Accounting Principles and Practices

VerifiedAdded on 2020/10/23

|26

|7021

|485

AI Summary

The assignment covers essential topics in accounting, including the significance of following accounting principles, the reliability of double-entry bookkeeping over single-entry systems, and the mandatory preparation of financial statements such as cash flows, income statements, and balance sheets. It also highlights the role of bank reconciliation statements and purchase/sales control accounts in maintaining accurate records and monitoring debtors/creditors positions. The assignment is a valuable resource for students seeking to understand key concepts in accounting and their practical applications.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

Principles

Principles

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

1. Financial accounting and its purposes ....................................................................................1

2. Regulation of financial accounting..........................................................................................2

3 . Accounting principles & rules : .............................................................................................2

4. Conventions related to consistency and material disclosure...................................................3

CLIENT 1........................................................................................................................................4

(a) Journal Entry in the books of David Study...........................................................................4

(b) Ledger Accounts....................................................................................................................6

(c) Trial Balance as at 31st January, 2018................................................................................13

CLIENT 2......................................................................................................................................14

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018 .............14

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018 ...................15

CLIENT 3......................................................................................................................................15

(a) Profit and loss account of Bowling Limited.........................................................................15

(b) Balance Sheet of Bowling Limited......................................................................................16

(c) Accounts concepts such as consistency and prudency.........................................................17

(d) Depreciation and its methods..............................................................................................17

Client 4...........................................................................................................................................17

(i) Purpose of bank reconciliation statement ............................................................................17

(ii) Prepare Durrell Ltd's updated cash book for December 2017.............................................18

(iii) Bank Reconciliation Statement as at 31"t December 2017................................................19

CLIENT 5......................................................................................................................................19

(a) Books of Henderson.............................................................................................................19

(b). Control account...................................................................................................................20

CLIENT 6......................................................................................................................................20

A. Suspense Account.................................................................................................................20

B. Drafting of Trial Balance......................................................................................................21

C. Journal entry for suspense account........................................................................................21

D . Difference between clearing account and suspense account ..............................................21

INTRODUCTION...........................................................................................................................1

1. Financial accounting and its purposes ....................................................................................1

2. Regulation of financial accounting..........................................................................................2

3 . Accounting principles & rules : .............................................................................................2

4. Conventions related to consistency and material disclosure...................................................3

CLIENT 1........................................................................................................................................4

(a) Journal Entry in the books of David Study...........................................................................4

(b) Ledger Accounts....................................................................................................................6

(c) Trial Balance as at 31st January, 2018................................................................................13

CLIENT 2......................................................................................................................................14

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018 .............14

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018 ...................15

CLIENT 3......................................................................................................................................15

(a) Profit and loss account of Bowling Limited.........................................................................15

(b) Balance Sheet of Bowling Limited......................................................................................16

(c) Accounts concepts such as consistency and prudency.........................................................17

(d) Depreciation and its methods..............................................................................................17

Client 4...........................................................................................................................................17

(i) Purpose of bank reconciliation statement ............................................................................17

(ii) Prepare Durrell Ltd's updated cash book for December 2017.............................................18

(iii) Bank Reconciliation Statement as at 31"t December 2017................................................19

CLIENT 5......................................................................................................................................19

(a) Books of Henderson.............................................................................................................19

(b). Control account...................................................................................................................20

CLIENT 6......................................................................................................................................20

A. Suspense Account.................................................................................................................20

B. Drafting of Trial Balance......................................................................................................21

C. Journal entry for suspense account........................................................................................21

D . Difference between clearing account and suspense account ..............................................21

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

REFERENCES..............................................................................................................................23

INTRODUCTION

Financial accounting is the field of accounting concerned with the analysis, summary and

recording the financial transactions pertaining to a business. It provides help to organisations for

preparation of financial statements appropriately and reflects the financial position of company.

There are various regulations and rules which are needed to be follow by the corporation. In this

report chosen company is RBS Accountants Ltd. which is incorporated in London, UK. The aim

of this report is to ensure that corporations follows the compliances and regulations of

accounting. There are following topics which are discussed in this report such as: accounting

rules and principles, conventions & concepts related to consistency and material disclosure,

business transactions using double entry book- keeping and trial balance, final accounts for sole

trader, partnerships & limited companies and bank reconciliation statement. Apart from this it

also discusses about recorded transactions from the suspense accounts to the right accounts.

1. Financial accounting and its purposes

It refers to the process of recording, analysing, summarizing and interpreting the

business transactions over a stipulated period of time. It is useful for supplier, creditors, investors

and other stakeholders which are directly or indirectly related to the organisation. Junior

accountant of RBS Accountants Ltd. is responsible to prepare financial reports as per the

regulations and rules of accounting as a result it will able to provide accurate data and

information which help the corporation to take important business decisions. It includes cash

flow statement, income statement and balance sheet. Cash flow statement is being prepared so

that company can know the inflow and outflow of cash through various activities such as:

operating, investing and financing activity. Income statement is being prepared so that

organisation can know its profitability level for a stipulated period of time. Balance sheet is

being prepared so that RBS Accountants Ltd. can know their total liabilities and assets of its

business. There are various purposes to financial accounting which are discussed as below:

Purpose of financial accounting is to give relevant information about financial position of

corporation (Agasist and Catalano, 2013).

To provide useful data and information to the stakeholders of company so that they can

take important decisions about the investment.

1

Financial accounting is the field of accounting concerned with the analysis, summary and

recording the financial transactions pertaining to a business. It provides help to organisations for

preparation of financial statements appropriately and reflects the financial position of company.

There are various regulations and rules which are needed to be follow by the corporation. In this

report chosen company is RBS Accountants Ltd. which is incorporated in London, UK. The aim

of this report is to ensure that corporations follows the compliances and regulations of

accounting. There are following topics which are discussed in this report such as: accounting

rules and principles, conventions & concepts related to consistency and material disclosure,

business transactions using double entry book- keeping and trial balance, final accounts for sole

trader, partnerships & limited companies and bank reconciliation statement. Apart from this it

also discusses about recorded transactions from the suspense accounts to the right accounts.

1. Financial accounting and its purposes

It refers to the process of recording, analysing, summarizing and interpreting the

business transactions over a stipulated period of time. It is useful for supplier, creditors, investors

and other stakeholders which are directly or indirectly related to the organisation. Junior

accountant of RBS Accountants Ltd. is responsible to prepare financial reports as per the

regulations and rules of accounting as a result it will able to provide accurate data and

information which help the corporation to take important business decisions. It includes cash

flow statement, income statement and balance sheet. Cash flow statement is being prepared so

that company can know the inflow and outflow of cash through various activities such as:

operating, investing and financing activity. Income statement is being prepared so that

organisation can know its profitability level for a stipulated period of time. Balance sheet is

being prepared so that RBS Accountants Ltd. can know their total liabilities and assets of its

business. There are various purposes to financial accounting which are discussed as below:

Purpose of financial accounting is to give relevant information about financial position of

corporation (Agasist and Catalano, 2013).

To provide useful data and information to the stakeholders of company so that they can

take important decisions about the investment.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

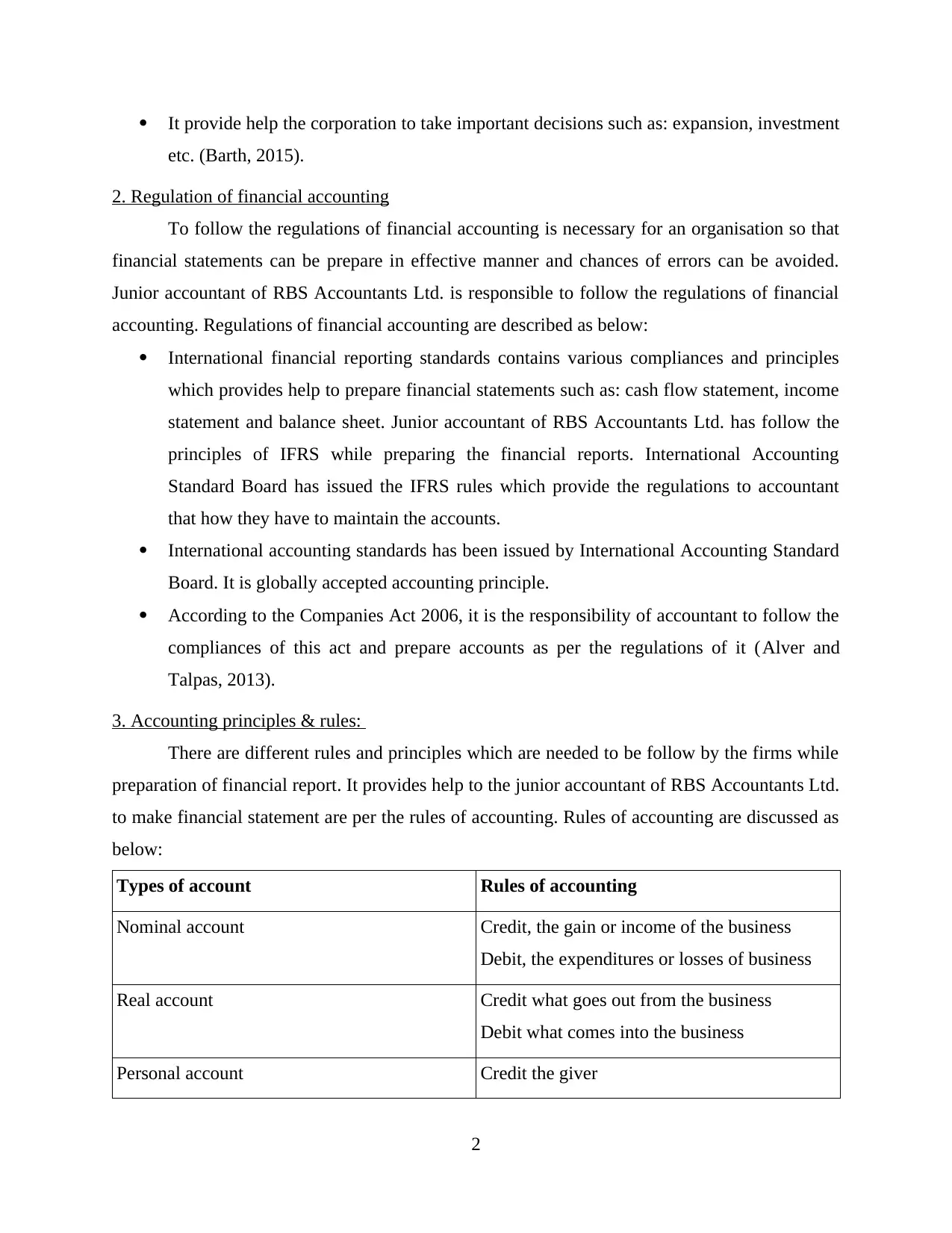

It provide help the corporation to take important decisions such as: expansion, investment

etc. (Barth, 2015).

2. Regulation of financial accounting

To follow the regulations of financial accounting is necessary for an organisation so that

financial statements can be prepare in effective manner and chances of errors can be avoided.

Junior accountant of RBS Accountants Ltd. is responsible to follow the regulations of financial

accounting. Regulations of financial accounting are described as below:

International financial reporting standards contains various compliances and principles

which provides help to prepare financial statements such as: cash flow statement, income

statement and balance sheet. Junior accountant of RBS Accountants Ltd. has follow the

principles of IFRS while preparing the financial reports. International Accounting

Standard Board has issued the IFRS rules which provide the regulations to accountant

that how they have to maintain the accounts.

International accounting standards has been issued by International Accounting Standard

Board. It is globally accepted accounting principle.

According to the Companies Act 2006, it is the responsibility of accountant to follow the

compliances of this act and prepare accounts as per the regulations of it (Alver and

Talpas, 2013).

3. Accounting principles & rules:

There are different rules and principles which are needed to be follow by the firms while

preparation of financial report. It provides help to the junior accountant of RBS Accountants Ltd.

to make financial statement are per the rules of accounting. Rules of accounting are discussed as

below:

Types of account Rules of accounting

Nominal account Credit, the gain or income of the business

Debit, the expenditures or losses of business

Real account Credit what goes out from the business

Debit what comes into the business

Personal account Credit the giver

2

etc. (Barth, 2015).

2. Regulation of financial accounting

To follow the regulations of financial accounting is necessary for an organisation so that

financial statements can be prepare in effective manner and chances of errors can be avoided.

Junior accountant of RBS Accountants Ltd. is responsible to follow the regulations of financial

accounting. Regulations of financial accounting are described as below:

International financial reporting standards contains various compliances and principles

which provides help to prepare financial statements such as: cash flow statement, income

statement and balance sheet. Junior accountant of RBS Accountants Ltd. has follow the

principles of IFRS while preparing the financial reports. International Accounting

Standard Board has issued the IFRS rules which provide the regulations to accountant

that how they have to maintain the accounts.

International accounting standards has been issued by International Accounting Standard

Board. It is globally accepted accounting principle.

According to the Companies Act 2006, it is the responsibility of accountant to follow the

compliances of this act and prepare accounts as per the regulations of it (Alver and

Talpas, 2013).

3. Accounting principles & rules:

There are different rules and principles which are needed to be follow by the firms while

preparation of financial report. It provides help to the junior accountant of RBS Accountants Ltd.

to make financial statement are per the rules of accounting. Rules of accounting are discussed as

below:

Types of account Rules of accounting

Nominal account Credit, the gain or income of the business

Debit, the expenditures or losses of business

Real account Credit what goes out from the business

Debit what comes into the business

Personal account Credit the giver

2

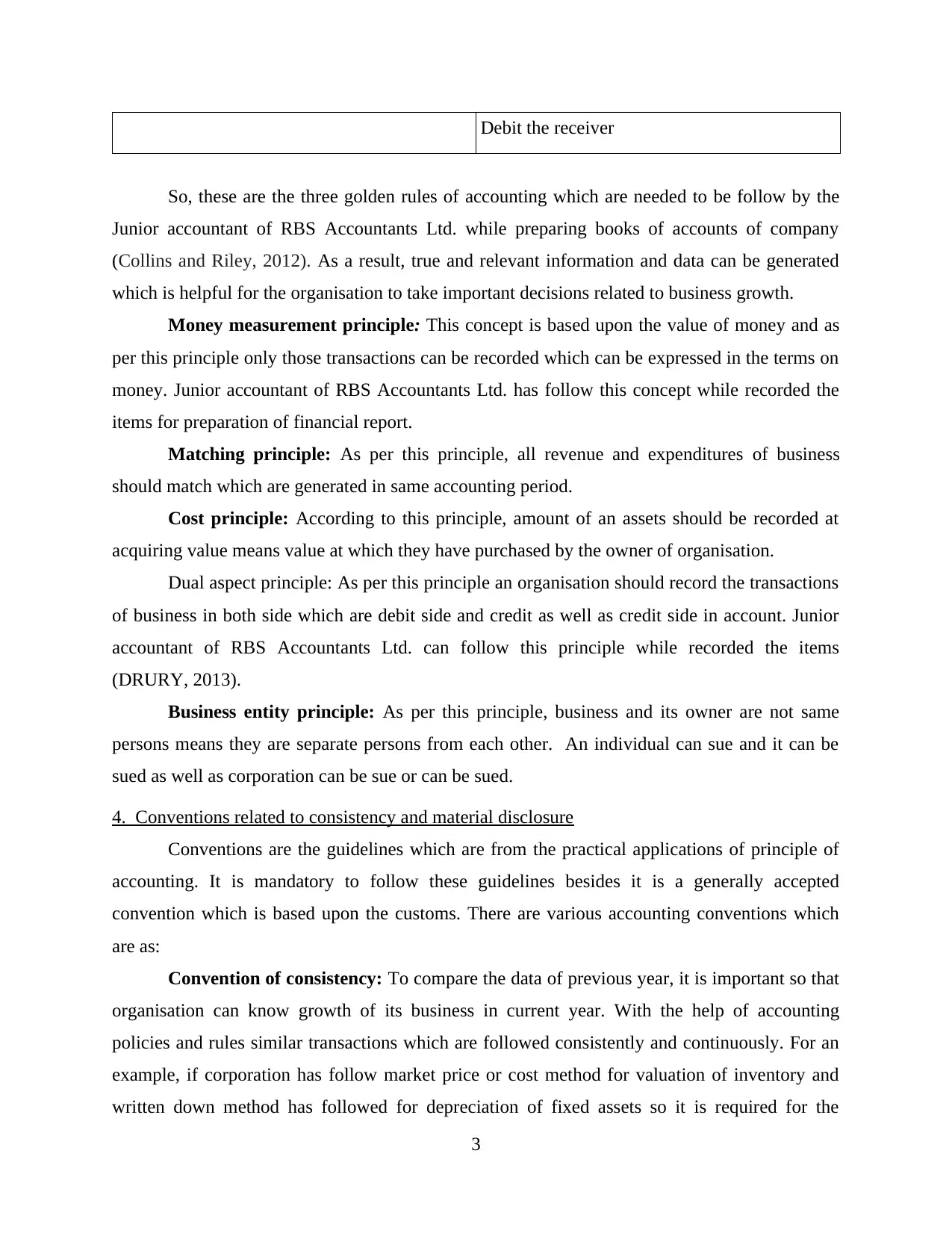

Debit the receiver

So, these are the three golden rules of accounting which are needed to be follow by the

Junior accountant of RBS Accountants Ltd. while preparing books of accounts of company

(Collins and Riley, 2012). As a result, true and relevant information and data can be generated

which is helpful for the organisation to take important decisions related to business growth.

Money measurement principle: This concept is based upon the value of money and as

per this principle only those transactions can be recorded which can be expressed in the terms on

money. Junior accountant of RBS Accountants Ltd. has follow this concept while recorded the

items for preparation of financial report.

Matching principle: As per this principle, all revenue and expenditures of business

should match which are generated in same accounting period.

Cost principle: According to this principle, amount of an assets should be recorded at

acquiring value means value at which they have purchased by the owner of organisation.

Dual aspect principle: As per this principle an organisation should record the transactions

of business in both side which are debit side and credit as well as credit side in account. Junior

accountant of RBS Accountants Ltd. can follow this principle while recorded the items

(DRURY, 2013).

Business entity principle: As per this principle, business and its owner are not same

persons means they are separate persons from each other. An individual can sue and it can be

sued as well as corporation can be sue or can be sued.

4. Conventions related to consistency and material disclosure

Conventions are the guidelines which are from the practical applications of principle of

accounting. It is mandatory to follow these guidelines besides it is a generally accepted

convention which is based upon the customs. There are various accounting conventions which

are as:

Convention of consistency: To compare the data of previous year, it is important so that

organisation can know growth of its business in current year. With the help of accounting

policies and rules similar transactions which are followed consistently and continuously. For an

example, if corporation has follow market price or cost method for valuation of inventory and

written down method has followed for depreciation of fixed assets so it is required for the

3

So, these are the three golden rules of accounting which are needed to be follow by the

Junior accountant of RBS Accountants Ltd. while preparing books of accounts of company

(Collins and Riley, 2012). As a result, true and relevant information and data can be generated

which is helpful for the organisation to take important decisions related to business growth.

Money measurement principle: This concept is based upon the value of money and as

per this principle only those transactions can be recorded which can be expressed in the terms on

money. Junior accountant of RBS Accountants Ltd. has follow this concept while recorded the

items for preparation of financial report.

Matching principle: As per this principle, all revenue and expenditures of business

should match which are generated in same accounting period.

Cost principle: According to this principle, amount of an assets should be recorded at

acquiring value means value at which they have purchased by the owner of organisation.

Dual aspect principle: As per this principle an organisation should record the transactions

of business in both side which are debit side and credit as well as credit side in account. Junior

accountant of RBS Accountants Ltd. can follow this principle while recorded the items

(DRURY, 2013).

Business entity principle: As per this principle, business and its owner are not same

persons means they are separate persons from each other. An individual can sue and it can be

sued as well as corporation can be sue or can be sued.

4. Conventions related to consistency and material disclosure

Conventions are the guidelines which are from the practical applications of principle of

accounting. It is mandatory to follow these guidelines besides it is a generally accepted

convention which is based upon the customs. There are various accounting conventions which

are as:

Convention of consistency: To compare the data of previous year, it is important so that

organisation can know growth of its business in current year. With the help of accounting

policies and rules similar transactions which are followed consistently and continuously. For an

example, if corporation has follow market price or cost method for valuation of inventory and

written down method has followed for depreciation of fixed assets so it is required for the

3

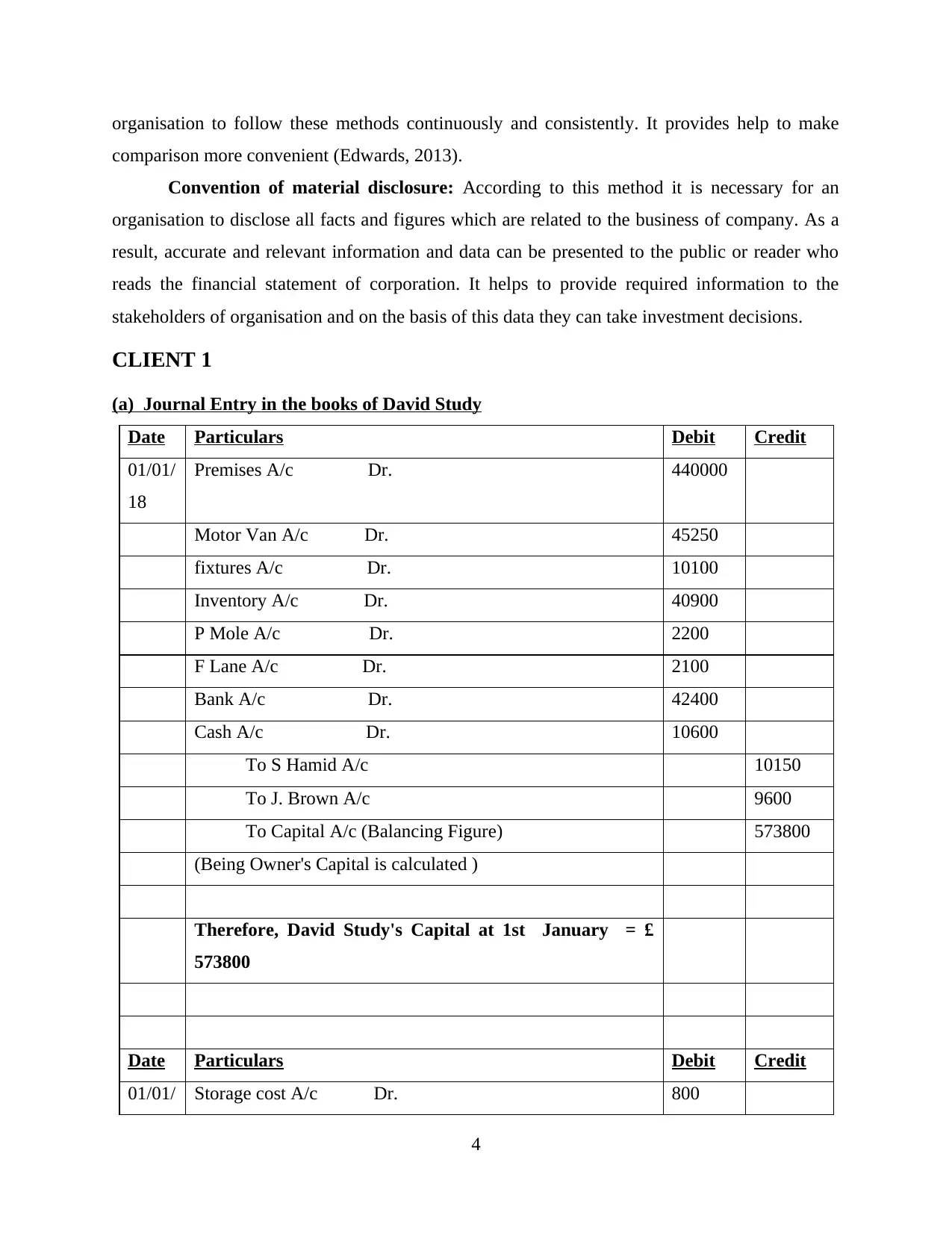

organisation to follow these methods continuously and consistently. It provides help to make

comparison more convenient (Edwards, 2013).

Convention of material disclosure: According to this method it is necessary for an

organisation to disclose all facts and figures which are related to the business of company. As a

result, accurate and relevant information and data can be presented to the public or reader who

reads the financial statement of corporation. It helps to provide required information to the

stakeholders of organisation and on the basis of this data they can take investment decisions.

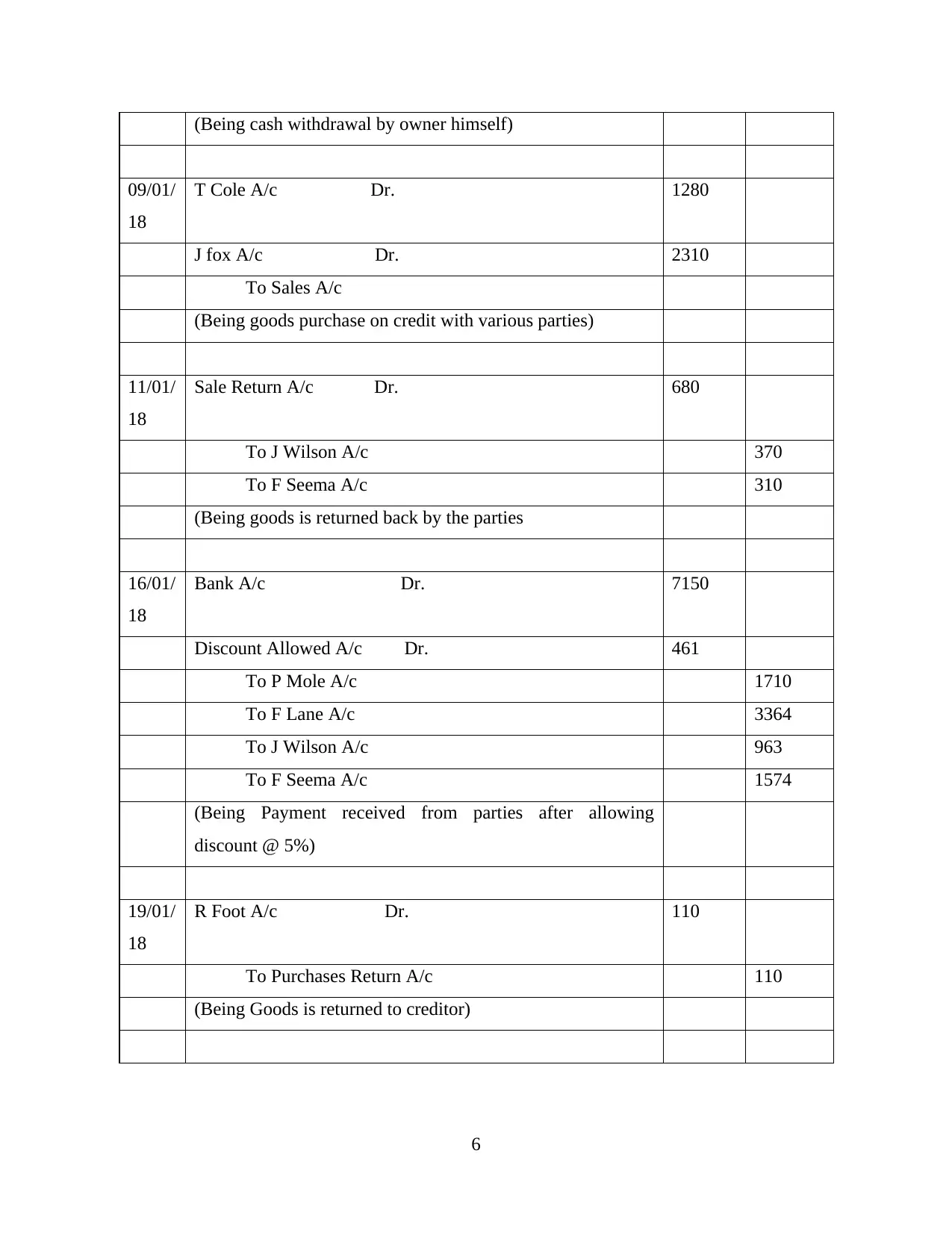

CLIENT 1

(a) Journal Entry in the books of David Study

Date Particulars Debit Credit

01/01/

18

Premises A/c Dr. 440000

Motor Van A/c Dr. 45250

fixtures A/c Dr. 10100

Inventory A/c Dr. 40900

P Mole A/c Dr. 2200

F Lane A/c Dr. 2100

Bank A/c Dr. 42400

Cash A/c Dr. 10600

To S Hamid A/c 10150

To J. Brown A/c 9600

To Capital A/c (Balancing Figure) 573800

(Being Owner's Capital is calculated )

Therefore, David Study's Capital at 1st January = £

573800

Date Particulars Debit Credit

01/01/ Storage cost A/c Dr. 800

4

comparison more convenient (Edwards, 2013).

Convention of material disclosure: According to this method it is necessary for an

organisation to disclose all facts and figures which are related to the business of company. As a

result, accurate and relevant information and data can be presented to the public or reader who

reads the financial statement of corporation. It helps to provide required information to the

stakeholders of organisation and on the basis of this data they can take investment decisions.

CLIENT 1

(a) Journal Entry in the books of David Study

Date Particulars Debit Credit

01/01/

18

Premises A/c Dr. 440000

Motor Van A/c Dr. 45250

fixtures A/c Dr. 10100

Inventory A/c Dr. 40900

P Mole A/c Dr. 2200

F Lane A/c Dr. 2100

Bank A/c Dr. 42400

Cash A/c Dr. 10600

To S Hamid A/c 10150

To J. Brown A/c 9600

To Capital A/c (Balancing Figure) 573800

(Being Owner's Capital is calculated )

Therefore, David Study's Capital at 1st January = £

573800

Date Particulars Debit Credit

01/01/ Storage cost A/c Dr. 800

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

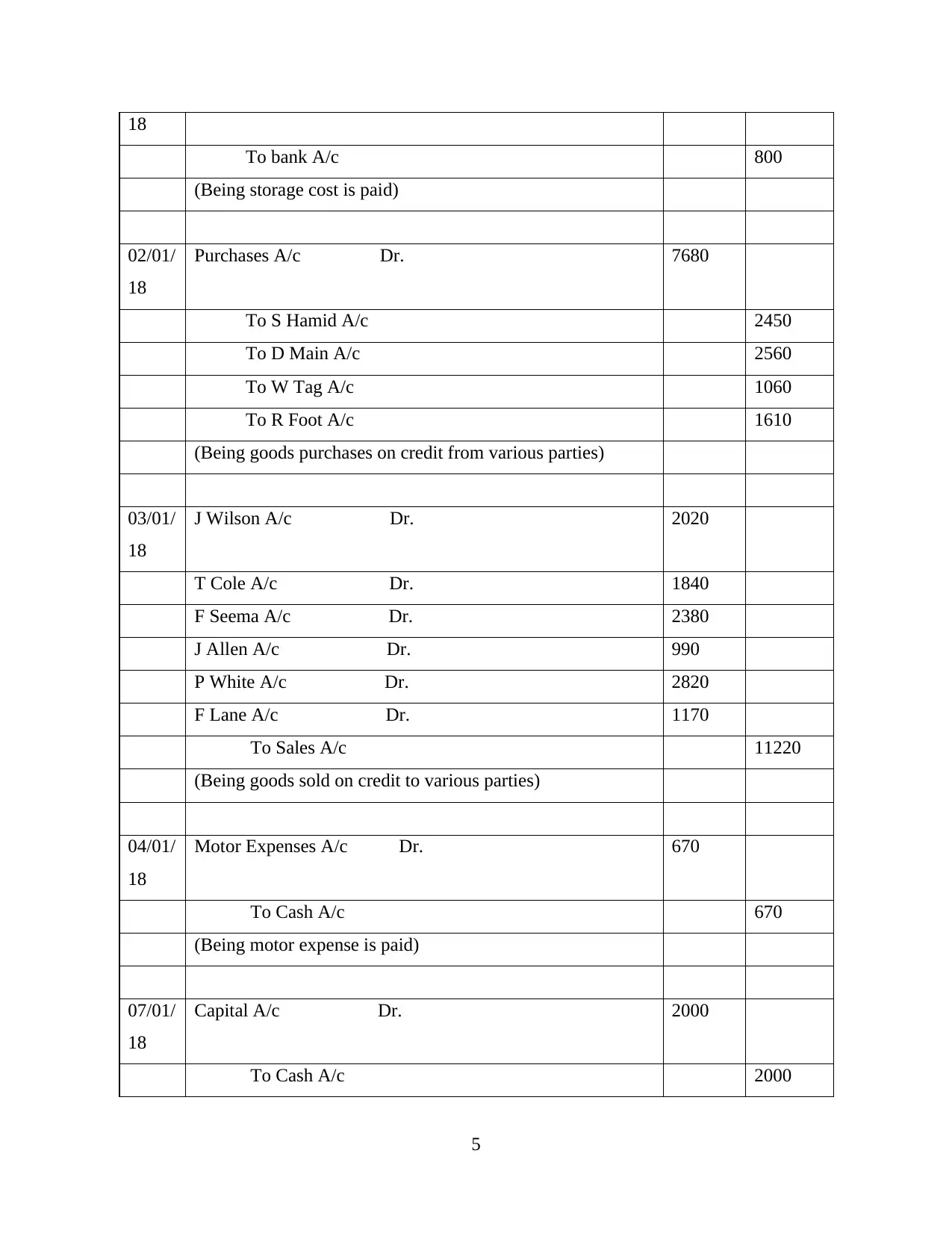

18

To bank A/c 800

(Being storage cost is paid)

02/01/

18

Purchases A/c Dr. 7680

To S Hamid A/c 2450

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/

18

J Wilson A/c Dr. 2020

T Cole A/c Dr. 1840

F Seema A/c Dr. 2380

J Allen A/c Dr. 990

P White A/c Dr. 2820

F Lane A/c Dr. 1170

To Sales A/c 11220

(Being goods sold on credit to various parties)

04/01/

18

Motor Expenses A/c Dr. 670

To Cash A/c 670

(Being motor expense is paid)

07/01/

18

Capital A/c Dr. 2000

To Cash A/c 2000

5

To bank A/c 800

(Being storage cost is paid)

02/01/

18

Purchases A/c Dr. 7680

To S Hamid A/c 2450

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/

18

J Wilson A/c Dr. 2020

T Cole A/c Dr. 1840

F Seema A/c Dr. 2380

J Allen A/c Dr. 990

P White A/c Dr. 2820

F Lane A/c Dr. 1170

To Sales A/c 11220

(Being goods sold on credit to various parties)

04/01/

18

Motor Expenses A/c Dr. 670

To Cash A/c 670

(Being motor expense is paid)

07/01/

18

Capital A/c Dr. 2000

To Cash A/c 2000

5

(Being cash withdrawal by owner himself)

09/01/

18

T Cole A/c Dr. 1280

J fox A/c Dr. 2310

To Sales A/c

(Being goods purchase on credit with various parties)

11/01/

18

Sale Return A/c Dr. 680

To J Wilson A/c 370

To F Seema A/c 310

(Being goods is returned back by the parties

16/01/

18

Bank A/c Dr. 7150

Discount Allowed A/c Dr. 461

To P Mole A/c 1710

To F Lane A/c 3364

To J Wilson A/c 963

To F Seema A/c 1574

(Being Payment received from parties after allowing

discount @ 5%)

19/01/

18

R Foot A/c Dr. 110

To Purchases Return A/c 110

(Being Goods is returned to creditor)

6

09/01/

18

T Cole A/c Dr. 1280

J fox A/c Dr. 2310

To Sales A/c

(Being goods purchase on credit with various parties)

11/01/

18

Sale Return A/c Dr. 680

To J Wilson A/c 370

To F Seema A/c 310

(Being goods is returned back by the parties

16/01/

18

Bank A/c Dr. 7150

Discount Allowed A/c Dr. 461

To P Mole A/c 1710

To F Lane A/c 3364

To J Wilson A/c 963

To F Seema A/c 1574

(Being Payment received from parties after allowing

discount @ 5%)

19/01/

18

R Foot A/c Dr. 110

To Purchases Return A/c 110

(Being Goods is returned to creditor)

6

22/01/

18

Purchases A/c Dr. 3140

To L Mole A/c 1330

To W Wright A/c 1810

(Being goods purchased on credit)

24/01/

18

S Hamid A/c Dr. 3860

J Brown A/c Dr. 4260

R Foot A/c Dr. 1750

To Bank A/c 7500

To Discount Recieved A/c 2370

(Being payment is made to creditors after receiving discount

@ 10%)

27/01/

18

Salaries A/c Dr. 14500

To Bank A/c 14500

(Being salaries are paid through cheque)

30/01/

18

Business Rates A/c Dr. 2220

To Bank A/c 2220

(Being business rates are paid through cheque)

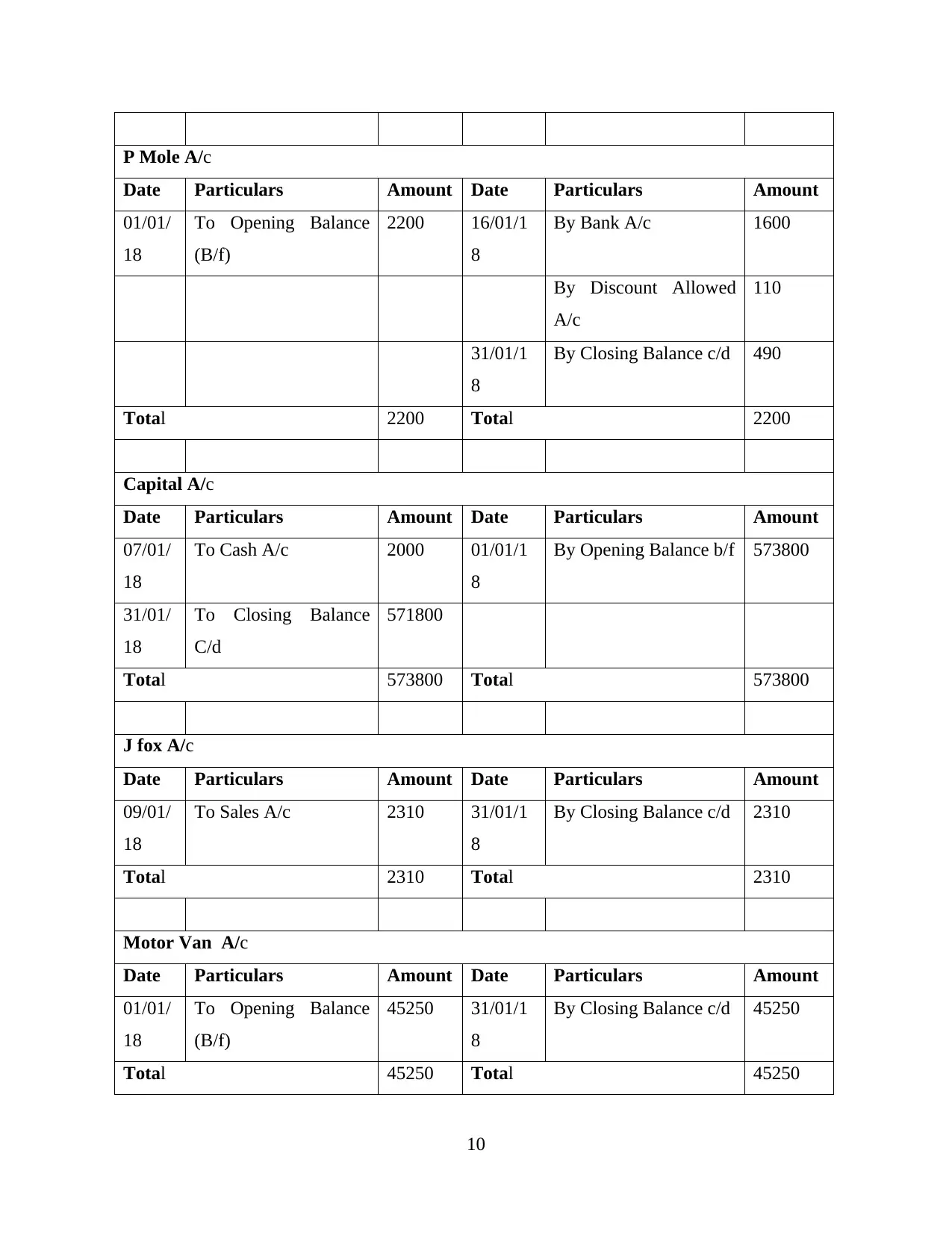

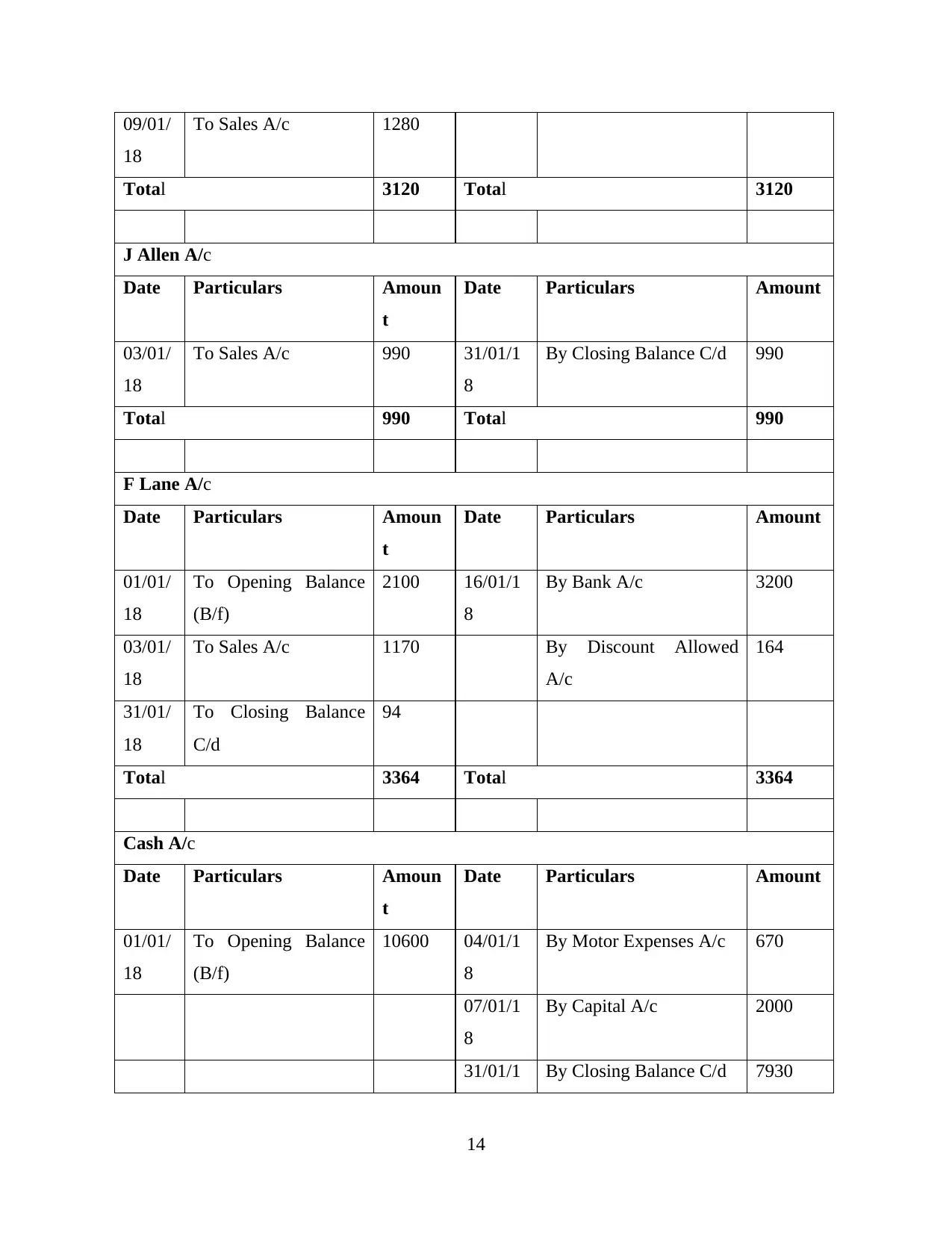

(b) Ledger Accounts

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/

18

To Bank A/c 800 31/07/1

8

By Profit & Loss A/c 800

Total 800 Total 800

7

18

Purchases A/c Dr. 3140

To L Mole A/c 1330

To W Wright A/c 1810

(Being goods purchased on credit)

24/01/

18

S Hamid A/c Dr. 3860

J Brown A/c Dr. 4260

R Foot A/c Dr. 1750

To Bank A/c 7500

To Discount Recieved A/c 2370

(Being payment is made to creditors after receiving discount

@ 10%)

27/01/

18

Salaries A/c Dr. 14500

To Bank A/c 14500

(Being salaries are paid through cheque)

30/01/

18

Business Rates A/c Dr. 2220

To Bank A/c 2220

(Being business rates are paid through cheque)

(b) Ledger Accounts

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/

18

To Bank A/c 800 31/07/1

8

By Profit & Loss A/c 800

Total 800 Total 800

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Sales A/c

Date Particulars Amount Date Particulars Amount

31/01/

18

To Trading and P&L

A/c

14810 03/01/1

8

By J Wilson A/c 2020

By T Cole A/c 1840

By F Seema A/c 2380

By J Allen A/c 990

By P White A/c 2820

By F Lane A/c 1170

09/01/1

8

By T Cole A/c 1280

By J fox A/c 2310

Total 14810 Total 14810

S Hamid A/c

Date Particulars Amount Date Particulars Amount

24/01/

18

To Discount Received

A/c

1260 01/01/1

8

By Opening Balance

(B/f)

10150

To Bank A/c 2600 02/01/1

8

By purchases A/c 2450

31/01/

18

To Closing Balance

C/d

8740

Total 12600 Total 12600

W Tag A/c

Date Particulars Amount Date Particulars Amount

31/01/

18

To Closing Balance

C/d

1060 02/01/1

8

By purchases A/c 1060

Total 1060 Total 1060

8

Date Particulars Amount Date Particulars Amount

31/01/

18

To Trading and P&L

A/c

14810 03/01/1

8

By J Wilson A/c 2020

By T Cole A/c 1840

By F Seema A/c 2380

By J Allen A/c 990

By P White A/c 2820

By F Lane A/c 1170

09/01/1

8

By T Cole A/c 1280

By J fox A/c 2310

Total 14810 Total 14810

S Hamid A/c

Date Particulars Amount Date Particulars Amount

24/01/

18

To Discount Received

A/c

1260 01/01/1

8

By Opening Balance

(B/f)

10150

To Bank A/c 2600 02/01/1

8

By purchases A/c 2450

31/01/

18

To Closing Balance

C/d

8740

Total 12600 Total 12600

W Tag A/c

Date Particulars Amount Date Particulars Amount

31/01/

18

To Closing Balance

C/d

1060 02/01/1

8

By purchases A/c 1060

Total 1060 Total 1060

8

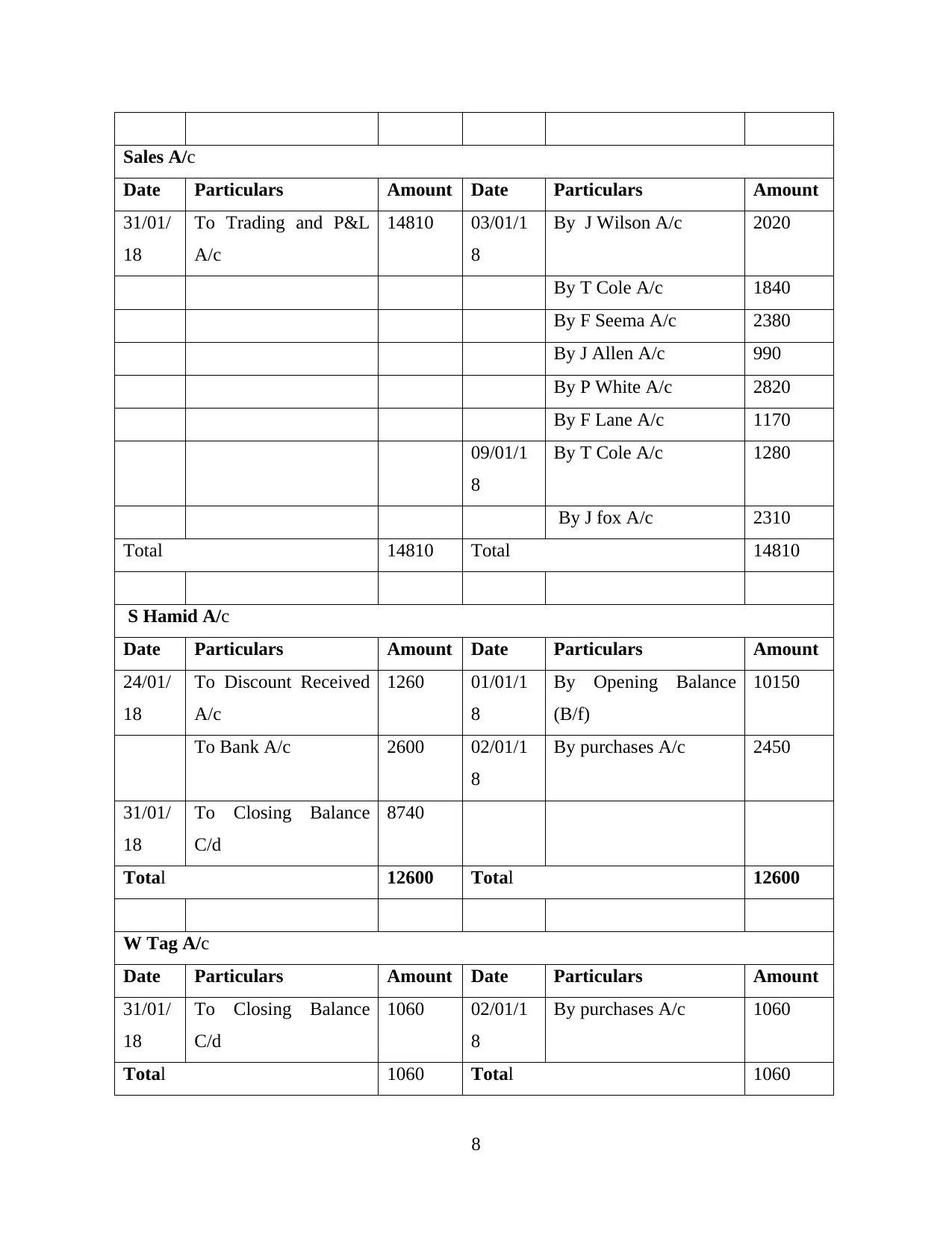

J Wilson A/c

Date Particulars Amount Date Particulars Amount

03/01/

18

To Sales A/c 2020 11/01/1

8

By Sales Return A/c 370

16/01/1

8

By Bank A/c 880

By Discount Allowed

A/c

83

31/01/1

8

By Closing Balance c/d 687

Total 2020 Total 2020

F Seema A/c

Date Particulars Amount Date Particulars Amount

03/01/

18

To Sales A/c 2380 11/01/1

8

By Sales Return A/c 310

16/01/1

8

By Bank A/c 1470

By Discount Allowed

A/c

104

31/01/1

8

By Closing Balance c/d 496

Total 2380 Total 2380

P White A/c

Date Particulars Amount Date Particulars Amount

03/01/

18

To Sales A/c 2820 31/01/1

8

By Closing Balance c/d 2820

Total 2820 Total 2820

9

Date Particulars Amount Date Particulars Amount

03/01/

18

To Sales A/c 2020 11/01/1

8

By Sales Return A/c 370

16/01/1

8

By Bank A/c 880

By Discount Allowed

A/c

83

31/01/1

8

By Closing Balance c/d 687

Total 2020 Total 2020

F Seema A/c

Date Particulars Amount Date Particulars Amount

03/01/

18

To Sales A/c 2380 11/01/1

8

By Sales Return A/c 310

16/01/1

8

By Bank A/c 1470

By Discount Allowed

A/c

104

31/01/1

8

By Closing Balance c/d 496

Total 2380 Total 2380

P White A/c

Date Particulars Amount Date Particulars Amount

03/01/

18

To Sales A/c 2820 31/01/1

8

By Closing Balance c/d 2820

Total 2820 Total 2820

9

P Mole A/c

Date Particulars Amount Date Particulars Amount

01/01/

18

To Opening Balance

(B/f)

2200 16/01/1

8

By Bank A/c 1600

By Discount Allowed

A/c

110

31/01/1

8

By Closing Balance c/d 490

Total 2200 Total 2200

Capital A/c

Date Particulars Amount Date Particulars Amount

07/01/

18

To Cash A/c 2000 01/01/1

8

By Opening Balance b/f 573800

31/01/

18

To Closing Balance

C/d

571800

Total 573800 Total 573800

J fox A/c

Date Particulars Amount Date Particulars Amount

09/01/

18

To Sales A/c 2310 31/01/1

8

By Closing Balance c/d 2310

Total 2310 Total 2310

Motor Van A/c

Date Particulars Amount Date Particulars Amount

01/01/

18

To Opening Balance

(B/f)

45250 31/01/1

8

By Closing Balance c/d 45250

Total 45250 Total 45250

10

Date Particulars Amount Date Particulars Amount

01/01/

18

To Opening Balance

(B/f)

2200 16/01/1

8

By Bank A/c 1600

By Discount Allowed

A/c

110

31/01/1

8

By Closing Balance c/d 490

Total 2200 Total 2200

Capital A/c

Date Particulars Amount Date Particulars Amount

07/01/

18

To Cash A/c 2000 01/01/1

8

By Opening Balance b/f 573800

31/01/

18

To Closing Balance

C/d

571800

Total 573800 Total 573800

J fox A/c

Date Particulars Amount Date Particulars Amount

09/01/

18

To Sales A/c 2310 31/01/1

8

By Closing Balance c/d 2310

Total 2310 Total 2310

Motor Van A/c

Date Particulars Amount Date Particulars Amount

01/01/

18

To Opening Balance

(B/f)

45250 31/01/1

8

By Closing Balance c/d 45250

Total 45250 Total 45250

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

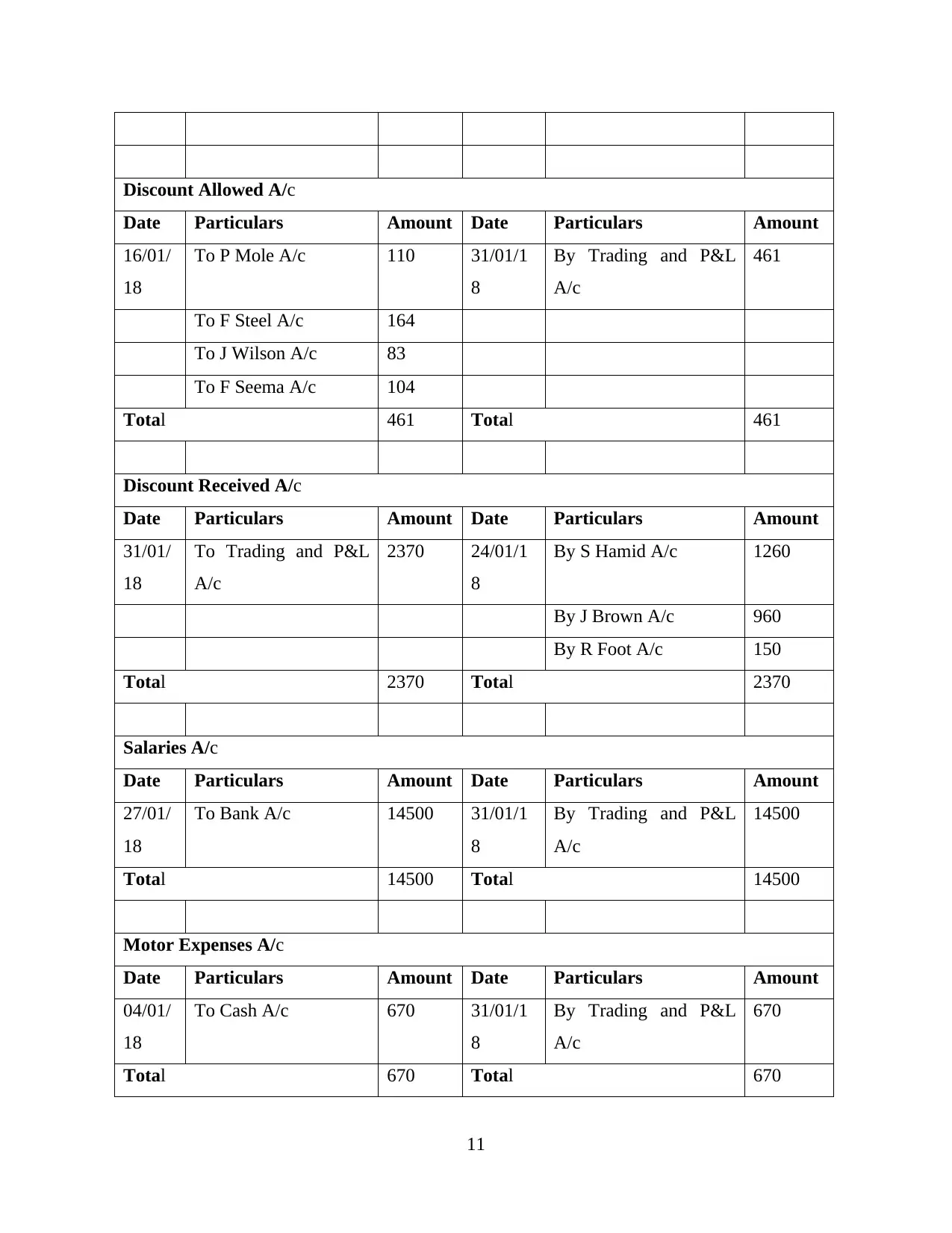

Discount Allowed A/c

Date Particulars Amount Date Particulars Amount

16/01/

18

To P Mole A/c 110 31/01/1

8

By Trading and P&L

A/c

461

To F Steel A/c 164

To J Wilson A/c 83

To F Seema A/c 104

Total 461 Total 461

Discount Received A/c

Date Particulars Amount Date Particulars Amount

31/01/

18

To Trading and P&L

A/c

2370 24/01/1

8

By S Hamid A/c 1260

By J Brown A/c 960

By R Foot A/c 150

Total 2370 Total 2370

Salaries A/c

Date Particulars Amount Date Particulars Amount

27/01/

18

To Bank A/c 14500 31/01/1

8

By Trading and P&L

A/c

14500

Total 14500 Total 14500

Motor Expenses A/c

Date Particulars Amount Date Particulars Amount

04/01/

18

To Cash A/c 670 31/01/1

8

By Trading and P&L

A/c

670

Total 670 Total 670

11

Date Particulars Amount Date Particulars Amount

16/01/

18

To P Mole A/c 110 31/01/1

8

By Trading and P&L

A/c

461

To F Steel A/c 164

To J Wilson A/c 83

To F Seema A/c 104

Total 461 Total 461

Discount Received A/c

Date Particulars Amount Date Particulars Amount

31/01/

18

To Trading and P&L

A/c

2370 24/01/1

8

By S Hamid A/c 1260

By J Brown A/c 960

By R Foot A/c 150

Total 2370 Total 2370

Salaries A/c

Date Particulars Amount Date Particulars Amount

27/01/

18

To Bank A/c 14500 31/01/1

8

By Trading and P&L

A/c

14500

Total 14500 Total 14500

Motor Expenses A/c

Date Particulars Amount Date Particulars Amount

04/01/

18

To Cash A/c 670 31/01/1

8

By Trading and P&L

A/c

670

Total 670 Total 670

11

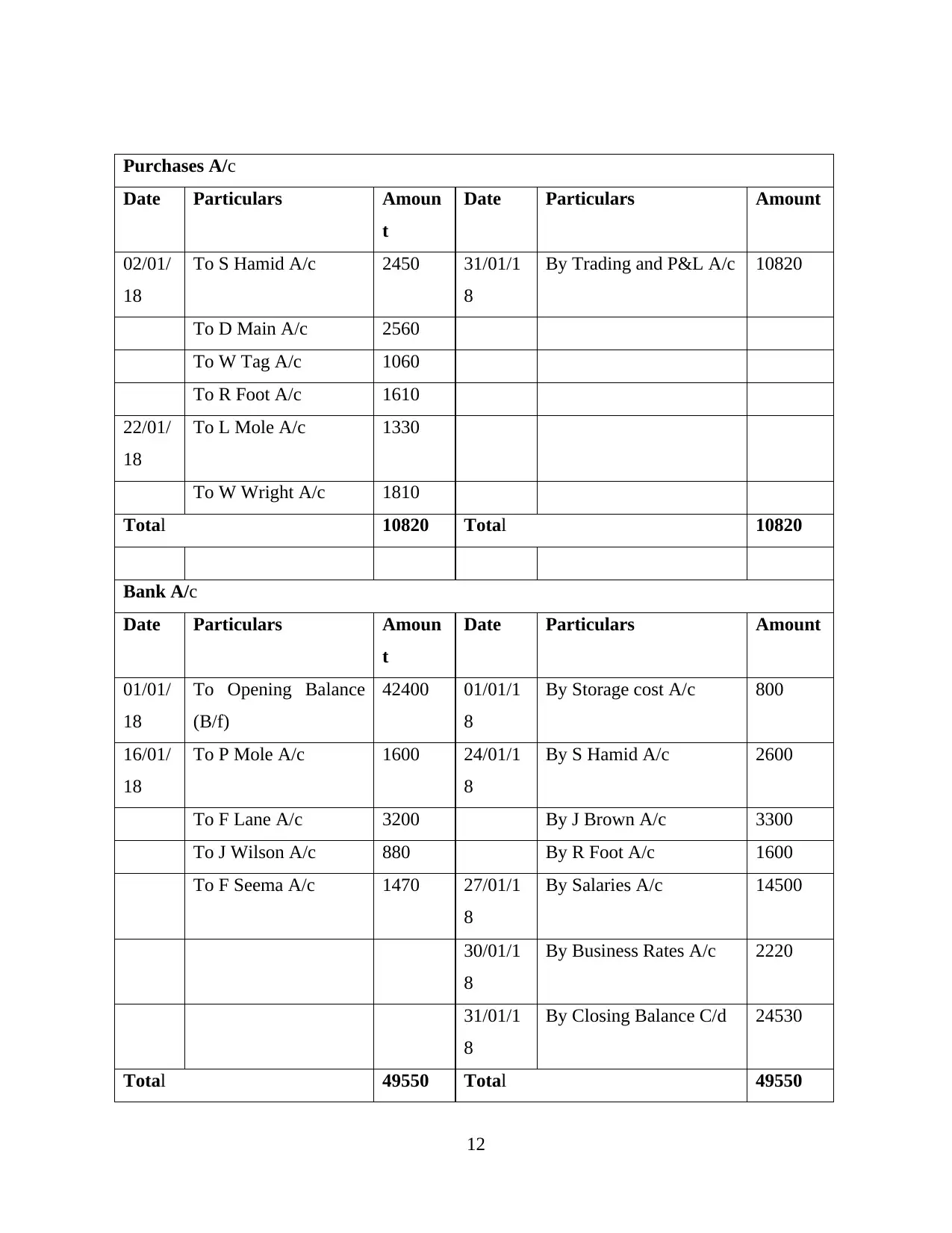

Purchases A/c

Date Particulars Amoun

t

Date Particulars Amount

02/01/

18

To S Hamid A/c 2450 31/01/1

8

By Trading and P&L A/c 10820

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

22/01/

18

To L Mole A/c 1330

To W Wright A/c 1810

Total 10820 Total 10820

Bank A/c

Date Particulars Amoun

t

Date Particulars Amount

01/01/

18

To Opening Balance

(B/f)

42400 01/01/1

8

By Storage cost A/c 800

16/01/

18

To P Mole A/c 1600 24/01/1

8

By S Hamid A/c 2600

To F Lane A/c 3200 By J Brown A/c 3300

To J Wilson A/c 880 By R Foot A/c 1600

To F Seema A/c 1470 27/01/1

8

By Salaries A/c 14500

30/01/1

8

By Business Rates A/c 2220

31/01/1

8

By Closing Balance C/d 24530

Total 49550 Total 49550

12

Date Particulars Amoun

t

Date Particulars Amount

02/01/

18

To S Hamid A/c 2450 31/01/1

8

By Trading and P&L A/c 10820

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

22/01/

18

To L Mole A/c 1330

To W Wright A/c 1810

Total 10820 Total 10820

Bank A/c

Date Particulars Amoun

t

Date Particulars Amount

01/01/

18

To Opening Balance

(B/f)

42400 01/01/1

8

By Storage cost A/c 800

16/01/

18

To P Mole A/c 1600 24/01/1

8

By S Hamid A/c 2600

To F Lane A/c 3200 By J Brown A/c 3300

To J Wilson A/c 880 By R Foot A/c 1600

To F Seema A/c 1470 27/01/1

8

By Salaries A/c 14500

30/01/1

8

By Business Rates A/c 2220

31/01/1

8

By Closing Balance C/d 24530

Total 49550 Total 49550

12

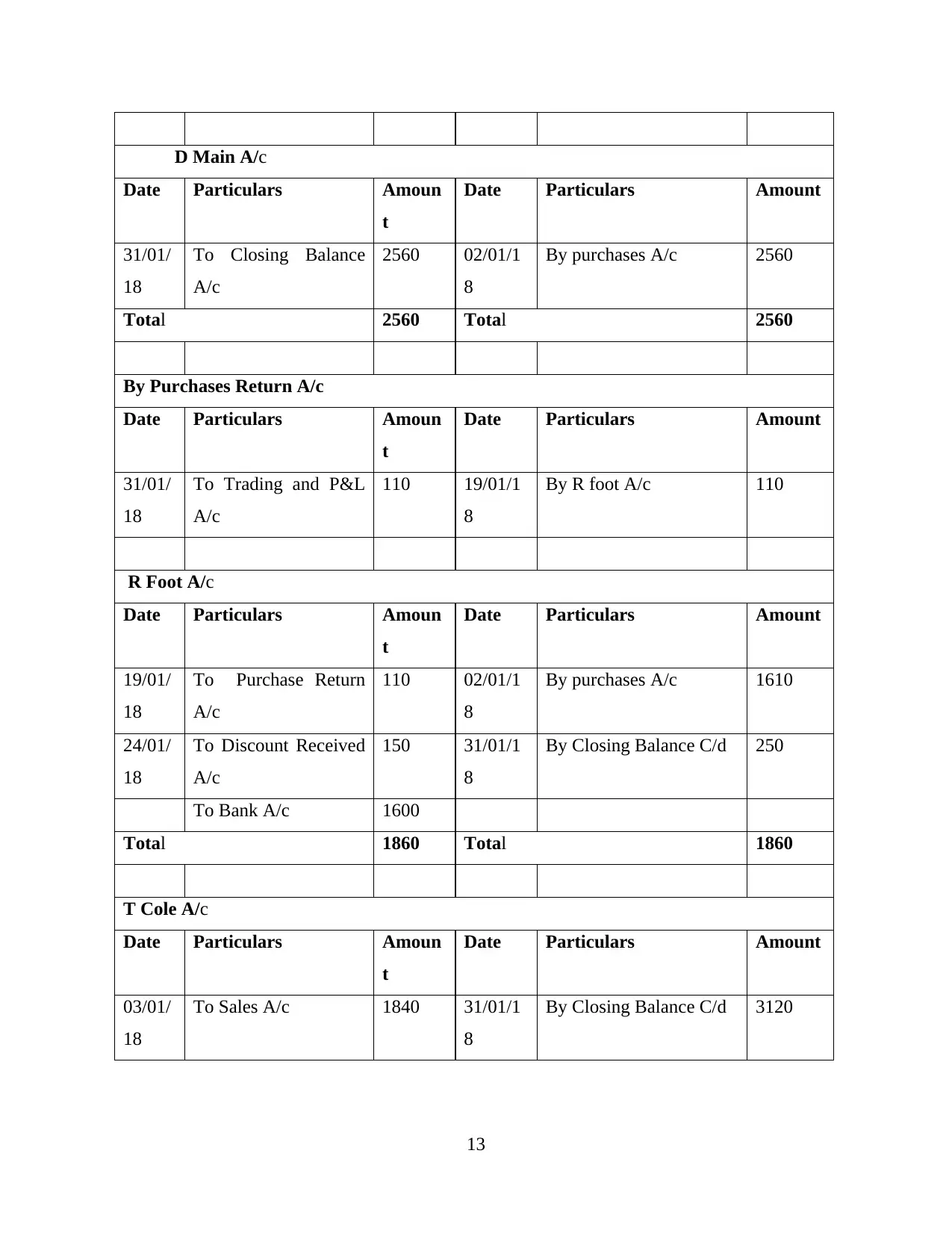

D Main A/c

Date Particulars Amoun

t

Date Particulars Amount

31/01/

18

To Closing Balance

A/c

2560 02/01/1

8

By purchases A/c 2560

Total 2560 Total 2560

By Purchases Return A/c

Date Particulars Amoun

t

Date Particulars Amount

31/01/

18

To Trading and P&L

A/c

110 19/01/1

8

By R foot A/c 110

R Foot A/c

Date Particulars Amoun

t

Date Particulars Amount

19/01/

18

To Purchase Return

A/c

110 02/01/1

8

By purchases A/c 1610

24/01/

18

To Discount Received

A/c

150 31/01/1

8

By Closing Balance C/d 250

To Bank A/c 1600

Total 1860 Total 1860

T Cole A/c

Date Particulars Amoun

t

Date Particulars Amount

03/01/

18

To Sales A/c 1840 31/01/1

8

By Closing Balance C/d 3120

13

Date Particulars Amoun

t

Date Particulars Amount

31/01/

18

To Closing Balance

A/c

2560 02/01/1

8

By purchases A/c 2560

Total 2560 Total 2560

By Purchases Return A/c

Date Particulars Amoun

t

Date Particulars Amount

31/01/

18

To Trading and P&L

A/c

110 19/01/1

8

By R foot A/c 110

R Foot A/c

Date Particulars Amoun

t

Date Particulars Amount

19/01/

18

To Purchase Return

A/c

110 02/01/1

8

By purchases A/c 1610

24/01/

18

To Discount Received

A/c

150 31/01/1

8

By Closing Balance C/d 250

To Bank A/c 1600

Total 1860 Total 1860

T Cole A/c

Date Particulars Amoun

t

Date Particulars Amount

03/01/

18

To Sales A/c 1840 31/01/1

8

By Closing Balance C/d 3120

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

09/01/

18

To Sales A/c 1280

Total 3120 Total 3120

J Allen A/c

Date Particulars Amoun

t

Date Particulars Amount

03/01/

18

To Sales A/c 990 31/01/1

8

By Closing Balance C/d 990

Total 990 Total 990

F Lane A/c

Date Particulars Amoun

t

Date Particulars Amount

01/01/

18

To Opening Balance

(B/f)

2100 16/01/1

8

By Bank A/c 3200

03/01/

18

To Sales A/c 1170 By Discount Allowed

A/c

164

31/01/

18

To Closing Balance

C/d

94

Total 3364 Total 3364

Cash A/c

Date Particulars Amoun

t

Date Particulars Amount

01/01/

18

To Opening Balance

(B/f)

10600 04/01/1

8

By Motor Expenses A/c 670

07/01/1

8

By Capital A/c 2000

31/01/1 By Closing Balance C/d 7930

14

18

To Sales A/c 1280

Total 3120 Total 3120

J Allen A/c

Date Particulars Amoun

t

Date Particulars Amount

03/01/

18

To Sales A/c 990 31/01/1

8

By Closing Balance C/d 990

Total 990 Total 990

F Lane A/c

Date Particulars Amoun

t

Date Particulars Amount

01/01/

18

To Opening Balance

(B/f)

2100 16/01/1

8

By Bank A/c 3200

03/01/

18

To Sales A/c 1170 By Discount Allowed

A/c

164

31/01/

18

To Closing Balance

C/d

94

Total 3364 Total 3364

Cash A/c

Date Particulars Amoun

t

Date Particulars Amount

01/01/

18

To Opening Balance

(B/f)

10600 04/01/1

8

By Motor Expenses A/c 670

07/01/1

8

By Capital A/c 2000

31/01/1 By Closing Balance C/d 7930

14

8

Total 10600 Total 10600

Sales Return A/c

Date Particulars Amoun

t

Date Particulars Amount

11/01/

18

To J Wilson A/c 370 31/01/1

8

By Trading and P&L A/c 680

To F Seema A/c 310

Total 680 Total 680

L Mole A/c

Date Particulars Amoun

t

Date Particulars Amount

31/01/

18

To Closing Balance

C/d

1330 22/01/1

8

By Purchases A/c 1330

Total 1330 Total 1330

W Wright A/c

Date Particulars Amoun

t

Date Particulars Amount

31/01/

18

To Closing Balance

C/d

1810 22/01/1

8

By Purchases A/c 1810

Total 1810 Total 1810

J Brown A/c

Date Particulars Amoun

t

Date Particulars Amount

24/01/

18

To Discount Received

A/c

960 01/01/1

8

By Opening Balance b/f 9600

15

Total 10600 Total 10600

Sales Return A/c

Date Particulars Amoun

t

Date Particulars Amount

11/01/

18

To J Wilson A/c 370 31/01/1

8

By Trading and P&L A/c 680

To F Seema A/c 310

Total 680 Total 680

L Mole A/c

Date Particulars Amoun

t

Date Particulars Amount

31/01/

18

To Closing Balance

C/d

1330 22/01/1

8

By Purchases A/c 1330

Total 1330 Total 1330

W Wright A/c

Date Particulars Amoun

t

Date Particulars Amount

31/01/

18

To Closing Balance

C/d

1810 22/01/1

8

By Purchases A/c 1810

Total 1810 Total 1810

J Brown A/c

Date Particulars Amoun

t

Date Particulars Amount

24/01/

18

To Discount Received

A/c

960 01/01/1

8

By Opening Balance b/f 9600

15

To Bank A/c 3300 31/01/1

8

By Closing Balance C/d

31/01/

18

To Closing Balance

C/d

5340

Total 9600 Total 9600

Business Rates A/c

Date Particulars Amoun

t

Date Particulars Amount

30/01/

18

To Bank A/c 2220 31/01/1

8

By Trading and P&L A/c 2220

Total 2220 Total 2220

(c) Trial Balance as at 31st January, 2018

Trial Balance for the month of July

Particulars Debit Credit

Purchases 10820 -

Bank 24530 -

D Main - 2560

Purchases Return - 110

R Foot 250 -

T Cole 3120 -

J Allen 990 -

F Lane - 94

Cash 7930 -

Sales Return 680 -

L Mole - 1330

W Wright - 1810

J Brown - 5340

16

8

By Closing Balance C/d

31/01/

18

To Closing Balance

C/d

5340

Total 9600 Total 9600

Business Rates A/c

Date Particulars Amoun

t

Date Particulars Amount

30/01/

18

To Bank A/c 2220 31/01/1

8

By Trading and P&L A/c 2220

Total 2220 Total 2220

(c) Trial Balance as at 31st January, 2018

Trial Balance for the month of July

Particulars Debit Credit

Purchases 10820 -

Bank 24530 -

D Main - 2560

Purchases Return - 110

R Foot 250 -

T Cole 3120 -

J Allen 990 -

F Lane - 94

Cash 7930 -

Sales Return 680 -

L Mole - 1330

W Wright - 1810

J Brown - 5340

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

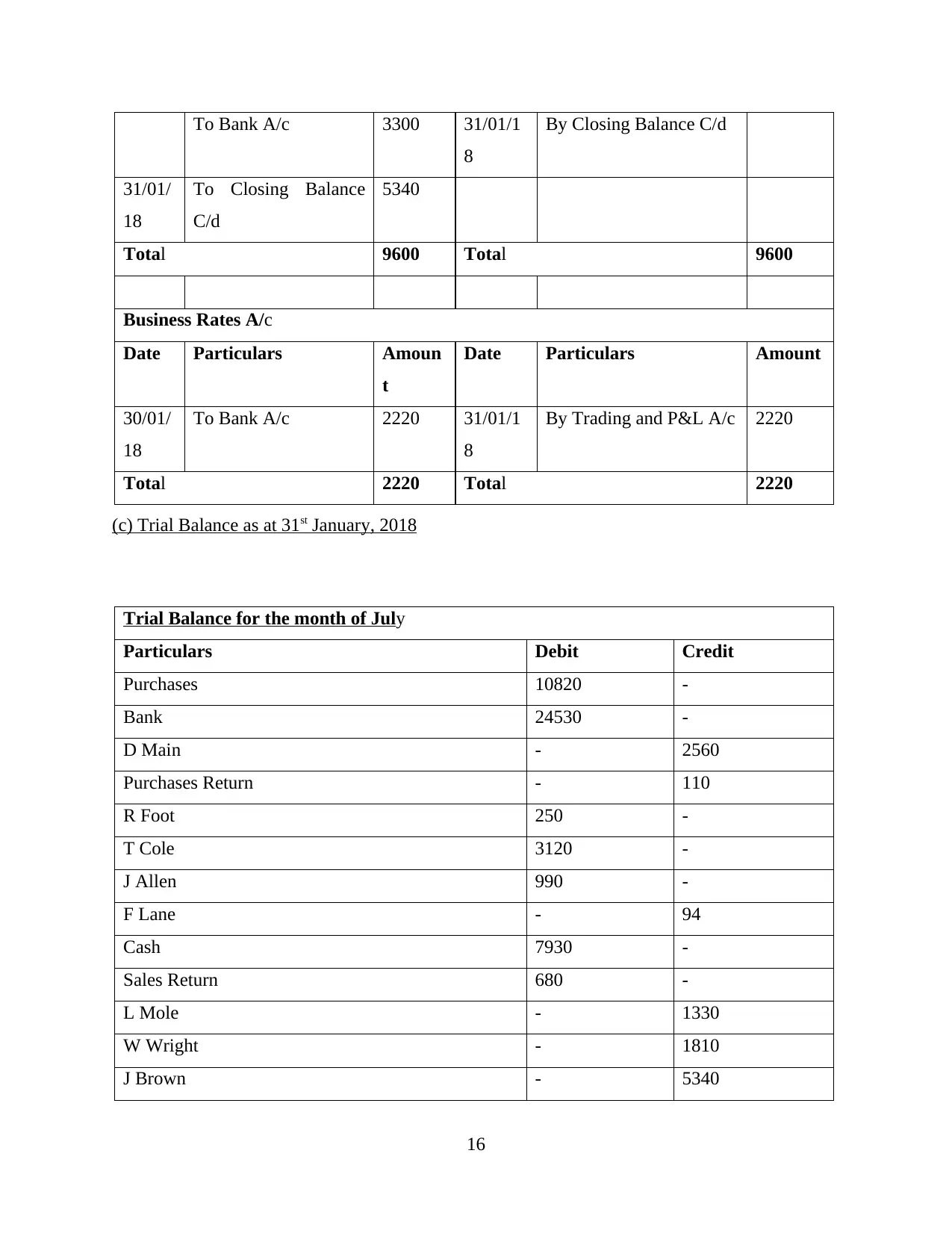

Business Rates 2220 -

Storage cost 800 -

Sales - 14810

S Hamid - 8740

W Tag - 1060

J Wilson 687 -

F Seema 496 -

P White 2820 -

P Mole 490 -

Capital - 571800

J fox 2310 -

Motor Van 45250 -

Discount Allowed 461 -

Discount Received - 2370

Salaries 14500 -

Motor Expenses 670 -

Premises 440000 -

Fixtures 10100 -

inventory 40900 -

Total 610024 610024

CLIENT 2

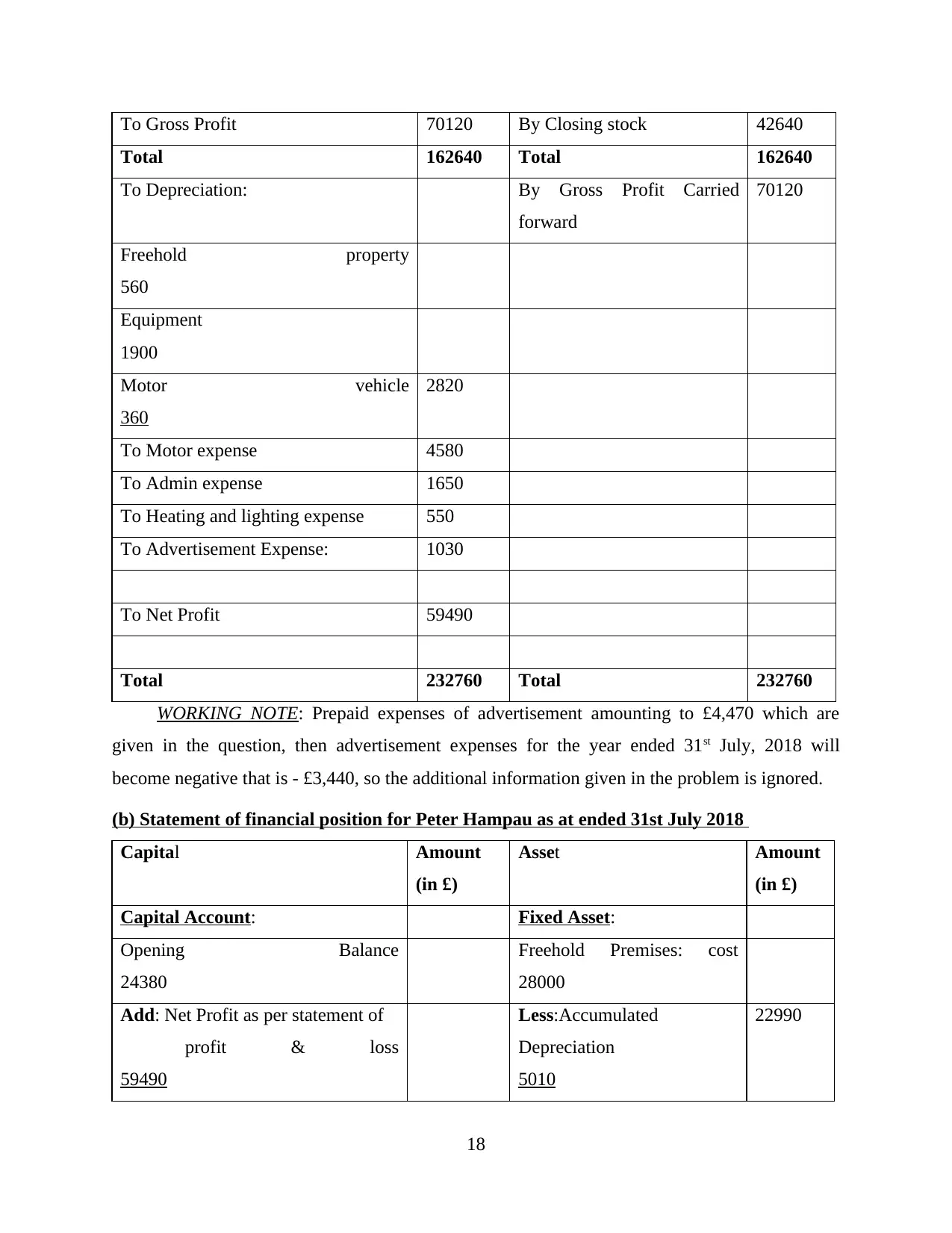

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018

Particulars Amount

(in £)

Particulars Amount

(in £)

To Opening stock 4500 By Sales 120000

To Purchase 70000

To Wages and salaries:

16500

Add: Outstanding wages & salaries

1520

18020

17

Storage cost 800 -

Sales - 14810

S Hamid - 8740

W Tag - 1060

J Wilson 687 -

F Seema 496 -

P White 2820 -

P Mole 490 -

Capital - 571800

J fox 2310 -

Motor Van 45250 -

Discount Allowed 461 -

Discount Received - 2370

Salaries 14500 -

Motor Expenses 670 -

Premises 440000 -

Fixtures 10100 -

inventory 40900 -

Total 610024 610024

CLIENT 2

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018

Particulars Amount

(in £)

Particulars Amount

(in £)

To Opening stock 4500 By Sales 120000

To Purchase 70000

To Wages and salaries:

16500

Add: Outstanding wages & salaries

1520

18020

17

To Gross Profit 70120 By Closing stock 42640

Total 162640 Total 162640

To Depreciation: By Gross Profit Carried

forward

70120

Freehold property

560

Equipment

1900

Motor vehicle

360

2820

To Motor expense 4580

To Admin expense 1650

To Heating and lighting expense 550

To Advertisement Expense: 1030

To Net Profit 59490

Total 232760 Total 232760

WORKING NOTE: Prepaid expenses of advertisement amounting to £4,470 which are

given in the question, then advertisement expenses for the year ended 31st July, 2018 will

become negative that is - £3,440, so the additional information given in the problem is ignored.

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018

Capital Amount

(in £)

Asset Amount

(in £)

Capital Account: Fixed Asset:

Opening Balance

24380

Freehold Premises: cost

28000

Add: Net Profit as per statement of

profit & loss

59490

Less:Accumulated

Depreciation

5010

22990

18

Total 162640 Total 162640

To Depreciation: By Gross Profit Carried

forward

70120

Freehold property

560

Equipment

1900

Motor vehicle

360

2820

To Motor expense 4580

To Admin expense 1650

To Heating and lighting expense 550

To Advertisement Expense: 1030

To Net Profit 59490

Total 232760 Total 232760

WORKING NOTE: Prepaid expenses of advertisement amounting to £4,470 which are

given in the question, then advertisement expenses for the year ended 31st July, 2018 will

become negative that is - £3,440, so the additional information given in the problem is ignored.

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018

Capital Amount

(in £)

Asset Amount

(in £)

Capital Account: Fixed Asset:

Opening Balance

24380

Freehold Premises: cost

28000

Add: Net Profit as per statement of

profit & loss

59490

Less:Accumulated

Depreciation

5010

22990

18

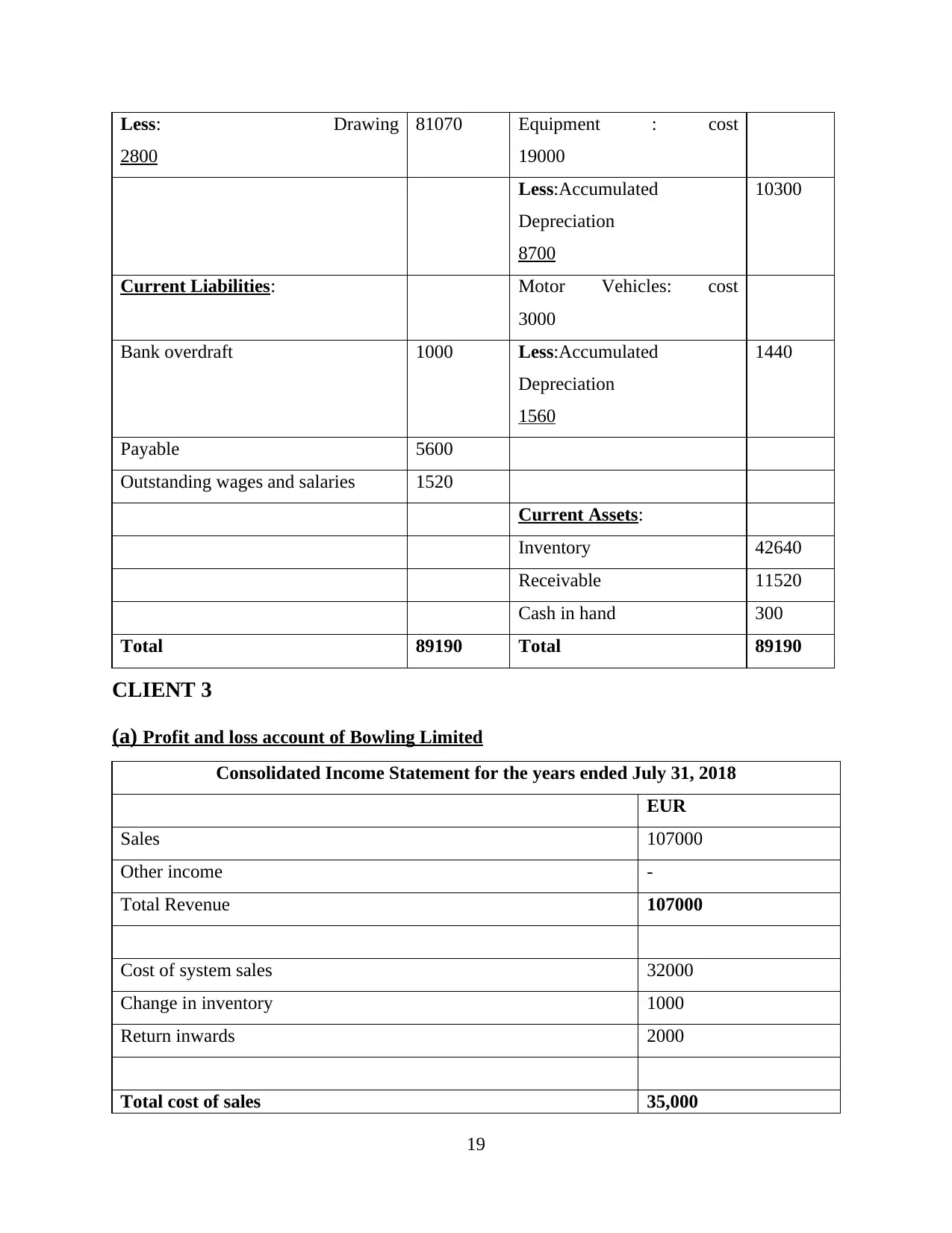

Less: Drawing

2800

81070 Equipment : cost

19000

Less:Accumulated

Depreciation

8700

10300

Current Liabilities: Motor Vehicles: cost

3000

Bank overdraft 1000 Less:Accumulated

Depreciation

1560

1440

Payable 5600

Outstanding wages and salaries 1520

Current Assets:

Inventory 42640

Receivable 11520

Cash in hand 300

Total 89190 Total 89190

CLIENT 3

(a) Profit and loss account of Bowling Limited

Consolidated Income Statement for the years ended July 31, 2018

EUR

Sales 107000

Other income -

Total Revenue 107000

Cost of system sales 32000

Change in inventory 1000

Return inwards 2000

Total cost of sales 35,000

19

2800

81070 Equipment : cost

19000

Less:Accumulated

Depreciation

8700

10300

Current Liabilities: Motor Vehicles: cost

3000

Bank overdraft 1000 Less:Accumulated

Depreciation

1560

1440

Payable 5600

Outstanding wages and salaries 1520

Current Assets:

Inventory 42640

Receivable 11520

Cash in hand 300

Total 89190 Total 89190

CLIENT 3

(a) Profit and loss account of Bowling Limited

Consolidated Income Statement for the years ended July 31, 2018

EUR

Sales 107000

Other income -

Total Revenue 107000

Cost of system sales 32000

Change in inventory 1000

Return inwards 2000

Total cost of sales 35,000

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

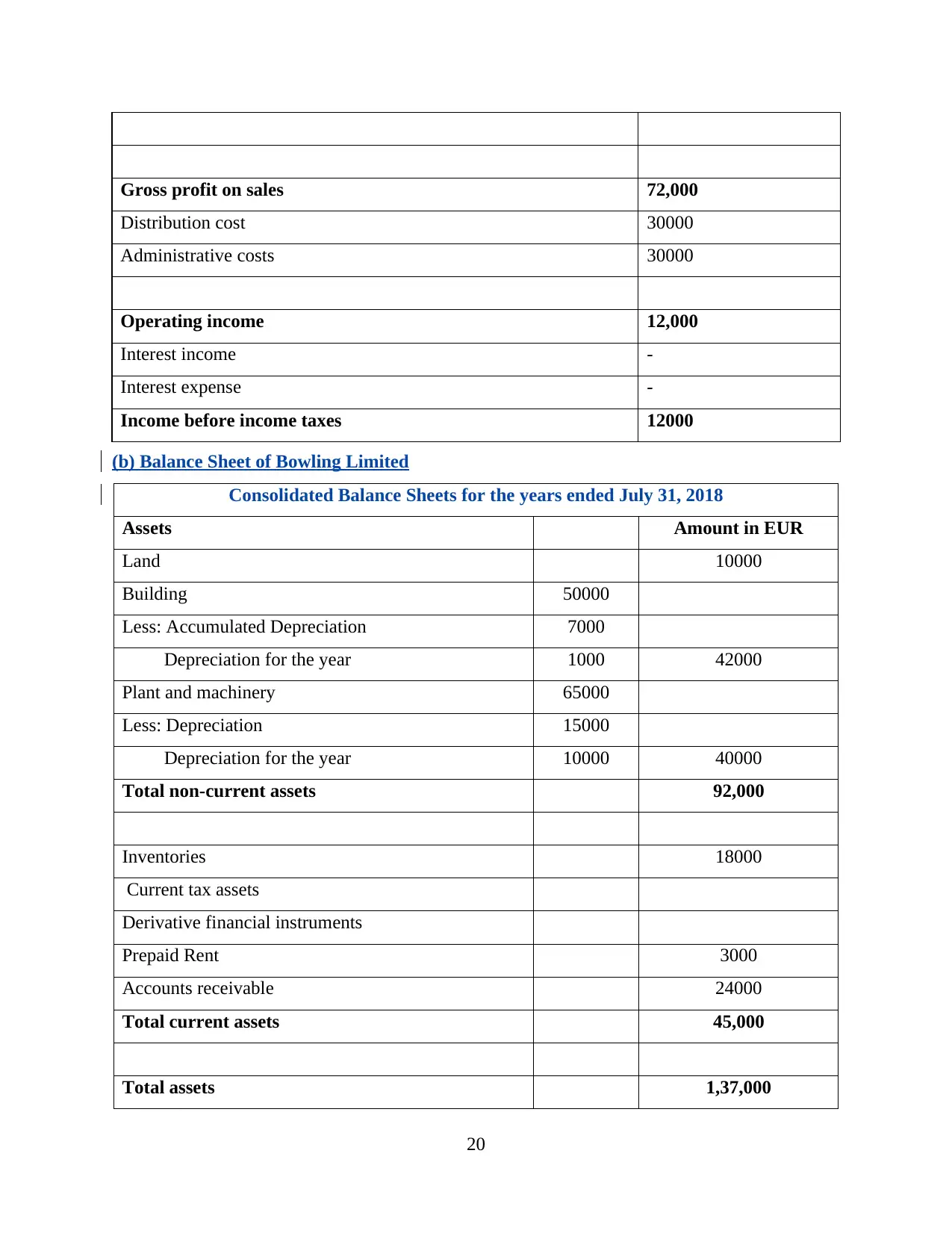

Gross profit on sales 72,000

Distribution cost 30000

Administrative costs 30000

Operating income 12,000

Interest income -

Interest expense -

Income before income taxes 12000

(b) Balance Sheet of Bowling Limited

Consolidated Balance Sheets for the years ended July 31, 2018

Assets Amount in EUR

Land 10000

Building 50000

Less: Accumulated Depreciation 7000

Depreciation for the year 1000 42000

Plant and machinery 65000

Less: Depreciation 15000

Depreciation for the year 10000 40000

Total non-current assets 92,000

Inventories 18000

Current tax assets

Derivative financial instruments

Prepaid Rent 3000

Accounts receivable 24000

Total current assets 45,000

Total assets 1,37,000

20

Distribution cost 30000

Administrative costs 30000

Operating income 12,000

Interest income -

Interest expense -

Income before income taxes 12000

(b) Balance Sheet of Bowling Limited

Consolidated Balance Sheets for the years ended July 31, 2018

Assets Amount in EUR

Land 10000

Building 50000

Less: Accumulated Depreciation 7000

Depreciation for the year 1000 42000

Plant and machinery 65000

Less: Depreciation 15000

Depreciation for the year 10000 40000

Total non-current assets 92,000

Inventories 18000

Current tax assets

Derivative financial instruments

Prepaid Rent 3000

Accounts receivable 24000

Total current assets 45,000

Total assets 1,37,000

20

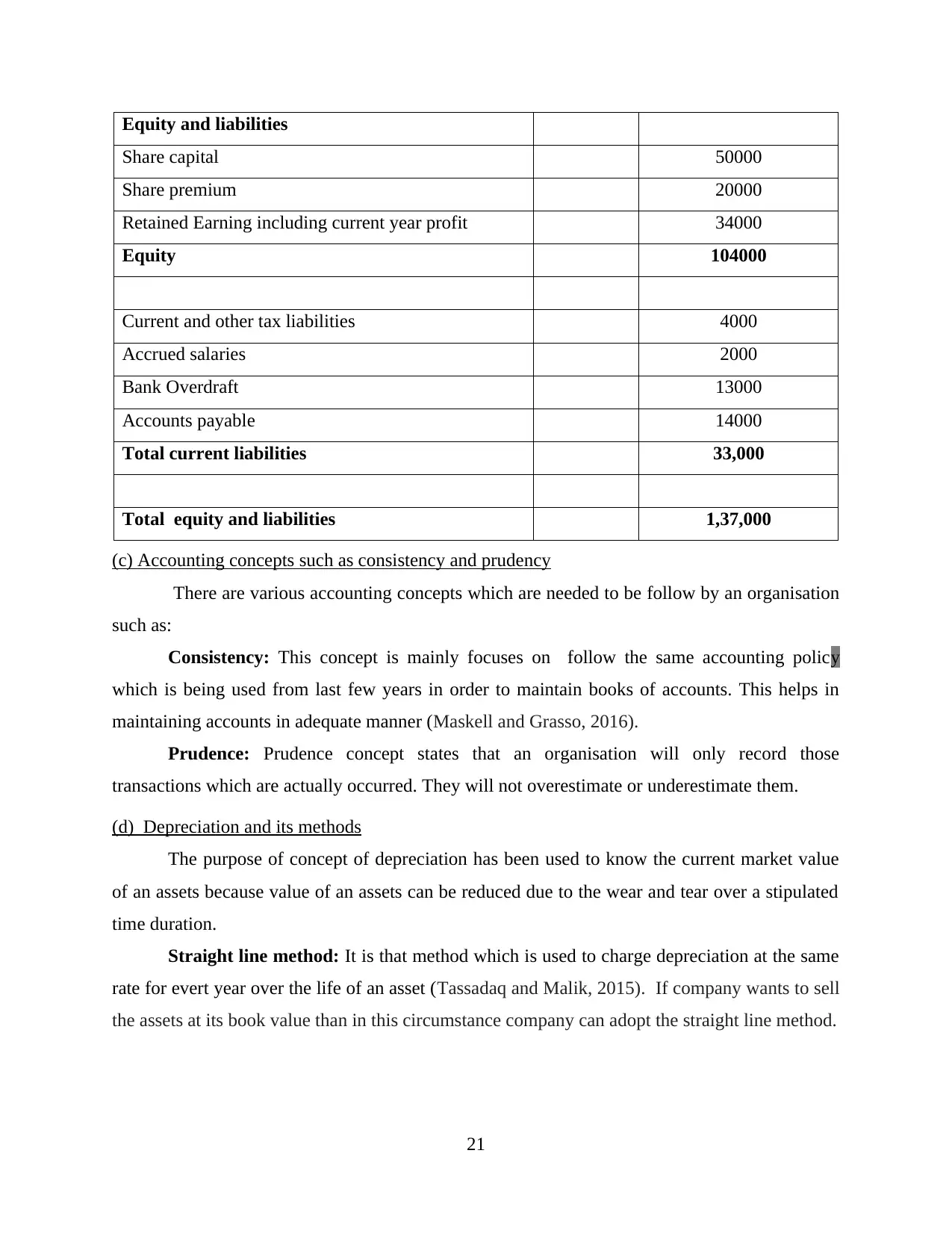

Equity and liabilities

Share capital 50000

Share premium 20000

Retained Earning including current year profit 34000

Equity 104000

Current and other tax liabilities 4000

Accrued salaries 2000

Bank Overdraft 13000

Accounts payable 14000

Total current liabilities 33,000

Total equity and liabilities 1,37,000

(c) Accounting concepts such as consistency and prudency

There are various accounting concepts which are needed to be follow by an organisation

such as:

Consistency: This concept is mainly focuses on follow the same accounting policy

which is being used from last few years in order to maintain books of accounts. This helps in

maintaining accounts in adequate manner (Maskell and Grasso, 2016).

Prudence: Prudence concept states that an organisation will only record those

transactions which are actually occurred. They will not overestimate or underestimate them.

(d) Depreciation and its methods

The purpose of concept of depreciation has been used to know the current market value

of an assets because value of an assets can be reduced due to the wear and tear over a stipulated

time duration.

Straight line method: It is that method which is used to charge depreciation at the same

rate for evert year over the life of an asset (Tassadaq and Malik, 2015). If company wants to sell

the assets at its book value than in this circumstance company can adopt the straight line method.

21

Share capital 50000

Share premium 20000

Retained Earning including current year profit 34000

Equity 104000

Current and other tax liabilities 4000

Accrued salaries 2000

Bank Overdraft 13000

Accounts payable 14000

Total current liabilities 33,000

Total equity and liabilities 1,37,000

(c) Accounting concepts such as consistency and prudency

There are various accounting concepts which are needed to be follow by an organisation

such as:

Consistency: This concept is mainly focuses on follow the same accounting policy

which is being used from last few years in order to maintain books of accounts. This helps in

maintaining accounts in adequate manner (Maskell and Grasso, 2016).

Prudence: Prudence concept states that an organisation will only record those

transactions which are actually occurred. They will not overestimate or underestimate them.

(d) Depreciation and its methods

The purpose of concept of depreciation has been used to know the current market value

of an assets because value of an assets can be reduced due to the wear and tear over a stipulated

time duration.

Straight line method: It is that method which is used to charge depreciation at the same

rate for evert year over the life of an asset (Tassadaq and Malik, 2015). If company wants to sell

the assets at its book value than in this circumstance company can adopt the straight line method.

21

Written down value method: According to this method the amount of depreciation at

different rates for every year over the life of an assets & assets value gets down year after year.

To know the actual market value of assets the company uses this method.

Client 4

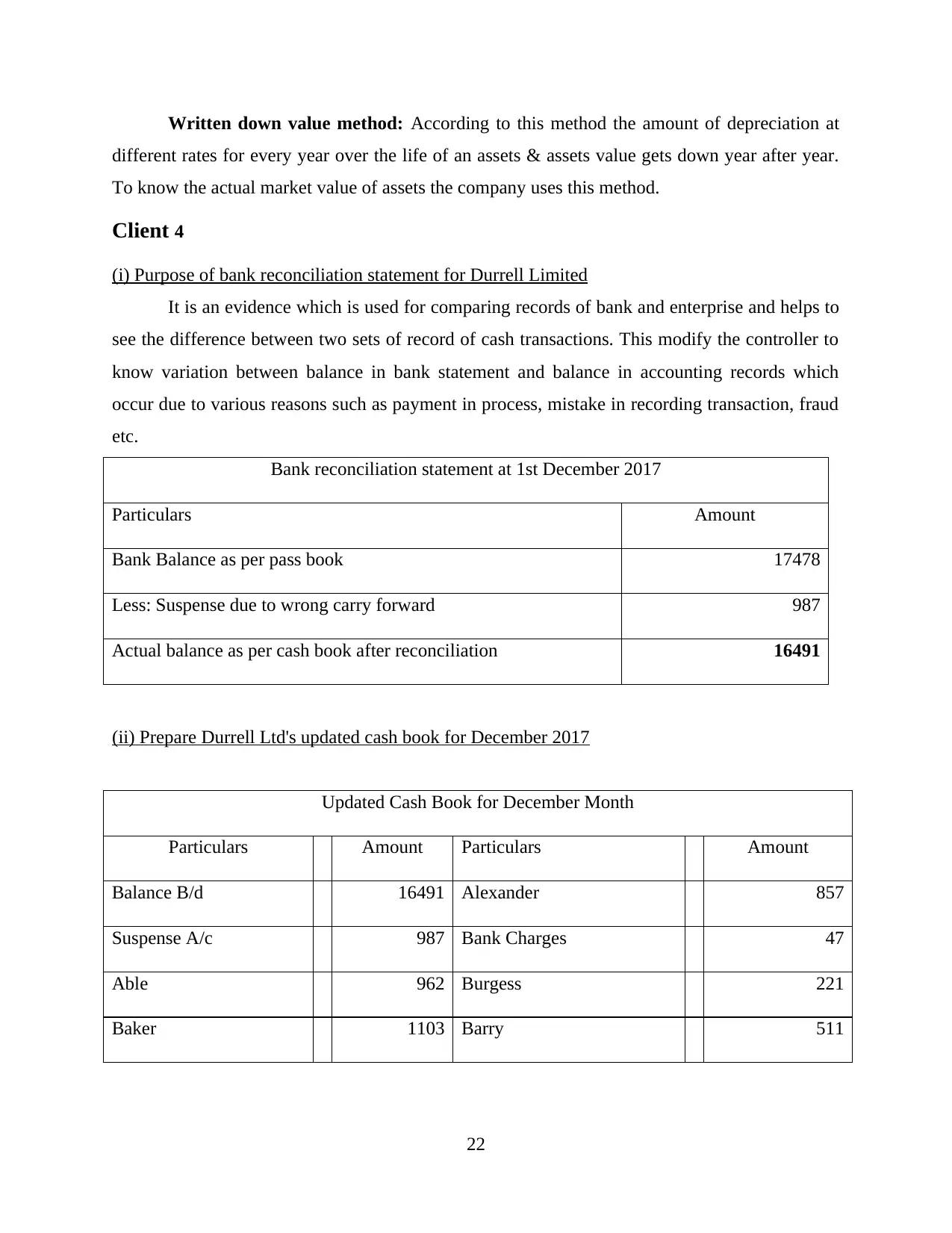

(i) Purpose of bank reconciliation statement for Durrell Limited

It is an evidence which is used for comparing records of bank and enterprise and helps to

see the difference between two sets of record of cash transactions. This modify the controller to

know variation between balance in bank statement and balance in accounting records which

occur due to various reasons such as payment in process, mistake in recording transaction, fraud

etc.

Bank reconciliation statement at 1st December 2017

Particulars Amount

Bank Balance as per pass book 17478

Less: Suspense due to wrong carry forward 987

Actual balance as per cash book after reconciliation 16491

(ii) Prepare Durrell Ltd's updated cash book for December 2017

Updated Cash Book for December Month

Particulars Amount Particulars Amount

Balance B/d 16491 Alexander 857

Suspense A/c 987 Bank Charges 47

Able 962 Burgess 221

Baker 1103 Barry 511

22

different rates for every year over the life of an assets & assets value gets down year after year.

To know the actual market value of assets the company uses this method.

Client 4

(i) Purpose of bank reconciliation statement for Durrell Limited

It is an evidence which is used for comparing records of bank and enterprise and helps to

see the difference between two sets of record of cash transactions. This modify the controller to

know variation between balance in bank statement and balance in accounting records which

occur due to various reasons such as payment in process, mistake in recording transaction, fraud

etc.

Bank reconciliation statement at 1st December 2017

Particulars Amount

Bank Balance as per pass book 17478

Less: Suspense due to wrong carry forward 987

Actual balance as per cash book after reconciliation 16491

(ii) Prepare Durrell Ltd's updated cash book for December 2017

Updated Cash Book for December Month

Particulars Amount Particulars Amount

Balance B/d 16491 Alexander 857

Suspense A/c 987 Bank Charges 47

Able 962 Burgess 221

Baker 1103 Barry 511

22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

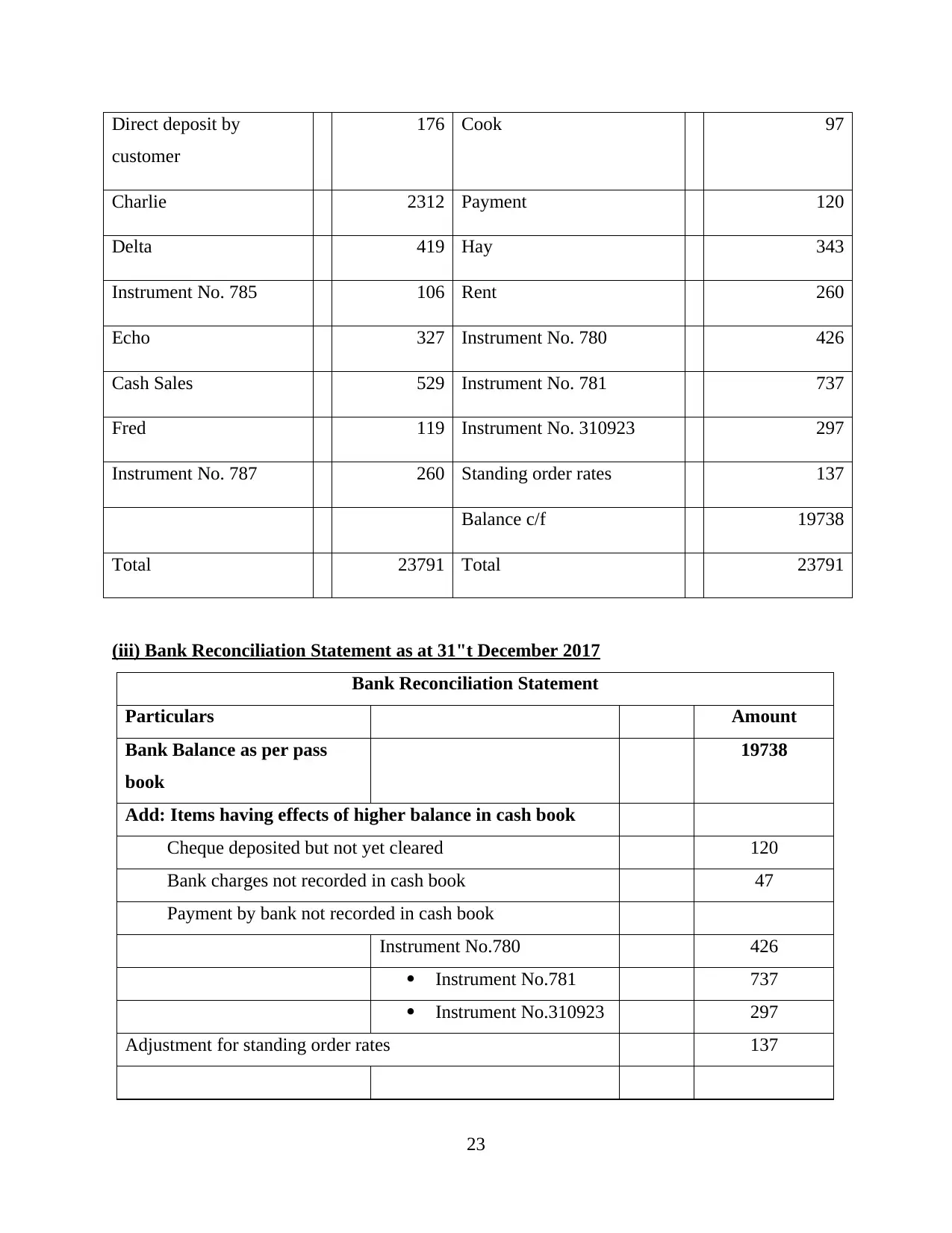

Direct deposit by

customer

176 Cook 97

Charlie 2312 Payment 120

Delta 419 Hay 343

Instrument No. 785 106 Rent 260

Echo 327 Instrument No. 780 426

Cash Sales 529 Instrument No. 781 737

Fred 119 Instrument No. 310923 297

Instrument No. 787 260 Standing order rates 137

Balance c/f 19738

Total 23791 Total 23791

(iii) Bank Reconciliation Statement as at 31"t December 2017

Bank Reconciliation Statement

Particulars Amount

Bank Balance as per pass

book

19738

Add: Items having effects of higher balance in cash book

Cheque deposited but not yet cleared 120

Bank charges not recorded in cash book 47

Payment by bank not recorded in cash book

Instrument No.780 426

Instrument No.781 737

Instrument No.310923 297

Adjustment for standing order rates 137

23

customer

176 Cook 97

Charlie 2312 Payment 120

Delta 419 Hay 343

Instrument No. 785 106 Rent 260

Echo 327 Instrument No. 780 426

Cash Sales 529 Instrument No. 781 737

Fred 119 Instrument No. 310923 297

Instrument No. 787 260 Standing order rates 137

Balance c/f 19738

Total 23791 Total 23791

(iii) Bank Reconciliation Statement as at 31"t December 2017

Bank Reconciliation Statement

Particulars Amount

Bank Balance as per pass

book

19738

Add: Items having effects of higher balance in cash book

Cheque deposited but not yet cleared 120

Bank charges not recorded in cash book 47

Payment by bank not recorded in cash book

Instrument No.780 426

Instrument No.781 737

Instrument No.310923 297

Adjustment for standing order rates 137

23

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.