Accounting Scenarios for Students

VerifiedAdded on 2020/09/08

|8

|1089

|421

AI Summary

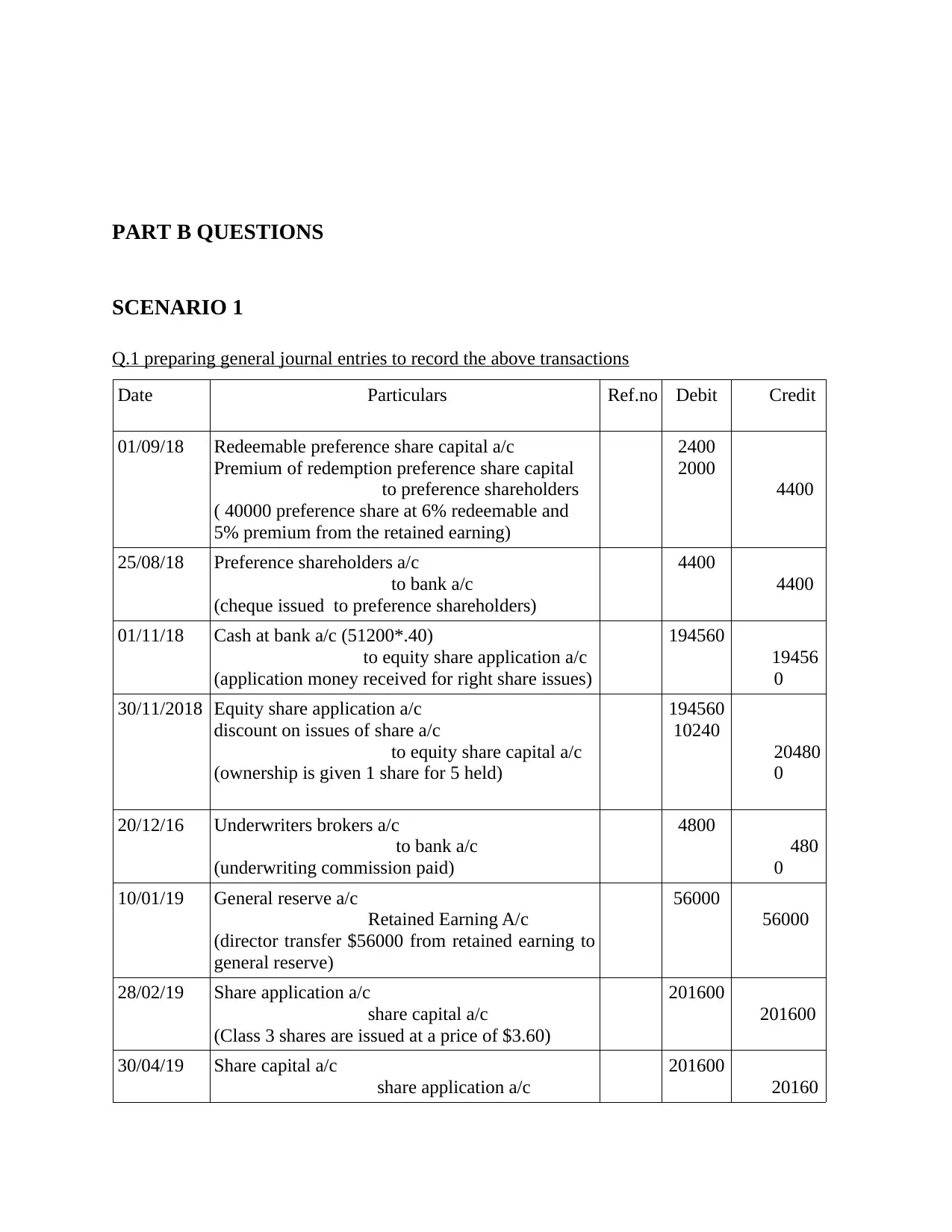

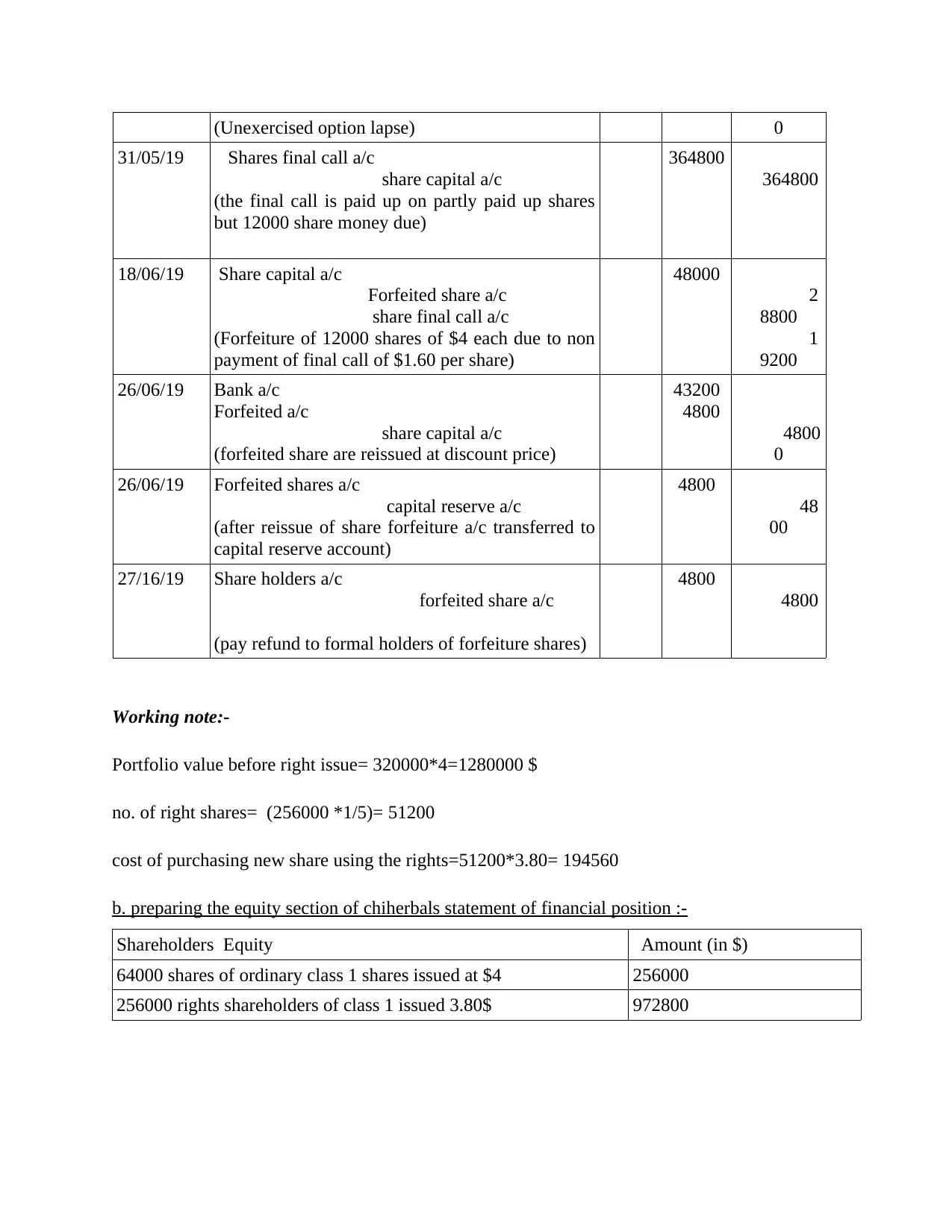

The assignment provides four accounting scenarios for students to practice their skills. Scenario 1 involves preparing journal entries and revaluing a truck asset. Scenario 2 covers leasing a motor vehicle, with journal entries for both the lessor and lessee. Scenario 3 includes disposing of a truck asset and calculating gain on disposal. Scenario 4 deals with research & development expenses, advertising costs, and sales. The assignment requires students to apply accounting principles, such as depreciation, amortization, and revaluation, to these scenarios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.