Financial Accounting: Recording Business Transactions and Preparation of Final Accounts

Added on 2023-01-10

36 Pages3541 Words74 Views

Financial Accounting

Contents

INTRODUCTION...........................................................................................................................................3

LO1 Recording of business transactions applying double-entry bookkeeping, and extraction of trial

balance:.......................................................................................................................................................3

LO2 Preparation final-accounts with respect to sole-traders, partnerships-firms and limited corporations

as per appropriate principles, key conventions as well as standards:.........................................................6

TASK 1...................................................................................................................................................6

1.1 Trial balance at 31st March 2020 and calculation of Owner’s Capital at 31st March 2020 using the

balancing figure:......................................................................................................................................6

1.2 Journal Entry......................................................................................................................................7

1.3 Ledgers............................................................................................................................................10

TASK 2........................................................................................................................................................19

TASK 2.................................................................................................................................................21

2.2 Statement of Profit or Loss in accordance with International Accounting Standards (IAS) for Italian

Wines Ltd for year ended 31 March 2020:............................................................................................21

2.3. Statement of Financial Position in accordance with International Accounting Standards (IAS) for

Italian Wines Ltd at 31 March 2020......................................................................................................22

2.4 Calculation of Ratios:......................................................................................................................24

LO3 Perform bank re-conciliations to ensure company and bank records are correct:.............................25

TASK 3.................................................................................................................................................25

3.1 Bank reconciliation and its importance:...........................................................................................25

3.3 Bank-reconciliation Statement for Texas Traders at 30th April 2020 :............................................28

3.4 Application of:.................................................................................................................................28

LO4 Reconciling control accounts and shifting recorded transactions from suspense accounts to

respective right accounts:.........................................................................................................................29

TASK 4.................................................................................................................................................29

4.1: Calculation of Total of Debtors’ balances at 31 March 2020 as it was extracted from the Sales

Ledger:..................................................................................................................................................29

4.2 Statement of Reconciliation of the Totals of the customers’ balances:............................................30

4.3 Balancing Trial Balance through Suspense Account:......................................................................30

4.4 Journal entries to correct the errors and clear the Suspense Account balance:.................................31

CONCLUSION.............................................................................................................................................33

INTRODUCTION...........................................................................................................................................3

LO1 Recording of business transactions applying double-entry bookkeeping, and extraction of trial

balance:.......................................................................................................................................................3

LO2 Preparation final-accounts with respect to sole-traders, partnerships-firms and limited corporations

as per appropriate principles, key conventions as well as standards:.........................................................6

TASK 1...................................................................................................................................................6

1.1 Trial balance at 31st March 2020 and calculation of Owner’s Capital at 31st March 2020 using the

balancing figure:......................................................................................................................................6

1.2 Journal Entry......................................................................................................................................7

1.3 Ledgers............................................................................................................................................10

TASK 2........................................................................................................................................................19

TASK 2.................................................................................................................................................21

2.2 Statement of Profit or Loss in accordance with International Accounting Standards (IAS) for Italian

Wines Ltd for year ended 31 March 2020:............................................................................................21

2.3. Statement of Financial Position in accordance with International Accounting Standards (IAS) for

Italian Wines Ltd at 31 March 2020......................................................................................................22

2.4 Calculation of Ratios:......................................................................................................................24

LO3 Perform bank re-conciliations to ensure company and bank records are correct:.............................25

TASK 3.................................................................................................................................................25

3.1 Bank reconciliation and its importance:...........................................................................................25

3.3 Bank-reconciliation Statement for Texas Traders at 30th April 2020 :............................................28

3.4 Application of:.................................................................................................................................28

LO4 Reconciling control accounts and shifting recorded transactions from suspense accounts to

respective right accounts:.........................................................................................................................29

TASK 4.................................................................................................................................................29

4.1: Calculation of Total of Debtors’ balances at 31 March 2020 as it was extracted from the Sales

Ledger:..................................................................................................................................................29

4.2 Statement of Reconciliation of the Totals of the customers’ balances:............................................30

4.3 Balancing Trial Balance through Suspense Account:......................................................................30

4.4 Journal entries to correct the errors and clear the Suspense Account balance:.................................31

CONCLUSION.............................................................................................................................................33

INTRODUCTION

Financial accounting is important to keep a detailed overview of company's monetary

reports. Financial accounting's key purpose is to collect data and reports on the monetary

performance of an organisation. They describe a corporation's payments, explaining which entity

has rendered the payment with the time and value within each purchase. Manufacturers make

expenditure financial statements that make details on how much the company is worth. Even

before investors give support they can begin planning the growth rate of the corporation.

Financial accounting reports offer an analysis of the financial performance of both diverse

stakeholders for the new financial period (Demerjian and Owens, 2016). The financial outlook

thus describes the objectives set, how well the company works, and the amount of employees

and other funds that can be separated into various divisions. This project is focused on the

particular role of tracking monetary operations in journals, ledger, trial balance and generating

final accounts for various business forms. Moreover, this report permitted a bank reconciliation

to classify whether or not bank statements are exactly right.

LO1 Recording of business transactions applying double-entry bookkeeping,

and extraction of trial balance:

Types of Business transaction: There are defined different types of business transactions that

conduct the organizations that are mentioned below such as:

Sales: The word "sales" includes all activities that include the selling of a product or service to a

customer or company. The company records all the transactions of sales in sales accounting

books to track the record of company. Businesses have entire marketing institutions composed of

members engaged in the business of their goods and services. Sales are marketing operations or

the amount of products or services sold within a given specified period of time. The dealer, or

the manufacturer of the products or services, makes a transaction at the time of consumption in

reply to an application, allocation, authorize or regular engagement with both the customer (Fang

and et.al, 2016).

Purchase: Purchases refer to the volume of products purchased by a corporation during the year.

This also refers to details about the nature, quality, quantity, and cost of the purchased goods

which should be preserved. Inventories are introduced. Sales are offset by discounts for

transactions and returns for sales and allocations. Buying activities are necessary to guarantee

that the people in a number are collected in a reasonable timeframe and at affordable price. To

find distributors who can supply products and facilities according to the specifications of the

purchaser.

Receipts: A receipt is a written confirmation of passing something of interest from one entity to

the next. Aside from invoices that potential customers actually receive from vendors and

suppliers, receivables are also authorized in business-to - business money transfers and also in

Financial accounting is important to keep a detailed overview of company's monetary

reports. Financial accounting's key purpose is to collect data and reports on the monetary

performance of an organisation. They describe a corporation's payments, explaining which entity

has rendered the payment with the time and value within each purchase. Manufacturers make

expenditure financial statements that make details on how much the company is worth. Even

before investors give support they can begin planning the growth rate of the corporation.

Financial accounting reports offer an analysis of the financial performance of both diverse

stakeholders for the new financial period (Demerjian and Owens, 2016). The financial outlook

thus describes the objectives set, how well the company works, and the amount of employees

and other funds that can be separated into various divisions. This project is focused on the

particular role of tracking monetary operations in journals, ledger, trial balance and generating

final accounts for various business forms. Moreover, this report permitted a bank reconciliation

to classify whether or not bank statements are exactly right.

LO1 Recording of business transactions applying double-entry bookkeeping,

and extraction of trial balance:

Types of Business transaction: There are defined different types of business transactions that

conduct the organizations that are mentioned below such as:

Sales: The word "sales" includes all activities that include the selling of a product or service to a

customer or company. The company records all the transactions of sales in sales accounting

books to track the record of company. Businesses have entire marketing institutions composed of

members engaged in the business of their goods and services. Sales are marketing operations or

the amount of products or services sold within a given specified period of time. The dealer, or

the manufacturer of the products or services, makes a transaction at the time of consumption in

reply to an application, allocation, authorize or regular engagement with both the customer (Fang

and et.al, 2016).

Purchase: Purchases refer to the volume of products purchased by a corporation during the year.

This also refers to details about the nature, quality, quantity, and cost of the purchased goods

which should be preserved. Inventories are introduced. Sales are offset by discounts for

transactions and returns for sales and allocations. Buying activities are necessary to guarantee

that the people in a number are collected in a reasonable timeframe and at affordable price. To

find distributors who can supply products and facilities according to the specifications of the

purchaser.

Receipts: A receipt is a written confirmation of passing something of interest from one entity to

the next. Aside from invoices that potential customers actually receive from vendors and

suppliers, receivables are also authorized in business-to - business money transfers and also in

major stock exchanges. Further such exchanges are registered in newspapers that vendors are

credited to trade receivables as debit or money or credit payment (Gimbar, Hansen and Ozlanski,

2016).

Payment: Trade is the movement of one kind of products, services or capital instruments in

consideration for the next type of correct quantities of goods, services or capital instruments

which were mutually promised amongst all parties concerned. Compensation may take the form

of money, assets or services. These are reported in accounting records that are further prepared

for financial reporting by publications. Expenditure is debits and revenues credited to another

party.

Regulation of financial accounting:

The Financial Accounting Standards Board (FASB) is an autonomous, nonprofit

organization body involved in setting accounting and financial reporting requirements for

American firms and nonprofit entities, applying commonly accepted accounting principles

(GAAP).

Full disclosure: The Full Disclosure Principle stipulates that all appropriate and essential details

for interpreting a financial statement would be involved in a collection of listed corporation

reports financial reports. Financial experts who review financial statements ought to recognize

what commodity accounting system was used, whether any major take-downs have occurred,

how impairment is measured, and other important details to strengthen the basic results.

Monetary terms: It is GAAP's most basic concept where any collective agreement has to be

registered in the accounting records. The theory of financial asset states that corporate activities

should be reported only when they can be described in terms of a commodity. In many other

terms, the financial statements of a company should not be based on something that is non -

numeric. Over moment, funds were embraced in financial reporting as a standard of length

(Hoitash and Hoitash, 2018).

Matching principle: This is also called the method of double entry journals where each

transaction has dual effect. The framework of matching and recording each income documented

with all associated costs, at the very same moment. In accounting standards in particular, the

corresponding property implies that there must be cash per each debit.

Concepts above are few examples of economic reporting legislation, much remained to

be incorporated by industry in order to sell their goods effectively.

Double entry

Sales: For the double-entry book keeping a retail transaction is reported as a debit to cash or

account receivable and a credit to the sales ledger in the general report. The sum reported is the

operation's real dollar value, and not the collectible figurines’ sales price.

credited to trade receivables as debit or money or credit payment (Gimbar, Hansen and Ozlanski,

2016).

Payment: Trade is the movement of one kind of products, services or capital instruments in

consideration for the next type of correct quantities of goods, services or capital instruments

which were mutually promised amongst all parties concerned. Compensation may take the form

of money, assets or services. These are reported in accounting records that are further prepared

for financial reporting by publications. Expenditure is debits and revenues credited to another

party.

Regulation of financial accounting:

The Financial Accounting Standards Board (FASB) is an autonomous, nonprofit

organization body involved in setting accounting and financial reporting requirements for

American firms and nonprofit entities, applying commonly accepted accounting principles

(GAAP).

Full disclosure: The Full Disclosure Principle stipulates that all appropriate and essential details

for interpreting a financial statement would be involved in a collection of listed corporation

reports financial reports. Financial experts who review financial statements ought to recognize

what commodity accounting system was used, whether any major take-downs have occurred,

how impairment is measured, and other important details to strengthen the basic results.

Monetary terms: It is GAAP's most basic concept where any collective agreement has to be

registered in the accounting records. The theory of financial asset states that corporate activities

should be reported only when they can be described in terms of a commodity. In many other

terms, the financial statements of a company should not be based on something that is non -

numeric. Over moment, funds were embraced in financial reporting as a standard of length

(Hoitash and Hoitash, 2018).

Matching principle: This is also called the method of double entry journals where each

transaction has dual effect. The framework of matching and recording each income documented

with all associated costs, at the very same moment. In accounting standards in particular, the

corresponding property implies that there must be cash per each debit.

Concepts above are few examples of economic reporting legislation, much remained to

be incorporated by industry in order to sell their goods effectively.

Double entry

Sales: For the double-entry book keeping a retail transaction is reported as a debit to cash or

account receivable and a credit to the sales ledger in the general report. The sum reported is the

operation's real dollar value, and not the collectible figurines’ sales price.

Purchase: Double entry bookkeeping system is a records management structure where each

transaction happens in different sides or more. There really is no limitation on the amount of

transactions that can be used in a purchase but two systems are the lower limit

Electronic and manual system: Manual storage systems include hand-held handling of records

in a format prescribed. Manual systems require more materials than the electronic components.

The Vertical Filing system which is called used manual process, much like the one contrary.

Documents are contained in storage boxes and stored one after the other in storage boxes.

Trial Balance: A trial balance is an accounting and reporting or financial reporting list of

statements that describe the balance sheets in the books of accounts of every company. (The

transactions with nil amounts are also not mentioned.) The debit balance figures are mentioned

in the category under the headline "Debit balances" and the credit amount figures are identified

in that other column under the headed "Credit balances." A trial balance is a document that at a

particular point in time shows the amounts of all a corporation's accounts in the general ledger.

All accounting estimates products, namely assets , liabilities , equity, profits, expenditures,

profits / losses, are linked to the statements represented on a trial ledger. It's being used recognize

the equilibrium of debit card transactions and credit listings from the information performed until

a certain period in history in the accounting system (Kanodia and Sapra, 2016).

Role of trial balance for identification and rectification of error:

Once the trial balance is met, it just presents us with evidence of the ledger accounts'

mathematical accuracy. Nevertheless, some mistakes can still be around. Many mistakes impact

the result of the court while others do not. This is a direct sign of the existence of mistakes

whenever the trial balance doesn't count. They need those errors to be identified and located.

Reassessment of mistakes is therefore also important after they have been found

When errors are not affecting trial balance: If an account includes quick debit or surplus credit

then ought to debit the account in question. However when an account contains a brief credit or

large amounts debit, humans have to credit the address involved. Explanations of certain

mistakes are total omission to monitor an entrance in the journal or in the holding company

books, inaccurate transcription of purchases in the journals, comprehensive inaccuracy of writing

and inconsistencies of concept (Pelz, 2019).

When errors affecting trial balance: Mistakes in casting, errors in wanting to carry the

equilibrium, mistakes in trying to balance the transactions, mistakes in submitting the wrong

amount in the right location, errors in submitting the right address on the losing end, failure to

show the address in the trial balance, inaccuracies in submitting the opposite side with the

incorrect size are illustrations of manipulating people the financial statement.

transaction happens in different sides or more. There really is no limitation on the amount of

transactions that can be used in a purchase but two systems are the lower limit

Electronic and manual system: Manual storage systems include hand-held handling of records

in a format prescribed. Manual systems require more materials than the electronic components.

The Vertical Filing system which is called used manual process, much like the one contrary.

Documents are contained in storage boxes and stored one after the other in storage boxes.

Trial Balance: A trial balance is an accounting and reporting or financial reporting list of

statements that describe the balance sheets in the books of accounts of every company. (The

transactions with nil amounts are also not mentioned.) The debit balance figures are mentioned

in the category under the headline "Debit balances" and the credit amount figures are identified

in that other column under the headed "Credit balances." A trial balance is a document that at a

particular point in time shows the amounts of all a corporation's accounts in the general ledger.

All accounting estimates products, namely assets , liabilities , equity, profits, expenditures,

profits / losses, are linked to the statements represented on a trial ledger. It's being used recognize

the equilibrium of debit card transactions and credit listings from the information performed until

a certain period in history in the accounting system (Kanodia and Sapra, 2016).

Role of trial balance for identification and rectification of error:

Once the trial balance is met, it just presents us with evidence of the ledger accounts'

mathematical accuracy. Nevertheless, some mistakes can still be around. Many mistakes impact

the result of the court while others do not. This is a direct sign of the existence of mistakes

whenever the trial balance doesn't count. They need those errors to be identified and located.

Reassessment of mistakes is therefore also important after they have been found

When errors are not affecting trial balance: If an account includes quick debit or surplus credit

then ought to debit the account in question. However when an account contains a brief credit or

large amounts debit, humans have to credit the address involved. Explanations of certain

mistakes are total omission to monitor an entrance in the journal or in the holding company

books, inaccurate transcription of purchases in the journals, comprehensive inaccuracy of writing

and inconsistencies of concept (Pelz, 2019).

When errors affecting trial balance: Mistakes in casting, errors in wanting to carry the

equilibrium, mistakes in trying to balance the transactions, mistakes in submitting the wrong

amount in the right location, errors in submitting the right address on the losing end, failure to

show the address in the trial balance, inaccuracies in submitting the opposite side with the

incorrect size are illustrations of manipulating people the financial statement.

LO2 Preparation final-accounts with respect to sole-traders, partnerships-

firms and limited corporations as per appropriate principles, key

conventions as well as standards:

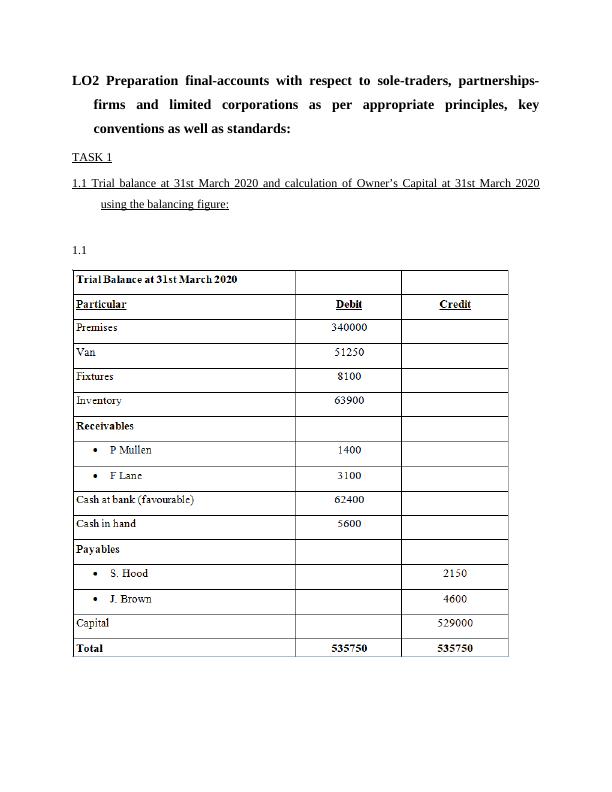

TASK 1

1.1 Trial balance at 31st March 2020 and calculation of Owner’s Capital at 31st March 2020

using the balancing figure:

1.1

firms and limited corporations as per appropriate principles, key

conventions as well as standards:

TASK 1

1.1 Trial balance at 31st March 2020 and calculation of Owner’s Capital at 31st March 2020

using the balancing figure:

1.1

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Accounting: Assignment Samplelg...

|37

|5577

|390

Financial Accounting Principles - Assignmentlg...

|37

|4664

|305

Financial Accountinglg...

|19

|4404

|22

Financial Accounting Principles and Techniqueslg...

|18

|3481

|25

Assignment on Financial Accounting pdflg...

|47

|5713

|177

Accounting Principles and Ruleslg...

|39

|4332

|322