Ask a question from expert

Report on Accounting Conventions and Principles

34 Pages3968 Words114 Views

Added on 2020-06-06

Report on Accounting Conventions and Principles

Added on 2020-06-06

BookmarkShareRelated Documents

Financial Accounting

TABLE OF CONTENTSINTRODUCTION...........................................................................................................................41. Financial accounting................................................................................................................42. Regulations relating financial accounting...............................................................................53. Accounting rules and principles..............................................................................................54. The conventions and the concepts relating to consistency and material.................................6CLIENT 1........................................................................................................................................7a. Doing entries in the journal of Alex Study’s...........................................................................7b. Presenting ledger accounts in relation to the transactions of Alex..........................................8c. Preparation of trial balance....................................................................................................16CLIENT 2......................................................................................................................................17a. Preparing profitability statement............................................................................................17b. Statement of financial position..............................................................................................18CLIENT 3......................................................................................................................................19a. Preparing profitability statement of Raintree Ltd..................................................................19b. Drafting balance sheet of Raintree Ltd..................................................................................20c. Defining prudence and consistency concept of accounting...................................................20d. Evaluating depreciation methods...........................................................................................21CLIENT 4......................................................................................................................................22a. Explaining the purpose of preparing bank reconciliation statement in the context of KendalLtd..............................................................................................................................................22b. Listing and explaining causes due to which cash records vary from bank accounts.............23c..................................................................................................................................................231. Preparing a bank reconciliation statement.............................................................................232. Drafting updated cash book of Kendal Ltd for December 2017..........................................233. Presenting bank reconciliation statement as at 31st December 2017....................................24

CLIENT 5......................................................................................................................................25a..................................................................................................................................................251. Sales ledger control account..................................................................................................252. Purchase ledger control account............................................................................................26b. Describing control account....................................................................................................26CLIENT 6......................................................................................................................................26a. Describing suspense account and its main features...............................................................26b. Drafting trial balance by using control account as a balancing figure..................................27c. Preparing Journal entries for showing necessary corrections and clearing suspense account...................................................................................................................................................28d. Differentiating clearing and suspense account......................................................................29CONCLUSION..............................................................................................................................29REFERENCES..............................................................................................................................30

INTRODUCTIONFinancial accounting field of finance lays high level of emphasis on preparing andpresenting annual reports at the end of accounting year. With the motive to assess businessperformance and providing stakeholders with suitable information for decision makingcompanies undertake financial accounting practices. The present report is based on different casescenario which in turn provides deeper insight about accounting conventions and principles.Besides this, report will shed light on the manner in which journal, edger and trial balance helpsin preparing financial statements. Further, it also depicts how bank reconciliation statement helpsin matching records of cash and pass book. In this, concept related to depreciation, suspense andcontrol account will also be described. 1. Financial accountingIt is a specialise branch of accounting it keeps the company financial records by usingstandardised guidelines. All the transactions are recorded, summarized and presented in afinancial statement. Financial accounting represent only just one sector and it provide financialinformation to the company. The financial statements consider as external because it is given tothe shareholders, and primary recipients they outsider of the company. Financial accountingmain purpose is to provide enough information which is related to financial statements. Financialaccounting is governed by local and international accounting standards. Financial accounting isnot limited to recording, classifying and summarizing the information which is related tobusiness transactions (Jannard, 2017). This accounting generates three financial statementswhich gives the required information these are balance sheet, income statements and cash flowstatements. For investors, they look the business history for taking a decision to investing in acompany. So the financial accounting should be relevant, reliable, comparable and it should beconsistent. Accounting information to be useful for the user for decision making purpose so itmust be relevant. End users need most recent data to make a decision in favour. If the companydoes not produce reliable financial data , so the investor are unable to gain accurate data. Thefinancial statement must be comparable, if the data should be comparable the investors are ableto make judgement (Schroeder, Clark and Cathey, 2016). Financial accounting is very useful fora company report so its easy to understand and comparable and credible.

2. Regulations relating financial accountingThe international accounting standard board (IASB) stated that the main objective offinancial accounting is to give or provide the financial information to their existing andpotential investors and other creditors in making decision regarding to investment in thecompany. Financial accounting is the process of identifying , measuring and to communicating .International financial reporting standards (IFRS) it is issued bye IASB and it becomes morewidely spread . In regulatory frame work for the preparation of financial statement is necessarythere are some reasons, these are: the needs of the users of financial statements are meet withbasic needed information (Macve, 2015). All the information which is provided to outsider isrelevant and comparable which in turn helps in increasing users confidence as well as regulatingthe behaviour of the company. Financial statements allow the organisation to communicate theinformation about their performance. Financial reports provide summarized information aboutorganisation transactions for external investors. The Companies Act 2006 is the main frame which the companies and accountant have tofollow. Accounting standards are authoritative statements detailing how particular type oftransaction should be recorded in financial statements and accordingly with accounting standardswill normally give the necessary or fair view of the report. The main and initial purpose ofcreating accounting standards was to define proper accounting practice with in a legal frameworkin this guideline give by accounting standard.3. Accounting rules and principlesA number of accounting principles have been developed for usages these are:Accrual principle: this is the concept of accounting that should be recorded in the accountingperiods when the actually occur. This is important for the construction of financial statementsthat show the actually happened in accounting period.Consistency principle: This concept stated that once a company can adopt an accountingprinciple every time they should use this concept. If they not to follow the principle thatmeans the business continuously jump between the different accounting treatments.Cost principle: in this concept business should only records its assets , liabilities andequity at original purchase cost . This concept is less valid.Economic entity principles: This is the concepts in which the transaction of a businessshould keep separately . The accountants keeps all the business transactions of a sole

proprietorship. For legal purpose sole proprietorship and its owner consider to be oneentity.Full disclosure principle: in this concept financial statements of a business all theinformation Jan impact on reader understanding of those financial investments.Going concern principle: this concept is used by the business that would be justified indeferring the recognition of some expenses like depreciation.Matching principle: in this concept when the company record revenue then they recordall the related expenses at the time (Basic accounting principles, 2018).Materiality principle: in this concept record all the transaction which is not doing so it Janchange the decision making process .This is the quite difficult concept.Monetary unit principle: in this concept that a business should only record thosetransaction which is done in unit of currency.Reliability concept: In this concept only those transaction should be recorded which isproven or have an evidence.Revenue recognition Principle: in this concept it only recognize revenue when businesscompleted the earning process (Robson, Young and Power, 2017).Time period principle: in this concept a business should report the results of its operation.It should be create a standard to set comparable periods.4. The conventions and the concepts relating to consistency and materialThe convention concept states that it requires transactions to be recorded at the price , and at timeand for assets to be valued at the original cost. If there is a possibility of loss so the account takeninto earliest. Consistency is the transactions and valuation of methods that are treated year to yearsimilarly. The person who will evaluate the financial statements so it makes more meaningfulcomparison of financial performance, in this all the practices should be unchanged from oneperiod to another (Narayanaswamy, 2017). Consistency doesn't mean inflexibility some timeinternal policies should be changed. If changes become necessary the change and its effectshould be clear. Materiality is an important convention, in this all the transaction should be recorded instatements is appropriate and materialistic and it is useful for auditors. In this only those eventsor items recorded which is significant for financial statements and insignificant things should be

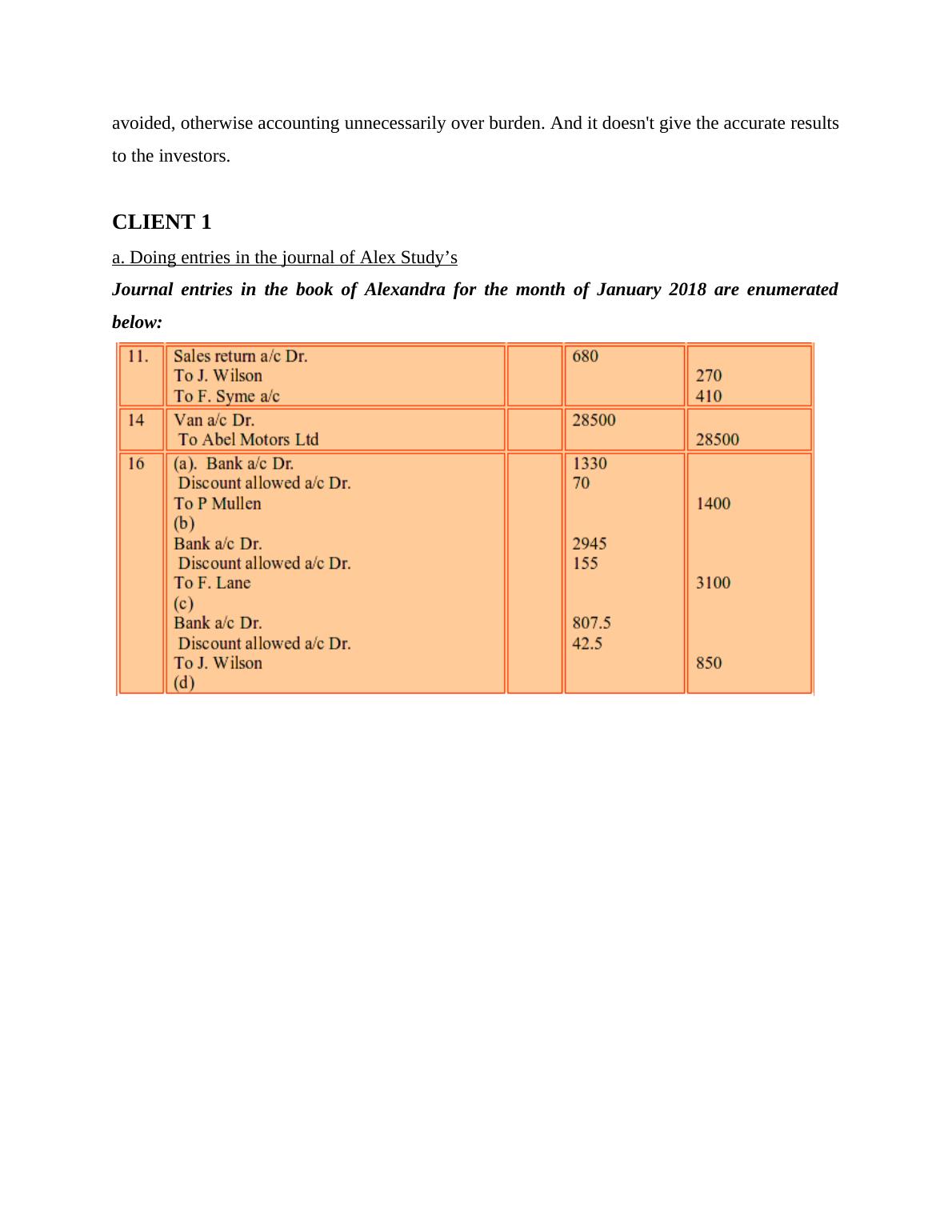

avoided, otherwise accounting unnecessarily over burden. And it doesn't give the accurate resultsto the investors.CLIENT 1a. Doing entries in the journal of Alex Study’sJournal entries in the book of Alexandra for the month of January 2018 are enumeratedbelow:

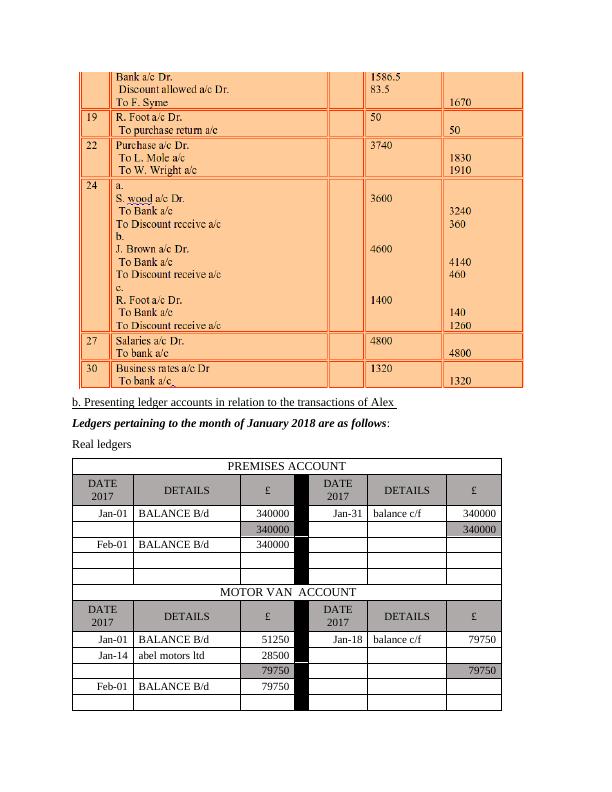

b. Presenting ledger accounts in relation to the transactions of Alex Ledgers pertaining to the month of January 2018 are as follows: Real ledgers PREMISES ACCOUNTDATE2017DETAILS£DATE2017DETAILS£Jan-01BALANCE B/d340000Jan-31balance c/f340000340000340000Feb-01BALANCE B/d340000 MOTOR VAN ACCOUNTDATE2017DETAILS£DATE2017DETAILS£Jan-01BALANCE B/d51250Jan-18balance c/f79750Jan-14abel motors ltd285007975079750Feb-01BALANCE B/d79750

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Accounting Principles Assignment Solvedlg...

|37

|6580

|173

Financial Accounting: Assignment Samplelg...

|37

|5577

|390

Accounting Principles Assignment | Financial Accounting Assignmentlg...

|32

|4628

|54

Financial accounting Field PDFlg...

|32

|3855

|370

FINANCIAL ACCOUNTING PRINCIPLES TABLE OF CONTENTSlg...

|31

|4286

|270

TABLE OF CONTENTS INTRODUCTION 4 (1) Regulations relating to financial accountinglg...

|38

|3927

|437