Financial Accounting Assignment: Bob's Account Analysis

VerifiedAdded on 2023/01/09

|13

|3300

|84

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial accounting assignment, addressing key concepts and practical applications. The solution begins with the preparation of financial statements, including trading accounts, profit and loss statements, and balance sheets, using data from Bob Peterson's fabric shop. It then delves into the analysis of financial ratios, such as gross profit margin, return on capital employed, and current ratio, interpreting their implications for business performance. Furthermore, the assignment explores bank account write-ups and the application of depreciation methods, specifically the straight-line method, to machinery accounts. The solution provides detailed calculations, interpretations, and explanations, covering essential aspects of financial accounting principles.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

QUESTION 1..............................................................................................................................................3

(A) Financial statement of Bob’s account................................................................................................3

(b) Three main features of information for users of financial statements.................................................4

QUESTION 2..............................................................................................................................................6

(2a) Calculation of ratio and interpretation..............................................................................................6

(2b) Business bank..................................................................................................................................8

(2c) Depreciation of machinery account..................................................................................................8

CONCLUSION.........................................................................................................................................10

REFERENCES..........................................................................................................................................11

INTRODUCTION.......................................................................................................................................3

QUESTION 1..............................................................................................................................................3

(A) Financial statement of Bob’s account................................................................................................3

(b) Three main features of information for users of financial statements.................................................4

QUESTION 2..............................................................................................................................................6

(2a) Calculation of ratio and interpretation..............................................................................................6

(2b) Business bank..................................................................................................................................8

(2c) Depreciation of machinery account..................................................................................................8

CONCLUSION.........................................................................................................................................10

REFERENCES..........................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is a broad concept with a range of tasks consisting of tracking,

analyzing and resubmitting the effects of these reports to consumers. The activities affected are

material to the financial statements. It’s used to prepare financial statements such as the balance

sheet, income statement and cash flow statement for the purpose of revealing the market

reputation and performance over a specific period of time that is usually yearly. Accurately,

financial accounting concerns the creation of such documents, which are centered on reliable

information and obey "Generally Accepted Accounting Principles" (anything else recognized as

GAAP). GAAP sets knowledge management on even a broad variety of subjects in the United

States, namely financial statement analysis (Anantharaman, 2017). The main aim is to present

these reports to the shareholders as their money is invested in the organization. In this report

consist of year end accounts, main features of information which are beneficial for the users.

Along with, calculate different types of financial ratio and interpret them to analysis the financial

position of business and write up bank account in each month. Moreover, apply different method

of depreciation and know different accounting concepts.

QUESTION 1

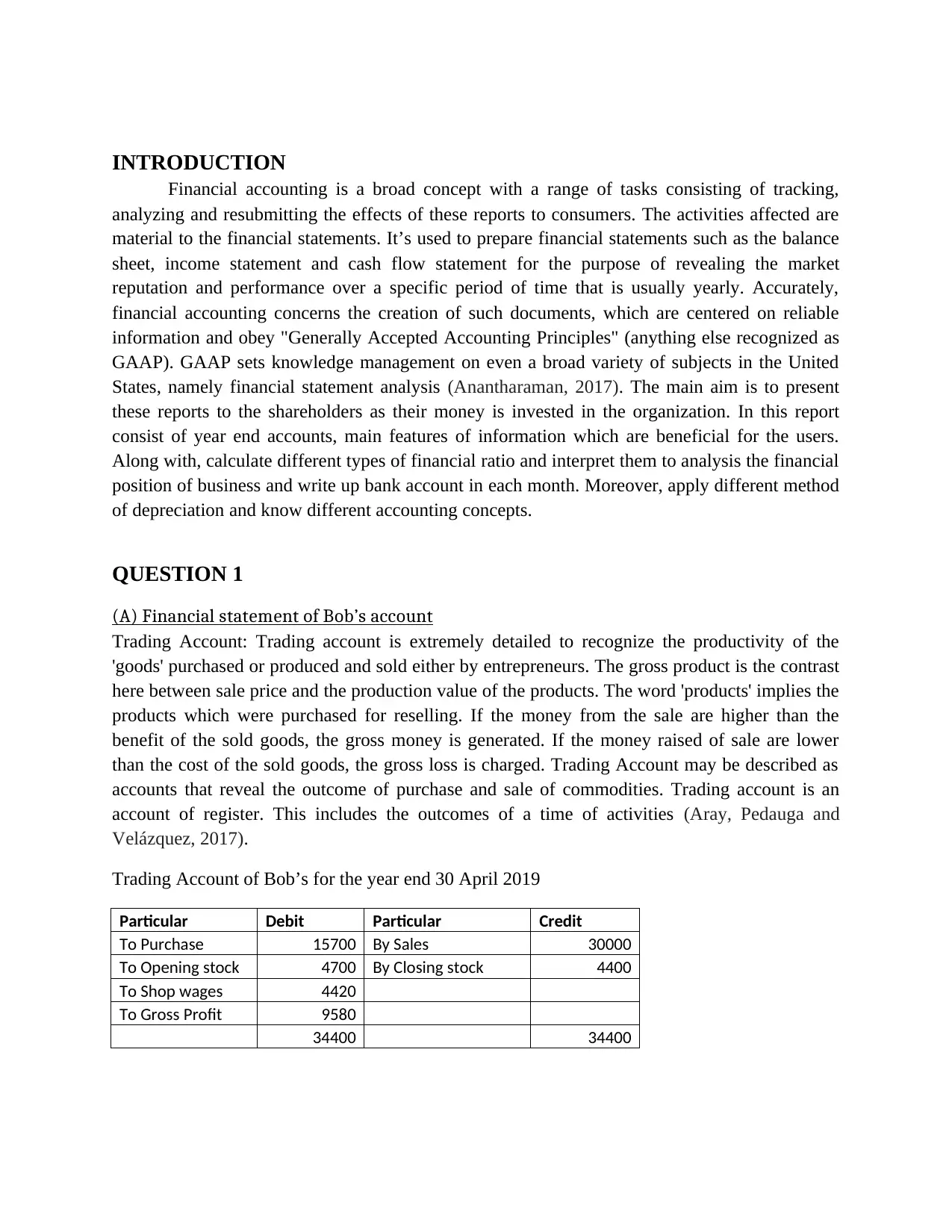

(A) Financial statement of Bob’s account

Trading Account: Trading account is extremely detailed to recognize the productivity of the

'goods' purchased or produced and sold either by entrepreneurs. The gross product is the contrast

here between sale price and the production value of the products. The word 'products' implies the

products which were purchased for reselling. If the money from the sale are higher than the

benefit of the sold goods, the gross money is generated. If the money raised of sale are lower

than the cost of the sold goods, the gross loss is charged. Trading Account may be described as

accounts that reveal the outcome of purchase and sale of commodities. Trading account is an

account of register. This includes the outcomes of a time of activities (Aray, Pedauga and

Velázquez, 2017).

Trading Account of Bob’s for the year end 30 April 2019

Particular Debit Particular Credit

To Purchase 15700 By Sales 30000

To Opening stock 4700 By Closing stock 4400

To Shop wages 4420

To Gross Profit 9580

34400 34400

Financial accounting is a broad concept with a range of tasks consisting of tracking,

analyzing and resubmitting the effects of these reports to consumers. The activities affected are

material to the financial statements. It’s used to prepare financial statements such as the balance

sheet, income statement and cash flow statement for the purpose of revealing the market

reputation and performance over a specific period of time that is usually yearly. Accurately,

financial accounting concerns the creation of such documents, which are centered on reliable

information and obey "Generally Accepted Accounting Principles" (anything else recognized as

GAAP). GAAP sets knowledge management on even a broad variety of subjects in the United

States, namely financial statement analysis (Anantharaman, 2017). The main aim is to present

these reports to the shareholders as their money is invested in the organization. In this report

consist of year end accounts, main features of information which are beneficial for the users.

Along with, calculate different types of financial ratio and interpret them to analysis the financial

position of business and write up bank account in each month. Moreover, apply different method

of depreciation and know different accounting concepts.

QUESTION 1

(A) Financial statement of Bob’s account

Trading Account: Trading account is extremely detailed to recognize the productivity of the

'goods' purchased or produced and sold either by entrepreneurs. The gross product is the contrast

here between sale price and the production value of the products. The word 'products' implies the

products which were purchased for reselling. If the money from the sale are higher than the

benefit of the sold goods, the gross money is generated. If the money raised of sale are lower

than the cost of the sold goods, the gross loss is charged. Trading Account may be described as

accounts that reveal the outcome of purchase and sale of commodities. Trading account is an

account of register. This includes the outcomes of a time of activities (Aray, Pedauga and

Velázquez, 2017).

Trading Account of Bob’s for the year end 30 April 2019

Particular Debit Particular Credit

To Purchase 15700 By Sales 30000

To Opening stock 4700 By Closing stock 4400

To Shop wages 4420

To Gross Profit 9580

34400 34400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

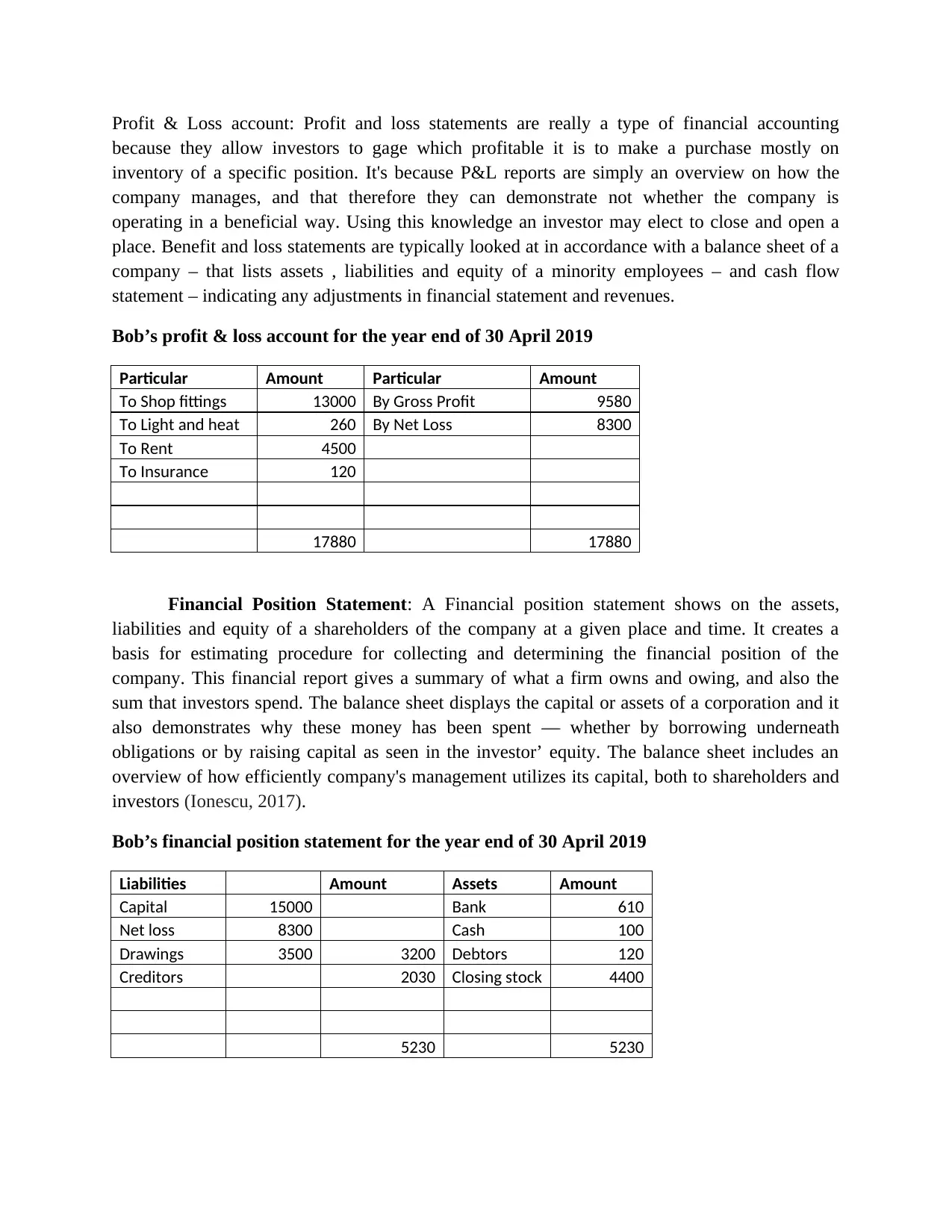

Profit & Loss account: Profit and loss statements are really a type of financial accounting

because they allow investors to gage which profitable it is to make a purchase mostly on

inventory of a specific position. It's because P&L reports are simply an overview on how the

company manages, and that therefore they can demonstrate not whether the company is

operating in a beneficial way. Using this knowledge an investor may elect to close and open a

place. Benefit and loss statements are typically looked at in accordance with a balance sheet of a

company – that lists assets , liabilities and equity of a minority employees – and cash flow

statement – indicating any adjustments in financial statement and revenues.

Bob’s profit & loss account for the year end of 30 April 2019

Particular Amount Particular Amount

To Shop fittings 13000 By Gross Profit 9580

To Light and heat 260 By Net Loss 8300

To Rent 4500

To Insurance 120

17880 17880

Financial Position Statement: A Financial position statement shows on the assets,

liabilities and equity of a shareholders of the company at a given place and time. It creates a

basis for estimating procedure for collecting and determining the financial position of the

company. This financial report gives a summary of what a firm owns and owing, and also the

sum that investors spend. The balance sheet displays the capital or assets of a corporation and it

also demonstrates why these money has been spent — whether by borrowing underneath

obligations or by raising capital as seen in the investor’ equity. The balance sheet includes an

overview of how efficiently company's management utilizes its capital, both to shareholders and

investors (Ionescu, 2017).

Bob’s financial position statement for the year end of 30 April 2019

Liabilities Amount Assets Amount

Capital 15000 Bank 610

Net loss 8300 Cash 100

Drawings 3500 3200 Debtors 120

Creditors 2030 Closing stock 4400

5230 5230

because they allow investors to gage which profitable it is to make a purchase mostly on

inventory of a specific position. It's because P&L reports are simply an overview on how the

company manages, and that therefore they can demonstrate not whether the company is

operating in a beneficial way. Using this knowledge an investor may elect to close and open a

place. Benefit and loss statements are typically looked at in accordance with a balance sheet of a

company – that lists assets , liabilities and equity of a minority employees – and cash flow

statement – indicating any adjustments in financial statement and revenues.

Bob’s profit & loss account for the year end of 30 April 2019

Particular Amount Particular Amount

To Shop fittings 13000 By Gross Profit 9580

To Light and heat 260 By Net Loss 8300

To Rent 4500

To Insurance 120

17880 17880

Financial Position Statement: A Financial position statement shows on the assets,

liabilities and equity of a shareholders of the company at a given place and time. It creates a

basis for estimating procedure for collecting and determining the financial position of the

company. This financial report gives a summary of what a firm owns and owing, and also the

sum that investors spend. The balance sheet displays the capital or assets of a corporation and it

also demonstrates why these money has been spent — whether by borrowing underneath

obligations or by raising capital as seen in the investor’ equity. The balance sheet includes an

overview of how efficiently company's management utilizes its capital, both to shareholders and

investors (Ionescu, 2017).

Bob’s financial position statement for the year end of 30 April 2019

Liabilities Amount Assets Amount

Capital 15000 Bank 610

Net loss 8300 Cash 100

Drawings 3500 3200 Debtors 120

Creditors 2030 Closing stock 4400

5230 5230

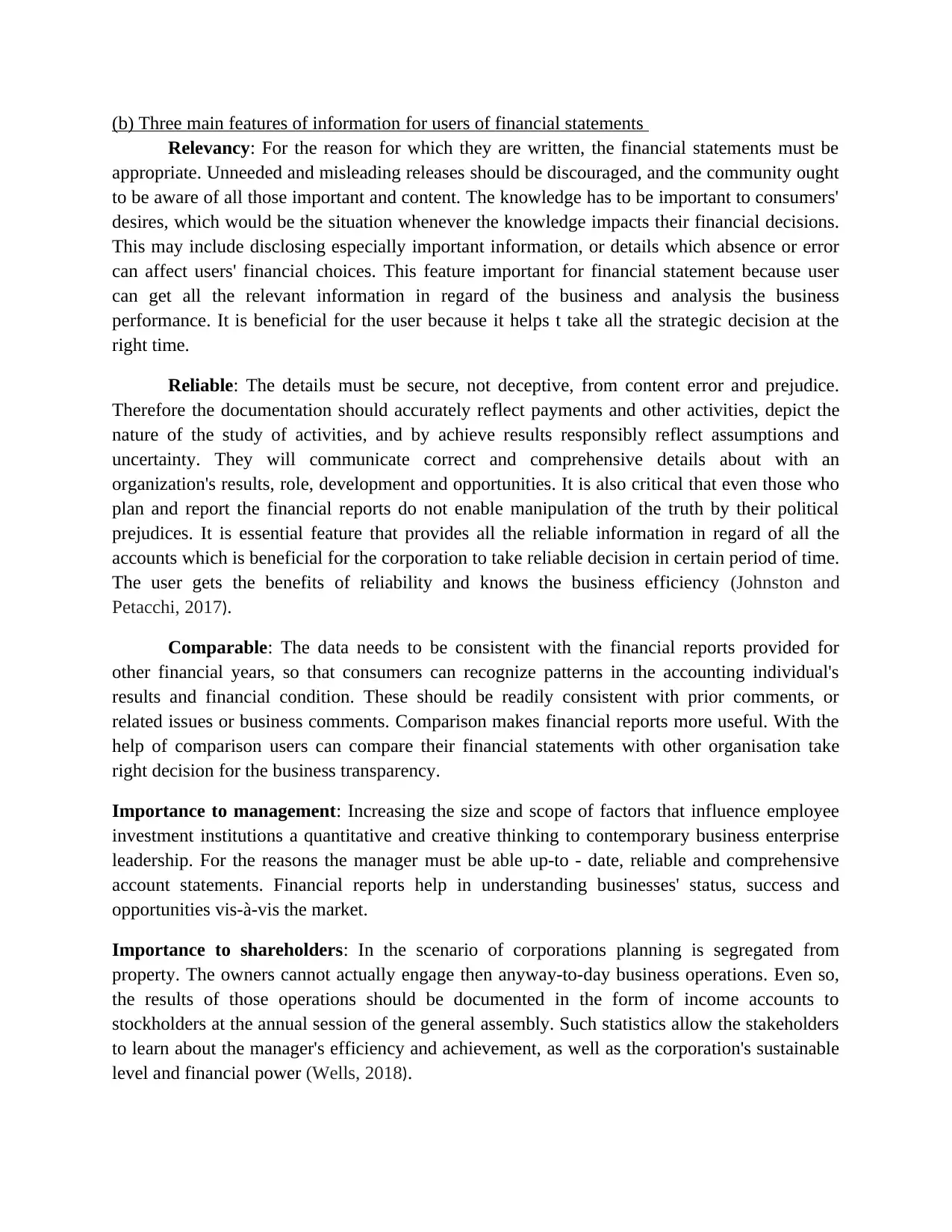

(b) Three main features of information for users of financial statements

Relevancy: For the reason for which they are written, the financial statements must be

appropriate. Unneeded and misleading releases should be discouraged, and the community ought

to be aware of all those important and content. The knowledge has to be important to consumers'

desires, which would be the situation whenever the knowledge impacts their financial decisions.

This may include disclosing especially important information, or details which absence or error

can affect users' financial choices. This feature important for financial statement because user

can get all the relevant information in regard of the business and analysis the business

performance. It is beneficial for the user because it helps t take all the strategic decision at the

right time.

Reliable: The details must be secure, not deceptive, from content error and prejudice.

Therefore the documentation should accurately reflect payments and other activities, depict the

nature of the study of activities, and by achieve results responsibly reflect assumptions and

uncertainty. They will communicate correct and comprehensive details about with an

organization's results, role, development and opportunities. It is also critical that even those who

plan and report the financial reports do not enable manipulation of the truth by their political

prejudices. It is essential feature that provides all the reliable information in regard of all the

accounts which is beneficial for the corporation to take reliable decision in certain period of time.

The user gets the benefits of reliability and knows the business efficiency (Johnston and

Petacchi, 2017).

Comparable: The data needs to be consistent with the financial reports provided for

other financial years, so that consumers can recognize patterns in the accounting individual's

results and financial condition. These should be readily consistent with prior comments, or

related issues or business comments. Comparison makes financial reports more useful. With the

help of comparison users can compare their financial statements with other organisation take

right decision for the business transparency.

Importance to management: Increasing the size and scope of factors that influence employee

investment institutions a quantitative and creative thinking to contemporary business enterprise

leadership. For the reasons the manager must be able up-to - date, reliable and comprehensive

account statements. Financial reports help in understanding businesses' status, success and

opportunities vis-à-vis the market.

Importance to shareholders: In the scenario of corporations planning is segregated from

property. The owners cannot actually engage then anyway-to-day business operations. Even so,

the results of those operations should be documented in the form of income accounts to

stockholders at the annual session of the general assembly. Such statistics allow the stakeholders

to learn about the manager's efficiency and achievement, as well as the corporation's sustainable

level and financial power (Wells, 2018).

Relevancy: For the reason for which they are written, the financial statements must be

appropriate. Unneeded and misleading releases should be discouraged, and the community ought

to be aware of all those important and content. The knowledge has to be important to consumers'

desires, which would be the situation whenever the knowledge impacts their financial decisions.

This may include disclosing especially important information, or details which absence or error

can affect users' financial choices. This feature important for financial statement because user

can get all the relevant information in regard of the business and analysis the business

performance. It is beneficial for the user because it helps t take all the strategic decision at the

right time.

Reliable: The details must be secure, not deceptive, from content error and prejudice.

Therefore the documentation should accurately reflect payments and other activities, depict the

nature of the study of activities, and by achieve results responsibly reflect assumptions and

uncertainty. They will communicate correct and comprehensive details about with an

organization's results, role, development and opportunities. It is also critical that even those who

plan and report the financial reports do not enable manipulation of the truth by their political

prejudices. It is essential feature that provides all the reliable information in regard of all the

accounts which is beneficial for the corporation to take reliable decision in certain period of time.

The user gets the benefits of reliability and knows the business efficiency (Johnston and

Petacchi, 2017).

Comparable: The data needs to be consistent with the financial reports provided for

other financial years, so that consumers can recognize patterns in the accounting individual's

results and financial condition. These should be readily consistent with prior comments, or

related issues or business comments. Comparison makes financial reports more useful. With the

help of comparison users can compare their financial statements with other organisation take

right decision for the business transparency.

Importance to management: Increasing the size and scope of factors that influence employee

investment institutions a quantitative and creative thinking to contemporary business enterprise

leadership. For the reasons the manager must be able up-to - date, reliable and comprehensive

account statements. Financial reports help in understanding businesses' status, success and

opportunities vis-à-vis the market.

Importance to shareholders: In the scenario of corporations planning is segregated from

property. The owners cannot actually engage then anyway-to-day business operations. Even so,

the results of those operations should be documented in the form of income accounts to

stockholders at the annual session of the general assembly. Such statistics allow the stakeholders

to learn about the manager's efficiency and achievement, as well as the corporation's sustainable

level and financial power (Wells, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

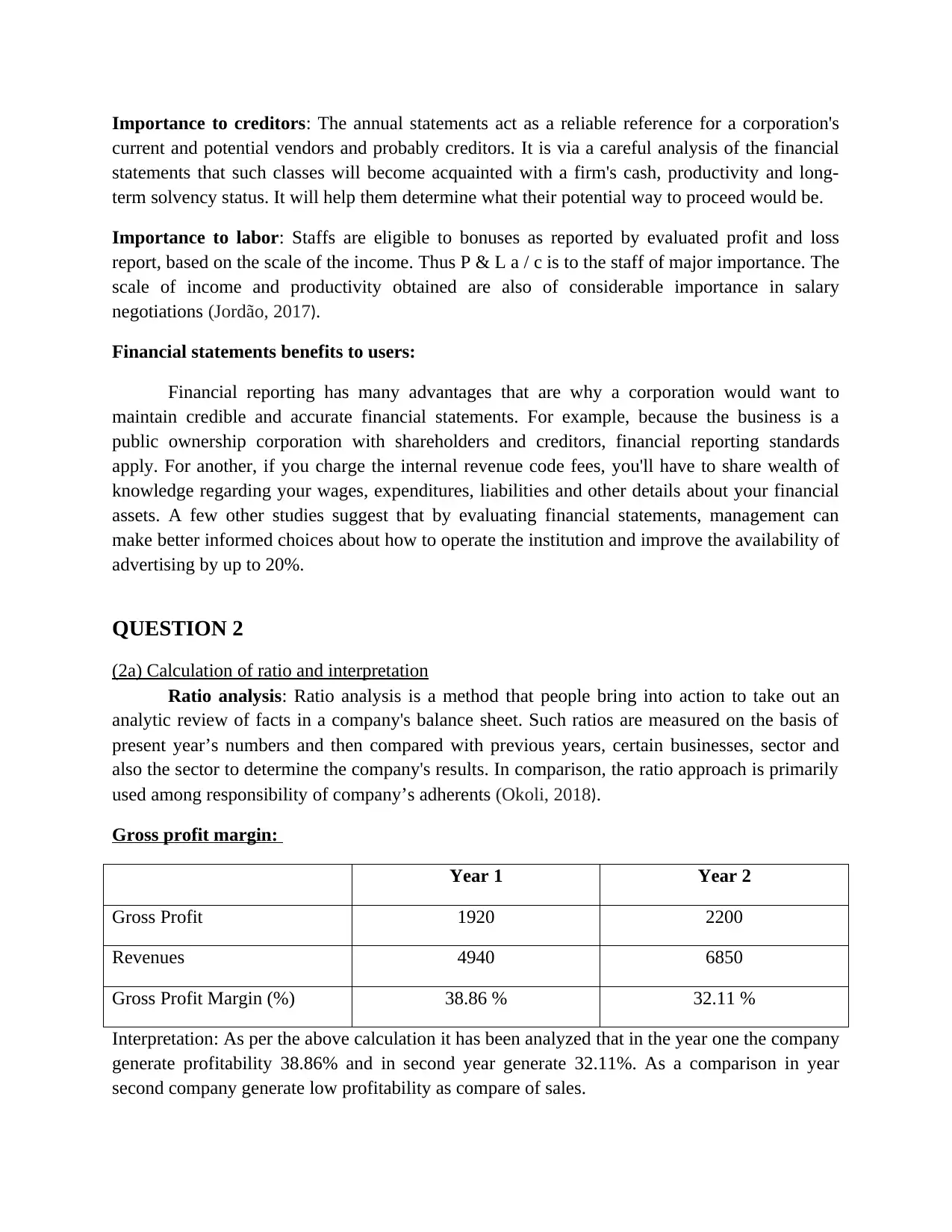

Importance to creditors: The annual statements act as a reliable reference for a corporation's

current and potential vendors and probably creditors. It is via a careful analysis of the financial

statements that such classes will become acquainted with a firm's cash, productivity and long-

term solvency status. It will help them determine what their potential way to proceed would be.

Importance to labor: Staffs are eligible to bonuses as reported by evaluated profit and loss

report, based on the scale of the income. Thus P & L a / c is to the staff of major importance. The

scale of income and productivity obtained are also of considerable importance in salary

negotiations (Jordão, 2017).

Financial statements benefits to users:

Financial reporting has many advantages that are why a corporation would want to

maintain credible and accurate financial statements. For example, because the business is a

public ownership corporation with shareholders and creditors, financial reporting standards

apply. For another, if you charge the internal revenue code fees, you'll have to share wealth of

knowledge regarding your wages, expenditures, liabilities and other details about your financial

assets. A few other studies suggest that by evaluating financial statements, management can

make better informed choices about how to operate the institution and improve the availability of

advertising by up to 20%.

QUESTION 2

(2a) Calculation of ratio and interpretation

Ratio analysis: Ratio analysis is a method that people bring into action to take out an

analytic review of facts in a company's balance sheet. Such ratios are measured on the basis of

present year’s numbers and then compared with previous years, certain businesses, sector and

also the sector to determine the company's results. In comparison, the ratio approach is primarily

used among responsibility of company’s adherents (Okoli, 2018).

Gross profit margin:

Year 1 Year 2

Gross Profit 1920 2200

Revenues 4940 6850

Gross Profit Margin (%) 38.86 % 32.11 %

Interpretation: As per the above calculation it has been analyzed that in the year one the company

generate profitability 38.86% and in second year generate 32.11%. As a comparison in year

second company generate low profitability as compare of sales.

current and potential vendors and probably creditors. It is via a careful analysis of the financial

statements that such classes will become acquainted with a firm's cash, productivity and long-

term solvency status. It will help them determine what their potential way to proceed would be.

Importance to labor: Staffs are eligible to bonuses as reported by evaluated profit and loss

report, based on the scale of the income. Thus P & L a / c is to the staff of major importance. The

scale of income and productivity obtained are also of considerable importance in salary

negotiations (Jordão, 2017).

Financial statements benefits to users:

Financial reporting has many advantages that are why a corporation would want to

maintain credible and accurate financial statements. For example, because the business is a

public ownership corporation with shareholders and creditors, financial reporting standards

apply. For another, if you charge the internal revenue code fees, you'll have to share wealth of

knowledge regarding your wages, expenditures, liabilities and other details about your financial

assets. A few other studies suggest that by evaluating financial statements, management can

make better informed choices about how to operate the institution and improve the availability of

advertising by up to 20%.

QUESTION 2

(2a) Calculation of ratio and interpretation

Ratio analysis: Ratio analysis is a method that people bring into action to take out an

analytic review of facts in a company's balance sheet. Such ratios are measured on the basis of

present year’s numbers and then compared with previous years, certain businesses, sector and

also the sector to determine the company's results. In comparison, the ratio approach is primarily

used among responsibility of company’s adherents (Okoli, 2018).

Gross profit margin:

Year 1 Year 2

Gross Profit 1920 2200

Revenues 4940 6850

Gross Profit Margin (%) 38.86 % 32.11 %

Interpretation: As per the above calculation it has been analyzed that in the year one the company

generate profitability 38.86% and in second year generate 32.11%. As a comparison in year

second company generate low profitability as compare of sales.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

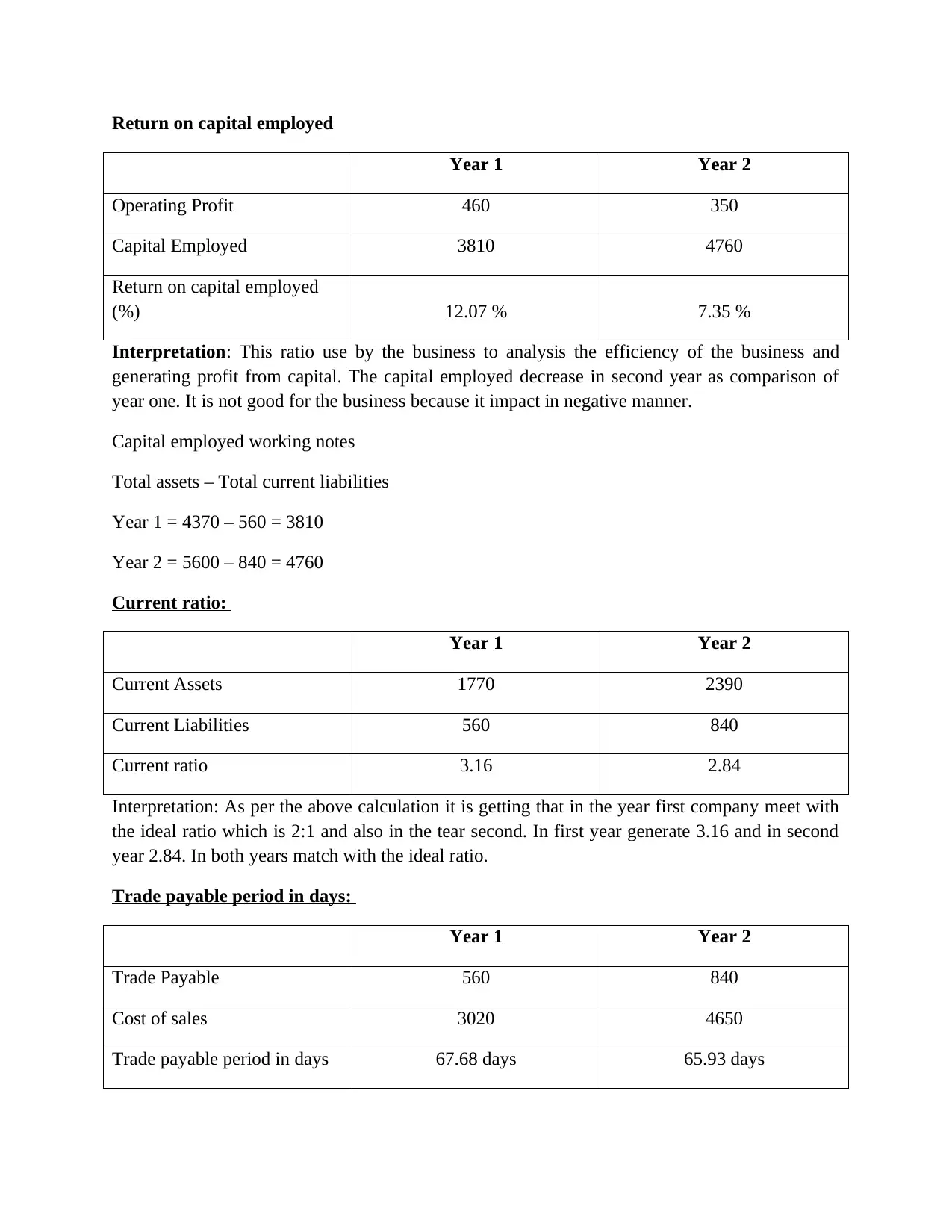

Return on capital employed

Year 1 Year 2

Operating Profit 460 350

Capital Employed 3810 4760

Return on capital employed

(%) 12.07 % 7.35 %

Interpretation: This ratio use by the business to analysis the efficiency of the business and

generating profit from capital. The capital employed decrease in second year as comparison of

year one. It is not good for the business because it impact in negative manner.

Capital employed working notes

Total assets – Total current liabilities

Year 1 = 4370 – 560 = 3810

Year 2 = 5600 – 840 = 4760

Current ratio:

Year 1 Year 2

Current Assets 1770 2390

Current Liabilities 560 840

Current ratio 3.16 2.84

Interpretation: As per the above calculation it is getting that in the year first company meet with

the ideal ratio which is 2:1 and also in the tear second. In first year generate 3.16 and in second

year 2.84. In both years match with the ideal ratio.

Trade payable period in days:

Year 1 Year 2

Trade Payable 560 840

Cost of sales 3020 4650

Trade payable period in days 67.68 days 65.93 days

Year 1 Year 2

Operating Profit 460 350

Capital Employed 3810 4760

Return on capital employed

(%) 12.07 % 7.35 %

Interpretation: This ratio use by the business to analysis the efficiency of the business and

generating profit from capital. The capital employed decrease in second year as comparison of

year one. It is not good for the business because it impact in negative manner.

Capital employed working notes

Total assets – Total current liabilities

Year 1 = 4370 – 560 = 3810

Year 2 = 5600 – 840 = 4760

Current ratio:

Year 1 Year 2

Current Assets 1770 2390

Current Liabilities 560 840

Current ratio 3.16 2.84

Interpretation: As per the above calculation it is getting that in the year first company meet with

the ideal ratio which is 2:1 and also in the tear second. In first year generate 3.16 and in second

year 2.84. In both years match with the ideal ratio.

Trade payable period in days:

Year 1 Year 2

Trade Payable 560 840

Cost of sales 3020 4650

Trade payable period in days 67.68 days 65.93 days

Interpretation: As per the above table it understands that the organisation can pay amount in the

67.78 days in first year but in second year it decrease and reach on 65.93 days that is not good

for the business entity.

Trade receivable period

Year 1 Year 2

Trade receivable 820 1230

Total sales 4940 6850

Trade receivable period 60.59 days 65.54 days

Interpretation: From the above computation it is analyzing that in first year company receive

mount from the debtors in 60.59 days but in second year it increase and reach on 65.54 days

which is not good for the business and impact on the liquidity position.

(2b) Business bank

Write up other accounts

(1) March account

Date Particulars Debit Credit Balance

March, 1 Opening balance 500 500

March, 1 Bought goods for

sale

150 350

March, 5 Paid rent 50 300

March, 10 Business taking

to date

290 590

March, 22 Paid for

advertising

25 565

March, 26 Thompson

drawings

100 465

March, 27 Business takings 240 705

705

April account

Date Particulars Debit Credit Balance

April, 1 Opening balance 705 705

April, 2 Bought goods for

resale

100 605

April, 5 Paid rent 50 555

67.78 days in first year but in second year it decrease and reach on 65.93 days that is not good

for the business entity.

Trade receivable period

Year 1 Year 2

Trade receivable 820 1230

Total sales 4940 6850

Trade receivable period 60.59 days 65.54 days

Interpretation: From the above computation it is analyzing that in first year company receive

mount from the debtors in 60.59 days but in second year it increase and reach on 65.54 days

which is not good for the business and impact on the liquidity position.

(2b) Business bank

Write up other accounts

(1) March account

Date Particulars Debit Credit Balance

March, 1 Opening balance 500 500

March, 1 Bought goods for

sale

150 350

March, 5 Paid rent 50 300

March, 10 Business taking

to date

290 590

March, 22 Paid for

advertising

25 565

March, 26 Thompson

drawings

100 465

March, 27 Business takings 240 705

705

April account

Date Particulars Debit Credit Balance

April, 1 Opening balance 705 705

April, 2 Bought goods for

resale

100 605

April, 5 Paid rent 50 555

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

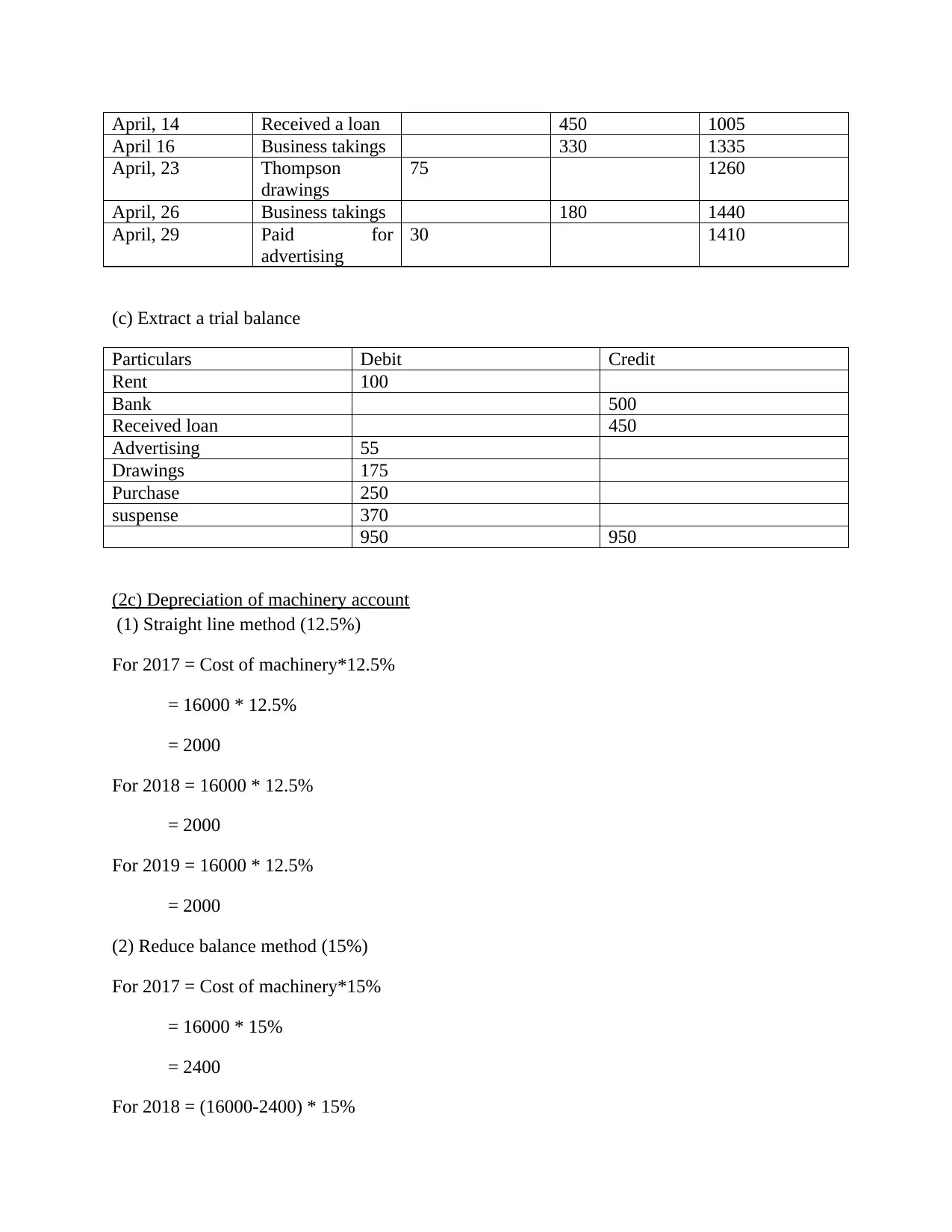

April, 14 Received a loan 450 1005

April 16 Business takings 330 1335

April, 23 Thompson

drawings

75 1260

April, 26 Business takings 180 1440

April, 29 Paid for

advertising

30 1410

(c) Extract a trial balance

Particulars Debit Credit

Rent 100

Bank 500

Received loan 450

Advertising 55

Drawings 175

Purchase 250

suspense 370

950 950

(2c) Depreciation of machinery account

(1) Straight line method (12.5%)

For 2017 = Cost of machinery*12.5%

= 16000 * 12.5%

= 2000

For 2018 = 16000 * 12.5%

= 2000

For 2019 = 16000 * 12.5%

= 2000

(2) Reduce balance method (15%)

For 2017 = Cost of machinery*15%

= 16000 * 15%

= 2400

For 2018 = (16000-2400) * 15%

April 16 Business takings 330 1335

April, 23 Thompson

drawings

75 1260

April, 26 Business takings 180 1440

April, 29 Paid for

advertising

30 1410

(c) Extract a trial balance

Particulars Debit Credit

Rent 100

Bank 500

Received loan 450

Advertising 55

Drawings 175

Purchase 250

suspense 370

950 950

(2c) Depreciation of machinery account

(1) Straight line method (12.5%)

For 2017 = Cost of machinery*12.5%

= 16000 * 12.5%

= 2000

For 2018 = 16000 * 12.5%

= 2000

For 2019 = 16000 * 12.5%

= 2000

(2) Reduce balance method (15%)

For 2017 = Cost of machinery*15%

= 16000 * 15%

= 2400

For 2018 = (16000-2400) * 15%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 13600*15%

= 2040

For 2019 = (13600-2040) * 15%

= 11560 * 15%

= 1734

(3) Accounting concepts

Going concern: Going concern is an accounting concept for a business that has the

capital necessary to begin to function continuously before verification of the opposite is given.

The word also applies to the willingness of an organization to raise enough profit to remain alive

or escape default. If a company is not a company, it means it has declared bankruptcy, and its

resources have been forced to liquidate. Accounting professionals use the standards of going

concern to assess which forms of disclosure will surface on the financial statements.

Organizations that are an ongoing concern can delay recording of long-term assets at original

cost or liquidation price, however at cost more. A business retains an ongoing problem unless the

disposal of property does not hinder its strength to conduct operating, such as the closing of a

small branch manager that due to complete staff to many other business units (Sledgianowski,

Gomaa and Tan, 2017).

Materiality: Exchanges should be reported as failure to do so could change a reader's

financial reports judgments. It thought to occur in extremely small expenditures becoming

reported, such that a firm's financial performance, financial condition, and cash flows are

accurately reported in the financial reports. The definition or principle of materiality is an

accounting law that specifies all payments or products that have a major material effect on the

financial should be compensated for solely utilizing GAAP. In other terms, if a payment or

incident occurs for the year that might impact how the business will be perceived by a

shareholder it must be reported for using GAAP on the income statement (Tinoco, Holmes and

Wilson, 2018).

Business entity concept: The business entity property implies that the payments relevant

to a company must be finding a variety from that of its shareholders or other entities. To do so

includes the use in the company of different financial statements which fully exempt some other

organization or landlord's income and expenses. Under this definition, numerous entities' records

will be mixed, making it very difficult to distinguish the economic or taxation performance of a

particular enterprise (Umar, 2017). The company entity definition has a variety of explanations

such as:

Each commercial entity is exempted from tax

= 2040

For 2019 = (13600-2040) * 15%

= 11560 * 15%

= 1734

(3) Accounting concepts

Going concern: Going concern is an accounting concept for a business that has the

capital necessary to begin to function continuously before verification of the opposite is given.

The word also applies to the willingness of an organization to raise enough profit to remain alive

or escape default. If a company is not a company, it means it has declared bankruptcy, and its

resources have been forced to liquidate. Accounting professionals use the standards of going

concern to assess which forms of disclosure will surface on the financial statements.

Organizations that are an ongoing concern can delay recording of long-term assets at original

cost or liquidation price, however at cost more. A business retains an ongoing problem unless the

disposal of property does not hinder its strength to conduct operating, such as the closing of a

small branch manager that due to complete staff to many other business units (Sledgianowski,

Gomaa and Tan, 2017).

Materiality: Exchanges should be reported as failure to do so could change a reader's

financial reports judgments. It thought to occur in extremely small expenditures becoming

reported, such that a firm's financial performance, financial condition, and cash flows are

accurately reported in the financial reports. The definition or principle of materiality is an

accounting law that specifies all payments or products that have a major material effect on the

financial should be compensated for solely utilizing GAAP. In other terms, if a payment or

incident occurs for the year that might impact how the business will be perceived by a

shareholder it must be reported for using GAAP on the income statement (Tinoco, Holmes and

Wilson, 2018).

Business entity concept: The business entity property implies that the payments relevant

to a company must be finding a variety from that of its shareholders or other entities. To do so

includes the use in the company of different financial statements which fully exempt some other

organization or landlord's income and expenses. Under this definition, numerous entities' records

will be mixed, making it very difficult to distinguish the economic or taxation performance of a

particular enterprise (Umar, 2017). The company entity definition has a variety of explanations

such as:

Each commercial entity is exempted from tax

The financial results and economic position of the organization must be calculated

It is important to assess the sums of payments to the multiple managers whenever an entity is

repossessed

It is important from the point of view of responsibility to determine the money available against

even a commercial enterprise in the case of a carefully considered

Documents of a company cannot be audited because the documents have been merged with those

of other companies and/or persons (Wang and Zhang, 2017)

CONCLUSION

As per the above report it has been concluded that financial accounting use by the

different types of organizations to analysis the financial performance of the business. In this

accounting company prepares various types of statements that present actual financial

performance and help to top executives to take right decision. There are making trading, profit

and loss statement to analysis the financial performance. For this also calculate ratio analysis and

user information features with the benefits.

It is important to assess the sums of payments to the multiple managers whenever an entity is

repossessed

It is important from the point of view of responsibility to determine the money available against

even a commercial enterprise in the case of a carefully considered

Documents of a company cannot be audited because the documents have been merged with those

of other companies and/or persons (Wang and Zhang, 2017)

CONCLUSION

As per the above report it has been concluded that financial accounting use by the

different types of organizations to analysis the financial performance of the business. In this

accounting company prepares various types of statements that present actual financial

performance and help to top executives to take right decision. There are making trading, profit

and loss statement to analysis the financial performance. For this also calculate ratio analysis and

user information features with the benefits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.