Financial Accounting Principles Doc

Added on 2020-10-22

39 Pages5227 Words225 Views

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A) Report to Line Manager explaining accounting regulations.............................................1

CLIENT 1........................................................................................................................................5

A) Producing journal entries for the business........................................................................5

B) Exhibiting ledger accounts for organisation......................................................................6

................................................................................................................................................7

C) Extracting trial balance by compiling accounts...............................................................21

CLIENT 2......................................................................................................................................22

A) Producing Statement of Profit and Loss for client..........................................................22

B) Preparing Statement of Financial Position......................................................................23

CLIENT 3......................................................................................................................................25

A) Profit and Loss account of LMS Ltd...............................................................................25

B) Statement of Financial Position of company...................................................................26

C) Explaining concepts of consistency and prudency (150)................................................27

D) Describing purpose of depreciation and explaining methods of charging depreciation. 28

CLIENT 4......................................................................................................................................29

A) Preparing bank reconciliation statement.........................................................................29

B) Causes of varying accounting records with bank statements..........................................29

C) Preparing cash book and bank reconciliation statement of Kendal Ltd .........................30

........................................................................................................................................................32

CLIENT 5......................................................................................................................................32

A) Enumerating sales and purchase ledger account of Henderson Ltd................................32

..............................................................................................................................................33

B) Describing the term control account................................................................................33

CLIENT 6......................................................................................................................................33

A) Explaining suspense account and discussing features.....................................................33

B) Trial balance....................................................................................................................34

C) Distinguishing clearing and suspense account................................................................35

CONCLUSION..............................................................................................................................35

REFERENCES..............................................................................................................................36

INTRODUCTION...........................................................................................................................1

A) Report to Line Manager explaining accounting regulations.............................................1

CLIENT 1........................................................................................................................................5

A) Producing journal entries for the business........................................................................5

B) Exhibiting ledger accounts for organisation......................................................................6

................................................................................................................................................7

C) Extracting trial balance by compiling accounts...............................................................21

CLIENT 2......................................................................................................................................22

A) Producing Statement of Profit and Loss for client..........................................................22

B) Preparing Statement of Financial Position......................................................................23

CLIENT 3......................................................................................................................................25

A) Profit and Loss account of LMS Ltd...............................................................................25

B) Statement of Financial Position of company...................................................................26

C) Explaining concepts of consistency and prudency (150)................................................27

D) Describing purpose of depreciation and explaining methods of charging depreciation. 28

CLIENT 4......................................................................................................................................29

A) Preparing bank reconciliation statement.........................................................................29

B) Causes of varying accounting records with bank statements..........................................29

C) Preparing cash book and bank reconciliation statement of Kendal Ltd .........................30

........................................................................................................................................................32

CLIENT 5......................................................................................................................................32

A) Enumerating sales and purchase ledger account of Henderson Ltd................................32

..............................................................................................................................................33

B) Describing the term control account................................................................................33

CLIENT 6......................................................................................................................................33

A) Explaining suspense account and discussing features.....................................................33

B) Trial balance....................................................................................................................34

C) Distinguishing clearing and suspense account................................................................35

CONCLUSION..............................................................................................................................35

REFERENCES..............................................................................................................................36

INTRODUCTION

Financial accounting principles are very important for preparing financial statements

which show the financial performance of a company. Financial accounting principles are general

guidelines and rules of accounting.

The present report helps in understanding the double entry book-keeping and how the

transactions are recorded in it. The report presents different final account of sole trader,

partnership or limited company. The report depicts different methods for depreciation of fixed

asset with proper examples.

The report complies Bank-reconciliation-statement with its needs and objectives with

preparing bank-reconciliation-statement of a month. The report mentioned the control and its

importance in financial statements. The report gives overview of different accounting concepts.

The report mentioned the suspense account and the purpose for preparing it. The differences

between suspense account and clearing account is mentioned in the report. The report includes

preparation of different financial statements.

A) Report to Line Manager explaining accounting regulations

To: Line Manager

From: Junior Accountant

Subject: Accounting terms and regulations useful for organisation to comply with

Respected Sir,

Accounting is a crucial activity to record each and every transaction occurring in the

business on day-to-day basis. Various transactions take place in the company on daily basis and

it is required to keep track of the same so that accounts can be maintained in a better way.

Accountants have main responsibility in recording all such transactions, which will be helpful

in preparation of final accounts with ease. Journal entries are recorded with sale and purchases

in business, then inflows and outflows are analysed.

Next step is to post journal entries into individual accounts known as ledger accounts.

Afterwards, summarized view of accounts is provided by producing trial balance reflecting

equality of debit and credit. In relation to this, errors if any prevailing in journals or ledgers are

1

Financial accounting principles are very important for preparing financial statements

which show the financial performance of a company. Financial accounting principles are general

guidelines and rules of accounting.

The present report helps in understanding the double entry book-keeping and how the

transactions are recorded in it. The report presents different final account of sole trader,

partnership or limited company. The report depicts different methods for depreciation of fixed

asset with proper examples.

The report complies Bank-reconciliation-statement with its needs and objectives with

preparing bank-reconciliation-statement of a month. The report mentioned the control and its

importance in financial statements. The report gives overview of different accounting concepts.

The report mentioned the suspense account and the purpose for preparing it. The differences

between suspense account and clearing account is mentioned in the report. The report includes

preparation of different financial statements.

A) Report to Line Manager explaining accounting regulations

To: Line Manager

From: Junior Accountant

Subject: Accounting terms and regulations useful for organisation to comply with

Respected Sir,

Accounting is a crucial activity to record each and every transaction occurring in the

business on day-to-day basis. Various transactions take place in the company on daily basis and

it is required to keep track of the same so that accounts can be maintained in a better way.

Accountants have main responsibility in recording all such transactions, which will be helpful

in preparation of final accounts with ease. Journal entries are recorded with sale and purchases

in business, then inflows and outflows are analysed.

Next step is to post journal entries into individual accounts known as ledger accounts.

Afterwards, summarized view of accounts is provided by producing trial balance reflecting

equality of debit and credit. In relation to this, errors if any prevailing in journals or ledgers are

1

rectified by extracting trial balance. Next step is to prepare final accounts such as cash flow

statement, income statement and Statement of Financial Position. Hence, financials are

prepared in effective manner by relying on reliability of accounting.

In order to extract true financials, accounting practices are followed that should be

proper so that organisation may be able to provide clear view of financial statements to internal

and external stakeholders in the best possible manner. For accomplishing this, accounting

concepts and regulations are vital to follow by accountants to extract accounts quite fairly. By

strictly following such concepts, true and fair statements are prepared revealing authentic and

reliable information of financial health of firm (Renz, 2016). This is because investors,

creditors, government and related parties rely on such statements so that they may take

enhanced decisions. Investors come to know earning capacity of an organisation whether

adequate returns will be generated and paid to them in the way of dividends. Creditors who lend

money to business who also seek solvency and liquidity aspect of company in paying-off

liabilities in a timely manner. Government and taxation authorities are benefited to analyse tax

obligation of firm and hence, reliability of financials is a must, which can be enhanced by

abiding with concepts and regulations imparted by accounting bodies.

Financial Accounting

It is a useful branch of accounting, which helps to prepare financial statements quite

effectively. Financial accounting takes past information and is mainly concerned with

summarizing, analysing, reporting of monetary transactions that pertains to organisation. Public

or external parties are benefited because it helps them to review financial standing of business

and then carry out better decisions with ease. Apart from external stakeholders, it is also

beneficial for the management to take enhanced decisions and straightening internal operations

so that productive results that may be achieved in effectual way. Costs can be controlled and

profits can be maximised (Warren and Jones, 2018.). Financial statements are formulated by

accountants, which are analysed by internal and external stakeholders by which decision-

making can be done. Overall, liquidity, profitability, solvency and efficiency of business is

carried out with the help of financial accounting as statements are produced on such basis.

Financial statements are useful for taxation authorities as it helps to carry out tax obligation of

business in effective manner. True and fair position of business can be assessed by relying on

2

statement, income statement and Statement of Financial Position. Hence, financials are

prepared in effective manner by relying on reliability of accounting.

In order to extract true financials, accounting practices are followed that should be

proper so that organisation may be able to provide clear view of financial statements to internal

and external stakeholders in the best possible manner. For accomplishing this, accounting

concepts and regulations are vital to follow by accountants to extract accounts quite fairly. By

strictly following such concepts, true and fair statements are prepared revealing authentic and

reliable information of financial health of firm (Renz, 2016). This is because investors,

creditors, government and related parties rely on such statements so that they may take

enhanced decisions. Investors come to know earning capacity of an organisation whether

adequate returns will be generated and paid to them in the way of dividends. Creditors who lend

money to business who also seek solvency and liquidity aspect of company in paying-off

liabilities in a timely manner. Government and taxation authorities are benefited to analyse tax

obligation of firm and hence, reliability of financials is a must, which can be enhanced by

abiding with concepts and regulations imparted by accounting bodies.

Financial Accounting

It is a useful branch of accounting, which helps to prepare financial statements quite

effectively. Financial accounting takes past information and is mainly concerned with

summarizing, analysing, reporting of monetary transactions that pertains to organisation. Public

or external parties are benefited because it helps them to review financial standing of business

and then carry out better decisions with ease. Apart from external stakeholders, it is also

beneficial for the management to take enhanced decisions and straightening internal operations

so that productive results that may be achieved in effectual way. Costs can be controlled and

profits can be maximised (Warren and Jones, 2018.). Financial statements are formulated by

accountants, which are analysed by internal and external stakeholders by which decision-

making can be done. Overall, liquidity, profitability, solvency and efficiency of business is

carried out with the help of financial accounting as statements are produced on such basis.

Financial statements are useful for taxation authorities as it helps to carry out tax obligation of

business in effective manner. True and fair position of business can be assessed by relying on

2

financials.

Financial accounting rules and regulations

Accounting is a large field by which professional records, summarizes and report data in

the form of final accounts that help stakeholders to make enhanced decisions with ease. It is

required for the preparation of true accounts, regulations governed by professional bodies that

are followed for presenting true health of business (Weygandt, Kimmel, and Kieso, 2015). This

is particularly important to eliminate manipulation of records that affect fairness and reliability

of statements up to a high extent. It is required so that business may be able to reveal perfect

information to users of financial accounting and as a result, external parties are not fooled by

inaccurate and manipulative information. In relation to this, financial regulator of UK FRC

(Financial Reporting Council) has imparted guidelines to be followed by corporates. Legal

frameworks provided by accounting bodies are enumerated as under-

FRC: It is a body which is formed as limited by guarantee and regulate not only corporates but

also government units. By such legal framework, UK economy is benefited as proper financials

principles are followed and as a result, true final accounts are produced revealing health of

company with much ease. Corporate governance is effectively regulated to promote economic

development of the nation.

IASB (International Accounting Standards Board): The body is empowered to effectively

regulate accounting policies so that true financials may be prepared. The accountants are

benefited as they prepare accounts in relation to the regulations prescribed by IASB and as

such, it helps company to produce statements exhibiting correct position.

IFRS (International Financial Reporting Standards): This professional body also helps and

guides in producing financial reports in the best possible manner. This helps accountants to

follow policies and rules so as to exhibit information and provide clarity to external parties for

making decisions.

Enumerating principles and rules for accounting

There are certain guidelines which are universally accepted by accountants in

preparation of financials. GAAP (Generally Accepted Accounting Principles) provide

3

Financial accounting rules and regulations

Accounting is a large field by which professional records, summarizes and report data in

the form of final accounts that help stakeholders to make enhanced decisions with ease. It is

required for the preparation of true accounts, regulations governed by professional bodies that

are followed for presenting true health of business (Weygandt, Kimmel, and Kieso, 2015). This

is particularly important to eliminate manipulation of records that affect fairness and reliability

of statements up to a high extent. It is required so that business may be able to reveal perfect

information to users of financial accounting and as a result, external parties are not fooled by

inaccurate and manipulative information. In relation to this, financial regulator of UK FRC

(Financial Reporting Council) has imparted guidelines to be followed by corporates. Legal

frameworks provided by accounting bodies are enumerated as under-

FRC: It is a body which is formed as limited by guarantee and regulate not only corporates but

also government units. By such legal framework, UK economy is benefited as proper financials

principles are followed and as a result, true final accounts are produced revealing health of

company with much ease. Corporate governance is effectively regulated to promote economic

development of the nation.

IASB (International Accounting Standards Board): The body is empowered to effectively

regulate accounting policies so that true financials may be prepared. The accountants are

benefited as they prepare accounts in relation to the regulations prescribed by IASB and as

such, it helps company to produce statements exhibiting correct position.

IFRS (International Financial Reporting Standards): This professional body also helps and

guides in producing financial reports in the best possible manner. This helps accountants to

follow policies and rules so as to exhibit information and provide clarity to external parties for

making decisions.

Enumerating principles and rules for accounting

There are certain guidelines which are universally accepted by accountants in

preparation of financials. GAAP (Generally Accepted Accounting Principles) provide

3

guidelines to professionals so that true information may be reflected in overall final accounts.

Monetary assumption (unit)- This assumption states that transactions may be handled or made

in that currency which is universally accepted. In relation to this, US Dollar should be used as

monetary currency value as it is less fluctuating for maintaining transactions.

Economic assumptions- The economic assumption means that firm takes into account of

economic environment which prevails in the country. In relation to this, assumptions are made

which help to estimate viability of upcoming project whether it will reflect the forthcoming

project of a company or not.

Cost principle- The costs which are needed to be incurred are analysed in anticipation of

requirements of departments and as such, budget is prepared so that needs may be fulfilled quite

effectually. It is helpful in order to initiate control on expenses and meet operational

requirements and thus, trade requirements are fulfilled as well.

Full disclosure concept- This concept postulates that each and every transaction that occurs at

a particular time period must be recorded so that proper financials may be extracted with ease.

This is a prerequisite because with absence of information, effective financial statements cannot

be prepared. In addition to this, to enhance reliability, audit should be conducted and

compilation should be done in single statements so as to provide attractive information readily

available to analyse by stakeholders. Hence, disclosure of income statement, balance sheet is

must at year ending.

Going concern concept- The concept clearly states that business commences its operations in

the market with a view to continue for a long-run and attain good market share. By complying

with this principle, financial statements are prepared which are imparted to external parties

which enhance their reliability and decisions are made accordingly.

Materiality concept- As the name suggests, material information is taken into account and

other immaterial information is ignored by the firm. This means that in books of accounts that

information must be reflected which could affect decision-making of firm. The information

which might not affect taking decisions should be ignored.

4

Monetary assumption (unit)- This assumption states that transactions may be handled or made

in that currency which is universally accepted. In relation to this, US Dollar should be used as

monetary currency value as it is less fluctuating for maintaining transactions.

Economic assumptions- The economic assumption means that firm takes into account of

economic environment which prevails in the country. In relation to this, assumptions are made

which help to estimate viability of upcoming project whether it will reflect the forthcoming

project of a company or not.

Cost principle- The costs which are needed to be incurred are analysed in anticipation of

requirements of departments and as such, budget is prepared so that needs may be fulfilled quite

effectually. It is helpful in order to initiate control on expenses and meet operational

requirements and thus, trade requirements are fulfilled as well.

Full disclosure concept- This concept postulates that each and every transaction that occurs at

a particular time period must be recorded so that proper financials may be extracted with ease.

This is a prerequisite because with absence of information, effective financial statements cannot

be prepared. In addition to this, to enhance reliability, audit should be conducted and

compilation should be done in single statements so as to provide attractive information readily

available to analyse by stakeholders. Hence, disclosure of income statement, balance sheet is

must at year ending.

Going concern concept- The concept clearly states that business commences its operations in

the market with a view to continue for a long-run and attain good market share. By complying

with this principle, financial statements are prepared which are imparted to external parties

which enhance their reliability and decisions are made accordingly.

Materiality concept- As the name suggests, material information is taken into account and

other immaterial information is ignored by the firm. This means that in books of accounts that

information must be reflected which could affect decision-making of firm. The information

which might not affect taking decisions should be ignored.

4

CLIENT 1

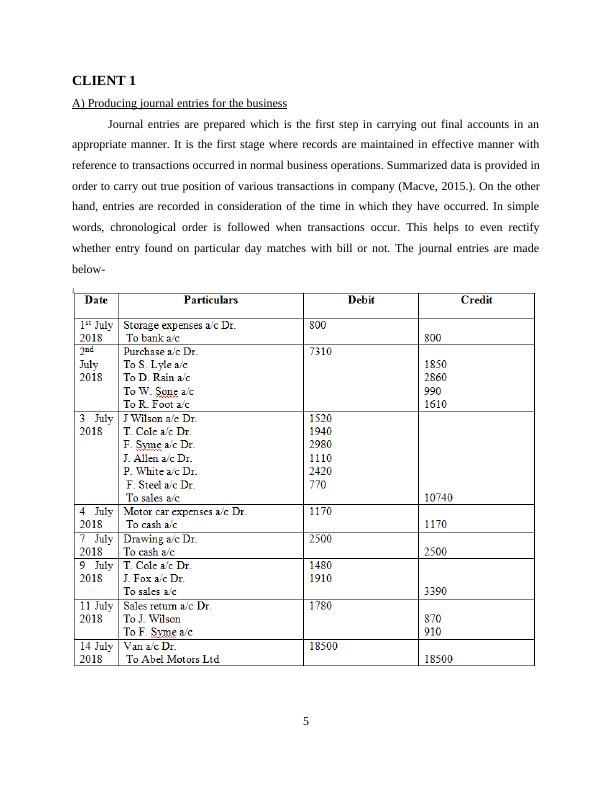

A) Producing journal entries for the business

Journal entries are prepared which is the first step in carrying out final accounts in an

appropriate manner. It is the first stage where records are maintained in effective manner with

reference to transactions occurred in normal business operations. Summarized data is provided in

order to carry out true position of various transactions in company (Macve, 2015.). On the other

hand, entries are recorded in consideration of the time in which they have occurred. In simple

words, chronological order is followed when transactions occur. This helps to even rectify

whether entry found on particular day matches with bill or not. The journal entries are made

below-

5

A) Producing journal entries for the business

Journal entries are prepared which is the first step in carrying out final accounts in an

appropriate manner. It is the first stage where records are maintained in effective manner with

reference to transactions occurred in normal business operations. Summarized data is provided in

order to carry out true position of various transactions in company (Macve, 2015.). On the other

hand, entries are recorded in consideration of the time in which they have occurred. In simple

words, chronological order is followed when transactions occur. This helps to even rectify

whether entry found on particular day matches with bill or not. The journal entries are made

below-

5

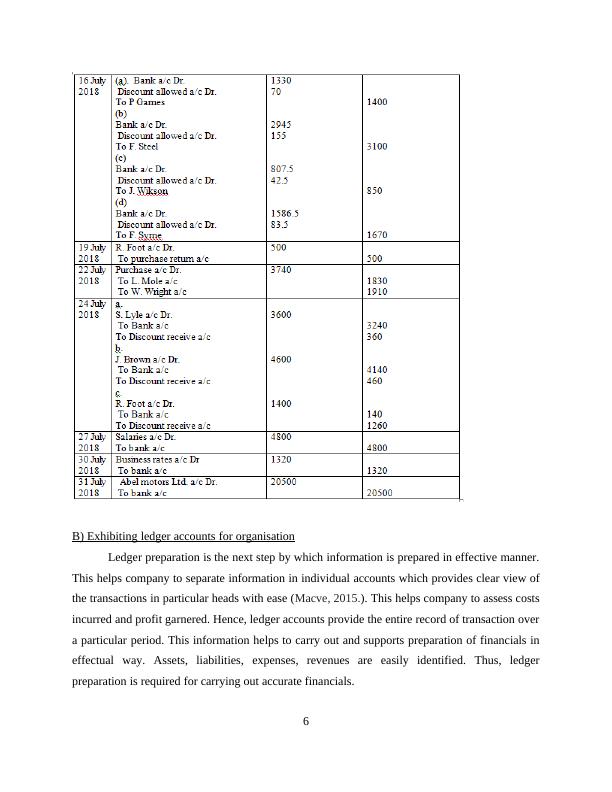

B) Exhibiting ledger accounts for organisation

Ledger preparation is the next step by which information is prepared in effective manner.

This helps company to separate information in individual accounts which provides clear view of

the transactions in particular heads with ease (Macve, 2015.). This helps company to assess costs

incurred and profit garnered. Hence, ledger accounts provide the entire record of transaction over

a particular period. This information helps to carry out and supports preparation of financials in

effectual way. Assets, liabilities, expenses, revenues are easily identified. Thus, ledger

preparation is required for carrying out accurate financials.

6

Ledger preparation is the next step by which information is prepared in effective manner.

This helps company to separate information in individual accounts which provides clear view of

the transactions in particular heads with ease (Macve, 2015.). This helps company to assess costs

incurred and profit garnered. Hence, ledger accounts provide the entire record of transaction over

a particular period. This information helps to carry out and supports preparation of financials in

effectual way. Assets, liabilities, expenses, revenues are easily identified. Thus, ledger

preparation is required for carrying out accurate financials.

6

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Assignment on Financial Accounting pdflg...

|47

|5713

|177

Accounting Principles and Ruleslg...

|39

|4332

|322

Importance of Accounting in Preparation of Financial Statements - Reportlg...

|34

|4240

|26

Accounting Principles Assignment Solvedlg...

|37

|6580

|173

Financial Accounting Principles: Assignmentlg...

|40

|3645

|142

Financial Accounting: Assignment Samplelg...

|37

|5577

|390