Financial Accounting | Report

Added on 2020-03-13

7 Pages1385 Words64 Views

FINANCIALACCOUNTINGSTUDENT ID:[Pick the date]

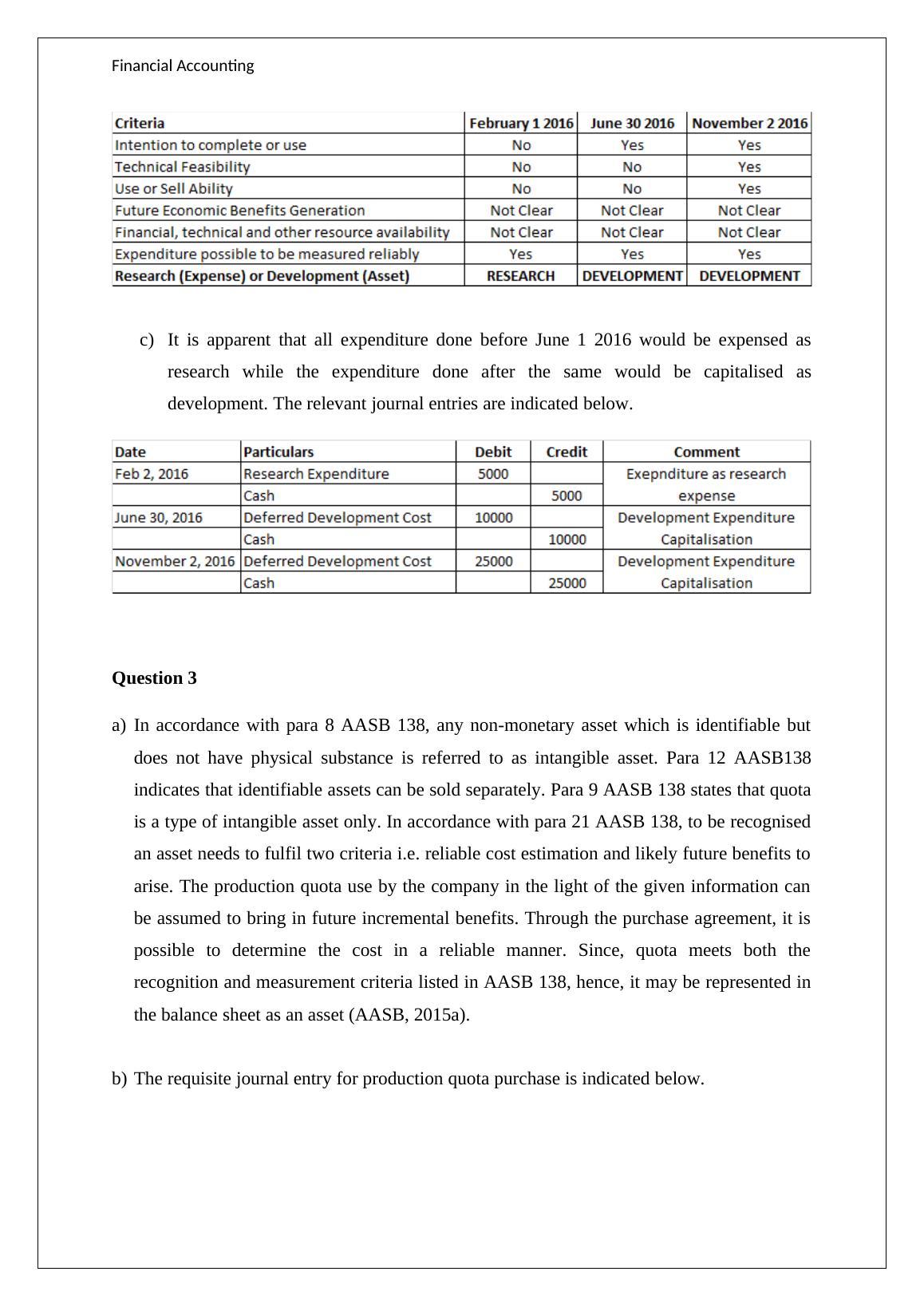

Financial AccountingQuestion 1a)Based on the given facts, it is apparent that no new business has been acquired byHillary and hence the goodwill which is being recognised has been internallygenerated. However, in accordance with para 48 AASB 138, internally generatedgoodwill cannot be represented (recognised) as an asset in the books of account(AASB, 2015a).b)Based on the given facts, it is apparent that Starlite Pty Ltd has purchased Syklite onJuly 1, 2016 and out of the purchase price, $ 5,000 is on account of goodwill. Hence,in accordance with para 33 AASB 138, the $ 5,000 paid for goodwill in the businesscombination can be recognised as the goodwill on Starlite’s balance sheet as on July1, 2016 (AASB, 2015a).c)For FY2017, the company i.e. Starlite cannot recognise any amortization expense onaccount of the available goodwill being purchased or internally generated. This is inline with para 107 AASB 138 according to which an intangible asset having indefinitelife (such as goodwill) would not face any amortization. However, as per para 108,such assets would have to undergo annual impairment test or whenever there isimpairment indication to determine if the carrying value of goodwill differs from thefair value (AASB, 2015a).d)In accordance with para 75 AASB 138, revaluation of intangible asset is possible ifthere is an active market which can be determine the fair value. However, in the givencase, no active market would exist for goodwill and hence no revaluation would becarried out (AASB, 2015a).Question 2a)It is apparent that there is development of software by the company which may berecognised as expenses related to either research or development. As a result, therelevant paragraphs would be para 8 (R&D definition), para 57(Capitalisation of R&Dexpenditure) and para 54 (Research expenditure to be treated as expense) (AASB,2015a).b)The requisite table is indicated below.

Financial Accountingc)It is apparent that all expenditure done before June 1 2016 would be expensed asresearch while the expenditure done after the same would be capitalised asdevelopment. The relevant journal entries are indicated below.Question 3a)In accordance with para 8 AASB 138, any non-monetary asset which is identifiable butdoes not have physical substance is referred to as intangible asset. Para 12 AASB138indicates that identifiable assets can be sold separately. Para 9 AASB 138 states that quotais a type of intangible asset only. In accordance with para 21 AASB 138, to be recognisedan asset needs to fulfil two criteria i.e. reliable cost estimation and likely future benefits toarise. The production quota use by the company in the light of the given information canbe assumed to bring in future incremental benefits. Through the purchase agreement, it ispossible to determine the cost in a reliable manner. Since, quota meets both therecognition and measurement criteria listed in AASB 138, hence, it may be represented inthe balance sheet as an asset (AASB, 2015a).b)The requisite journal entry for production quota purchase is indicated below.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Contemporary Issue Relating to Accountinglg...

|7

|627

|234

Financial Accounting And Intangible Assetslg...

|7

|1679

|64

Financial Accounting & Reporting - Assignmentlg...

|5

|765

|30

Accounting Treatment of Research and Development Projectlg...

|10

|2621

|317

MAA261 Calculation of Carrying Amount of Machinelg...

|3

|1077

|113

Consolidation of Entitieslg...

|6

|607

|60