ACCT6003 Financial Accounting Process: ChiHerbal Ltd Detailed Report

VerifiedAdded on 2023/06/09

|14

|1648

|386

Report

AI Summary

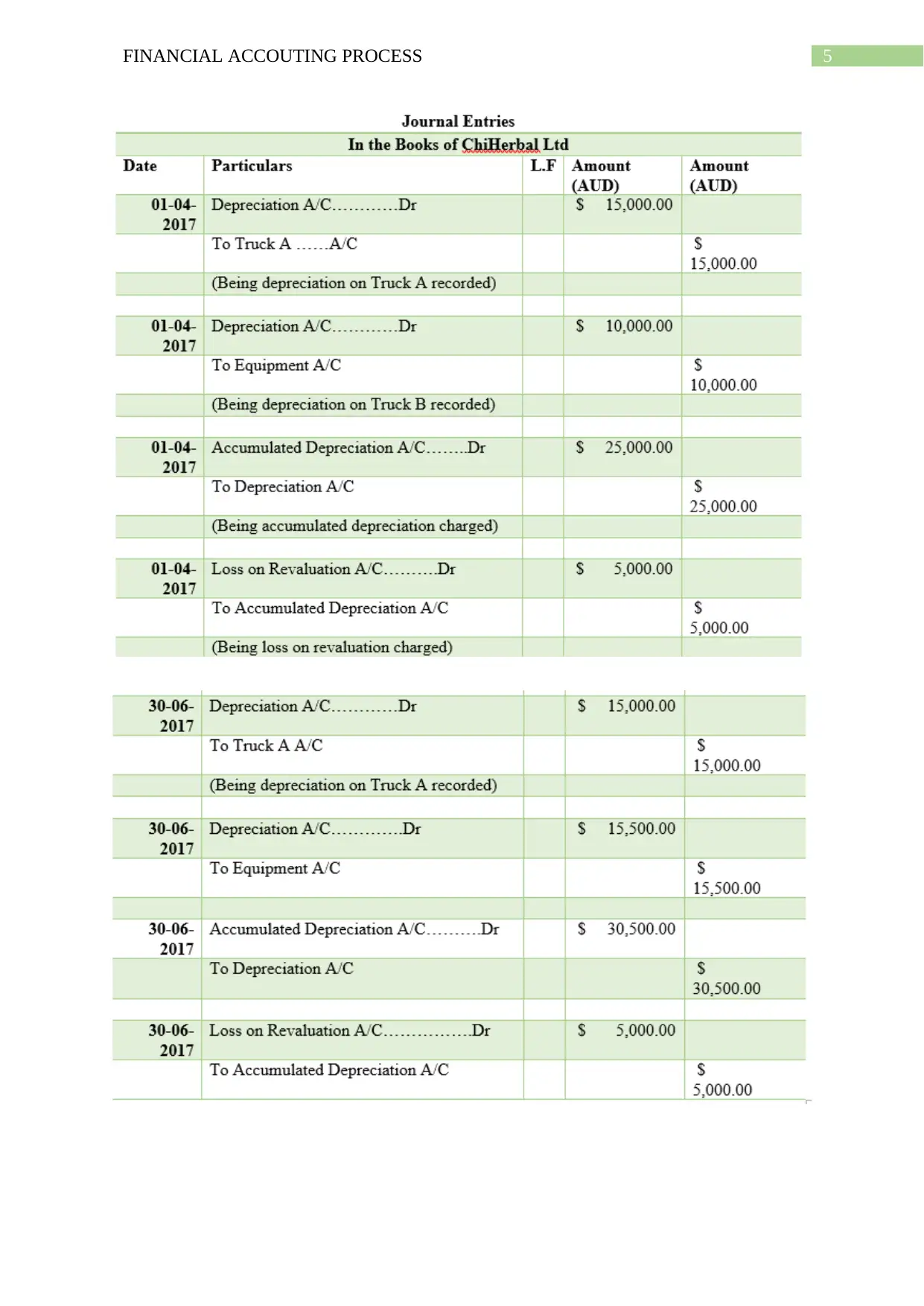

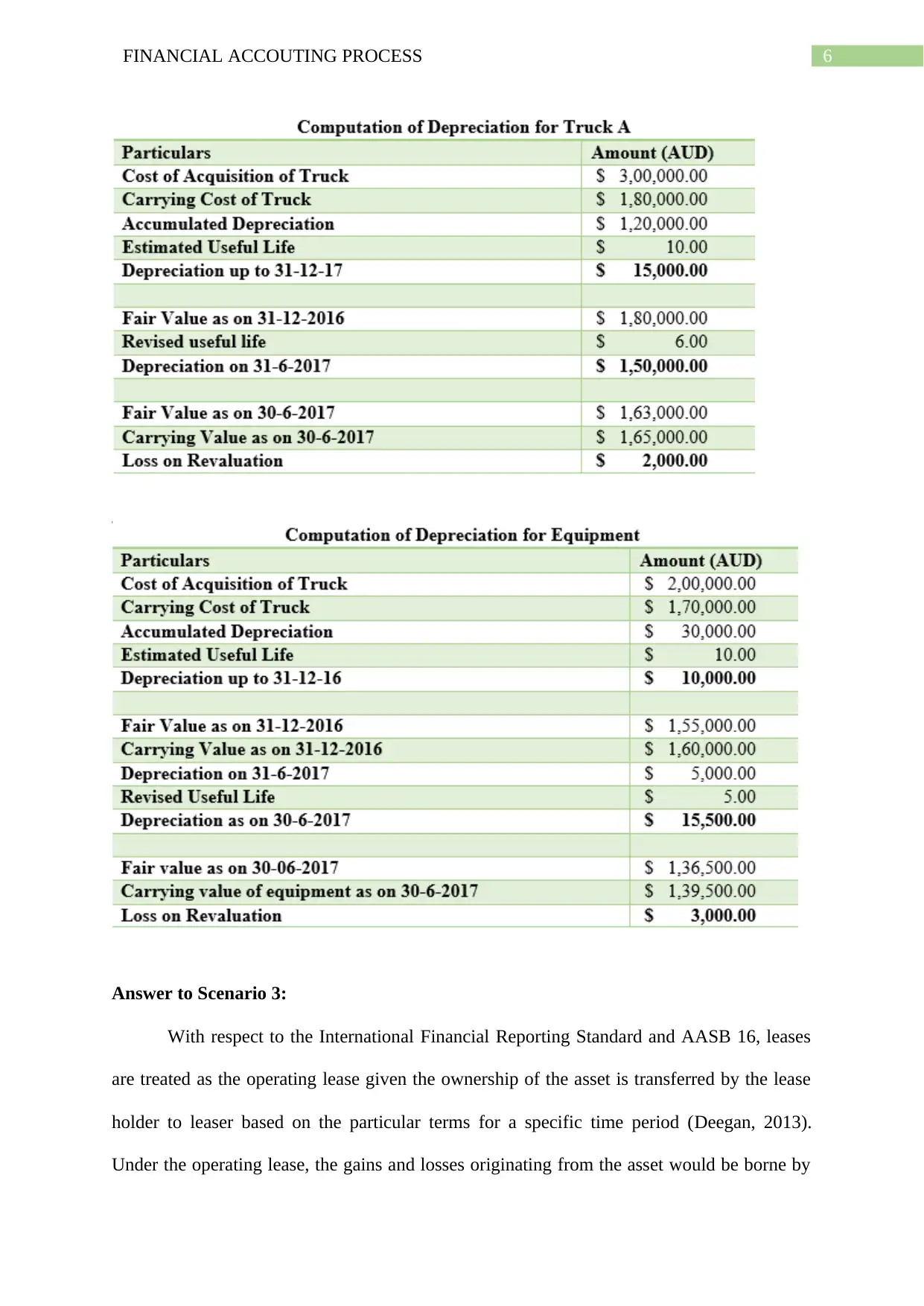

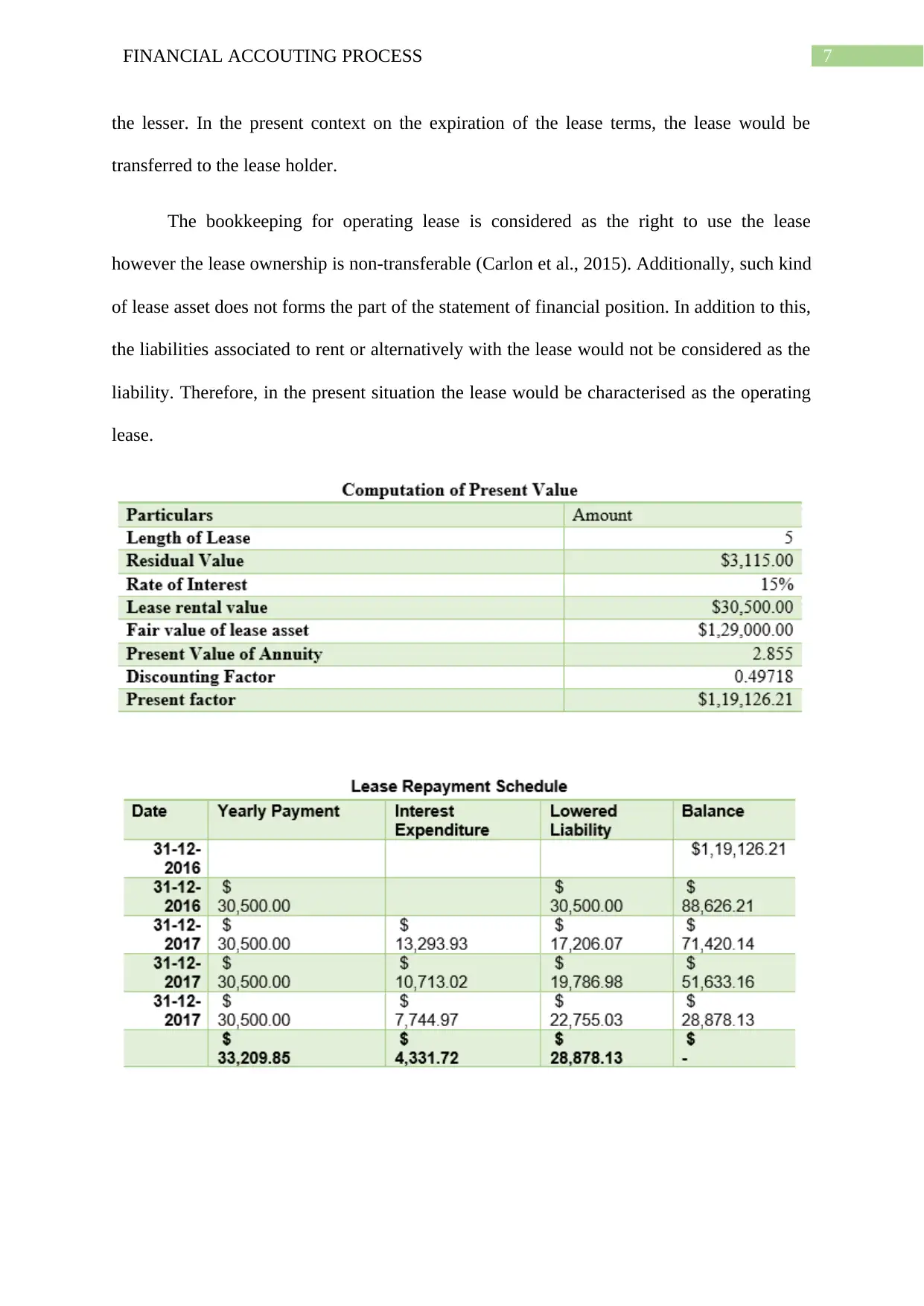

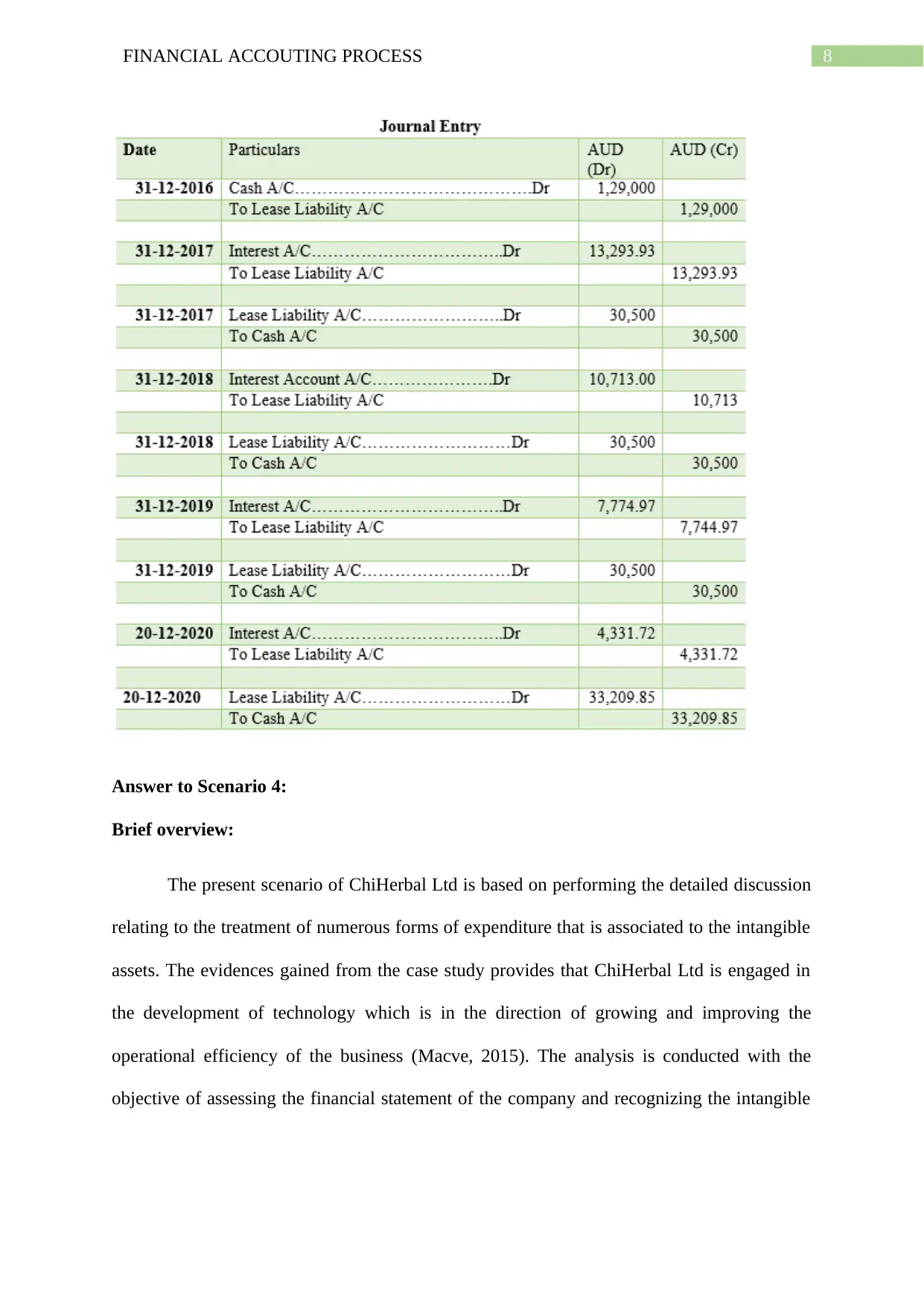

This report provides a financial accounting analysis of ChiHerbal Ltd, focusing on key areas such as lease accounting, intangible assets, and compliance with Australian Accounting Standards Board (AASB) standards, particularly AASB 138. The analysis includes a review of the company's balance sheet, the treatment of leases under IFRS and AASB 16, and a detailed examination of research and development expenditures related to a new filtration technology. The report assesses whether these expenditures can be classified as intangible assets, considering the provisions of AASB 138 regarding the capitalization of development costs and the recognition of intangible assets in financial statements. The report concludes that the expenditures meet the requirements of AASB 138 and should be recognized as intangible assets, with the management of ChiHerbal Ltd obligated to adhere to the provisions outlined in the standard. Desklib provides access to solved assignments and study tools for students.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.