics

Suspense account indicates the account which is prepared for extracting the mistake

which is created in previous year. This nature of this account is temporary and for very less

duration. After finding these problems and resolving issues there will be absence of any single

amount in this account. While preparing this account, it should be always considered that its

duration is very less, as it should be rectified as soon as possible. Its deadline for becoming zero

is before drafting final accounts and these mistakes should be resolved simultaneously.

B. Preparing trial balance

The particular list should be identified with closing balance of the account of ledger at

some given date and it is the most prior step for drafting financial statements. Usually the

preparation of trial balance and all financial statement in the end of accounting period. Basically

there are two sides in trial balance i.e. debit side and credit side. Various assets are included in

debit side and all liabilities, expenses and income consists in credit side (Trial Balance, 2017).

Interpretation : The present statement is considered as a trial balance of the year end.

The particulars side gives the names of account about its extraction. Generally it is applicable for

all the entries which are drafted in right manner and if debit and credit side are not matched then

there is some error in trial balance.

24

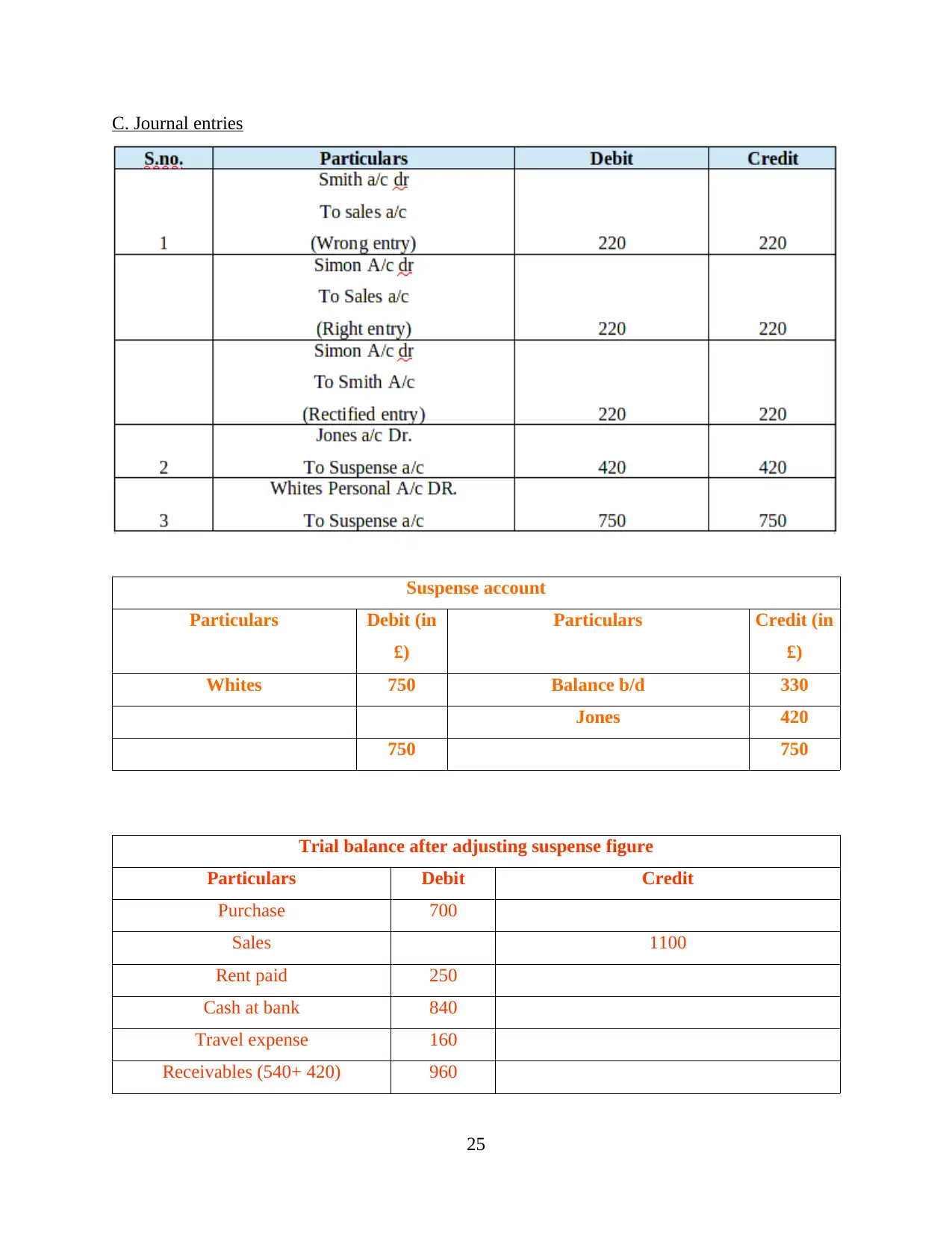

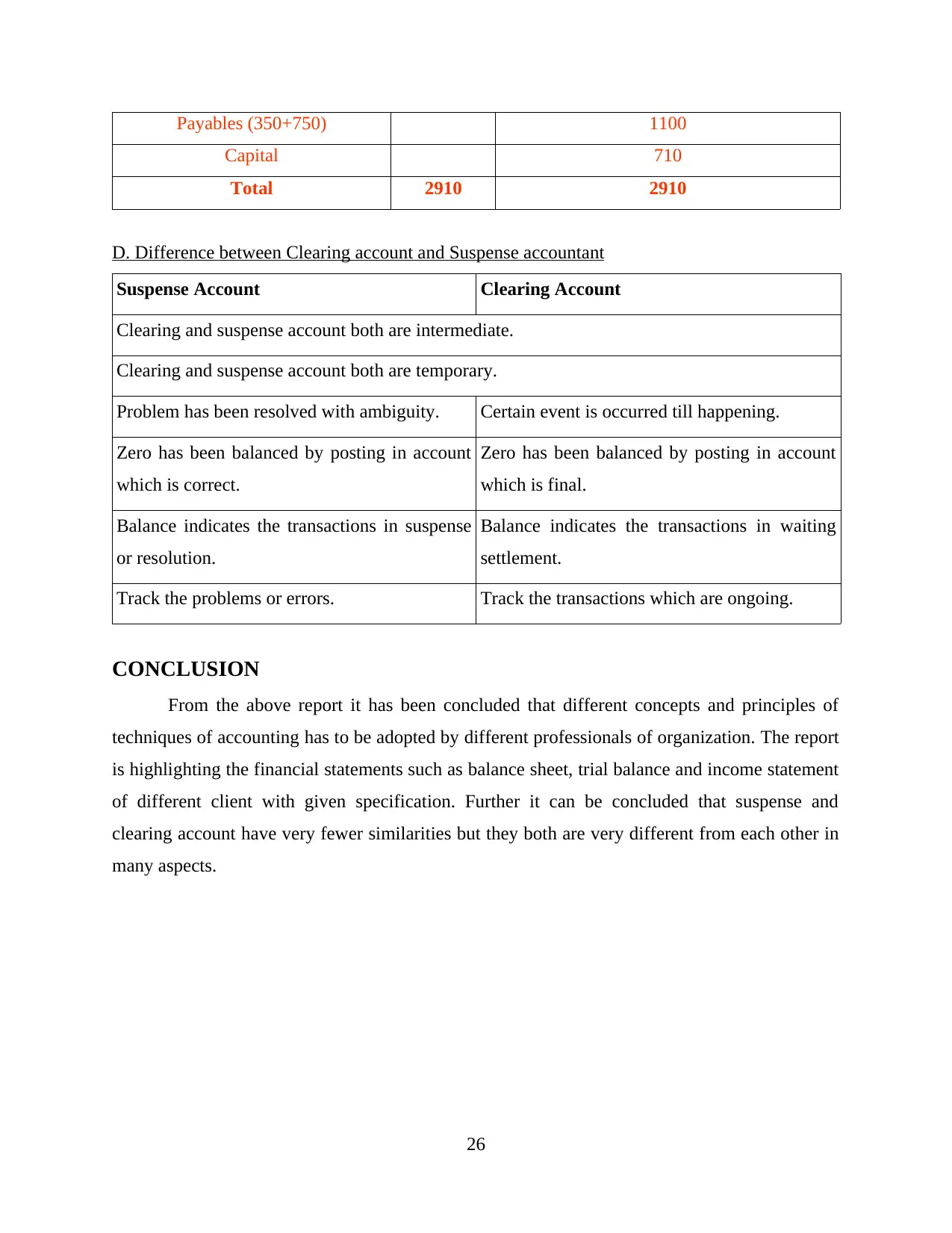

C. Journal entries

Suspense account

Particulars Debit (in

£)

Particulars Credit (in

£)

Whites 750 Balance b/d 330

Jones 420

750 750

Trial balance after adjusting suspense figure

Particulars Debit Credit

Purchase 700

Sales 1100

Rent paid 250

Cash at bank 840

Travel expense 160

Receivables (540+ 420) 960

25

Suspense account

Particulars Debit (in

£)

Particulars Credit (in

£)

Whites 750 Balance b/d 330

Jones 420

750 750

Trial balance after adjusting suspense figure

Particulars Debit Credit

Purchase 700

Sales 1100

Rent paid 250

Cash at bank 840

Travel expense 160

Receivables (540+ 420) 960

25

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Payables (350+750) 1100

Capital 710

Total 2910 2910

D. Difference between Clearing account and Suspense accountant

Suspense Account Clearing Account

Clearing and suspense account both are intermediate.

Clearing and suspense account both are temporary.

Problem has been resolved with ambiguity. Certain event is occurred till happening.

Zero has been balanced by posting in account

which is correct.

Zero has been balanced by posting in account

which is final.

Balance indicates the transactions in suspense

or resolution.

Balance indicates the transactions in waiting

settlement.

Track the problems or errors. Track the transactions which are ongoing.

CONCLUSION

From the above report it has been concluded that different concepts and principles of

techniques of accounting has to be adopted by different professionals of organization. The report

is highlighting the financial statements such as balance sheet, trial balance and income statement

of different client with given specification. Further it can be concluded that suspense and

clearing account have very fewer similarities but they both are very different from each other in

many aspects.

26

Capital 710

Total 2910 2910

D. Difference between Clearing account and Suspense accountant

Suspense Account Clearing Account

Clearing and suspense account both are intermediate.

Clearing and suspense account both are temporary.

Problem has been resolved with ambiguity. Certain event is occurred till happening.

Zero has been balanced by posting in account

which is correct.

Zero has been balanced by posting in account

which is final.

Balance indicates the transactions in suspense

or resolution.

Balance indicates the transactions in waiting

settlement.

Track the problems or errors. Track the transactions which are ongoing.

CONCLUSION

From the above report it has been concluded that different concepts and principles of

techniques of accounting has to be adopted by different professionals of organization. The report

is highlighting the financial statements such as balance sheet, trial balance and income statement

of different client with given specification. Further it can be concluded that suspense and

clearing account have very fewer similarities but they both are very different from each other in

many aspects.

26

REFERENCES

Books and Journals

Dung, N. V., 2016. Value-relevance of financial statement information: A flexible application of

modern theories to the Vietnamese stock market. Quarterly Journal of Economics. 84.

pp.488-500.

Hepworth, N., 2017. Is implementing the IPSASs an appropriate reform?. Public Money &

Management. 37(2). 141-148.

Küpper, H. U. and Pedell, B., 2016. Which asset valuation and depreciation method should be

used for regulated utilities? An analytical and simulation-based comparison. Utilities

Policy. 40. pp.88-103.

Li, S., Sougiannis, T. and Wang, I., 2017. Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows.

Ritchi, H., Fettry, S., & Susanto, A, 2016. Toward Defining Key Success Factors of E-

Government and Accounting Information Quality: Case of Indonesia. International

Journal of Accounting Research. 2(1). 20-35.

Shroff, N., 2017. Corporate investment and changes in GAAP. Review of Accounting

Studies. 22(1). pp.1-63.

Trucco, S., 2015. Premises for the Convergence of Financial Accounting and Management

Accounting. In Financial Accounting (pp. 41-64). Springer, Cham.

ONLINE

Control Account. 2018. [Online]. Available through

:<https://www.accountingcoach.com/blog/accounts-receivable-control-account-subsidiary-

ledger>.

Sales Ledger Control account. 2018. [Online]. Available through

:<https://www.accountingcapital.com/books-and-accounts/sales-ledger-control-and-

purchase-ledger-control/>.

Trial Balance. 2017. [Online]. Available through :<http://accounting-simplified.com/trial-

balance.html>.

27

Books and Journals

Dung, N. V., 2016. Value-relevance of financial statement information: A flexible application of

modern theories to the Vietnamese stock market. Quarterly Journal of Economics. 84.

pp.488-500.

Hepworth, N., 2017. Is implementing the IPSASs an appropriate reform?. Public Money &

Management. 37(2). 141-148.

Küpper, H. U. and Pedell, B., 2016. Which asset valuation and depreciation method should be

used for regulated utilities? An analytical and simulation-based comparison. Utilities

Policy. 40. pp.88-103.

Li, S., Sougiannis, T. and Wang, I., 2017. Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows.

Ritchi, H., Fettry, S., & Susanto, A, 2016. Toward Defining Key Success Factors of E-

Government and Accounting Information Quality: Case of Indonesia. International

Journal of Accounting Research. 2(1). 20-35.

Shroff, N., 2017. Corporate investment and changes in GAAP. Review of Accounting

Studies. 22(1). pp.1-63.

Trucco, S., 2015. Premises for the Convergence of Financial Accounting and Management

Accounting. In Financial Accounting (pp. 41-64). Springer, Cham.

ONLINE

Control Account. 2018. [Online]. Available through

:<https://www.accountingcoach.com/blog/accounts-receivable-control-account-subsidiary-

ledger>.

Sales Ledger Control account. 2018. [Online]. Available through

:<https://www.accountingcapital.com/books-and-accounts/sales-ledger-control-and-

purchase-ledger-control/>.

Trial Balance. 2017. [Online]. Available through :<http://accounting-simplified.com/trial-

balance.html>.

27

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.