Financial Accounting: Income, Revenue, Gains, Cash Flow & Airbus Order

VerifiedAdded on 2023/06/18

|9

|1636

|95

Case Study

AI Summary

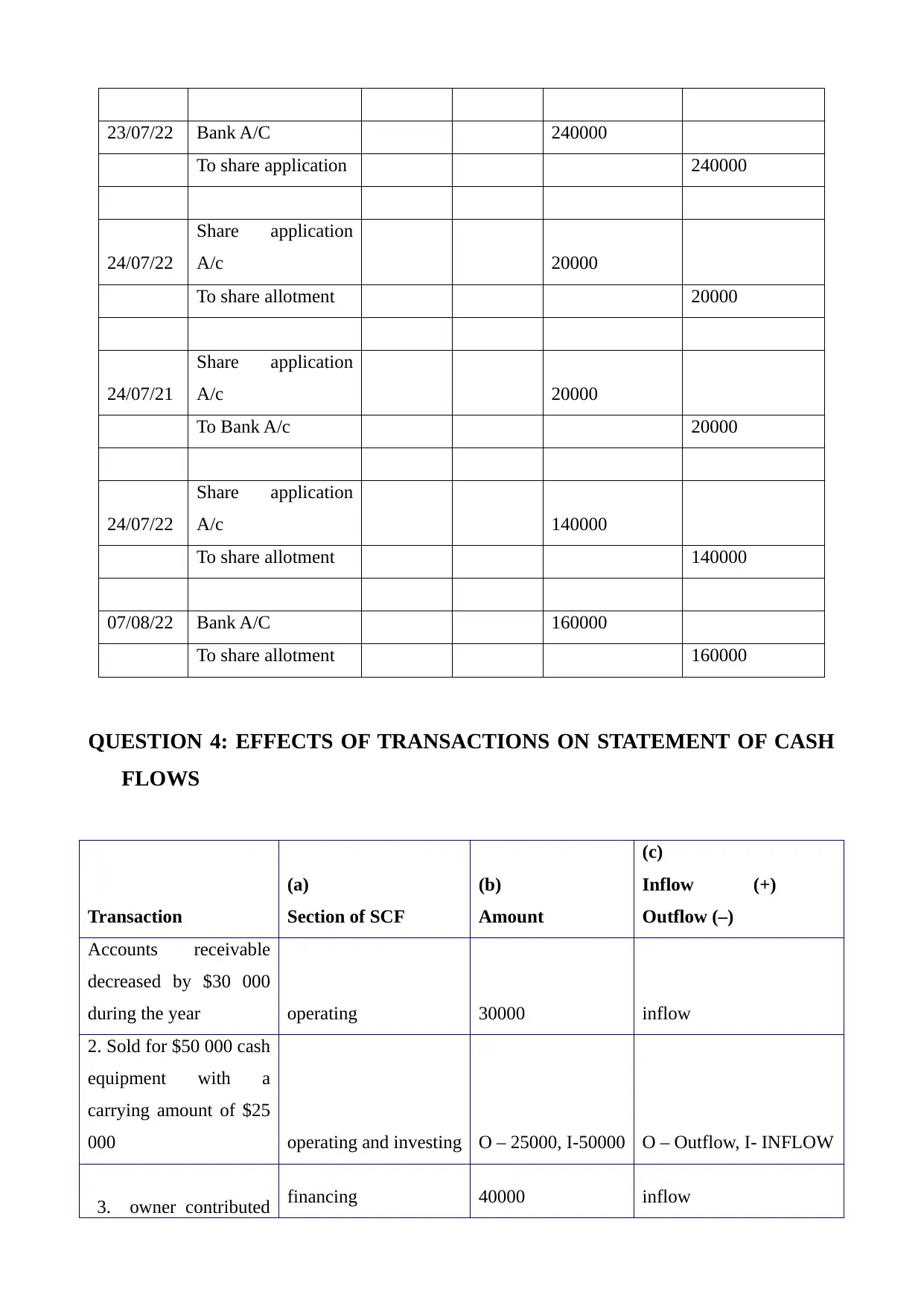

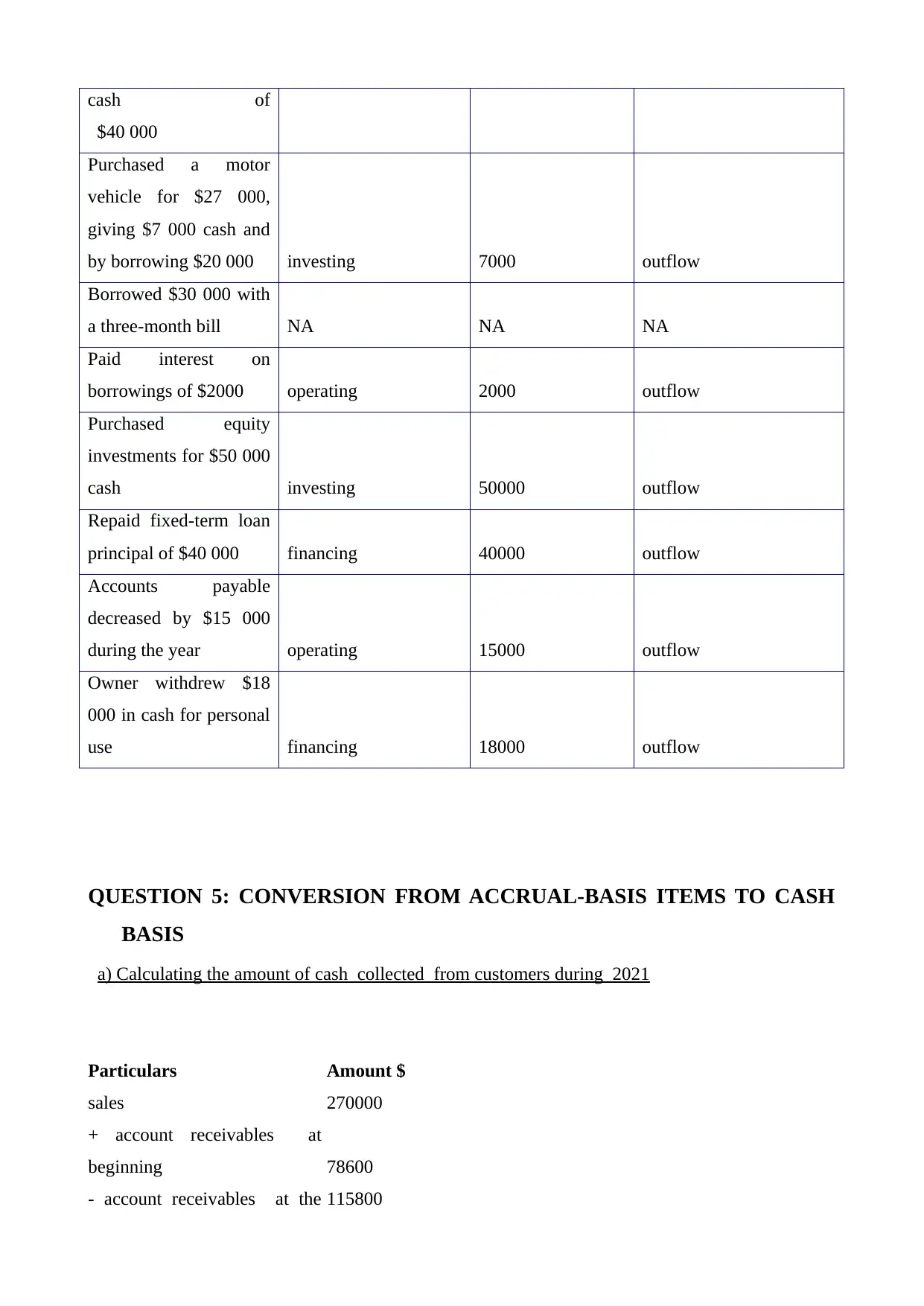

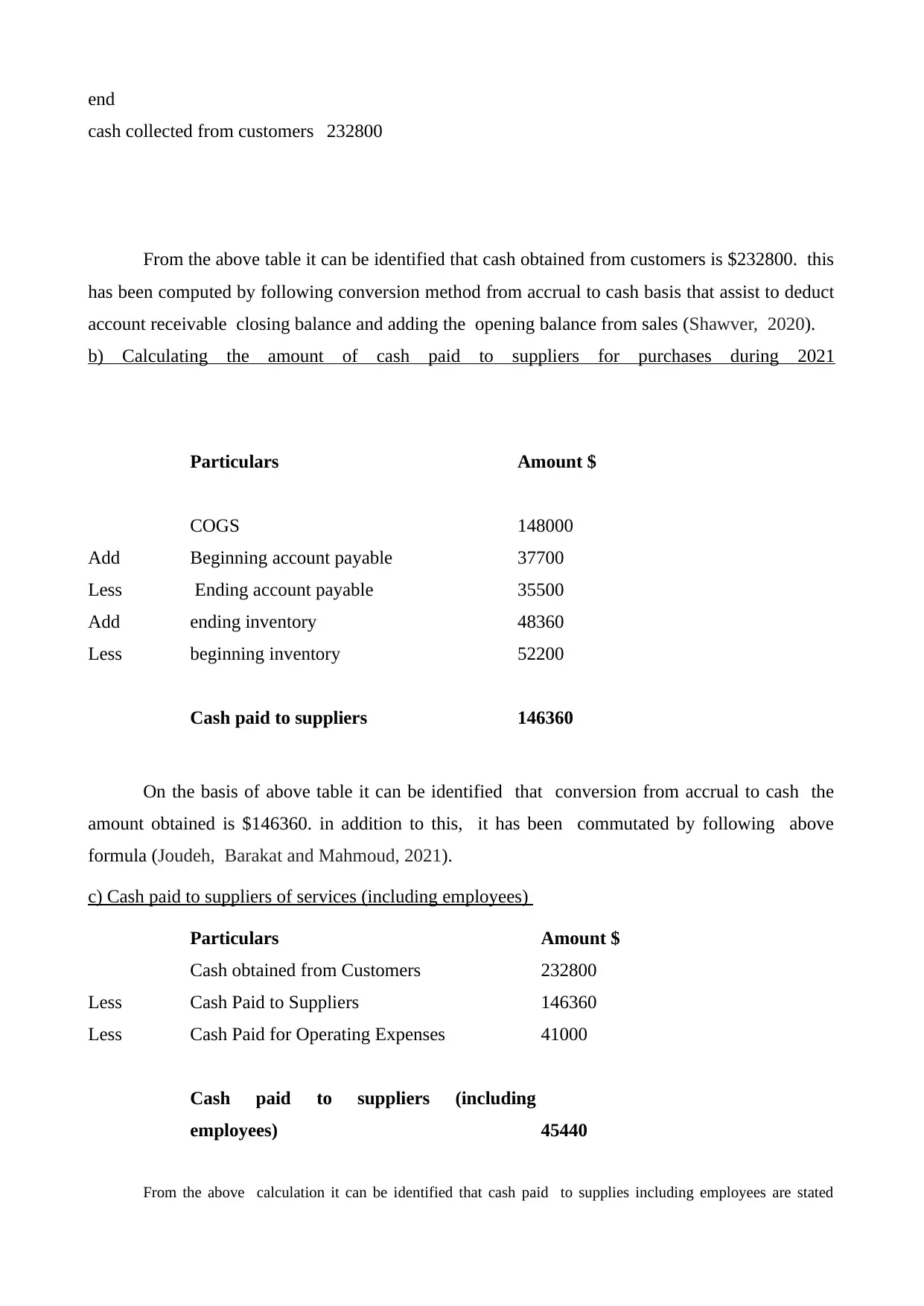

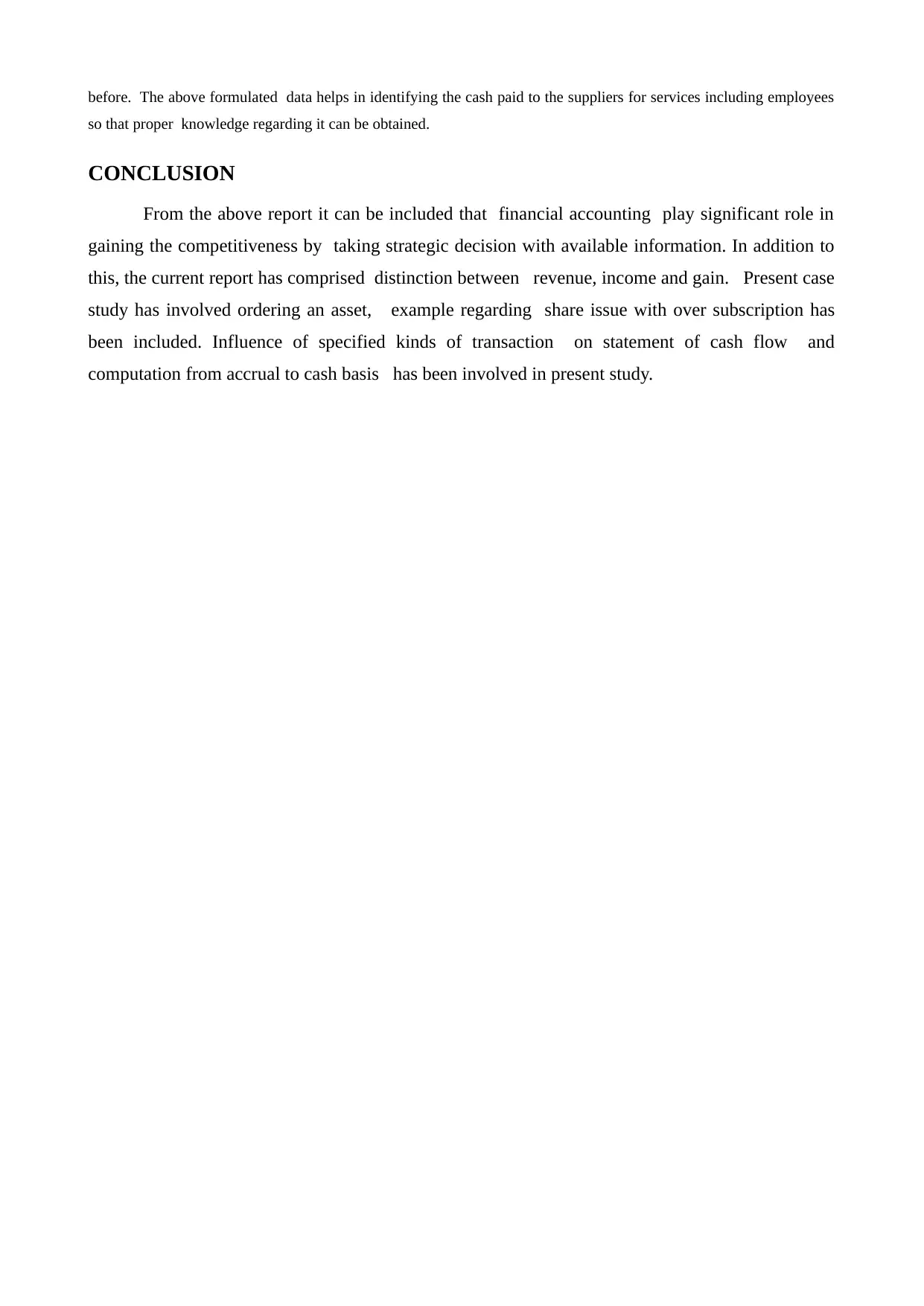

This case study delves into key aspects of financial accounting, starting with a clarification of the differences between income, revenue, and gains. It addresses the accounting treatment of an Airbus A380 order, considering the conceptual framework's definitions of assets and liabilities, and examines the implications of price fluctuations. The study also provides a practical example of share issuance with oversubscription, demonstrating the relevant journal entries. Furthermore, it analyzes the effects of various transactions on the statement of cash flows, categorizing them as operating, investing, or financing activities. Finally, the case study includes a conversion from accrual-basis items to cash basis, calculating cash collected from customers and cash paid to suppliers and employees, highlighting the importance of accurate financial reporting for strategic decision-making. Desklib offers solved assignments and past papers for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.