Financial Accounting and Regulatory Framework Exam Answers and Solutions

VerifiedAdded on 2023/06/11

|9

|2436

|443

AI Summary

This content provides solved answers for Financial Accounting and Regulatory Framework exam questions. It includes a profit and loss account, statement of financial position, trial balance, partnership appropriation account, and cash flow statement. The content also explains the importance of ratio analysis and the limitations of cash flow statements. The subject is BMP6018 and the course is BA (Hons) Business Finance Pathway. The content is relevant for students of the Institute of Management in Semester 2 of the academic year 2021/22.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BA (HONS) BUSINESS FINANCE PATHWAY

SEMESTER 2 EXAMINATIONS 2021/22

FINANCIAL ACCOUNTING AND THE

REGULATORY FRAMEWORK

ANSWER BOOKLET

INSTRUCTIONS TO CANDIDATES:

There are four compulsory questions on

this paper.

Answer all four questions.

All questions carry equal marks.

Calculators may be used but full workings

must be shown. You can copy and paste

any calculation from Excel to MS Word

answer Booklet.

Please submit your Answer Booklet

through Turnitin Link in Moodle.

SEMESTER 2 EXAMINATIONS 2021/22

FINANCIAL ACCOUNTING AND THE

REGULATORY FRAMEWORK

ANSWER BOOKLET

INSTRUCTIONS TO CANDIDATES:

There are four compulsory questions on

this paper.

Answer all four questions.

All questions carry equal marks.

Calculators may be used but full workings

must be shown. You can copy and paste

any calculation from Excel to MS Word

answer Booklet.

Please submit your Answer Booklet

through Turnitin Link in Moodle.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Institute of Management

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

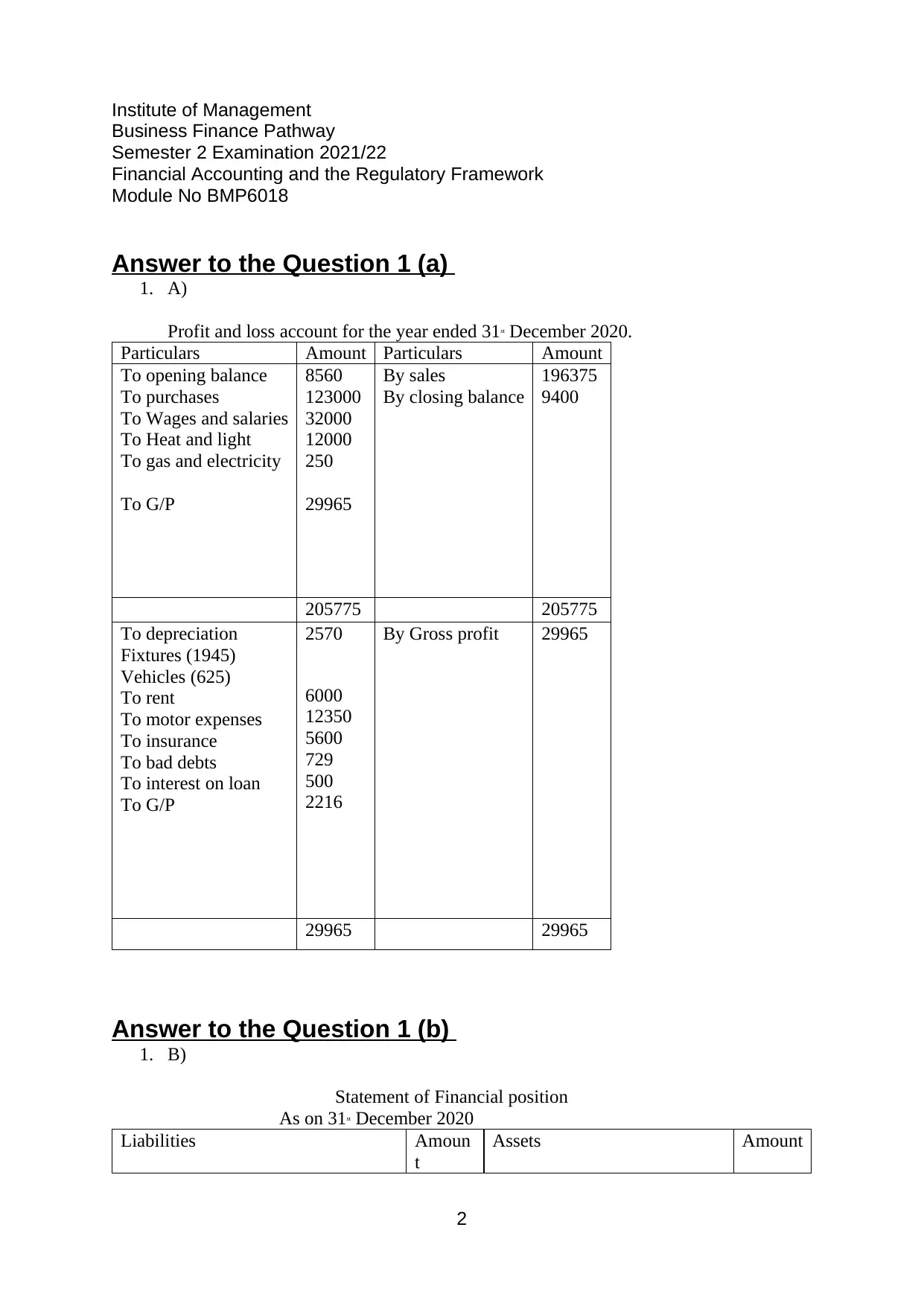

Answer to the Question 1 (a)

1. A)

Profit and loss account for the year ended 31st December 2020.

Particulars Amount Particulars Amount

To opening balance

To purchases

To Wages and salaries

To Heat and light

To gas and electricity

To G/P

8560

123000

32000

12000

250

29965

By sales

By closing balance

196375

9400

205775 205775

To depreciation

Fixtures (1945)

Vehicles (625)

To rent

To motor expenses

To insurance

To bad debts

To interest on loan

To G/P

2570

6000

12350

5600

729

500

2216

By Gross profit 29965

29965 29965

Answer to the Question 1 (b)

1. B)

Statement of Financial position

As on 31st December 2020

Liabilities Amoun

t

Assets Amount

2

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Answer to the Question 1 (a)

1. A)

Profit and loss account for the year ended 31st December 2020.

Particulars Amount Particulars Amount

To opening balance

To purchases

To Wages and salaries

To Heat and light

To gas and electricity

To G/P

8560

123000

32000

12000

250

29965

By sales

By closing balance

196375

9400

205775 205775

To depreciation

Fixtures (1945)

Vehicles (625)

To rent

To motor expenses

To insurance

To bad debts

To interest on loan

To G/P

2570

6000

12350

5600

729

500

2216

By Gross profit 29965

29965 29965

Answer to the Question 1 (b)

1. B)

Statement of Financial position

As on 31st December 2020

Liabilities Amoun

t

Assets Amount

2

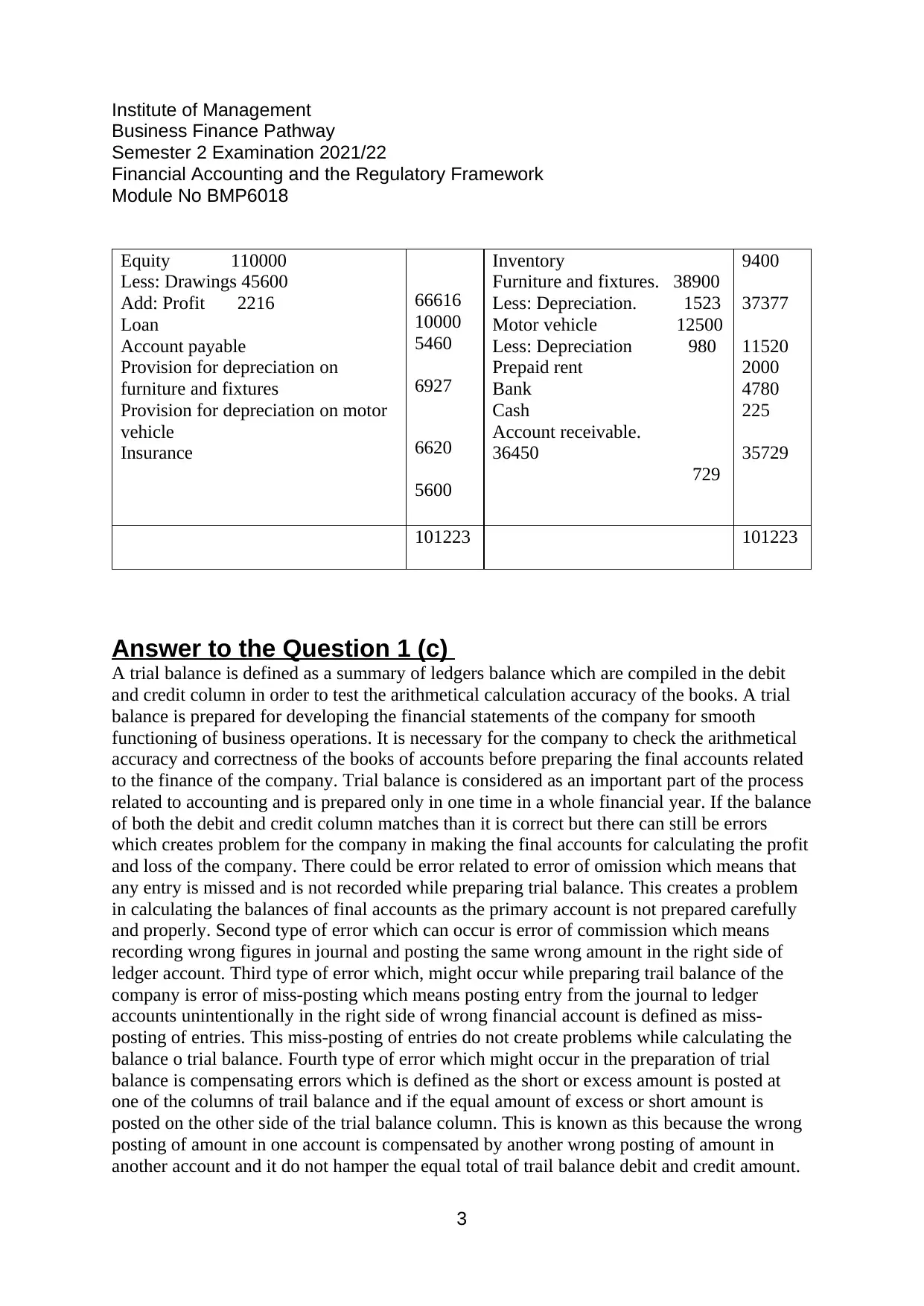

Institute of Management

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Equity 110000

Less: Drawings 45600

Add: Profit 2216

Loan

Account payable

Provision for depreciation on

furniture and fixtures

Provision for depreciation on motor

vehicle

Insurance

66616

10000

5460

6927

6620

5600

Inventory

Furniture and fixtures. 38900

Less: Depreciation. 1523

Motor vehicle 12500

Less: Depreciation 980

Prepaid rent

Bank

Cash

Account receivable.

36450

729

9400

37377

11520

2000

4780

225

35729

101223 101223

Answer to the Question 1 (c)

A trial balance is defined as a summary of ledgers balance which are compiled in the debit

and credit column in order to test the arithmetical calculation accuracy of the books. A trial

balance is prepared for developing the financial statements of the company for smooth

functioning of business operations. It is necessary for the company to check the arithmetical

accuracy and correctness of the books of accounts before preparing the final accounts related

to the finance of the company. Trial balance is considered as an important part of the process

related to accounting and is prepared only in one time in a whole financial year. If the balance

of both the debit and credit column matches than it is correct but there can still be errors

which creates problem for the company in making the final accounts for calculating the profit

and loss of the company. There could be error related to error of omission which means that

any entry is missed and is not recorded while preparing trial balance. This creates a problem

in calculating the balances of final accounts as the primary account is not prepared carefully

and properly. Second type of error which can occur is error of commission which means

recording wrong figures in journal and posting the same wrong amount in the right side of

ledger account. Third type of error which, might occur while preparing trail balance of the

company is error of miss-posting which means posting entry from the journal to ledger

accounts unintentionally in the right side of wrong financial account is defined as miss-

posting of entries. This miss-posting of entries do not create problems while calculating the

balance o trial balance. Fourth type of error which might occur in the preparation of trial

balance is compensating errors which is defined as the short or excess amount is posted at

one of the columns of trail balance and if the equal amount of excess or short amount is

posted on the other side of the trial balance column. This is known as this because the wrong

posting of amount in one account is compensated by another wrong posting of amount in

another account and it do not hamper the equal total of trail balance debit and credit amount.

3

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Equity 110000

Less: Drawings 45600

Add: Profit 2216

Loan

Account payable

Provision for depreciation on

furniture and fixtures

Provision for depreciation on motor

vehicle

Insurance

66616

10000

5460

6927

6620

5600

Inventory

Furniture and fixtures. 38900

Less: Depreciation. 1523

Motor vehicle 12500

Less: Depreciation 980

Prepaid rent

Bank

Cash

Account receivable.

36450

729

9400

37377

11520

2000

4780

225

35729

101223 101223

Answer to the Question 1 (c)

A trial balance is defined as a summary of ledgers balance which are compiled in the debit

and credit column in order to test the arithmetical calculation accuracy of the books. A trial

balance is prepared for developing the financial statements of the company for smooth

functioning of business operations. It is necessary for the company to check the arithmetical

accuracy and correctness of the books of accounts before preparing the final accounts related

to the finance of the company. Trial balance is considered as an important part of the process

related to accounting and is prepared only in one time in a whole financial year. If the balance

of both the debit and credit column matches than it is correct but there can still be errors

which creates problem for the company in making the final accounts for calculating the profit

and loss of the company. There could be error related to error of omission which means that

any entry is missed and is not recorded while preparing trial balance. This creates a problem

in calculating the balances of final accounts as the primary account is not prepared carefully

and properly. Second type of error which can occur is error of commission which means

recording wrong figures in journal and posting the same wrong amount in the right side of

ledger account. Third type of error which, might occur while preparing trail balance of the

company is error of miss-posting which means posting entry from the journal to ledger

accounts unintentionally in the right side of wrong financial account is defined as miss-

posting of entries. This miss-posting of entries do not create problems while calculating the

balance o trial balance. Fourth type of error which might occur in the preparation of trial

balance is compensating errors which is defined as the short or excess amount is posted at

one of the columns of trail balance and if the equal amount of excess or short amount is

posted on the other side of the trial balance column. This is known as this because the wrong

posting of amount in one account is compensated by another wrong posting of amount in

another account and it do not hamper the equal total of trail balance debit and credit amount.

3

Institute of Management

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Write your response here

Answer to the Question 2 (a)

1. A)

Partnership appropriation account

Particulars Amount Particulars Amount

To interest on capital

Bridge 15000

Marsh 7500

To salary

Bridge 15000

Marsh 25000

To profit distributed (2:1)

Bridge 46433

Marsh 23217

22500

40000

69650

By profits

By interest on drawings

Less: interest on loan by bridge

132000

650

(500)

132150 132150

Answer to the Question 2 (b)

2 b) Partner’s capital account

Particulars Bridge Marsh Particulars Bridge Marsh

To balance c/d 30000

0

150000 By balance b/d 30000

0

150000

Partner’s current account

Particulars Bridge Marsh Particulars Bridge Marsh

To interest on drawings 400 250 By bank 30000

0

150000

To interest on loan 500 By interest on capital 15000 7500

To profit and loss 88000 44000 By salary 46433 23217

To balance c/d 27253

3

136467

36143

3

180717 36143

3

180717

4

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Write your response here

Answer to the Question 2 (a)

1. A)

Partnership appropriation account

Particulars Amount Particulars Amount

To interest on capital

Bridge 15000

Marsh 7500

To salary

Bridge 15000

Marsh 25000

To profit distributed (2:1)

Bridge 46433

Marsh 23217

22500

40000

69650

By profits

By interest on drawings

Less: interest on loan by bridge

132000

650

(500)

132150 132150

Answer to the Question 2 (b)

2 b) Partner’s capital account

Particulars Bridge Marsh Particulars Bridge Marsh

To balance c/d 30000

0

150000 By balance b/d 30000

0

150000

Partner’s current account

Particulars Bridge Marsh Particulars Bridge Marsh

To interest on drawings 400 250 By bank 30000

0

150000

To interest on loan 500 By interest on capital 15000 7500

To profit and loss 88000 44000 By salary 46433 23217

To balance c/d 27253

3

136467

36143

3

180717 36143

3

180717

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Institute of Management

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Answer to the Question 2 (c)

Partnership is a type of business which is done by two or more persons to carry out the

business operations together in order to share the profits and losses incurred in equal ratios. In

this type of business every partner work with a aim to achieve the common set goals and

objectives of the business for earning high profitability and growth in the market. A

partnership deed is defined as an agreement between the partners of the company who wants

to continue in the business with the amount of capital invested. The agreement generally

defines about the following things such as nature of the company, rights and duties of

partners, their liabilities and the amount of ratio in which the partner will distribute their

profit and losses of the company among them. But in the absence of partnership deed the

partners need to share the amount of profit and losses between partners in equal share.

Without partnership deed the partners will not get the amount of interest on capital because

interest will only be paid to the partners in the case when the company will earn profits and if

it is agreed within the partners to distribute it. The amount of interest on capital will not be

paid in case of loss to the company in case of absence of partnership deed. The partners will

also not be charged interest related to drawings they make in the absence of partnership deed

between the partners. The partners will also not receive a predetermined amount of salary if

they are not agreed to do business in a deed as they will not be liable of any compensate. The

interest on loan is entitles on the rate of six percent to the partners on advancing a good

amount of money to run the business operations of the company. Thus, for running the

business operations smoothly and in accordance to the market it is necessary for the

partnership firm to get itself registered and make a partnership deed in order to protect the

interest of the company as they have invested a big amount of money in the business.

partnership deed also helps in solving the disputes and in dissolving or partnership firm in a

easy and desirable way for gaining high growth in the competitive market.

Answer to the Question 3 (a)

a) Profitability ratios:

Return on asset ratio: Net income/ Total asset

Delta: 109.89/1430 *100 = 7.68%

Horizon: 117.81/1559.4*100 = 7.55%

Operating profit ratio: Operating profit/ Sales

Delta: 166.43/1625.91*100 = 10.23%

Horizon: 183.59/1969.44*100 = 9.32%

Gross profit ratio: GP/Sales *100

Delta: 505.78/1625.91*100 = 31.1075%

Horizon: 633.05/1969.44*100 = 3214.1436%

Net profit ratio: NP/Sales*100

5

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Answer to the Question 2 (c)

Partnership is a type of business which is done by two or more persons to carry out the

business operations together in order to share the profits and losses incurred in equal ratios. In

this type of business every partner work with a aim to achieve the common set goals and

objectives of the business for earning high profitability and growth in the market. A

partnership deed is defined as an agreement between the partners of the company who wants

to continue in the business with the amount of capital invested. The agreement generally

defines about the following things such as nature of the company, rights and duties of

partners, their liabilities and the amount of ratio in which the partner will distribute their

profit and losses of the company among them. But in the absence of partnership deed the

partners need to share the amount of profit and losses between partners in equal share.

Without partnership deed the partners will not get the amount of interest on capital because

interest will only be paid to the partners in the case when the company will earn profits and if

it is agreed within the partners to distribute it. The amount of interest on capital will not be

paid in case of loss to the company in case of absence of partnership deed. The partners will

also not be charged interest related to drawings they make in the absence of partnership deed

between the partners. The partners will also not receive a predetermined amount of salary if

they are not agreed to do business in a deed as they will not be liable of any compensate. The

interest on loan is entitles on the rate of six percent to the partners on advancing a good

amount of money to run the business operations of the company. Thus, for running the

business operations smoothly and in accordance to the market it is necessary for the

partnership firm to get itself registered and make a partnership deed in order to protect the

interest of the company as they have invested a big amount of money in the business.

partnership deed also helps in solving the disputes and in dissolving or partnership firm in a

easy and desirable way for gaining high growth in the competitive market.

Answer to the Question 3 (a)

a) Profitability ratios:

Return on asset ratio: Net income/ Total asset

Delta: 109.89/1430 *100 = 7.68%

Horizon: 117.81/1559.4*100 = 7.55%

Operating profit ratio: Operating profit/ Sales

Delta: 166.43/1625.91*100 = 10.23%

Horizon: 183.59/1969.44*100 = 9.32%

Gross profit ratio: GP/Sales *100

Delta: 505.78/1625.91*100 = 31.1075%

Horizon: 633.05/1969.44*100 = 3214.1436%

Net profit ratio: NP/Sales*100

5

Institute of Management

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Delta: 109.89/1625.91*100 = 6.7586%

Horizon: 117.81/1969.44*100 = 5.9819%

Liquidity ratios:

Cash ratios: Cash marketable securities/ Current liabilities

Delta: 93.14/464.64 = 0.20

Horizon: 1007/322.37 = 0.312

Current ratio: Current asset/Current liabilities

Delta: 938.3/46464 = 2.019

Horizon: 898.1/322.37 = 2.786

Quick ratio: Current asset-Stock/current liability

Delta: 938.3-651.2/464.64 = 0.6178

Horizon: 898.1-443.3/322.37 = 1.4108

Efficiency ratios:

Inventory turnover ratio: Cost of goods sold/ Total inventory

Delta: 1120.13/1625.91 = 0.689

Horizon: 1336.39/1969.44 = 0.679

Receivable turnover ratio: Debtors/total inventory

Delta: 194/1625.91 = 0.12

Horizon: 354.1/1969.49 = 0.18

Asset turnover ratio: Sales/Total assets

Delta: 1625.91/1430 = 1.137

Horizon: 1969.44/1559.4 = 1.263

Answer to the Question 3 (b)

1. The Managing Director of Delta Plc requires you to report your findings to him in a memo

format.

From the above gathered data from the above calculations, it is

recommended that Delta PLC must prepare efficient and accurate financial

statements in order to assess the ability of the business in order to generate

income, operating costs, balance sheet assets or equity of shareholder over

the time. The ratios related to profitability can be compared with the

efficiency ratios which helps in considering how well and effectively the

company uses the assets for generating income. Higher ratios results are

often regarded as more favourable and accurate which helps the company in

determining the current position of the company assets and how to utilize

them efficiently ns effectively for attaining future growth. The liquidity ratio

help the company in determining the ability to pay the amount related to

short term debt obligation. Liquidity is defined as the ability to convert the

company asset into cash cheaply and quickly which helps the business in

gaining financial assistance easily. Efficiency ratio considered by the company

because it helps in determining and evaluating the performance in order to

6

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Delta: 109.89/1625.91*100 = 6.7586%

Horizon: 117.81/1969.44*100 = 5.9819%

Liquidity ratios:

Cash ratios: Cash marketable securities/ Current liabilities

Delta: 93.14/464.64 = 0.20

Horizon: 1007/322.37 = 0.312

Current ratio: Current asset/Current liabilities

Delta: 938.3/46464 = 2.019

Horizon: 898.1/322.37 = 2.786

Quick ratio: Current asset-Stock/current liability

Delta: 938.3-651.2/464.64 = 0.6178

Horizon: 898.1-443.3/322.37 = 1.4108

Efficiency ratios:

Inventory turnover ratio: Cost of goods sold/ Total inventory

Delta: 1120.13/1625.91 = 0.689

Horizon: 1336.39/1969.44 = 0.679

Receivable turnover ratio: Debtors/total inventory

Delta: 194/1625.91 = 0.12

Horizon: 354.1/1969.49 = 0.18

Asset turnover ratio: Sales/Total assets

Delta: 1625.91/1430 = 1.137

Horizon: 1969.44/1559.4 = 1.263

Answer to the Question 3 (b)

1. The Managing Director of Delta Plc requires you to report your findings to him in a memo

format.

From the above gathered data from the above calculations, it is

recommended that Delta PLC must prepare efficient and accurate financial

statements in order to assess the ability of the business in order to generate

income, operating costs, balance sheet assets or equity of shareholder over

the time. The ratios related to profitability can be compared with the

efficiency ratios which helps in considering how well and effectively the

company uses the assets for generating income. Higher ratios results are

often regarded as more favourable and accurate which helps the company in

determining the current position of the company assets and how to utilize

them efficiently ns effectively for attaining future growth. The liquidity ratio

help the company in determining the ability to pay the amount related to

short term debt obligation. Liquidity is defined as the ability to convert the

company asset into cash cheaply and quickly which helps the business in

gaining financial assistance easily. Efficiency ratio considered by the company

because it helps in determining and evaluating the performance in order to

6

Institute of Management

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

gain high growth and profitability in the current competitive environment.

Thus, it is important for the company to manage its company assets and

liabilities properly so that they earn high return in the future and helps in

improving the performance an working efficiency of the comp0ny and its

employees. As ratio analysis is important for the company in order to analyse

financial, liquidity, risk, profitability, solvency, efficiency and effectiveness of

the proper utilization the company funds for better management of finance.

Answer to the Question 4 (a)

Shelton PLC

Statement of cash flow

For the year ended 31 December 2020

Particulars Amount

Cash Flow from operating activities

Cash received from customers 216149

Cash paid to employees -26285

Cash paid for interest -137.5

Cash paid for income taxes -670

Net Cash inflow from operating activities 189056.5

Answer to the Question 4 (b)

Cash flow statement is defined as a tool or method of analysing financial statements which

help in managing the working capital funds of the company. This statement includes the

following aspects such as accounts receivable, accounts payable, office related expenses and

many more. Cash flow statement have certain limitations which creates problem for the

company in calculating their finances which are explained below:

The concluded information in the statement of cash flow fails to provide a complete

and accurate picture about the financial position of the company.

The main problem of cash flow statement is that its accuracy is majorly depended on

the concerned balance sheet. If the calculations done in balance sheet is incorrect than

the prepared cash flow statement will also prove to be wrong.

7

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

gain high growth and profitability in the current competitive environment.

Thus, it is important for the company to manage its company assets and

liabilities properly so that they earn high return in the future and helps in

improving the performance an working efficiency of the comp0ny and its

employees. As ratio analysis is important for the company in order to analyse

financial, liquidity, risk, profitability, solvency, efficiency and effectiveness of

the proper utilization the company funds for better management of finance.

Answer to the Question 4 (a)

Shelton PLC

Statement of cash flow

For the year ended 31 December 2020

Particulars Amount

Cash Flow from operating activities

Cash received from customers 216149

Cash paid to employees -26285

Cash paid for interest -137.5

Cash paid for income taxes -670

Net Cash inflow from operating activities 189056.5

Answer to the Question 4 (b)

Cash flow statement is defined as a tool or method of analysing financial statements which

help in managing the working capital funds of the company. This statement includes the

following aspects such as accounts receivable, accounts payable, office related expenses and

many more. Cash flow statement have certain limitations which creates problem for the

company in calculating their finances which are explained below:

The concluded information in the statement of cash flow fails to provide a complete

and accurate picture about the financial position of the company.

The main problem of cash flow statement is that its accuracy is majorly depended on

the concerned balance sheet. If the calculations done in balance sheet is incorrect than

the prepared cash flow statement will also prove to be wrong.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Institute of Management

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

The preparation of cash flow statement is not prepared on the basis of accrual concept

if accounting and because of this the accuracy of cash flow is questionable and

doubtable.

It is also not appropriate for measuring the profitability of the company because the

non-cash items are not involved in the calculation part of cash flow from operating

activities.

Answer to the Question 4 (c)

1. From next year, Shelton PLC is required to prepare consolidated financial statements as

they are planning to take control over another entity. Write an email of the board of

directors of Shelton PLC explaining the requirements to prepare consolidated financial

statements

2. EMAIL

Consolidated financial statements are defined as a collected of financial

statements of a large group of entities that are represented as a single entity in

the economy. These statements help in determining and analysing the financial

position of the whole group of commonly owned and controlled companies. The

board of directors of Shelton PLC must prepare consolidated financial statements

as they want to take over the control of other entities. These financial statements

help the company in providing a true picture about the financial health of the

company in all subsidiaries and divisions. In simplest words, consolidated

statements helps the company in bringing together the parent company and

subsidiary company financial statements under one umbrella. As incomplete

understanding about the financial health of other company can put Shelton PLC in

danger and can hamper the growth and profitability of the company in the

competitive market. Consolidated accounts majorly provide benefit to the

managers, stakeholders and directors of the parent company and will reduce the

interest in checking the subsidiary company which do not have these type of

statements.

8

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

The preparation of cash flow statement is not prepared on the basis of accrual concept

if accounting and because of this the accuracy of cash flow is questionable and

doubtable.

It is also not appropriate for measuring the profitability of the company because the

non-cash items are not involved in the calculation part of cash flow from operating

activities.

Answer to the Question 4 (c)

1. From next year, Shelton PLC is required to prepare consolidated financial statements as

they are planning to take control over another entity. Write an email of the board of

directors of Shelton PLC explaining the requirements to prepare consolidated financial

statements

2. EMAIL

Consolidated financial statements are defined as a collected of financial

statements of a large group of entities that are represented as a single entity in

the economy. These statements help in determining and analysing the financial

position of the whole group of commonly owned and controlled companies. The

board of directors of Shelton PLC must prepare consolidated financial statements

as they want to take over the control of other entities. These financial statements

help the company in providing a true picture about the financial health of the

company in all subsidiaries and divisions. In simplest words, consolidated

statements helps the company in bringing together the parent company and

subsidiary company financial statements under one umbrella. As incomplete

understanding about the financial health of other company can put Shelton PLC in

danger and can hamper the growth and profitability of the company in the

competitive market. Consolidated accounts majorly provide benefit to the

managers, stakeholders and directors of the parent company and will reduce the

interest in checking the subsidiary company which do not have these type of

statements.

8

Institute of Management

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

END

9

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

END

9

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.