Financial Accounting Analysis: Income Statement and Position 2018

VerifiedAdded on 2023/06/18

|12

|1463

|89

Report

AI Summary

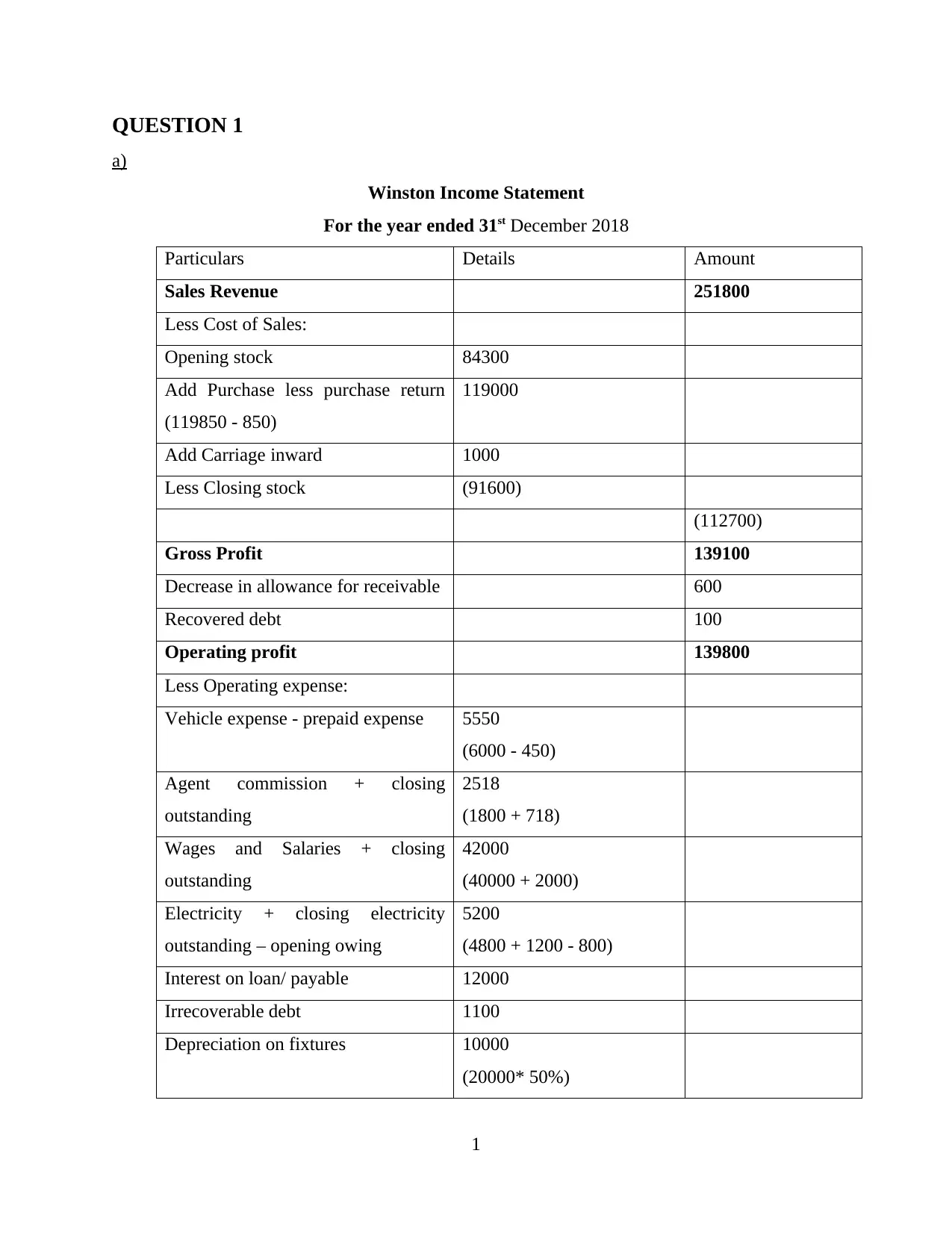

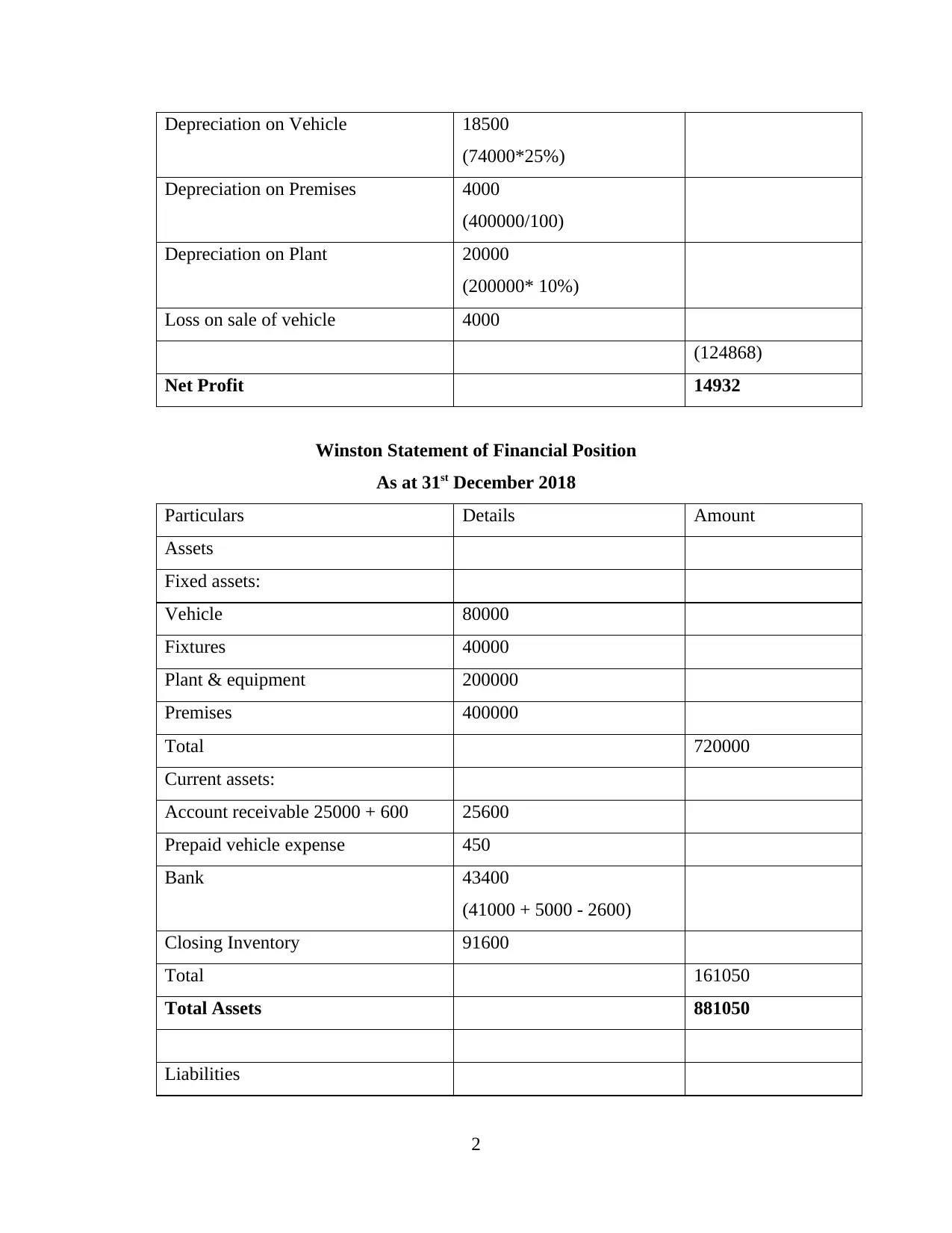

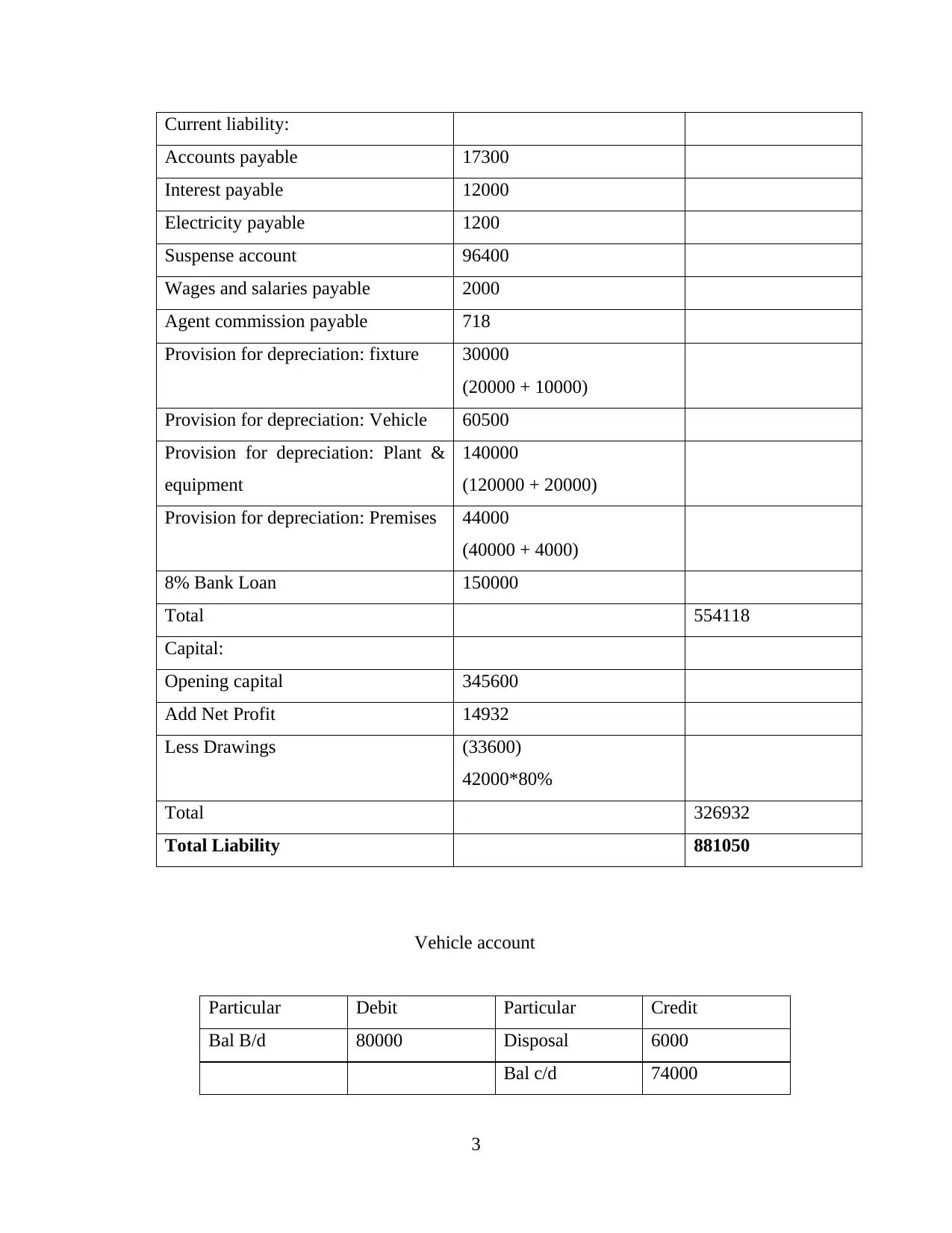

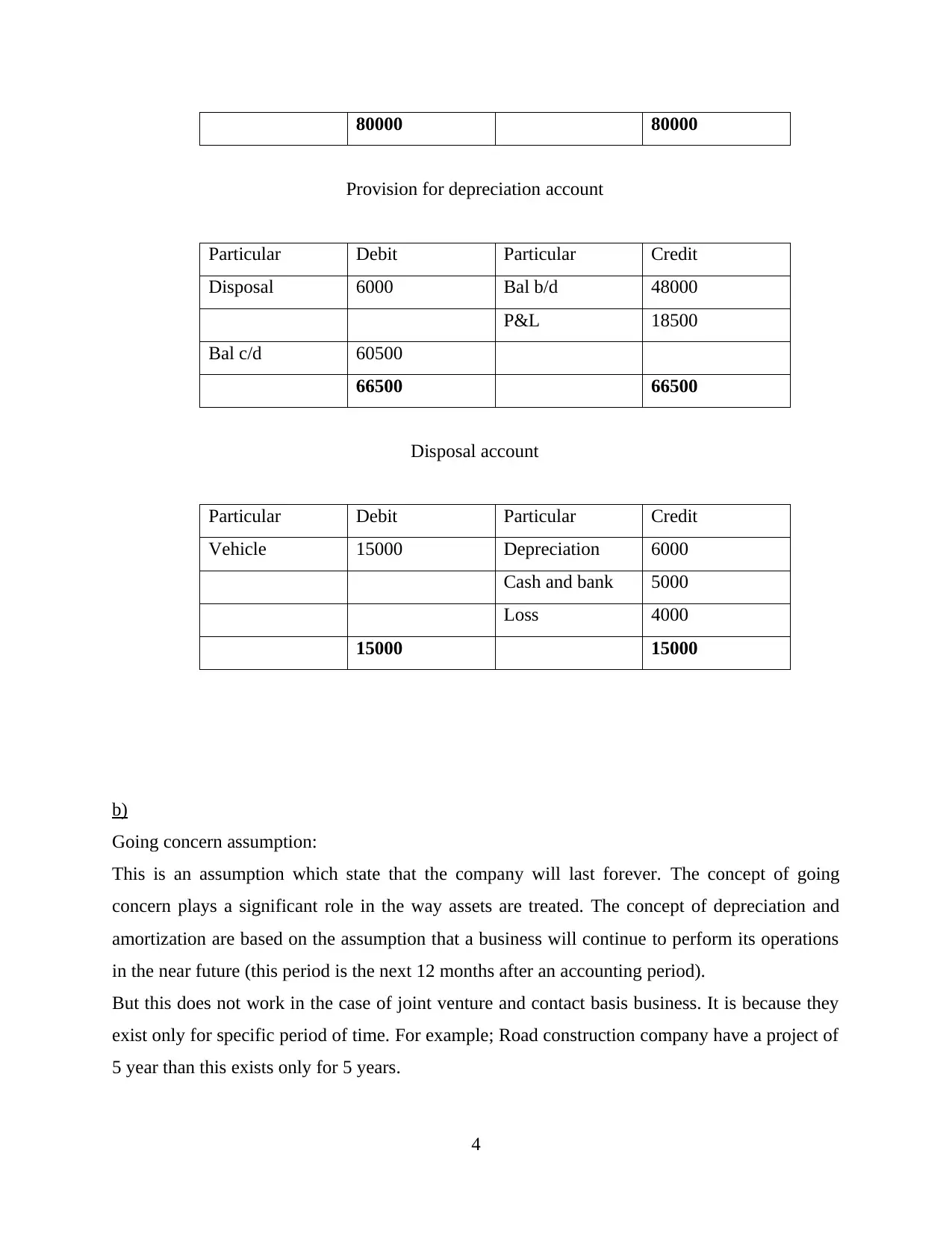

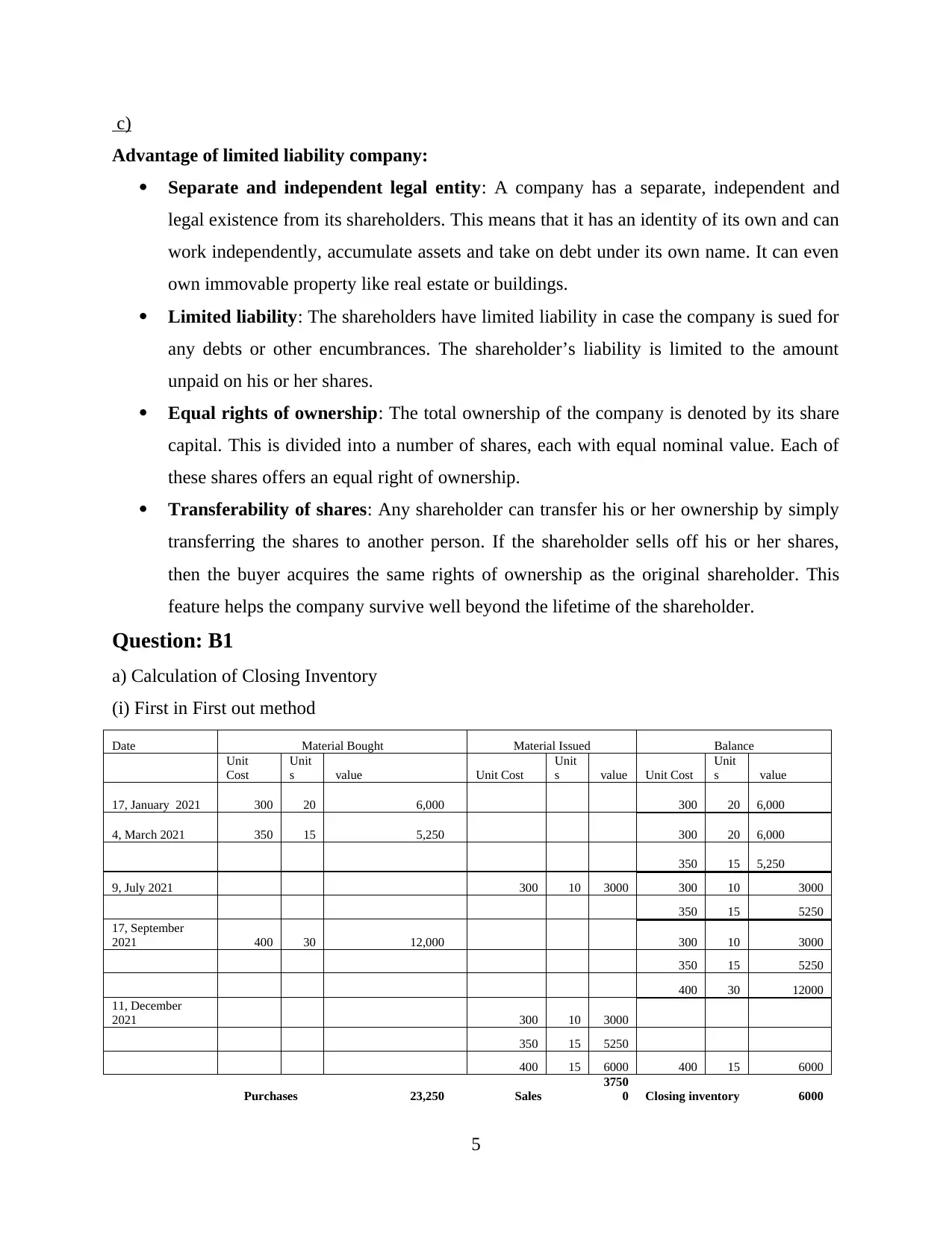

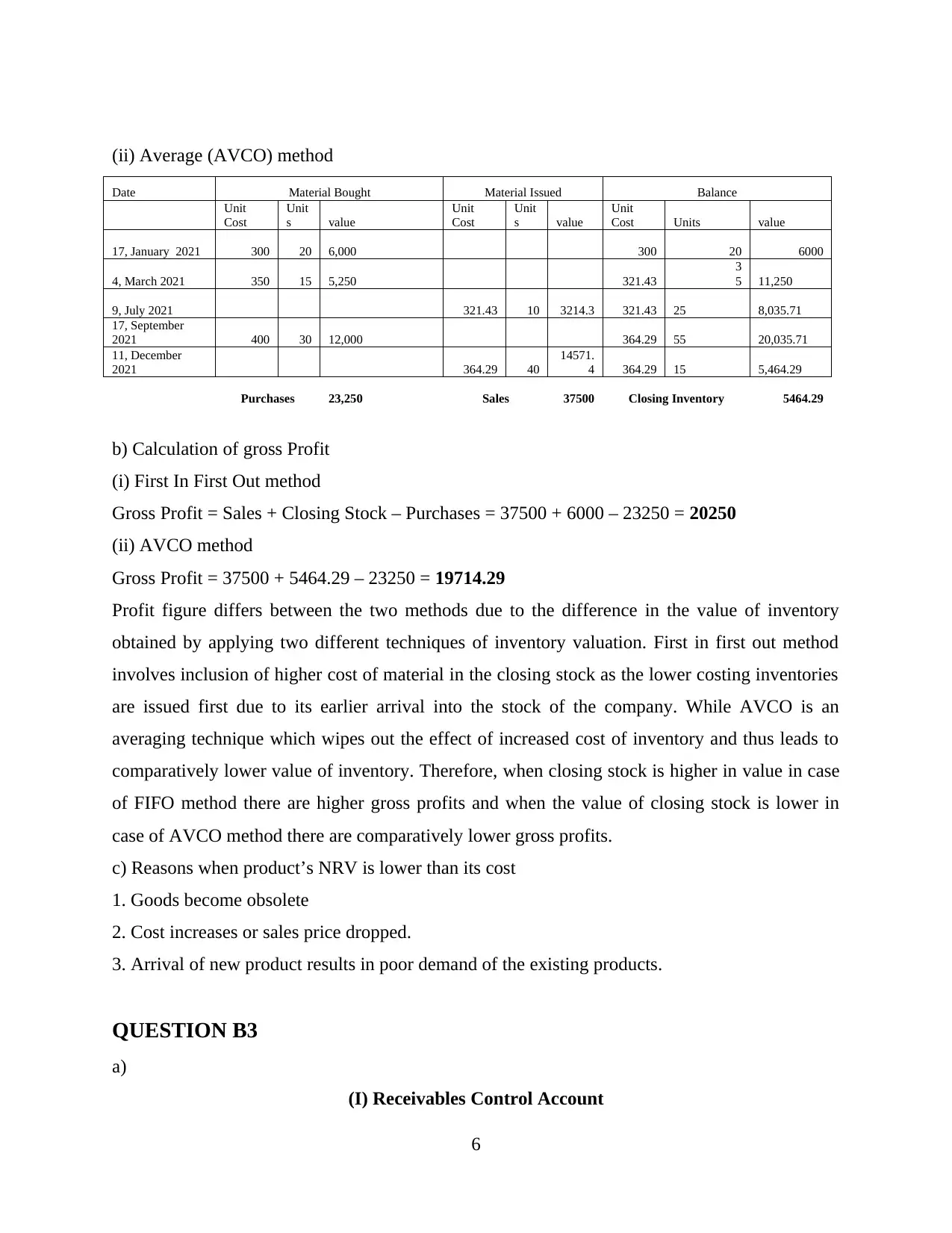

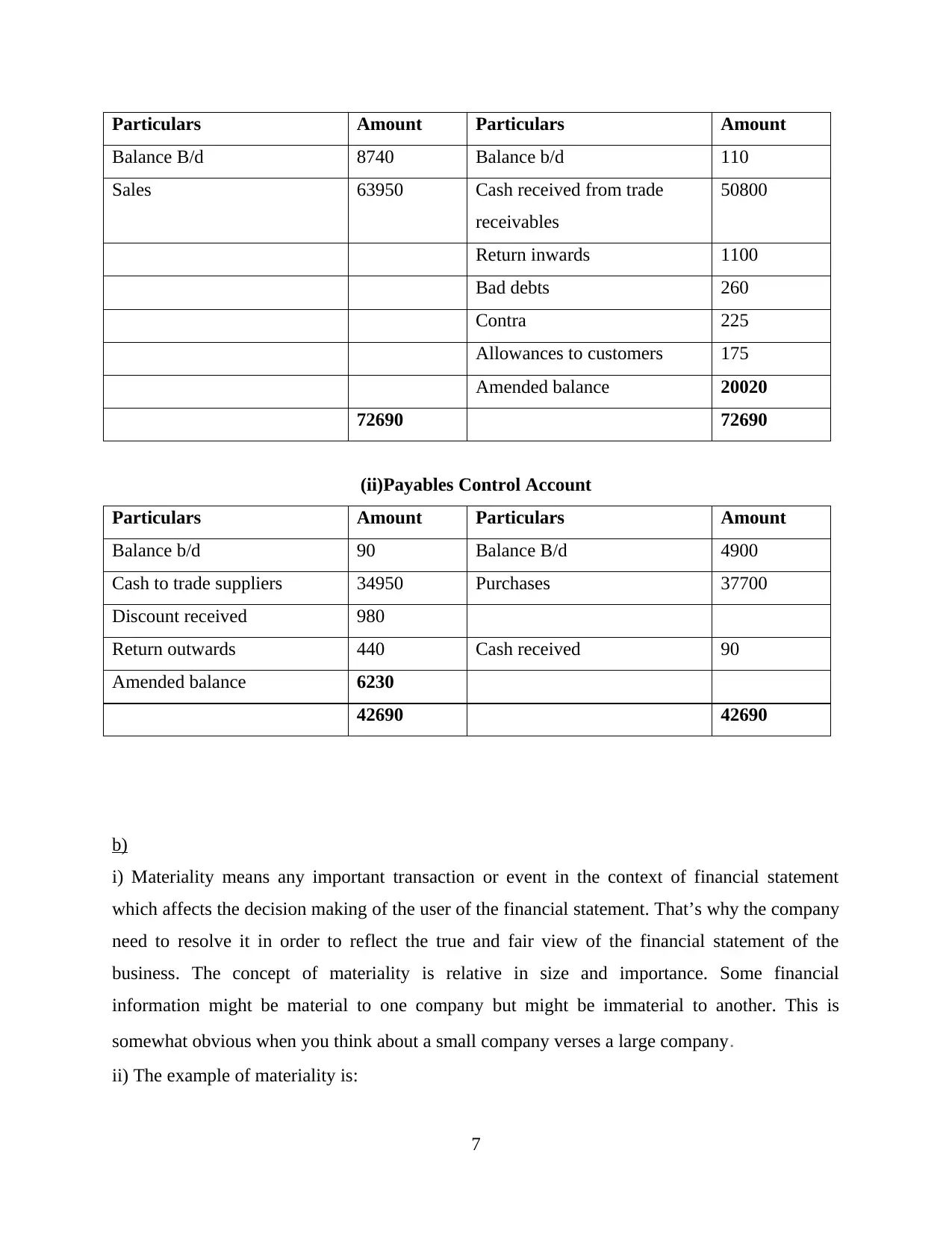

This financial accounting report provides a detailed analysis of Winston's financial statements, including the income statement for the year ended December 31, 2018, and the statement of financial position as of the same date. The report covers calculations related to sales revenue, cost of sales, gross profit, operating expenses, and net profit. It also includes an analysis of Winston's assets, liabilities, and capital, along with vehicle and disposal account details. Furthermore, the report discusses accounting concepts such as the going concern assumption and the advantages of limited liability companies. It also addresses inventory valuation using both the First-In, First-Out (FIFO) and Average Cost (AVCO) methods, along with a calculation of gross profit under each method and a discussion of when a product's net realizable value (NRV) is lower than its cost. Finally, the report includes receivables and payables control accounts and a discussion of materiality in financial statements, providing a comprehensive overview of key financial accounting principles and their application to a specific business scenario.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.