Financial Accounting and Regulatory Framework Exam Answers and Solutions

Added on 2023-06-11

9 Pages2436 Words443 Views

BA (HONS) BUSINESS FINANCE PATHWAY

SEMESTER 2 EXAMINATIONS 2021/22

FINANCIAL ACCOUNTING AND THE

REGULATORY FRAMEWORK

ANSWER BOOKLET

INSTRUCTIONS TO CANDIDATES:

There are four compulsory questions on

this paper.

Answer all four questions.

All questions carry equal marks.

Calculators may be used but full workings

must be shown. You can copy and paste

any calculation from Excel to MS Word

answer Booklet.

Please submit your Answer Booklet

through Turnitin Link in Moodle.

SEMESTER 2 EXAMINATIONS 2021/22

FINANCIAL ACCOUNTING AND THE

REGULATORY FRAMEWORK

ANSWER BOOKLET

INSTRUCTIONS TO CANDIDATES:

There are four compulsory questions on

this paper.

Answer all four questions.

All questions carry equal marks.

Calculators may be used but full workings

must be shown. You can copy and paste

any calculation from Excel to MS Word

answer Booklet.

Please submit your Answer Booklet

through Turnitin Link in Moodle.

Institute of Management

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

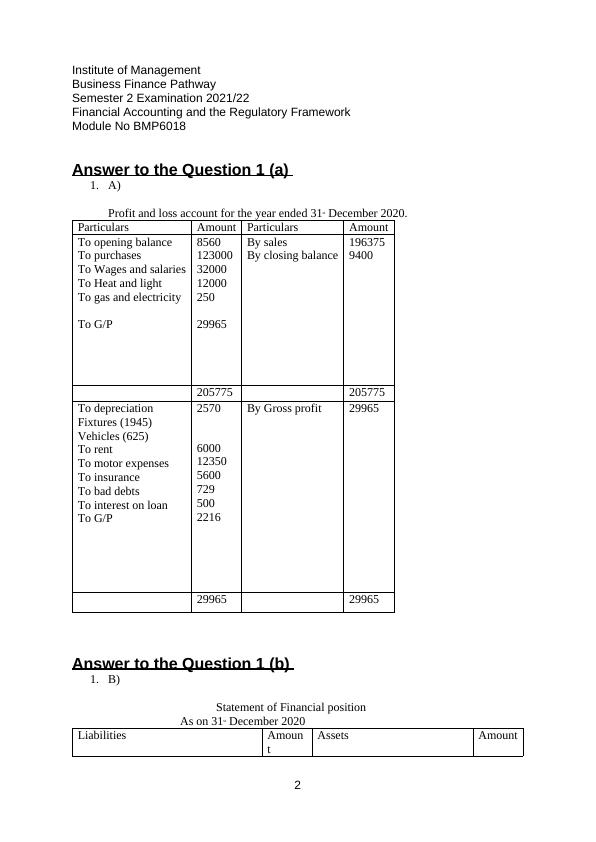

Answer to the Question 1 (a)

1. A)

Profit and loss account for the year ended 31st December 2020.

Particulars Amount Particulars Amount

To opening balance

To purchases

To Wages and salaries

To Heat and light

To gas and electricity

To G/P

8560

123000

32000

12000

250

29965

By sales

By closing balance

196375

9400

205775 205775

To depreciation

Fixtures (1945)

Vehicles (625)

To rent

To motor expenses

To insurance

To bad debts

To interest on loan

To G/P

2570

6000

12350

5600

729

500

2216

By Gross profit 29965

29965 29965

Answer to the Question 1 (b)

1. B)

Statement of Financial position

As on 31st December 2020

Liabilities Amoun

t

Assets Amount

2

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Answer to the Question 1 (a)

1. A)

Profit and loss account for the year ended 31st December 2020.

Particulars Amount Particulars Amount

To opening balance

To purchases

To Wages and salaries

To Heat and light

To gas and electricity

To G/P

8560

123000

32000

12000

250

29965

By sales

By closing balance

196375

9400

205775 205775

To depreciation

Fixtures (1945)

Vehicles (625)

To rent

To motor expenses

To insurance

To bad debts

To interest on loan

To G/P

2570

6000

12350

5600

729

500

2216

By Gross profit 29965

29965 29965

Answer to the Question 1 (b)

1. B)

Statement of Financial position

As on 31st December 2020

Liabilities Amoun

t

Assets Amount

2

Institute of Management

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

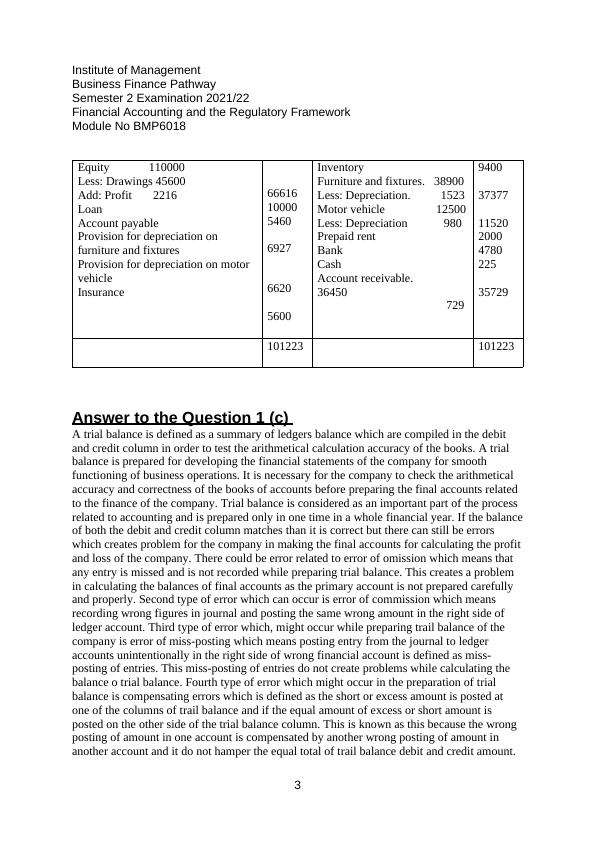

Equity 110000

Less: Drawings 45600

Add: Profit 2216

Loan

Account payable

Provision for depreciation on

furniture and fixtures

Provision for depreciation on motor

vehicle

Insurance

66616

10000

5460

6927

6620

5600

Inventory

Furniture and fixtures. 38900

Less: Depreciation. 1523

Motor vehicle 12500

Less: Depreciation 980

Prepaid rent

Bank

Cash

Account receivable.

36450

729

9400

37377

11520

2000

4780

225

35729

101223 101223

Answer to the Question 1 (c)

A trial balance is defined as a summary of ledgers balance which are compiled in the debit

and credit column in order to test the arithmetical calculation accuracy of the books. A trial

balance is prepared for developing the financial statements of the company for smooth

functioning of business operations. It is necessary for the company to check the arithmetical

accuracy and correctness of the books of accounts before preparing the final accounts related

to the finance of the company. Trial balance is considered as an important part of the process

related to accounting and is prepared only in one time in a whole financial year. If the balance

of both the debit and credit column matches than it is correct but there can still be errors

which creates problem for the company in making the final accounts for calculating the profit

and loss of the company. There could be error related to error of omission which means that

any entry is missed and is not recorded while preparing trial balance. This creates a problem

in calculating the balances of final accounts as the primary account is not prepared carefully

and properly. Second type of error which can occur is error of commission which means

recording wrong figures in journal and posting the same wrong amount in the right side of

ledger account. Third type of error which, might occur while preparing trail balance of the

company is error of miss-posting which means posting entry from the journal to ledger

accounts unintentionally in the right side of wrong financial account is defined as miss-

posting of entries. This miss-posting of entries do not create problems while calculating the

balance o trial balance. Fourth type of error which might occur in the preparation of trial

balance is compensating errors which is defined as the short or excess amount is posted at

one of the columns of trail balance and if the equal amount of excess or short amount is

posted on the other side of the trial balance column. This is known as this because the wrong

posting of amount in one account is compensated by another wrong posting of amount in

another account and it do not hamper the equal total of trail balance debit and credit amount.

3

Business Finance Pathway

Semester 2 Examination 2021/22

Financial Accounting and the Regulatory Framework

Module No BMP6018

Equity 110000

Less: Drawings 45600

Add: Profit 2216

Loan

Account payable

Provision for depreciation on

furniture and fixtures

Provision for depreciation on motor

vehicle

Insurance

66616

10000

5460

6927

6620

5600

Inventory

Furniture and fixtures. 38900

Less: Depreciation. 1523

Motor vehicle 12500

Less: Depreciation 980

Prepaid rent

Bank

Cash

Account receivable.

36450

729

9400

37377

11520

2000

4780

225

35729

101223 101223

Answer to the Question 1 (c)

A trial balance is defined as a summary of ledgers balance which are compiled in the debit

and credit column in order to test the arithmetical calculation accuracy of the books. A trial

balance is prepared for developing the financial statements of the company for smooth

functioning of business operations. It is necessary for the company to check the arithmetical

accuracy and correctness of the books of accounts before preparing the final accounts related

to the finance of the company. Trial balance is considered as an important part of the process

related to accounting and is prepared only in one time in a whole financial year. If the balance

of both the debit and credit column matches than it is correct but there can still be errors

which creates problem for the company in making the final accounts for calculating the profit

and loss of the company. There could be error related to error of omission which means that

any entry is missed and is not recorded while preparing trial balance. This creates a problem

in calculating the balances of final accounts as the primary account is not prepared carefully

and properly. Second type of error which can occur is error of commission which means

recording wrong figures in journal and posting the same wrong amount in the right side of

ledger account. Third type of error which, might occur while preparing trail balance of the

company is error of miss-posting which means posting entry from the journal to ledger

accounts unintentionally in the right side of wrong financial account is defined as miss-

posting of entries. This miss-posting of entries do not create problems while calculating the

balance o trial balance. Fourth type of error which might occur in the preparation of trial

balance is compensating errors which is defined as the short or excess amount is posted at

one of the columns of trail balance and if the equal amount of excess or short amount is

posted on the other side of the trial balance column. This is known as this because the wrong

posting of amount in one account is compensated by another wrong posting of amount in

another account and it do not hamper the equal total of trail balance debit and credit amount.

3

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Accounting and the Regulatory Framework Answer Bookletlg...

|16

|3397

|458

Financial Accounting and the Regulatory Framework - Exam Answer Bookletlg...

|17

|3390

|319

LT4001 Economics And Finance For The Service Sector | Assignmentlg...

|6

|1164

|258

Online Project: Accounting Questions and Answerslg...

|9

|997

|495