Financial Accounting and Control

VerifiedAdded on 2020/07/23

|37

|2902

|88

AI Summary

This assignment delves into the world of financial accounting, covering topics such as sales and purchase ledgers, control accounts, and suspense accounts. It highlights the significance of financial accounting in analyzing a company's overall financial performance and prepares students for real-world scenarios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting &

Principles

Principles

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A) Preparation of report for Line Manager............................................................................1

CLIENT 1........................................................................................................................................4

1. Passing journal entries........................................................................................................4

2. Preparation of ledger accounts...........................................................................................8

................................................................................................................................................9

................................................................................................................................................9

................................................................................................................................................9

..............................................................................................................................................10

..............................................................................................................................................10

..............................................................................................................................................11

3. Trial balance.....................................................................................................................18

M1. Purchase and sale transactions......................................................................................19

D1 Trial balance...................................................................................................................19

CLIENT 2......................................................................................................................................19

A) Income statement.............................................................................................................19

B) Balance sheet...................................................................................................................20

CLIENT 3......................................................................................................................................22

A) Income statement for the company.................................................................................22

..............................................................................................................................................23

B) Balance sheet...................................................................................................................24

..............................................................................................................................................27

..............................................................................................................................................28

..............................................................................................................................................28

C) Concepts of accounting...................................................................................................28

D) Methods of deprecation...................................................................................................29

M2 Income statement, balance sheet and cash flow statements...........................................29

D2 Calculations in producing final accounts........................................................................29

CLIENT 4......................................................................................................................................29

INTRODUCTION...........................................................................................................................1

A) Preparation of report for Line Manager............................................................................1

CLIENT 1........................................................................................................................................4

1. Passing journal entries........................................................................................................4

2. Preparation of ledger accounts...........................................................................................8

................................................................................................................................................9

................................................................................................................................................9

................................................................................................................................................9

..............................................................................................................................................10

..............................................................................................................................................10

..............................................................................................................................................11

3. Trial balance.....................................................................................................................18

M1. Purchase and sale transactions......................................................................................19

D1 Trial balance...................................................................................................................19

CLIENT 2......................................................................................................................................19

A) Income statement.............................................................................................................19

B) Balance sheet...................................................................................................................20

CLIENT 3......................................................................................................................................22

A) Income statement for the company.................................................................................22

..............................................................................................................................................23

B) Balance sheet...................................................................................................................24

..............................................................................................................................................27

..............................................................................................................................................28

..............................................................................................................................................28

C) Concepts of accounting...................................................................................................28

D) Methods of deprecation...................................................................................................29

M2 Income statement, balance sheet and cash flow statements...........................................29

D2 Calculations in producing final accounts........................................................................29

CLIENT 4......................................................................................................................................29

A) Bank statement................................................................................................................29

B) Outlining causes for preparing bank statements..............................................................29

C) Cash books.......................................................................................................................30

M3 Reconciliation process...................................................................................................31

D3 BRS.................................................................................................................................31

CLIENT 5......................................................................................................................................31

A) Sales and purchase ledger...............................................................................................31

B) Control account...............................................................................................................31

CLIENT 6......................................................................................................................................32

A) Suspense account and explaining features......................................................................32

B) Trial balance....................................................................................................................32

C) Journal entries..................................................................................................................32

D) Distinguishing between clearing and suspense account..................................................33

M4 Various accounts and reconciliation..............................................................................33

D4 Outlining accounting methods for the organisation.......................................................33

CONCLUSION..............................................................................................................................33

REFERENCES..............................................................................................................................34

B) Outlining causes for preparing bank statements..............................................................29

C) Cash books.......................................................................................................................30

M3 Reconciliation process...................................................................................................31

D3 BRS.................................................................................................................................31

CLIENT 5......................................................................................................................................31

A) Sales and purchase ledger...............................................................................................31

B) Control account...............................................................................................................31

CLIENT 6......................................................................................................................................32

A) Suspense account and explaining features......................................................................32

B) Trial balance....................................................................................................................32

C) Journal entries..................................................................................................................32

D) Distinguishing between clearing and suspense account..................................................33

M4 Various accounts and reconciliation..............................................................................33

D4 Outlining accounting methods for the organisation.......................................................33

CONCLUSION..............................................................................................................................33

REFERENCES..............................................................................................................................34

INTRODUCTION

Financial accounting is quite important in the business as it helps to record every

transaction which occurs in the organisation. This is required so that final accounts can be

prepared with much ease. Present report deals with various companies which requires following

accounting regulations and concepts in the best possible manner. Moreover, various accounting

concepts and relevant terms are discussed in this report. Financials of the company such as

balance sheet, cash flow statement and income statements are prepared for assessing overall

financial performance of organisations in effective way.

A) Preparation of report for Line Manager

To: Line Manager of Firm

From: Junior Accountant

Subject: Accounting terms and regulations useful for the company

Respected Sir,

Accounting principles and regulations play crucial role in the company so that may be

able to prepare various financial statements in the best possible manner. This is quite important

so that effective financials may be prepared in consideration of various regulations implemented

by accounting bodies. In relation to this, financials of company are income statement and cash

flow statement and balance sheet which are three statements which provides clarity about the

financial health of organisation quite easily. Accounting concepts are required to be followed by

the company so that error free and true financial statements may be prepared exhibiting real

financial position of the organisation.

Financial accounting

The term financial accounting is the major branch of accounting which deals with

recording, summarizing of business transactions held over particular time frame. This is quite

essential for the business so that it may be able to analyse various transactions. Once financial

transactions are recorded and summarized, final accounts can be easily prepared. The final

accounts are then provided to various stakeholders such as investors, creditors so that they may

be able to take effective and better decisions with much ease. Thus, financial accounting is

1

Financial accounting is quite important in the business as it helps to record every

transaction which occurs in the organisation. This is required so that final accounts can be

prepared with much ease. Present report deals with various companies which requires following

accounting regulations and concepts in the best possible manner. Moreover, various accounting

concepts and relevant terms are discussed in this report. Financials of the company such as

balance sheet, cash flow statement and income statements are prepared for assessing overall

financial performance of organisations in effective way.

A) Preparation of report for Line Manager

To: Line Manager of Firm

From: Junior Accountant

Subject: Accounting terms and regulations useful for the company

Respected Sir,

Accounting principles and regulations play crucial role in the company so that may be

able to prepare various financial statements in the best possible manner. This is quite important

so that effective financials may be prepared in consideration of various regulations implemented

by accounting bodies. In relation to this, financials of company are income statement and cash

flow statement and balance sheet which are three statements which provides clarity about the

financial health of organisation quite easily. Accounting concepts are required to be followed by

the company so that error free and true financial statements may be prepared exhibiting real

financial position of the organisation.

Financial accounting

The term financial accounting is the major branch of accounting which deals with

recording, summarizing of business transactions held over particular time frame. This is quite

essential for the business so that it may be able to analyse various transactions. Once financial

transactions are recorded and summarized, final accounts can be easily prepared. The final

accounts are then provided to various stakeholders such as investors, creditors so that they may

be able to take effective and better decisions with much ease. Thus, financial accounting is

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

required in the organisation and should be adhered to accounting concepts and policies

governed by professional bodies. Moreover, when financials of the company are prepared then,

it is available for various stakeholders to take effective and better decisions whether to provide

funds to organisation or not.

Financial accounting regulations

Accounting regulations are required to be abide by the company so that accurate

financial statements can be prepared having transparency in the best possible way. This is

required to be followed by accountant so that he may formulate financials of the company in

effectual way and that too error and mistake free. In relation to this, UK's corporate governance

professional body such as FRC (Financial Reporting Council) has provided legal framework to

be followed by the company while preparing financial statements of the organisation in the best

possible way. These legal frameworks help accountants to prepare financials in quite effective

manner.

Legal frameworks

FRC : It is a professional body limited by guarantee and regulates entire organisations of UK so

that financials may be prepared in the best possible way. Moreover, government departments

are also regulated by it (Financial Reporting Council, 2017). The main objective of FRC is to

adequately foster investment in UK and as such, benefiting whole economy in effective way.

IASB : It is abbreviated as IASB (International Accounting Standards Board) which regulates

organisations so that adequate financial statements may be prepared. It provides guidelines

which help accountants to prepare financials so that true and fair view may be extracted out of

the statements in the best possible manner.

IFRS :It is abbreviated as IFRS (International Financial Reporting Standards) which is another

accounting body facilitating accountants to prepare fair financial statements exhibiting true

financial health of the company.

Principles of accounting

Principles of accounting are provided by GAAP (Generally Accepted Accounting

Principles) which are as follows-

2

governed by professional bodies. Moreover, when financials of the company are prepared then,

it is available for various stakeholders to take effective and better decisions whether to provide

funds to organisation or not.

Financial accounting regulations

Accounting regulations are required to be abide by the company so that accurate

financial statements can be prepared having transparency in the best possible way. This is

required to be followed by accountant so that he may formulate financials of the company in

effectual way and that too error and mistake free. In relation to this, UK's corporate governance

professional body such as FRC (Financial Reporting Council) has provided legal framework to

be followed by the company while preparing financial statements of the organisation in the best

possible way. These legal frameworks help accountants to prepare financials in quite effective

manner.

Legal frameworks

FRC : It is a professional body limited by guarantee and regulates entire organisations of UK so

that financials may be prepared in the best possible way. Moreover, government departments

are also regulated by it (Financial Reporting Council, 2017). The main objective of FRC is to

adequately foster investment in UK and as such, benefiting whole economy in effective way.

IASB : It is abbreviated as IASB (International Accounting Standards Board) which regulates

organisations so that adequate financial statements may be prepared. It provides guidelines

which help accountants to prepare financials so that true and fair view may be extracted out of

the statements in the best possible manner.

IFRS :It is abbreviated as IFRS (International Financial Reporting Standards) which is another

accounting body facilitating accountants to prepare fair financial statements exhibiting true

financial health of the company.

Principles of accounting

Principles of accounting are provided by GAAP (Generally Accepted Accounting

Principles) which are as follows-

2

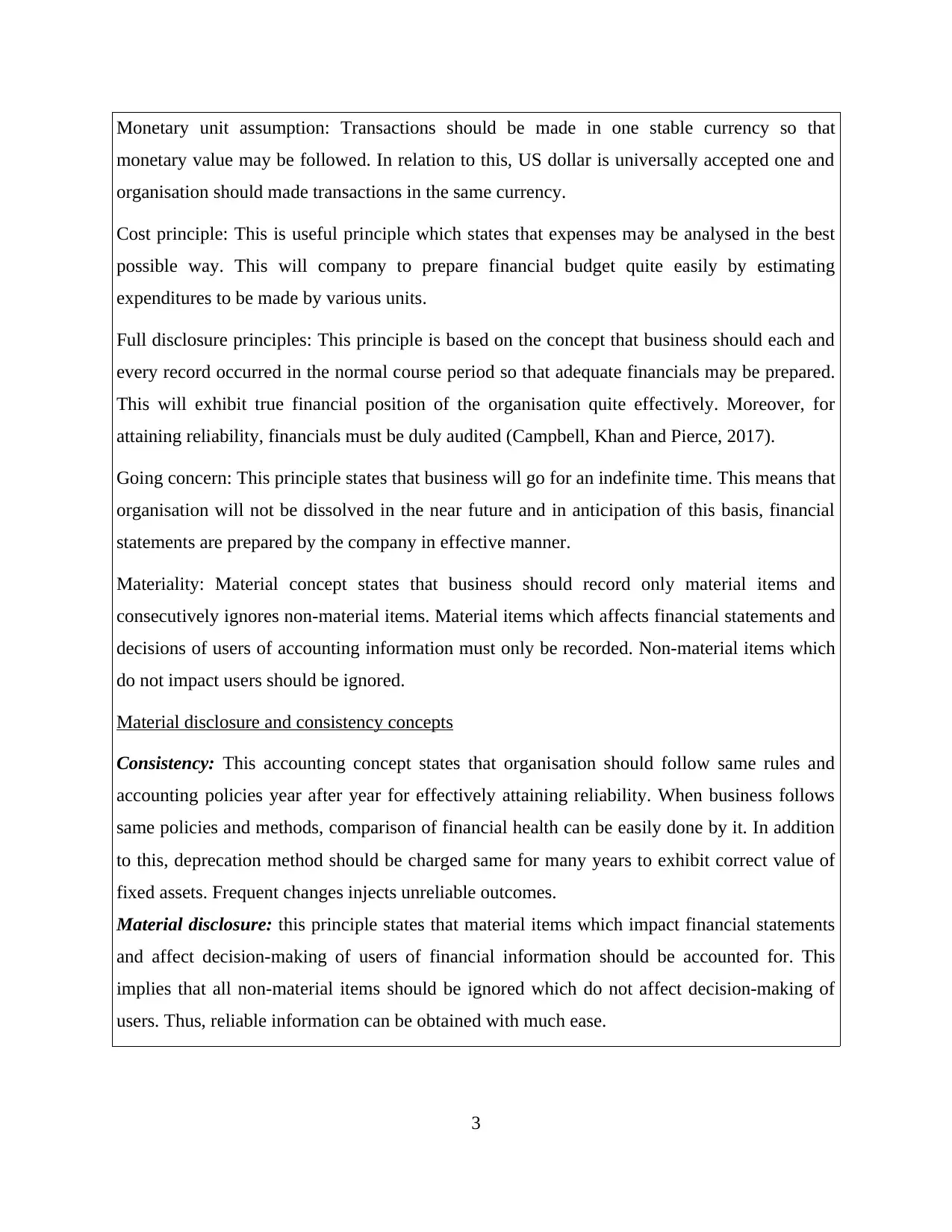

Monetary unit assumption: Transactions should be made in one stable currency so that

monetary value may be followed. In relation to this, US dollar is universally accepted one and

organisation should made transactions in the same currency.

Cost principle: This is useful principle which states that expenses may be analysed in the best

possible way. This will company to prepare financial budget quite easily by estimating

expenditures to be made by various units.

Full disclosure principles: This principle is based on the concept that business should each and

every record occurred in the normal course period so that adequate financials may be prepared.

This will exhibit true financial position of the organisation quite effectively. Moreover, for

attaining reliability, financials must be duly audited (Campbell, Khan and Pierce, 2017).

Going concern: This principle states that business will go for an indefinite time. This means that

organisation will not be dissolved in the near future and in anticipation of this basis, financial

statements are prepared by the company in effective manner.

Materiality: Material concept states that business should record only material items and

consecutively ignores non-material items. Material items which affects financial statements and

decisions of users of accounting information must only be recorded. Non-material items which

do not impact users should be ignored.

Material disclosure and consistency concepts

Consistency: This accounting concept states that organisation should follow same rules and

accounting policies year after year for effectively attaining reliability. When business follows

same policies and methods, comparison of financial health can be easily done by it. In addition

to this, deprecation method should be charged same for many years to exhibit correct value of

fixed assets. Frequent changes injects unreliable outcomes.

Material disclosure: this principle states that material items which impact financial statements

and affect decision-making of users of financial information should be accounted for. This

implies that all non-material items should be ignored which do not affect decision-making of

users. Thus, reliable information can be obtained with much ease.

3

monetary value may be followed. In relation to this, US dollar is universally accepted one and

organisation should made transactions in the same currency.

Cost principle: This is useful principle which states that expenses may be analysed in the best

possible way. This will company to prepare financial budget quite easily by estimating

expenditures to be made by various units.

Full disclosure principles: This principle is based on the concept that business should each and

every record occurred in the normal course period so that adequate financials may be prepared.

This will exhibit true financial position of the organisation quite effectively. Moreover, for

attaining reliability, financials must be duly audited (Campbell, Khan and Pierce, 2017).

Going concern: This principle states that business will go for an indefinite time. This means that

organisation will not be dissolved in the near future and in anticipation of this basis, financial

statements are prepared by the company in effective manner.

Materiality: Material concept states that business should record only material items and

consecutively ignores non-material items. Material items which affects financial statements and

decisions of users of accounting information must only be recorded. Non-material items which

do not impact users should be ignored.

Material disclosure and consistency concepts

Consistency: This accounting concept states that organisation should follow same rules and

accounting policies year after year for effectively attaining reliability. When business follows

same policies and methods, comparison of financial health can be easily done by it. In addition

to this, deprecation method should be charged same for many years to exhibit correct value of

fixed assets. Frequent changes injects unreliable outcomes.

Material disclosure: this principle states that material items which impact financial statements

and affect decision-making of users of financial information should be accounted for. This

implies that all non-material items should be ignored which do not affect decision-making of

users. Thus, reliable information can be obtained with much ease.

3

CLIENT 1

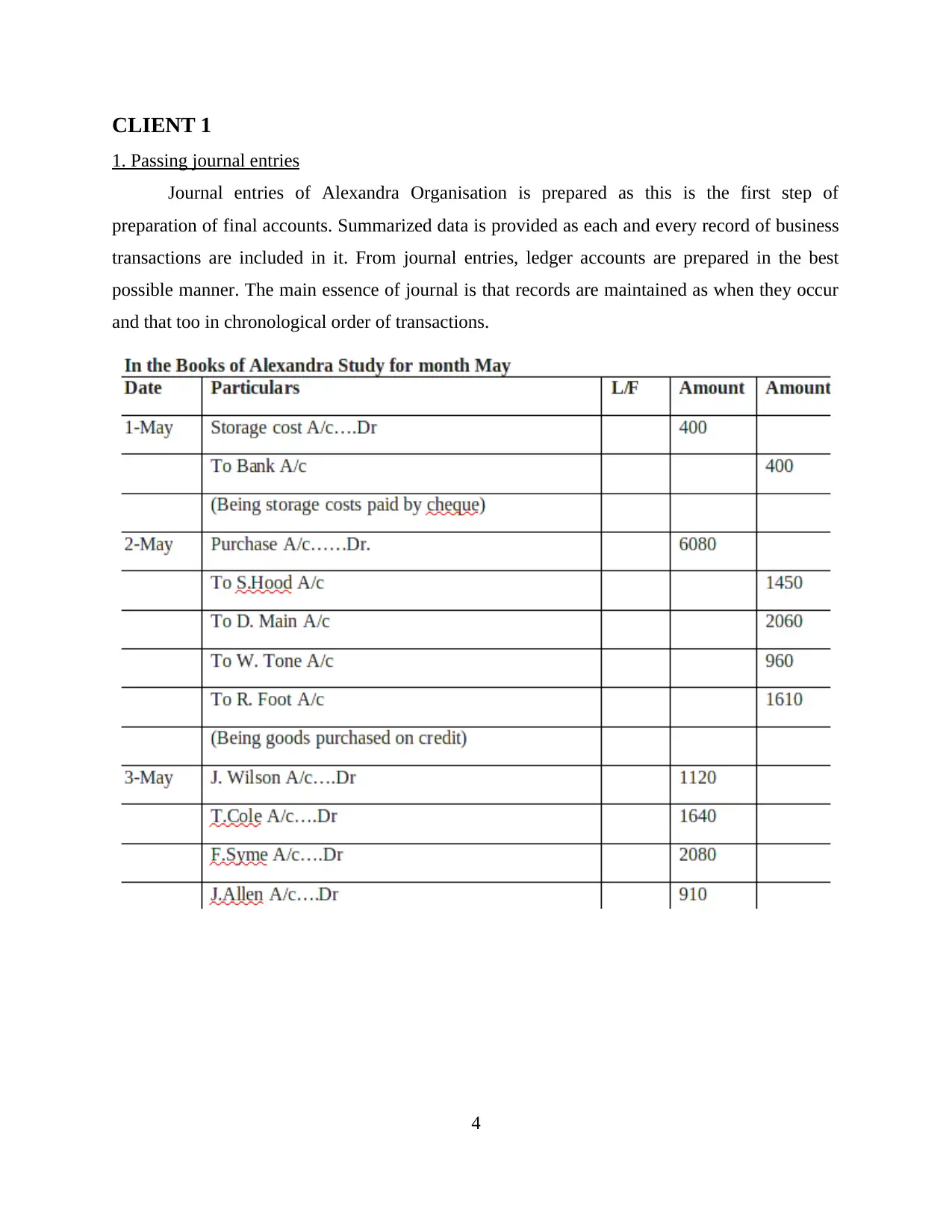

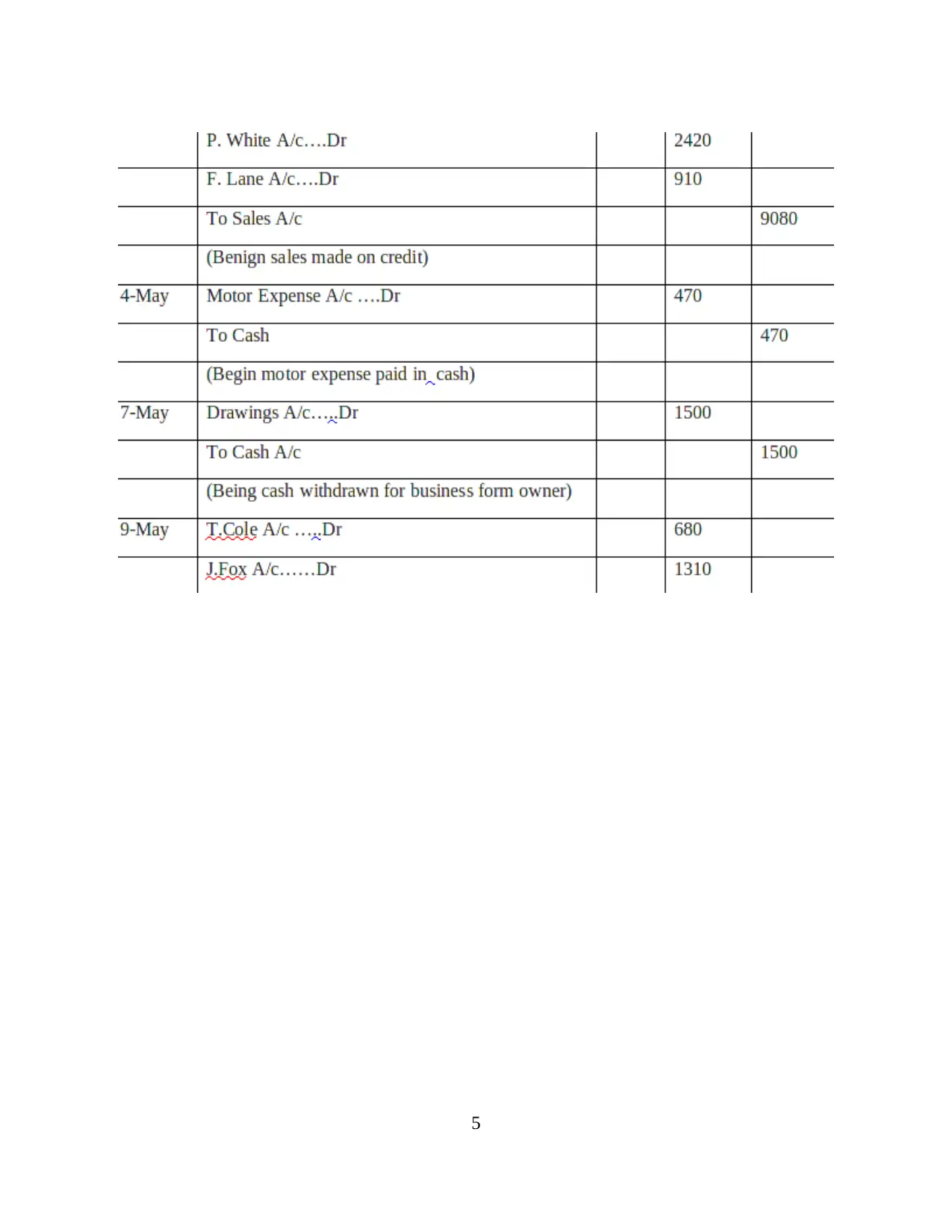

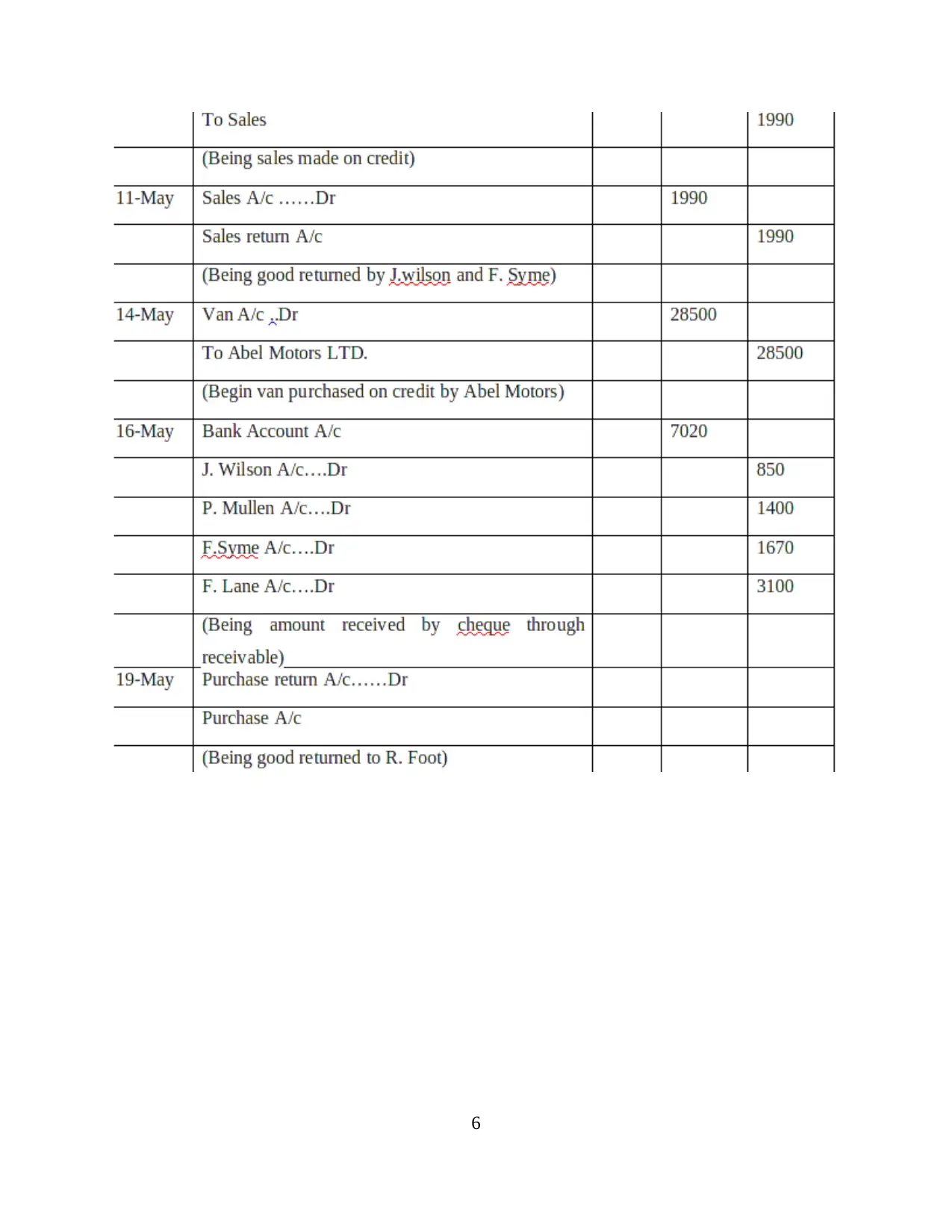

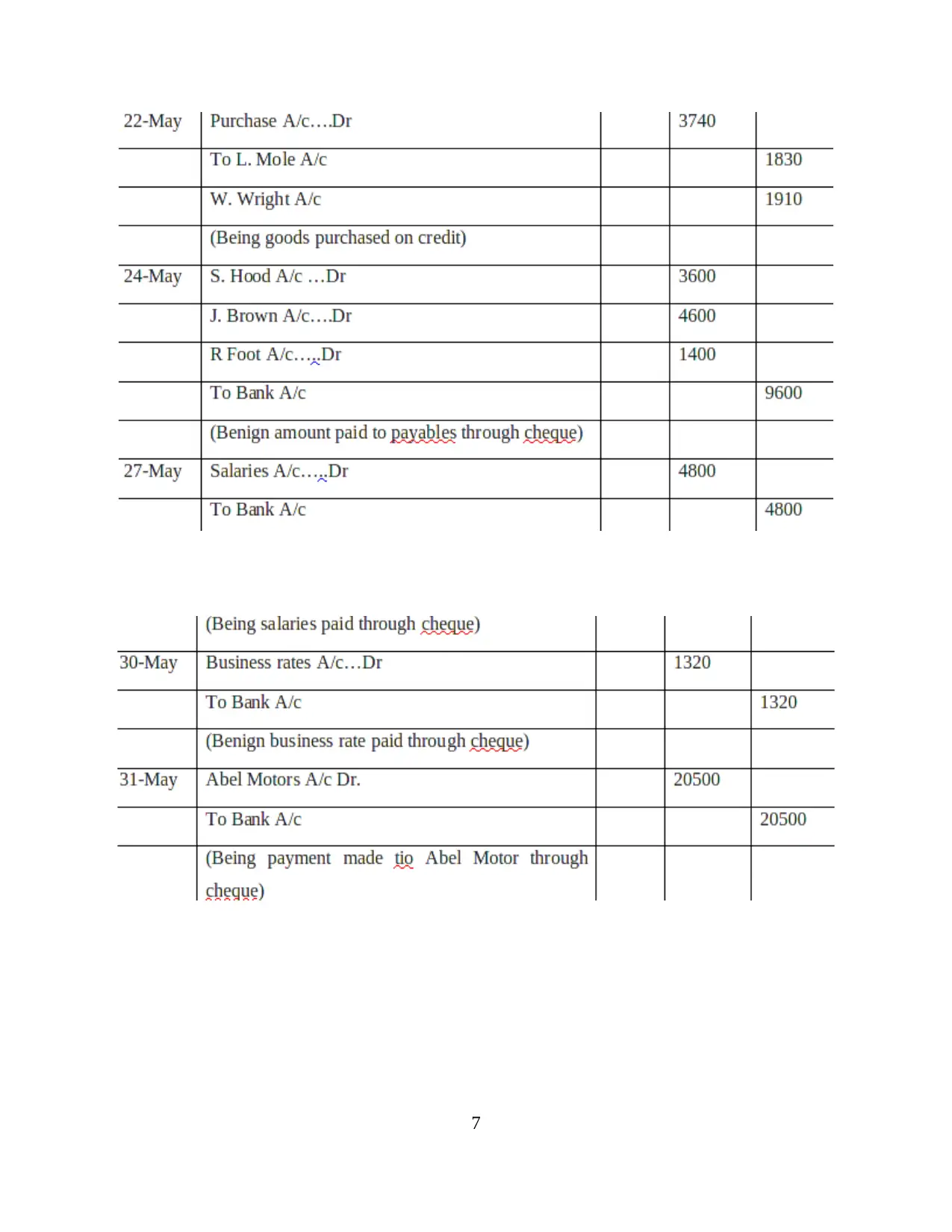

1. Passing journal entries

Journal entries of Alexandra Organisation is prepared as this is the first step of

preparation of final accounts. Summarized data is provided as each and every record of business

transactions are included in it. From journal entries, ledger accounts are prepared in the best

possible manner. The main essence of journal is that records are maintained as when they occur

and that too in chronological order of transactions.

4

1. Passing journal entries

Journal entries of Alexandra Organisation is prepared as this is the first step of

preparation of final accounts. Summarized data is provided as each and every record of business

transactions are included in it. From journal entries, ledger accounts are prepared in the best

possible manner. The main essence of journal is that records are maintained as when they occur

and that too in chronological order of transactions.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

6

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

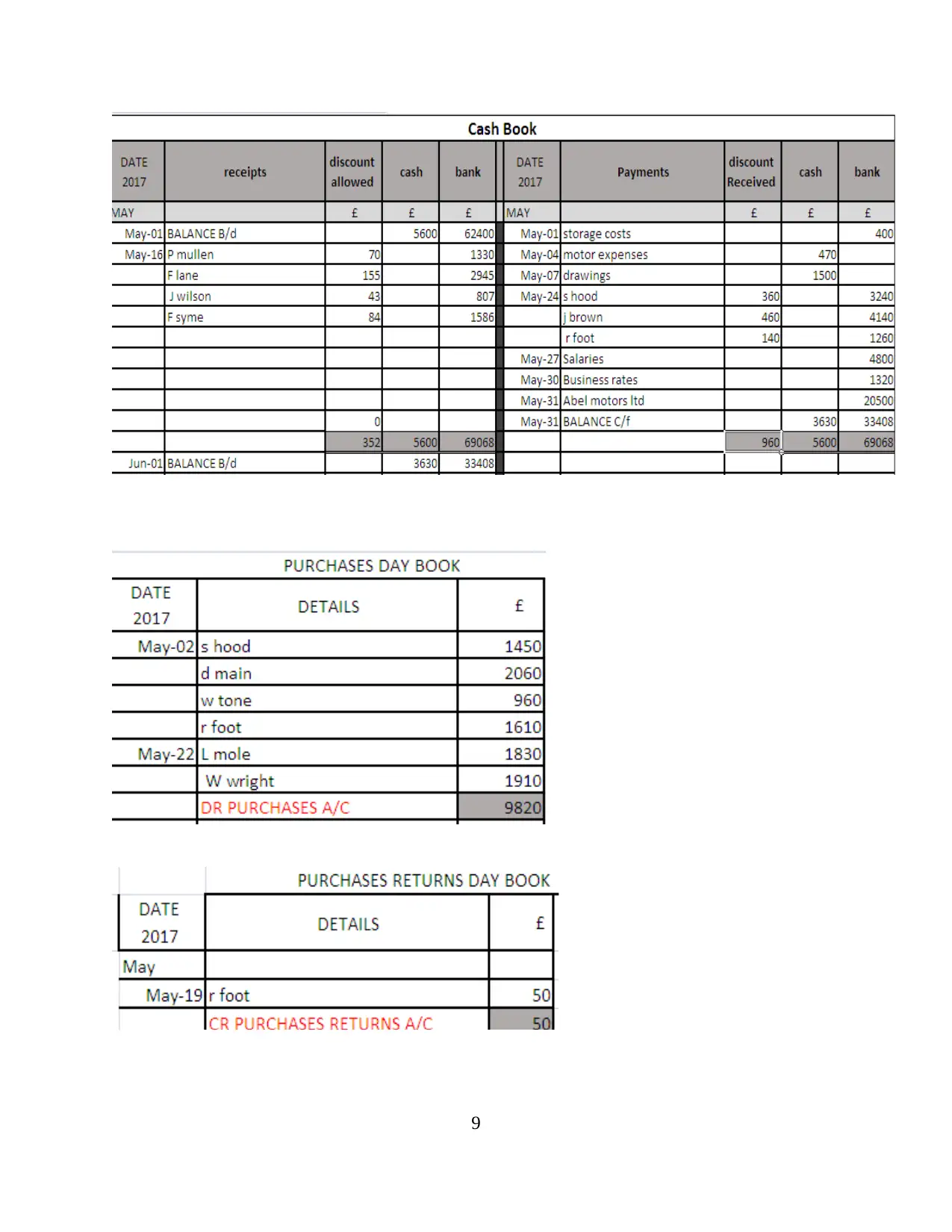

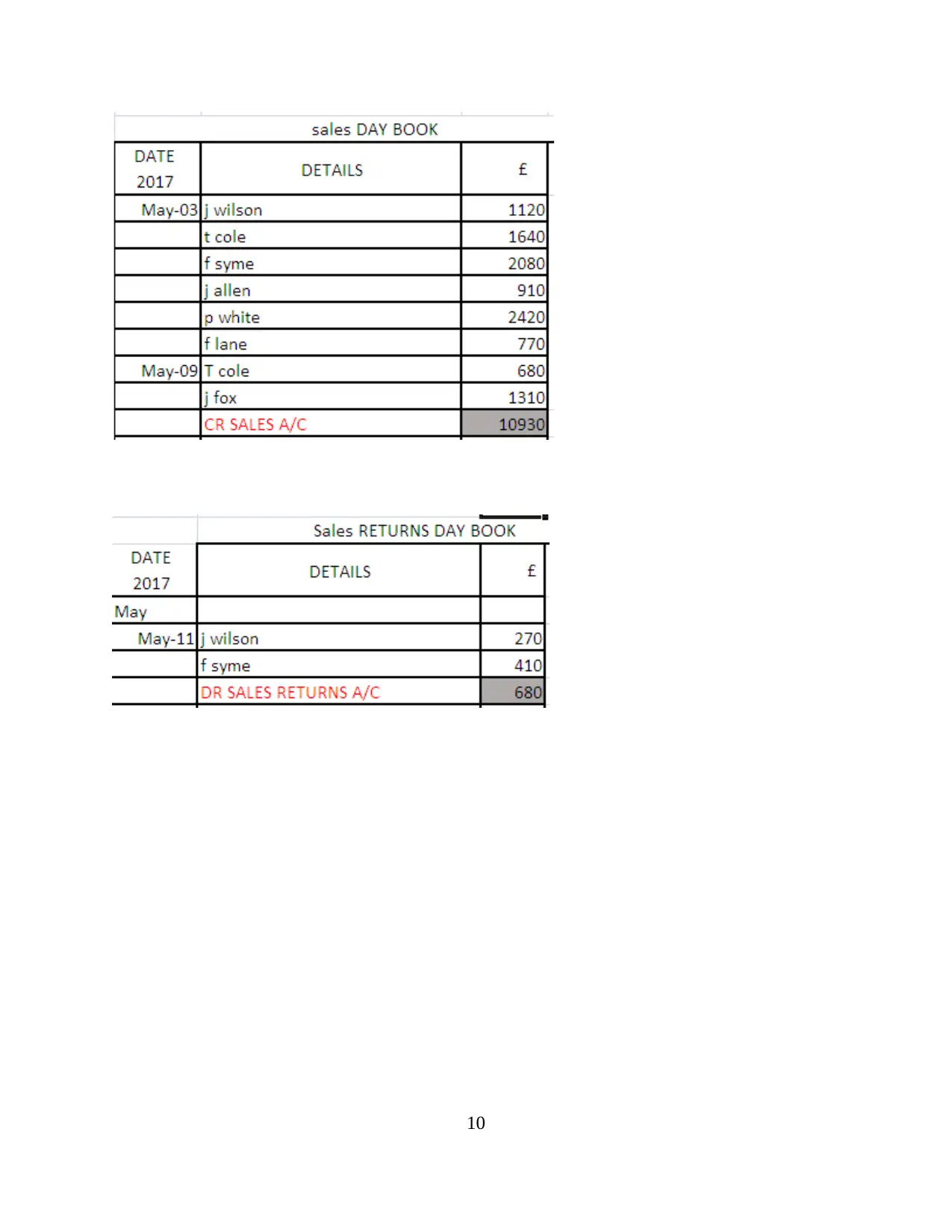

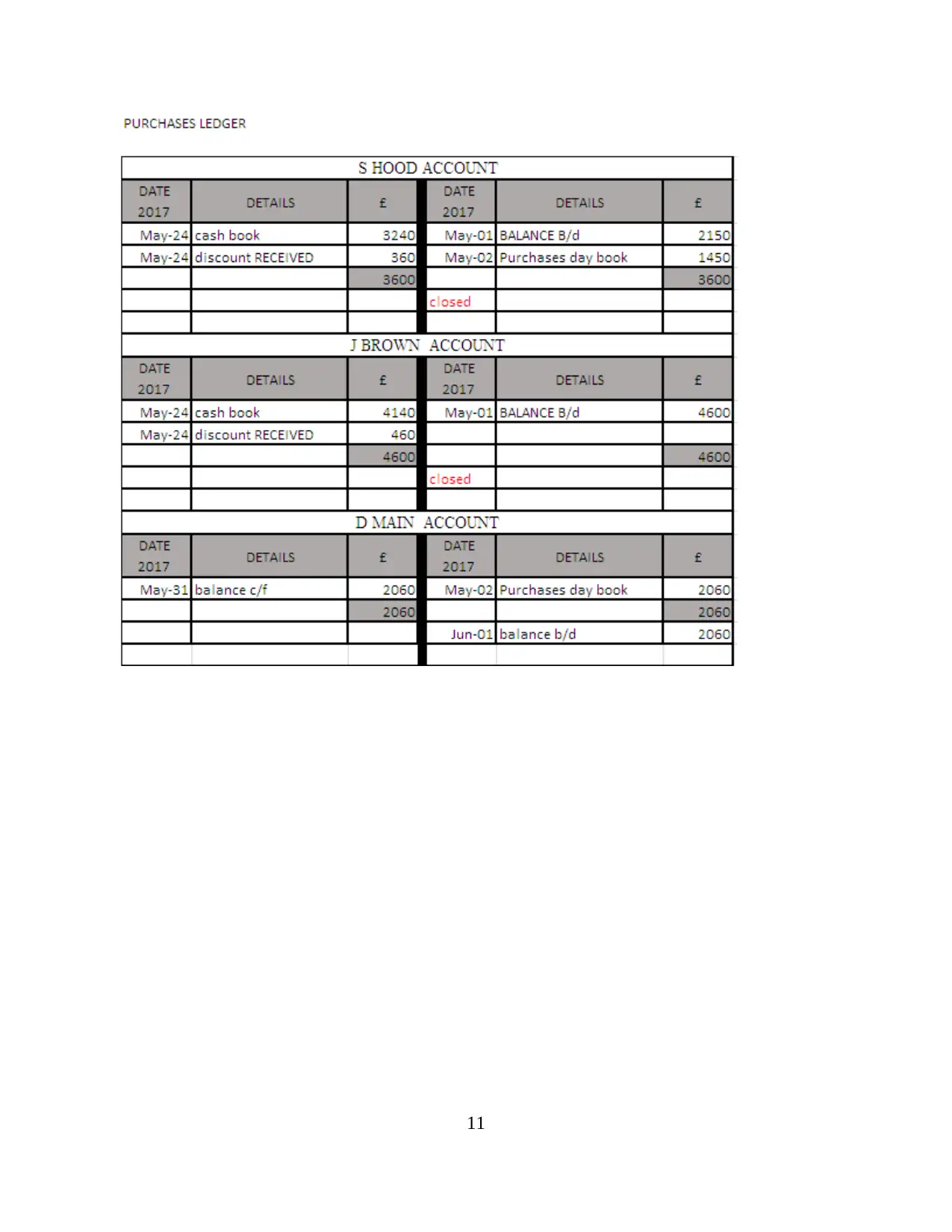

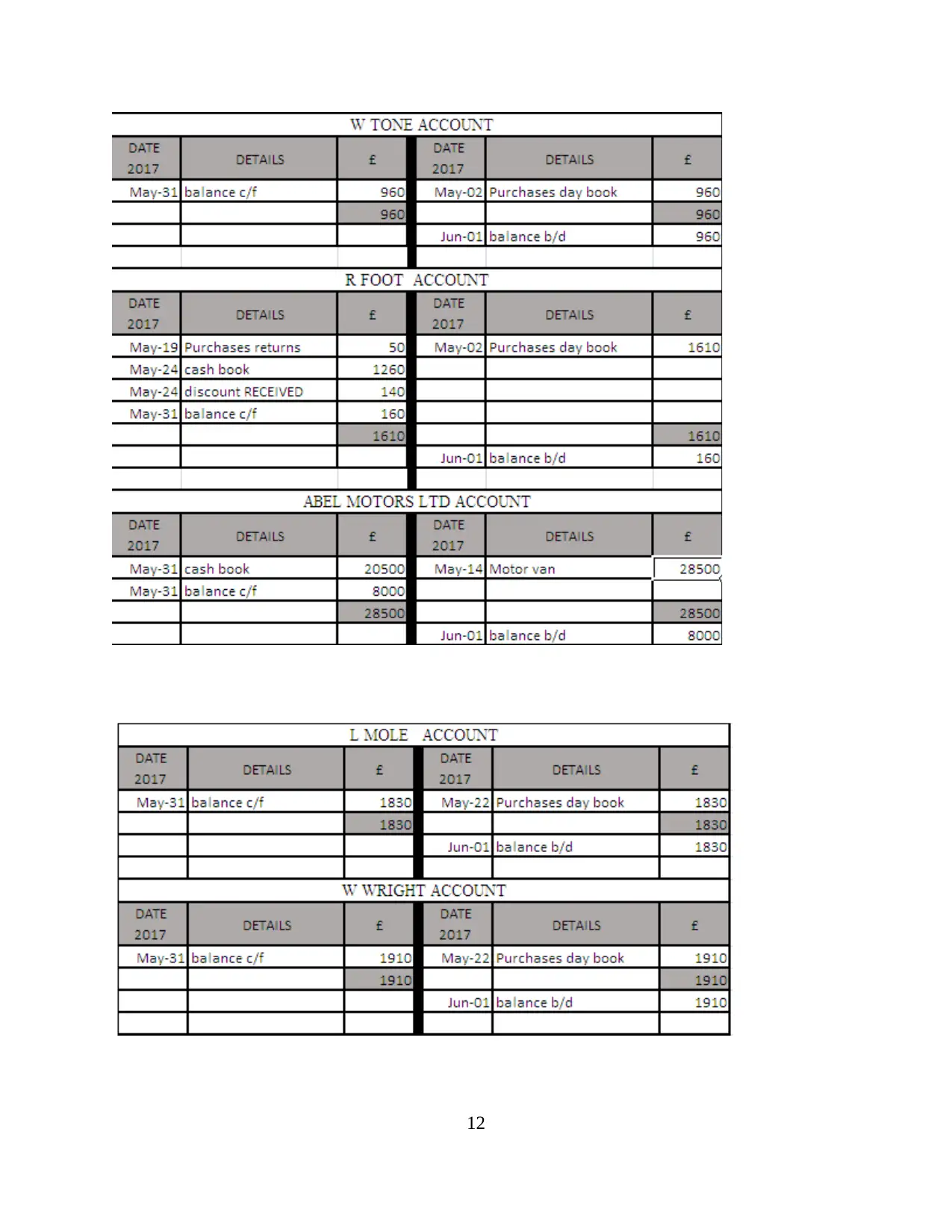

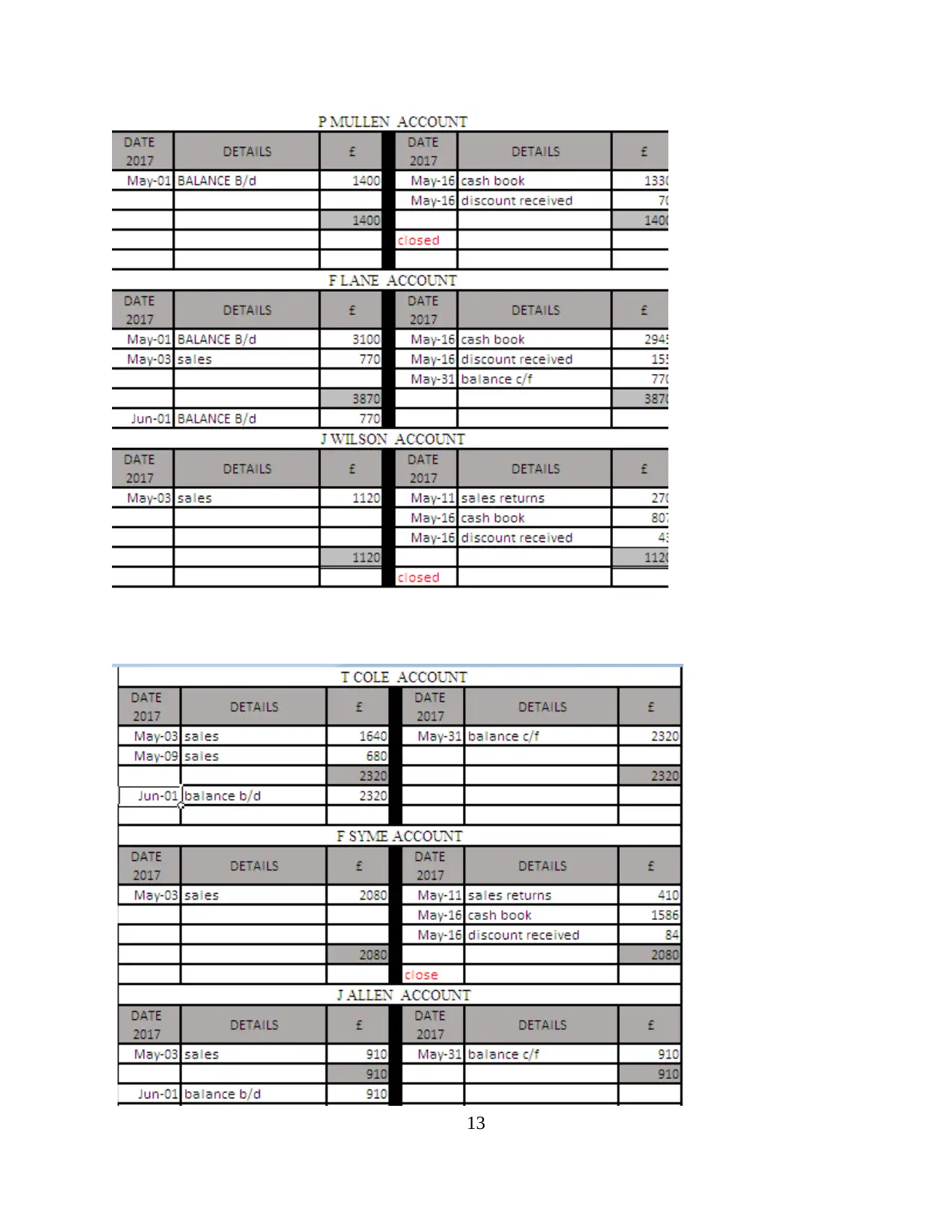

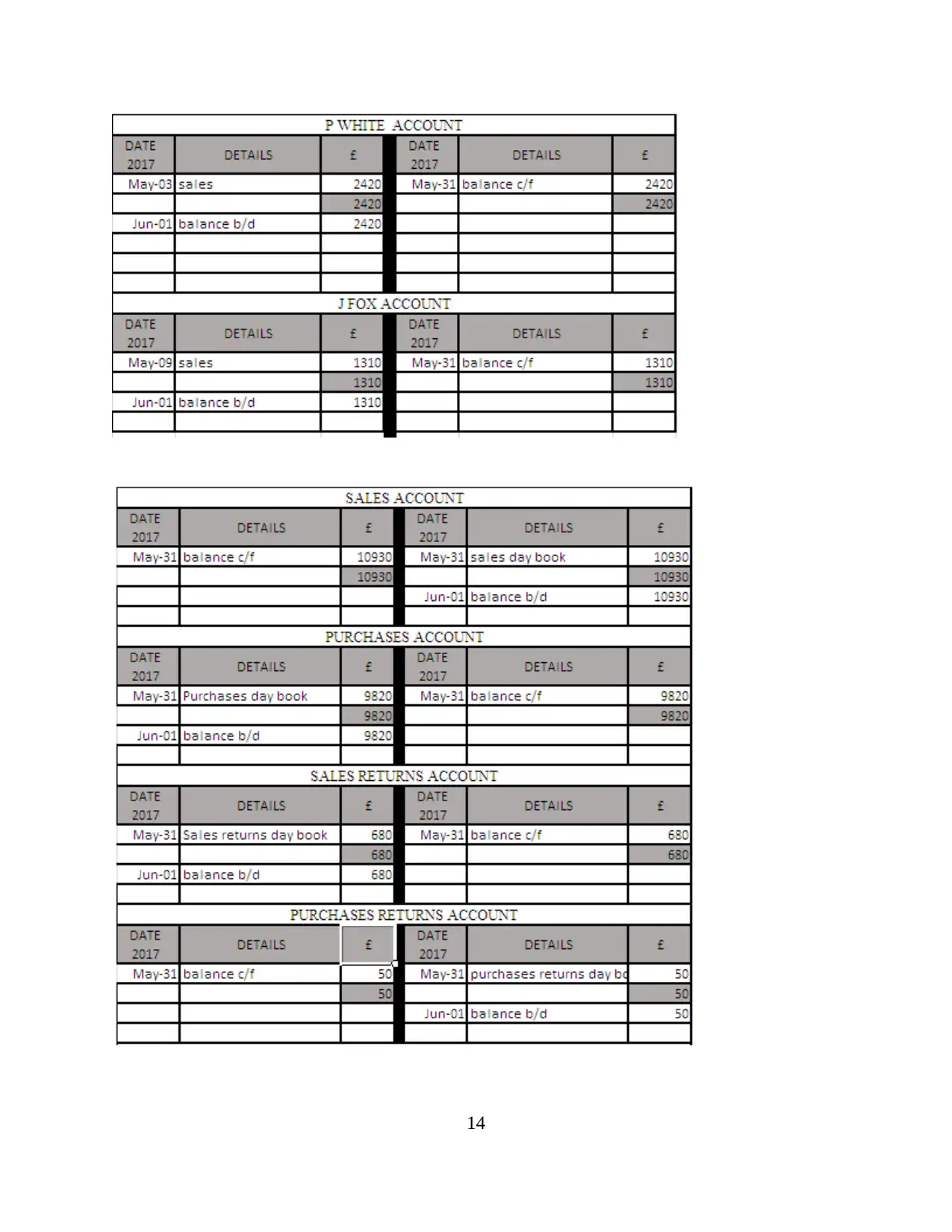

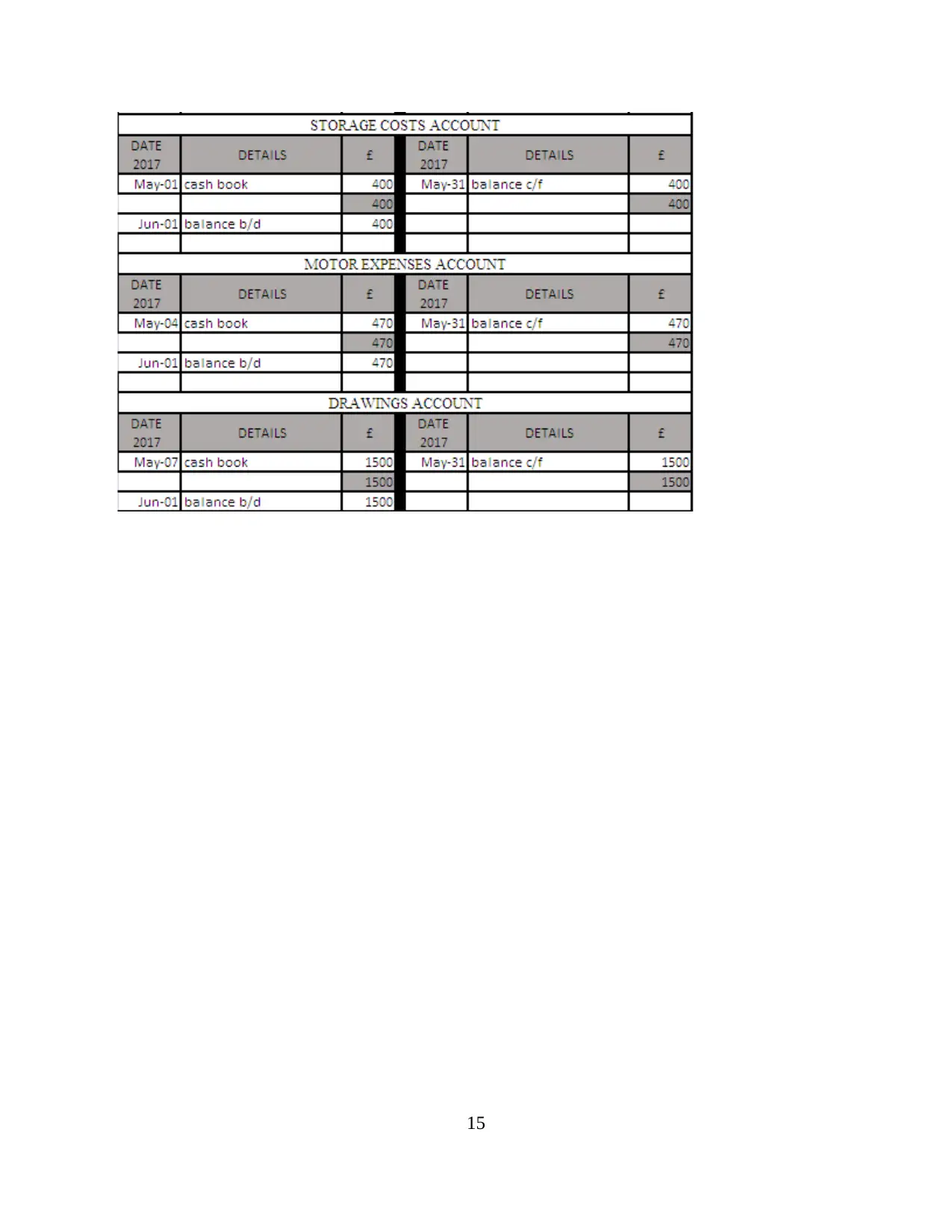

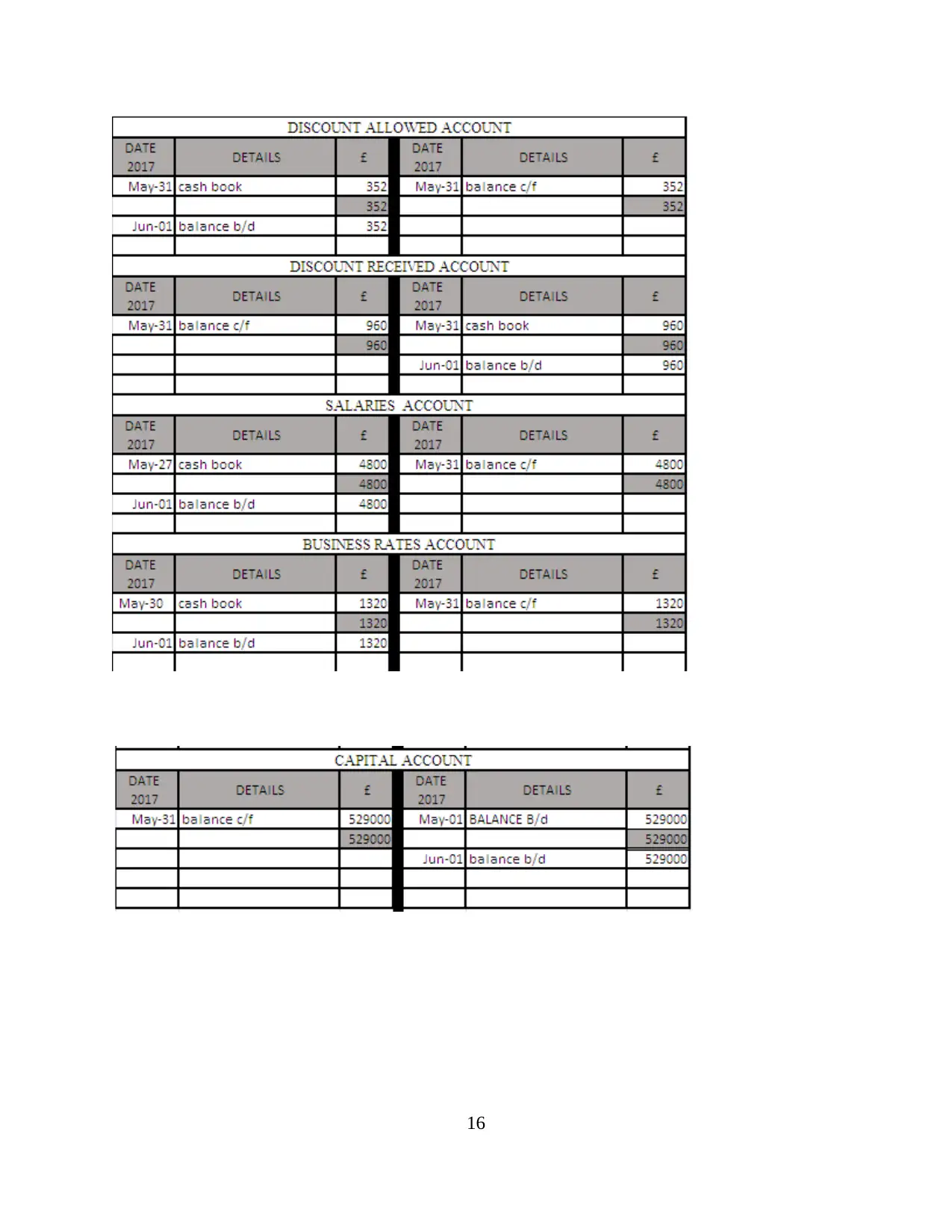

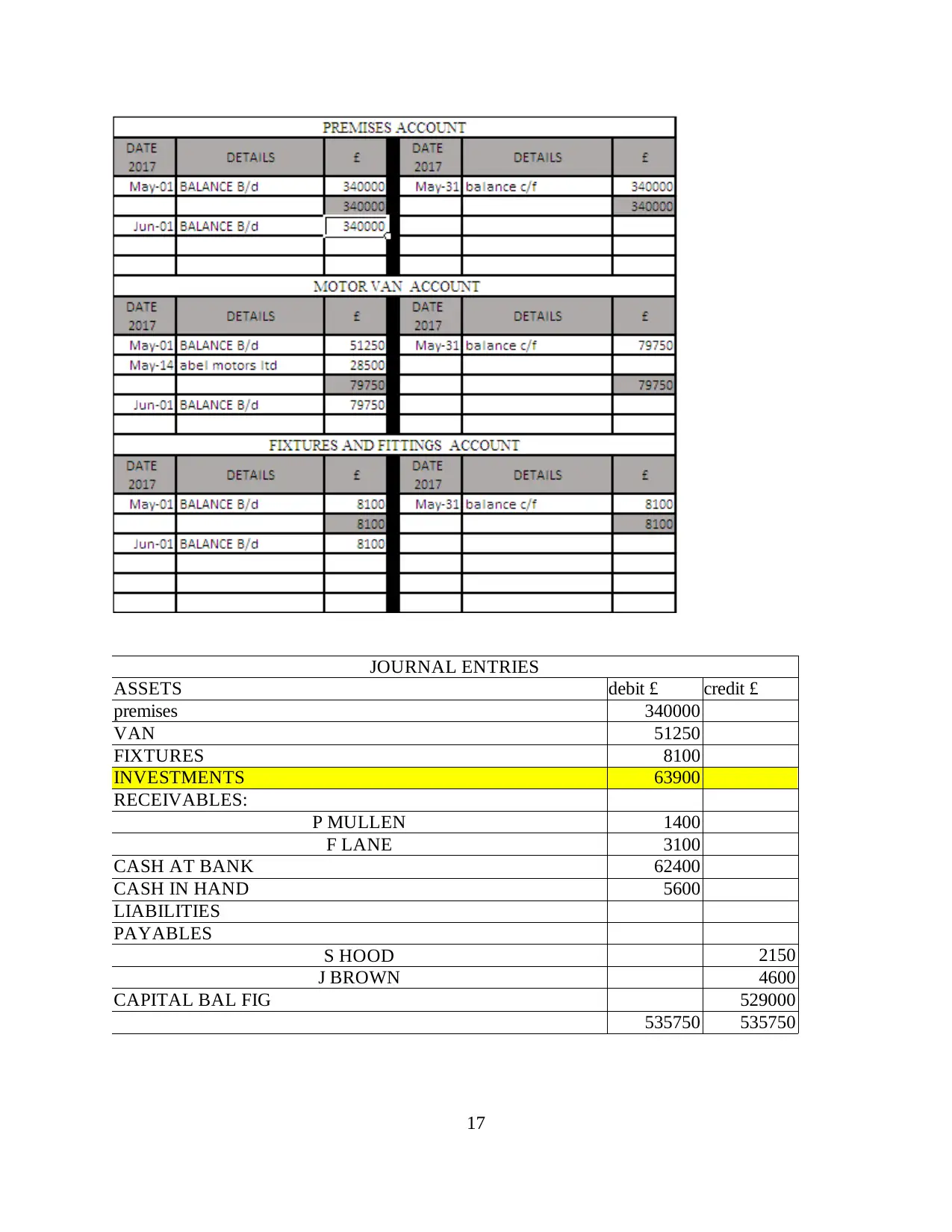

2. Preparation of ledger accounts

Ledger accounts are further bifurcation of the entries passed in journal. This means that

individual accounts are maintained by the business. This provides clarity to organisation

regarding various costs and income earned as every transaction is evaluated in it. This help

management to analyse expenditures and as such, control can be easily initiated on the same.

8

Ledger accounts are further bifurcation of the entries passed in journal. This means that

individual accounts are maintained by the business. This provides clarity to organisation

regarding various costs and income earned as every transaction is evaluated in it. This help

management to analyse expenditures and as such, control can be easily initiated on the same.

8

9

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

12

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

14

15

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

JOURNAL ENTRIES

ASSETS debit £ credit £

premises 340000

VAN 51250

FIXTURES 8100

INVESTMENTS 63900

RECEIVABLES:

P MULLEN 1400

F LANE 3100

CASH AT BANK 62400

CASH IN HAND 5600

LIABILITIES

PAYABLES

S HOOD 2150

J BROWN 4600

CAPITAL BAL FIG 529000

535750 535750

17

ASSETS debit £ credit £

premises 340000

VAN 51250

FIXTURES 8100

INVESTMENTS 63900

RECEIVABLES:

P MULLEN 1400

F LANE 3100

CASH AT BANK 62400

CASH IN HAND 5600

LIABILITIES

PAYABLES

S HOOD 2150

J BROWN 4600

CAPITAL BAL FIG 529000

535750 535750

17

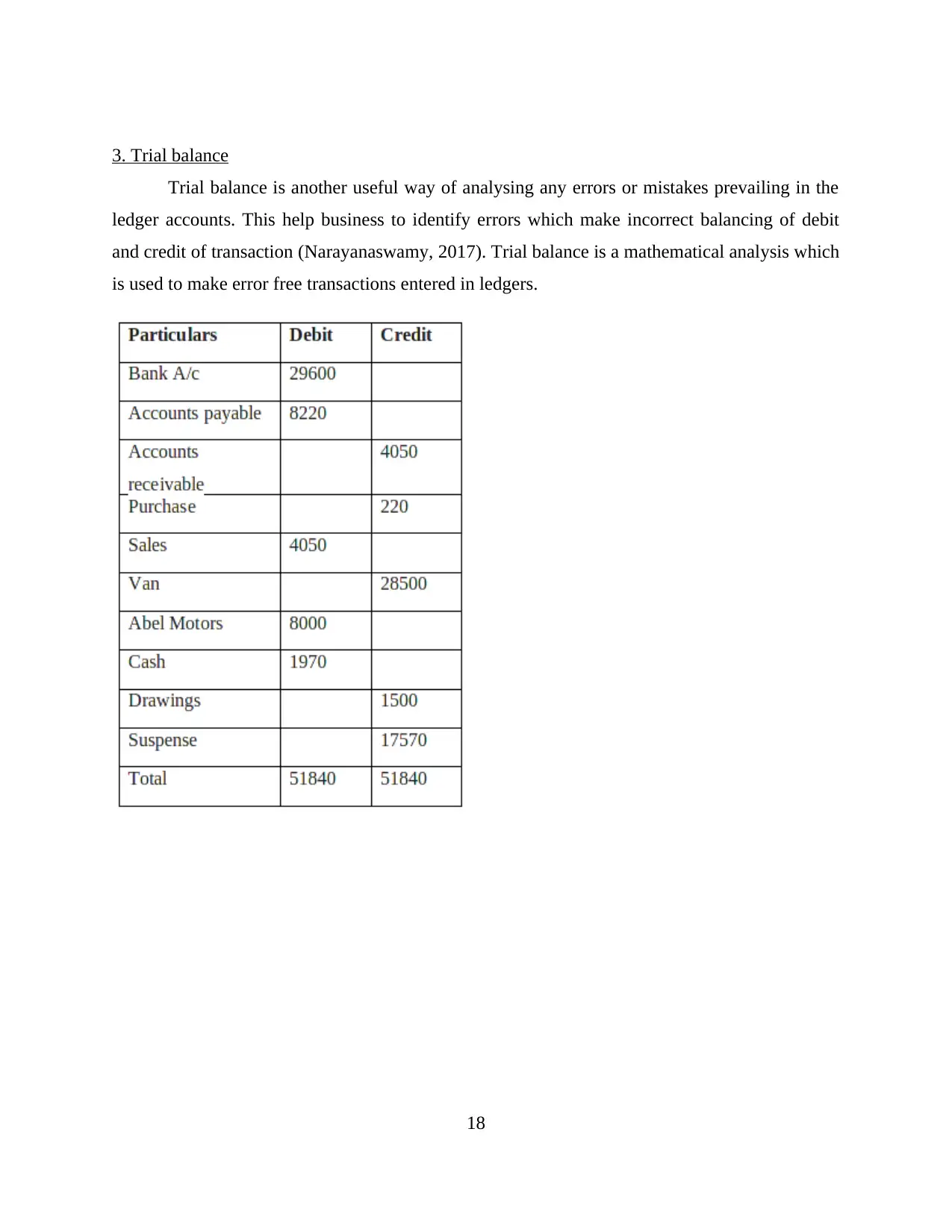

3. Trial balance

Trial balance is another useful way of analysing any errors or mistakes prevailing in the

ledger accounts. This help business to identify errors which make incorrect balancing of debit

and credit of transaction (Narayanaswamy, 2017). Trial balance is a mathematical analysis which

is used to make error free transactions entered in ledgers.

18

Trial balance is another useful way of analysing any errors or mistakes prevailing in the

ledger accounts. This help business to identify errors which make incorrect balancing of debit

and credit of transaction (Narayanaswamy, 2017). Trial balance is a mathematical analysis which

is used to make error free transactions entered in ledgers.

18

M1. Purchase and sale transactions

Purchase and sale transactions can be analysed. Purchase transactions is 38320 and

figures of sales is 10930.

D1 Trial balance

It is prepared in accordance to the guidelines provided by various accounting professional

bodies to remove mistakes and initiate accuracy.

CLIENT 2

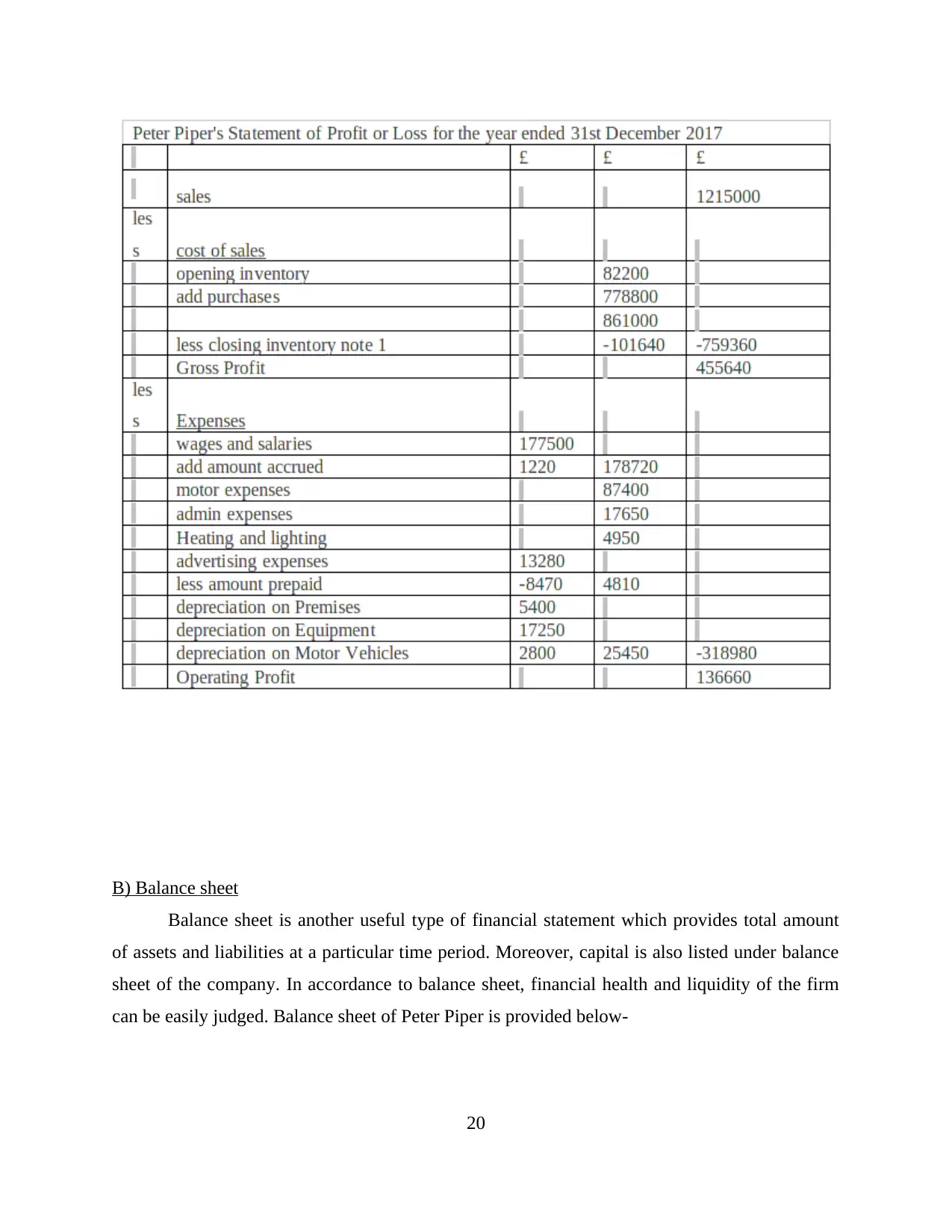

A) Income statement

Income statement is prepared to make analysis of profit earned or loss suffered by the

business for a particular time period. Thus, income statement provides clarity about financial

performance of the company in the best possible way (Richardson, 2017). This help to attain

overall efficiency and effectiveness of organisation whether it is earning adequately or not.

19

Purchase and sale transactions can be analysed. Purchase transactions is 38320 and

figures of sales is 10930.

D1 Trial balance

It is prepared in accordance to the guidelines provided by various accounting professional

bodies to remove mistakes and initiate accuracy.

CLIENT 2

A) Income statement

Income statement is prepared to make analysis of profit earned or loss suffered by the

business for a particular time period. Thus, income statement provides clarity about financial

performance of the company in the best possible way (Richardson, 2017). This help to attain

overall efficiency and effectiveness of organisation whether it is earning adequately or not.

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

B) Balance sheet

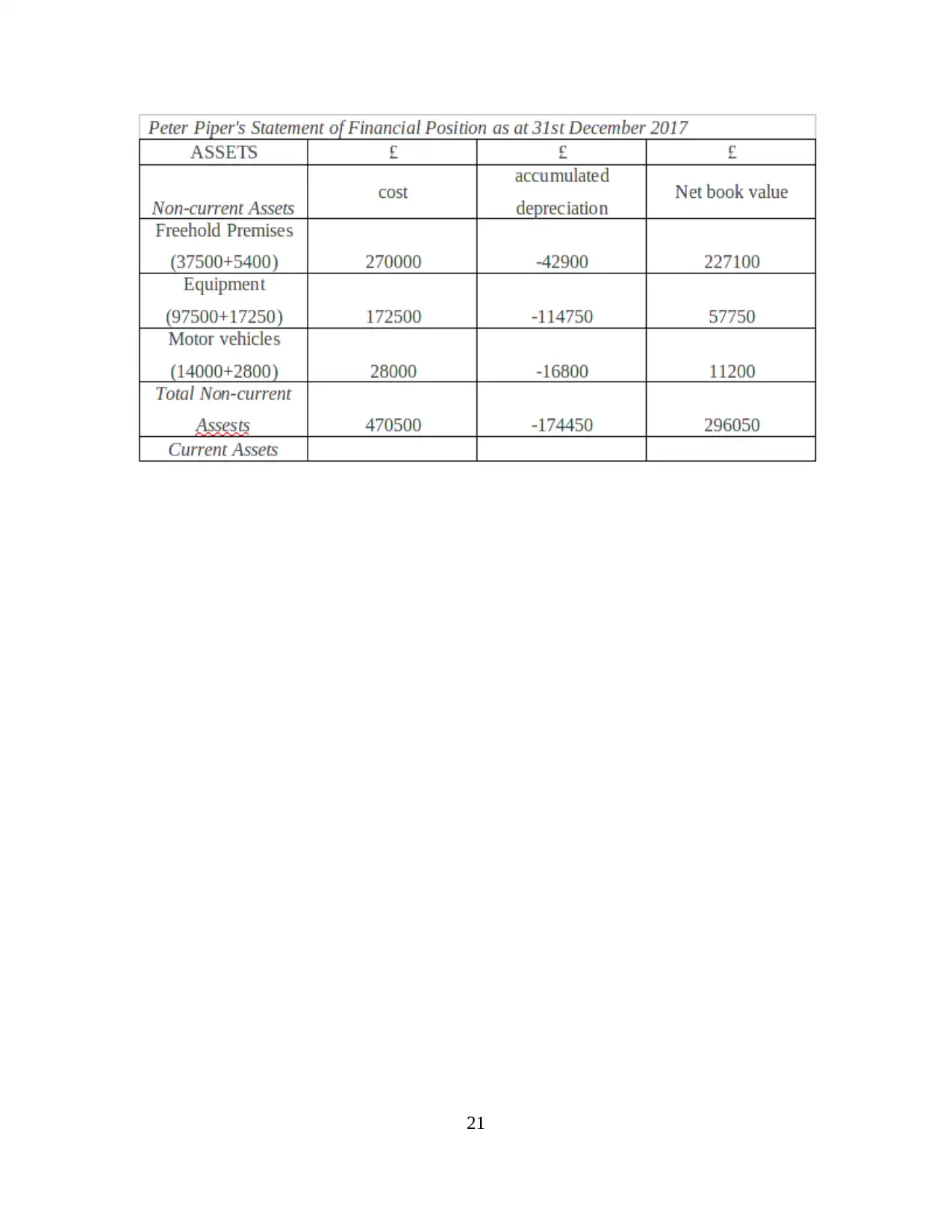

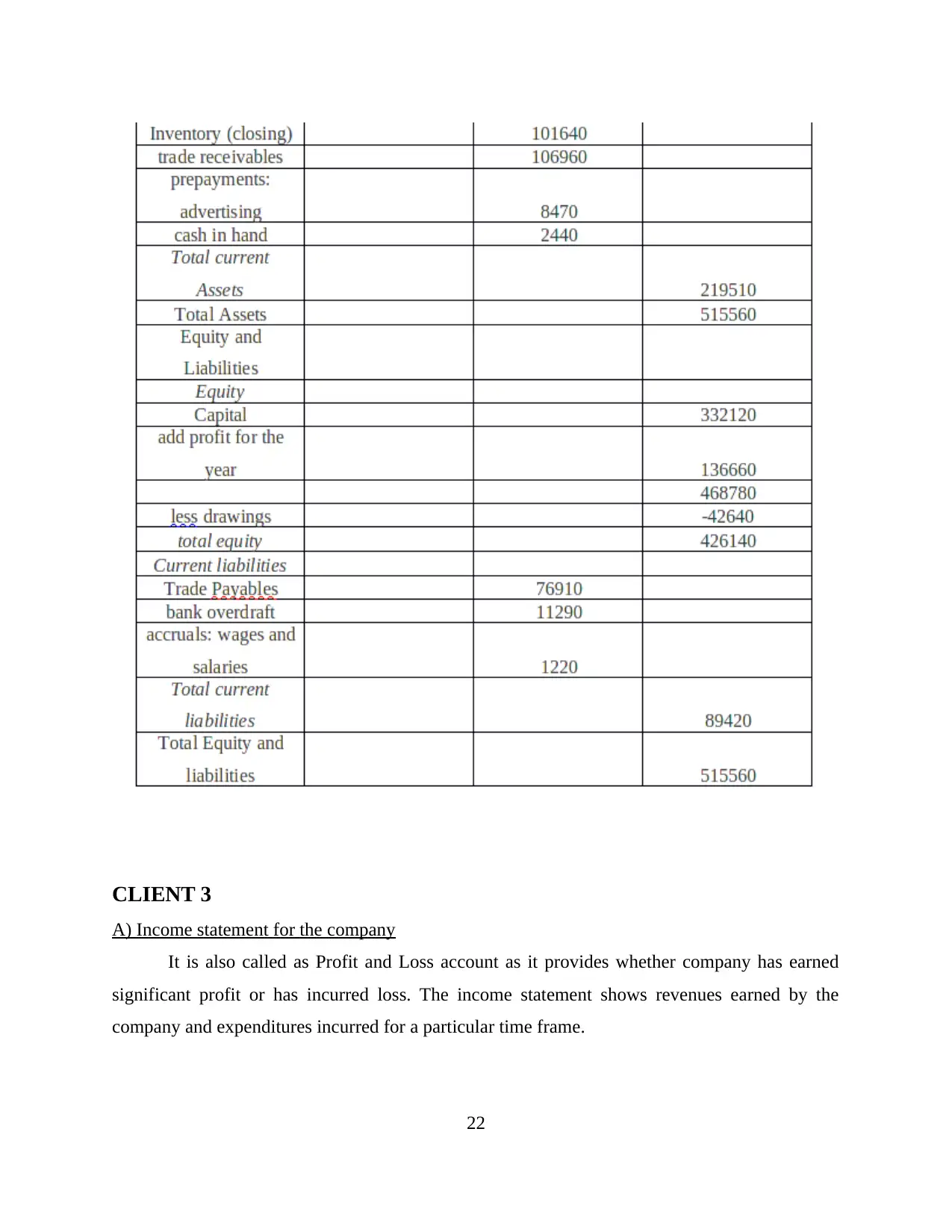

Balance sheet is another useful type of financial statement which provides total amount

of assets and liabilities at a particular time period. Moreover, capital is also listed under balance

sheet of the company. In accordance to balance sheet, financial health and liquidity of the firm

can be easily judged. Balance sheet of Peter Piper is provided below-

20

Balance sheet is another useful type of financial statement which provides total amount

of assets and liabilities at a particular time period. Moreover, capital is also listed under balance

sheet of the company. In accordance to balance sheet, financial health and liquidity of the firm

can be easily judged. Balance sheet of Peter Piper is provided below-

20

21

CLIENT 3

A) Income statement for the company

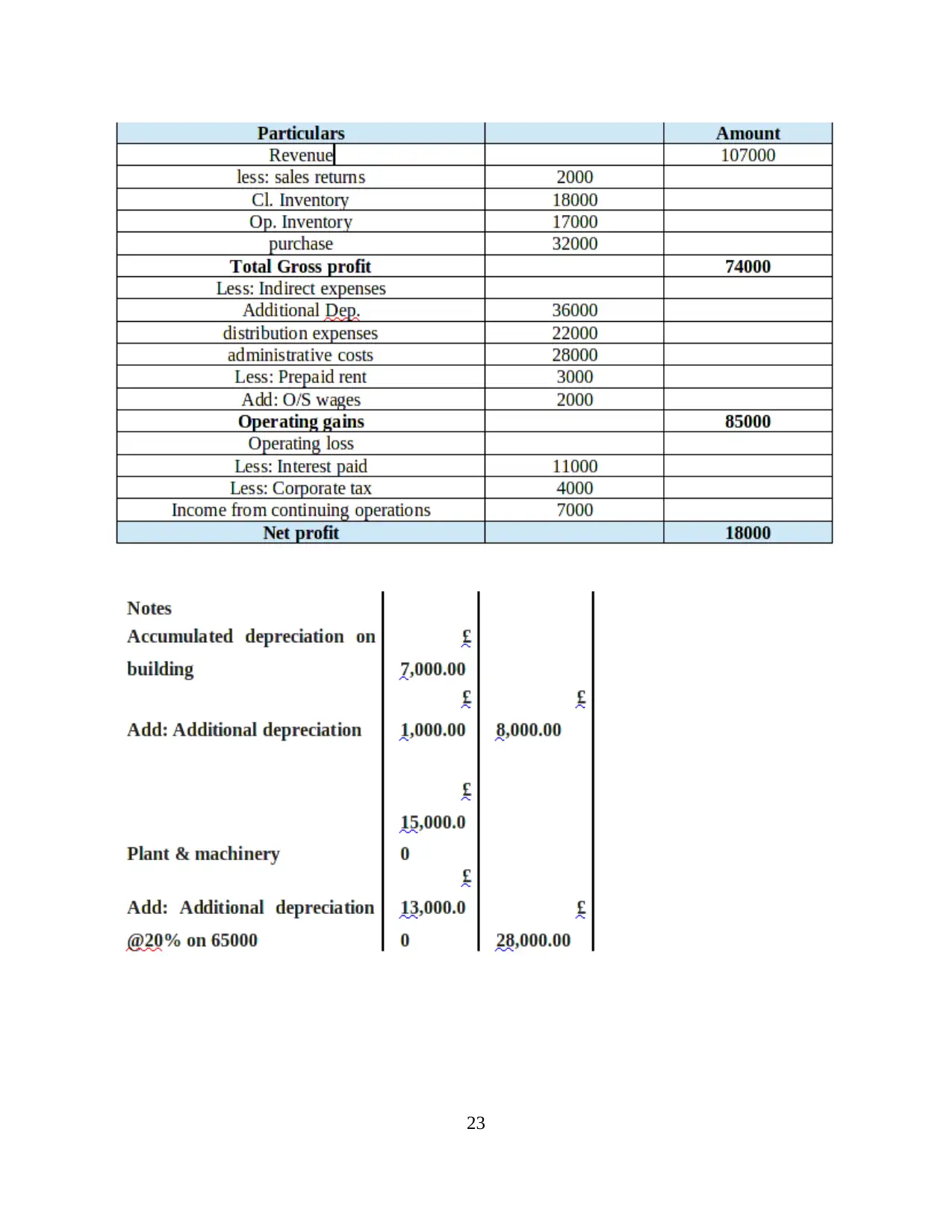

It is also called as Profit and Loss account as it provides whether company has earned

significant profit or has incurred loss. The income statement shows revenues earned by the

company and expenditures incurred for a particular time frame.

22

A) Income statement for the company

It is also called as Profit and Loss account as it provides whether company has earned

significant profit or has incurred loss. The income statement shows revenues earned by the

company and expenditures incurred for a particular time frame.

22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

23

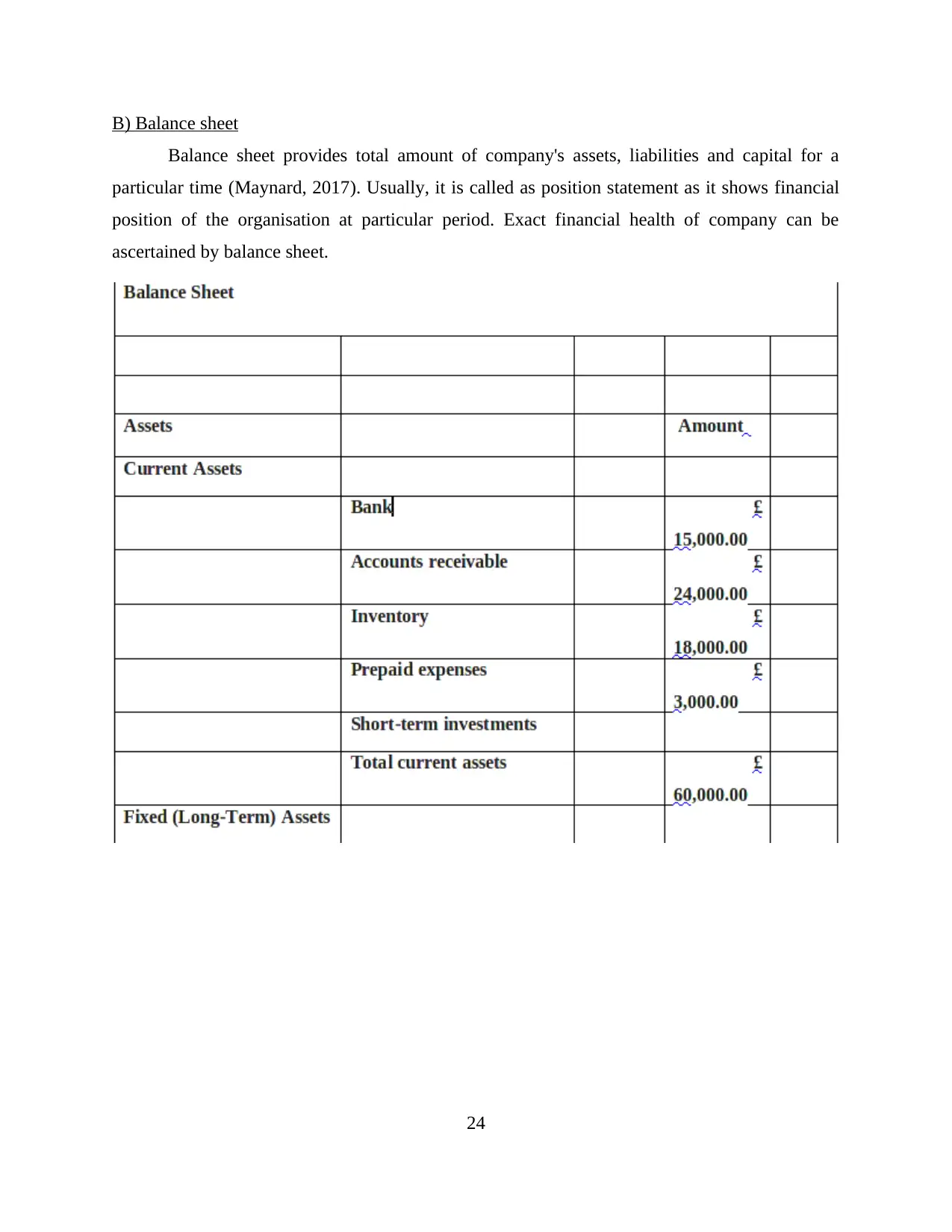

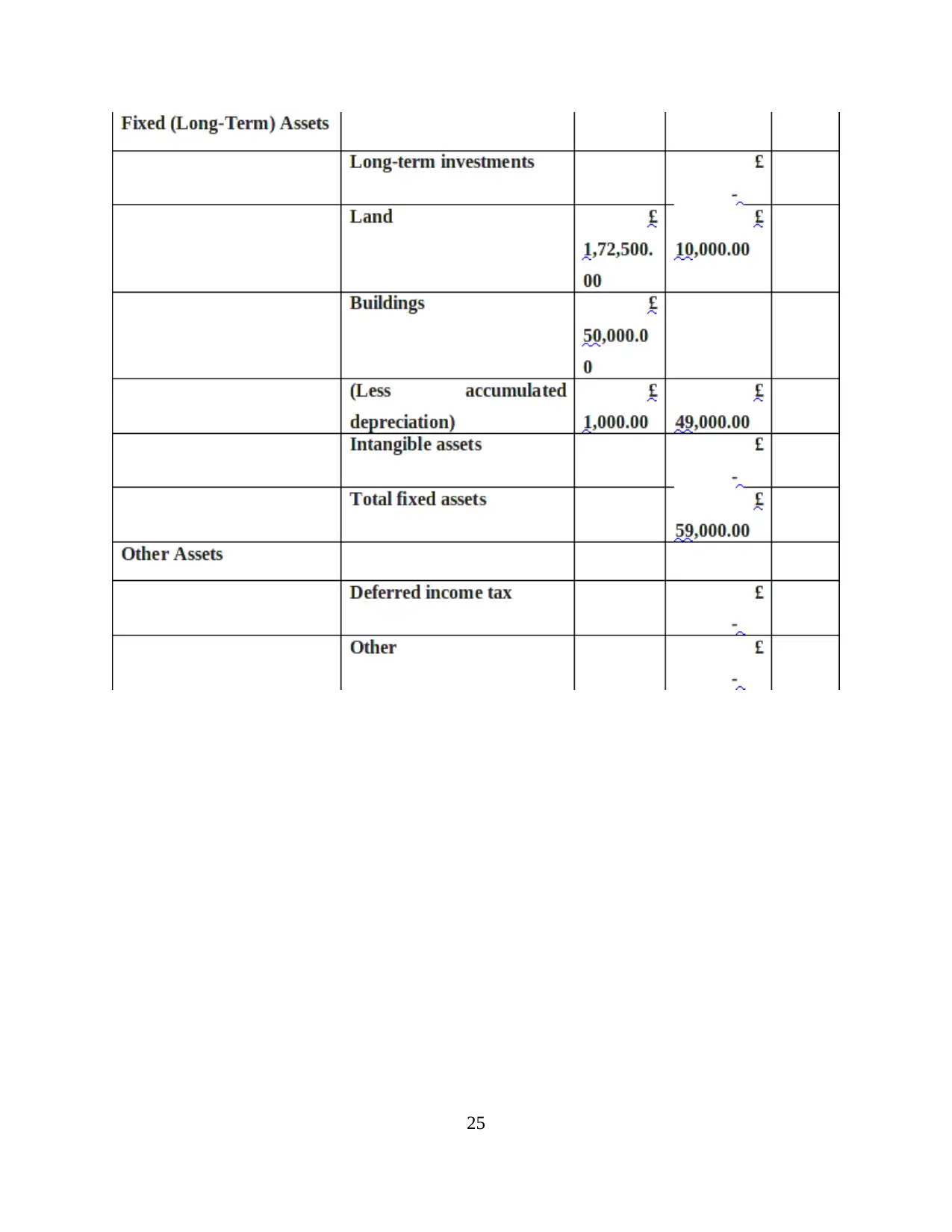

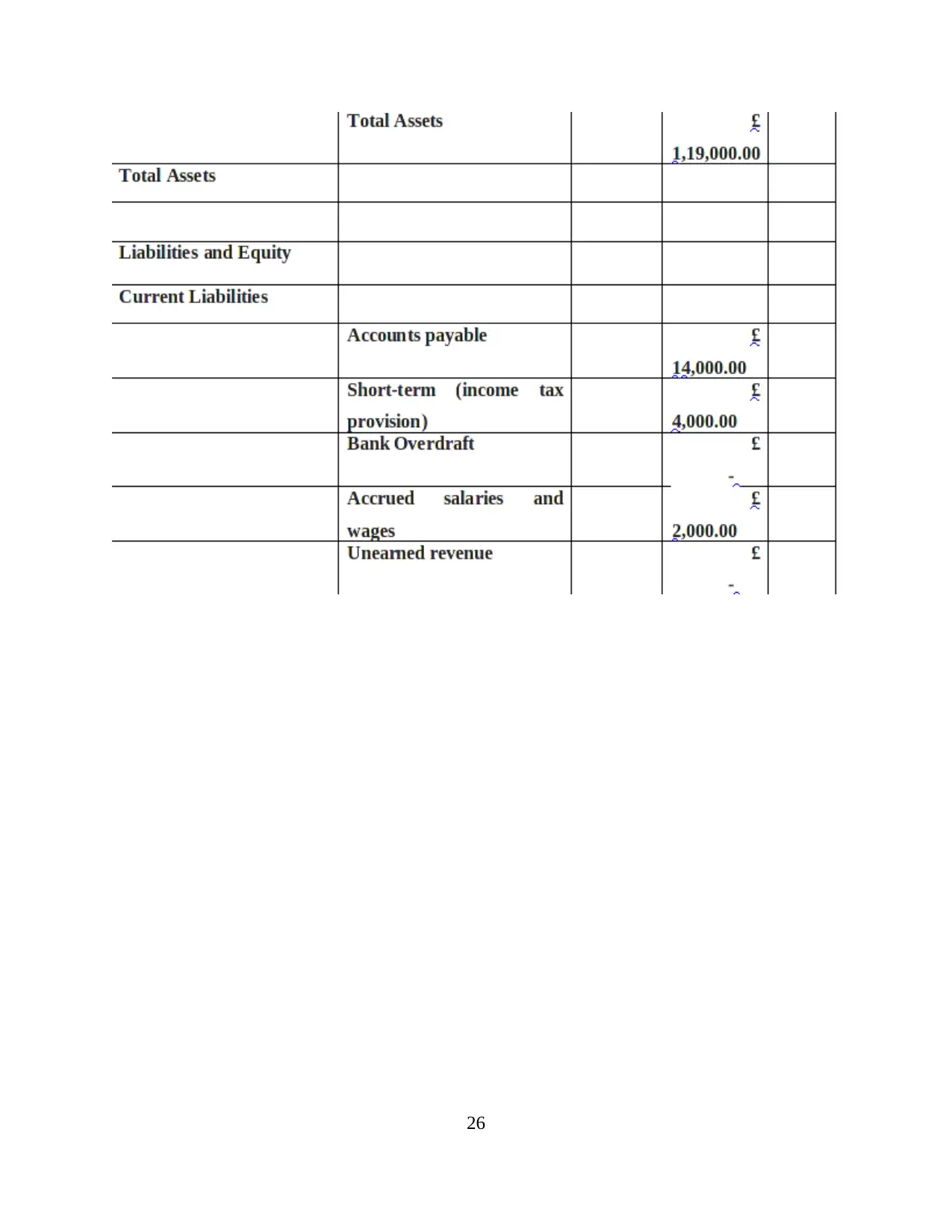

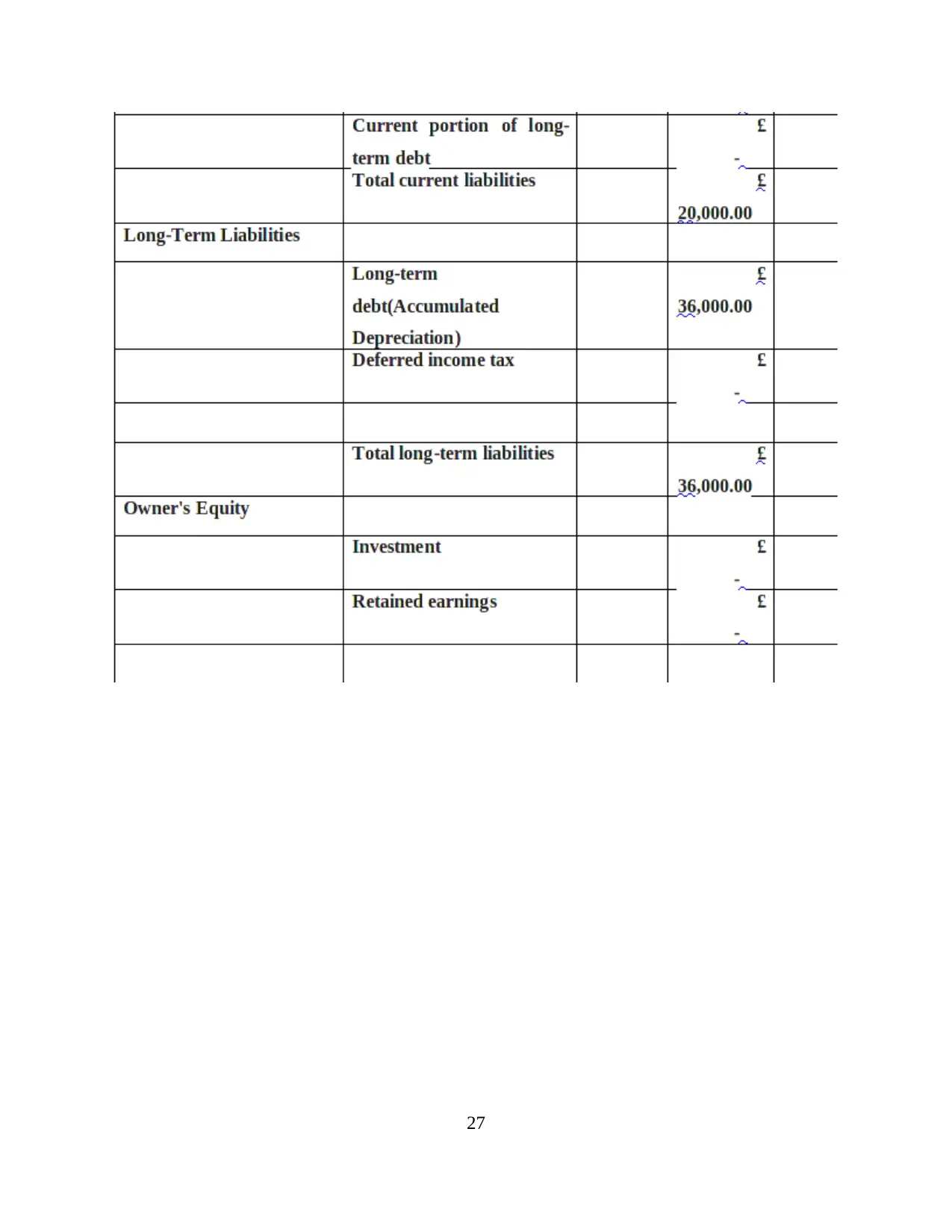

B) Balance sheet

Balance sheet provides total amount of company's assets, liabilities and capital for a

particular time (Maynard, 2017). Usually, it is called as position statement as it shows financial

position of the organisation at particular period. Exact financial health of company can be

ascertained by balance sheet.

24

Balance sheet provides total amount of company's assets, liabilities and capital for a

particular time (Maynard, 2017). Usually, it is called as position statement as it shows financial

position of the organisation at particular period. Exact financial health of company can be

ascertained by balance sheet.

24

25

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

26

27

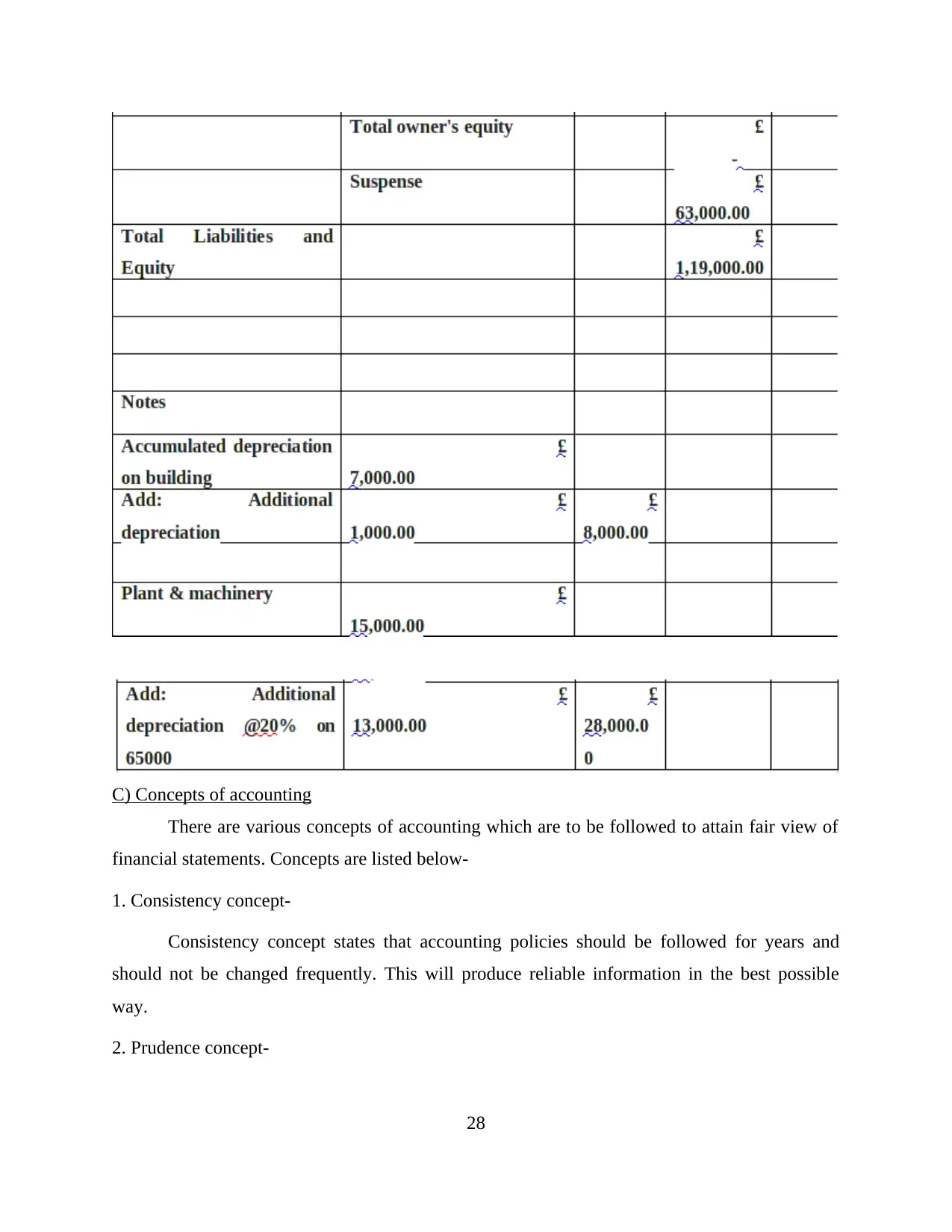

C) Concepts of accounting

There are various concepts of accounting which are to be followed to attain fair view of

financial statements. Concepts are listed below-

1. Consistency concept-

Consistency concept states that accounting policies should be followed for years and

should not be changed frequently. This will produce reliable information in the best possible

way.

2. Prudence concept-

28

There are various concepts of accounting which are to be followed to attain fair view of

financial statements. Concepts are listed below-

1. Consistency concept-

Consistency concept states that accounting policies should be followed for years and

should not be changed frequently. This will produce reliable information in the best possible

way.

2. Prudence concept-

28

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Prudence concept states that organisation should estimate for losses and not for income.

This is required as business initiates activities in dynamic world where changes quite frequently.

Thus, underestimation of liabilities and overestimation of assets should not be implemented.

D) Methods of deprecation

Deprecation is charge on profit made on the fixed assets caused due to passage of time

and normal wear and tear over a period (Dung, 2016). The various methods of deprecation are as

follows-

1. Straight line method:

The deprecation is charged same year after year and remains constant. It is charged until

life of fixed asset does not become zero at the end of asset life.

2. Written down method :

The deprecation does not remain constant and amount diminishes year after year.

Moreover, life of asset never become zero.

M2 Income statement, balance sheet and cash flow statements

All the three financial statements are required in the company so that true position

regarding financial performance of company may be evaluated.

D2 Calculations in producing final accounts

Assets and liabilities is shown from the balance sheet prepared. Assets are 137000,

liabilities are 137000 and stockholder's equity is 102000.

CLIENT 4

A) Bank statement

Bank statement is required as transactions recorded by the business and bank are never

listed at the same date. This produces discrepancies as both the balance are not matched. Thus,

bank statement is prepared for removing differences (Damodaran, 2016).

B) Outlining causes for preparing bank statements

The balances differ of bank's passbook and organisation because when cheques are

outstanding, cheque become dishonoured and other reasons.

29

This is required as business initiates activities in dynamic world where changes quite frequently.

Thus, underestimation of liabilities and overestimation of assets should not be implemented.

D) Methods of deprecation

Deprecation is charge on profit made on the fixed assets caused due to passage of time

and normal wear and tear over a period (Dung, 2016). The various methods of deprecation are as

follows-

1. Straight line method:

The deprecation is charged same year after year and remains constant. It is charged until

life of fixed asset does not become zero at the end of asset life.

2. Written down method :

The deprecation does not remain constant and amount diminishes year after year.

Moreover, life of asset never become zero.

M2 Income statement, balance sheet and cash flow statements

All the three financial statements are required in the company so that true position

regarding financial performance of company may be evaluated.

D2 Calculations in producing final accounts

Assets and liabilities is shown from the balance sheet prepared. Assets are 137000,

liabilities are 137000 and stockholder's equity is 102000.

CLIENT 4

A) Bank statement

Bank statement is required as transactions recorded by the business and bank are never

listed at the same date. This produces discrepancies as both the balance are not matched. Thus,

bank statement is prepared for removing differences (Damodaran, 2016).

B) Outlining causes for preparing bank statements

The balances differ of bank's passbook and organisation because when cheques are

outstanding, cheque become dishonoured and other reasons.

29

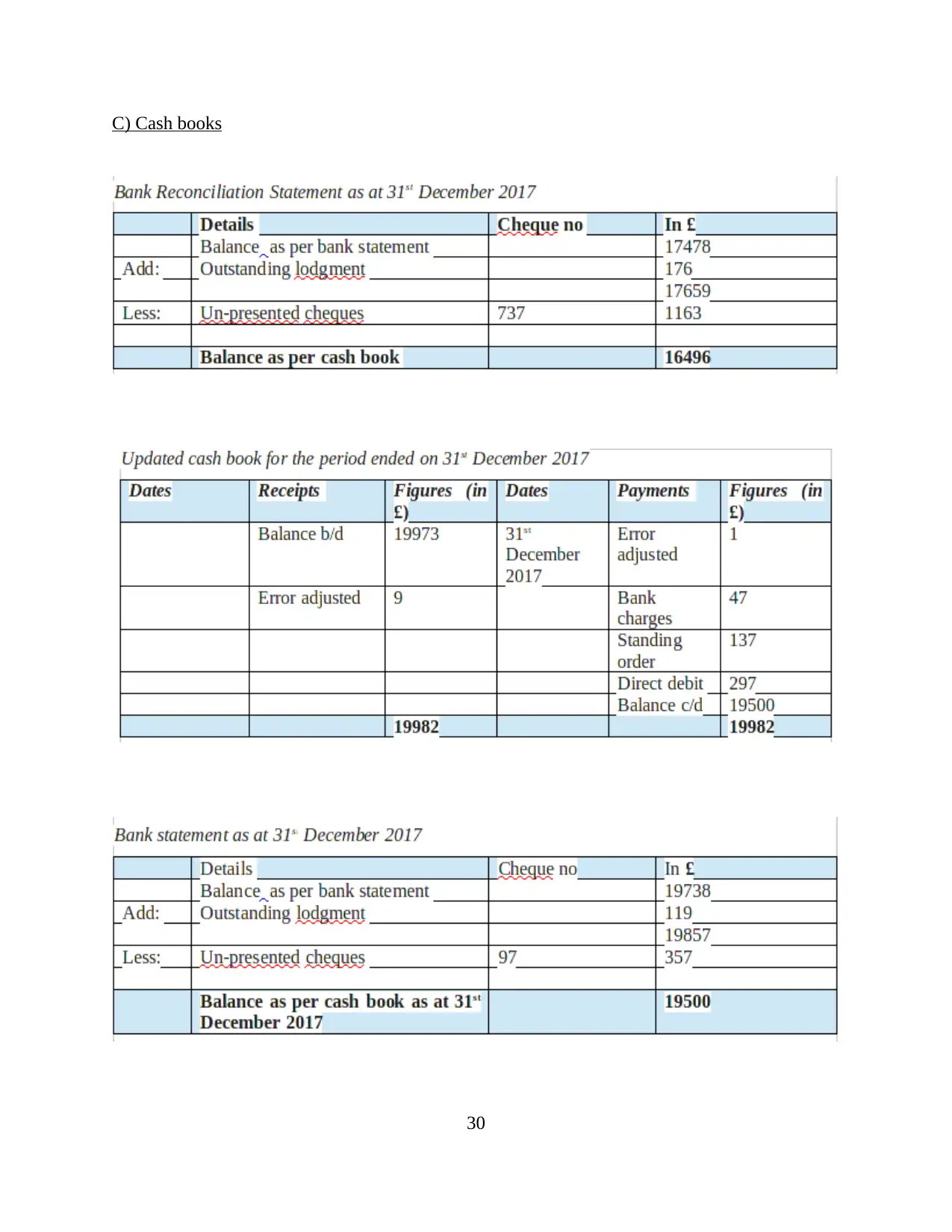

C) Cash books

30

30

M3 Reconciliation process

Cheques outstanding: When bank clears cheque at a later date, then, balance differs of

organisation and bank's passbook (Dutta and Patatoukas, 2016).

Insufficient funds in account: In the case of insufficient funds, differences will exist.

D3 BRS

CLIENT 5

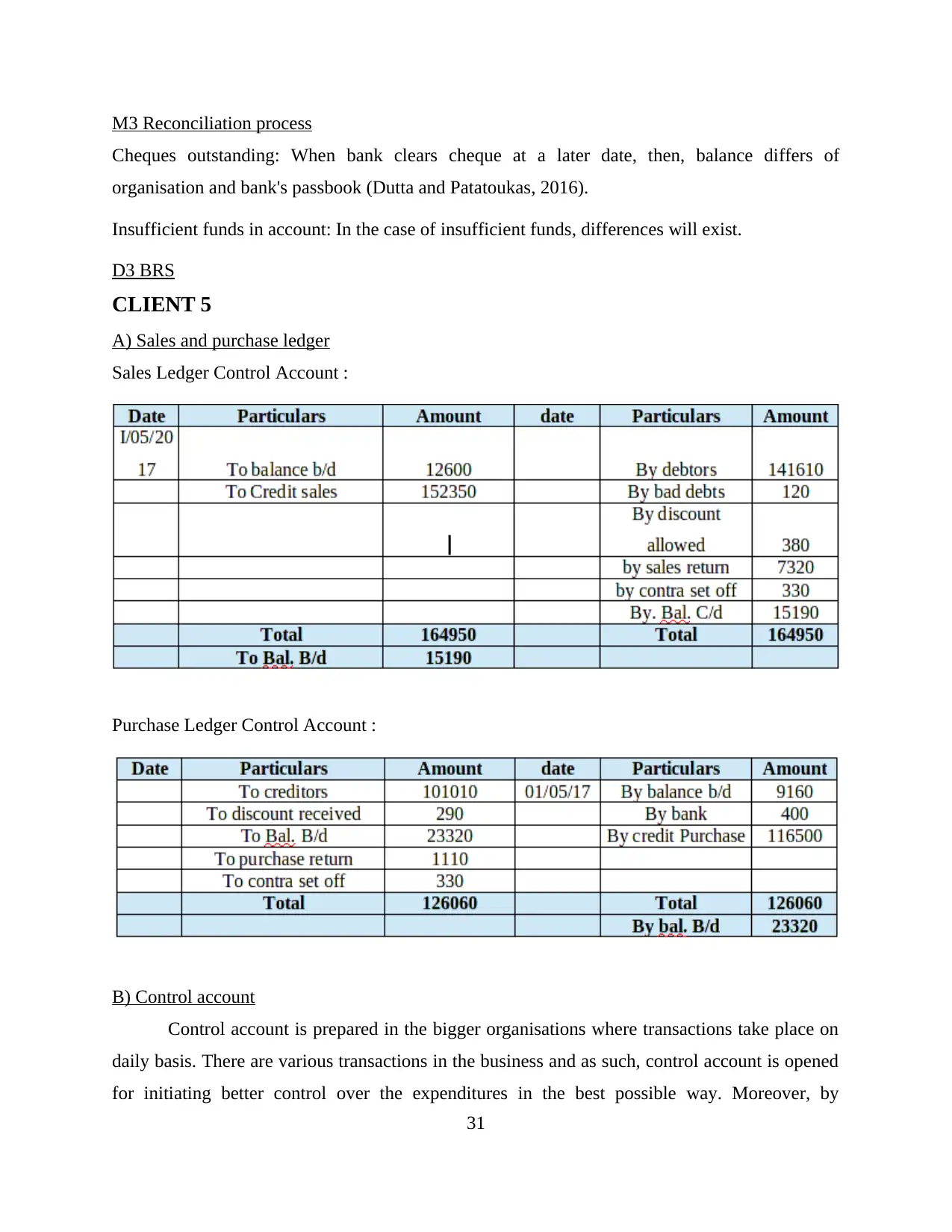

A) Sales and purchase ledger

Sales Ledger Control Account :

Purchase Ledger Control Account :

B) Control account

Control account is prepared in the bigger organisations where transactions take place on

daily basis. There are various transactions in the business and as such, control account is opened

for initiating better control over the expenditures in the best possible way. Moreover, by

31

Cheques outstanding: When bank clears cheque at a later date, then, balance differs of

organisation and bank's passbook (Dutta and Patatoukas, 2016).

Insufficient funds in account: In the case of insufficient funds, differences will exist.

D3 BRS

CLIENT 5

A) Sales and purchase ledger

Sales Ledger Control Account :

Purchase Ledger Control Account :

B) Control account

Control account is prepared in the bigger organisations where transactions take place on

daily basis. There are various transactions in the business and as such, control account is opened

for initiating better control over the expenditures in the best possible way. Moreover, by

31

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

analysing various costs, monitoring can be easily done and as a result, business can earn good

revenue quite easily.

CLIENT 6

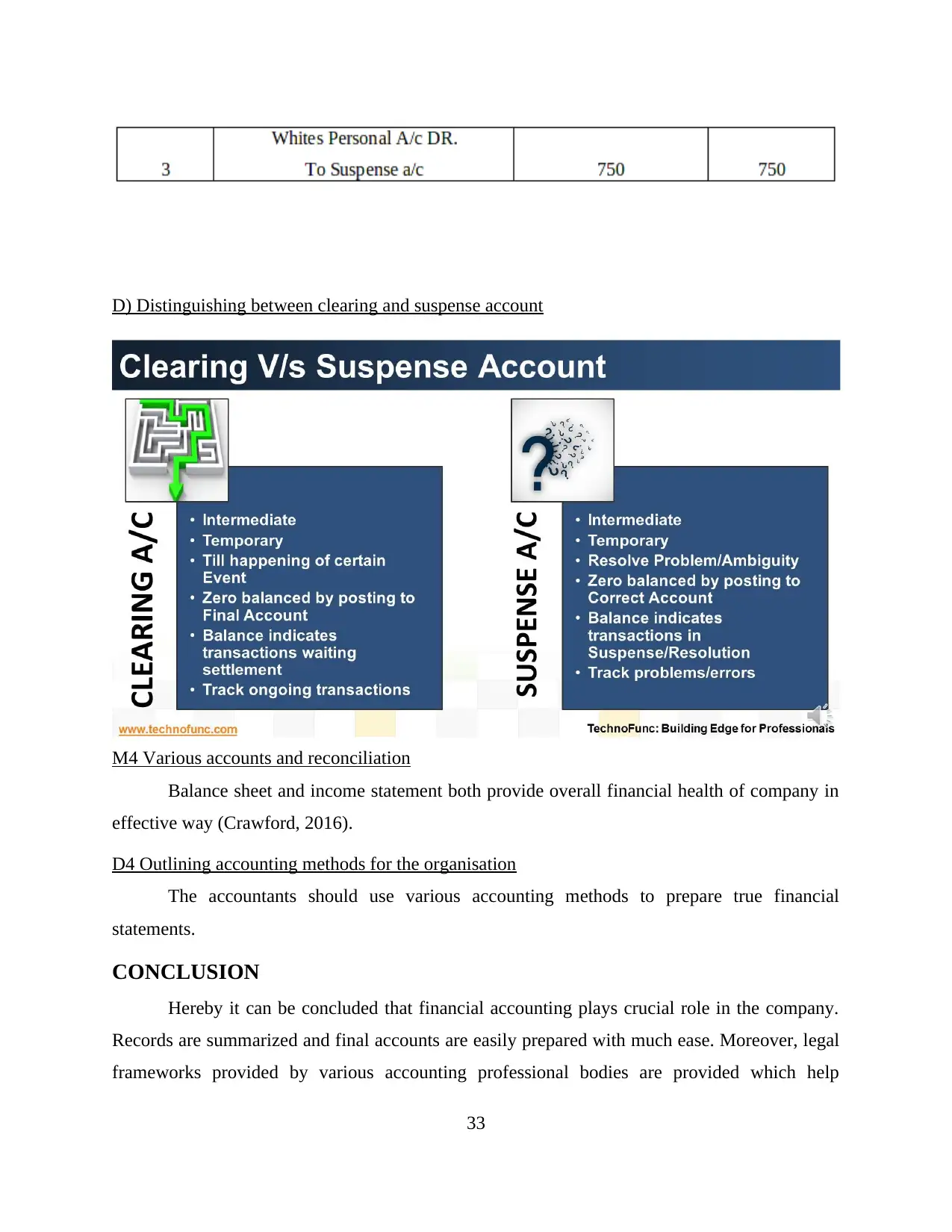

A) Suspense account and explaining features

Suspense account is prepared in the event when there exists inequality in the transaction.

This account is a type of temporary ledger account which is prepared until variations are not

analysed by the company (Grant, 2016).

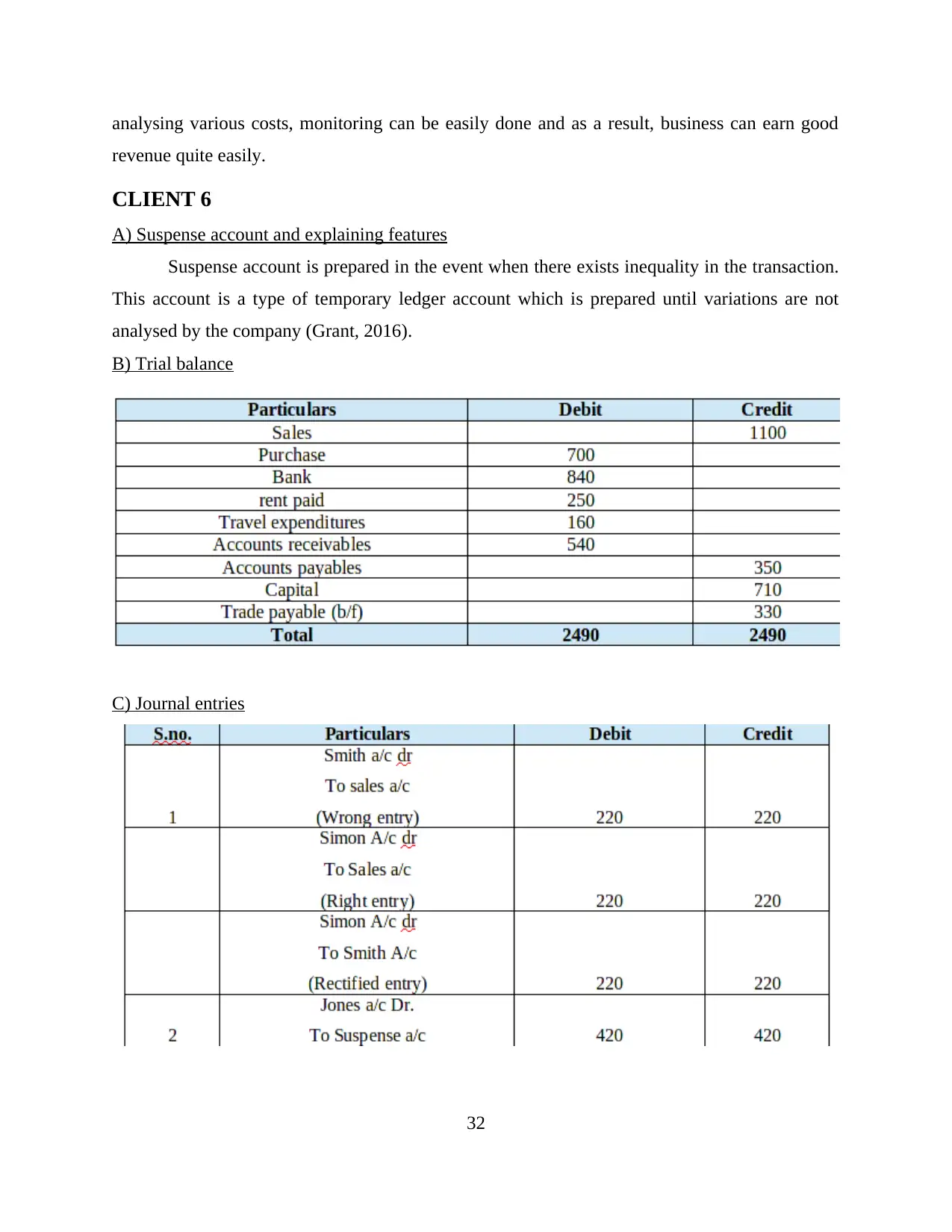

B) Trial balance

C) Journal entries

32

revenue quite easily.

CLIENT 6

A) Suspense account and explaining features

Suspense account is prepared in the event when there exists inequality in the transaction.

This account is a type of temporary ledger account which is prepared until variations are not

analysed by the company (Grant, 2016).

B) Trial balance

C) Journal entries

32

D) Distinguishing between clearing and suspense account

M4 Various accounts and reconciliation

Balance sheet and income statement both provide overall financial health of company in

effective way (Crawford, 2016).

D4 Outlining accounting methods for the organisation

The accountants should use various accounting methods to prepare true financial

statements.

CONCLUSION

Hereby it can be concluded that financial accounting plays crucial role in the company.

Records are summarized and final accounts are easily prepared with much ease. Moreover, legal

frameworks provided by various accounting professional bodies are provided which help

33

M4 Various accounts and reconciliation

Balance sheet and income statement both provide overall financial health of company in

effective way (Crawford, 2016).

D4 Outlining accounting methods for the organisation

The accountants should use various accounting methods to prepare true financial

statements.

CONCLUSION

Hereby it can be concluded that financial accounting plays crucial role in the company.

Records are summarized and final accounts are easily prepared with much ease. Moreover, legal

frameworks provided by various accounting professional bodies are provided which help

33

accountants to adhere to and prepare adequate financials of the company. Thus, financial

accounting is quite significant to company in analysing overall financial performance in effectual

manner.

REFERENCES

Books and Journals

Campbell, J. L., Khan, U. and Pierce, S., 2017. The effect of mandatory disclosure on market

inefficiencies: Evidence from Statement of Financial Accounting Standard Number 161.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd.

Richardson, A. J., 2017. The Relationship between Management and Financial Accounting as

Professions and Technologies of Practice.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Dung, N. V., 2016. Value-relevance of financial statement information: A flexible application of

modern theories to the Vietnamese stock market. Quarterly Journal of Economics.

84. pp.488-500.

Dutta, S. and Patatoukas, P. N., 2016. Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review.

Grant, R. M., 2016. Contemporary Strategy Analysis Text Only. John Wiley & Sons.

Crawford, C. W., 2016. ACTG 201.05: Principles of Financial Accounting.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Online

Financial Reporting Council. 2017. [Online]. Available through :<https://www.frc.org.uk/>

34

accounting is quite significant to company in analysing overall financial performance in effectual

manner.

REFERENCES

Books and Journals

Campbell, J. L., Khan, U. and Pierce, S., 2017. The effect of mandatory disclosure on market

inefficiencies: Evidence from Statement of Financial Accounting Standard Number 161.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd.

Richardson, A. J., 2017. The Relationship between Management and Financial Accounting as

Professions and Technologies of Practice.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Dung, N. V., 2016. Value-relevance of financial statement information: A flexible application of

modern theories to the Vietnamese stock market. Quarterly Journal of Economics.

84. pp.488-500.

Dutta, S. and Patatoukas, P. N., 2016. Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review.

Grant, R. M., 2016. Contemporary Strategy Analysis Text Only. John Wiley & Sons.

Crawford, C. W., 2016. ACTG 201.05: Principles of Financial Accounting.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Online

Financial Reporting Council. 2017. [Online]. Available through :<https://www.frc.org.uk/>

34

1 out of 37

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.