Financial Accounting: Detailed Analysis of Financial Statements

VerifiedAdded on 2023/06/05

|13

|882

|208

Report

AI Summary

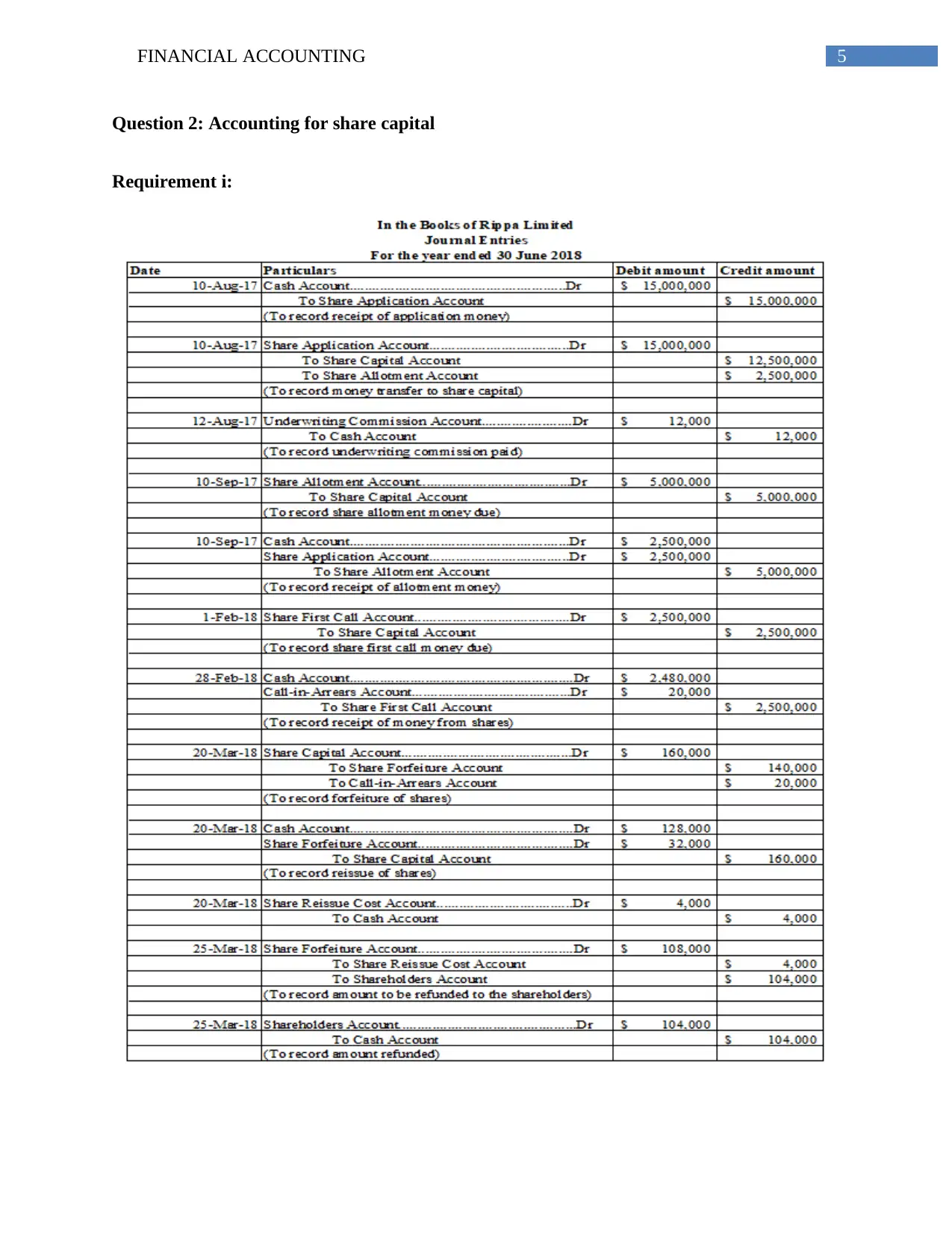

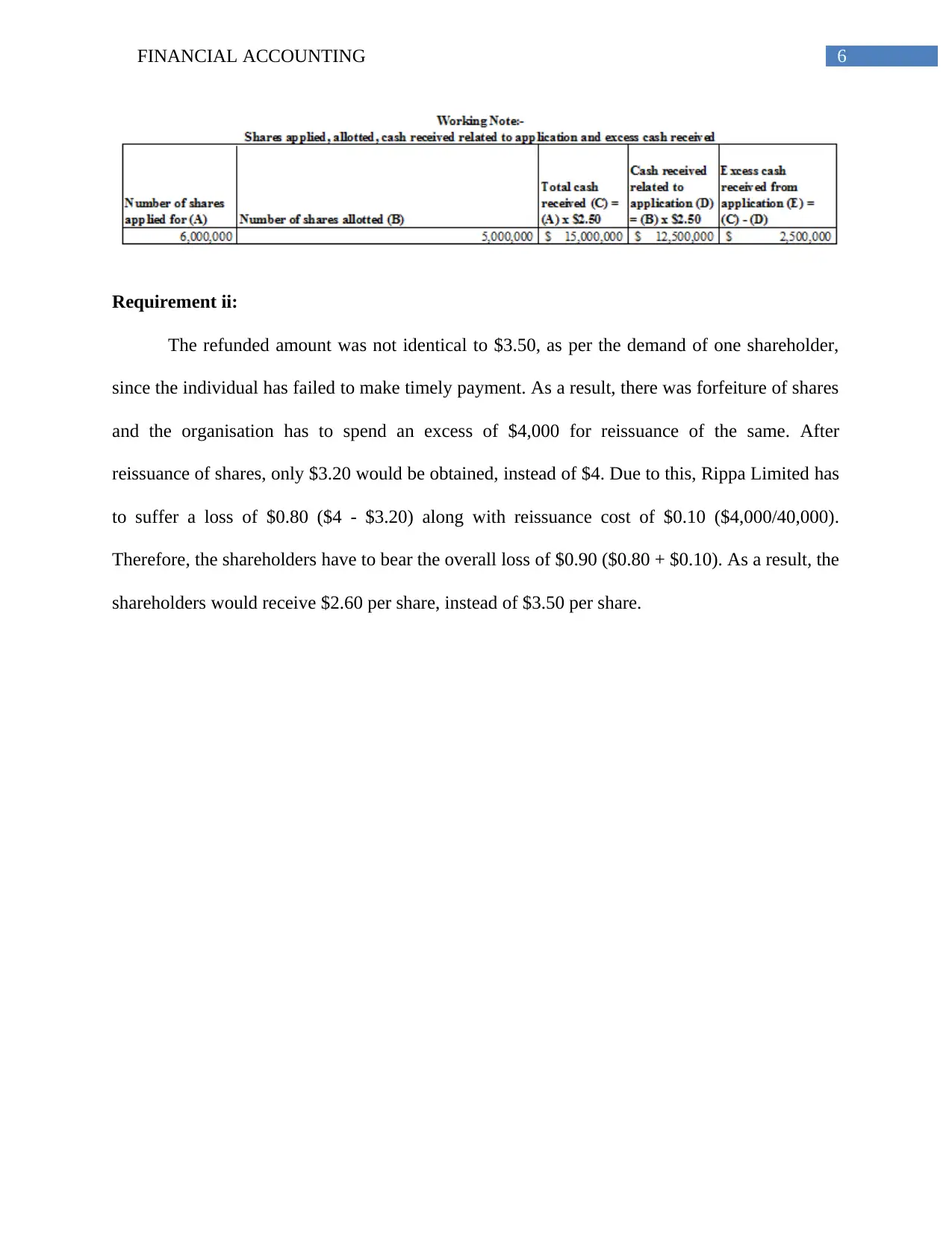

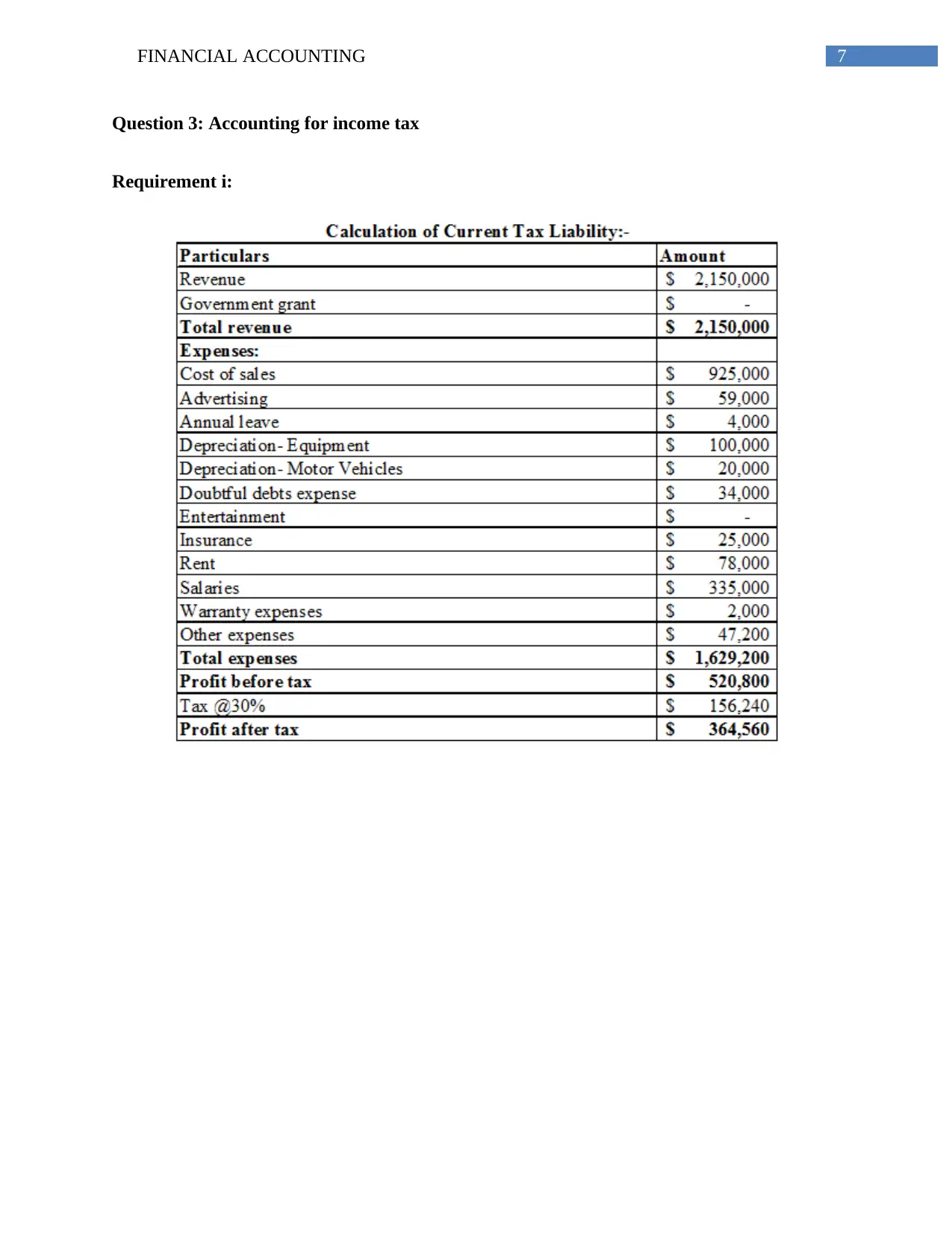

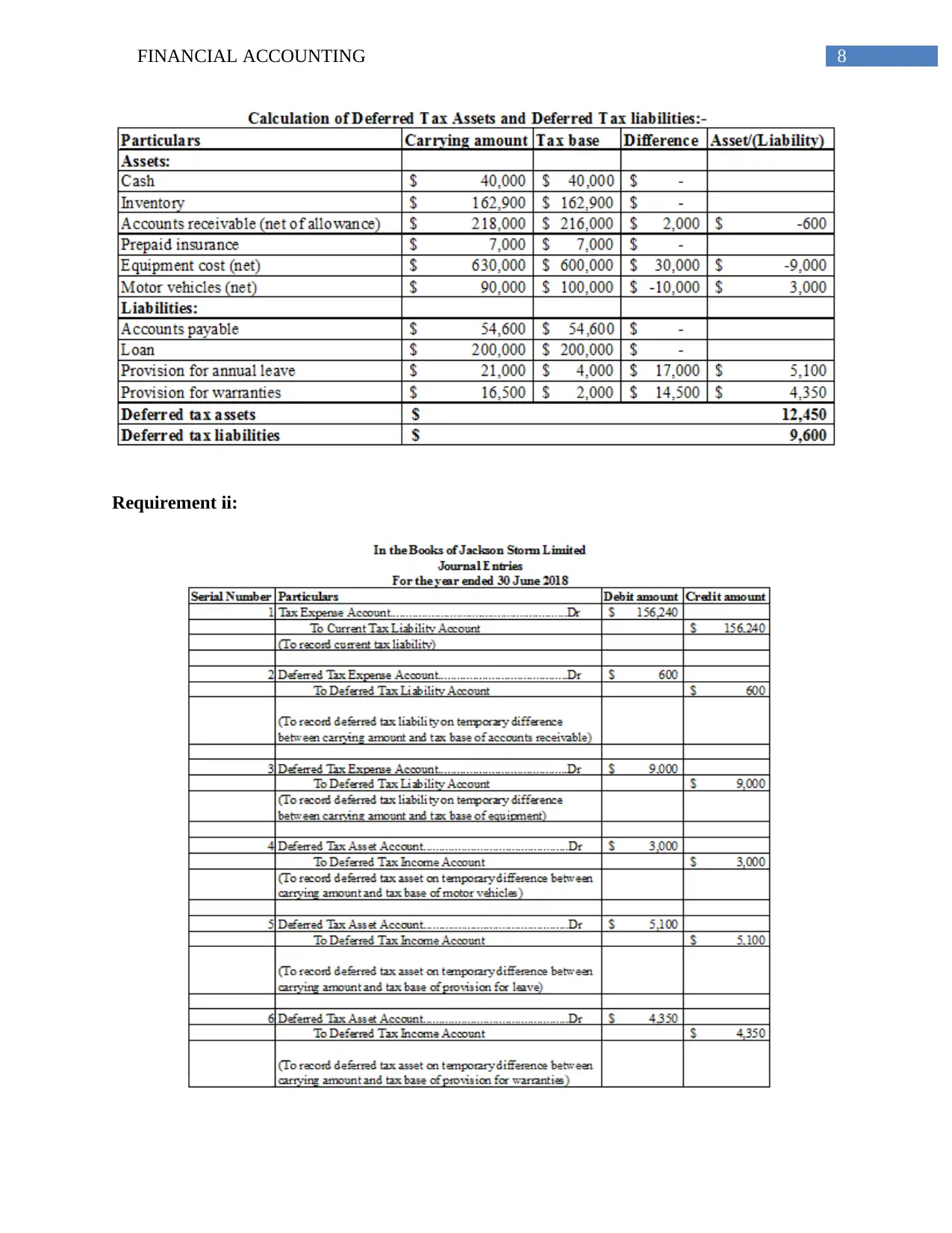

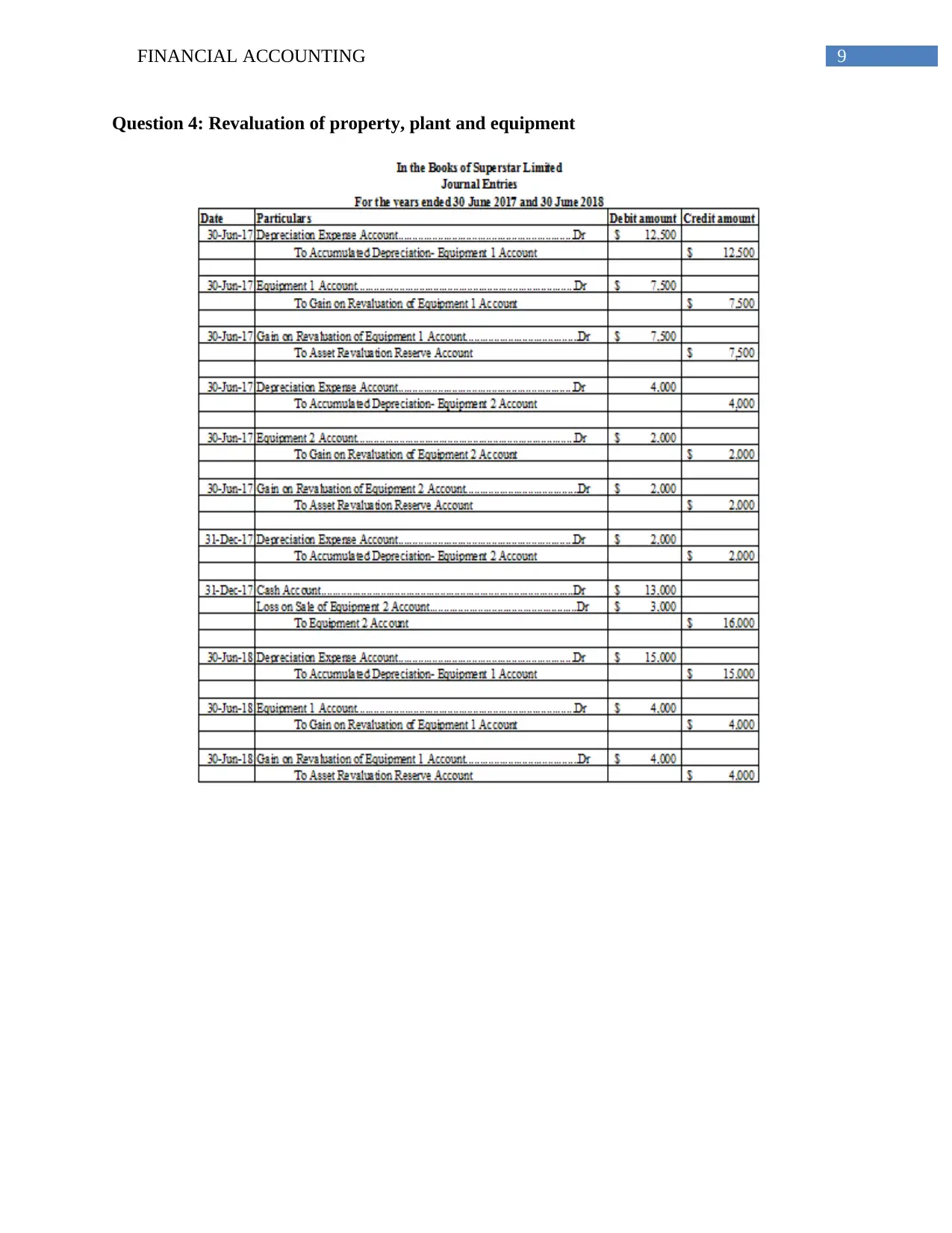

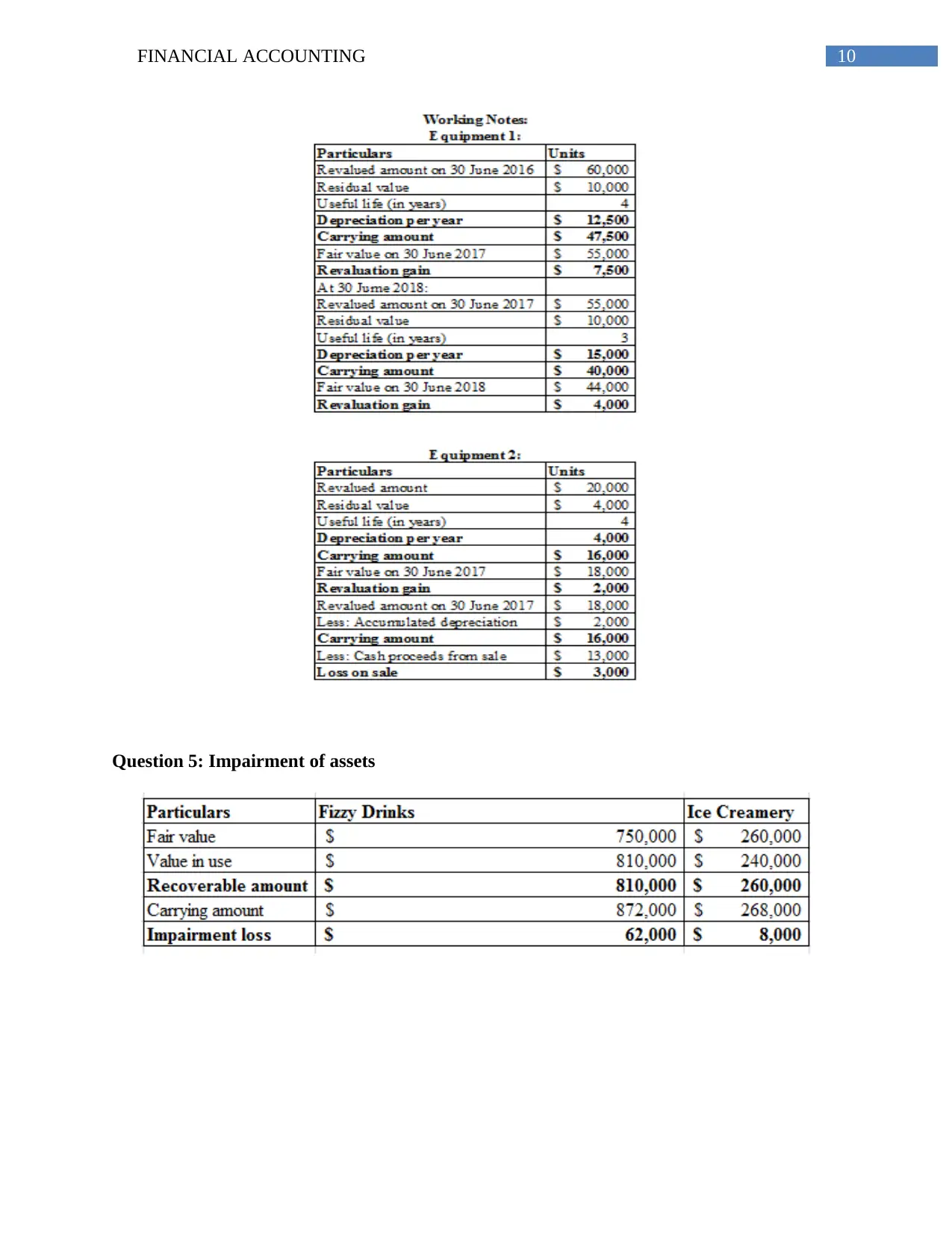

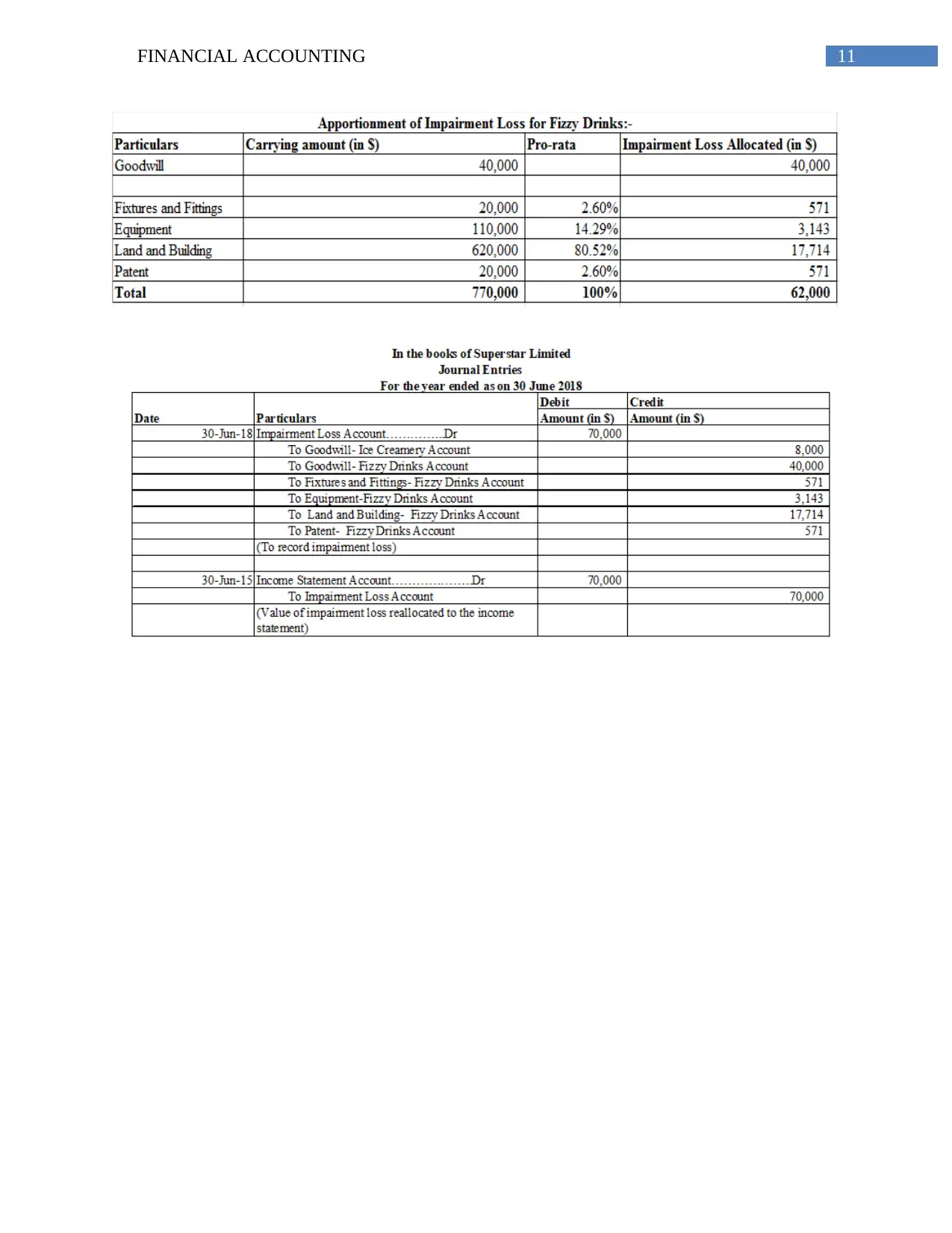

This financial accounting report covers several key areas including financial statement disclosures, accounting for share capital, accounting for income tax, revaluation of property, plant, and equipment, and impairment of assets. The report analyzes different scenarios related to financial statement disclosures, such as changes in asset useful life, unpaid repair expenses, investment value falls, and errors or fraud identification. It further discusses accounting for share capital, including share issuance and forfeiture. The report also delves into accounting for income tax, covering taxable and deductible temporary differences and deferred tax assets. Additionally, it addresses the revaluation of property, plant, and equipment and the impairment of assets, providing a comprehensive overview of these financial accounting topics. Desklib provides access to this and other solved assignments.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.