Bank Reconciliation and Suspense Account

VerifiedAdded on 2020/11/23

|8

|1393

|370

Project

AI Summary

This assignment explores the crucial aspects of bank reconciliation, focusing on identifying discrepancies between the cash book and bank statements. It delves into the process of rectifying errors through journal entries and highlights the significance of a suspense account in resolving unresolved items during reconciliation. The document emphasizes the importance of accurate financial reporting and the role of bank reconciliations in ensuring its integrity.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL ACCOUNTING

PROJECT 2

PROJECT 2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

PROJECT 2......................................................................................................................................1

(A): Comparison among direct debit as well as standing orders, banks cost and dishonour of

cheque.........................................................................................................................................1

P5: Preparation of bank reconciliation statements......................................................................3

P6: Rectification entries and suspense account...........................................................................4

(A): Journal entries......................................................................................................................4

(B): Suspense account ................................................................................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

PROJECT 2......................................................................................................................................1

(A): Comparison among direct debit as well as standing orders, banks cost and dishonour of

cheque.........................................................................................................................................1

P5: Preparation of bank reconciliation statements......................................................................3

P6: Rectification entries and suspense account...........................................................................4

(A): Journal entries......................................................................................................................4

(B): Suspense account ................................................................................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION

Finance is considered as the most vital function of the organisation which assists the

organisation in Functioning efficiently without any hindrances in the operations. This part of the

project performs an analysis and comparison of the banking functions such as Direct debit,

standing charges, bank charges and dishonour of cheque(Bank charges. 2018.). This part of

project also perform rectification of the errors made in the accounts and preparation of suspense

account for rectifying difference amount.

PROJECT 2

(A): Comparison among direct debit as well as standing orders, banks cost and dishonour of

cheque

Direct debit: Direct debit is considered as the type of the financial transaction, according

to which one individual draws the funds from some other person's bank account. This is kind of

pre authorised payment in which the account holder allows the bank to pay certain regular fixed

amount to the particular party (such as monthly rents and mortgage payments to the landlords

and banks) or some variable types of payments that are made on regular basis such as bills ,

invoices etc., supplier or utility company at the fixed time interval for the material they supply to

the organisation(Porter, and Norton, 2012). By using the process of direct debit, the individual

get all the power and right to collect payment from the related party.

Direct debit is considered as the most reliable and simple form for the purpose of making

regular payments such as bills, monthly mortgages and rents. Direct debit methods are generally

utilised for many purposes:

This function can be used for making many payments but it is generally utilised for these

purposes:

Regular Bills for variable amounts: With Utilising direct debit functions, the

companies and business can ensure that monthly bills and payments will be made on

timely basis without any delay and they do not have to worry for making the payments.

As per the data it has been seen that in 2011 almost 2.4 billion payments has been made

using direct debit function.

Paying on account: Many business provides the functions of direct debit as an

instrument for spreading the cost of the company and making payments on the account.

1

Finance is considered as the most vital function of the organisation which assists the

organisation in Functioning efficiently without any hindrances in the operations. This part of the

project performs an analysis and comparison of the banking functions such as Direct debit,

standing charges, bank charges and dishonour of cheque(Bank charges. 2018.). This part of

project also perform rectification of the errors made in the accounts and preparation of suspense

account for rectifying difference amount.

PROJECT 2

(A): Comparison among direct debit as well as standing orders, banks cost and dishonour of

cheque

Direct debit: Direct debit is considered as the type of the financial transaction, according

to which one individual draws the funds from some other person's bank account. This is kind of

pre authorised payment in which the account holder allows the bank to pay certain regular fixed

amount to the particular party (such as monthly rents and mortgage payments to the landlords

and banks) or some variable types of payments that are made on regular basis such as bills ,

invoices etc., supplier or utility company at the fixed time interval for the material they supply to

the organisation(Porter, and Norton, 2012). By using the process of direct debit, the individual

get all the power and right to collect payment from the related party.

Direct debit is considered as the most reliable and simple form for the purpose of making

regular payments such as bills, monthly mortgages and rents. Direct debit methods are generally

utilised for many purposes:

This function can be used for making many payments but it is generally utilised for these

purposes:

Regular Bills for variable amounts: With Utilising direct debit functions, the

companies and business can ensure that monthly bills and payments will be made on

timely basis without any delay and they do not have to worry for making the payments.

As per the data it has been seen that in 2011 almost 2.4 billion payments has been made

using direct debit function.

Paying on account: Many business provides the functions of direct debit as an

instrument for spreading the cost of the company and making payments on the account.

1

Standing Orders: The standing order is an form of automatic payments that are made

between the customers and the banks so that they can transfer payment to the third parties and

other companies. The standing order method is kind of similar to the direct debit method but the

only difference in this is that it is authorise by the customer and this method is generally adopted

by the companies(Otley, and Emmanuel, 2013).

Various differences between standing orders and direct debit order:

Standing orders Direct debit

There is no provider that is required for the set

up. The set up is being controlled by the

customers. The company is totally dependent

on customers. But this system will prove to be

unfeasible if the company have less then 25

customers.

Under this method, the provides is needed for

the set up and for the purpose of controlling

amounts and payments dates.

The cost which is incurred under this method is

apparently free or a very small charge is

charged from the customers for every payment.

The cost for the every payment here is very

low. Here, the customers is expected to pay

even less then 1% of the payment amount.

Bank charges:These charges are those that are levied by the commercial banks for the services

they provide to the customers(Linsmeier, 2011). These charges are generally related to the

transaction and account holders related to the current and savings account. The charges which

are imposed by these banks may include many forms such as:

the commercial banks charges fees regarding various transactions such as on overdraft

when the account holder withdraws amount across the limits.

Monthly charges that are levied by the banks on certain provisions related to the

accounts.

Dishonoured cheque:

These are referred to those cheques which are declined or returned by the banks when

there is lack of sufficient funds in the account of the person fro whom the cheque has to be paid.

If the account holder knowingly issues the cheque with the amount which is more then the

available balance in his account then, this is considered as an criminal offence.

2

between the customers and the banks so that they can transfer payment to the third parties and

other companies. The standing order method is kind of similar to the direct debit method but the

only difference in this is that it is authorise by the customer and this method is generally adopted

by the companies(Otley, and Emmanuel, 2013).

Various differences between standing orders and direct debit order:

Standing orders Direct debit

There is no provider that is required for the set

up. The set up is being controlled by the

customers. The company is totally dependent

on customers. But this system will prove to be

unfeasible if the company have less then 25

customers.

Under this method, the provides is needed for

the set up and for the purpose of controlling

amounts and payments dates.

The cost which is incurred under this method is

apparently free or a very small charge is

charged from the customers for every payment.

The cost for the every payment here is very

low. Here, the customers is expected to pay

even less then 1% of the payment amount.

Bank charges:These charges are those that are levied by the commercial banks for the services

they provide to the customers(Linsmeier, 2011). These charges are generally related to the

transaction and account holders related to the current and savings account. The charges which

are imposed by these banks may include many forms such as:

the commercial banks charges fees regarding various transactions such as on overdraft

when the account holder withdraws amount across the limits.

Monthly charges that are levied by the banks on certain provisions related to the

accounts.

Dishonoured cheque:

These are referred to those cheques which are declined or returned by the banks when

there is lack of sufficient funds in the account of the person fro whom the cheque has to be paid.

If the account holder knowingly issues the cheque with the amount which is more then the

available balance in his account then, this is considered as an criminal offence.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

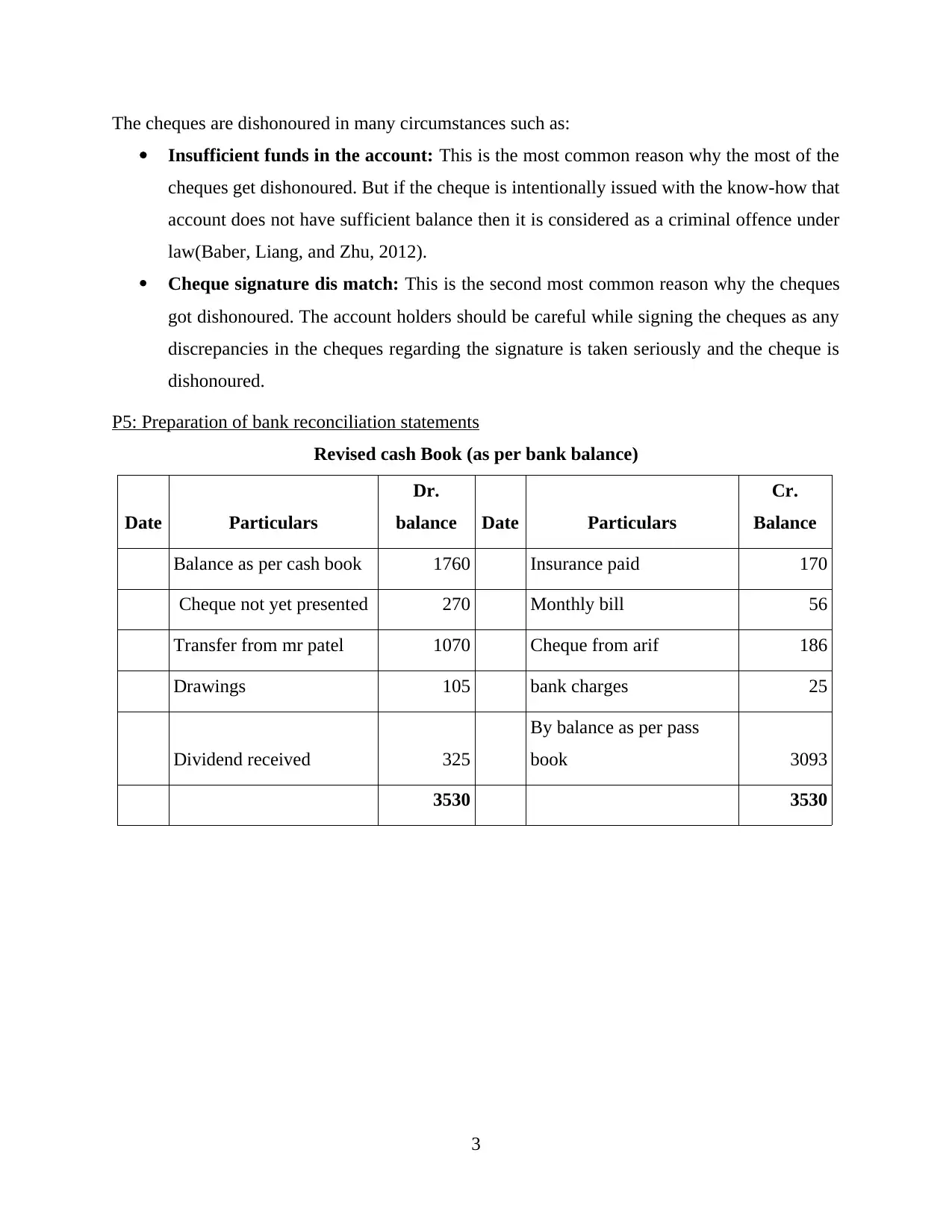

The cheques are dishonoured in many circumstances such as:

Insufficient funds in the account: This is the most common reason why the most of the

cheques get dishonoured. But if the cheque is intentionally issued with the know-how that

account does not have sufficient balance then it is considered as a criminal offence under

law(Baber, Liang, and Zhu, 2012).

Cheque signature dis match: This is the second most common reason why the cheques

got dishonoured. The account holders should be careful while signing the cheques as any

discrepancies in the cheques regarding the signature is taken seriously and the cheque is

dishonoured.

P5: Preparation of bank reconciliation statements

Revised cash Book (as per bank balance)

Date Particulars

Dr.

balance Date Particulars

Cr.

Balance

Balance as per cash book 1760 Insurance paid 170

Cheque not yet presented 270 Monthly bill 56

Transfer from mr patel 1070 Cheque from arif 186

Drawings 105 bank charges 25

Dividend received 325

By balance as per pass

book 3093

3530 3530

3

Insufficient funds in the account: This is the most common reason why the most of the

cheques get dishonoured. But if the cheque is intentionally issued with the know-how that

account does not have sufficient balance then it is considered as a criminal offence under

law(Baber, Liang, and Zhu, 2012).

Cheque signature dis match: This is the second most common reason why the cheques

got dishonoured. The account holders should be careful while signing the cheques as any

discrepancies in the cheques regarding the signature is taken seriously and the cheque is

dishonoured.

P5: Preparation of bank reconciliation statements

Revised cash Book (as per bank balance)

Date Particulars

Dr.

balance Date Particulars

Cr.

Balance

Balance as per cash book 1760 Insurance paid 170

Cheque not yet presented 270 Monthly bill 56

Transfer from mr patel 1070 Cheque from arif 186

Drawings 105 bank charges 25

Dividend received 325

By balance as per pass

book 3093

3530 3530

3

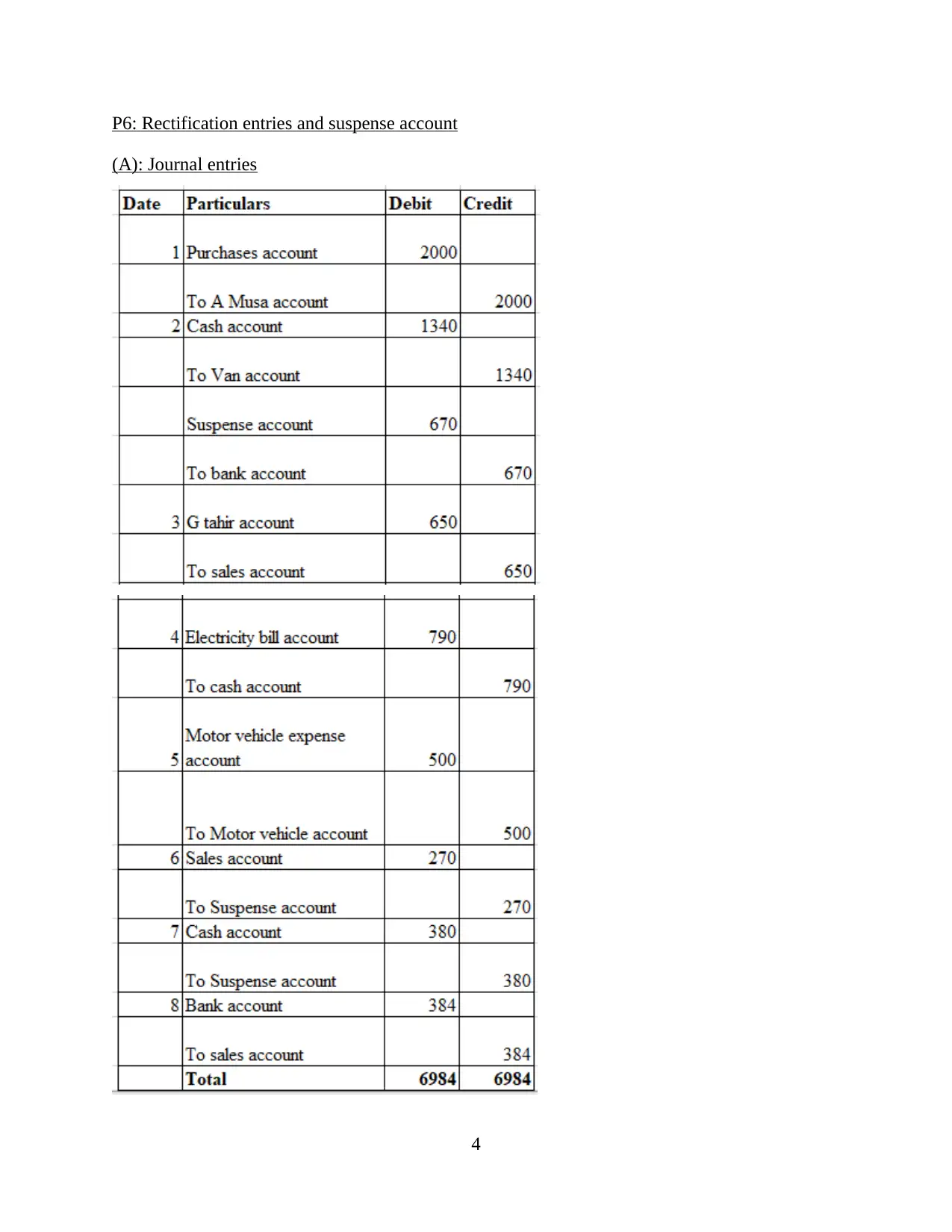

P6: Rectification entries and suspense account

(A): Journal entries

4

(A): Journal entries

4

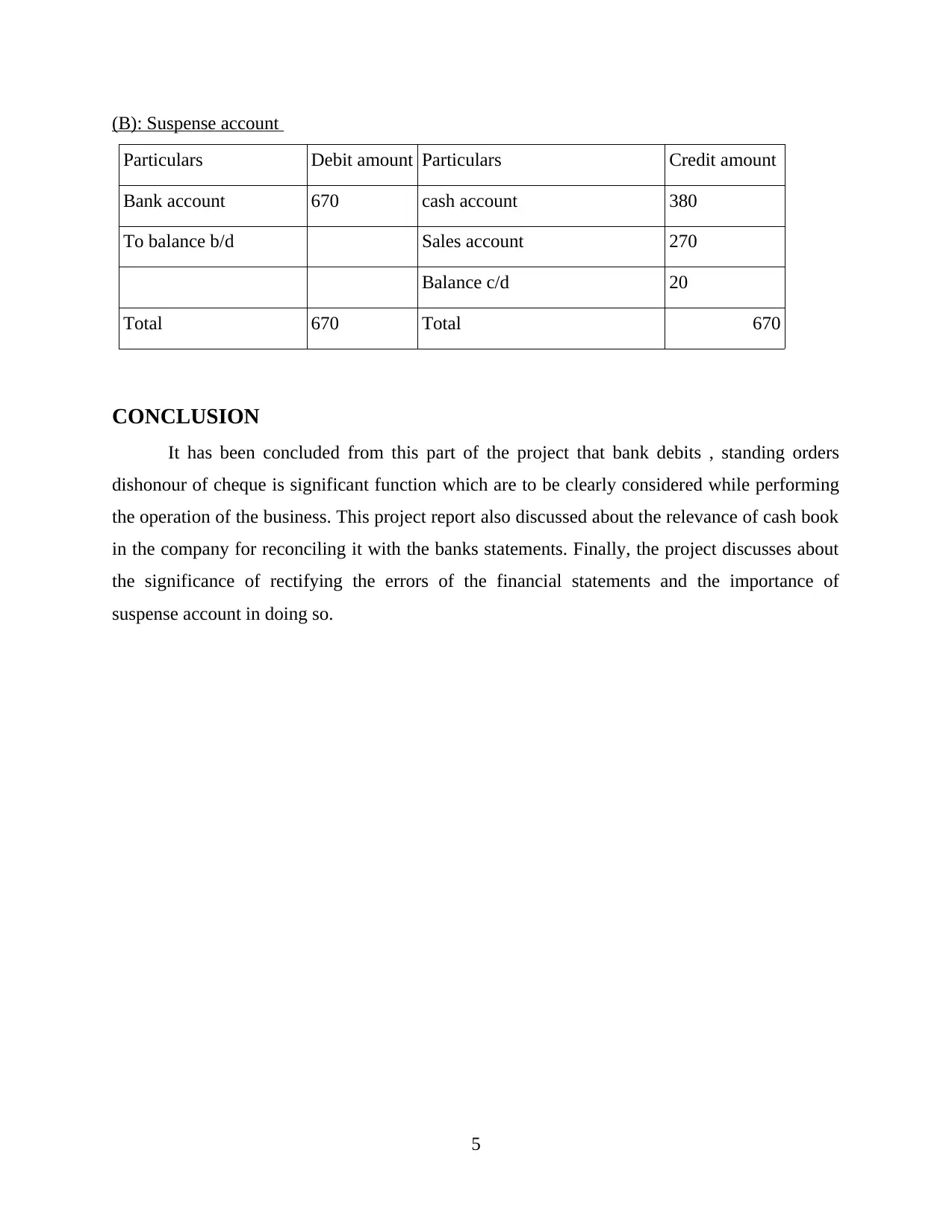

(B): Suspense account

Particulars Debit amount Particulars Credit amount

Bank account 670 cash account 380

To balance b/d Sales account 270

Balance c/d 20

Total 670 Total 670

CONCLUSION

It has been concluded from this part of the project that bank debits , standing orders

dishonour of cheque is significant function which are to be clearly considered while performing

the operation of the business. This project report also discussed about the relevance of cash book

in the company for reconciling it with the banks statements. Finally, the project discusses about

the significance of rectifying the errors of the financial statements and the importance of

suspense account in doing so.

5

Particulars Debit amount Particulars Credit amount

Bank account 670 cash account 380

To balance b/d Sales account 270

Balance c/d 20

Total 670 Total 670

CONCLUSION

It has been concluded from this part of the project that bank debits , standing orders

dishonour of cheque is significant function which are to be clearly considered while performing

the operation of the business. This project report also discussed about the relevance of cash book

in the company for reconciling it with the banks statements. Finally, the project discusses about

the significance of rectifying the errors of the financial statements and the importance of

suspense account in doing so.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals:

Baber, W. R. , Liang, L. and Zhu, Z. , 2012. Associations between internal and external corporate

governance characteristics: Implications for investigating financial accounting

restatements. Accounting Horizons. 26(2). pp.219-237.

Linsmeier, T. J. , 2011. Financial reporting and financial crises: The case for measuring financial

instruments at fair value in the financial statements. Accounting horizons. 25(2).

pp.409-417.

Otley, D. and Emmanuel, K. M. C. , 2013. Readings in accounting for management control.

Springer.

Porter, G. A. and Norton, C. L., 2012. Financial accounting: the impact on decision.

Online

Bank charges. 2018.[Online]. Available through: < http://www.accounting-basics-for-

students.com/accounting-reports.html>.

6

Books and journals:

Baber, W. R. , Liang, L. and Zhu, Z. , 2012. Associations between internal and external corporate

governance characteristics: Implications for investigating financial accounting

restatements. Accounting Horizons. 26(2). pp.219-237.

Linsmeier, T. J. , 2011. Financial reporting and financial crises: The case for measuring financial

instruments at fair value in the financial statements. Accounting horizons. 25(2).

pp.409-417.

Otley, D. and Emmanuel, K. M. C. , 2013. Readings in accounting for management control.

Springer.

Porter, G. A. and Norton, C. L., 2012. Financial accounting: the impact on decision.

Online

Bank charges. 2018.[Online]. Available through: < http://www.accounting-basics-for-

students.com/accounting-reports.html>.

6

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.