Financial Accounting Principles: A Comprehensive Guide

VerifiedAdded on 2024/06/04

|39

|4580

|181

AI Summary

This comprehensive guide explores the fundamental principles of financial accounting, covering key definitions, regulations, rules, and conventions. It delves into practical applications through a portfolio of client case studies, demonstrating the application of accounting principles in real-world scenarios. The guide also examines essential concepts like consistency, material disclosure, bank reconciliation, control accounts, and suspense accounts, providing a thorough understanding of financial accounting practices.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting Principles

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

A. Report..........................................................................................................................................4

1. Define financial accounting.........................................................................................................4

2. Explain the regulations relating to financial accounting.............................................................4

3. Describe accounting rules and principles....................................................................................4

4. Explain the conventions and concepts relating to consistency and material disclosure..............5

B. Portfolio of clients.......................................................................................................................6

Client 1.............................................................................................................................................6

Client 2...........................................................................................................................................24

(a) The statement of profit or loss for Peter Piper for the period ended 31st December 2017.......24

(b) The statement of financial position for Peter Piper as at 31st December 2017........................24

Client 3...........................................................................................................................................27

(a) Prepare the statement of profit and loss of Raintree Ltd., for the year ended 30 September

2017...............................................................................................................................................27

(b) The statement of financial position of Raintree Ltd. as at 30 September 2017.......................27

(c) Explain the accounting concept of “consistency” and “prudence”..........................................28

(d) Briefly discuss the purpose of depreciation in formulating accounting statements and

illustrate two widely used methods of calculating it.....................................................................28

Client 4...........................................................................................................................................30

A. Explain the purpose of preparing bank reconciliation statement..............................................30

B. List and explain some of the areas, which may cause your record to vary from the bank

records............................................................................................................................................30

C. (i) Bank reconciliation statement at December 1, 2017............................................................30

(ii) Updated cash book...................................................................................................................30

(iii) Bank reconciliation statement as on December 2017.............................................................31

Client 5...........................................................................................................................................33

A. (i) Sales ledger control account................................................................................................33

(ii) Purchase ledger control account..............................................................................................33

B. Explain the term “control account”...........................................................................................34

Client 6...........................................................................................................................................35

A. Suspense account and its features.............................................................................................35

2

A. Report..........................................................................................................................................4

1. Define financial accounting.........................................................................................................4

2. Explain the regulations relating to financial accounting.............................................................4

3. Describe accounting rules and principles....................................................................................4

4. Explain the conventions and concepts relating to consistency and material disclosure..............5

B. Portfolio of clients.......................................................................................................................6

Client 1.............................................................................................................................................6

Client 2...........................................................................................................................................24

(a) The statement of profit or loss for Peter Piper for the period ended 31st December 2017.......24

(b) The statement of financial position for Peter Piper as at 31st December 2017........................24

Client 3...........................................................................................................................................27

(a) Prepare the statement of profit and loss of Raintree Ltd., for the year ended 30 September

2017...............................................................................................................................................27

(b) The statement of financial position of Raintree Ltd. as at 30 September 2017.......................27

(c) Explain the accounting concept of “consistency” and “prudence”..........................................28

(d) Briefly discuss the purpose of depreciation in formulating accounting statements and

illustrate two widely used methods of calculating it.....................................................................28

Client 4...........................................................................................................................................30

A. Explain the purpose of preparing bank reconciliation statement..............................................30

B. List and explain some of the areas, which may cause your record to vary from the bank

records............................................................................................................................................30

C. (i) Bank reconciliation statement at December 1, 2017............................................................30

(ii) Updated cash book...................................................................................................................30

(iii) Bank reconciliation statement as on December 2017.............................................................31

Client 5...........................................................................................................................................33

A. (i) Sales ledger control account................................................................................................33

(ii) Purchase ledger control account..............................................................................................33

B. Explain the term “control account”...........................................................................................34

Client 6...........................................................................................................................................35

A. Suspense account and its features.............................................................................................35

2

B. Trial balance..............................................................................................................................35

C. Journal entries to clear suspense account..................................................................................36

D. Differentiate between suspense and clearing account..............................................................37

Reference list.................................................................................................................................38

3

C. Journal entries to clear suspense account..................................................................................36

D. Differentiate between suspense and clearing account..............................................................37

Reference list.................................................................................................................................38

3

A. Report

1. Define financial accounting

According to Deegan (2013), financial accounting is one of the specialized branches in

accountancy that is concerned with the tracking of the financial transactions of companies and

converting them into financial statements and accounts by applying standardized guidelines.

2. Explain the regulations relating to financial accounting

Williams (2014) stated that the regulations related to financial accounting is different in different

countries. For instance, the companies in Australia follow the financial accounting regulations

stated under the Australian Accounting Standard Board. On the contrary, the companies working

in UK have to follow the regulations of financial accounting mentioned under the IFRS

(International Financial Regulatory Standards) and GAAP (Generally Accepted Accounting

Principles).

However, the regulations of financial accounting in UK vary from sector to sector. For instance,

the firms in the financial and banking sector of UK need to adapt to the regulations mentioned in

“Financial Services and Markets Act, 2000”, which states that all firms are required the

maintenance of high transparency of their financial statements and accounts (Warren, 2016). The

overall regulations and frameworks in UK related to financial accounting are governed through

UK’s Financial Reporting Council (Council, 2013). According to Council (2014), the new

regulations related to financial accounting in UK had been published in the FRS 100 in

November 2012. These are major regulations related to financial accounting in the UK, which

have to be followed in every company in the country for preparing financial statements.

3. Describe accounting rules and principles

Financial accounting consists of different rules and principles. As stated by Marshall (2016), the

golden rules of accounting are the basic financial accounting rules, which are as follows -

“Debit the receiver, credit the giver” (personal account)

“Debit what comes in, credit what goes out” (real account)

4

1. Define financial accounting

According to Deegan (2013), financial accounting is one of the specialized branches in

accountancy that is concerned with the tracking of the financial transactions of companies and

converting them into financial statements and accounts by applying standardized guidelines.

2. Explain the regulations relating to financial accounting

Williams (2014) stated that the regulations related to financial accounting is different in different

countries. For instance, the companies in Australia follow the financial accounting regulations

stated under the Australian Accounting Standard Board. On the contrary, the companies working

in UK have to follow the regulations of financial accounting mentioned under the IFRS

(International Financial Regulatory Standards) and GAAP (Generally Accepted Accounting

Principles).

However, the regulations of financial accounting in UK vary from sector to sector. For instance,

the firms in the financial and banking sector of UK need to adapt to the regulations mentioned in

“Financial Services and Markets Act, 2000”, which states that all firms are required the

maintenance of high transparency of their financial statements and accounts (Warren, 2016). The

overall regulations and frameworks in UK related to financial accounting are governed through

UK’s Financial Reporting Council (Council, 2013). According to Council (2014), the new

regulations related to financial accounting in UK had been published in the FRS 100 in

November 2012. These are major regulations related to financial accounting in the UK, which

have to be followed in every company in the country for preparing financial statements.

3. Describe accounting rules and principles

Financial accounting consists of different rules and principles. As stated by Marshall (2016), the

golden rules of accounting are the basic financial accounting rules, which are as follows -

“Debit the receiver, credit the giver” (personal account)

“Debit what comes in, credit what goes out” (real account)

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

“Debit losses and expenses, credit incomes and gains (nominal account)

The following are the basic principles of financial accounting -

Materiality principle - Edgley (2016) stated the materiality principle of financial

accounting states that only material transactions of a company should be recorded in its

financial accounts.

Conservatism principle - According to the conservatism principle, expenses and

liabilities are to be realized as and when recognized even when there are uncertainties

related to the outcomes (Penman, 2016). However, revenue and assets are to be realized

only when there it is assured to be received.

Accrual principle - This principle of financial accounting states that financial

transactions of a company are to be recorded when they occur, not when cash is realized

from the transactions (Kausar et al., 2017).

4. Explain the conventions and concepts relating to consistency and material disclosure

Material disclosure consistency - This convention of accountancy states that a business needs to

provided all necessary information relating to the company in its financial statements (Picker et

al., 2016).

Convention of consistency - Warren (2015) stated that the convention of consistency in financial

accounting says that accounting techniques, which have been adopted once, should be

consistently applied during the future as well. In all similar situations, the accounting techniques

must be consistent.

5

The following are the basic principles of financial accounting -

Materiality principle - Edgley (2016) stated the materiality principle of financial

accounting states that only material transactions of a company should be recorded in its

financial accounts.

Conservatism principle - According to the conservatism principle, expenses and

liabilities are to be realized as and when recognized even when there are uncertainties

related to the outcomes (Penman, 2016). However, revenue and assets are to be realized

only when there it is assured to be received.

Accrual principle - This principle of financial accounting states that financial

transactions of a company are to be recorded when they occur, not when cash is realized

from the transactions (Kausar et al., 2017).

4. Explain the conventions and concepts relating to consistency and material disclosure

Material disclosure consistency - This convention of accountancy states that a business needs to

provided all necessary information relating to the company in its financial statements (Picker et

al., 2016).

Convention of consistency - Warren (2015) stated that the convention of consistency in financial

accounting says that accounting techniques, which have been adopted once, should be

consistently applied during the future as well. In all similar situations, the accounting techniques

must be consistent.

5

B. Portfolio of clients

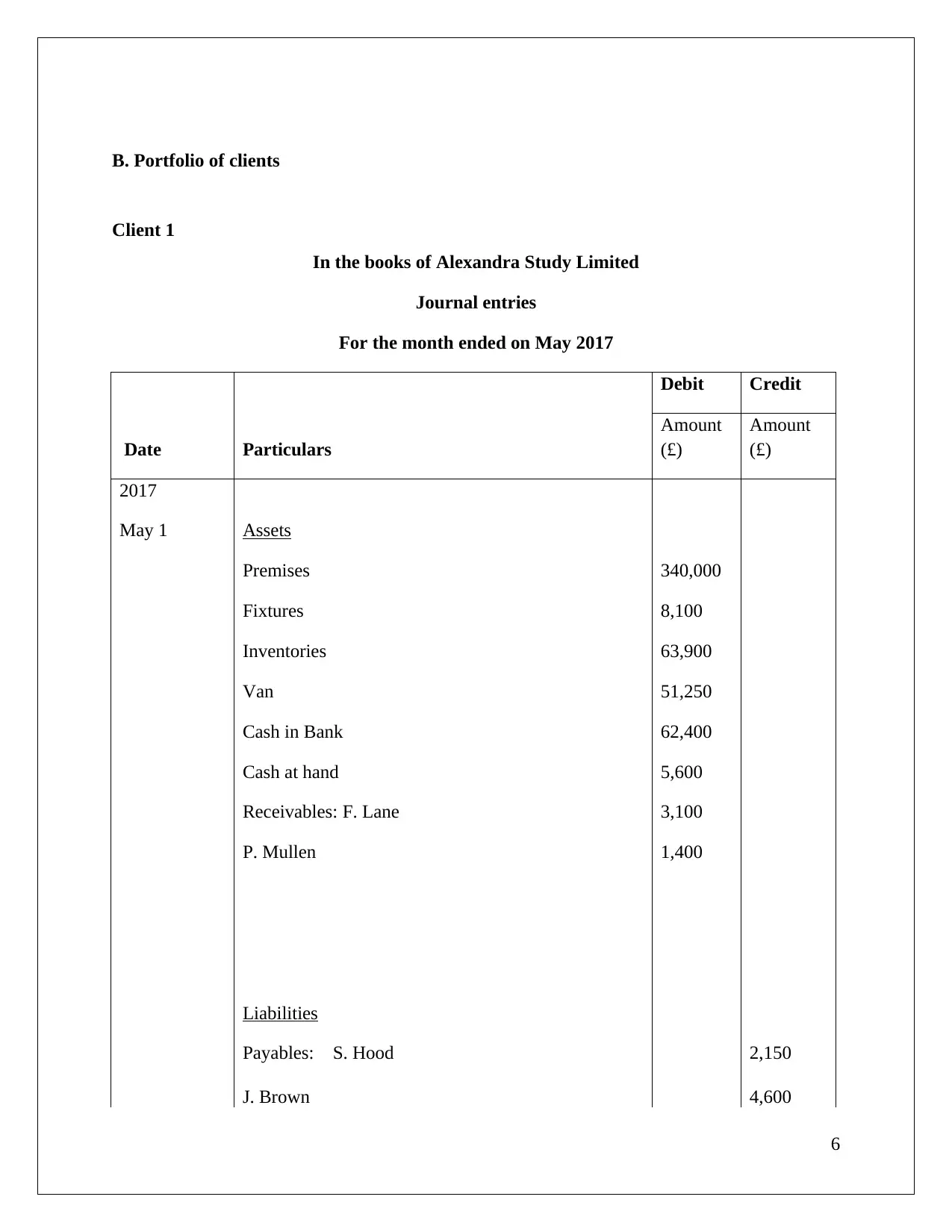

Client 1

In the books of Alexandra Study Limited

Journal entries

For the month ended on May 2017

Date Particulars

Debit Credit

Amount

(£)

Amount

(£)

2017

May 1 Assets

Premises 340,000

Fixtures 8,100

Inventories 63,900

Van 51,250

Cash in Bank 62,400

Cash at hand 5,600

Receivables: F. Lane 3,100

P. Mullen 1,400

Liabilities

Payables: S. Hood 2,150

J. Brown 4,600

6

Client 1

In the books of Alexandra Study Limited

Journal entries

For the month ended on May 2017

Date Particulars

Debit Credit

Amount

(£)

Amount

(£)

2017

May 1 Assets

Premises 340,000

Fixtures 8,100

Inventories 63,900

Van 51,250

Cash in Bank 62,400

Cash at hand 5,600

Receivables: F. Lane 3,100

P. Mullen 1,400

Liabilities

Payables: S. Hood 2,150

J. Brown 4,600

6

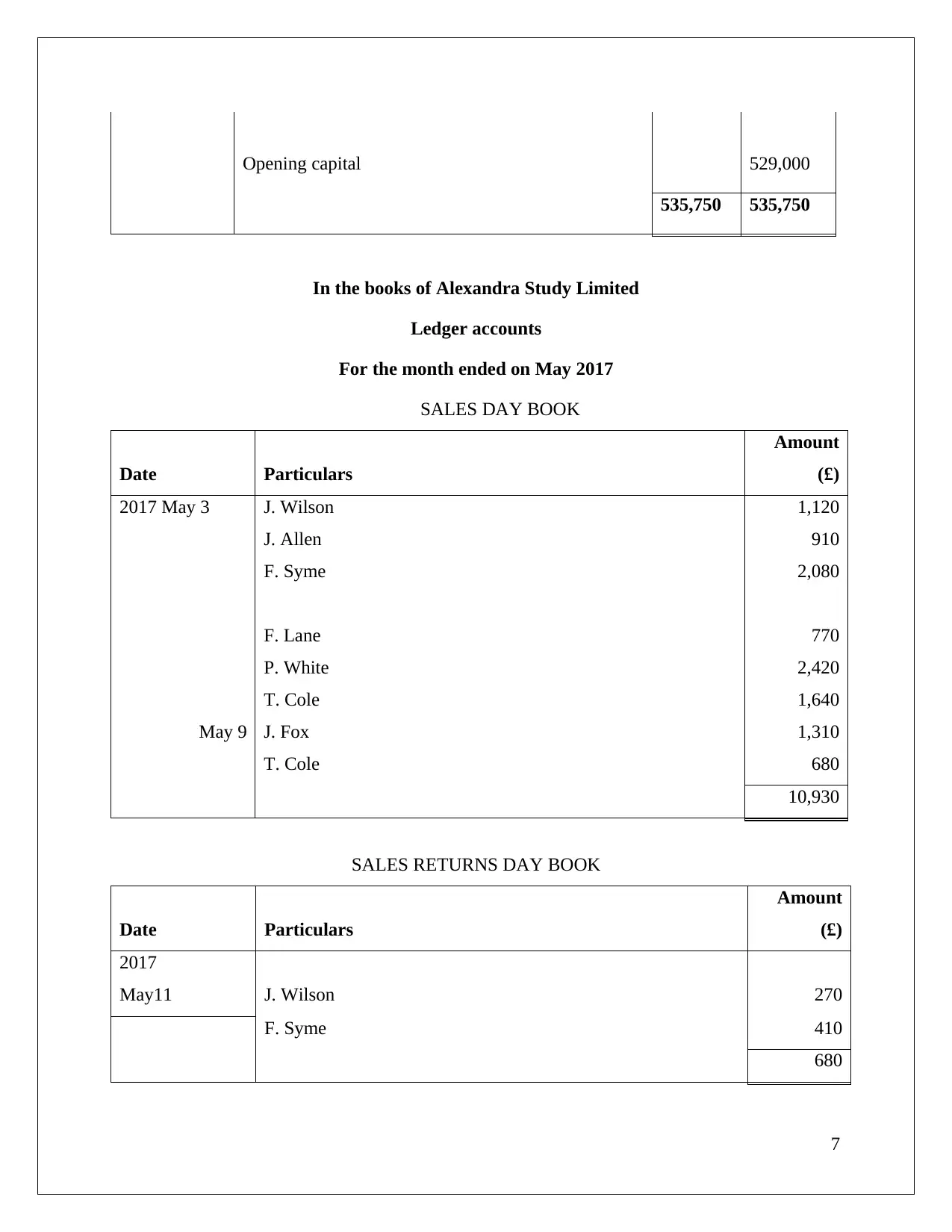

Opening capital 529,000

535,750 535,750

In the books of Alexandra Study Limited

Ledger accounts

For the month ended on May 2017

SALES DAY BOOK

Date Particulars

Amount

(£)

2017 May 3 J. Wilson 1,120

J. Allen 910

F. Syme 2,080

F. Lane 770

P. White 2,420

T. Cole 1,640

May 9 J. Fox 1,310

T. Cole 680

10,930

SALES RETURNS DAY BOOK

Date Particulars

Amount

(£)

2017

May11 J. Wilson 270

F. Syme 410

680

7

535,750 535,750

In the books of Alexandra Study Limited

Ledger accounts

For the month ended on May 2017

SALES DAY BOOK

Date Particulars

Amount

(£)

2017 May 3 J. Wilson 1,120

J. Allen 910

F. Syme 2,080

F. Lane 770

P. White 2,420

T. Cole 1,640

May 9 J. Fox 1,310

T. Cole 680

10,930

SALES RETURNS DAY BOOK

Date Particulars

Amount

(£)

2017

May11 J. Wilson 270

F. Syme 410

680

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

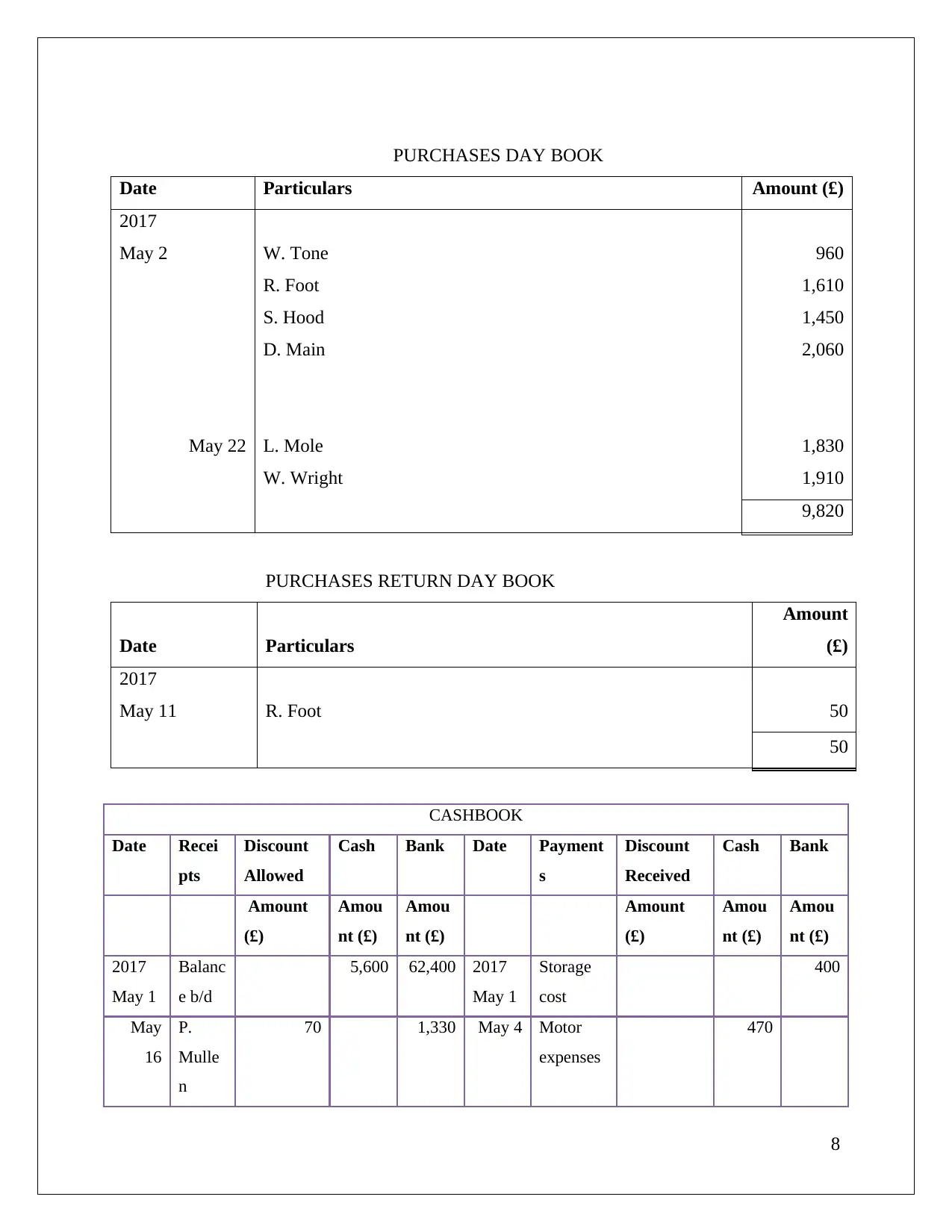

PURCHASES DAY BOOK

Date Particulars Amount (£)

2017

May 2 W. Tone 960

R. Foot 1,610

S. Hood 1,450

D. Main 2,060

May 22 L. Mole 1,830

W. Wright 1,910

9,820

PURCHASES RETURN DAY BOOK

Date Particulars

Amount

(£)

2017

May 11 R. Foot 50

50

CASHBOOK

Date Recei

pts

Discount

Allowed

Cash Bank Date Payment

s

Discount

Received

Cash Bank

Amount

(£)

Amou

nt (£)

Amou

nt (£)

Amount

(£)

Amou

nt (£)

Amou

nt (£)

2017

May 1

Balanc

e b/d

5,600 62,400 2017

May 1

Storage

cost

400

May

16

P.

Mulle

n

70 1,330 May 4 Motor

expenses

470

8

Date Particulars Amount (£)

2017

May 2 W. Tone 960

R. Foot 1,610

S. Hood 1,450

D. Main 2,060

May 22 L. Mole 1,830

W. Wright 1,910

9,820

PURCHASES RETURN DAY BOOK

Date Particulars

Amount

(£)

2017

May 11 R. Foot 50

50

CASHBOOK

Date Recei

pts

Discount

Allowed

Cash Bank Date Payment

s

Discount

Received

Cash Bank

Amount

(£)

Amou

nt (£)

Amou

nt (£)

Amount

(£)

Amou

nt (£)

Amou

nt (£)

2017

May 1

Balanc

e b/d

5,600 62,400 2017

May 1

Storage

cost

400

May

16

P.

Mulle

n

70 1,330 May 4 Motor

expenses

470

8

F.

Lane

155 2,945 May 7

Drawings

1500

J.

Wilso

n

43 807 May

24

S. Hood 360 3,240

F.

Syme

84 1,586 J. Brown 460 4,140

R. Foot 140 1,260

May

27

Salary 4,800

May

30

Business

rates

1,320

May

31

Abel

Motors

Ltd

20,500

May

31

Balance

c/d

3630 33,408

352 5,600 69,068 960 5,600 69,068

31

May

Balanc

e b/d

3630 33,408

DR P. Mullen Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017 2017

May 1

To balance brought

down 1400 May 16 By Discount allowed 70

May 16 By Cash 1330

1,400 1,400

F. Lane Account

9

Lane

155 2,945 May 7

Drawings

1500

J.

Wilso

n

43 807 May

24

S. Hood 360 3,240

F.

Syme

84 1,586 J. Brown 460 4,140

R. Foot 140 1,260

May

27

Salary 4,800

May

30

Business

rates

1,320

May

31

Abel

Motors

Ltd

20,500

May

31

Balance

c/d

3630 33,408

352 5,600 69,068 960 5,600 69,068

31

May

Balanc

e b/d

3630 33,408

DR P. Mullen Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017 2017

May 1

To balance brought

down 1400 May 16 By Discount allowed 70

May 16 By Cash 1330

1,400 1,400

F. Lane Account

9

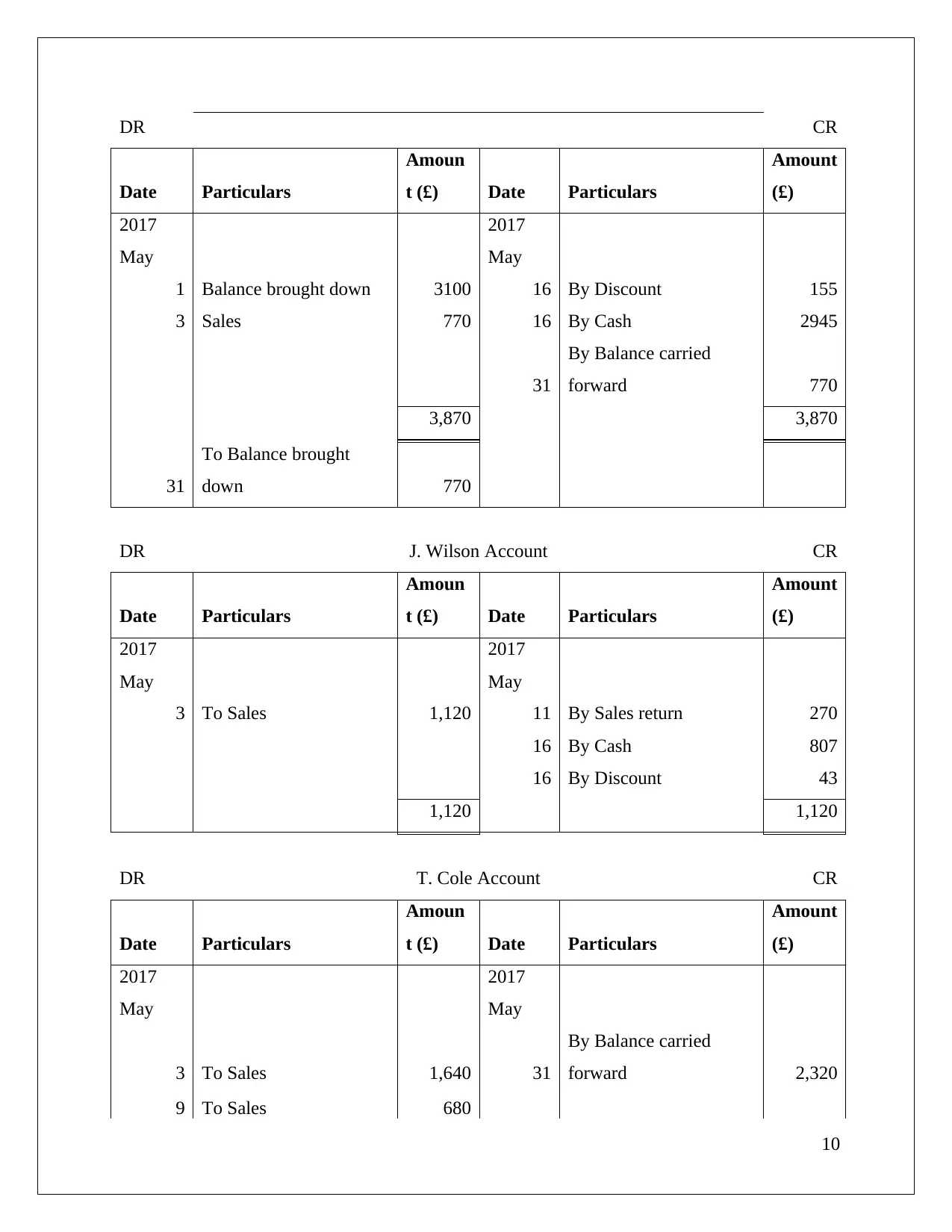

DR CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1 Balance brought down 3100 16 By Discount 155

3 Sales 770 16 By Cash 2945

31

By Balance carried

forward 770

3,870 3,870

31

To Balance brought

down 770

DR J. Wilson Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 1,120 11 By Sales return 270

16 By Cash 807

16 By Discount 43

1,120 1,120

DR T. Cole Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 1,640 31

By Balance carried

forward 2,320

9 To Sales 680

10

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1 Balance brought down 3100 16 By Discount 155

3 Sales 770 16 By Cash 2945

31

By Balance carried

forward 770

3,870 3,870

31

To Balance brought

down 770

DR J. Wilson Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 1,120 11 By Sales return 270

16 By Cash 807

16 By Discount 43

1,120 1,120

DR T. Cole Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 1,640 31

By Balance carried

forward 2,320

9 To Sales 680

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2,320 2,320

31

To Balance brought

down 2,320

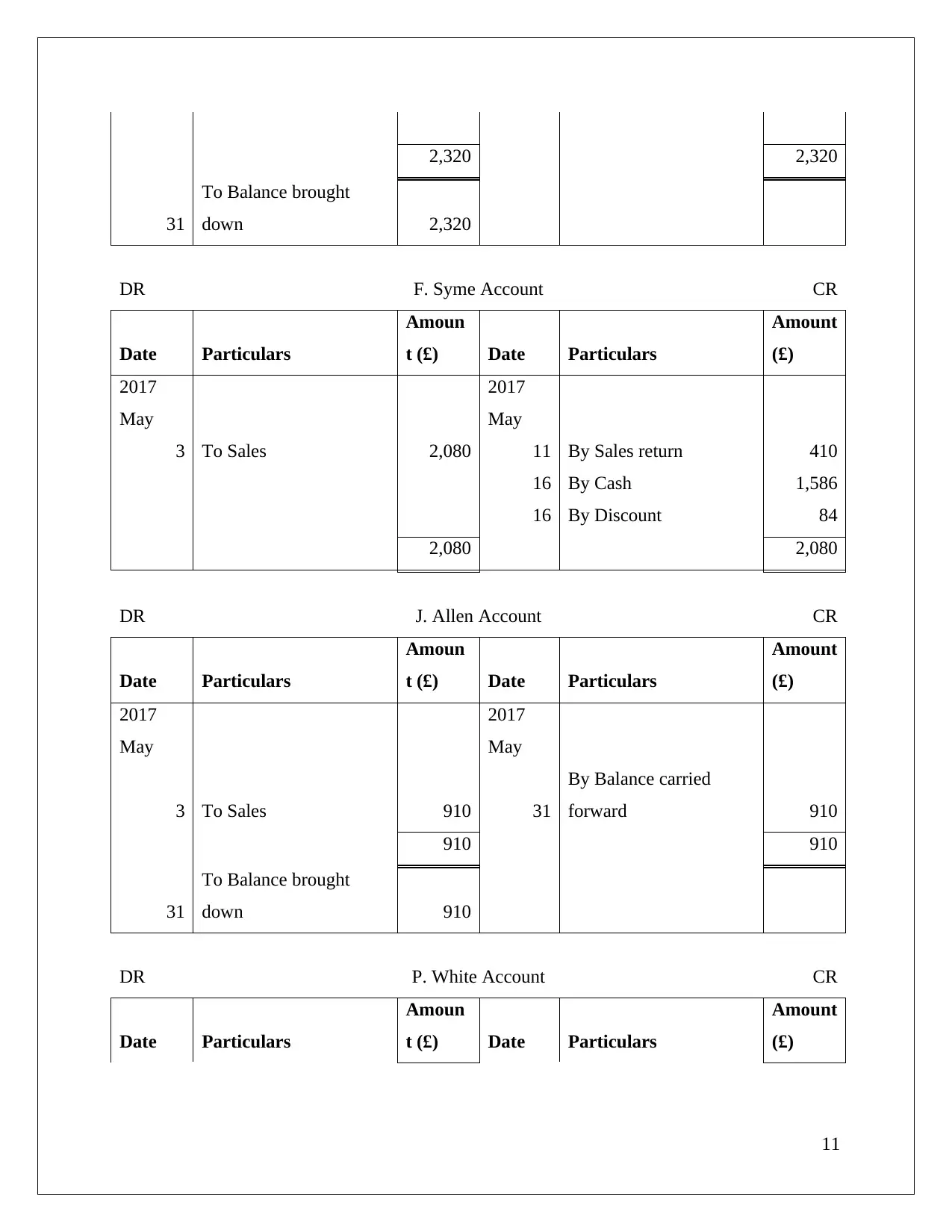

DR F. Syme Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 2,080 11 By Sales return 410

16 By Cash 1,586

16 By Discount 84

2,080 2,080

DR J. Allen Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 910 31

By Balance carried

forward 910

910 910

31

To Balance brought

down 910

DR P. White Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

11

31

To Balance brought

down 2,320

DR F. Syme Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 2,080 11 By Sales return 410

16 By Cash 1,586

16 By Discount 84

2,080 2,080

DR J. Allen Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 910 31

By Balance carried

forward 910

910 910

31

To Balance brought

down 910

DR P. White Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

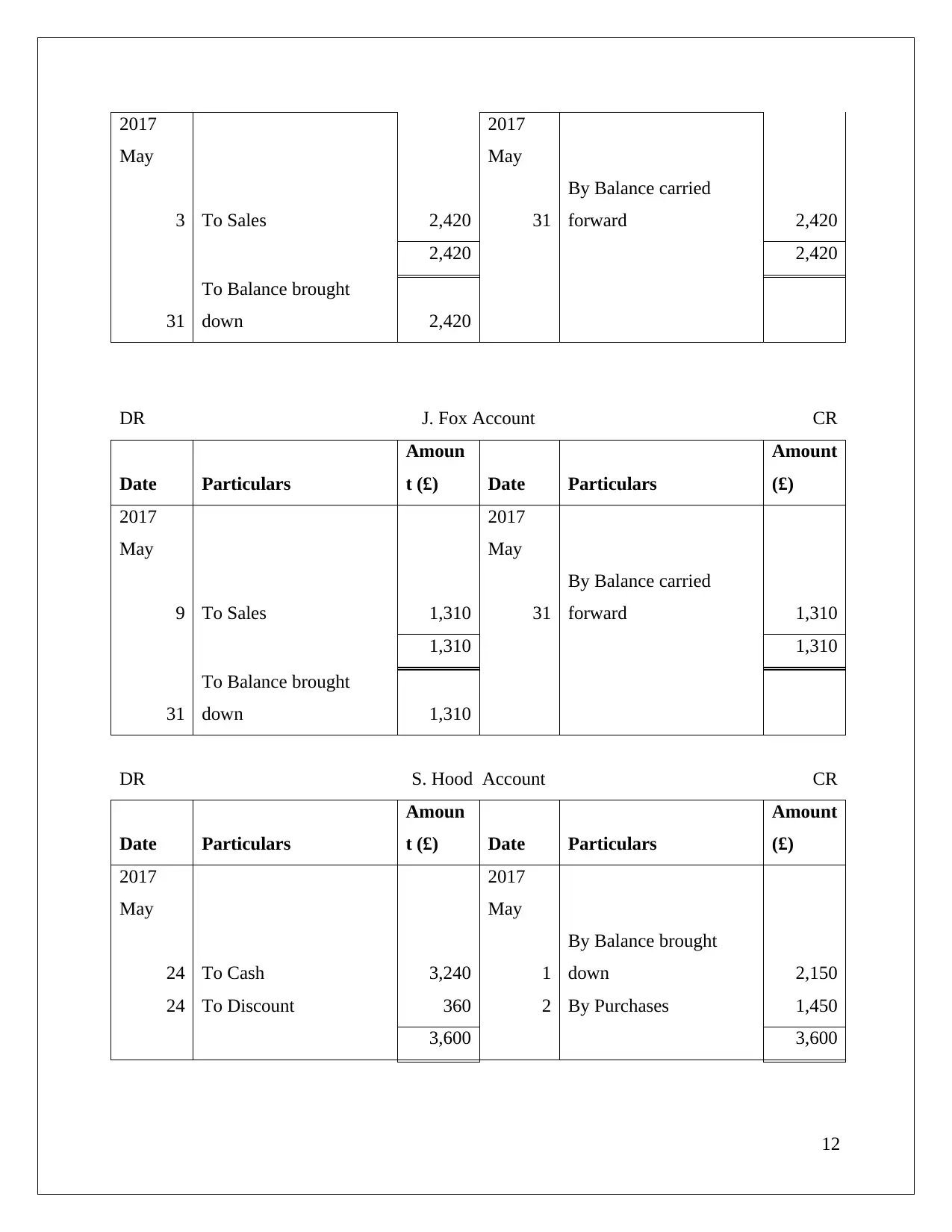

11

2017

May

2017

May

3 To Sales 2,420 31

By Balance carried

forward 2,420

2,420 2,420

31

To Balance brought

down 2,420

DR J. Fox Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

9 To Sales 1,310 31

By Balance carried

forward 1,310

1,310 1,310

31

To Balance brought

down 1,310

DR S. Hood Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

24 To Cash 3,240 1

By Balance brought

down 2,150

24 To Discount 360 2 By Purchases 1,450

3,600 3,600

12

May

2017

May

3 To Sales 2,420 31

By Balance carried

forward 2,420

2,420 2,420

31

To Balance brought

down 2,420

DR J. Fox Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

9 To Sales 1,310 31

By Balance carried

forward 1,310

1,310 1,310

31

To Balance brought

down 1,310

DR S. Hood Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

24 To Cash 3,240 1

By Balance brought

down 2,150

24 To Discount 360 2 By Purchases 1,450

3,600 3,600

12

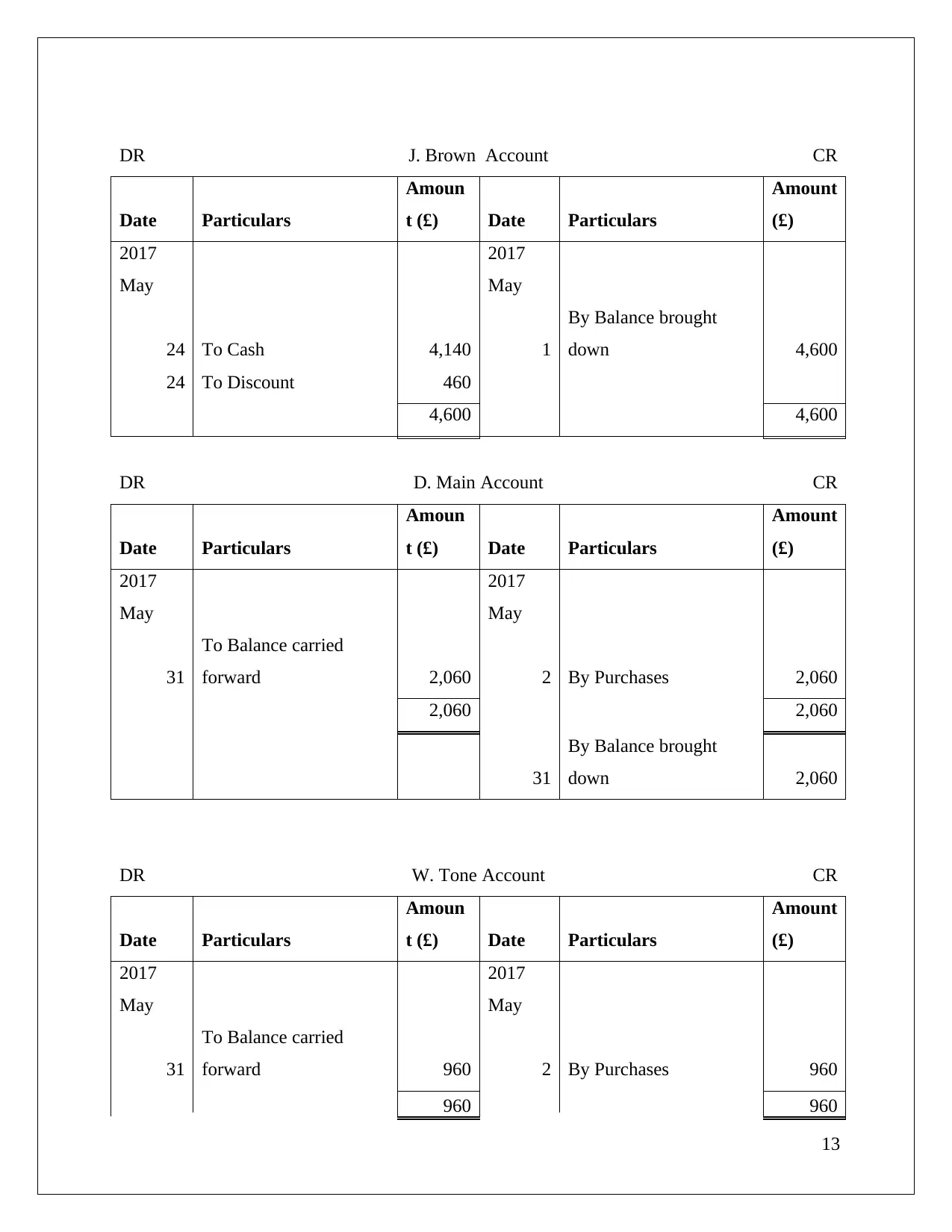

DR J. Brown Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

24 To Cash 4,140 1

By Balance brought

down 4,600

24 To Discount 460

4,600 4,600

DR D. Main Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 2,060 2 By Purchases 2,060

2,060 2,060

31

By Balance brought

down 2,060

DR W. Tone Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 960 2 By Purchases 960

960 960

13

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

24 To Cash 4,140 1

By Balance brought

down 4,600

24 To Discount 460

4,600 4,600

DR D. Main Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 2,060 2 By Purchases 2,060

2,060 2,060

31

By Balance brought

down 2,060

DR W. Tone Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 960 2 By Purchases 960

960 960

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31

By Balance brought

down 960

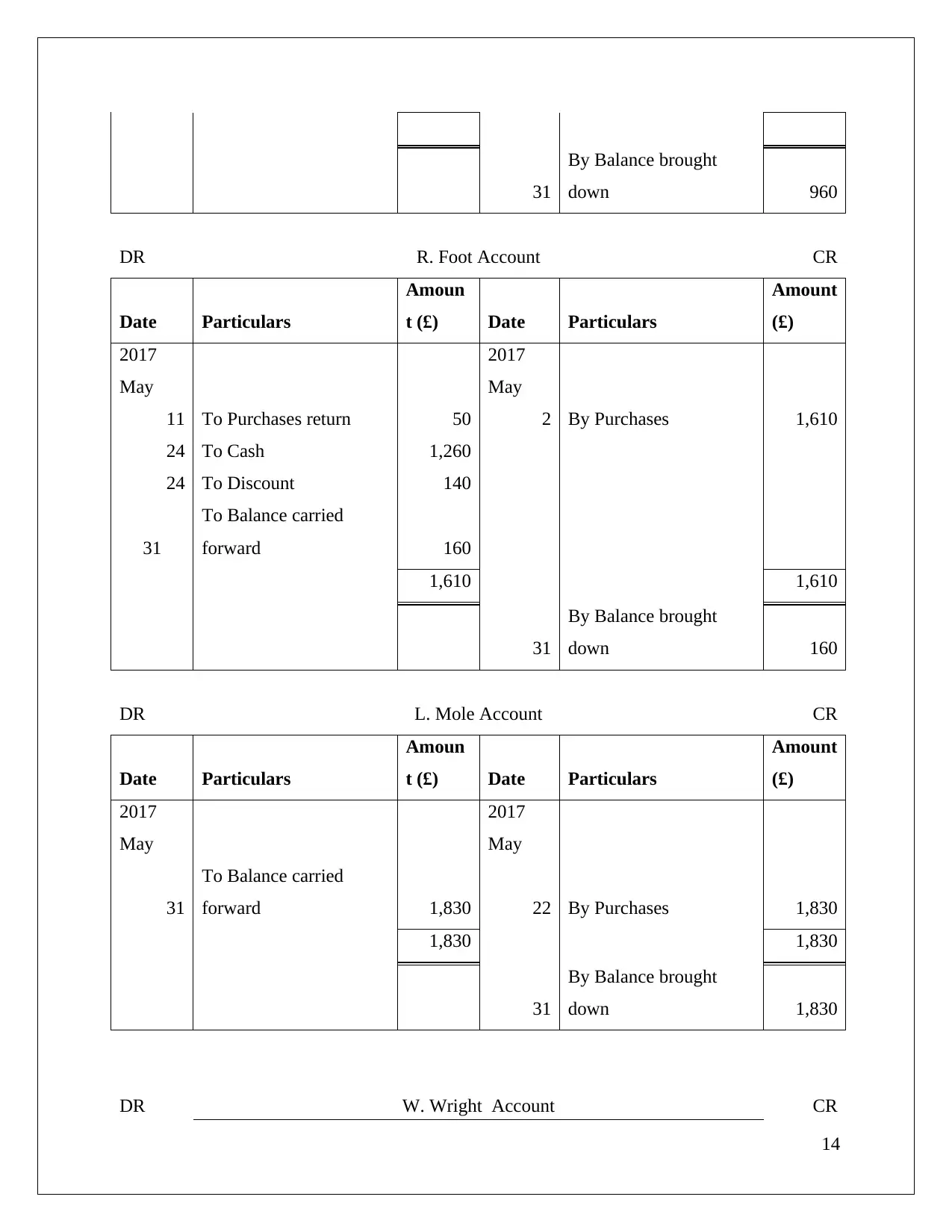

DR R. Foot Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

11 To Purchases return 50 2 By Purchases 1,610

24 To Cash 1,260

24 To Discount 140

31

To Balance carried

forward 160

1,610 1,610

31

By Balance brought

down 160

DR L. Mole Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 1,830 22 By Purchases 1,830

1,830 1,830

31

By Balance brought

down 1,830

DR W. Wright Account CR

14

By Balance brought

down 960

DR R. Foot Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

11 To Purchases return 50 2 By Purchases 1,610

24 To Cash 1,260

24 To Discount 140

31

To Balance carried

forward 160

1,610 1,610

31

By Balance brought

down 160

DR L. Mole Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 1,830 22 By Purchases 1,830

1,830 1,830

31

By Balance brought

down 1,830

DR W. Wright Account CR

14

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 1,910 22 By Purchases 1,910

1,910 1,910

31

By Balance brought

down 1,910

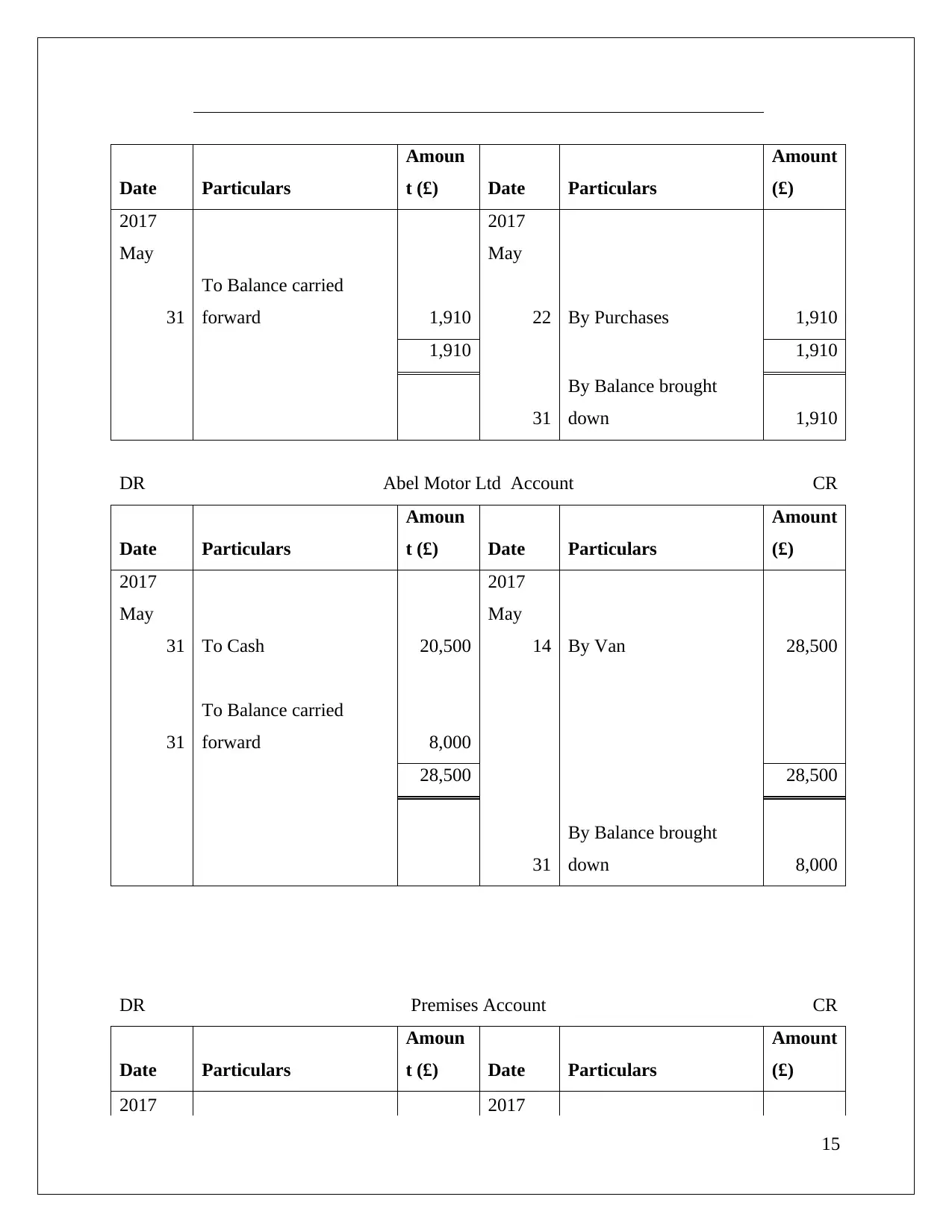

DR Abel Motor Ltd Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31 To Cash 20,500 14 By Van 28,500

31

To Balance carried

forward 8,000

28,500 28,500

31

By Balance brought

down 8,000

DR Premises Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017 2017

15

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 1,910 22 By Purchases 1,910

1,910 1,910

31

By Balance brought

down 1,910

DR Abel Motor Ltd Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31 To Cash 20,500 14 By Van 28,500

31

To Balance carried

forward 8,000

28,500 28,500

31

By Balance brought

down 8,000

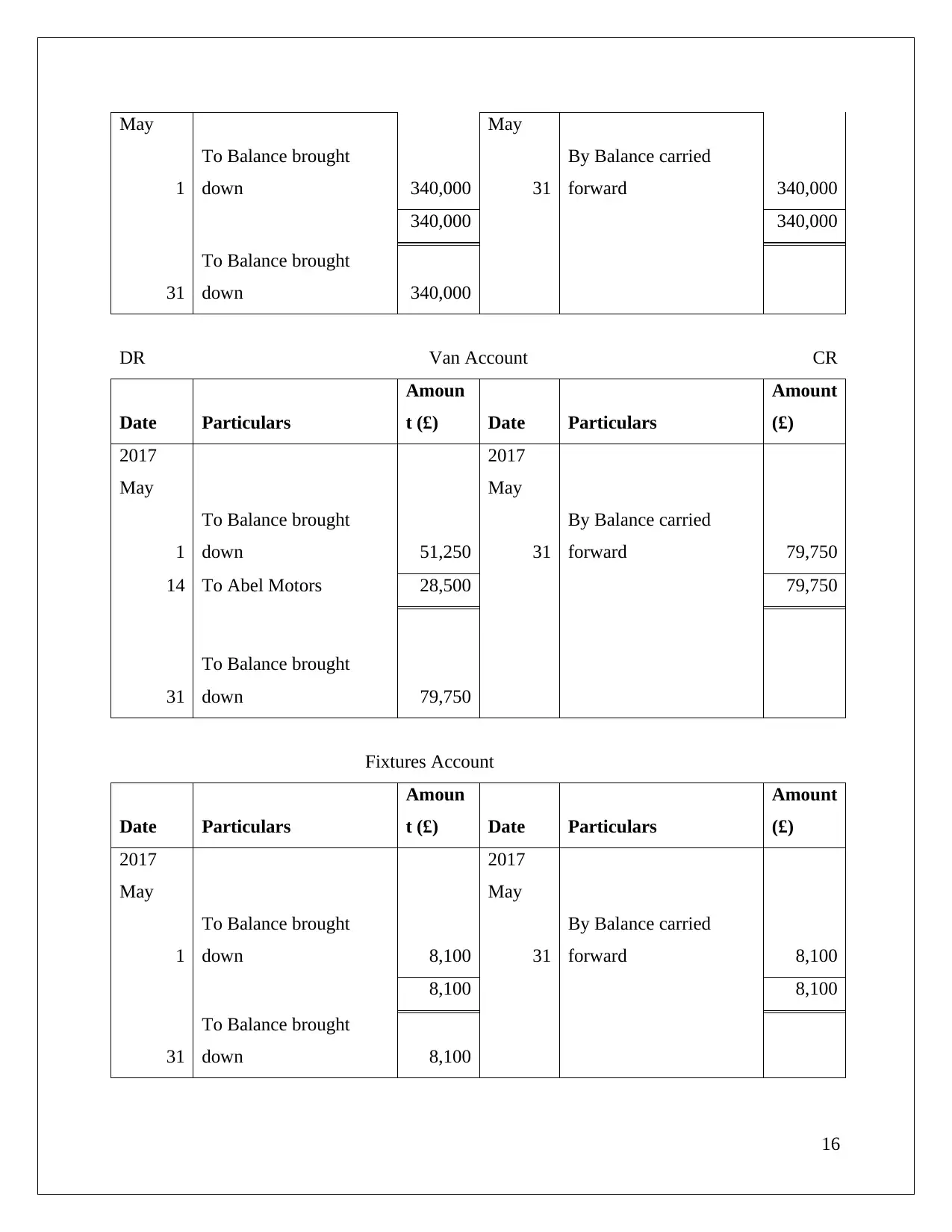

DR Premises Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017 2017

15

May May

1

To Balance brought

down 340,000 31

By Balance carried

forward 340,000

340,000 340,000

31

To Balance brought

down 340,000

DR Van Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1

To Balance brought

down 51,250 31

By Balance carried

forward 79,750

14 To Abel Motors 28,500 79,750

31

To Balance brought

down 79,750

Fixtures Account

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1

To Balance brought

down 8,100 31

By Balance carried

forward 8,100

8,100 8,100

31

To Balance brought

down 8,100

16

1

To Balance brought

down 340,000 31

By Balance carried

forward 340,000

340,000 340,000

31

To Balance brought

down 340,000

DR Van Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1

To Balance brought

down 51,250 31

By Balance carried

forward 79,750

14 To Abel Motors 28,500 79,750

31

To Balance brought

down 79,750

Fixtures Account

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1

To Balance brought

down 8,100 31

By Balance carried

forward 8,100

8,100 8,100

31

To Balance brought

down 8,100

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

DR Inventory Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1

To Balance brought

down 63,900 31

By Balance carried

forward 63,900

63,900 63,900

31

To Balance brought

down 63,900

DR Sales Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 10,930 31 By Sales day book 10,930

10,930 10,930

31

By Balance brought

down 10,930

DR Purchases Account CR

Date Particulars Amoun Date Particulars Amount

17

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1

To Balance brought

down 63,900 31

By Balance carried

forward 63,900

63,900 63,900

31

To Balance brought

down 63,900

DR Sales Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 10,930 31 By Sales day book 10,930

10,930 10,930

31

By Balance brought

down 10,930

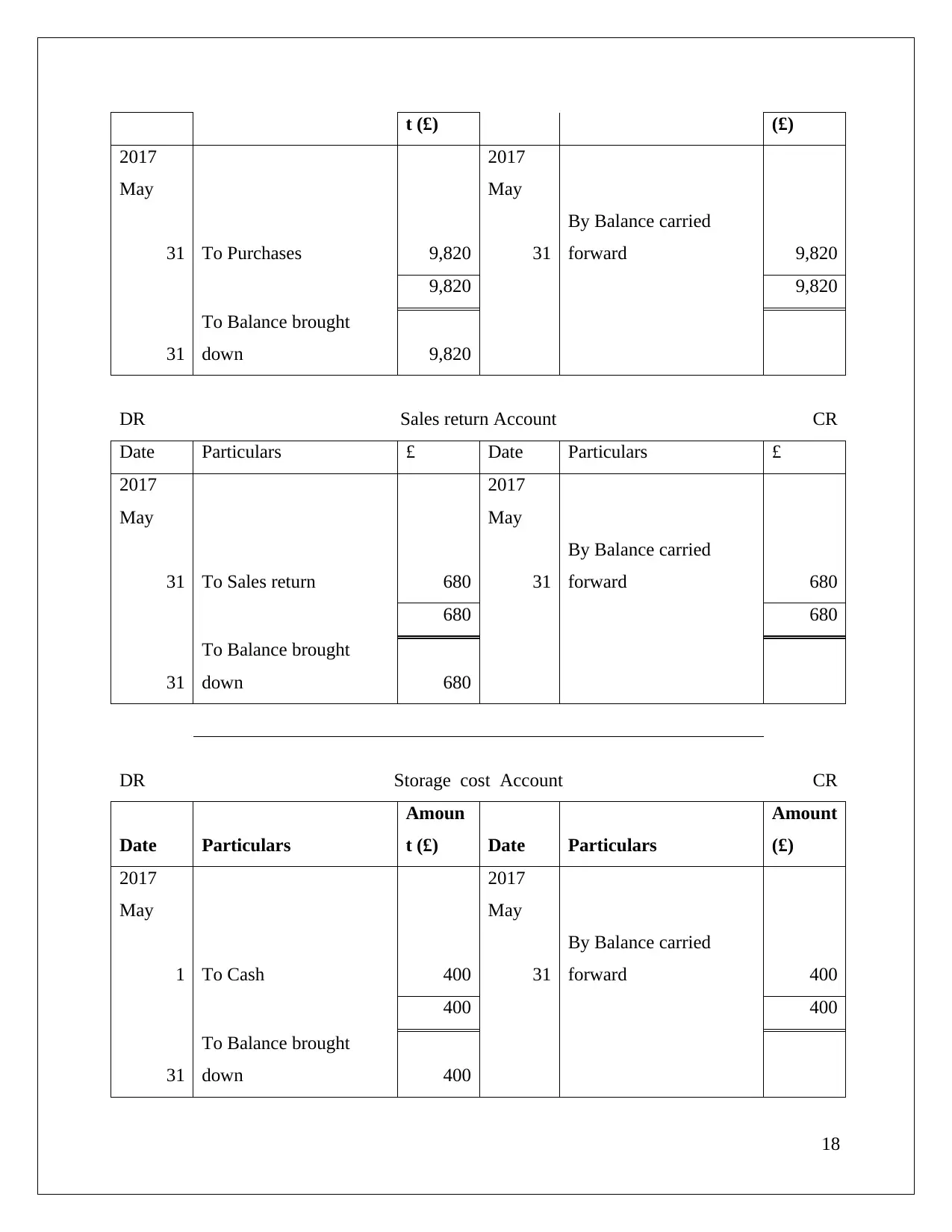

DR Purchases Account CR

Date Particulars Amoun Date Particulars Amount

17

t (£) (£)

2017

May

2017

May

31 To Purchases 9,820 31

By Balance carried

forward 9,820

9,820 9,820

31

To Balance brought

down 9,820

DR Sales return Account CR

Date Particulars £ Date Particulars £

2017

May

2017

May

31 To Sales return 680 31

By Balance carried

forward 680

680 680

31

To Balance brought

down 680

DR Storage cost Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1 To Cash 400 31

By Balance carried

forward 400

400 400

31

To Balance brought

down 400

18

2017

May

2017

May

31 To Purchases 9,820 31

By Balance carried

forward 9,820

9,820 9,820

31

To Balance brought

down 9,820

DR Sales return Account CR

Date Particulars £ Date Particulars £

2017

May

2017

May

31 To Sales return 680 31

By Balance carried

forward 680

680 680

31

To Balance brought

down 680

DR Storage cost Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1 To Cash 400 31

By Balance carried

forward 400

400 400

31

To Balance brought

down 400

18

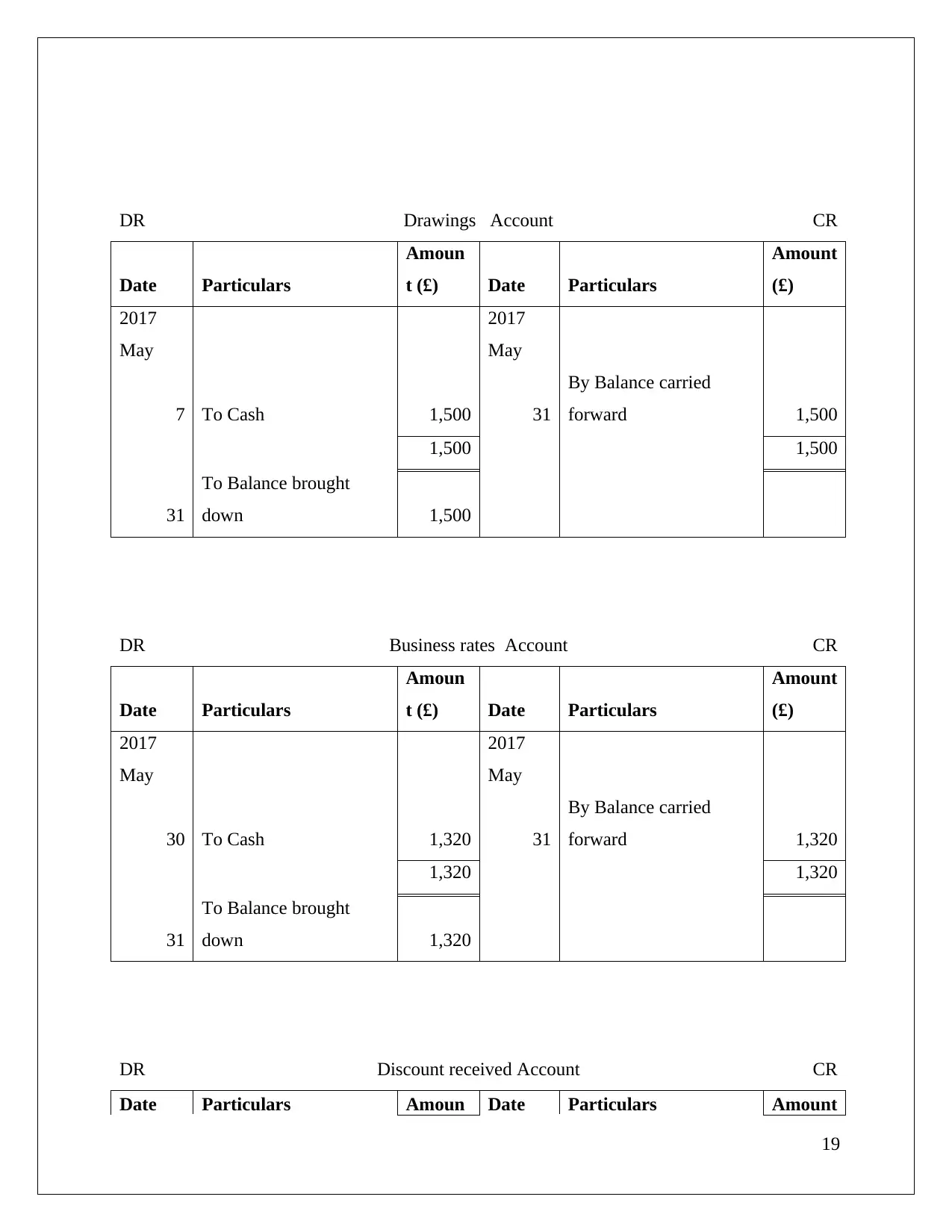

DR Drawings Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

7 To Cash 1,500 31

By Balance carried

forward 1,500

1,500 1,500

31

To Balance brought

down 1,500

DR Business rates Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

30 To Cash 1,320 31

By Balance carried

forward 1,320

1,320 1,320

31

To Balance brought

down 1,320

DR Discount received Account CR

Date Particulars Amoun Date Particulars Amount

19

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

7 To Cash 1,500 31

By Balance carried

forward 1,500

1,500 1,500

31

To Balance brought

down 1,500

DR Business rates Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

30 To Cash 1,320 31

By Balance carried

forward 1,320

1,320 1,320

31

To Balance brought

down 1,320

DR Discount received Account CR

Date Particulars Amoun Date Particulars Amount

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

t (£) (£)

2017

May

2017

May

31

To Balance carried

forward 960 31 By Cash 960

960 960

31

By Balance brought

down 960

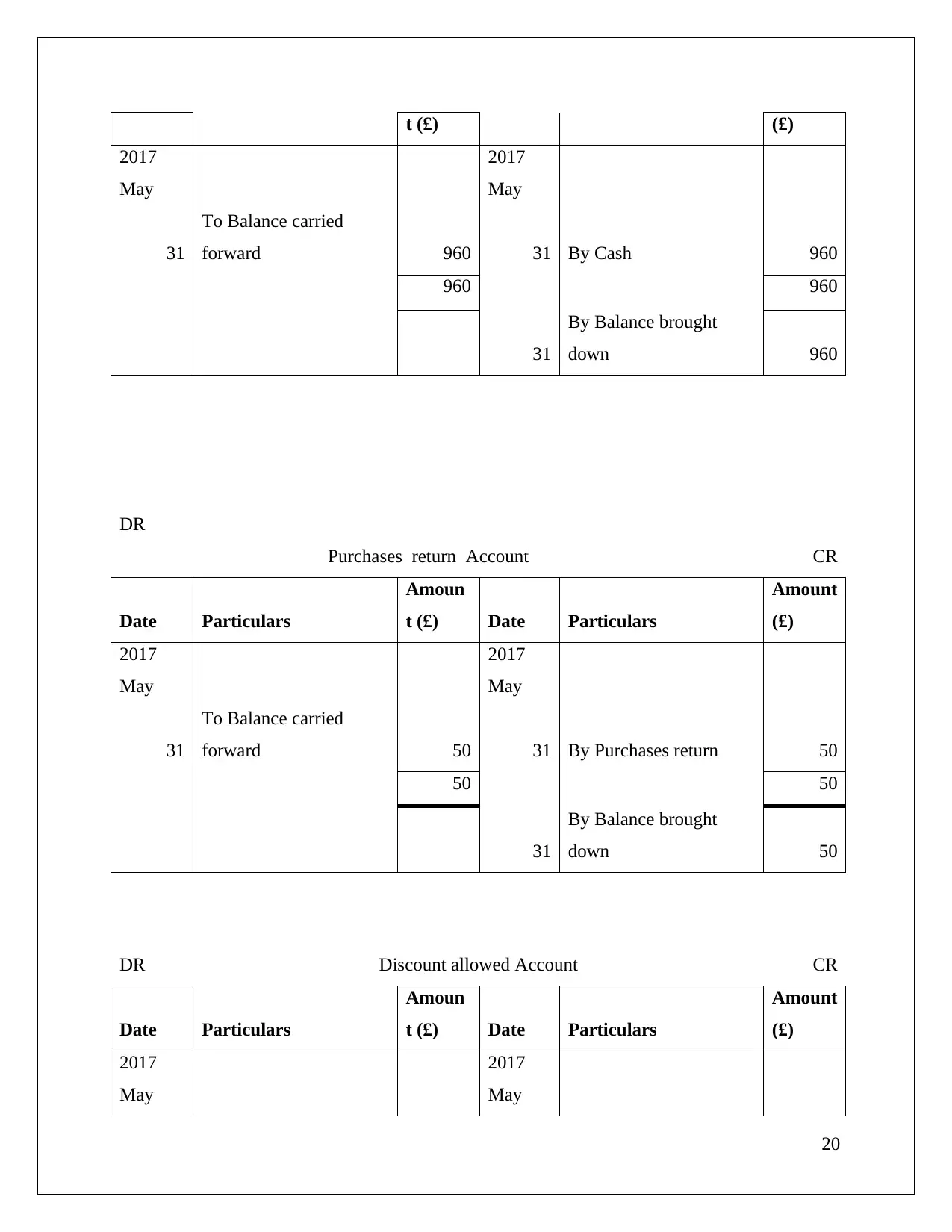

DR

Purchases return Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 50 31 By Purchases return 50

50 50

31

By Balance brought

down 50

DR Discount allowed Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

20

2017

May

2017

May

31

To Balance carried

forward 960 31 By Cash 960

960 960

31

By Balance brought

down 960

DR

Purchases return Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

31

To Balance carried

forward 50 31 By Purchases return 50

50 50

31

By Balance brought

down 50

DR Discount allowed Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

20

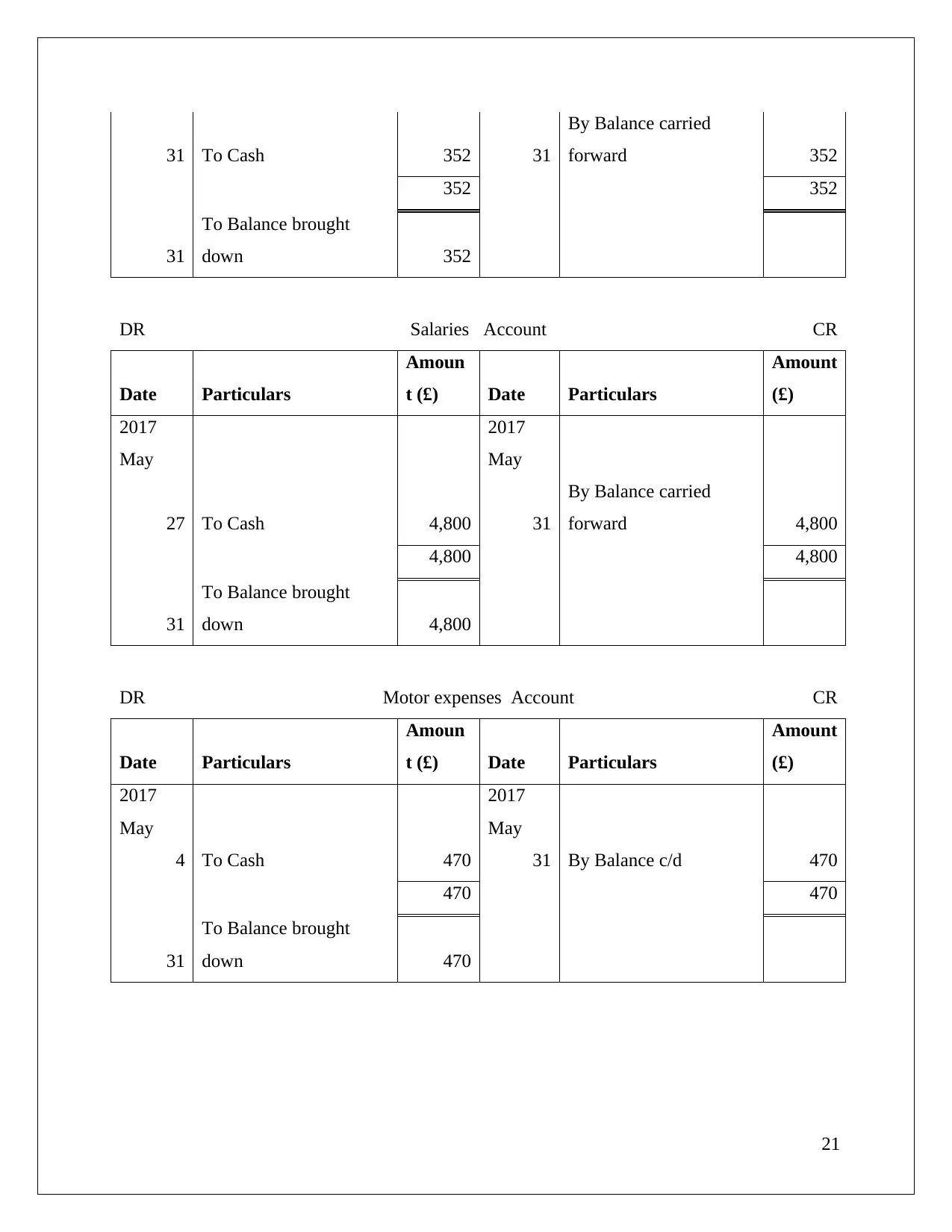

31 To Cash 352 31

By Balance carried

forward 352

352 352

31

To Balance brought

down 352

DR Salaries Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

27 To Cash 4,800 31

By Balance carried

forward 4,800

4,800 4,800

31

To Balance brought

down 4,800

DR Motor expenses Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

4 To Cash 470 31 By Balance c/d 470

470 470

31

To Balance brought

down 470

21

By Balance carried

forward 352

352 352

31

To Balance brought

down 352

DR Salaries Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

27 To Cash 4,800 31

By Balance carried

forward 4,800

4,800 4,800

31

To Balance brought

down 4,800

DR Motor expenses Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

4 To Cash 470 31 By Balance c/d 470

470 470

31

To Balance brought

down 470

21

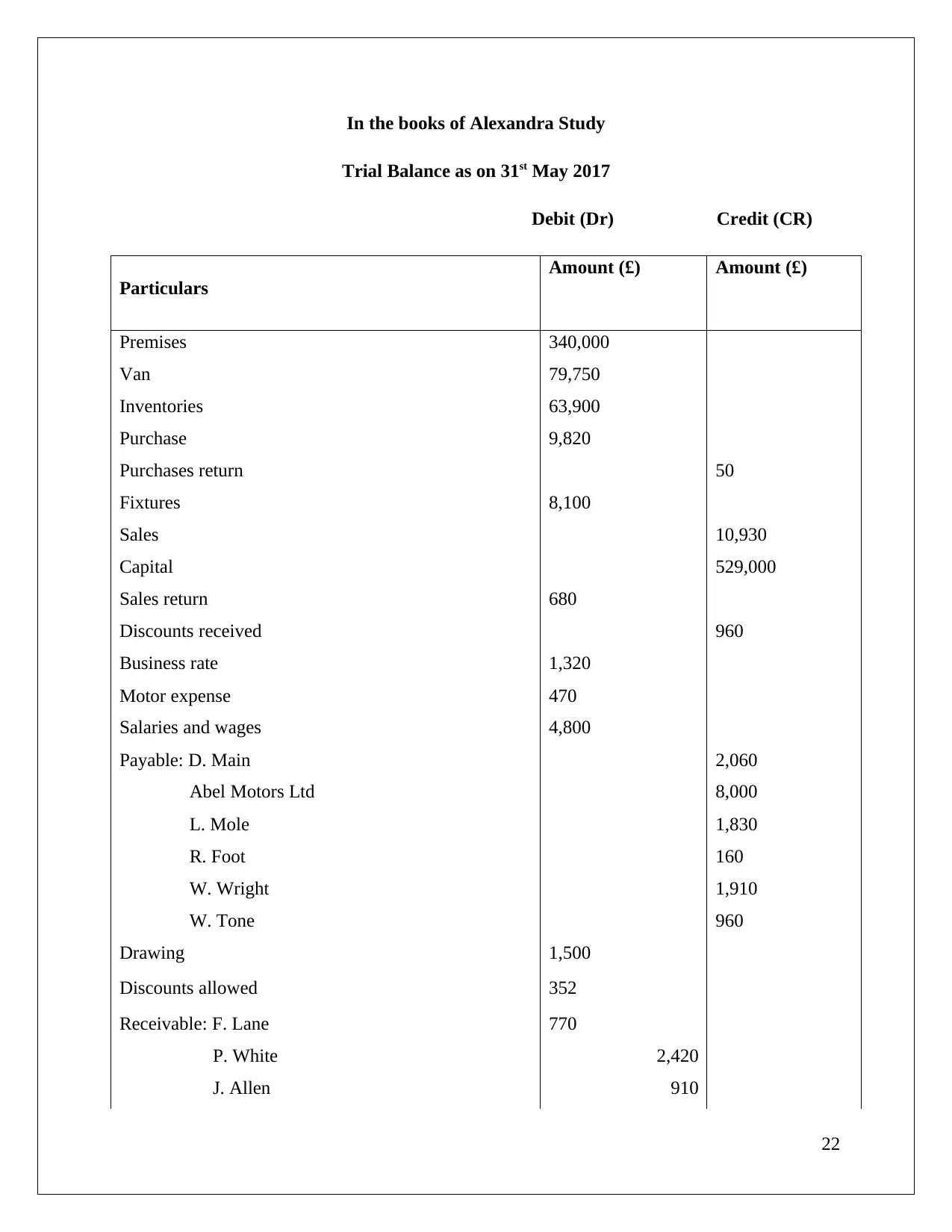

In the books of Alexandra Study

Trial Balance as on 31st May 2017

Debit (Dr) Credit (CR)

Particulars

Amount (£) Amount (£)

Premises 340,000

Van 79,750

Inventories 63,900

Purchase 9,820

Purchases return 50

Fixtures 8,100

Sales 10,930

Capital 529,000

Sales return 680

Discounts received 960

Business rate 1,320

Motor expense 470

Salaries and wages 4,800

Payable: D. Main 2,060

Abel Motors Ltd 8,000

L. Mole 1,830

R. Foot 160

W. Wright 1,910

W. Tone 960

Drawing 1,500

Discounts allowed 352

Receivable: F. Lane 770

P. White 2,420

J. Allen 910

22

Trial Balance as on 31st May 2017

Debit (Dr) Credit (CR)

Particulars

Amount (£) Amount (£)

Premises 340,000

Van 79,750

Inventories 63,900

Purchase 9,820

Purchases return 50

Fixtures 8,100

Sales 10,930

Capital 529,000

Sales return 680

Discounts received 960

Business rate 1,320

Motor expense 470

Salaries and wages 4,800

Payable: D. Main 2,060

Abel Motors Ltd 8,000

L. Mole 1,830

R. Foot 160

W. Wright 1,910

W. Tone 960

Drawing 1,500

Discounts allowed 352

Receivable: F. Lane 770

P. White 2,420

J. Allen 910

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

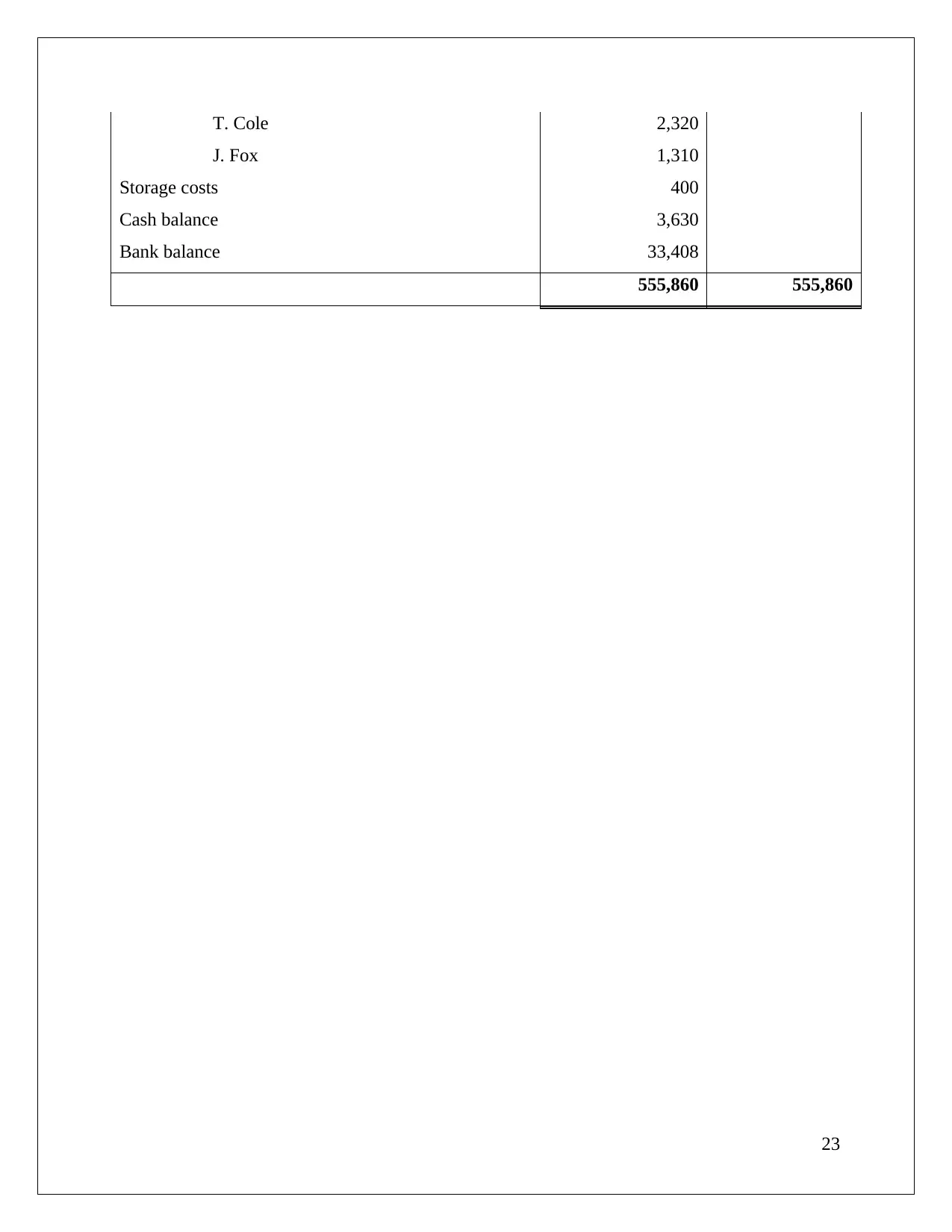

T. Cole 2,320

J. Fox 1,310

Storage costs 400

Cash balance 3,630

Bank balance 33,408

555,860 555,860

23

J. Fox 1,310

Storage costs 400

Cash balance 3,630

Bank balance 33,408

555,860 555,860

23

Client 2

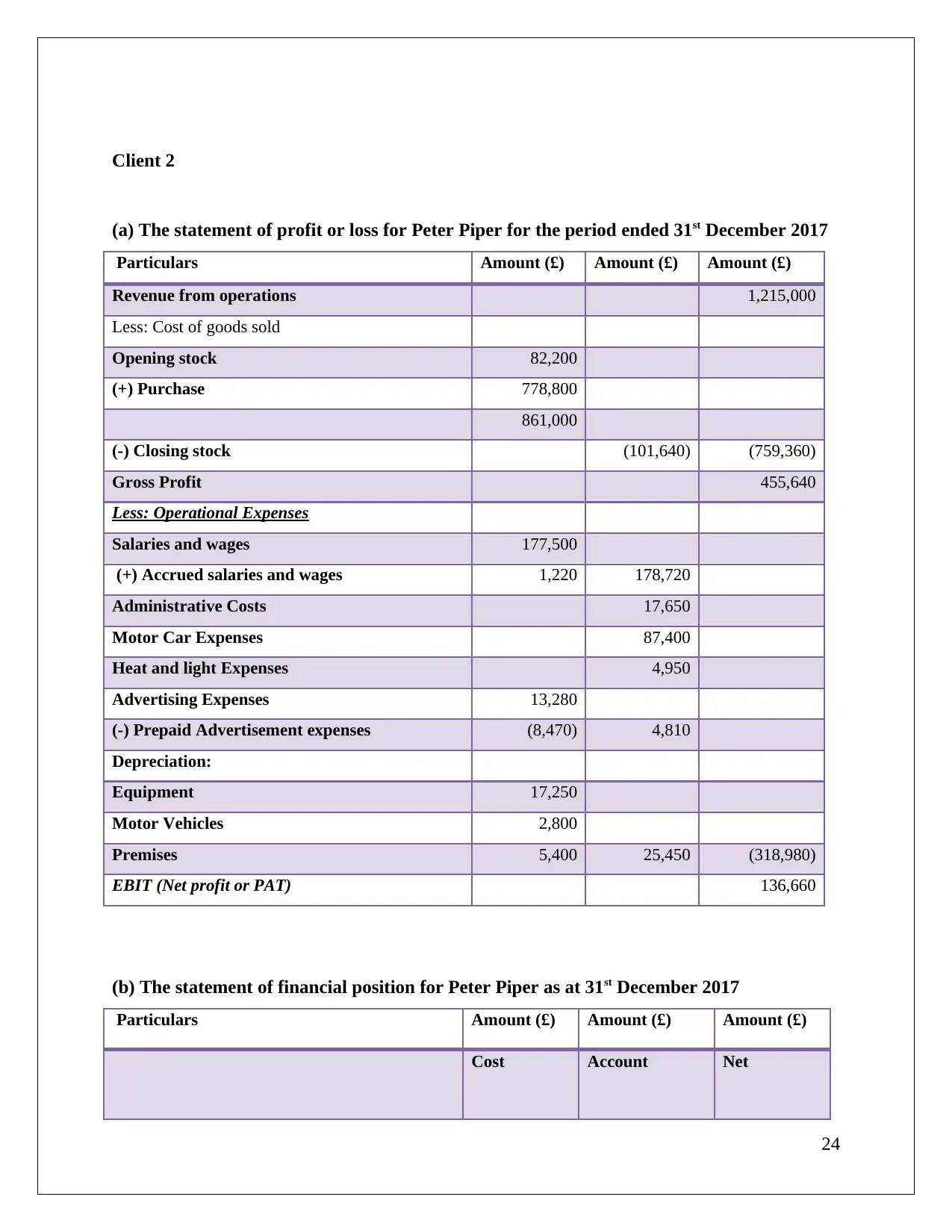

(a) The statement of profit or loss for Peter Piper for the period ended 31st December 2017

Particulars Amount (£) Amount (£) Amount (£)

Revenue from operations 1,215,000

Less: Cost of goods sold

Opening stock 82,200

(+) Purchase 778,800

861,000

(-) Closing stock (101,640) (759,360)

Gross Profit 455,640

Less: Operational Expenses

Salaries and wages 177,500

(+) Accrued salaries and wages 1,220 178,720

Administrative Costs 17,650

Motor Car Expenses 87,400

Heat and light Expenses 4,950

Advertising Expenses 13,280

(-) Prepaid Advertisement expenses (8,470) 4,810

Depreciation:

Equipment 17,250

Motor Vehicles 2,800

Premises 5,400 25,450 (318,980)

EBIT (Net profit or PAT) 136,660

(b) The statement of financial position for Peter Piper as at 31st December 2017

Particulars Amount (£) Amount (£) Amount (£)

Cost Account Net

24

(a) The statement of profit or loss for Peter Piper for the period ended 31st December 2017

Particulars Amount (£) Amount (£) Amount (£)

Revenue from operations 1,215,000

Less: Cost of goods sold

Opening stock 82,200

(+) Purchase 778,800

861,000

(-) Closing stock (101,640) (759,360)

Gross Profit 455,640

Less: Operational Expenses

Salaries and wages 177,500

(+) Accrued salaries and wages 1,220 178,720

Administrative Costs 17,650

Motor Car Expenses 87,400

Heat and light Expenses 4,950

Advertising Expenses 13,280

(-) Prepaid Advertisement expenses (8,470) 4,810

Depreciation:

Equipment 17,250

Motor Vehicles 2,800

Premises 5,400 25,450 (318,980)

EBIT (Net profit or PAT) 136,660

(b) The statement of financial position for Peter Piper as at 31st December 2017

Particulars Amount (£) Amount (£) Amount (£)

Cost Account Net

24

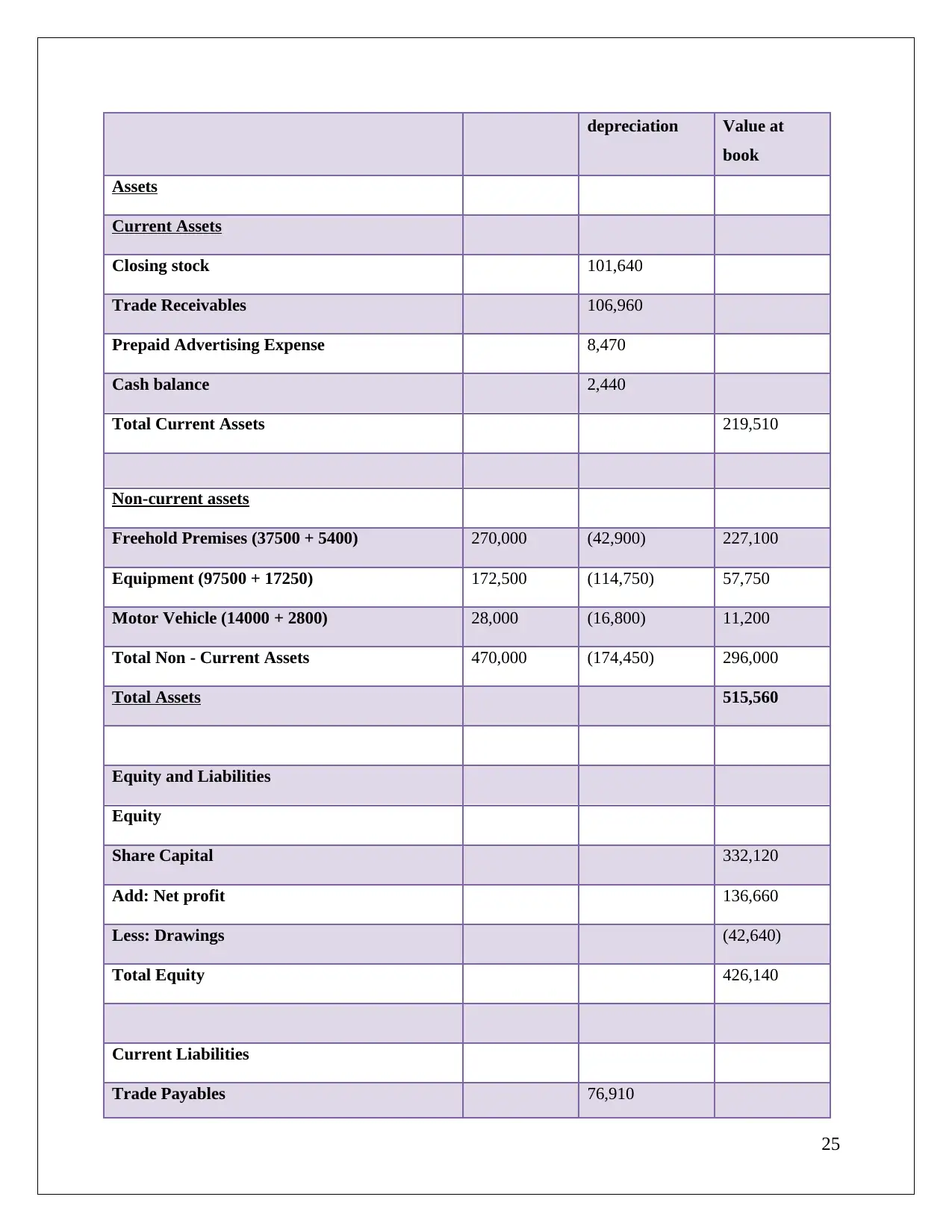

depreciation Value at

book

Assets

Current Assets

Closing stock 101,640

Trade Receivables 106,960

Prepaid Advertising Expense 8,470

Cash balance 2,440

Total Current Assets 219,510

Non-current assets

Freehold Premises (37500 + 5400) 270,000 (42,900) 227,100

Equipment (97500 + 17250) 172,500 (114,750) 57,750

Motor Vehicle (14000 + 2800) 28,000 (16,800) 11,200

Total Non - Current Assets 470,000 (174,450) 296,000

Total Assets 515,560

Equity and Liabilities

Equity

Share Capital 332,120

Add: Net profit 136,660

Less: Drawings (42,640)

Total Equity 426,140

Current Liabilities

Trade Payables 76,910

25

book

Assets

Current Assets

Closing stock 101,640

Trade Receivables 106,960

Prepaid Advertising Expense 8,470

Cash balance 2,440

Total Current Assets 219,510

Non-current assets

Freehold Premises (37500 + 5400) 270,000 (42,900) 227,100

Equipment (97500 + 17250) 172,500 (114,750) 57,750

Motor Vehicle (14000 + 2800) 28,000 (16,800) 11,200

Total Non - Current Assets 470,000 (174,450) 296,000

Total Assets 515,560

Equity and Liabilities

Equity

Share Capital 332,120

Add: Net profit 136,660

Less: Drawings (42,640)

Total Equity 426,140

Current Liabilities

Trade Payables 76,910

25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

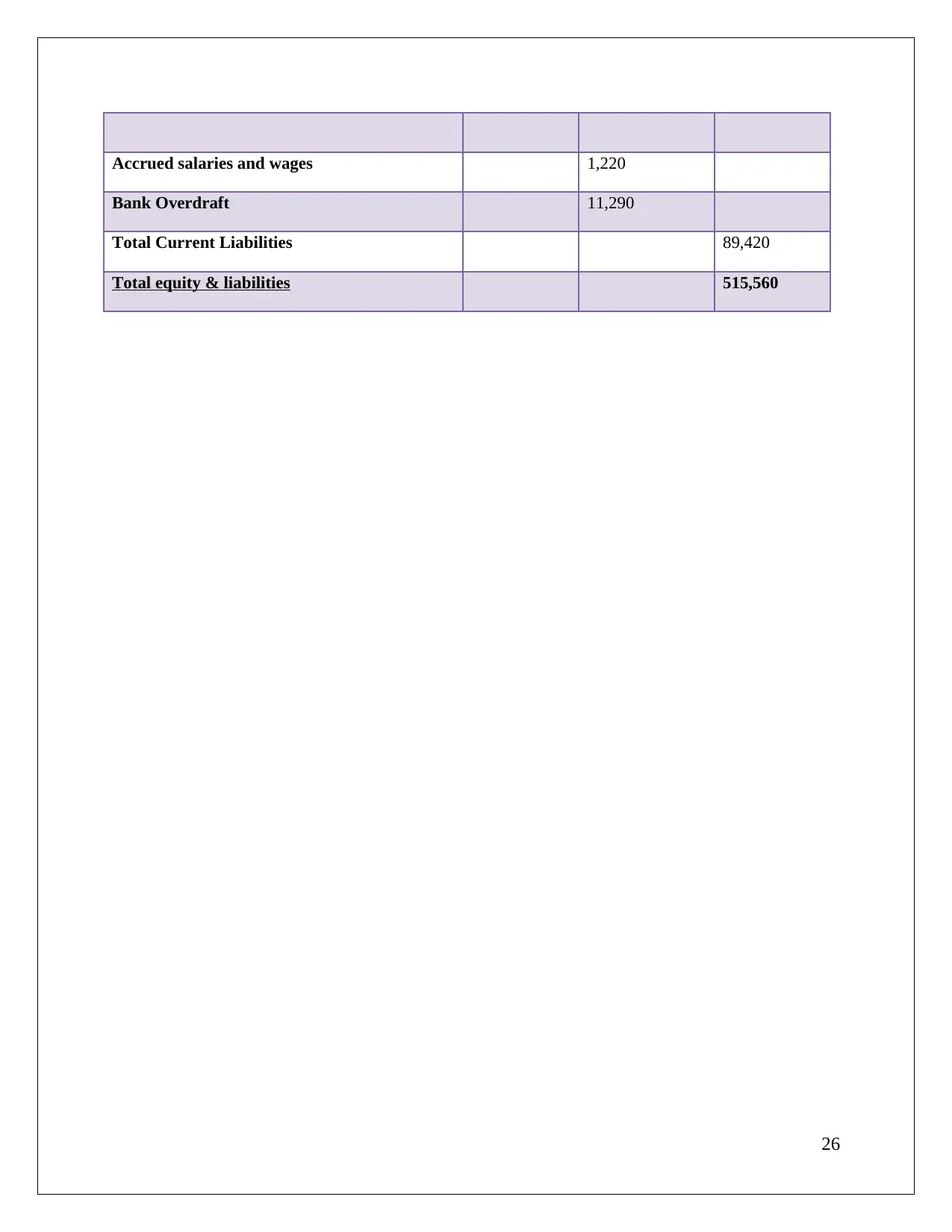

Accrued salaries and wages 1,220

Bank Overdraft 11,290

Total Current Liabilities 89,420

Total equity & liabilities 515,560

26

Bank Overdraft 11,290

Total Current Liabilities 89,420

Total equity & liabilities 515,560

26

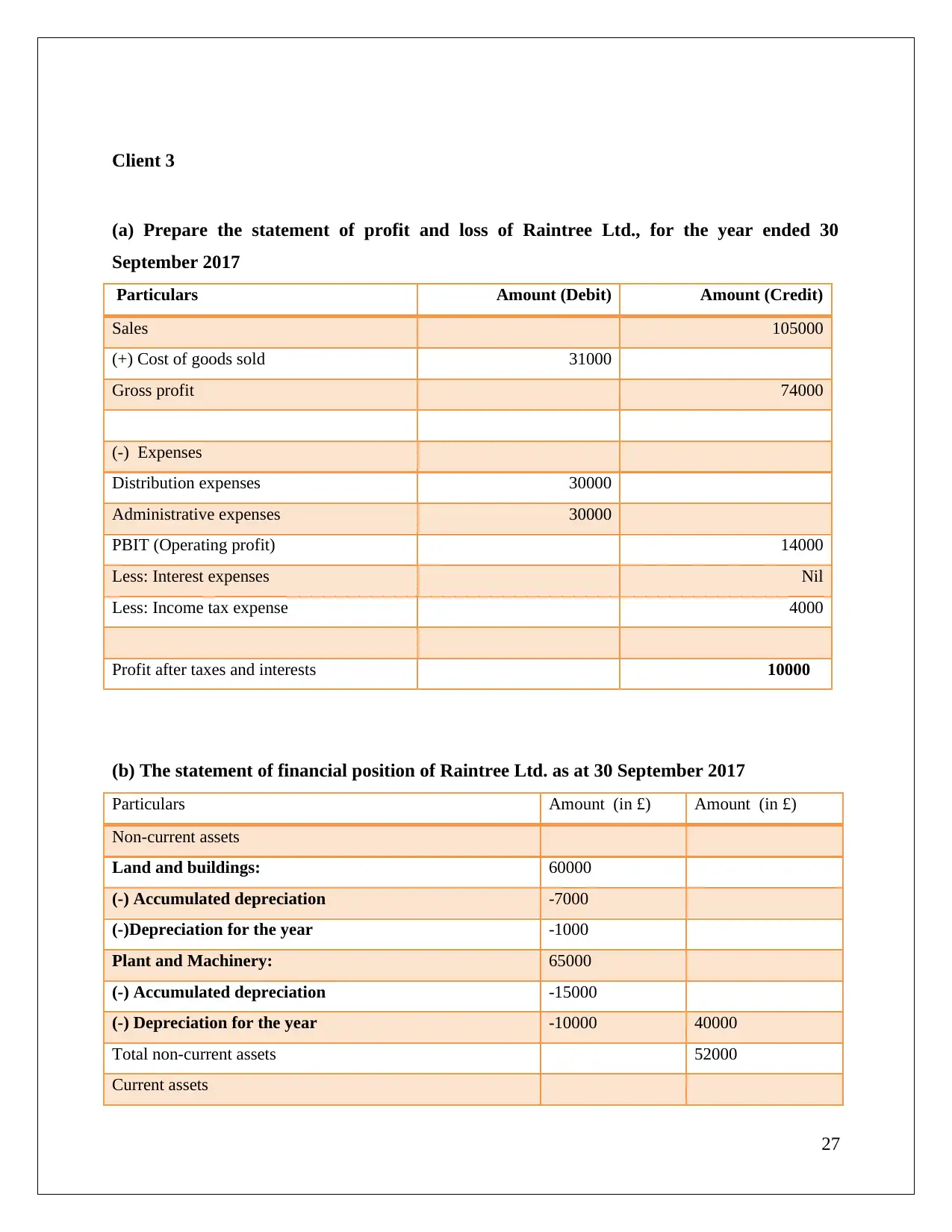

Client 3

(a) Prepare the statement of profit and loss of Raintree Ltd., for the year ended 30

September 2017

Particulars Amount (Debit) Amount (Credit)

Sales 105000

(+) Cost of goods sold 31000

Gross profit 74000

(-) Expenses

Distribution expenses 30000

Administrative expenses 30000

PBIT (Operating profit) 14000

Less: Interest expenses Nil

Less: Income tax expense 4000

Profit after taxes and interests 10000

(b) The statement of financial position of Raintree Ltd. as at 30 September 2017

Particulars Amount (in £) Amount (in £)

Non-current assets

Land and buildings: 60000

(-) Accumulated depreciation -7000

(-)Depreciation for the year -1000

Plant and Machinery: 65000

(-) Accumulated depreciation -15000

(-) Depreciation for the year -10000 40000

Total non-current assets 52000

Current assets

27

(a) Prepare the statement of profit and loss of Raintree Ltd., for the year ended 30

September 2017

Particulars Amount (Debit) Amount (Credit)

Sales 105000

(+) Cost of goods sold 31000

Gross profit 74000

(-) Expenses

Distribution expenses 30000

Administrative expenses 30000

PBIT (Operating profit) 14000

Less: Interest expenses Nil

Less: Income tax expense 4000

Profit after taxes and interests 10000

(b) The statement of financial position of Raintree Ltd. as at 30 September 2017

Particulars Amount (in £) Amount (in £)

Non-current assets

Land and buildings: 60000

(-) Accumulated depreciation -7000

(-)Depreciation for the year -1000

Plant and Machinery: 65000

(-) Accumulated depreciation -15000

(-) Depreciation for the year -10000 40000

Total non-current assets 52000

Current assets

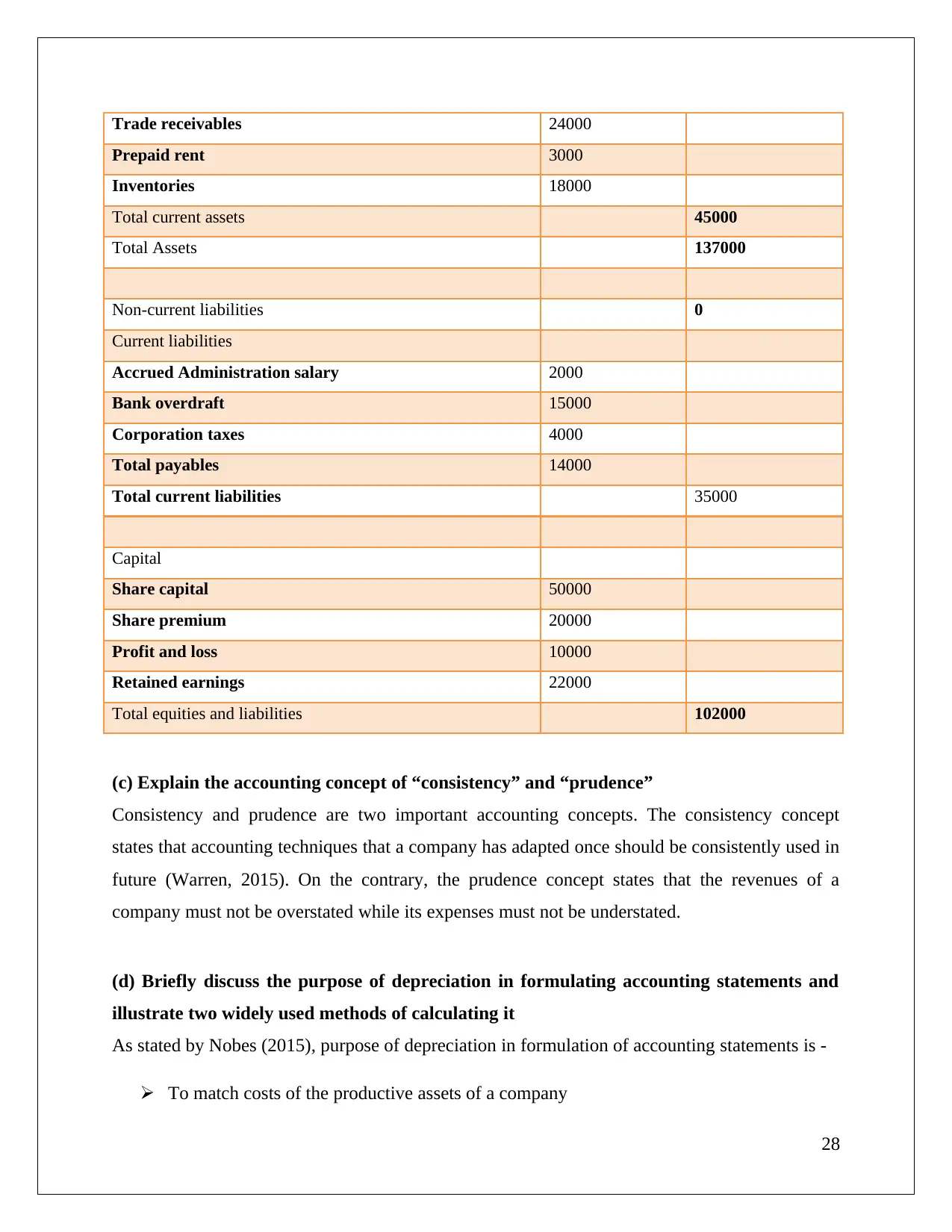

27

Trade receivables 24000

Prepaid rent 3000

Inventories 18000

Total current assets 45000

Total Assets 137000

Non-current liabilities 0

Current liabilities

Accrued Administration salary 2000

Bank overdraft 15000

Corporation taxes 4000

Total payables 14000

Total current liabilities 35000

Capital

Share capital 50000

Share premium 20000

Profit and loss 10000

Retained earnings 22000

Total equities and liabilities 102000

(c) Explain the accounting concept of “consistency” and “prudence”

Consistency and prudence are two important accounting concepts. The consistency concept

states that accounting techniques that a company has adapted once should be consistently used in

future (Warren, 2015). On the contrary, the prudence concept states that the revenues of a

company must not be overstated while its expenses must not be understated.

(d) Briefly discuss the purpose of depreciation in formulating accounting statements and

illustrate two widely used methods of calculating it

As stated by Nobes (2015), purpose of depreciation in formulation of accounting statements is -

To match costs of the productive assets of a company

28

Prepaid rent 3000

Inventories 18000

Total current assets 45000

Total Assets 137000

Non-current liabilities 0

Current liabilities

Accrued Administration salary 2000

Bank overdraft 15000

Corporation taxes 4000

Total payables 14000

Total current liabilities 35000

Capital

Share capital 50000

Share premium 20000

Profit and loss 10000

Retained earnings 22000

Total equities and liabilities 102000

(c) Explain the accounting concept of “consistency” and “prudence”

Consistency and prudence are two important accounting concepts. The consistency concept

states that accounting techniques that a company has adapted once should be consistently used in

future (Warren, 2015). On the contrary, the prudence concept states that the revenues of a

company must not be overstated while its expenses must not be understated.

(d) Briefly discuss the purpose of depreciation in formulating accounting statements and

illustrate two widely used methods of calculating it

As stated by Nobes (2015), purpose of depreciation in formulation of accounting statements is -

To match costs of the productive assets of a company

28

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

To determine the correct value of assets after physical wear and tear

To determine a company’s correct financial position

To recognize a company’s actual asset value

29

To determine a company’s correct financial position

To recognize a company’s actual asset value

29

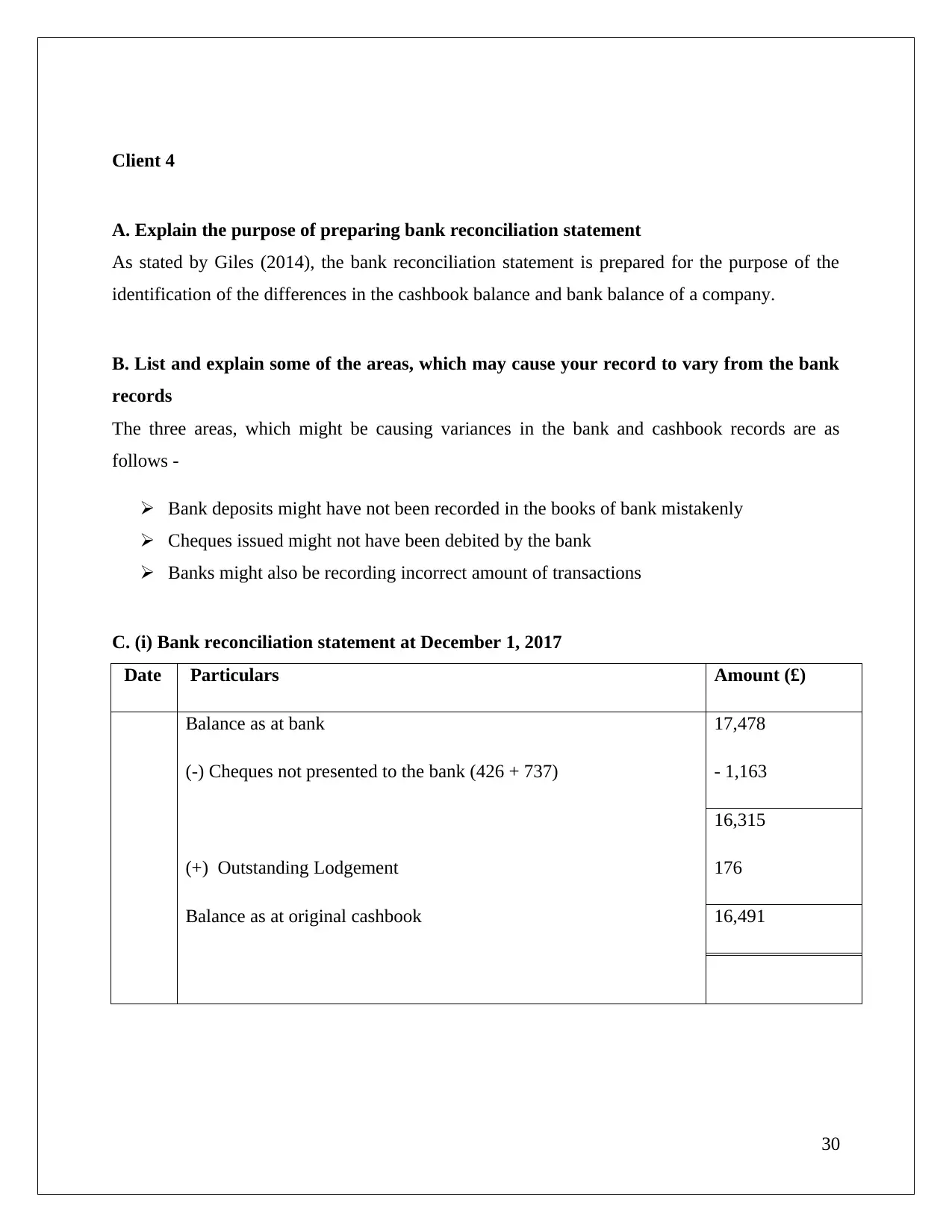

Client 4

A. Explain the purpose of preparing bank reconciliation statement

As stated by Giles (2014), the bank reconciliation statement is prepared for the purpose of the

identification of the differences in the cashbook balance and bank balance of a company.

B. List and explain some of the areas, which may cause your record to vary from the bank

records

The three areas, which might be causing variances in the bank and cashbook records are as

follows -

Bank deposits might have not been recorded in the books of bank mistakenly

Cheques issued might not have been debited by the bank

Banks might also be recording incorrect amount of transactions

C. (i) Bank reconciliation statement at December 1, 2017

Date Particulars Amount (£)

Balance as at bank 17,478

(-) Cheques not presented to the bank (426 + 737) - 1,163

16,315

(+) Outstanding Lodgement 176

Balance as at original cashbook 16,491

30

A. Explain the purpose of preparing bank reconciliation statement

As stated by Giles (2014), the bank reconciliation statement is prepared for the purpose of the

identification of the differences in the cashbook balance and bank balance of a company.

B. List and explain some of the areas, which may cause your record to vary from the bank

records

The three areas, which might be causing variances in the bank and cashbook records are as

follows -

Bank deposits might have not been recorded in the books of bank mistakenly

Cheques issued might not have been debited by the bank

Banks might also be recording incorrect amount of transactions

C. (i) Bank reconciliation statement at December 1, 2017

Date Particulars Amount (£)

Balance as at bank 17,478

(-) Cheques not presented to the bank (426 + 737) - 1,163

16,315

(+) Outstanding Lodgement 176

Balance as at original cashbook 16,491

30

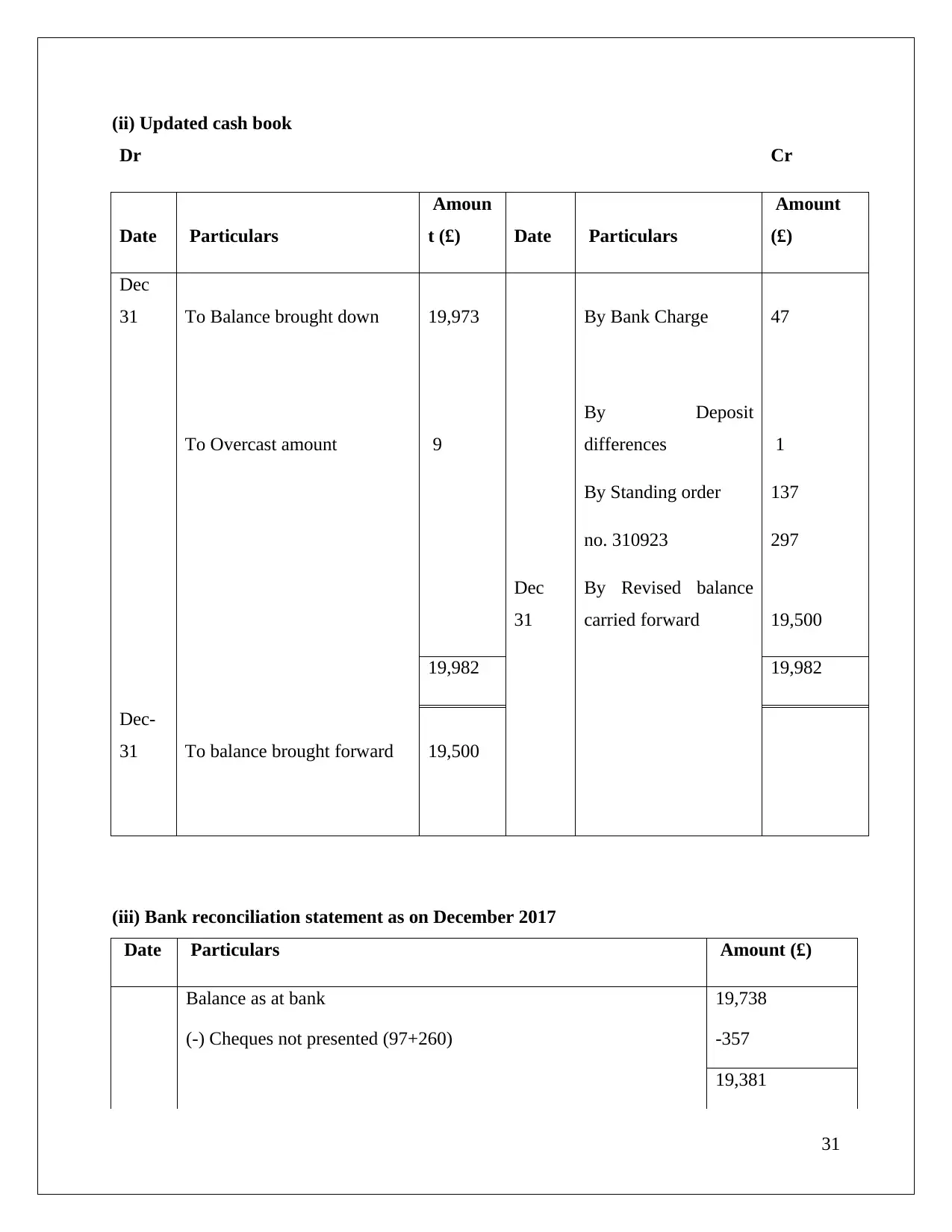

(ii) Updated cash book

Dr Cr

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

Dec

31 To Balance brought down 19,973 By Bank Charge 47

To Overcast amount 9

By Deposit

differences 1

By Standing order 137

no. 310923 297

Dec

31

By Revised balance

carried forward 19,500

19,982 19,982

Dec-

31 To balance brought forward 19,500

(iii) Bank reconciliation statement as on December 2017

Date Particulars Amount (£)

Balance as at bank 19,738

(-) Cheques not presented (97+260) -357

19,381

31

Dr Cr

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

Dec

31 To Balance brought down 19,973 By Bank Charge 47

To Overcast amount 9

By Deposit

differences 1

By Standing order 137

no. 310923 297

Dec

31

By Revised balance

carried forward 19,500

19,982 19,982

Dec-

31 To balance brought forward 19,500

(iii) Bank reconciliation statement as on December 2017

Date Particulars Amount (£)

Balance as at bank 19,738

(-) Cheques not presented (97+260) -357

19,381

31

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

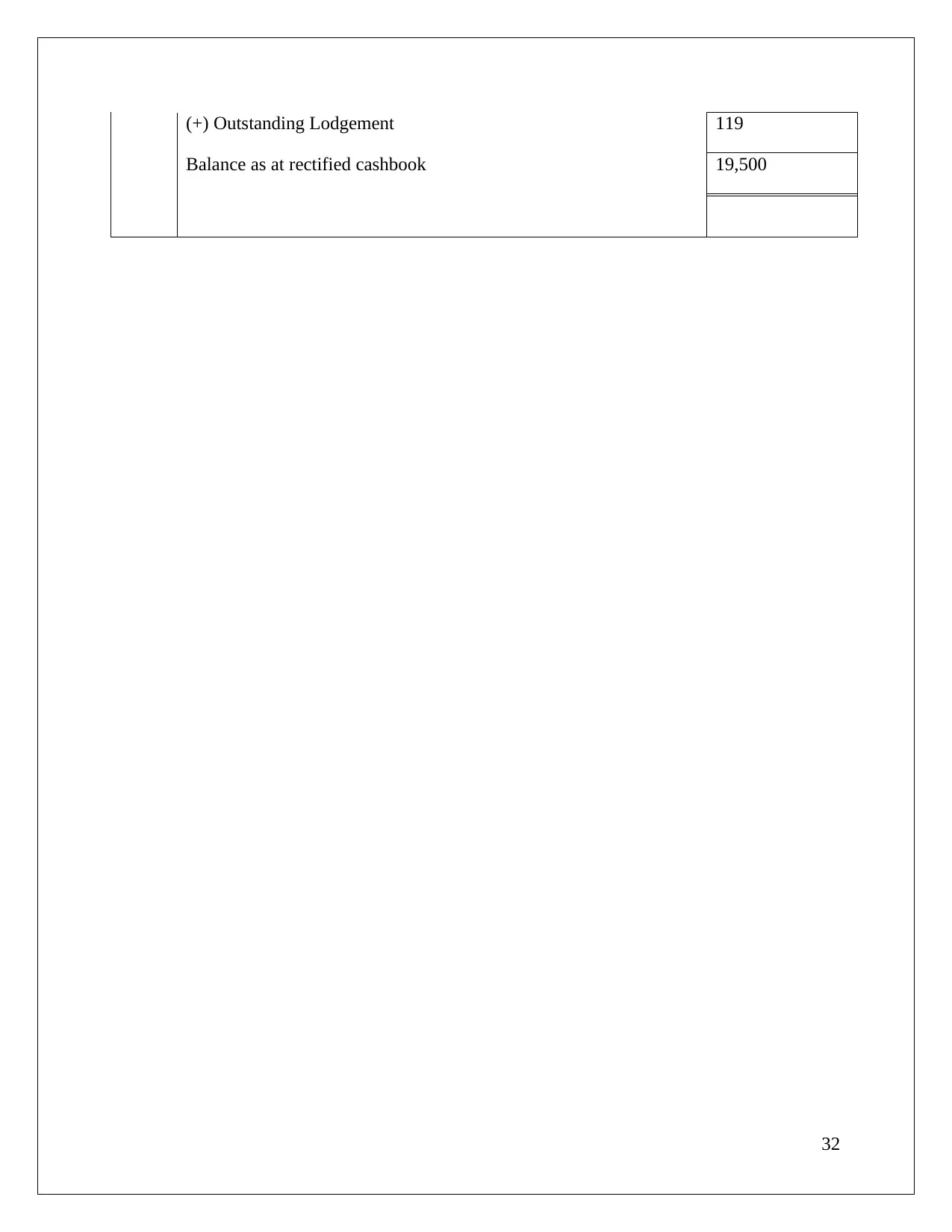

(+) Outstanding Lodgement 119

Balance as at rectified cashbook 19,500

32

Balance as at rectified cashbook 19,500

32

Client 5

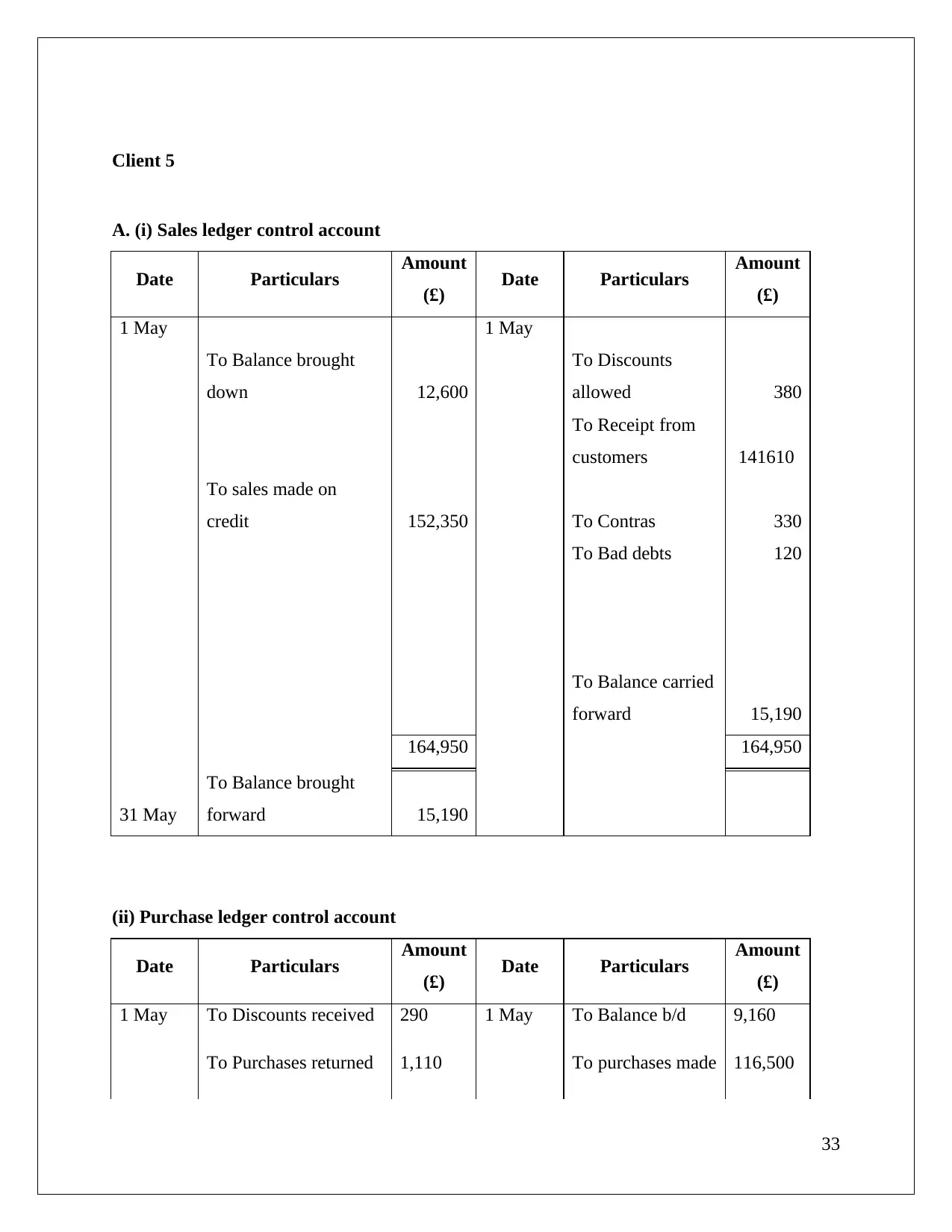

A. (i) Sales ledger control account

Date Particulars Amount

(£) Date Particulars Amount

(£)

1 May 1 May

To Balance brought

down 12,600

To Discounts

allowed 380

To Receipt from

customers 141610

To sales made on

credit 152,350 To Contras 330

To Bad debts 120

To Balance carried

forward 15,190

164,950 164,950

31 May

To Balance brought

forward 15,190

(ii) Purchase ledger control account

Date Particulars Amount

(£) Date Particulars Amount

(£)

1 May To Discounts received 290 1 May To Balance b/d 9,160

To Purchases returned 1,110 To purchases made 116,500

33

A. (i) Sales ledger control account

Date Particulars Amount

(£) Date Particulars Amount

(£)

1 May 1 May

To Balance brought

down 12,600

To Discounts

allowed 380

To Receipt from

customers 141610

To sales made on

credit 152,350 To Contras 330

To Bad debts 120

To Balance carried

forward 15,190

164,950 164,950

31 May

To Balance brought

forward 15,190

(ii) Purchase ledger control account

Date Particulars Amount

(£) Date Particulars Amount

(£)

1 May To Discounts received 290 1 May To Balance b/d 9,160

To Purchases returned 1,110 To purchases made 116,500

33

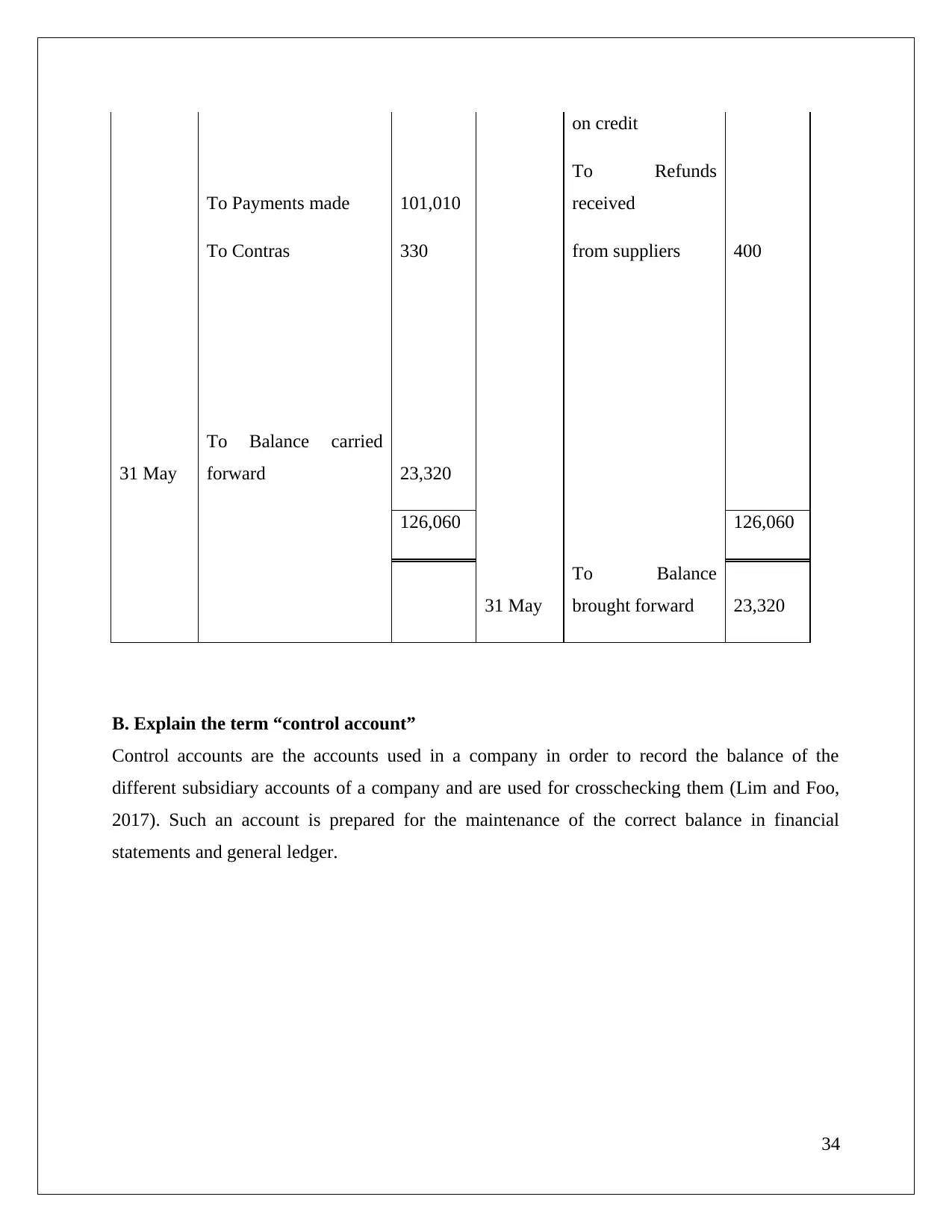

on credit

To Payments made 101,010

To Refunds

received

To Contras 330 from suppliers 400

31 May

To Balance carried

forward 23,320

126,060 126,060

31 May

To Balance

brought forward 23,320

B. Explain the term “control account”

Control accounts are the accounts used in a company in order to record the balance of the

different subsidiary accounts of a company and are used for crosschecking them (Lim and Foo,

2017). Such an account is prepared for the maintenance of the correct balance in financial

statements and general ledger.

34

To Payments made 101,010

To Refunds

received

To Contras 330 from suppliers 400

31 May

To Balance carried

forward 23,320

126,060 126,060

31 May

To Balance

brought forward 23,320

B. Explain the term “control account”

Control accounts are the accounts used in a company in order to record the balance of the

different subsidiary accounts of a company and are used for crosschecking them (Lim and Foo,

2017). Such an account is prepared for the maintenance of the correct balance in financial

statements and general ledger.

34

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Client 6

A. Suspense account and its features

Suspense accounts are temporary accounts created in a business for recording transactions before

the determination of the discrepancies in the books of accounts maintained in the business

(Horner, 2017). The main features of suspense accounts are -

It is temporary by nature

Shows the discrepancies and mistakes in a company’s books of accounts

Shows zero balance after errors have been reconciled and automatically disappears

B. Trial balance

Particulars Amount (Debit) Amount (Credit)

Purchase 700

Sales 1100

Cash at Bank 840

Travel Expense 160

Rent Paid 250

Receivable 540

Payable 350

Capital 710

Suspense 330

2490 2490

35

A. Suspense account and its features

Suspense accounts are temporary accounts created in a business for recording transactions before

the determination of the discrepancies in the books of accounts maintained in the business

(Horner, 2017). The main features of suspense accounts are -

It is temporary by nature

Shows the discrepancies and mistakes in a company’s books of accounts

Shows zero balance after errors have been reconciled and automatically disappears

B. Trial balance

Particulars Amount (Debit) Amount (Credit)

Purchase 700

Sales 1100

Cash at Bank 840

Travel Expense 160

Rent Paid 250

Receivable 540

Payable 350

Capital 710

Suspense 330

2490 2490

35

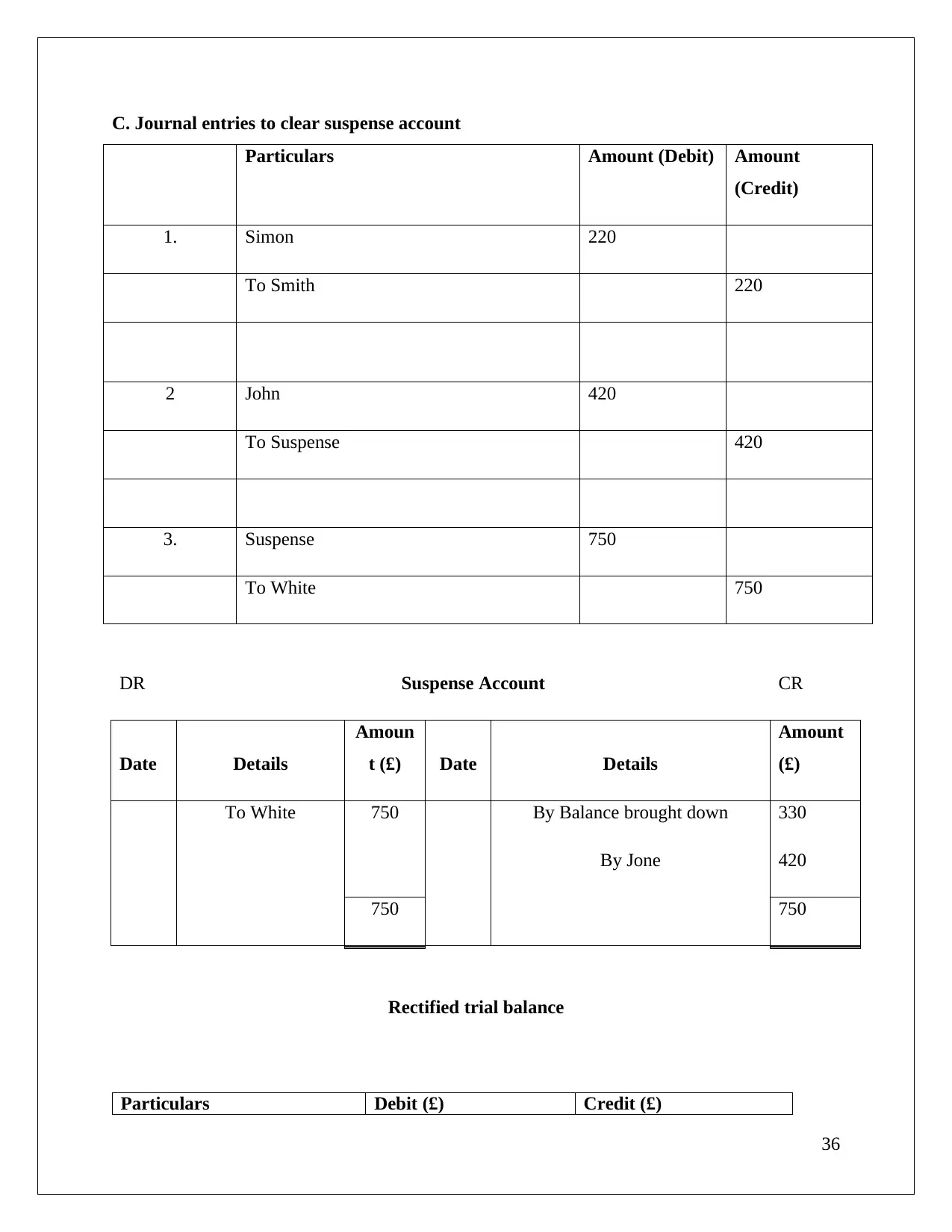

C. Journal entries to clear suspense account

Particulars Amount (Debit) Amount

(Credit)

1. Simon 220

To Smith 220

2 John 420

To Suspense 420

3. Suspense 750

To White 750

DR Suspense Account CR

Date Details

Amoun

t (£) Date Details

Amount

(£)

To White 750 By Balance brought down 330

By Jone 420

750 750

Rectified trial balance

Particulars Debit (£) Credit (£)

36

Particulars Amount (Debit) Amount

(Credit)

1. Simon 220

To Smith 220

2 John 420

To Suspense 420

3. Suspense 750

To White 750

DR Suspense Account CR

Date Details

Amoun

t (£) Date Details

Amount

(£)

To White 750 By Balance brought down 330

By Jone 420

750 750

Rectified trial balance

Particulars Debit (£) Credit (£)

36

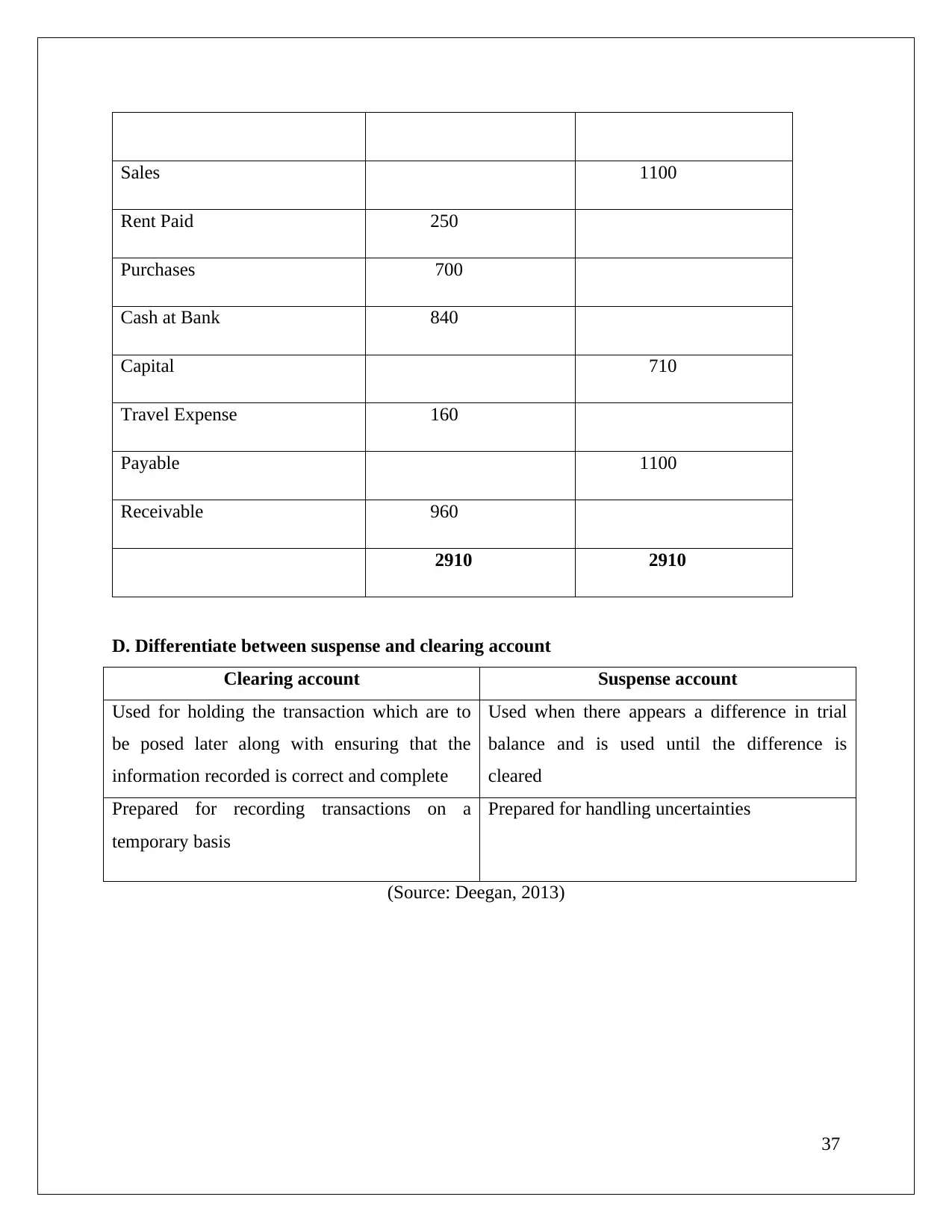

Sales 1100

Rent Paid 250

Purchases 700

Cash at Bank 840

Capital 710

Travel Expense 160

Payable 1100

Receivable 960

2910 2910

D. Differentiate between suspense and clearing account

Clearing account Suspense account

Used for holding the transaction which are to

be posed later along with ensuring that the

information recorded is correct and complete

Used when there appears a difference in trial

balance and is used until the difference is

cleared

Prepared for recording transactions on a

temporary basis

Prepared for handling uncertainties

(Source: Deegan, 2013)

37

Rent Paid 250

Purchases 700

Cash at Bank 840

Capital 710

Travel Expense 160

Payable 1100

Receivable 960

2910 2910

D. Differentiate between suspense and clearing account

Clearing account Suspense account

Used for holding the transaction which are to

be posed later along with ensuring that the

information recorded is correct and complete

Used when there appears a difference in trial

balance and is used until the difference is

cleared

Prepared for recording transactions on a

temporary basis

Prepared for handling uncertainties

(Source: Deegan, 2013)

37

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reference list

Cooper, S., 2015. A tale of ‘prudence’. Investor Perspectives, IFRS.

Council, F.R., 2013. Financial Reporting Council.

Council, F.R., 2014. FRC publications.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Del Giudice, V., Manganelli, B. and De Paola, P., 2016, July. Depreciation methods for firm’s

assets. In International Conference on Computational Science and Its Applications(pp. 214-227).

Springer International Publishing.

DiTommaso, M., Ruppel, W. and Larkin, R.F., 2017. CASH VERSUS ACCRUAL‐BASIS

ACCOUNTING. Wiley Not

‐for

‐Profit GAAP 2017: Interpretation and Application of Generally

Accepted Accounting Principles, pp.11-20.

Edgley, C., 2014. A genealogy of accounting materiality. Critical Perspectives on

Accounting, 25(3), pp.255-271.

Farrell, B., 2016. Depreciation and the Time Value of Money. arXiv preprint arXiv:1605.00080.

Giles, R., 2014. Finance & Accounting New 4th Edition. Lulu. com.

Horner, D., 2017. Accounting for Non-accountants. Kogan Page Publishers.

Kausar, A., Taffler, R.J. and Tan, C.E., 2017. Legal regimes and investor response to the

auditor’s going-concern opinion. Journal of Accounting, Auditing & Finance, 32(1), pp.40-72.

Lim, C.Y. and Foo, S.L., 2017. relation to financial instruments. The Routledge Companion to

Accounting and Risk.

Marshall, D., 2016. Accounting: What the numbers mean. McGraw-Hill Higher Education.

Nobes, C., 2015. Accounting for capital: the evolution of an idea. Accounting and Business

Research, 45(4), pp.413-441.

38

Cooper, S., 2015. A tale of ‘prudence’. Investor Perspectives, IFRS.

Council, F.R., 2013. Financial Reporting Council.

Council, F.R., 2014. FRC publications.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Del Giudice, V., Manganelli, B. and De Paola, P., 2016, July. Depreciation methods for firm’s

assets. In International Conference on Computational Science and Its Applications(pp. 214-227).

Springer International Publishing.

DiTommaso, M., Ruppel, W. and Larkin, R.F., 2017. CASH VERSUS ACCRUAL‐BASIS

ACCOUNTING. Wiley Not

‐for

‐Profit GAAP 2017: Interpretation and Application of Generally

Accepted Accounting Principles, pp.11-20.

Edgley, C., 2014. A genealogy of accounting materiality. Critical Perspectives on

Accounting, 25(3), pp.255-271.

Farrell, B., 2016. Depreciation and the Time Value of Money. arXiv preprint arXiv:1605.00080.

Giles, R., 2014. Finance & Accounting New 4th Edition. Lulu. com.

Horner, D., 2017. Accounting for Non-accountants. Kogan Page Publishers.

Kausar, A., Taffler, R.J. and Tan, C.E., 2017. Legal regimes and investor response to the

auditor’s going-concern opinion. Journal of Accounting, Auditing & Finance, 32(1), pp.40-72.

Lim, C.Y. and Foo, S.L., 2017. relation to financial instruments. The Routledge Companion to

Accounting and Risk.

Marshall, D., 2016. Accounting: What the numbers mean. McGraw-Hill Higher Education.

Nobes, C., 2015. Accounting for capital: the evolution of an idea. Accounting and Business

Research, 45(4), pp.413-441.

38

Penman, S., 2016. Conservatism as a Defining Principle for Accounting. The Japanese

Accounting Review, pp.6-2016.

Picker, R., Clark, K., Dunn, J., Kolitz, D., Livne, G., Loftus, J. and Van der Tas, L.,

2016. Applying international financial reporting standards. John Wiley & Sons.

Warren, C.M., 2016. The impact of International Accounting Standards Board

(IASB)/International Financial Reporting Standard 16 (IFRS 16). Property Management, 34(3).

Warren, J., 2015. Conventionalism, consistency, and consistency sentences. Synthese, 192(5),

pp.1351-1371.

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

39

Accounting Review, pp.6-2016.

Picker, R., Clark, K., Dunn, J., Kolitz, D., Livne, G., Loftus, J. and Van der Tas, L.,

2016. Applying international financial reporting standards. John Wiley & Sons.

Warren, C.M., 2016. The impact of International Accounting Standards Board

(IASB)/International Financial Reporting Standard 16 (IFRS 16). Property Management, 34(3).

Warren, J., 2015. Conventionalism, consistency, and consistency sentences. Synthese, 192(5),

pp.1351-1371.

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

39

1 out of 39

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.