Financial Accounting Report: FCT Group Financial Analysis and Policies

VerifiedAdded on 2020/01/07

|10

|2610

|232

Report

AI Summary

This financial accounting report provides a comprehensive analysis of the Flight Centre Travel Group (FCT). It begins with an introduction to financial accounting and the company's operations, followed by an examination of accounting policies related to property, plant, and equipment, including depreciation methods and impairment losses, referencing AASB116 and AASB 136. The report then explores intangible assets, categorizing them and discussing amortization and impairment policies. It also covers accounting treatments for provisions, specifically long service leaves and unrecognised dividends, in accordance with accounting standards. Furthermore, it delves into contingent assets and liabilities, detailing their disclosure requirements in financial statements as per IAS 37. The report concludes with an analysis of financial ratios, including current ratio, rate of return on total assets, times interest earned, debt-equity ratio, and price-earning ratio, providing insights into the company's financial position and performance.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

FINANCIAL ACCOUNTING.........................................................................................................1

Q.1.INTRODUCTION....................................................................................................................3

Accounting policies that relates to property, plant and equipment of FCT Group .....................3

Disclosure Requirements of AASB116 and AASB 136..............................................................3

CONCLUSION................................................................................................................................4

Categories of intangible assets of FLT group..............................................................................4

CONCLUSION................................................................................................................................5

Q.3. INTRODUCTION...................................................................................................................5

Accounting treatment of provisions and policies in respect to long service leaves.....................5

Accounting treatment of unrecognised dividend ........................................................................6

CONCLUSION................................................................................................................................6

Q.4. INTRODUCTION...................................................................................................................6

Contingent assets and liabilities and their disclosure in financial statements.............................6

Q.5 INTRODUCTION....................................................................................................................7

Analysis of the financial ratios....................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

FINANCIAL ACCOUNTING.........................................................................................................1

Q.1.INTRODUCTION....................................................................................................................3

Accounting policies that relates to property, plant and equipment of FCT Group .....................3

Disclosure Requirements of AASB116 and AASB 136..............................................................3

CONCLUSION................................................................................................................................4

Categories of intangible assets of FLT group..............................................................................4

CONCLUSION................................................................................................................................5

Q.3. INTRODUCTION...................................................................................................................5

Accounting treatment of provisions and policies in respect to long service leaves.....................5

Accounting treatment of unrecognised dividend ........................................................................6

CONCLUSION................................................................................................................................6

Q.4. INTRODUCTION...................................................................................................................6

Contingent assets and liabilities and their disclosure in financial statements.............................6

Q.5 INTRODUCTION....................................................................................................................7

Analysis of the financial ratios....................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

Q.1.INTRODUCTION

Financial Accounting can be defined as a branch of accounting which deals with the

financial transactions of the company as well as records, summarizes and presents the financial

statements. Flight centre travel group is the world's top-most and profitable travel retailer

personally delivering amazing experiences to people, partners, and satisfying their customers to

a great extent. This report deals with the financial policies that the company is adopting and

various accounting standards.

Accounting policies that relates to property, plant and equipment of FCT Group

As per the Annual report of FCT Group, company is following the guidelines provided

by the Australian Accounting Standard Board. Financial statements are prepared as per the

Australian Accounting standards which show true and fair view. These accounting standards

needs to be followed by the company in order to set the disclosure of financial transactions.

Flight centre travel group is charging depreciation on assets as per the policies given by the

Accounting standards of Australia (Acharya, V.V.,and et.al., 2013)Company is charging

depreciation by following Straight line method so as to reduce the carrying amount of an asset

over its useful life. Property, plants and equipment are disclosed at historical cost less

depreciation. The useful life of property, plants and equipment are analyzed and checked at the

end of each financial year (Al-Najjar, B. and Hussainey, K., 2011)

According to the financial statement of FLT, it can be seen that book amount of building

at the end of financial year 2016 is declined in comparison to 2015. This is due to the gain

realized in the year 2016 on sale of New Zealand head office building. There was no disposal of

property in 2015 which results in higher book value. But if analyzing the accounting policies

followed by FLT group, there is an increase in net book amount of plant and equipment in 2016

as compared to 2015 by $31111 which is due to the impairment of the plant and equipment in

USA segment. Impairment loss is identified and assessed by the firm when the asset's carrying

cost exceeds its recoverable amount. FLT recognizes its impairment loss in profit and loss

statement.

Disclosure Requirements of AASB116 and AASB 136

FLT group has prepared its financial report as per the Australian Accounting Standards

which helps the company to present true and fair view to their customers, competitors etc. In the

Financial Accounting can be defined as a branch of accounting which deals with the

financial transactions of the company as well as records, summarizes and presents the financial

statements. Flight centre travel group is the world's top-most and profitable travel retailer

personally delivering amazing experiences to people, partners, and satisfying their customers to

a great extent. This report deals with the financial policies that the company is adopting and

various accounting standards.

Accounting policies that relates to property, plant and equipment of FCT Group

As per the Annual report of FCT Group, company is following the guidelines provided

by the Australian Accounting Standard Board. Financial statements are prepared as per the

Australian Accounting standards which show true and fair view. These accounting standards

needs to be followed by the company in order to set the disclosure of financial transactions.

Flight centre travel group is charging depreciation on assets as per the policies given by the

Accounting standards of Australia (Acharya, V.V.,and et.al., 2013)Company is charging

depreciation by following Straight line method so as to reduce the carrying amount of an asset

over its useful life. Property, plants and equipment are disclosed at historical cost less

depreciation. The useful life of property, plants and equipment are analyzed and checked at the

end of each financial year (Al-Najjar, B. and Hussainey, K., 2011)

According to the financial statement of FLT, it can be seen that book amount of building

at the end of financial year 2016 is declined in comparison to 2015. This is due to the gain

realized in the year 2016 on sale of New Zealand head office building. There was no disposal of

property in 2015 which results in higher book value. But if analyzing the accounting policies

followed by FLT group, there is an increase in net book amount of plant and equipment in 2016

as compared to 2015 by $31111 which is due to the impairment of the plant and equipment in

USA segment. Impairment loss is identified and assessed by the firm when the asset's carrying

cost exceeds its recoverable amount. FLT recognizes its impairment loss in profit and loss

statement.

Disclosure Requirements of AASB116 and AASB 136

FLT group has prepared its financial report as per the Australian Accounting Standards

which helps the company to present true and fair view to their customers, competitors etc. In the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

context of property, plant and equipment company has referred AASB116 which deals with the

accounting treatment of the assets so as to help the customers to infer information regarding the

depreciation charged on asset, recognition on sale of any asset, impairment losses etc (Cassell,

C.A., and et.al., 2012.)

AASB 136 deals specifically with the impairment of assets and this accounting standard

helps to ensure that no asset should be carried more than its recoverable amount but is its more

than recoverable amount then impairment loss must be recognized and the related disclosures.

CONCLUSION

FLT has followed all the accounting standards prescribed by AASB that is they have

stated their assets at historical cost less depreciation. Impairment loss has also been recognized

by the company which shows that their financial statements show true facts and figures regarding

property, plant and equipment.

Q.2. INTRODUCTION

An intangible asset can be defined as a non-physical asset and which are also considered

as non-monetary asset having a life greater than one year. FLT considers many intangible assets

and they are not subject to amortisation but they can be impaired therefore, impairment losses

must be recognized in the financial statements regarding goodwill and other intangible assets.

Categories of intangible assets of FLT group

Other than goodwill, FLT has also considered brand names and customer relationships

and other intangible assets which are related to software and these intangible assets are amortised

over their expected useful life. As the brand names have indefinite life , therefore company owns

these brands and use them on a continuous basis.

Net book amount of goodwill increases at the end of 2016 as no impairment loss is

considered in goodwill therefore, its value increases because of the acquistions inspite of some

portion is transferred to reserves. But in the case of brand names and other intangible assets,

impairment loss is recognized. In the financial year 2016, various brand names as well as other

intangible assets have been acquired by the company which results in increment in the net book

value of assets. FLT had not charged any impairment losses in the prior years. Impairment

charges of indefinite life intangibles are recognised in profit and loss statements other than

goodwill.

accounting treatment of the assets so as to help the customers to infer information regarding the

depreciation charged on asset, recognition on sale of any asset, impairment losses etc (Cassell,

C.A., and et.al., 2012.)

AASB 136 deals specifically with the impairment of assets and this accounting standard

helps to ensure that no asset should be carried more than its recoverable amount but is its more

than recoverable amount then impairment loss must be recognized and the related disclosures.

CONCLUSION

FLT has followed all the accounting standards prescribed by AASB that is they have

stated their assets at historical cost less depreciation. Impairment loss has also been recognized

by the company which shows that their financial statements show true facts and figures regarding

property, plant and equipment.

Q.2. INTRODUCTION

An intangible asset can be defined as a non-physical asset and which are also considered

as non-monetary asset having a life greater than one year. FLT considers many intangible assets

and they are not subject to amortisation but they can be impaired therefore, impairment losses

must be recognized in the financial statements regarding goodwill and other intangible assets.

Categories of intangible assets of FLT group

Other than goodwill, FLT has also considered brand names and customer relationships

and other intangible assets which are related to software and these intangible assets are amortised

over their expected useful life. As the brand names have indefinite life , therefore company owns

these brands and use them on a continuous basis.

Net book amount of goodwill increases at the end of 2016 as no impairment loss is

considered in goodwill therefore, its value increases because of the acquistions inspite of some

portion is transferred to reserves. But in the case of brand names and other intangible assets,

impairment loss is recognized. In the financial year 2016, various brand names as well as other

intangible assets have been acquired by the company which results in increment in the net book

value of assets. FLT had not charged any impairment losses in the prior years. Impairment

charges of indefinite life intangibles are recognised in profit and loss statements other than

goodwill.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Their useful lives are estimated according to the class or group of intangible assets.

Goodwill and other intangible assets have an indefinite useful life but customer relationships are

amortized over their expected useful life but their expected useful life must not exceed seven

years. And the useful life of other intangible assets should not exceed 2.5-5 years.

Company is also considering impairment charges of intangible assets. An impairment

loss is recognised when an asset's carrying amount exceeds its recoverable value. This loss is

recognized in profit and loss statement. Other than goodwill, impairment loss must be reviwed

for reversal at the end of each financial period.

CONCLUSION

FLT group has amortised various intangible assets like goodwill, brand names and

customer relationships etc. They have followed different policies regarding impairment of

intangible assets.

Q.3. INTRODUCTION

As per Accounting standards, provision can be defined as an amount set aside from the

company's profits for an expected liability to be arised in future. Company specifies in its report

an accounting treatment of provisions in the financial statements.

Accounting treatment of provisions and policies in respect to long service leaves

Provision is an amount set aside from the profits of the company therefore, it becomes the

liability of the company. Provisions appear in the liabilities side of the balance sheet under the

head current liabilities.

As per accounting standards, company has followed accounting policies in respect of

long service leaves(LSL). Long service leaves can be defined as the leaves which are given to an

employee after working for a long period of time. As per the annual report of FLT Group,

employees who have completed the required service period are entitled for long service leaves

with an entitlement of pro-rata payments within next 12 months after the end of financial year.

LSL obligations which are expected to be settled within next 12 months is increased in 2016

which means that amounts are not settled within the given period of time. It is stated in an annual

report of FLT group in notes to financial statements F7 (Covas, F. and Den Haan, W.J.,

Goodwill and other intangible assets have an indefinite useful life but customer relationships are

amortized over their expected useful life but their expected useful life must not exceed seven

years. And the useful life of other intangible assets should not exceed 2.5-5 years.

Company is also considering impairment charges of intangible assets. An impairment

loss is recognised when an asset's carrying amount exceeds its recoverable value. This loss is

recognized in profit and loss statement. Other than goodwill, impairment loss must be reviwed

for reversal at the end of each financial period.

CONCLUSION

FLT group has amortised various intangible assets like goodwill, brand names and

customer relationships etc. They have followed different policies regarding impairment of

intangible assets.

Q.3. INTRODUCTION

As per Accounting standards, provision can be defined as an amount set aside from the

company's profits for an expected liability to be arised in future. Company specifies in its report

an accounting treatment of provisions in the financial statements.

Accounting treatment of provisions and policies in respect to long service leaves

Provision is an amount set aside from the profits of the company therefore, it becomes the

liability of the company. Provisions appear in the liabilities side of the balance sheet under the

head current liabilities.

As per accounting standards, company has followed accounting policies in respect of

long service leaves(LSL). Long service leaves can be defined as the leaves which are given to an

employee after working for a long period of time. As per the annual report of FLT Group,

employees who have completed the required service period are entitled for long service leaves

with an entitlement of pro-rata payments within next 12 months after the end of financial year.

LSL obligations which are expected to be settled within next 12 months is increased in 2016

which means that amounts are not settled within the given period of time. It is stated in an annual

report of FLT group in notes to financial statements F7 (Covas, F. and Den Haan, W.J.,

2012.)Value of long service leave obligation which appears in the balance sheet in the year 2015

was $21475 and in the year 2016 is $25634.

Accounting treatment of unrecognised dividend

Unrecognized dividends are considered as dividends which have been declared by the

company after the balance sheet date but they are not recognized. This unrecognized dividend

will come under the head of provisions as it will be considered as an obligation of the company

to pay in future to the shareholders. According to the IAS 10 “Events occuring after the balance

sheet date”, it will be considered as a liability for the FLT group (Taani, K. and Banykhaled,

M.H.H., 2011.)

CONCLUSION

As per the above assessment of Long service leaves and unrecognized dividends,

company has followed proper accounting policies and procedures to expand their productivity

and gives customers an accurate feedback about the company.

Q.4. INTRODUCTION

This section deals with contingent liabilities of the company and about the disclosure

requirements needs to be presented by the company in their financial statements. It also presents

about the contingent assets and their disclosure requirements.

Contingent assets and liabilities and their disclosure in financial statements

IAS 37 deals with the provisions, contingents assets and contingent liabilities. As per IAS

37, contingent liabilities can be defined as a present obligation for the company which depends

on some uncertain future events. It is required by the companies to disclose contingent liabilities

in financial statements even if they are not recognized by the company. They are to be disclosed

in financial statements as a footnote and not really shown in balance sheet as they are not

estimated by the company (Ahmed Sheikh, N. and Wang, Z., 2011)

Company is having its contingent liabilities regarding the rental expenses as it becomes

the present obligation for FLT group. FLT has also having contingent consideration regarding a

law test case against ACCC who further appealed to the high court for which the judgement was

anticipated at the end of the year 2016. therefore, this liability is regarded as contingent liability.

was $21475 and in the year 2016 is $25634.

Accounting treatment of unrecognised dividend

Unrecognized dividends are considered as dividends which have been declared by the

company after the balance sheet date but they are not recognized. This unrecognized dividend

will come under the head of provisions as it will be considered as an obligation of the company

to pay in future to the shareholders. According to the IAS 10 “Events occuring after the balance

sheet date”, it will be considered as a liability for the FLT group (Taani, K. and Banykhaled,

M.H.H., 2011.)

CONCLUSION

As per the above assessment of Long service leaves and unrecognized dividends,

company has followed proper accounting policies and procedures to expand their productivity

and gives customers an accurate feedback about the company.

Q.4. INTRODUCTION

This section deals with contingent liabilities of the company and about the disclosure

requirements needs to be presented by the company in their financial statements. It also presents

about the contingent assets and their disclosure requirements.

Contingent assets and liabilities and their disclosure in financial statements

IAS 37 deals with the provisions, contingents assets and contingent liabilities. As per IAS

37, contingent liabilities can be defined as a present obligation for the company which depends

on some uncertain future events. It is required by the companies to disclose contingent liabilities

in financial statements even if they are not recognized by the company. They are to be disclosed

in financial statements as a footnote and not really shown in balance sheet as they are not

estimated by the company (Ahmed Sheikh, N. and Wang, Z., 2011)

Company is having its contingent liabilities regarding the rental expenses as it becomes

the present obligation for FLT group. FLT has also having contingent consideration regarding a

law test case against ACCC who further appealed to the high court for which the judgement was

anticipated at the end of the year 2016. therefore, this liability is regarded as contingent liability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

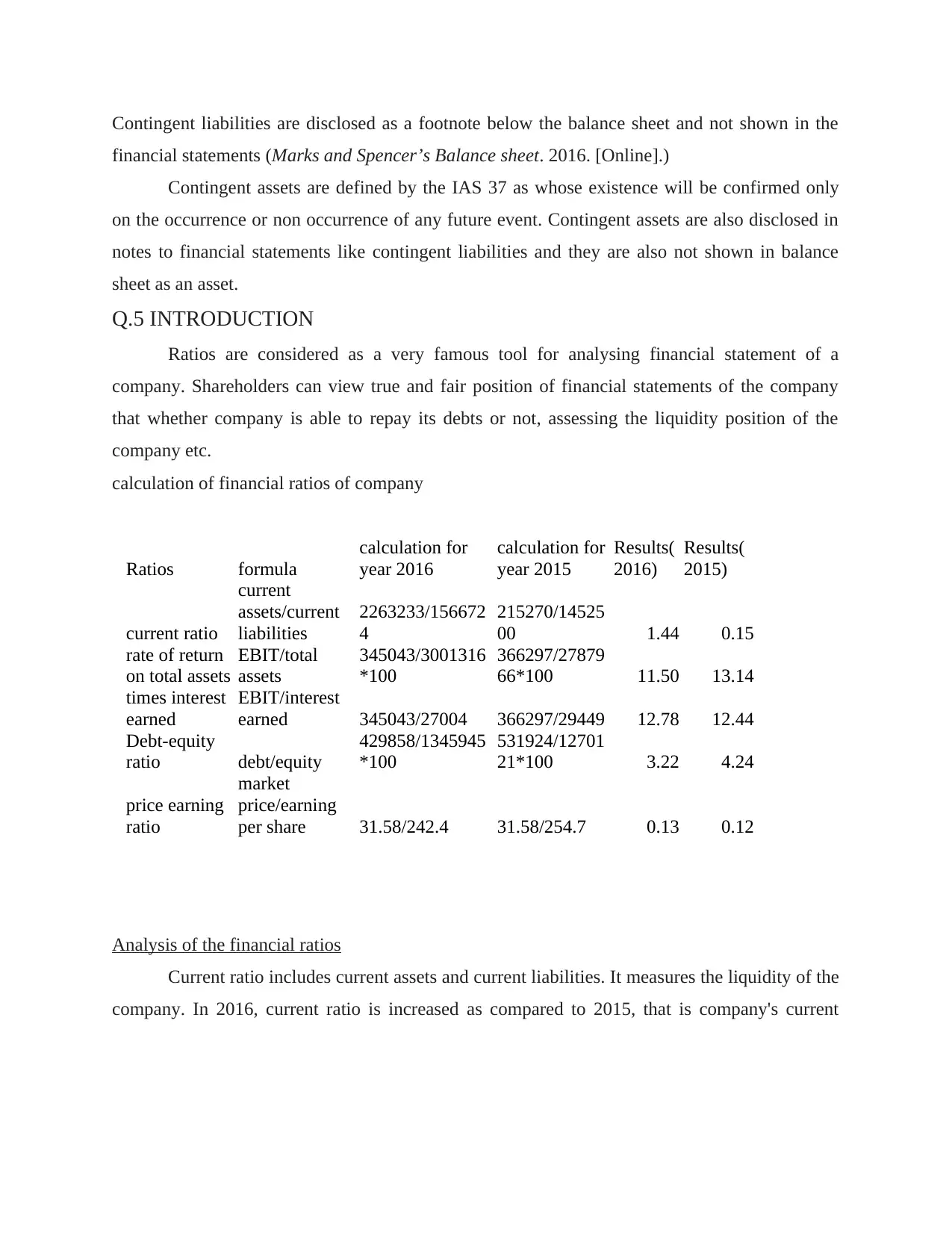

Contingent liabilities are disclosed as a footnote below the balance sheet and not shown in the

financial statements (Marks and Spencer’s Balance sheet. 2016. [Online].)

Contingent assets are defined by the IAS 37 as whose existence will be confirmed only

on the occurrence or non occurrence of any future event. Contingent assets are also disclosed in

notes to financial statements like contingent liabilities and they are also not shown in balance

sheet as an asset.

Q.5 INTRODUCTION

Ratios are considered as a very famous tool for analysing financial statement of a

company. Shareholders can view true and fair position of financial statements of the company

that whether company is able to repay its debts or not, assessing the liquidity position of the

company etc.

calculation of financial ratios of company

Ratios formula

calculation for

year 2016

calculation for

year 2015

Results(

2016)

Results(

2015)

current ratio

current

assets/current

liabilities

2263233/156672

4

215270/14525

00 1.44 0.15

rate of return

on total assets

EBIT/total

assets

345043/3001316

*100

366297/27879

66*100 11.50 13.14

times interest

earned

EBIT/interest

earned 345043/27004 366297/29449 12.78 12.44

Debt-equity

ratio debt/equity

429858/1345945

*100

531924/12701

21*100 3.22 4.24

price earning

ratio

market

price/earning

per share 31.58/242.4 31.58/254.7 0.13 0.12

Analysis of the financial ratios

Current ratio includes current assets and current liabilities. It measures the liquidity of the

company. In 2016, current ratio is increased as compared to 2015, that is company's current

financial statements (Marks and Spencer’s Balance sheet. 2016. [Online].)

Contingent assets are defined by the IAS 37 as whose existence will be confirmed only

on the occurrence or non occurrence of any future event. Contingent assets are also disclosed in

notes to financial statements like contingent liabilities and they are also not shown in balance

sheet as an asset.

Q.5 INTRODUCTION

Ratios are considered as a very famous tool for analysing financial statement of a

company. Shareholders can view true and fair position of financial statements of the company

that whether company is able to repay its debts or not, assessing the liquidity position of the

company etc.

calculation of financial ratios of company

Ratios formula

calculation for

year 2016

calculation for

year 2015

Results(

2016)

Results(

2015)

current ratio

current

assets/current

liabilities

2263233/156672

4

215270/14525

00 1.44 0.15

rate of return

on total assets

EBIT/total

assets

345043/3001316

*100

366297/27879

66*100 11.50 13.14

times interest

earned

EBIT/interest

earned 345043/27004 366297/29449 12.78 12.44

Debt-equity

ratio debt/equity

429858/1345945

*100

531924/12701

21*100 3.22 4.24

price earning

ratio

market

price/earning

per share 31.58/242.4 31.58/254.7 0.13 0.12

Analysis of the financial ratios

Current ratio includes current assets and current liabilities. It measures the liquidity of the

company. In 2016, current ratio is increased as compared to 2015, that is company's current

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

assets are 1.44 times more than current liabilities which shows the company's better financial

position (Industrial benchmark ratios for UK Retail Industry. 2016.)

Rate of return on total assets indicated that how effectively a company is using its assets.

Company's capacity of using its total assets in 2016 in comparison to 2015 is decreased by

approximately 2%.

Interest is earned on operating profit is higher in both the periods which shows the better

financial position of the organization.

Debt-equity ratio is used by the company to see that how much debt a company is using

to finance its assets. High debt equity ratio indicated that company is undertaking high debt and

thus has high risk. Here, FLT is not undertaking high risk as they have lower debt-equity ratio.

Price earning ratio indicates that how much an investor can expect to invest in a company

in order to receive company's earnings. Companies with higher P/E ratio are expect to grow in

future as compared to the lower P/E ratio.

CONCLUSION

As per the annual reports of the company, company's financial position is sound and it is

able to repay its debts. Ratios indicates the performance of the company and its growth which

helps the investors to decide whether to invest or not.

position (Industrial benchmark ratios for UK Retail Industry. 2016.)

Rate of return on total assets indicated that how effectively a company is using its assets.

Company's capacity of using its total assets in 2016 in comparison to 2015 is decreased by

approximately 2%.

Interest is earned on operating profit is higher in both the periods which shows the better

financial position of the organization.

Debt-equity ratio is used by the company to see that how much debt a company is using

to finance its assets. High debt equity ratio indicated that company is undertaking high debt and

thus has high risk. Here, FLT is not undertaking high risk as they have lower debt-equity ratio.

Price earning ratio indicates that how much an investor can expect to invest in a company

in order to receive company's earnings. Companies with higher P/E ratio are expect to grow in

future as compared to the lower P/E ratio.

CONCLUSION

As per the annual reports of the company, company's financial position is sound and it is

able to repay its debts. Ratios indicates the performance of the company and its growth which

helps the investors to decide whether to invest or not.

REFERENCES

Books and journals

Acharya, V.V.,and et.al., 2013. Corporate governance and value creation: Evidence from private

equity. Review of Financial Studies, 26(2), pp.368-402.

Ahmed Sheikh, N. and Wang, Z., 2011. Determinants of capital structure: An empirical study of

firms in manufacturing industry of Pakistan. Managerial Finance. 37(2). pp.117-133.

Al-Najjar, B. and Hussainey, K., 2011. Revisiting the capital-structure puzzle: UK evidence. The

Journal of Risk Finance. 12(4). pp.329-338.

Cassell, C.A., and et.al., 2012. Seeking safety: The relation between CEO inside debt holdings

and the riskiness of firm investment and financial policies. Journal of Financial Economics.

103(3). pp.588-610.

Covas, F. and Den Haan, W.J., 2012. The role of debt and equity finance over the business cycle.

The Economic Journal. 122(565). pp.1262-1286.

Taani, K. and Banykhaled, M.H.H., 2011. The effect of financial ratios, firm size and cash flows

from operating activities on earnings per share:(an applied study: on Jordanian industrial

sector).International journal of social sciences and humanity studies. 3(1). pp.1309-8063.

Wei, C. and Yermack, D., 2011. Investor reactions to CEOs' inside debt incentives. Review of

Financial Studies. 24(11). pp.3813-3840.

Online

Basha, A. D., 2014. Capital structure theories. [Online]. Available through: <

https://www.slideshare.net/ShahidAfzalSyed/5-capital-structuretheories-32694984>.[Accessed

on 29th March 2017].

Books and journals

Acharya, V.V.,and et.al., 2013. Corporate governance and value creation: Evidence from private

equity. Review of Financial Studies, 26(2), pp.368-402.

Ahmed Sheikh, N. and Wang, Z., 2011. Determinants of capital structure: An empirical study of

firms in manufacturing industry of Pakistan. Managerial Finance. 37(2). pp.117-133.

Al-Najjar, B. and Hussainey, K., 2011. Revisiting the capital-structure puzzle: UK evidence. The

Journal of Risk Finance. 12(4). pp.329-338.

Cassell, C.A., and et.al., 2012. Seeking safety: The relation between CEO inside debt holdings

and the riskiness of firm investment and financial policies. Journal of Financial Economics.

103(3). pp.588-610.

Covas, F. and Den Haan, W.J., 2012. The role of debt and equity finance over the business cycle.

The Economic Journal. 122(565). pp.1262-1286.

Taani, K. and Banykhaled, M.H.H., 2011. The effect of financial ratios, firm size and cash flows

from operating activities on earnings per share:(an applied study: on Jordanian industrial

sector).International journal of social sciences and humanity studies. 3(1). pp.1309-8063.

Wei, C. and Yermack, D., 2011. Investor reactions to CEOs' inside debt incentives. Review of

Financial Studies. 24(11). pp.3813-3840.

Online

Basha, A. D., 2014. Capital structure theories. [Online]. Available through: <

https://www.slideshare.net/ShahidAfzalSyed/5-capital-structuretheories-32694984>.[Accessed

on 29th March 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Industrial benchmark ratios for UK Retail Industry. 2016. [Online]. Available through:

<http://csimarket.com/Industry/industry_Financial_Strength_Ratios.php?s=1300>.[Accessed on

29th March 2017].

Marks and Spencer’s Balance sheet. 2016. [Online]. Available through:

<http://financials.morningstar.com/balance-sheet/bs.html?t=MKS®ion=gbr&culture=en-

US>.[Accessed on 29th March 2017].

<http://csimarket.com/Industry/industry_Financial_Strength_Ratios.php?s=1300>.[Accessed on

29th March 2017].

Marks and Spencer’s Balance sheet. 2016. [Online]. Available through:

<http://financials.morningstar.com/balance-sheet/bs.html?t=MKS®ion=gbr&culture=en-

US>.[Accessed on 29th March 2017].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.