Financial Accounting Assignment: XYZ Corp & ABC Analysis

VerifiedAdded on 2022/11/23

|15

|2697

|123

Homework Assignment

AI Summary

This financial accounting assignment analyzes various financial statements and key metrics. It begins with the preparation of cash flow statements using the indirect method, detailing operating, investing, and financing activities for XYZ Corporation in 2019. The assignment then calculates the equity return for the same company. Further, it examines the equity section of ABC, including authorized, issued, and paid-in capital, retained earnings, and treasury shares. Basic and diluted Earnings Per Share (EPS) are calculated. The assignment concludes with an analysis of Husky Co.'s short-term and long-term investments, presenting the impact of these investments on the statement of comprehensive income and the statement of cash flow. The analysis covers unrealized gains, profit on sales, and dividend impacts. The document includes journal entries and detailed explanations of financial statement components and their implications.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Exercise 1.........................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................4

Exercise 2.........................................................................................................................................4

Question 1....................................................................................................................................4

Question 2....................................................................................................................................6

Question 3....................................................................................................................................6

Exercise 3.........................................................................................................................................7

Question 1....................................................................................................................................7

Question 2....................................................................................................................................8

Question 3....................................................................................................................................9

Analysis...........................................................................................................................................9

Introduction......................................................................................................................................3

Exercise 1.........................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................4

Exercise 2.........................................................................................................................................4

Question 1....................................................................................................................................4

Question 2....................................................................................................................................6

Question 3....................................................................................................................................6

Exercise 3.........................................................................................................................................7

Question 1....................................................................................................................................7

Question 2....................................................................................................................................8

Question 3....................................................................................................................................9

Analysis...........................................................................................................................................9

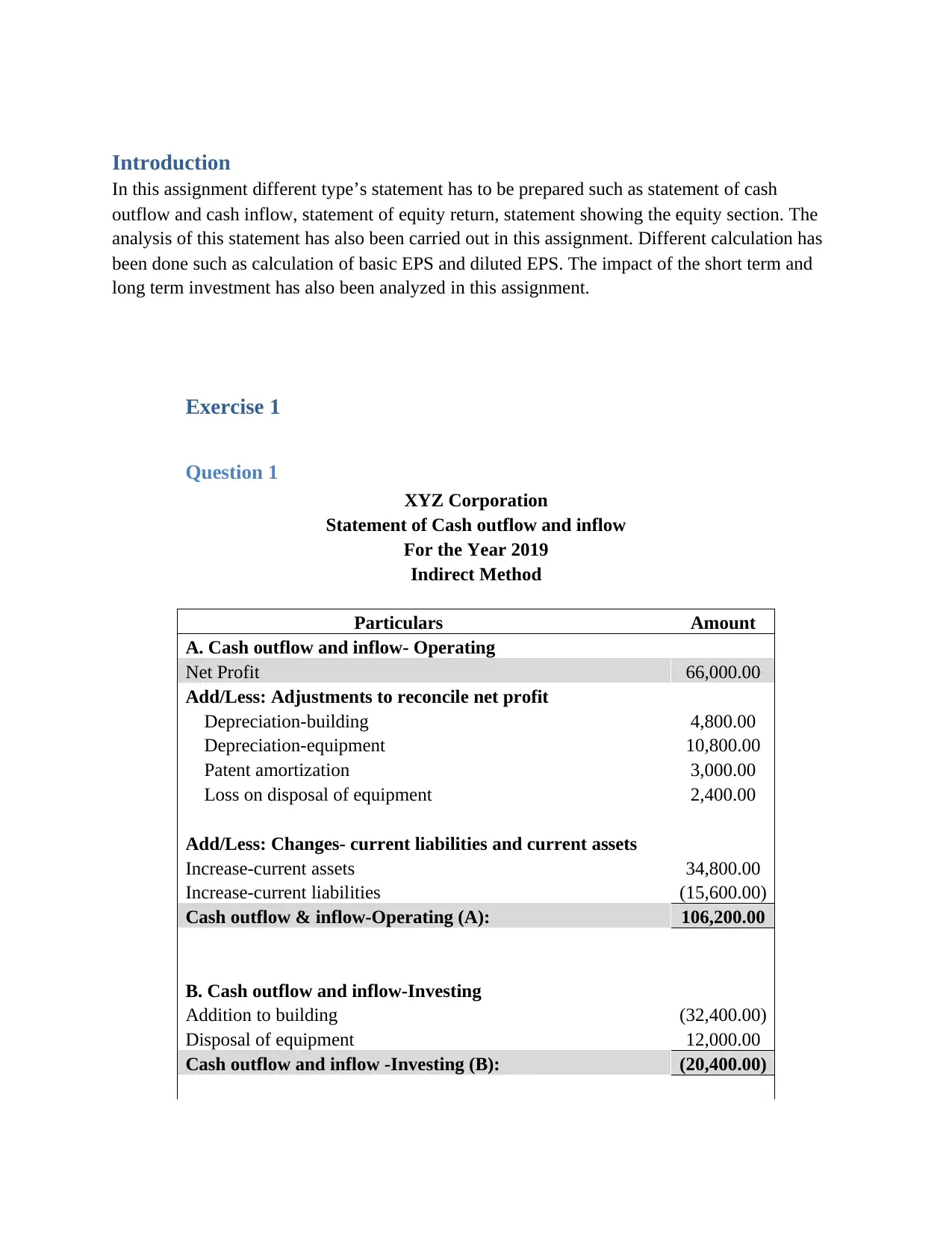

Introduction

In this assignment different type’s statement has to be prepared such as statement of cash

outflow and cash inflow, statement of equity return, statement showing the equity section. The

analysis of this statement has also been carried out in this assignment. Different calculation has

been done such as calculation of basic EPS and diluted EPS. The impact of the short term and

long term investment has also been analyzed in this assignment.

Exercise 1

Question 1

XYZ Corporation

Statement of Cash outflow and inflow

For the Year 2019

Indirect Method

Particulars Amount

A. Cash outflow and inflow- Operating

Net Profit 66,000.00

Add/Less: Adjustments to reconcile net profit

Depreciation-building 4,800.00

Depreciation-equipment 10,800.00

Patent amortization 3,000.00

Loss on disposal of equipment 2,400.00

Add/Less: Changes- current liabilities and current assets

Increase-current assets 34,800.00

Increase-current liabilities (15,600.00)

Cash outflow & inflow-Operating (A): 106,200.00

B. Cash outflow and inflow-Investing

Addition to building (32,400.00)

Disposal of equipment 12,000.00

Cash outflow and inflow -Investing (B): (20,400.00)

In this assignment different type’s statement has to be prepared such as statement of cash

outflow and cash inflow, statement of equity return, statement showing the equity section. The

analysis of this statement has also been carried out in this assignment. Different calculation has

been done such as calculation of basic EPS and diluted EPS. The impact of the short term and

long term investment has also been analyzed in this assignment.

Exercise 1

Question 1

XYZ Corporation

Statement of Cash outflow and inflow

For the Year 2019

Indirect Method

Particulars Amount

A. Cash outflow and inflow- Operating

Net Profit 66,000.00

Add/Less: Adjustments to reconcile net profit

Depreciation-building 4,800.00

Depreciation-equipment 10,800.00

Patent amortization 3,000.00

Loss on disposal of equipment 2,400.00

Add/Less: Changes- current liabilities and current assets

Increase-current assets 34,800.00

Increase-current liabilities (15,600.00)

Cash outflow & inflow-Operating (A): 106,200.00

B. Cash outflow and inflow-Investing

Addition to building (32,400.00)

Disposal of equipment 12,000.00

Cash outflow and inflow -Investing (B): (20,400.00)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

C. Cash outflow and inflow-Financing Activities

treasury shares-purchase (13,200.00)

Payment of Cash dividend (36,000.00)

Issue of bonds at par 60,000.00

Cash outflow and inflow- Financing (C): 10,800.00

Net increase in cash & cash equivalents (A+B+C) 96,600.00

Add: Cash balance as on 31st December 2018 100,000.00

Cash balance as on 31st December 2019 196,600.00

Question 2

Calculation of Equity Return

Particulars Amount

A. Net Profit 66,000.00

B. Share Capital 216,000.00

C. Retained Earnings 52,800.00

D. Shareholders' Equity 268,800.00

E. Equity Return (A/D) 0.25

Exercise 2

Question 1

ABC

Statement Showing Equity Section

As On 31st December, 2018

treasury shares-purchase (13,200.00)

Payment of Cash dividend (36,000.00)

Issue of bonds at par 60,000.00

Cash outflow and inflow- Financing (C): 10,800.00

Net increase in cash & cash equivalents (A+B+C) 96,600.00

Add: Cash balance as on 31st December 2018 100,000.00

Cash balance as on 31st December 2019 196,600.00

Question 2

Calculation of Equity Return

Particulars Amount

A. Net Profit 66,000.00

B. Share Capital 216,000.00

C. Retained Earnings 52,800.00

D. Shareholders' Equity 268,800.00

E. Equity Return (A/D) 0.25

Exercise 2

Question 1

ABC

Statement Showing Equity Section

As On 31st December, 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

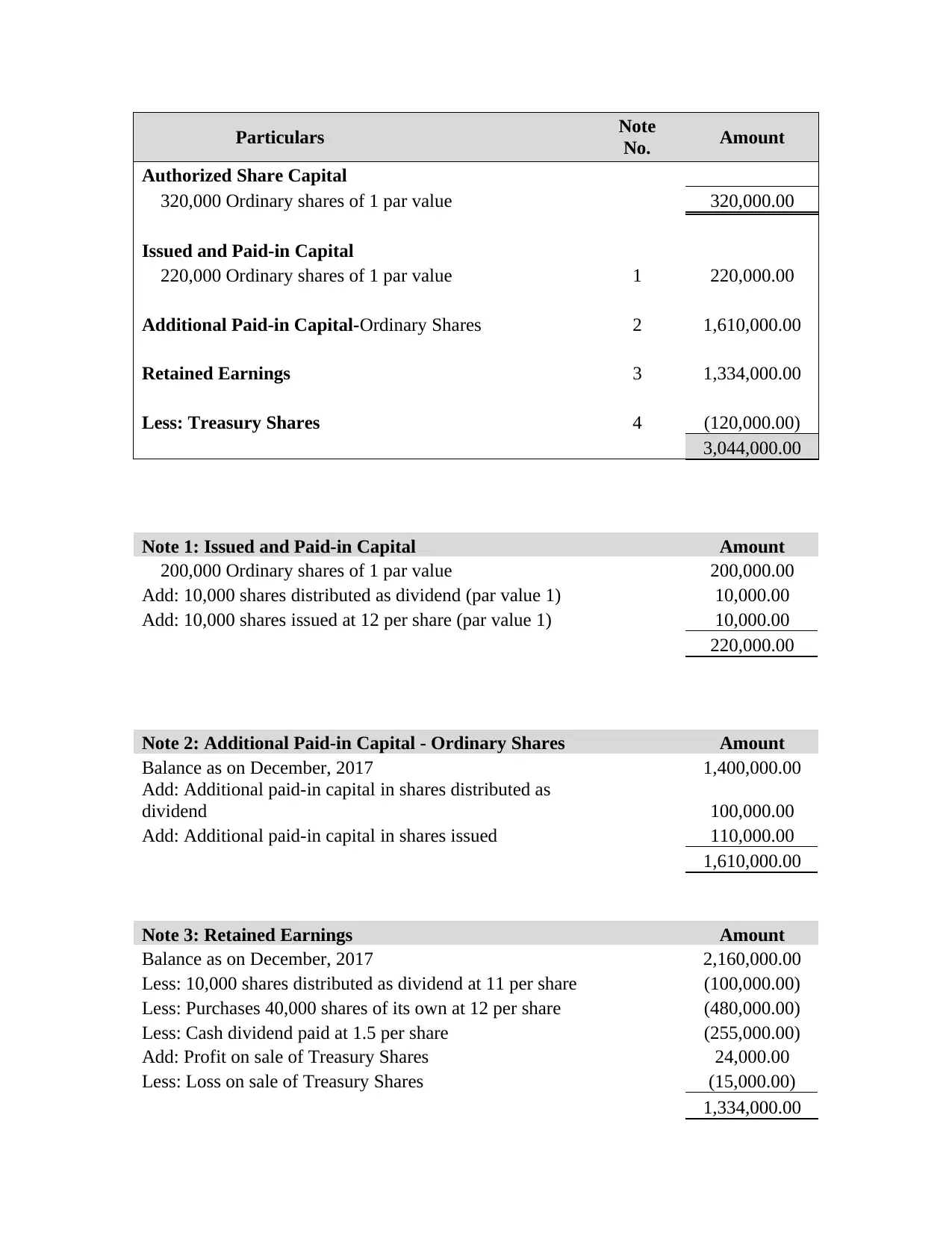

Particulars Note

No. Amount

Authorized Share Capital

320,000 Ordinary shares of 1 par value 320,000.00

Issued and Paid-in Capital

220,000 Ordinary shares of 1 par value 1 220,000.00

Additional Paid-in Capital-Ordinary Shares 2 1,610,000.00

Retained Earnings 3 1,334,000.00

Less: Treasury Shares 4 (120,000.00)

3,044,000.00

Note 1: Issued and Paid-in Capital Amount

200,000 Ordinary shares of 1 par value 200,000.00

Add: 10,000 shares distributed as dividend (par value 1) 10,000.00

Add: 10,000 shares issued at 12 per share (par value 1) 10,000.00

220,000.00

Note 2: Additional Paid-in Capital - Ordinary Shares Amount

Balance as on December, 2017 1,400,000.00

Add: Additional paid-in capital in shares distributed as

dividend 100,000.00

Add: Additional paid-in capital in shares issued 110,000.00

1,610,000.00

Note 3: Retained Earnings Amount

Balance as on December, 2017 2,160,000.00

Less: 10,000 shares distributed as dividend at 11 per share (100,000.00)

Less: Purchases 40,000 shares of its own at 12 per share (480,000.00)

Less: Cash dividend paid at 1.5 per share (255,000.00)

Add: Profit on sale of Treasury Shares 24,000.00

Less: Loss on sale of Treasury Shares (15,000.00)

1,334,000.00

No. Amount

Authorized Share Capital

320,000 Ordinary shares of 1 par value 320,000.00

Issued and Paid-in Capital

220,000 Ordinary shares of 1 par value 1 220,000.00

Additional Paid-in Capital-Ordinary Shares 2 1,610,000.00

Retained Earnings 3 1,334,000.00

Less: Treasury Shares 4 (120,000.00)

3,044,000.00

Note 1: Issued and Paid-in Capital Amount

200,000 Ordinary shares of 1 par value 200,000.00

Add: 10,000 shares distributed as dividend (par value 1) 10,000.00

Add: 10,000 shares issued at 12 per share (par value 1) 10,000.00

220,000.00

Note 2: Additional Paid-in Capital - Ordinary Shares Amount

Balance as on December, 2017 1,400,000.00

Add: Additional paid-in capital in shares distributed as

dividend 100,000.00

Add: Additional paid-in capital in shares issued 110,000.00

1,610,000.00

Note 3: Retained Earnings Amount

Balance as on December, 2017 2,160,000.00

Less: 10,000 shares distributed as dividend at 11 per share (100,000.00)

Less: Purchases 40,000 shares of its own at 12 per share (480,000.00)

Less: Cash dividend paid at 1.5 per share (255,000.00)

Add: Profit on sale of Treasury Shares 24,000.00

Less: Loss on sale of Treasury Shares (15,000.00)

1,334,000.00

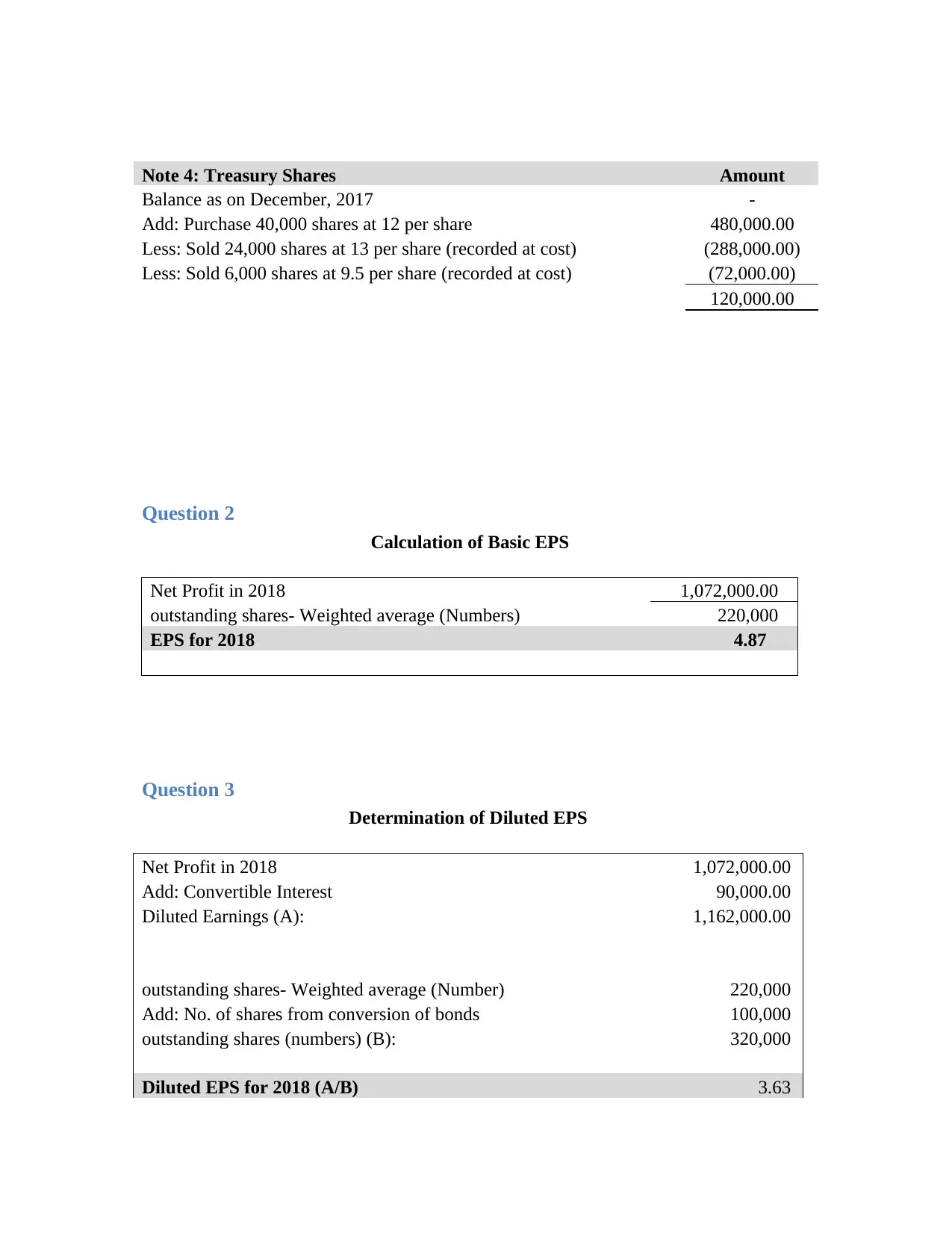

Note 4: Treasury Shares Amount

Balance as on December, 2017 -

Add: Purchase 40,000 shares at 12 per share 480,000.00

Less: Sold 24,000 shares at 13 per share (recorded at cost) (288,000.00)

Less: Sold 6,000 shares at 9.5 per share (recorded at cost) (72,000.00)

120,000.00

Question 2

Calculation of Basic EPS

Net Profit in 2018 1,072,000.00

outstanding shares- Weighted average (Numbers) 220,000

EPS for 2018 4.87

Question 3

Determination of Diluted EPS

Net Profit in 2018 1,072,000.00

Add: Convertible Interest 90,000.00

Diluted Earnings (A): 1,162,000.00

outstanding shares- Weighted average (Number) 220,000

Add: No. of shares from conversion of bonds 100,000

outstanding shares (numbers) (B): 320,000

Diluted EPS for 2018 (A/B) 3.63

Balance as on December, 2017 -

Add: Purchase 40,000 shares at 12 per share 480,000.00

Less: Sold 24,000 shares at 13 per share (recorded at cost) (288,000.00)

Less: Sold 6,000 shares at 9.5 per share (recorded at cost) (72,000.00)

120,000.00

Question 2

Calculation of Basic EPS

Net Profit in 2018 1,072,000.00

outstanding shares- Weighted average (Numbers) 220,000

EPS for 2018 4.87

Question 3

Determination of Diluted EPS

Net Profit in 2018 1,072,000.00

Add: Convertible Interest 90,000.00

Diluted Earnings (A): 1,162,000.00

outstanding shares- Weighted average (Number) 220,000

Add: No. of shares from conversion of bonds 100,000

outstanding shares (numbers) (B): 320,000

Diluted EPS for 2018 (A/B) 3.63

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Exercise 3

Question 1

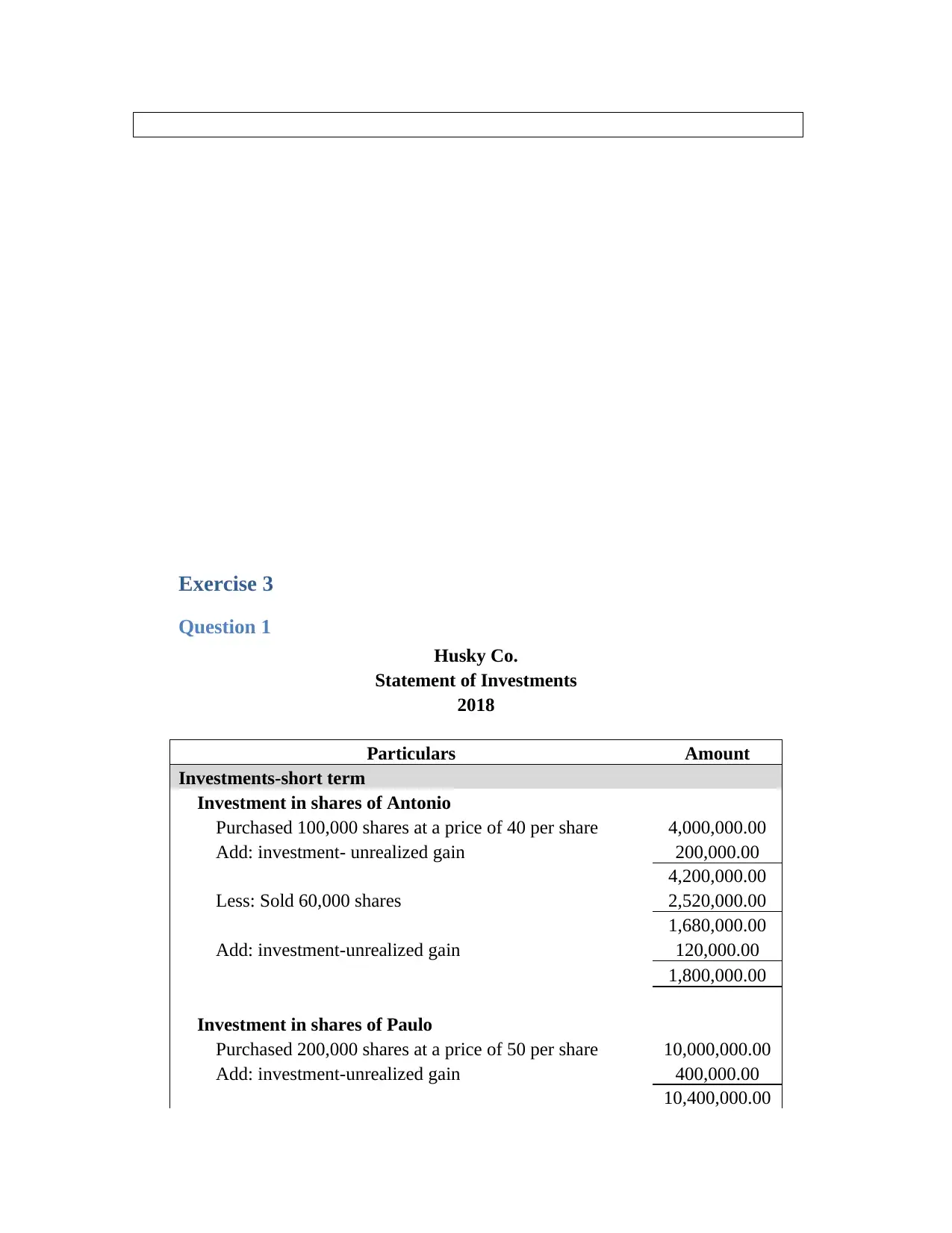

Husky Co.

Statement of Investments

2018

Particulars Amount

Investments-short term

Investment in shares of Antonio

Purchased 100,000 shares at a price of 40 per share 4,000,000.00

Add: investment- unrealized gain 200,000.00

4,200,000.00

Less: Sold 60,000 shares 2,520,000.00

1,680,000.00

Add: investment-unrealized gain 120,000.00

1,800,000.00

Investment in shares of Paulo

Purchased 200,000 shares at a price of 50 per share 10,000,000.00

Add: investment-unrealized gain 400,000.00

10,400,000.00

Question 1

Husky Co.

Statement of Investments

2018

Particulars Amount

Investments-short term

Investment in shares of Antonio

Purchased 100,000 shares at a price of 40 per share 4,000,000.00

Add: investment- unrealized gain 200,000.00

4,200,000.00

Less: Sold 60,000 shares 2,520,000.00

1,680,000.00

Add: investment-unrealized gain 120,000.00

1,800,000.00

Investment in shares of Paulo

Purchased 200,000 shares at a price of 50 per share 10,000,000.00

Add: investment-unrealized gain 400,000.00

10,400,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

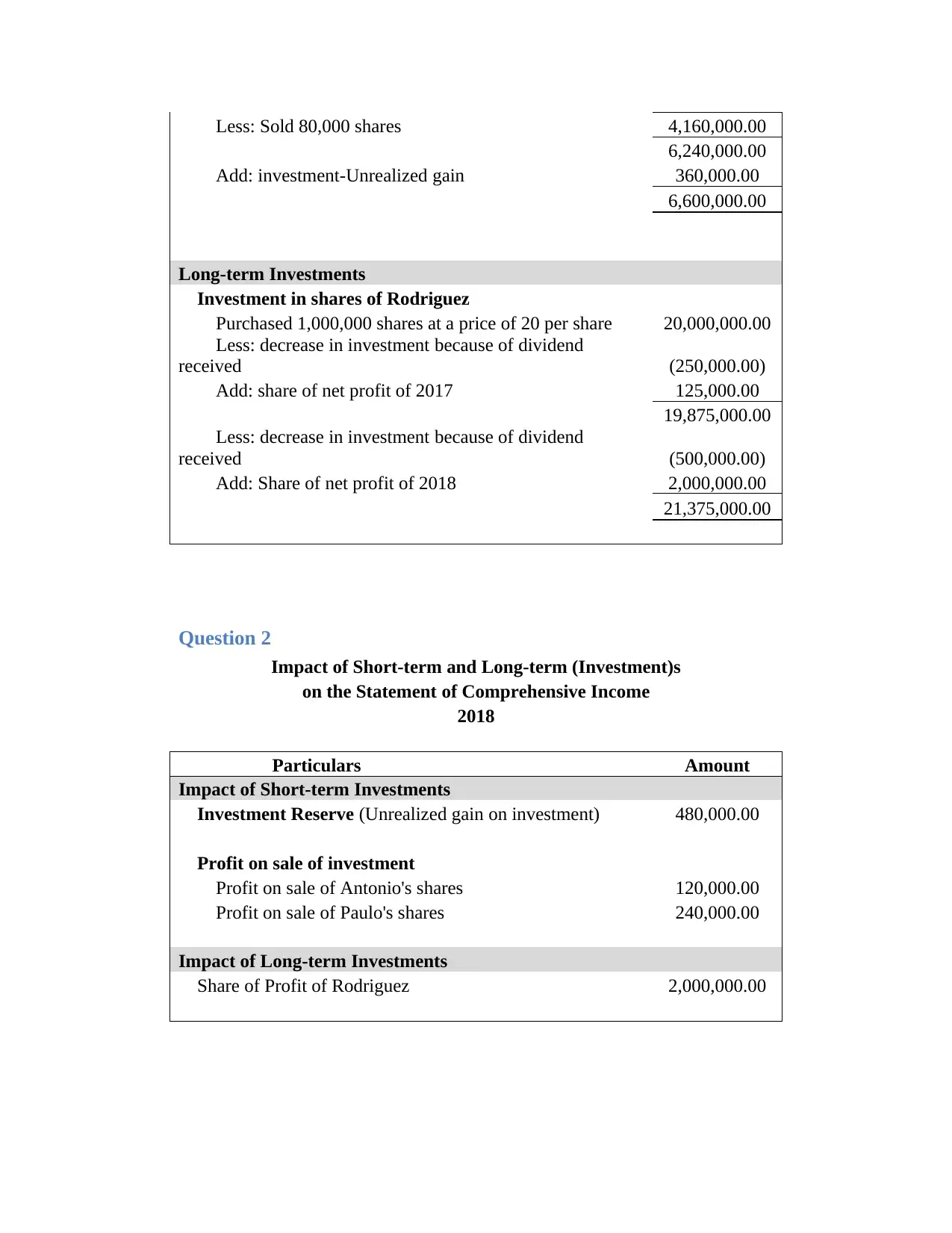

Less: Sold 80,000 shares 4,160,000.00

6,240,000.00

Add: investment-Unrealized gain 360,000.00

6,600,000.00

Long-term Investments

Investment in shares of Rodriguez

Purchased 1,000,000 shares at a price of 20 per share 20,000,000.00

Less: decrease in investment because of dividend

received (250,000.00)

Add: share of net profit of 2017 125,000.00

19,875,000.00

Less: decrease in investment because of dividend

received (500,000.00)

Add: Share of net profit of 2018 2,000,000.00

21,375,000.00

Question 2

Impact of Short-term and Long-term (Investment)s

on the Statement of Comprehensive Income

2018

Particulars Amount

Impact of Short-term Investments

Investment Reserve (Unrealized gain on investment) 480,000.00

Profit on sale of investment

Profit on sale of Antonio's shares 120,000.00

Profit on sale of Paulo's shares 240,000.00

Impact of Long-term Investments

Share of Profit of Rodriguez 2,000,000.00

6,240,000.00

Add: investment-Unrealized gain 360,000.00

6,600,000.00

Long-term Investments

Investment in shares of Rodriguez

Purchased 1,000,000 shares at a price of 20 per share 20,000,000.00

Less: decrease in investment because of dividend

received (250,000.00)

Add: share of net profit of 2017 125,000.00

19,875,000.00

Less: decrease in investment because of dividend

received (500,000.00)

Add: Share of net profit of 2018 2,000,000.00

21,375,000.00

Question 2

Impact of Short-term and Long-term (Investment)s

on the Statement of Comprehensive Income

2018

Particulars Amount

Impact of Short-term Investments

Investment Reserve (Unrealized gain on investment) 480,000.00

Profit on sale of investment

Profit on sale of Antonio's shares 120,000.00

Profit on sale of Paulo's shares 240,000.00

Impact of Long-term Investments

Share of Profit of Rodriguez 2,000,000.00

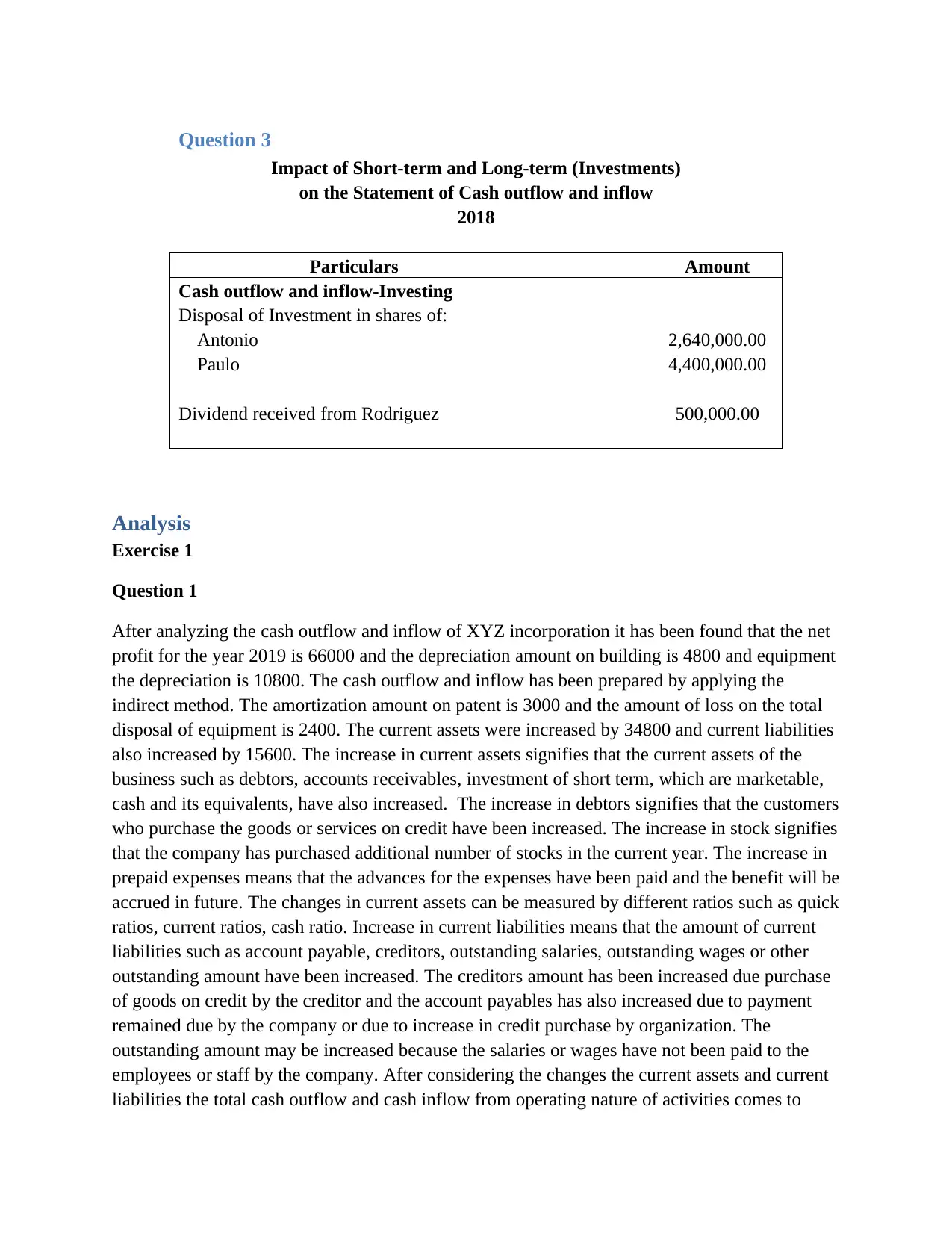

Question 3

Impact of Short-term and Long-term (Investments)

on the Statement of Cash outflow and inflow

2018

Particulars Amount

Cash outflow and inflow-Investing

Disposal of Investment in shares of:

Antonio 2,640,000.00

Paulo 4,400,000.00

Dividend received from Rodriguez 500,000.00

Analysis

Exercise 1

Question 1

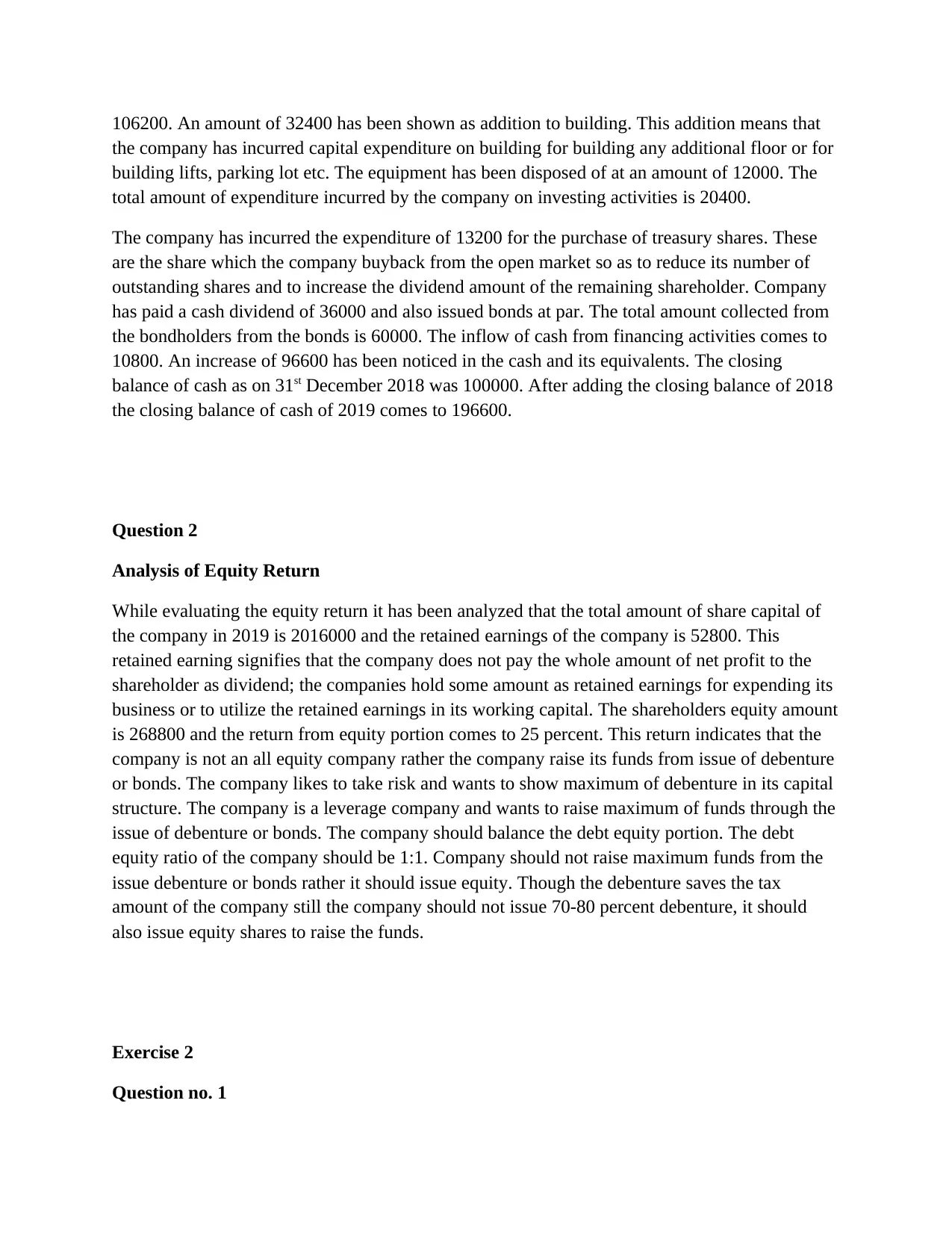

After analyzing the cash outflow and inflow of XYZ incorporation it has been found that the net

profit for the year 2019 is 66000 and the depreciation amount on building is 4800 and equipment

the depreciation is 10800. The cash outflow and inflow has been prepared by applying the

indirect method. The amortization amount on patent is 3000 and the amount of loss on the total

disposal of equipment is 2400. The current assets were increased by 34800 and current liabilities

also increased by 15600. The increase in current assets signifies that the current assets of the

business such as debtors, accounts receivables, investment of short term, which are marketable,

cash and its equivalents, have also increased. The increase in debtors signifies that the customers

who purchase the goods or services on credit have been increased. The increase in stock signifies

that the company has purchased additional number of stocks in the current year. The increase in

prepaid expenses means that the advances for the expenses have been paid and the benefit will be

accrued in future. The changes in current assets can be measured by different ratios such as quick

ratios, current ratios, cash ratio. Increase in current liabilities means that the amount of current

liabilities such as account payable, creditors, outstanding salaries, outstanding wages or other

outstanding amount have been increased. The creditors amount has been increased due purchase

of goods on credit by the creditor and the account payables has also increased due to payment

remained due by the company or due to increase in credit purchase by organization. The

outstanding amount may be increased because the salaries or wages have not been paid to the

employees or staff by the company. After considering the changes the current assets and current

liabilities the total cash outflow and cash inflow from operating nature of activities comes to

Impact of Short-term and Long-term (Investments)

on the Statement of Cash outflow and inflow

2018

Particulars Amount

Cash outflow and inflow-Investing

Disposal of Investment in shares of:

Antonio 2,640,000.00

Paulo 4,400,000.00

Dividend received from Rodriguez 500,000.00

Analysis

Exercise 1

Question 1

After analyzing the cash outflow and inflow of XYZ incorporation it has been found that the net

profit for the year 2019 is 66000 and the depreciation amount on building is 4800 and equipment

the depreciation is 10800. The cash outflow and inflow has been prepared by applying the

indirect method. The amortization amount on patent is 3000 and the amount of loss on the total

disposal of equipment is 2400. The current assets were increased by 34800 and current liabilities

also increased by 15600. The increase in current assets signifies that the current assets of the

business such as debtors, accounts receivables, investment of short term, which are marketable,

cash and its equivalents, have also increased. The increase in debtors signifies that the customers

who purchase the goods or services on credit have been increased. The increase in stock signifies

that the company has purchased additional number of stocks in the current year. The increase in

prepaid expenses means that the advances for the expenses have been paid and the benefit will be

accrued in future. The changes in current assets can be measured by different ratios such as quick

ratios, current ratios, cash ratio. Increase in current liabilities means that the amount of current

liabilities such as account payable, creditors, outstanding salaries, outstanding wages or other

outstanding amount have been increased. The creditors amount has been increased due purchase

of goods on credit by the creditor and the account payables has also increased due to payment

remained due by the company or due to increase in credit purchase by organization. The

outstanding amount may be increased because the salaries or wages have not been paid to the

employees or staff by the company. After considering the changes the current assets and current

liabilities the total cash outflow and cash inflow from operating nature of activities comes to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

106200. An amount of 32400 has been shown as addition to building. This addition means that

the company has incurred capital expenditure on building for building any additional floor or for

building lifts, parking lot etc. The equipment has been disposed of at an amount of 12000. The

total amount of expenditure incurred by the company on investing activities is 20400.

The company has incurred the expenditure of 13200 for the purchase of treasury shares. These

are the share which the company buyback from the open market so as to reduce its number of

outstanding shares and to increase the dividend amount of the remaining shareholder. Company

has paid a cash dividend of 36000 and also issued bonds at par. The total amount collected from

the bondholders from the bonds is 60000. The inflow of cash from financing activities comes to

10800. An increase of 96600 has been noticed in the cash and its equivalents. The closing

balance of cash as on 31st December 2018 was 100000. After adding the closing balance of 2018

the closing balance of cash of 2019 comes to 196600.

Question 2

Analysis of Equity Return

While evaluating the equity return it has been analyzed that the total amount of share capital of

the company in 2019 is 2016000 and the retained earnings of the company is 52800. This

retained earning signifies that the company does not pay the whole amount of net profit to the

shareholder as dividend; the companies hold some amount as retained earnings for expending its

business or to utilize the retained earnings in its working capital. The shareholders equity amount

is 268800 and the return from equity portion comes to 25 percent. This return indicates that the

company is not an all equity company rather the company raise its funds from issue of debenture

or bonds. The company likes to take risk and wants to show maximum of debenture in its capital

structure. The company is a leverage company and wants to raise maximum of funds through the

issue of debenture or bonds. The company should balance the debt equity portion. The debt

equity ratio of the company should be 1:1. Company should not raise maximum funds from the

issue debenture or bonds rather it should issue equity. Though the debenture saves the tax

amount of the company still the company should not issue 70-80 percent debenture, it should

also issue equity shares to raise the funds.

Exercise 2

Question no. 1

the company has incurred capital expenditure on building for building any additional floor or for

building lifts, parking lot etc. The equipment has been disposed of at an amount of 12000. The

total amount of expenditure incurred by the company on investing activities is 20400.

The company has incurred the expenditure of 13200 for the purchase of treasury shares. These

are the share which the company buyback from the open market so as to reduce its number of

outstanding shares and to increase the dividend amount of the remaining shareholder. Company

has paid a cash dividend of 36000 and also issued bonds at par. The total amount collected from

the bondholders from the bonds is 60000. The inflow of cash from financing activities comes to

10800. An increase of 96600 has been noticed in the cash and its equivalents. The closing

balance of cash as on 31st December 2018 was 100000. After adding the closing balance of 2018

the closing balance of cash of 2019 comes to 196600.

Question 2

Analysis of Equity Return

While evaluating the equity return it has been analyzed that the total amount of share capital of

the company in 2019 is 2016000 and the retained earnings of the company is 52800. This

retained earning signifies that the company does not pay the whole amount of net profit to the

shareholder as dividend; the companies hold some amount as retained earnings for expending its

business or to utilize the retained earnings in its working capital. The shareholders equity amount

is 268800 and the return from equity portion comes to 25 percent. This return indicates that the

company is not an all equity company rather the company raise its funds from issue of debenture

or bonds. The company likes to take risk and wants to show maximum of debenture in its capital

structure. The company is a leverage company and wants to raise maximum of funds through the

issue of debenture or bonds. The company should balance the debt equity portion. The debt

equity ratio of the company should be 1:1. Company should not raise maximum funds from the

issue debenture or bonds rather it should issue equity. Though the debenture saves the tax

amount of the company still the company should not issue 70-80 percent debenture, it should

also issue equity shares to raise the funds.

Exercise 2

Question no. 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

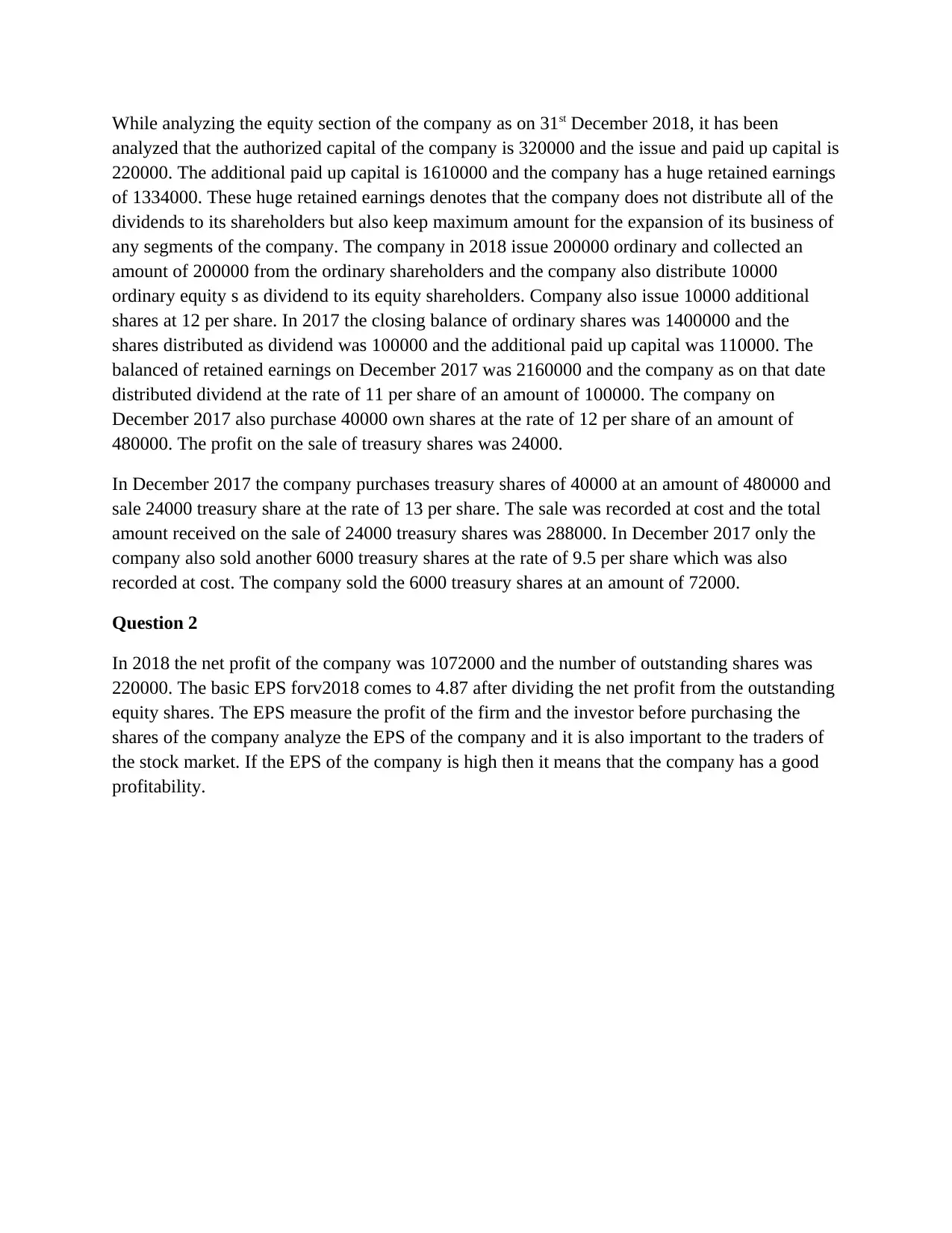

While analyzing the equity section of the company as on 31st December 2018, it has been

analyzed that the authorized capital of the company is 320000 and the issue and paid up capital is

220000. The additional paid up capital is 1610000 and the company has a huge retained earnings

of 1334000. These huge retained earnings denotes that the company does not distribute all of the

dividends to its shareholders but also keep maximum amount for the expansion of its business of

any segments of the company. The company in 2018 issue 200000 ordinary and collected an

amount of 200000 from the ordinary shareholders and the company also distribute 10000

ordinary equity s as dividend to its equity shareholders. Company also issue 10000 additional

shares at 12 per share. In 2017 the closing balance of ordinary shares was 1400000 and the

shares distributed as dividend was 100000 and the additional paid up capital was 110000. The

balanced of retained earnings on December 2017 was 2160000 and the company as on that date

distributed dividend at the rate of 11 per share of an amount of 100000. The company on

December 2017 also purchase 40000 own shares at the rate of 12 per share of an amount of

480000. The profit on the sale of treasury shares was 24000.

In December 2017 the company purchases treasury shares of 40000 at an amount of 480000 and

sale 24000 treasury share at the rate of 13 per share. The sale was recorded at cost and the total

amount received on the sale of 24000 treasury shares was 288000. In December 2017 only the

company also sold another 6000 treasury shares at the rate of 9.5 per share which was also

recorded at cost. The company sold the 6000 treasury shares at an amount of 72000.

Question 2

In 2018 the net profit of the company was 1072000 and the number of outstanding shares was

220000. The basic EPS forv2018 comes to 4.87 after dividing the net profit from the outstanding

equity shares. The EPS measure the profit of the firm and the investor before purchasing the

shares of the company analyze the EPS of the company and it is also important to the traders of

the stock market. If the EPS of the company is high then it means that the company has a good

profitability.

analyzed that the authorized capital of the company is 320000 and the issue and paid up capital is

220000. The additional paid up capital is 1610000 and the company has a huge retained earnings

of 1334000. These huge retained earnings denotes that the company does not distribute all of the

dividends to its shareholders but also keep maximum amount for the expansion of its business of

any segments of the company. The company in 2018 issue 200000 ordinary and collected an

amount of 200000 from the ordinary shareholders and the company also distribute 10000

ordinary equity s as dividend to its equity shareholders. Company also issue 10000 additional

shares at 12 per share. In 2017 the closing balance of ordinary shares was 1400000 and the

shares distributed as dividend was 100000 and the additional paid up capital was 110000. The

balanced of retained earnings on December 2017 was 2160000 and the company as on that date

distributed dividend at the rate of 11 per share of an amount of 100000. The company on

December 2017 also purchase 40000 own shares at the rate of 12 per share of an amount of

480000. The profit on the sale of treasury shares was 24000.

In December 2017 the company purchases treasury shares of 40000 at an amount of 480000 and

sale 24000 treasury share at the rate of 13 per share. The sale was recorded at cost and the total

amount received on the sale of 24000 treasury shares was 288000. In December 2017 only the

company also sold another 6000 treasury shares at the rate of 9.5 per share which was also

recorded at cost. The company sold the 6000 treasury shares at an amount of 72000.

Question 2

In 2018 the net profit of the company was 1072000 and the number of outstanding shares was

220000. The basic EPS forv2018 comes to 4.87 after dividing the net profit from the outstanding

equity shares. The EPS measure the profit of the firm and the investor before purchasing the

shares of the company analyze the EPS of the company and it is also important to the traders of

the stock market. If the EPS of the company is high then it means that the company has a good

profitability.

Exercise 2

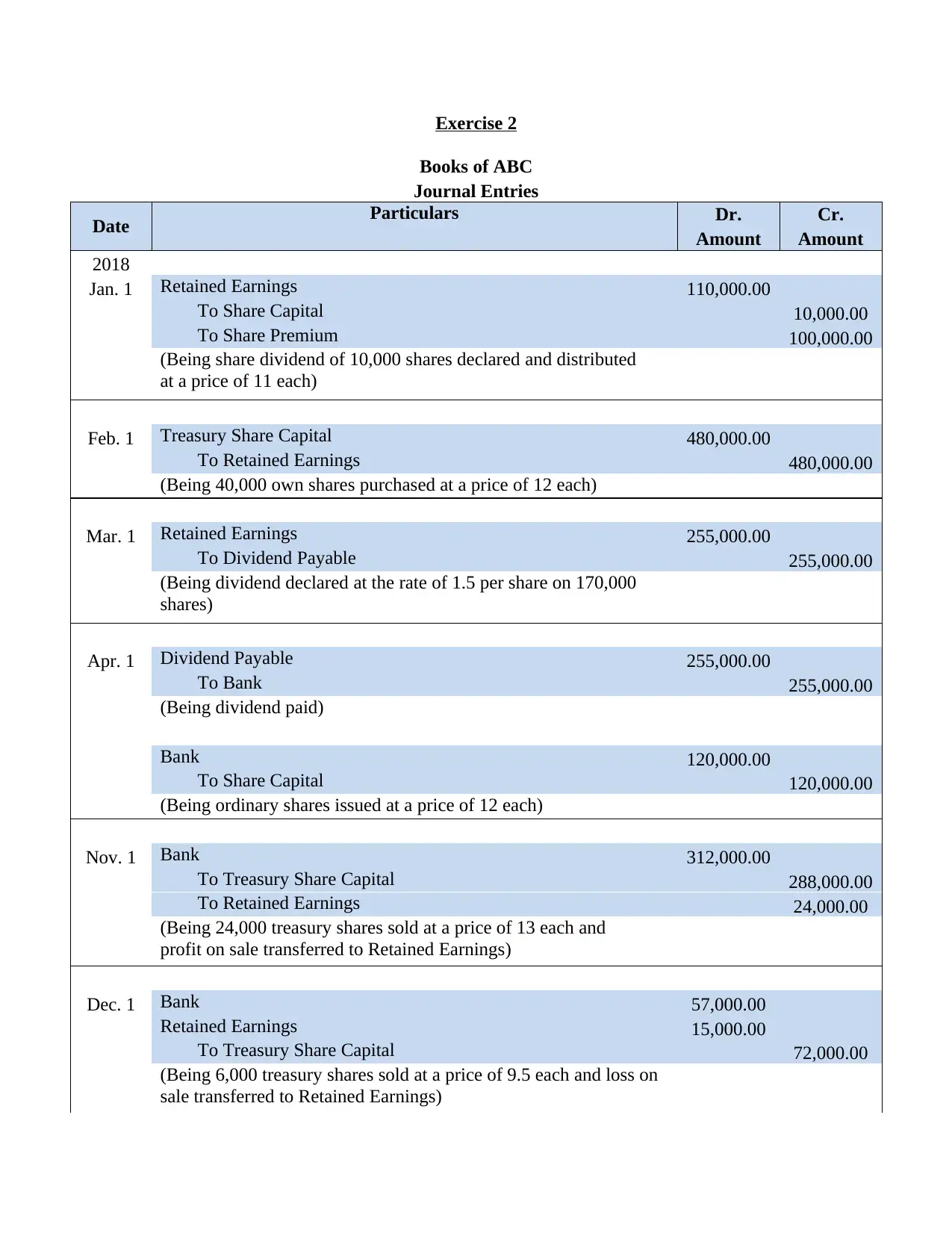

Books of ABC

Journal Entries

Date Particulars Dr. Cr.

Amount Amount

2018

Jan. 1 Retained Earnings 110,000.00

To Share Capital 10,000.00

To Share Premium 100,000.00

(Being share dividend of 10,000 shares declared and distributed

at a price of 11 each)

Feb. 1 Treasury Share Capital 480,000.00

To Retained Earnings 480,000.00

(Being 40,000 own shares purchased at a price of 12 each)

Mar. 1 Retained Earnings 255,000.00

To Dividend Payable 255,000.00

(Being dividend declared at the rate of 1.5 per share on 170,000

shares)

Apr. 1 Dividend Payable 255,000.00

To Bank 255,000.00

(Being dividend paid)

Bank 120,000.00

To Share Capital 120,000.00

(Being ordinary shares issued at a price of 12 each)

Nov. 1 Bank 312,000.00

To Treasury Share Capital 288,000.00

To Retained Earnings 24,000.00

(Being 24,000 treasury shares sold at a price of 13 each and

profit on sale transferred to Retained Earnings)

Dec. 1 Bank 57,000.00

Retained Earnings 15,000.00

To Treasury Share Capital 72,000.00

(Being 6,000 treasury shares sold at a price of 9.5 each and loss on

sale transferred to Retained Earnings)

Books of ABC

Journal Entries

Date Particulars Dr. Cr.

Amount Amount

2018

Jan. 1 Retained Earnings 110,000.00

To Share Capital 10,000.00

To Share Premium 100,000.00

(Being share dividend of 10,000 shares declared and distributed

at a price of 11 each)

Feb. 1 Treasury Share Capital 480,000.00

To Retained Earnings 480,000.00

(Being 40,000 own shares purchased at a price of 12 each)

Mar. 1 Retained Earnings 255,000.00

To Dividend Payable 255,000.00

(Being dividend declared at the rate of 1.5 per share on 170,000

shares)

Apr. 1 Dividend Payable 255,000.00

To Bank 255,000.00

(Being dividend paid)

Bank 120,000.00

To Share Capital 120,000.00

(Being ordinary shares issued at a price of 12 each)

Nov. 1 Bank 312,000.00

To Treasury Share Capital 288,000.00

To Retained Earnings 24,000.00

(Being 24,000 treasury shares sold at a price of 13 each and

profit on sale transferred to Retained Earnings)

Dec. 1 Bank 57,000.00

Retained Earnings 15,000.00

To Treasury Share Capital 72,000.00

(Being 6,000 treasury shares sold at a price of 9.5 each and loss on

sale transferred to Retained Earnings)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.