Comprehensive Financial Accounting Report: Aderonke Ltd Analysis 2020

VerifiedAdded on 2023/06/17

|11

|1740

|150

Report

AI Summary

This report provides a comprehensive analysis of financial accounting principles, using Aderonke Ltd as a case study. It includes a detailed income statement, showcasing revenue, cost of sales, and operating expenses to arrive at net profit. The balance sheet outlines assets, liabilities, and ca...

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

QUESTION 1.................................................................................................................................................3

Income statement...................................................................................................................................3

Statement of financial position................................................................................................................4

QUESTION 2.................................................................................................................................................5

Question 2a.............................................................................................................................................5

Question 2b.............................................................................................................................................6

REFERENCES................................................................................................................................................8

QUESTION 1.................................................................................................................................................3

Income statement...................................................................................................................................3

Statement of financial position................................................................................................................4

QUESTION 2.................................................................................................................................................5

Question 2a.............................................................................................................................................5

Question 2b.............................................................................................................................................6

REFERENCES................................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

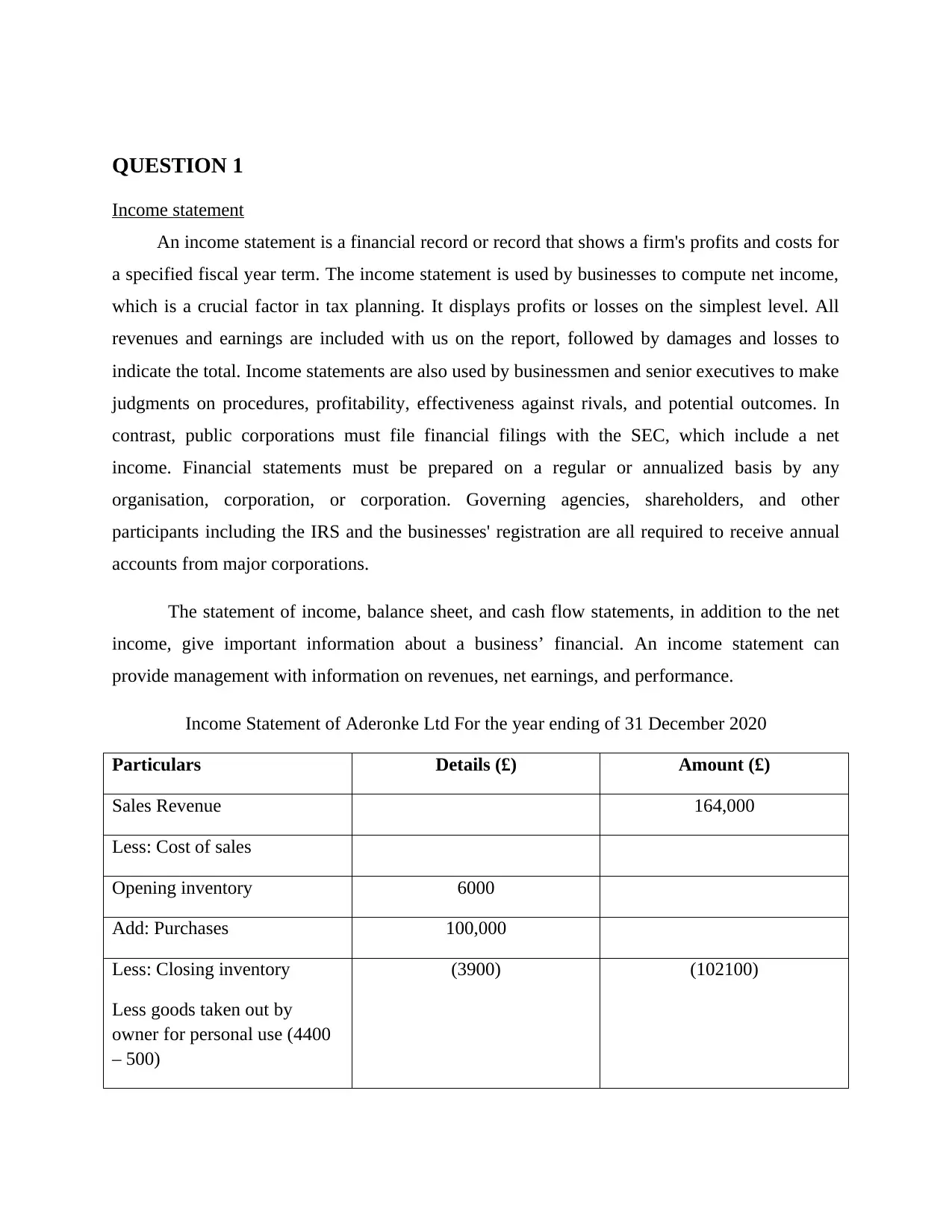

QUESTION 1

Income statement

An income statement is a financial record or record that shows a firm's profits and costs for

a specified fiscal year term. The income statement is used by businesses to compute net income,

which is a crucial factor in tax planning. It displays profits or losses on the simplest level. All

revenues and earnings are included with us on the report, followed by damages and losses to

indicate the total. Income statements are also used by businessmen and senior executives to make

judgments on procedures, profitability, effectiveness against rivals, and potential outcomes. In

contrast, public corporations must file financial filings with the SEC, which include a net

income. Financial statements must be prepared on a regular or annualized basis by any

organisation, corporation, or corporation. Governing agencies, shareholders, and other

participants including the IRS and the businesses' registration are all required to receive annual

accounts from major corporations.

The statement of income, balance sheet, and cash flow statements, in addition to the net

income, give important information about a business’ financial. An income statement can

provide management with information on revenues, net earnings, and performance.

Income Statement of Aderonke Ltd For the year ending of 31 December 2020

Particulars Details (£) Amount (£)

Sales Revenue 164,000

Less: Cost of sales

Opening inventory 6000

Add: Purchases 100,000

Less: Closing inventory

Less goods taken out by

owner for personal use (4400

– 500)

(3900) (102100)

Income statement

An income statement is a financial record or record that shows a firm's profits and costs for

a specified fiscal year term. The income statement is used by businesses to compute net income,

which is a crucial factor in tax planning. It displays profits or losses on the simplest level. All

revenues and earnings are included with us on the report, followed by damages and losses to

indicate the total. Income statements are also used by businessmen and senior executives to make

judgments on procedures, profitability, effectiveness against rivals, and potential outcomes. In

contrast, public corporations must file financial filings with the SEC, which include a net

income. Financial statements must be prepared on a regular or annualized basis by any

organisation, corporation, or corporation. Governing agencies, shareholders, and other

participants including the IRS and the businesses' registration are all required to receive annual

accounts from major corporations.

The statement of income, balance sheet, and cash flow statements, in addition to the net

income, give important information about a business’ financial. An income statement can

provide management with information on revenues, net earnings, and performance.

Income Statement of Aderonke Ltd For the year ending of 31 December 2020

Particulars Details (£) Amount (£)

Sales Revenue 164,000

Less: Cost of sales

Opening inventory 6000

Add: Purchases 100,000

Less: Closing inventory

Less goods taken out by

owner for personal use (4400

– 500)

(3900) (102100)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

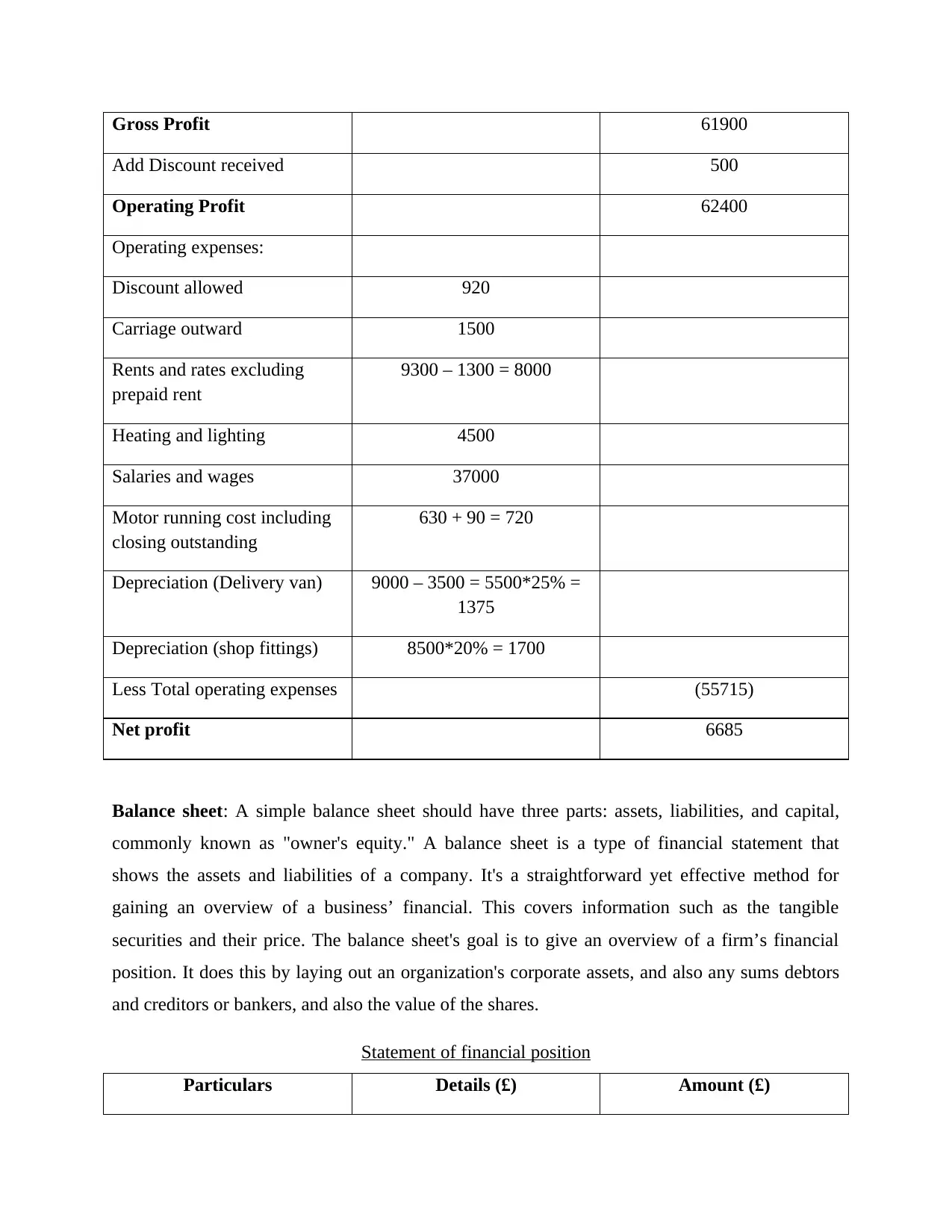

Gross Profit 61900

Add Discount received 500

Operating Profit 62400

Operating expenses:

Discount allowed 920

Carriage outward 1500

Rents and rates excluding

prepaid rent

9300 – 1300 = 8000

Heating and lighting 4500

Salaries and wages 37000

Motor running cost including

closing outstanding

630 + 90 = 720

Depreciation (Delivery van) 9000 – 3500 = 5500*25% =

1375

Depreciation (shop fittings) 8500*20% = 1700

Less Total operating expenses (55715)

Net profit 6685

Balance sheet: A simple balance sheet should have three parts: assets, liabilities, and capital,

commonly known as "owner's equity." A balance sheet is a type of financial statement that

shows the assets and liabilities of a company. It's a straightforward yet effective method for

gaining an overview of a business’ financial. This covers information such as the tangible

securities and their price. The balance sheet's goal is to give an overview of a firm’s financial

position. It does this by laying out an organization's corporate assets, and also any sums debtors

and creditors or bankers, and also the value of the shares.

Statement of financial position

Particulars Details (£) Amount (£)

Add Discount received 500

Operating Profit 62400

Operating expenses:

Discount allowed 920

Carriage outward 1500

Rents and rates excluding

prepaid rent

9300 – 1300 = 8000

Heating and lighting 4500

Salaries and wages 37000

Motor running cost including

closing outstanding

630 + 90 = 720

Depreciation (Delivery van) 9000 – 3500 = 5500*25% =

1375

Depreciation (shop fittings) 8500*20% = 1700

Less Total operating expenses (55715)

Net profit 6685

Balance sheet: A simple balance sheet should have three parts: assets, liabilities, and capital,

commonly known as "owner's equity." A balance sheet is a type of financial statement that

shows the assets and liabilities of a company. It's a straightforward yet effective method for

gaining an overview of a business’ financial. This covers information such as the tangible

securities and their price. The balance sheet's goal is to give an overview of a firm’s financial

position. It does this by laying out an organization's corporate assets, and also any sums debtors

and creditors or bankers, and also the value of the shares.

Statement of financial position

Particulars Details (£) Amount (£)

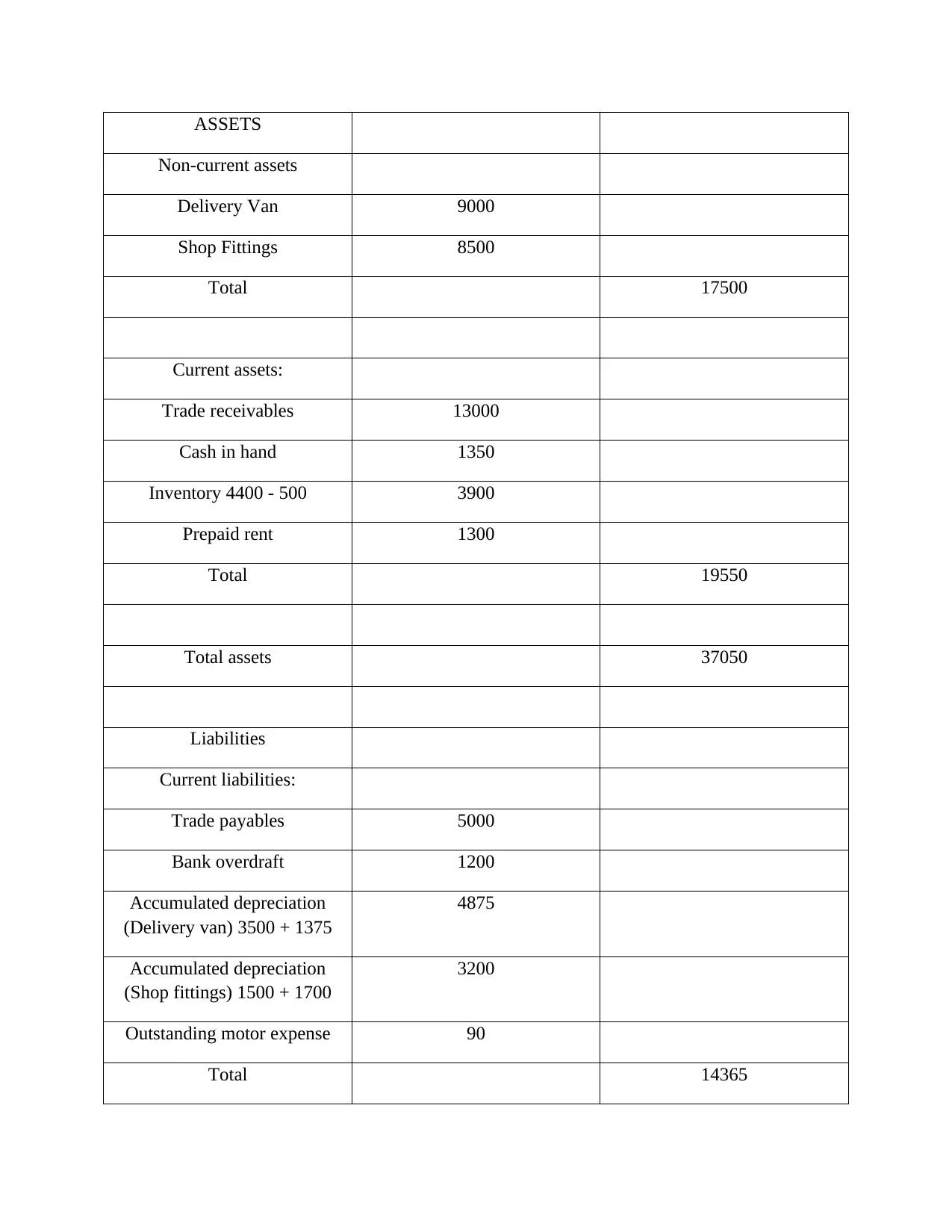

ASSETS

Non-current assets

Delivery Van 9000

Shop Fittings 8500

Total 17500

Current assets:

Trade receivables 13000

Cash in hand 1350

Inventory 4400 - 500 3900

Prepaid rent 1300

Total 19550

Total assets 37050

Liabilities

Current liabilities:

Trade payables 5000

Bank overdraft 1200

Accumulated depreciation

(Delivery van) 3500 + 1375

4875

Accumulated depreciation

(Shop fittings) 1500 + 1700

3200

Outstanding motor expense 90

Total 14365

Non-current assets

Delivery Van 9000

Shop Fittings 8500

Total 17500

Current assets:

Trade receivables 13000

Cash in hand 1350

Inventory 4400 - 500 3900

Prepaid rent 1300

Total 19550

Total assets 37050

Liabilities

Current liabilities:

Trade payables 5000

Bank overdraft 1200

Accumulated depreciation

(Delivery van) 3500 + 1375

4875

Accumulated depreciation

(Shop fittings) 1500 + 1700

3200

Outstanding motor expense 90

Total 14365

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

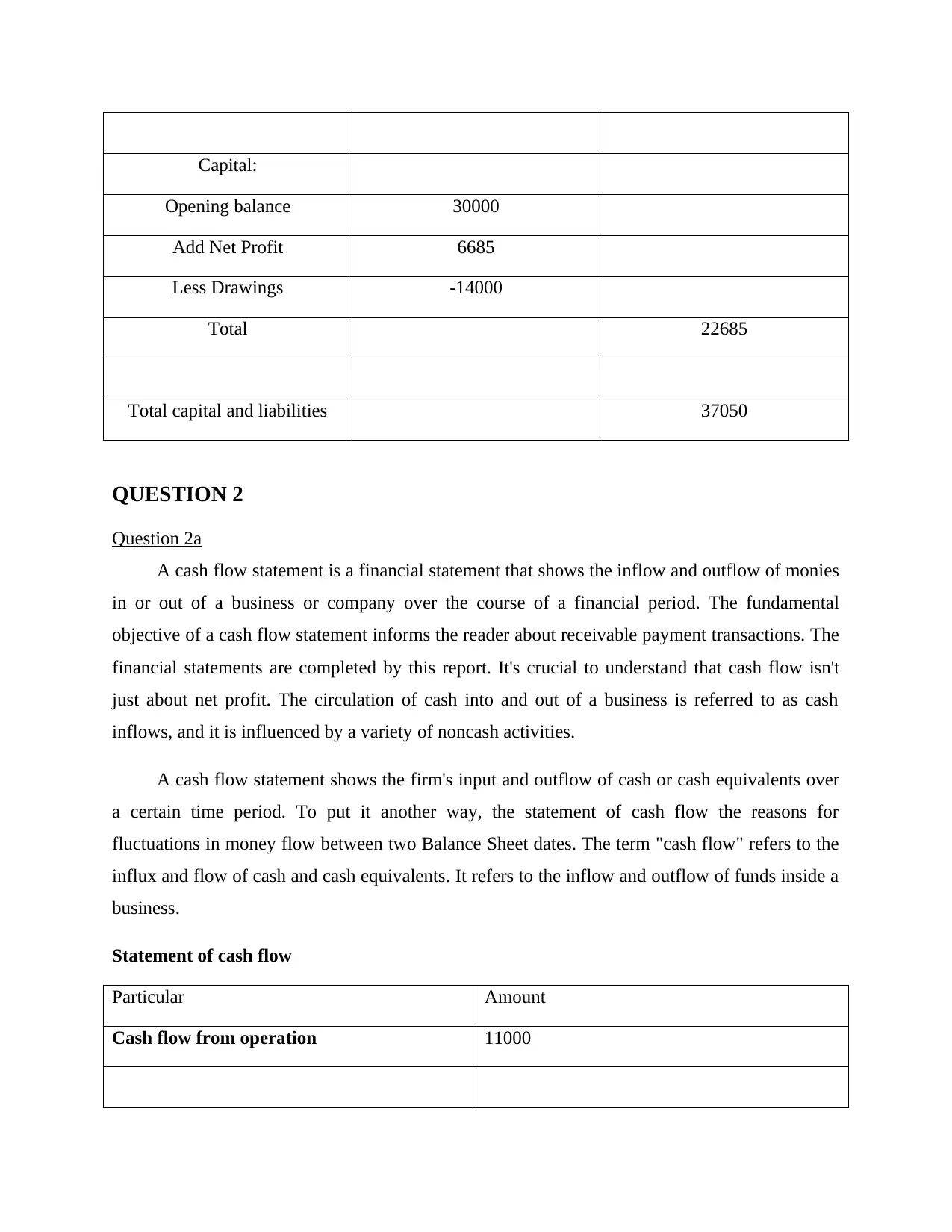

Capital:

Opening balance 30000

Add Net Profit 6685

Less Drawings -14000

Total 22685

Total capital and liabilities 37050

QUESTION 2

Question 2a

A cash flow statement is a financial statement that shows the inflow and outflow of monies

in or out of a business or company over the course of a financial period. The fundamental

objective of a cash flow statement informs the reader about receivable payment transactions. The

financial statements are completed by this report. It's crucial to understand that cash flow isn't

just about net profit. The circulation of cash into and out of a business is referred to as cash

inflows, and it is influenced by a variety of noncash activities.

A cash flow statement shows the firm's input and outflow of cash or cash equivalents over

a certain time period. To put it another way, the statement of cash flow the reasons for

fluctuations in money flow between two Balance Sheet dates. The term "cash flow" refers to the

influx and flow of cash and cash equivalents. It refers to the inflow and outflow of funds inside a

business.

Statement of cash flow

Particular Amount

Cash flow from operation 11000

Opening balance 30000

Add Net Profit 6685

Less Drawings -14000

Total 22685

Total capital and liabilities 37050

QUESTION 2

Question 2a

A cash flow statement is a financial statement that shows the inflow and outflow of monies

in or out of a business or company over the course of a financial period. The fundamental

objective of a cash flow statement informs the reader about receivable payment transactions. The

financial statements are completed by this report. It's crucial to understand that cash flow isn't

just about net profit. The circulation of cash into and out of a business is referred to as cash

inflows, and it is influenced by a variety of noncash activities.

A cash flow statement shows the firm's input and outflow of cash or cash equivalents over

a certain time period. To put it another way, the statement of cash flow the reasons for

fluctuations in money flow between two Balance Sheet dates. The term "cash flow" refers to the

influx and flow of cash and cash equivalents. It refers to the inflow and outflow of funds inside a

business.

Statement of cash flow

Particular Amount

Cash flow from operation 11000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

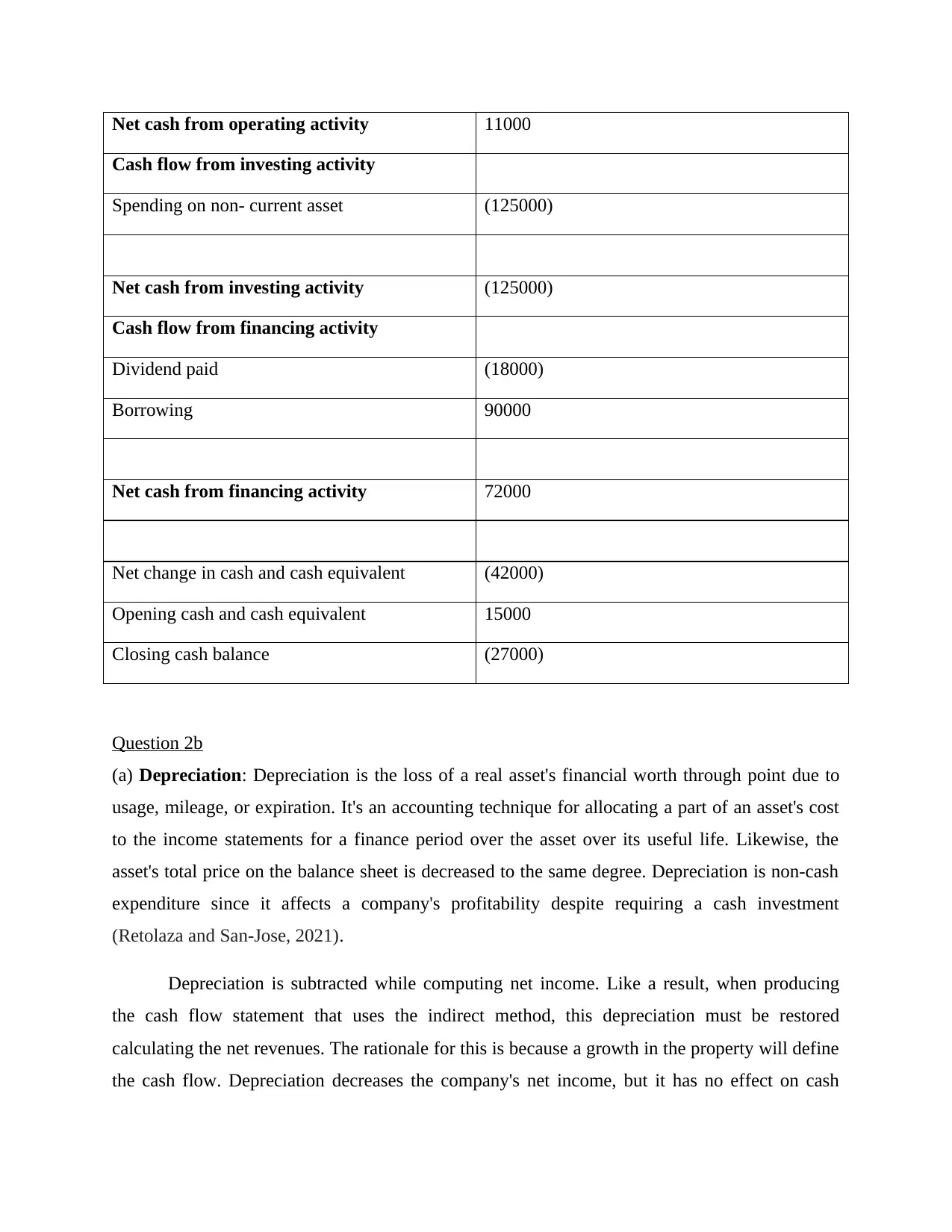

Net cash from operating activity 11000

Cash flow from investing activity

Spending on non- current asset (125000)

Net cash from investing activity (125000)

Cash flow from financing activity

Dividend paid (18000)

Borrowing 90000

Net cash from financing activity 72000

Net change in cash and cash equivalent (42000)

Opening cash and cash equivalent 15000

Closing cash balance (27000)

Question 2b

(a) Depreciation: Depreciation is the loss of a real asset's financial worth through point due to

usage, mileage, or expiration. It's an accounting technique for allocating a part of an asset's cost

to the income statements for a finance period over the asset over its useful life. Likewise, the

asset's total price on the balance sheet is decreased to the same degree. Depreciation is non-cash

expenditure since it affects a company's profitability despite requiring a cash investment

(Retolaza and San-Jose, 2021).

Depreciation is subtracted while computing net income. Like a result, when producing

the cash flow statement that uses the indirect method, this depreciation must be restored

calculating the net revenues. The rationale for this is because a growth in the property will define

the cash flow. Depreciation decreases the company's net income, but it has no effect on cash

Cash flow from investing activity

Spending on non- current asset (125000)

Net cash from investing activity (125000)

Cash flow from financing activity

Dividend paid (18000)

Borrowing 90000

Net cash from financing activity 72000

Net change in cash and cash equivalent (42000)

Opening cash and cash equivalent 15000

Closing cash balance (27000)

Question 2b

(a) Depreciation: Depreciation is the loss of a real asset's financial worth through point due to

usage, mileage, or expiration. It's an accounting technique for allocating a part of an asset's cost

to the income statements for a finance period over the asset over its useful life. Likewise, the

asset's total price on the balance sheet is decreased to the same degree. Depreciation is non-cash

expenditure since it affects a company's profitability despite requiring a cash investment

(Retolaza and San-Jose, 2021).

Depreciation is subtracted while computing net income. Like a result, when producing

the cash flow statement that uses the indirect method, this depreciation must be restored

calculating the net revenues. The rationale for this is because a growth in the property will define

the cash flow. Depreciation decreases the company's net income, but it has no effect on cash

because it is a non-cash operation. As a result, depreciation is officially added when computing

the statement of cash flows.

(b) Disposal of non current asset: The process of disposing of assets includes removing assets

from the financial statements. This is required to entirely eliminate an asset from the financial

statements. A deficit or surplus on an asset disposal may necessitate the accounting of a gains

and losses on the activity in the period ending in which the disposal happens. In this situation,

the sale of non-current assets led to a loss for the firm, which will be subtracted from the net

income from investment operations. From the other side, if a company is profitable on the sale of

net current assets, the proceeds will be added to the investment activity. As a result, the

noncurrent currency value is charged up or removed from the investment activity (Setyawati and

Sudaryati, 2021).

The revenues from the selling of lengthy assets are recorded in the investment operations

portion of the cash flow statement, whereas the profit on the selling is recorded as a reduction

from net earnings in the operating operations section. The differential between the earnings and

the price to book or significant increases of the lengthy assets at the time of the transaction is a

profit on the sale or disposition. The relationship between the cost obtained and the purchase

price is a loss on the selling or disposal. To determine the asset's market price at the time of

selling, depreciation must be documented prior to the time of disposition.

(c) An increase in inventories: The term "increase in inventory" involves the purchase of stock

levels and the excessive amount of stocks in the firm. This means that the inventories will only

be expanded once money is collected. As a consequence, it comes under the heading of cash

flows, which is a drop in money. As a consequence, when compiling the summary, it will be

subtracted from the cash flow figures. This is due, in part, to the fact that declines in cash flow

from the outflow of excess cash result in a drop in the cash payout. As a result, it will be lowered

when calculating cash flow using the indirectly technique (Putsom, 2021). But at the other

extreme, if a profit is made on the sale of non-current assets, it will be included in the cash

inflows from investment operations.

Stock creates cash flow; however acquiring inventory necessitates a financial outlay,

which impacts the cash position of the organisation. In the cash flow sheet, a growth in inventory

the statement of cash flows.

(b) Disposal of non current asset: The process of disposing of assets includes removing assets

from the financial statements. This is required to entirely eliminate an asset from the financial

statements. A deficit or surplus on an asset disposal may necessitate the accounting of a gains

and losses on the activity in the period ending in which the disposal happens. In this situation,

the sale of non-current assets led to a loss for the firm, which will be subtracted from the net

income from investment operations. From the other side, if a company is profitable on the sale of

net current assets, the proceeds will be added to the investment activity. As a result, the

noncurrent currency value is charged up or removed from the investment activity (Setyawati and

Sudaryati, 2021).

The revenues from the selling of lengthy assets are recorded in the investment operations

portion of the cash flow statement, whereas the profit on the selling is recorded as a reduction

from net earnings in the operating operations section. The differential between the earnings and

the price to book or significant increases of the lengthy assets at the time of the transaction is a

profit on the sale or disposition. The relationship between the cost obtained and the purchase

price is a loss on the selling or disposal. To determine the asset's market price at the time of

selling, depreciation must be documented prior to the time of disposition.

(c) An increase in inventories: The term "increase in inventory" involves the purchase of stock

levels and the excessive amount of stocks in the firm. This means that the inventories will only

be expanded once money is collected. As a consequence, it comes under the heading of cash

flows, which is a drop in money. As a consequence, when compiling the summary, it will be

subtracted from the cash flow figures. This is due, in part, to the fact that declines in cash flow

from the outflow of excess cash result in a drop in the cash payout. As a result, it will be lowered

when calculating cash flow using the indirectly technique (Putsom, 2021). But at the other

extreme, if a profit is made on the sale of non-current assets, it will be included in the cash

inflows from investment operations.

Stock creates cash flow; however acquiring inventory necessitates a financial outlay,

which impacts the cash position of the organisation. In the cash flow sheet, a growth in inventory

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

levels will show as a bad sum, suggesting a cash outflow or that a company has acquired more

things than has been delivered.

things than has been delivered.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journal

Retolaza, J. L. and San-Jose, L., 2021. Understanding Social Accounting Based on

Evidence. SAGE Open. 11(2). p.21582440211003865.

Setyawati, D. and Sudaryati, E., 2021. Accounting Ethics in Financial Reporting in The Context

of The Metaphor of ‘Lawang Sewu’(thousands of doors, thousands of information,

thousands of interests). The Indonesian Accounting Review. 11(2). pp.187-195.

Putsom, S., 2021. The Testing of the Reliability and Validity of Accounting and Financial Skills

Measures: An Empirical Evidence of Thai Dairy Farm Entrepreneurs. St. Theresa

Journal of Humanities and Social Sciences. 7(1). pp.1-22.

Hwang, K. J., Kang, P. K. and Jung, D. J., 2021. The association between human resource

investments in the internal accounting control system and non-audit fees: evidence from

South Korea. International Journal of Trade and Global Markets. 14(2). pp.97-106.

Books and Journal

Retolaza, J. L. and San-Jose, L., 2021. Understanding Social Accounting Based on

Evidence. SAGE Open. 11(2). p.21582440211003865.

Setyawati, D. and Sudaryati, E., 2021. Accounting Ethics in Financial Reporting in The Context

of The Metaphor of ‘Lawang Sewu’(thousands of doors, thousands of information,

thousands of interests). The Indonesian Accounting Review. 11(2). pp.187-195.

Putsom, S., 2021. The Testing of the Reliability and Validity of Accounting and Financial Skills

Measures: An Empirical Evidence of Thai Dairy Farm Entrepreneurs. St. Theresa

Journal of Humanities and Social Sciences. 7(1). pp.1-22.

Hwang, K. J., Kang, P. K. and Jung, D. J., 2021. The association between human resource

investments in the internal accounting control system and non-audit fees: evidence from

South Korea. International Journal of Trade and Global Markets. 14(2). pp.97-106.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.