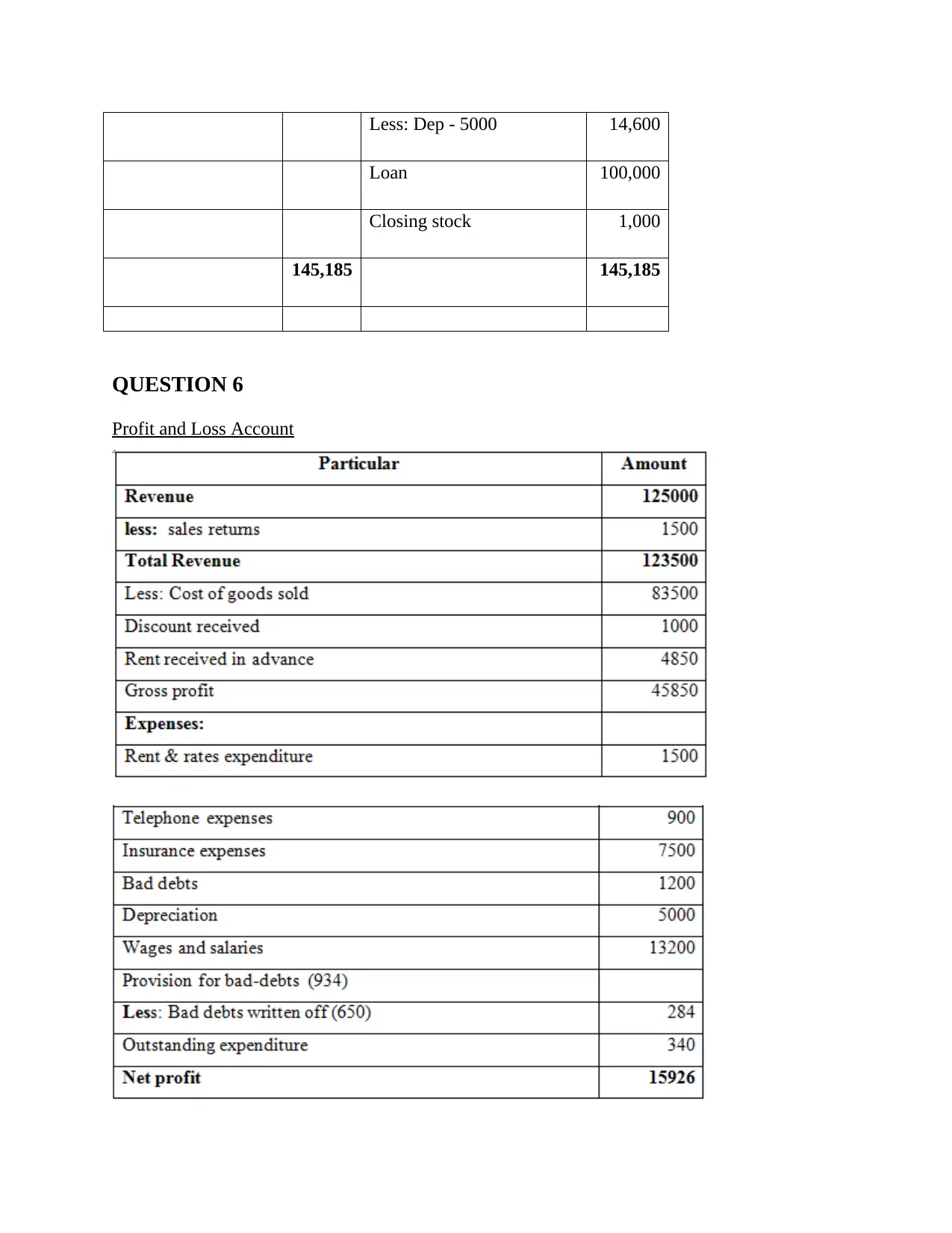

Financial Accounting

VerifiedAdded on 2022/11/24

|28

|4585

|487

AI Summary

This document provides an introduction to financial accounting, including its purpose and goals. It covers different types of business transactions, calculation methods, the difference between financial statements and financial reports, principles of accounting, and a cash flow statement. The document also includes a profit and loss account and balance sheet.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

Different types of business transaction...................................................................................................3

QUESTION 2.................................................................................................................................................5

Calculation...............................................................................................................................................5

QUESTION 3...............................................................................................................................................10

Different between financial statement and financial report.................................................................10

QUESTION 4...............................................................................................................................................12

Principles of accounting.........................................................................................................................12

QUESTION 5...............................................................................................................................................13

Calculation.............................................................................................................................................13

QUESTION 6...............................................................................................................................................15

Profit and Loss Account.........................................................................................................................15

QUESTION 7...............................................................................................................................................16

Cash flow statement..............................................................................................................................16

SCENARIO 2...............................................................................................................................................18

QUESTION 1...............................................................................................................................................18

Bank Reconciliation...............................................................................................................................18

QUESTION 2...............................................................................................................................................19

Control accounts....................................................................................................................................19

QUESTION 3...............................................................................................................................................20

Suspense Account..................................................................................................................................20

QUESTION 4...............................................................................................................................................21

(a) Required to prepare updated cash book and bank reconciliation statement..................................21

QUESTION 5...............................................................................................................................................23

Journal entries.......................................................................................................................................23

CONCLUSION.............................................................................................................................................25

REFERENCES..............................................................................................................................................26

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

Different types of business transaction...................................................................................................3

QUESTION 2.................................................................................................................................................5

Calculation...............................................................................................................................................5

QUESTION 3...............................................................................................................................................10

Different between financial statement and financial report.................................................................10

QUESTION 4...............................................................................................................................................12

Principles of accounting.........................................................................................................................12

QUESTION 5...............................................................................................................................................13

Calculation.............................................................................................................................................13

QUESTION 6...............................................................................................................................................15

Profit and Loss Account.........................................................................................................................15

QUESTION 7...............................................................................................................................................16

Cash flow statement..............................................................................................................................16

SCENARIO 2...............................................................................................................................................18

QUESTION 1...............................................................................................................................................18

Bank Reconciliation...............................................................................................................................18

QUESTION 2...............................................................................................................................................19

Control accounts....................................................................................................................................19

QUESTION 3...............................................................................................................................................20

Suspense Account..................................................................................................................................20

QUESTION 4...............................................................................................................................................21

(a) Required to prepare updated cash book and bank reconciliation statement..................................21

QUESTION 5...............................................................................................................................................23

Journal entries.......................................................................................................................................23

CONCLUSION.............................................................................................................................................25

REFERENCES..............................................................................................................................................26

INTRODUCTION

Financial accounting is the process of recording, summarizing and analyzing a corporation's

money transfer in order to achieve an accurate image of the company's financial condition and

performance. The creation of accounting policies other than an accounting records, cash flow

statement, and profitability statement – which capture their operational efficiency over a certain

period and liquidity statements at a single point in time is the primary goal of financial

accounting. Financial accounting is a branch of accounting that assists businesses in reflecting on

their assets and debts (balance sheet), sales and costs (income statement), and working capital

(operating cash declaration) (cash flow statement). Those spaces can be utilized for both internal

and exterior reasons especially when combined.

The work is split into two categories, one with its own amount of details. Some problems,

such as the types of investments integrating single-entry and double-entry bookkeeping, balance

sheet, and its usefulness, should always be completed well before the portion can be performed.

The second section of this component aims at creating journal entries for each action, and

perhaps even the Documents and a Control Account. The contrast between an accounting records

and a financial results, including the fundamentals of accountants and the net profit margin, are

all provided in the following section.

QUESTION 1

Different types of business transaction

A financial transaction is an operation or occurrence that has an economic or functional

impact on a firm and can be quantified in terms of finances. Accounting systems are any

business activities that have a direct impact on the company's financial condition and income

reports. To guarantee comprehensive and term associated while preparing financial statements, a

bookkeeping system needs to be able to capture all company activities.

Commercial transaction: It involves most operations or exchanges that have been detectable in

cash form and have an immediate impact on employment processes. There are three indicators

on the industrial association's prosperity, liability, operations, and profitability. Business

activities are behaviors some of which are essential to management and are reflected in the firm's

Financial accounting is the process of recording, summarizing and analyzing a corporation's

money transfer in order to achieve an accurate image of the company's financial condition and

performance. The creation of accounting policies other than an accounting records, cash flow

statement, and profitability statement – which capture their operational efficiency over a certain

period and liquidity statements at a single point in time is the primary goal of financial

accounting. Financial accounting is a branch of accounting that assists businesses in reflecting on

their assets and debts (balance sheet), sales and costs (income statement), and working capital

(operating cash declaration) (cash flow statement). Those spaces can be utilized for both internal

and exterior reasons especially when combined.

The work is split into two categories, one with its own amount of details. Some problems,

such as the types of investments integrating single-entry and double-entry bookkeeping, balance

sheet, and its usefulness, should always be completed well before the portion can be performed.

The second section of this component aims at creating journal entries for each action, and

perhaps even the Documents and a Control Account. The contrast between an accounting records

and a financial results, including the fundamentals of accountants and the net profit margin, are

all provided in the following section.

QUESTION 1

Different types of business transaction

A financial transaction is an operation or occurrence that has an economic or functional

impact on a firm and can be quantified in terms of finances. Accounting systems are any

business activities that have a direct impact on the company's financial condition and income

reports. To guarantee comprehensive and term associated while preparing financial statements, a

bookkeeping system needs to be able to capture all company activities.

Commercial transaction: It involves most operations or exchanges that have been detectable in

cash form and have an immediate impact on employment processes. There are three indicators

on the industrial association's prosperity, liability, operations, and profitability. Business

activities are behaviors some of which are essential to management and are reflected in the firm's

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

journals. Trades and credit financial transactions are the two kinds of services that are

commonplace.

Cash buyer: Involving the incoming and exterior stream of money. It involves trades,

expenditures, and financial transactions, along with other things.

Credit trade: It is defined as any process in which currency is not demanded at the period of

contract.

Things purchased on credit, equities generated from the sale are just a few instance.

Certain events prompt expanded the union's requirement and have a consequence on future cash

flow, although merchandise supplied on credit strengthens the foundation's assets.

Define single entry book keeping:

All recorded corporate actions must be supported by some type of realistic evidence or

form, according to this notion. It also indicates that accountancy and financial information

should be kept separately, free of any suspicion of impropriety. Monetary accounts receivable

are handled using a single entry bookkeeping system. Only one instruction is executed by the

bookkeeper. Like the double input system, there are no card payment sides.

Define double entry book keeping:

Entrance with two doors Every monetary transaction is handled by two or more accounts in the

accounting system. A individual, for example, sold a piece of wood at a marketplace. As a result,

the monthly payment accounts will grow, but the furniture account will drop by the same

amount. In today's world, it's a key concept that encompasses books of accounts. Each monetary

transaction has an opposite and comparable effect on two separate accounts.

Explain trial balance and its importance:

It is a report that outlines a statement of all information shared all business dealings most of

which are documented in the logbook records. In this circumstance, every company holding

quantities have really been represented on the document's bank transfer section. In other regards,

a trial balance is a marketed at the ending of every accountancy year just to represent the debit

commonplace.

Cash buyer: Involving the incoming and exterior stream of money. It involves trades,

expenditures, and financial transactions, along with other things.

Credit trade: It is defined as any process in which currency is not demanded at the period of

contract.

Things purchased on credit, equities generated from the sale are just a few instance.

Certain events prompt expanded the union's requirement and have a consequence on future cash

flow, although merchandise supplied on credit strengthens the foundation's assets.

Define single entry book keeping:

All recorded corporate actions must be supported by some type of realistic evidence or

form, according to this notion. It also indicates that accountancy and financial information

should be kept separately, free of any suspicion of impropriety. Monetary accounts receivable

are handled using a single entry bookkeeping system. Only one instruction is executed by the

bookkeeper. Like the double input system, there are no card payment sides.

Define double entry book keeping:

Entrance with two doors Every monetary transaction is handled by two or more accounts in the

accounting system. A individual, for example, sold a piece of wood at a marketplace. As a result,

the monthly payment accounts will grow, but the furniture account will drop by the same

amount. In today's world, it's a key concept that encompasses books of accounts. Each monetary

transaction has an opposite and comparable effect on two separate accounts.

Explain trial balance and its importance:

It is a report that outlines a statement of all information shared all business dealings most of

which are documented in the logbook records. In this circumstance, every company holding

quantities have really been represented on the document's bank transfer section. In other regards,

a trial balance is a marketed at the ending of every accountancy year just to represent the debit

and credit sums of the entities but use a leading. In the framework of trial balance importance are

mentioned below:

Trial balance is used by employers to determine the debit and credit balances of accounts.

It is committed to the employees in mitigating risk through record submission.

It facilitates in the books of accounts by presenting essential data.

QUESTION 2

Calculation

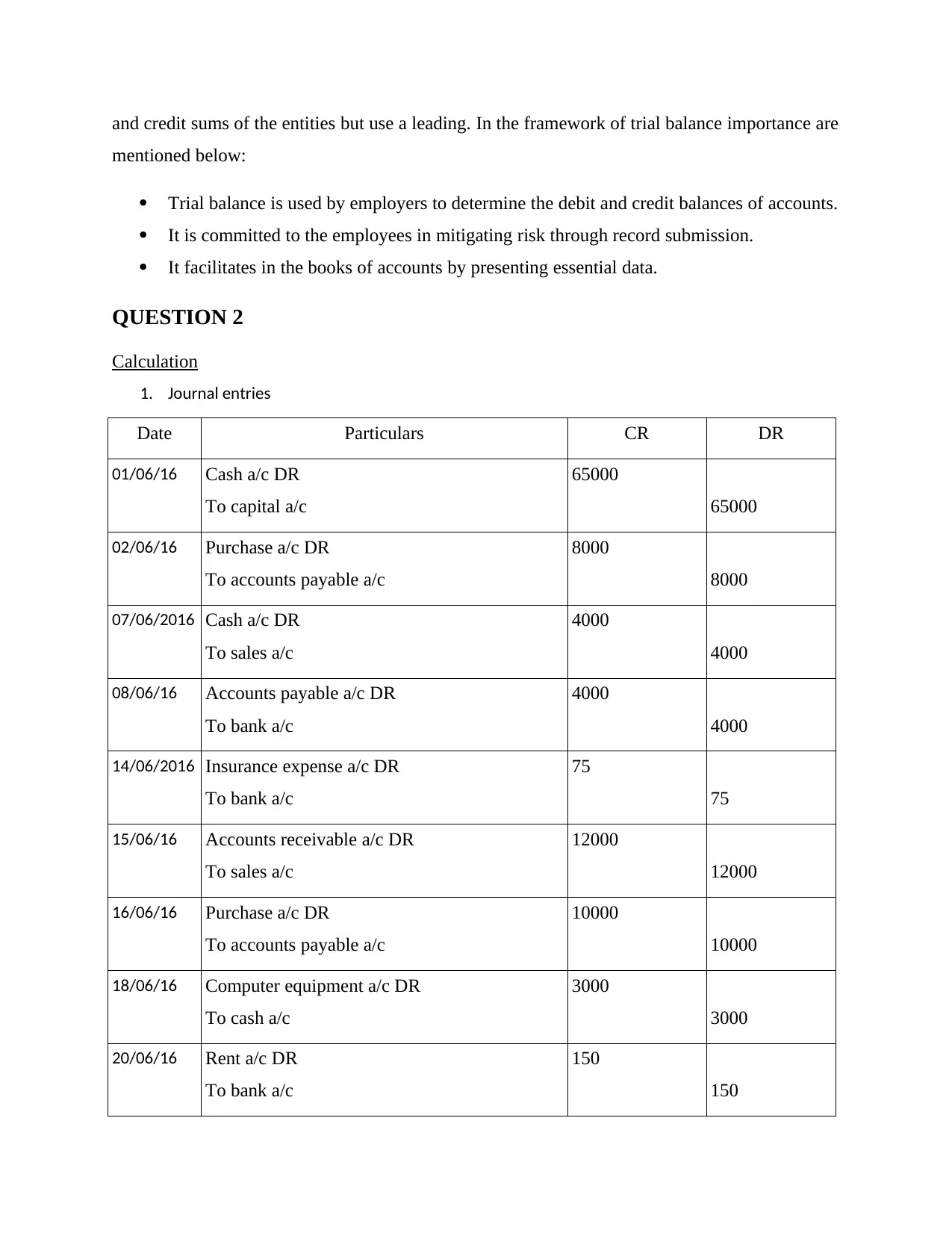

1. Journal entries

Date Particulars CR DR

01/06/16 Cash a/c DR

To capital a/c

65000

65000

02/06/16 Purchase a/c DR

To accounts payable a/c

8000

8000

07/06/2016 Cash a/c DR

To sales a/c

4000

4000

08/06/16 Accounts payable a/c DR

To bank a/c

4000

4000

14/06/2016 Insurance expense a/c DR

To bank a/c

75

75

15/06/16 Accounts receivable a/c DR

To sales a/c

12000

12000

16/06/16 Purchase a/c DR

To accounts payable a/c

10000

10000

18/06/16 Computer equipment a/c DR

To cash a/c

3000

3000

20/06/16 Rent a/c DR

To bank a/c

150

150

mentioned below:

Trial balance is used by employers to determine the debit and credit balances of accounts.

It is committed to the employees in mitigating risk through record submission.

It facilitates in the books of accounts by presenting essential data.

QUESTION 2

Calculation

1. Journal entries

Date Particulars CR DR

01/06/16 Cash a/c DR

To capital a/c

65000

65000

02/06/16 Purchase a/c DR

To accounts payable a/c

8000

8000

07/06/2016 Cash a/c DR

To sales a/c

4000

4000

08/06/16 Accounts payable a/c DR

To bank a/c

4000

4000

14/06/2016 Insurance expense a/c DR

To bank a/c

75

75

15/06/16 Accounts receivable a/c DR

To sales a/c

12000

12000

16/06/16 Purchase a/c DR

To accounts payable a/c

10000

10000

18/06/16 Computer equipment a/c DR

To cash a/c

3000

3000

20/06/16 Rent a/c DR

To bank a/c

150

150

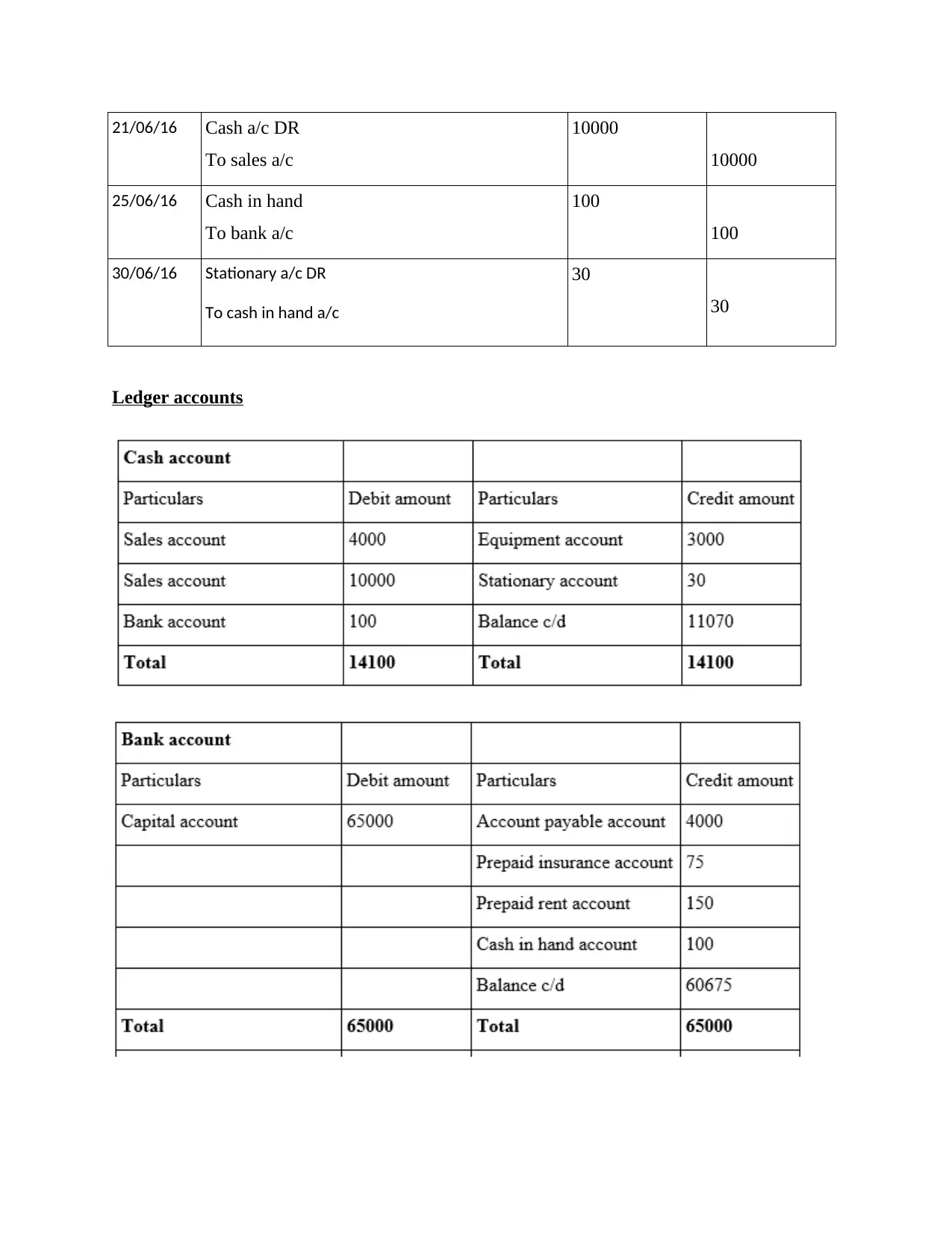

21/06/16 Cash a/c DR

To sales a/c

10000

10000

25/06/16 Cash in hand

To bank a/c

100

100

30/06/16 Stationary a/c DR

To cash in hand a/c

30

30

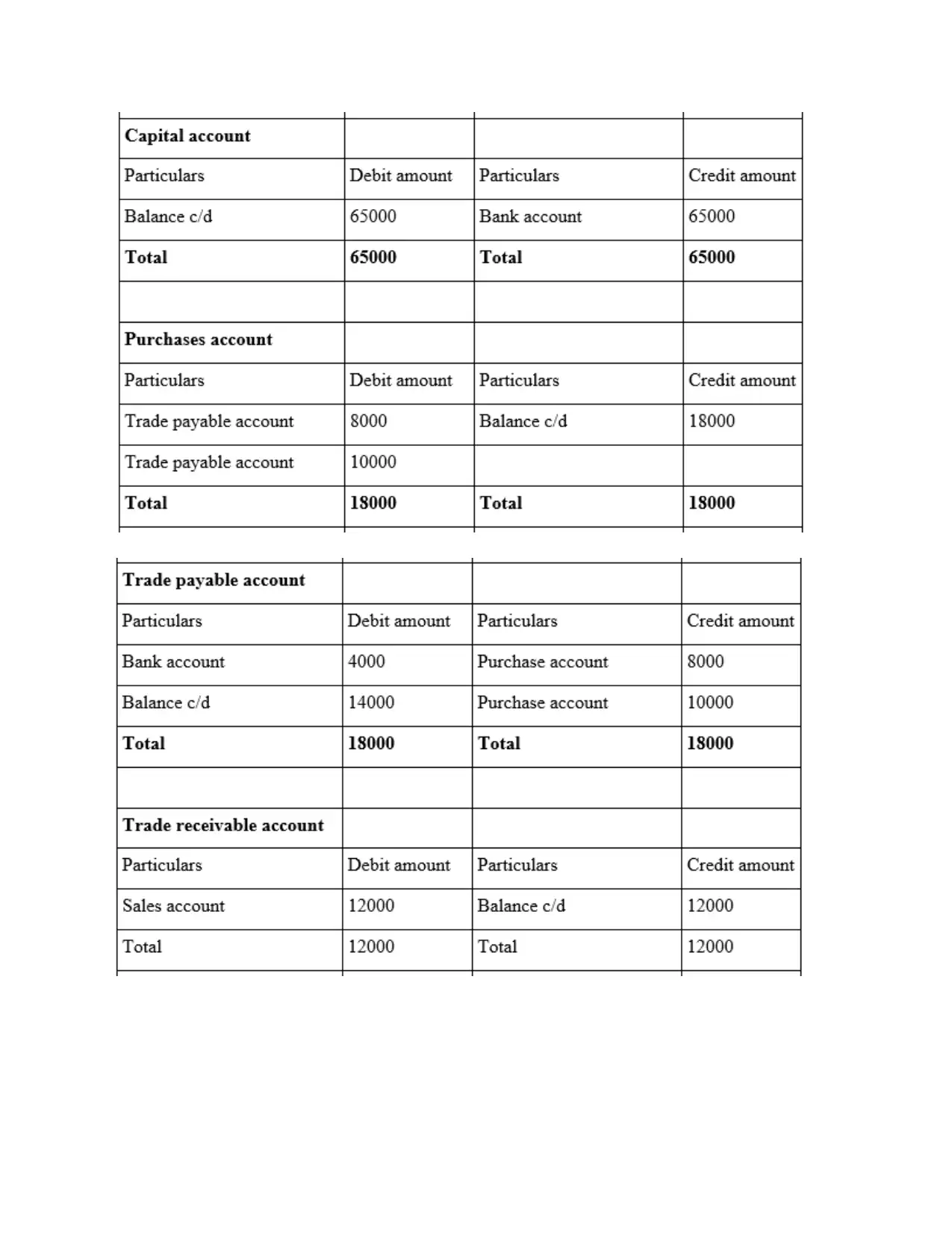

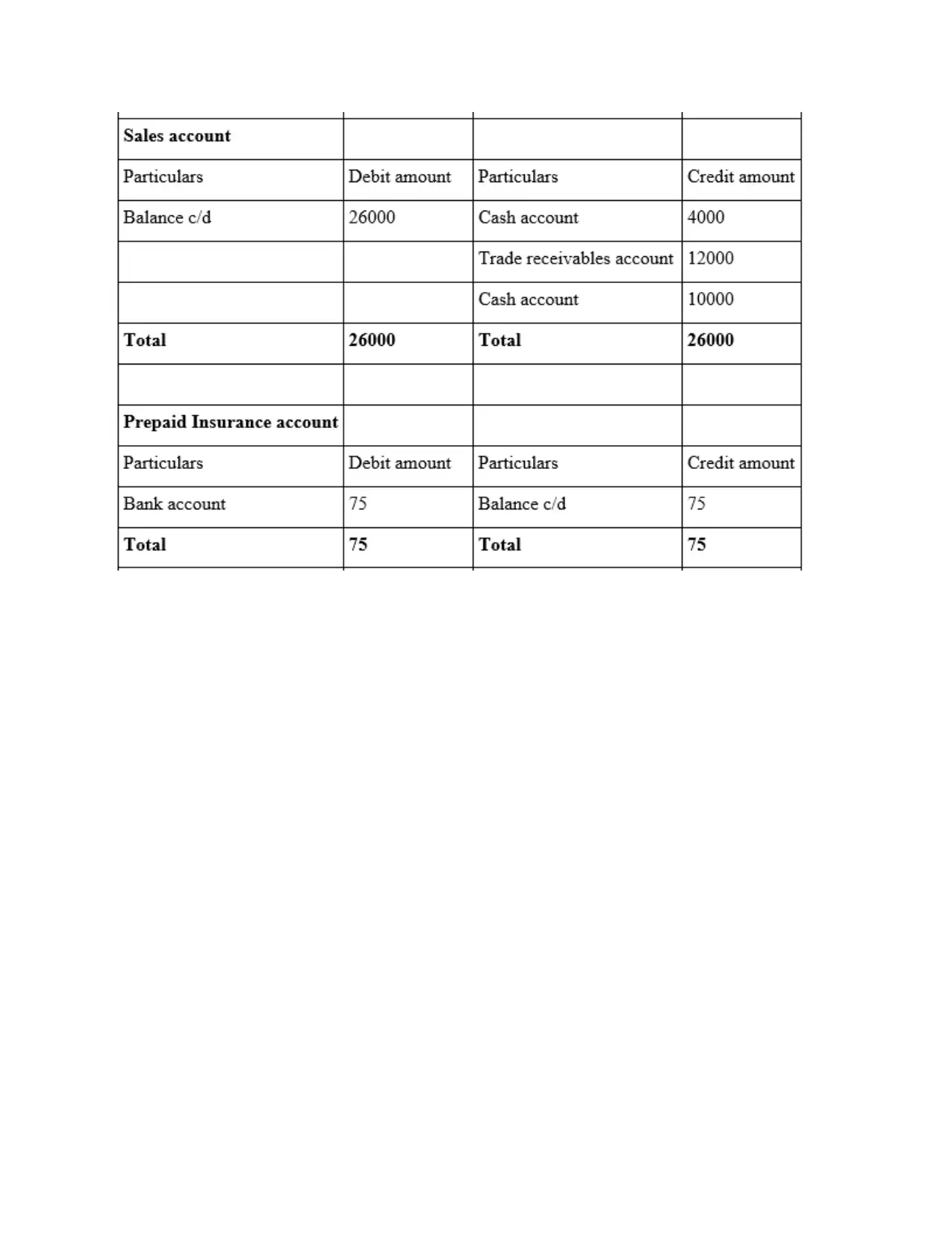

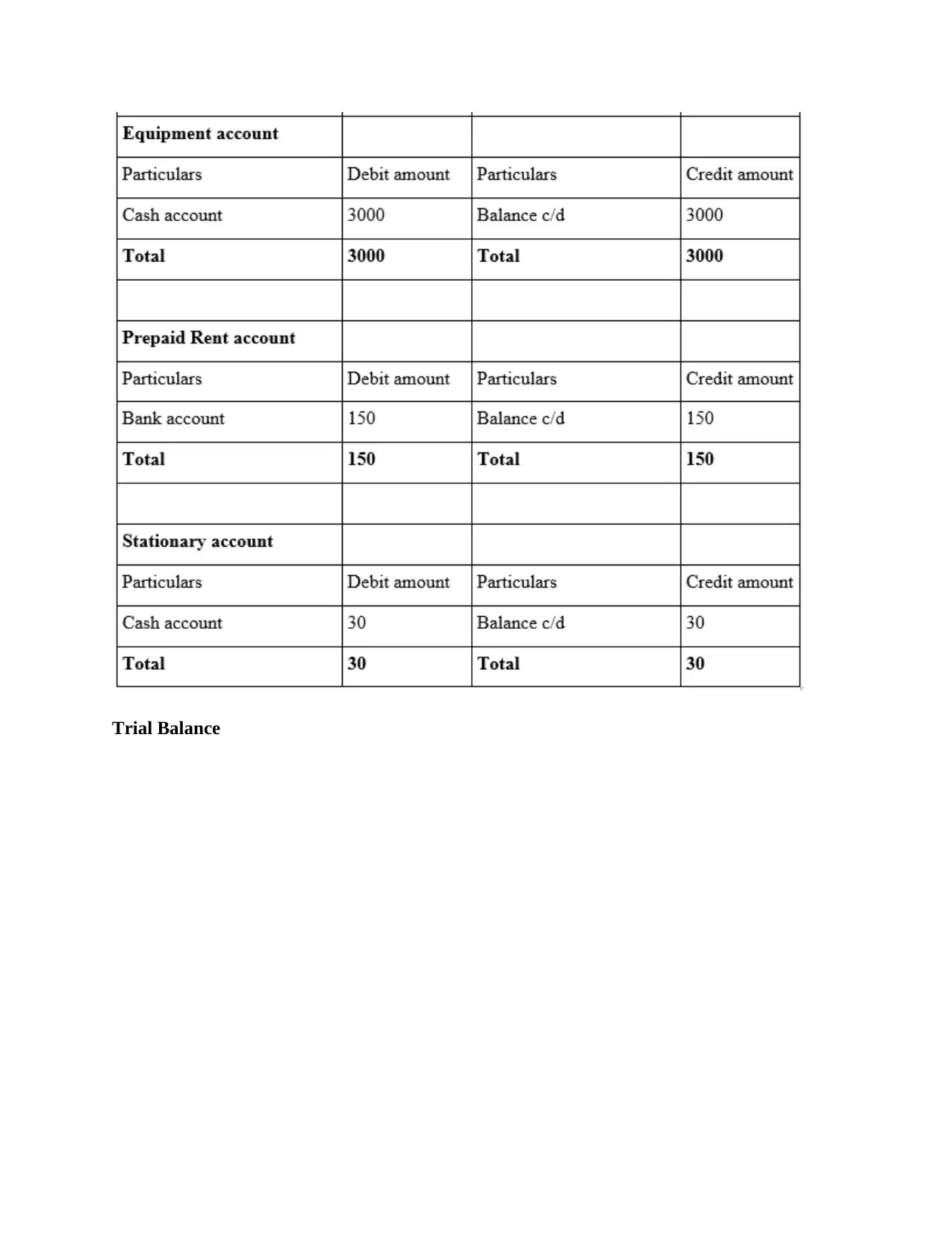

Ledger accounts

To sales a/c

10000

10000

25/06/16 Cash in hand

To bank a/c

100

100

30/06/16 Stationary a/c DR

To cash in hand a/c

30

30

Ledger accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

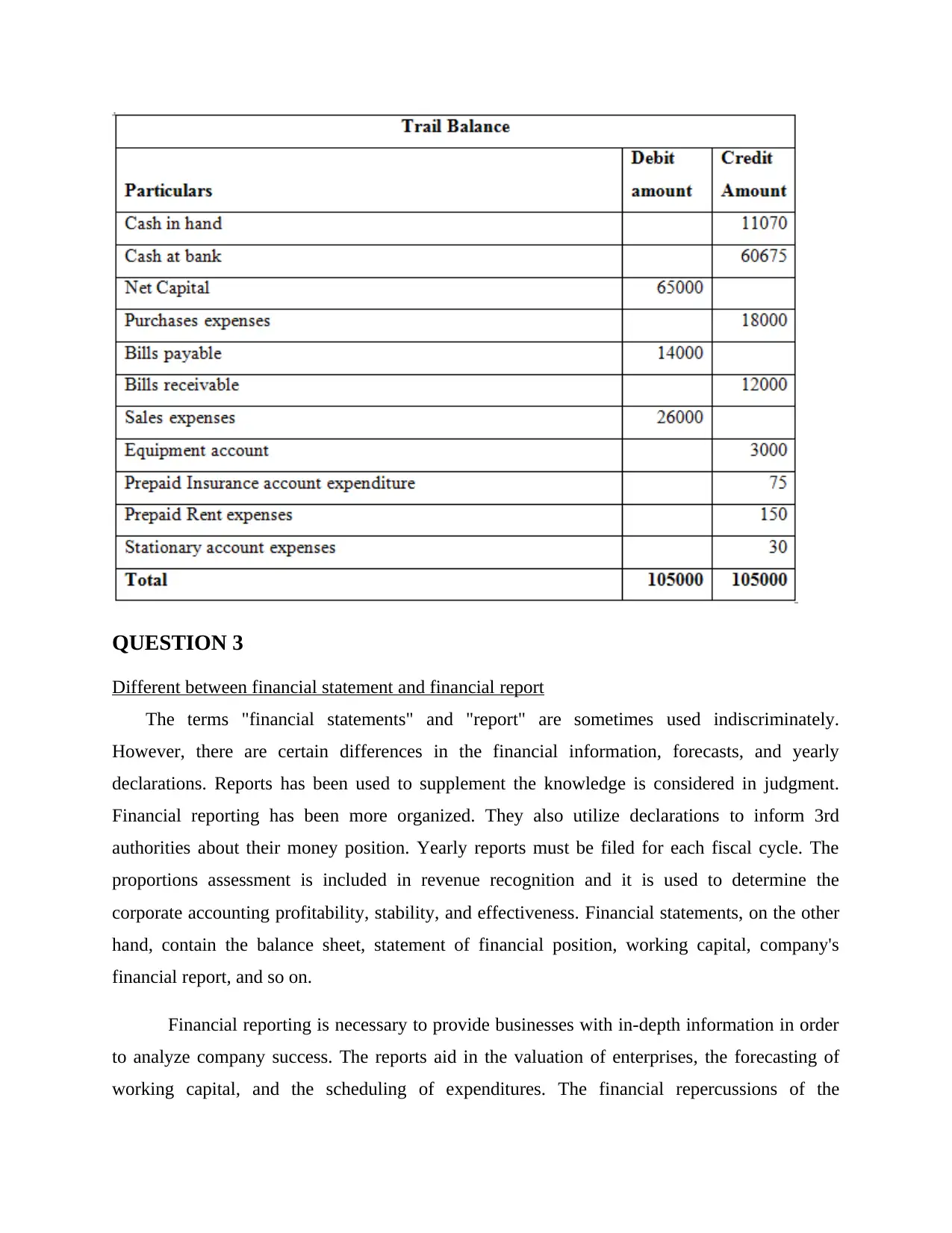

Trial Balance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

QUESTION 3

Different between financial statement and financial report

The terms "financial statements" and "report" are sometimes used indiscriminately.

However, there are certain differences in the financial information, forecasts, and yearly

declarations. Reports has been used to supplement the knowledge is considered in judgment.

Financial reporting has been more organized. They also utilize declarations to inform 3rd

authorities about their money position. Yearly reports must be filed for each fiscal cycle. The

proportions assessment is included in revenue recognition and it is used to determine the

corporate accounting profitability, stability, and effectiveness. Financial statements, on the other

hand, contain the balance sheet, statement of financial position, working capital, company's

financial report, and so on.

Financial reporting is necessary to provide businesses with in-depth information in order

to analyze company success. The reports aid in the valuation of enterprises, the forecasting of

working capital, and the scheduling of expenditures. The financial repercussions of the

Different between financial statement and financial report

The terms "financial statements" and "report" are sometimes used indiscriminately.

However, there are certain differences in the financial information, forecasts, and yearly

declarations. Reports has been used to supplement the knowledge is considered in judgment.

Financial reporting has been more organized. They also utilize declarations to inform 3rd

authorities about their money position. Yearly reports must be filed for each fiscal cycle. The

proportions assessment is included in revenue recognition and it is used to determine the

corporate accounting profitability, stability, and effectiveness. Financial statements, on the other

hand, contain the balance sheet, statement of financial position, working capital, company's

financial report, and so on.

Financial reporting is necessary to provide businesses with in-depth information in order

to analyze company success. The reports aid in the valuation of enterprises, the forecasting of

working capital, and the scheduling of expenditures. The financial repercussions of the

corporation's choices are shown in the accounting in the documents. Some of these documents

are for internal use, while others are utilized by other organizations. Bankers, financiers, and

public officials scrutinize the corporate accounting records. They may also need to impose

adherence limitations on revenue recognition to other authorities in order to assure uniformity.

With each document they prepare, they should take a reasoned approach.

In the perspective of Brightstar Financial Company, there are many examples of financial

accounting, which are addressed elsewhere here:

Leader: Partners and owner make government technology to help them evaluate either to hold,

borrow, or offer so much of their properties.

Owners: Managers may even be calculated and the results. In new enterprises, although, model

is commonly consisted of skilled employees who have also been responsible the administering

the enterprise or an industry sector. They act as a means of platform independent brokers.

Executives: Those other researchers are concerned about either the intermediate and long

existence or viability. They're all over whether or not organisation can paying members' wages

and bring discounts. They may also be participating in the financial condition and outcomes in

addition to assessing client services and profession promotion opportunity.

Buyers: Unless an allowing firms have had a heavier or commitment, shoppers grow committed

in the person's capacity to sustain its appearance and establish overall quality. This necessity is

intensified in conditions at which employee’s consumers depend on something.

Funders: Equity financing is essential with institutional clients in evaluate the manufacturer's

financial performance. Independent big corporations, too, involve public data and evaluate how

well an investment is worthwhile or that it should be completed, altered, or scrapped.

While its percentage of users who’s provided government accounting is minimal, there were

some who could otherwise think critically. Investors and creditors facts would be both direct and

indirect. In almost the same method, Brightstar compiles accounting records for its subscribers.

are for internal use, while others are utilized by other organizations. Bankers, financiers, and

public officials scrutinize the corporate accounting records. They may also need to impose

adherence limitations on revenue recognition to other authorities in order to assure uniformity.

With each document they prepare, they should take a reasoned approach.

In the perspective of Brightstar Financial Company, there are many examples of financial

accounting, which are addressed elsewhere here:

Leader: Partners and owner make government technology to help them evaluate either to hold,

borrow, or offer so much of their properties.

Owners: Managers may even be calculated and the results. In new enterprises, although, model

is commonly consisted of skilled employees who have also been responsible the administering

the enterprise or an industry sector. They act as a means of platform independent brokers.

Executives: Those other researchers are concerned about either the intermediate and long

existence or viability. They're all over whether or not organisation can paying members' wages

and bring discounts. They may also be participating in the financial condition and outcomes in

addition to assessing client services and profession promotion opportunity.

Buyers: Unless an allowing firms have had a heavier or commitment, shoppers grow committed

in the person's capacity to sustain its appearance and establish overall quality. This necessity is

intensified in conditions at which employee’s consumers depend on something.

Funders: Equity financing is essential with institutional clients in evaluate the manufacturer's

financial performance. Independent big corporations, too, involve public data and evaluate how

well an investment is worthwhile or that it should be completed, altered, or scrapped.

While its percentage of users who’s provided government accounting is minimal, there were

some who could otherwise think critically. Investors and creditors facts would be both direct and

indirect. In almost the same method, Brightstar compiles accounting records for its subscribers.

QUESTION 4

Principles of accounting

There are mentioned some principles of accounting which is used by the most of the

business entity such as:

Business entity: A company is regarded a separate company from its proprietors and should be

handled as such. Privatizing of the operator ought not to be documented in the entity's balance

sheet of the firm, and vice versa. Because if the sole proprietor record contains the firm acquiring

and/or extracting funds.

Going concern: It is presumptively assumed that an object will remain viable perpetually. Items

are documented using this method based on their initial cost rather than selling price. Assets are

considered to be utilized indefinitely and are not meant to be transferred right away.

Monetary unit: Economic activities in the firm should be collected and processed in financial

terms also including INR, US Dollar, Canadian Dollar, Euro, and so on. As a result, any non-

monetary knowledge that can still be quantified in dollar amounts will be entered in a statement

rather than in the general ledger.

Historical cost: The real cash comparable or unique expense of purchase should be used to

assess and preserve all products and services received, not the current valuation or projected

worth. Unless an organization is in the process of buying and dissolution, there was an exception

to norm.

Matching concept: This concept states that in order to reflect the real profit of a firm, every

dollar of profit reported in a sales transaction must be matched by an equal amount of cost.

Accounting period: This principle requires a company to finish its whole accounting procedure

within a defined operational time frame. It might be reviewed on an ongoing, weekly, or annual

basis. It is essential to observe a Calendar or Fiscal Year for the yearly accounting cycle.

Conservatism: This concept argues that whenever two choices for valuing exchange of goods

and services are presented, the lesser worth should be reported than about the greater.

Principles of accounting

There are mentioned some principles of accounting which is used by the most of the

business entity such as:

Business entity: A company is regarded a separate company from its proprietors and should be

handled as such. Privatizing of the operator ought not to be documented in the entity's balance

sheet of the firm, and vice versa. Because if the sole proprietor record contains the firm acquiring

and/or extracting funds.

Going concern: It is presumptively assumed that an object will remain viable perpetually. Items

are documented using this method based on their initial cost rather than selling price. Assets are

considered to be utilized indefinitely and are not meant to be transferred right away.

Monetary unit: Economic activities in the firm should be collected and processed in financial

terms also including INR, US Dollar, Canadian Dollar, Euro, and so on. As a result, any non-

monetary knowledge that can still be quantified in dollar amounts will be entered in a statement

rather than in the general ledger.

Historical cost: The real cash comparable or unique expense of purchase should be used to

assess and preserve all products and services received, not the current valuation or projected

worth. Unless an organization is in the process of buying and dissolution, there was an exception

to norm.

Matching concept: This concept states that in order to reflect the real profit of a firm, every

dollar of profit reported in a sales transaction must be matched by an equal amount of cost.

Accounting period: This principle requires a company to finish its whole accounting procedure

within a defined operational time frame. It might be reviewed on an ongoing, weekly, or annual

basis. It is essential to observe a Calendar or Fiscal Year for the yearly accounting cycle.

Conservatism: This concept argues that whenever two choices for valuing exchange of goods

and services are presented, the lesser worth should be reported than about the greater.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Consistency: This concept guarantees that the corporate individual's budgetary control is

consistent from one accounting cycle to another. It makes it possible to compare financial data

from two balance sheets fairly.

Materiality: In an ideal world, economic activities that may influence a user's financial choice

would be deemed vital or substantial, and so would need to be appropriately disclosed. This

approach allows for SharePoint mistakes or breaches concerning insignificant and modest

amounts of documented company transactions.

Objectivity: This concept dictates that all documented company operations be accompanied by

some sort of objective documentation or paperwork. It also implies that accounting and business

records should be done independently, without suspicion of wrongdoing.

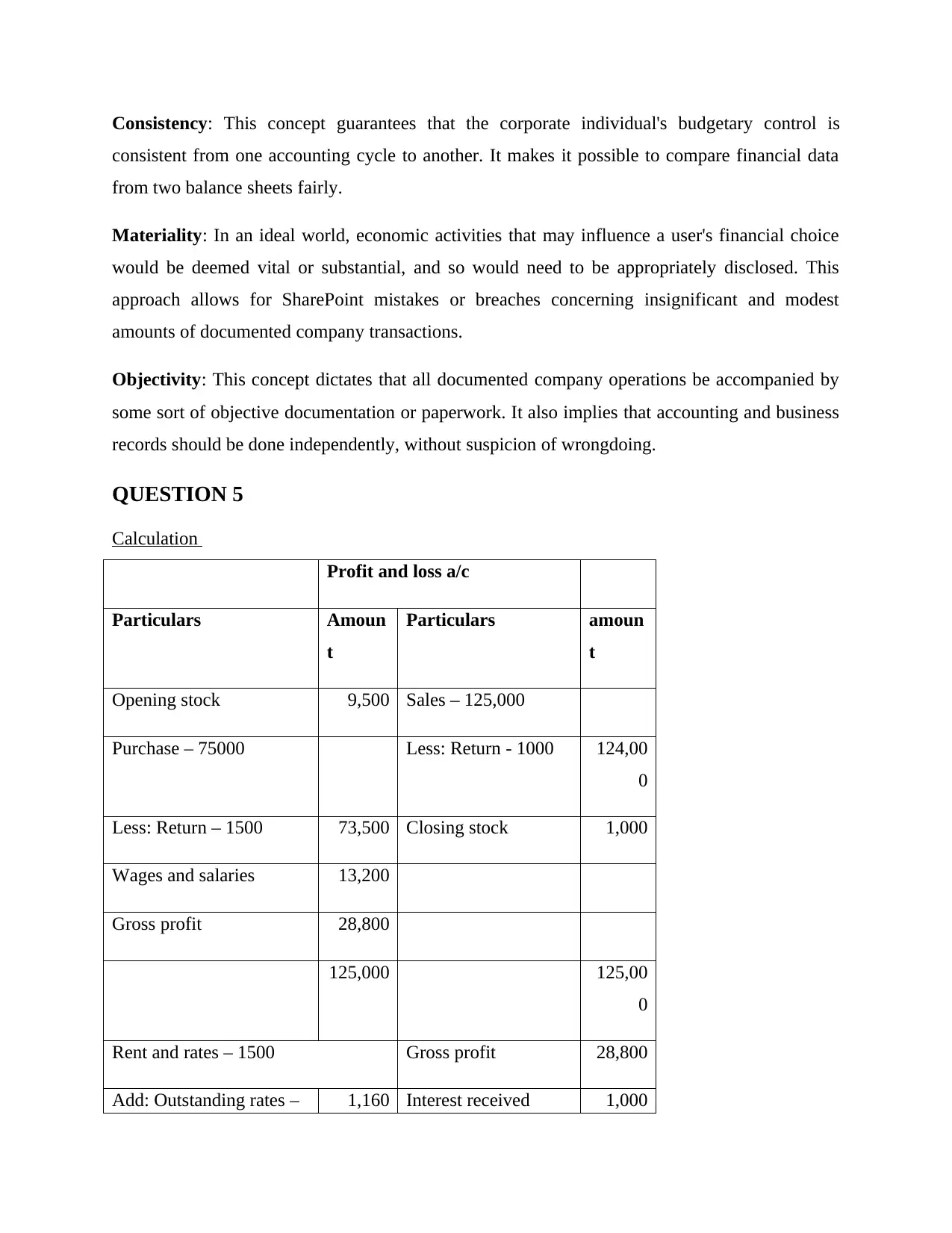

QUESTION 5

Calculation

Profit and loss a/c

Particulars Amoun

t

Particulars amoun

t

Opening stock 9,500 Sales – 125,000

Purchase – 75000 Less: Return - 1000 124,00

0

Less: Return – 1500 73,500 Closing stock 1,000

Wages and salaries 13,200

Gross profit 28,800

125,000 125,00

0

Rent and rates – 1500 Gross profit 28,800

Add: Outstanding rates – 1,160 Interest received 1,000

consistent from one accounting cycle to another. It makes it possible to compare financial data

from two balance sheets fairly.

Materiality: In an ideal world, economic activities that may influence a user's financial choice

would be deemed vital or substantial, and so would need to be appropriately disclosed. This

approach allows for SharePoint mistakes or breaches concerning insignificant and modest

amounts of documented company transactions.

Objectivity: This concept dictates that all documented company operations be accompanied by

some sort of objective documentation or paperwork. It also implies that accounting and business

records should be done independently, without suspicion of wrongdoing.

QUESTION 5

Calculation

Profit and loss a/c

Particulars Amoun

t

Particulars amoun

t

Opening stock 9,500 Sales – 125,000

Purchase – 75000 Less: Return - 1000 124,00

0

Less: Return – 1500 73,500 Closing stock 1,000

Wages and salaries 13,200

Gross profit 28,800

125,000 125,00

0

Rent and rates – 1500 Gross profit 28,800

Add: Outstanding rates – 1,160 Interest received 1,000

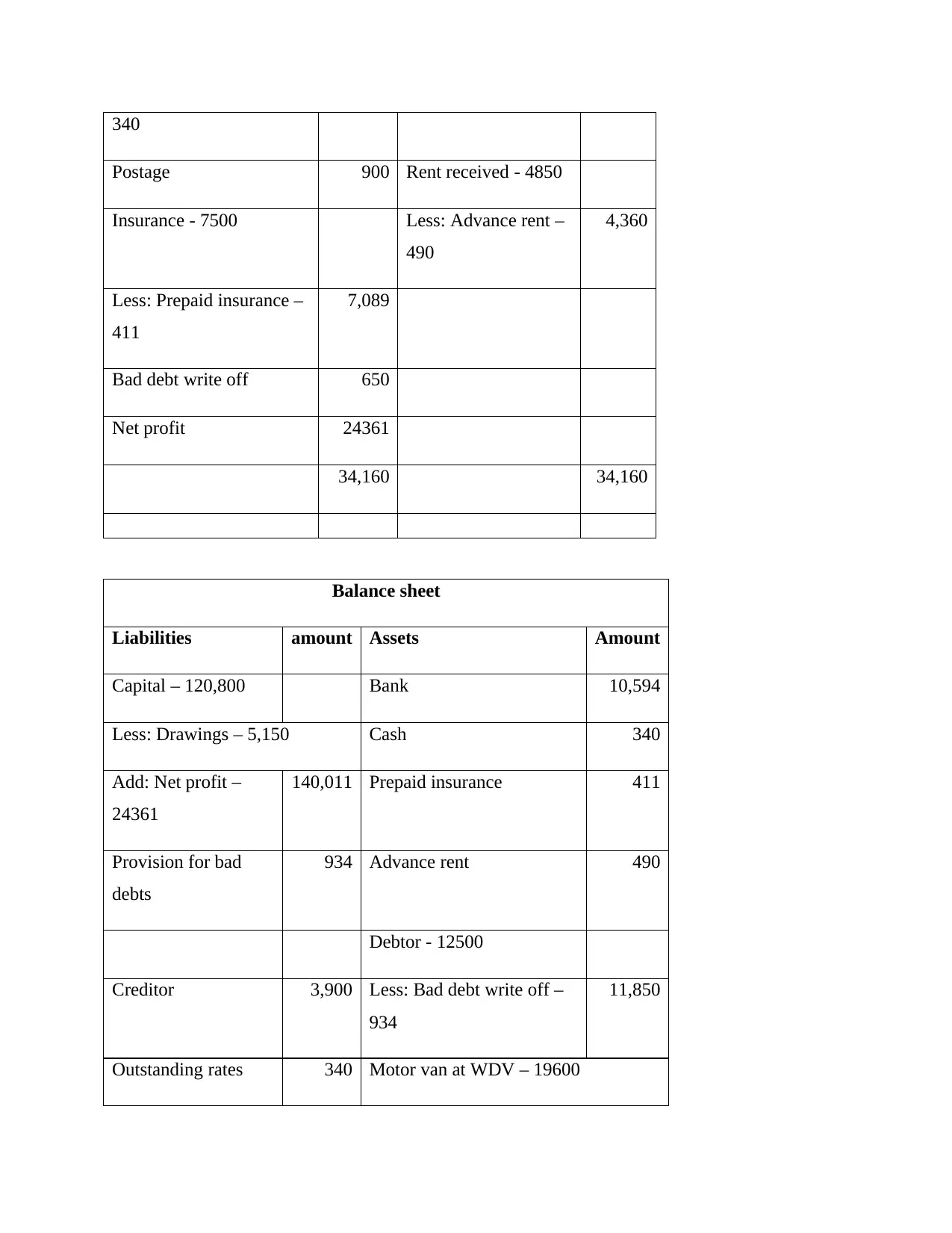

340

Postage 900 Rent received - 4850

Insurance - 7500 Less: Advance rent –

490

4,360

Less: Prepaid insurance –

411

7,089

Bad debt write off 650

Net profit 24361

34,160 34,160

Balance sheet

Liabilities amount Assets Amount

Capital – 120,800 Bank 10,594

Less: Drawings – 5,150 Cash 340

Add: Net profit –

24361

140,011 Prepaid insurance 411

Provision for bad

debts

934 Advance rent 490

Debtor - 12500

Creditor 3,900 Less: Bad debt write off –

934

11,850

Outstanding rates 340 Motor van at WDV – 19600

Postage 900 Rent received - 4850

Insurance - 7500 Less: Advance rent –

490

4,360

Less: Prepaid insurance –

411

7,089

Bad debt write off 650

Net profit 24361

34,160 34,160

Balance sheet

Liabilities amount Assets Amount

Capital – 120,800 Bank 10,594

Less: Drawings – 5,150 Cash 340

Add: Net profit –

24361

140,011 Prepaid insurance 411

Provision for bad

debts

934 Advance rent 490

Debtor - 12500

Creditor 3,900 Less: Bad debt write off –

934

11,850

Outstanding rates 340 Motor van at WDV – 19600

Less: Dep - 5000 14,600

Loan 100,000

Closing stock 1,000

145,185 145,185

QUESTION 6

Profit and Loss Account

Loan 100,000

Closing stock 1,000

145,185 145,185

QUESTION 6

Profit and Loss Account

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

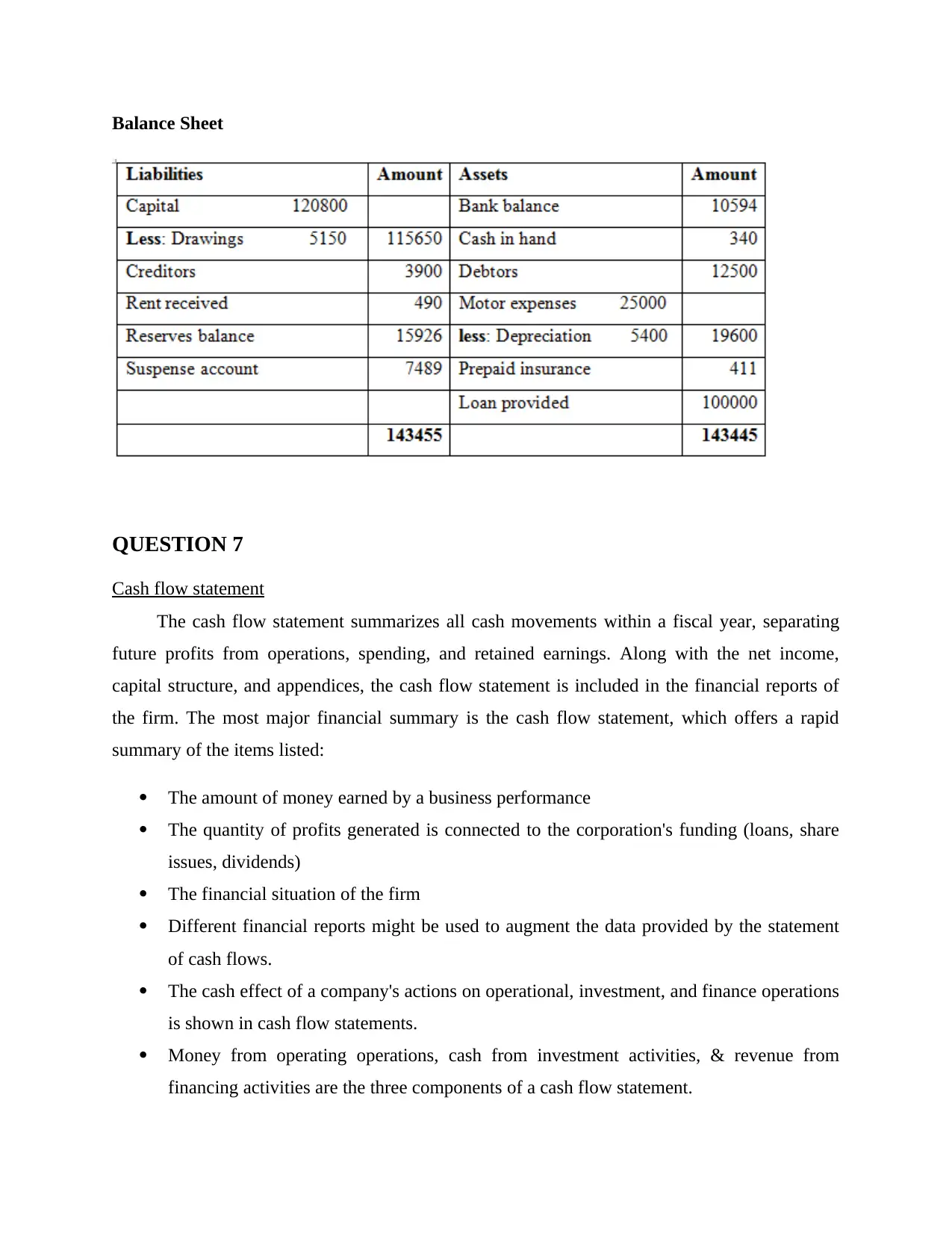

Balance Sheet

QUESTION 7

Cash flow statement

The cash flow statement summarizes all cash movements within a fiscal year, separating

future profits from operations, spending, and retained earnings. Along with the net income,

capital structure, and appendices, the cash flow statement is included in the financial reports of

the firm. The most major financial summary is the cash flow statement, which offers a rapid

summary of the items listed:

The amount of money earned by a business performance

The quantity of profits generated is connected to the corporation's funding (loans, share

issues, dividends)

The financial situation of the firm

Different financial reports might be used to augment the data provided by the statement

of cash flows.

The cash effect of a company's actions on operational, investment, and finance operations

is shown in cash flow statements.

Money from operating operations, cash from investment activities, & revenue from

financing activities are the three components of a cash flow statement.

QUESTION 7

Cash flow statement

The cash flow statement summarizes all cash movements within a fiscal year, separating

future profits from operations, spending, and retained earnings. Along with the net income,

capital structure, and appendices, the cash flow statement is included in the financial reports of

the firm. The most major financial summary is the cash flow statement, which offers a rapid

summary of the items listed:

The amount of money earned by a business performance

The quantity of profits generated is connected to the corporation's funding (loans, share

issues, dividends)

The financial situation of the firm

Different financial reports might be used to augment the data provided by the statement

of cash flows.

The cash effect of a company's actions on operational, investment, and finance operations

is shown in cash flow statements.

Money from operating operations, cash from investment activities, & revenue from

financing activities are the three components of a cash flow statement.

There are two ways for preparing a cash flow statement: directly and indirectly.

Changes in cash collections and expenditures are calculated using the direct approach. To

calculate inferred working capital, the indirectly process encompasses period started net

revenue and inserts or removes movements in the balance sheet categories.

Modifications in accounts receivable are a crucial part for every business.

Property purchases, amount owed on borrowing, and expenditures connected to leveraged

buyouts should all be included in your investment activities.

Profit and loss statement isn't necessarily a reason for concern; some companies opt to

invest so much to achieve their objectives, and they may need to depend on borrowing to

get back on track.

Between both the income statement and balance statement, the cash flow statement acts as a link.

There are four main factors for the importance of a cash flow statement:

1. It exposes a company's liquidity; individuals understand however much cash they have

on hand and, as a result, their anticipated horizon till cash runs out.

2. It shows how assets, obligations, and capital have changed over time.

3. It removes the impact of differing bookkeeping systems (for illustration, private money

versus absorption costing), allowing investors to evaluate the business results of several

companies more easily.

4. It assists in analyzing and forecasting the quantity, timeliness, and likelihood of future

financial requirements.

For example:

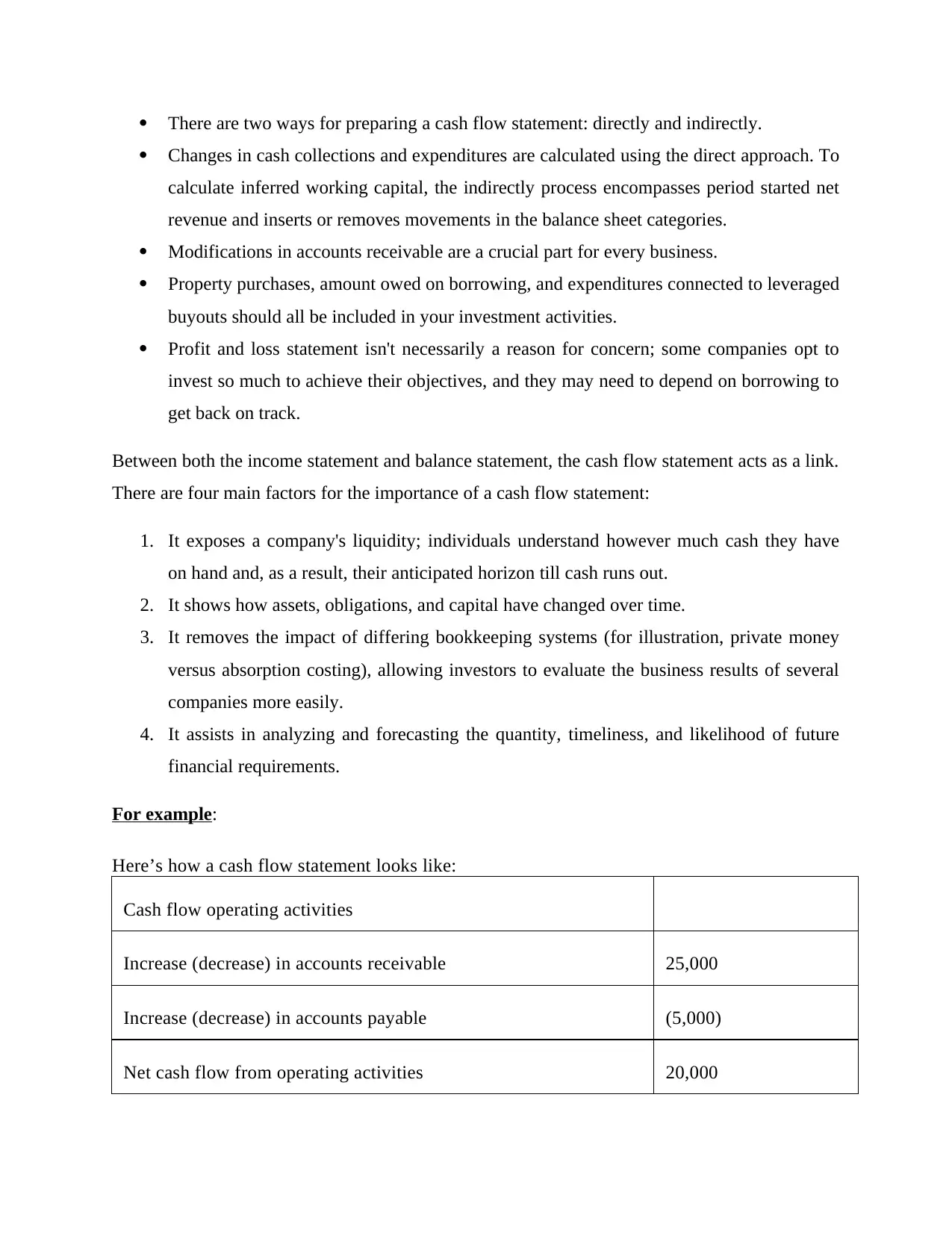

Here’s how a cash flow statement looks like:

Cash flow operating activities

Increase (decrease) in accounts receivable 25,000

Increase (decrease) in accounts payable (5,000)

Net cash flow from operating activities 20,000

Changes in cash collections and expenditures are calculated using the direct approach. To

calculate inferred working capital, the indirectly process encompasses period started net

revenue and inserts or removes movements in the balance sheet categories.

Modifications in accounts receivable are a crucial part for every business.

Property purchases, amount owed on borrowing, and expenditures connected to leveraged

buyouts should all be included in your investment activities.

Profit and loss statement isn't necessarily a reason for concern; some companies opt to

invest so much to achieve their objectives, and they may need to depend on borrowing to

get back on track.

Between both the income statement and balance statement, the cash flow statement acts as a link.

There are four main factors for the importance of a cash flow statement:

1. It exposes a company's liquidity; individuals understand however much cash they have

on hand and, as a result, their anticipated horizon till cash runs out.

2. It shows how assets, obligations, and capital have changed over time.

3. It removes the impact of differing bookkeeping systems (for illustration, private money

versus absorption costing), allowing investors to evaluate the business results of several

companies more easily.

4. It assists in analyzing and forecasting the quantity, timeliness, and likelihood of future

financial requirements.

For example:

Here’s how a cash flow statement looks like:

Cash flow operating activities

Increase (decrease) in accounts receivable 25,000

Increase (decrease) in accounts payable (5,000)

Net cash flow from operating activities 20,000

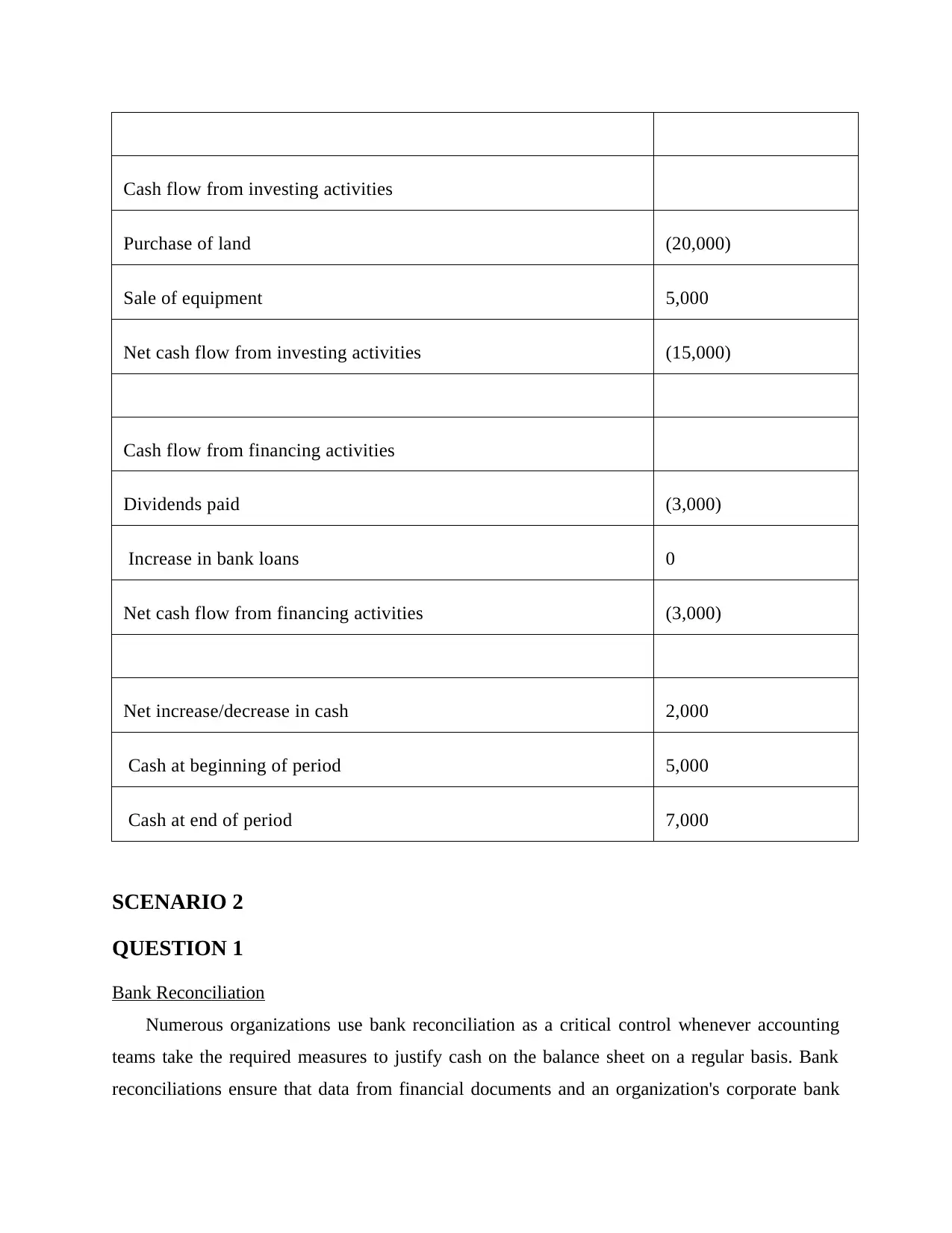

Cash flow from investing activities

Purchase of land (20,000)

Sale of equipment 5,000

Net cash flow from investing activities (15,000)

Cash flow from financing activities

Dividends paid (3,000)

Increase in bank loans 0

Net cash flow from financing activities (3,000)

Net increase/decrease in cash 2,000

Cash at beginning of period 5,000

Cash at end of period 7,000

SCENARIO 2

QUESTION 1

Bank Reconciliation

Numerous organizations use bank reconciliation as a critical control whenever accounting

teams take the required measures to justify cash on the balance sheet on a regular basis. Bank

reconciliations ensure that data from financial documents and an organization's corporate bank

Purchase of land (20,000)

Sale of equipment 5,000

Net cash flow from investing activities (15,000)

Cash flow from financing activities

Dividends paid (3,000)

Increase in bank loans 0

Net cash flow from financing activities (3,000)

Net increase/decrease in cash 2,000

Cash at beginning of period 5,000

Cash at end of period 7,000

SCENARIO 2

QUESTION 1

Bank Reconciliation

Numerous organizations use bank reconciliation as a critical control whenever accounting

teams take the required measures to justify cash on the balance sheet on a regular basis. Bank

reconciliations ensure that data from financial documents and an organization's corporate bank

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

documents is accurate. A reconciliation control is by its very design investigative, identifying

problems like corruption, mistakes, and absent goods just after event, even before the financial

statements are published. Internal control systems, such as bank reconciliations, are in place to

discover problems, and what if there would be a method to carry out the negotiation process in

such a manner that it really prevented mistakes from occurring in the future? It's also worth

noting that all donations are recorded in the credit side of a bank passbook, while all transactions

are recorded in the debit side. As a result, if contributions exceed disbursements, the passbook

displays a credit balance. When transfers exceed contributions, however, a negative balance is

displayed.

A financial statement is a recording of all company's cash activities made by a company.

All money and banking transactions are reported on the debit side of the ledger, according to

financial reporting. The credit side of the cash book is where these transactions are entered, and

the debit side is in which all deposits are recorded. Therefore, the corporate individual's bank

also maintains track of its money transfers. This enables the company to maintain control of its

bank accounts and reconcile cash withdrawals with its accounting books. The passbook amounts

must correspond to the cashbook amounts. However, these equilibriums are not always

consistent. Such discrepancies between both the cash book and the passbook are caused by

scheduling variations in documenting accounts payable and receivable, or by mistakes on the

side of the business organization or the bank while transaction processing. As a result, it's

important to figure out what's causing the discrepancies and make appropriate monetary

improvement in the cash book to assure correctness.

QUESTION 2

Control accounts

Overall accounting in the cost ledger that aggregate the sums of separate bank accounts are

known as control accounts (subsidiary ledger). Application will be processed before at the

balance sheet date in such categories, monthly return averages of activities in associated

accounting system and records. The correctness of the assessment is double-checked using

control accounts. The aggregate of the values of all accounting system in the cash book should

match the value of the control account at any moment.

problems like corruption, mistakes, and absent goods just after event, even before the financial

statements are published. Internal control systems, such as bank reconciliations, are in place to

discover problems, and what if there would be a method to carry out the negotiation process in

such a manner that it really prevented mistakes from occurring in the future? It's also worth

noting that all donations are recorded in the credit side of a bank passbook, while all transactions

are recorded in the debit side. As a result, if contributions exceed disbursements, the passbook

displays a credit balance. When transfers exceed contributions, however, a negative balance is

displayed.

A financial statement is a recording of all company's cash activities made by a company.

All money and banking transactions are reported on the debit side of the ledger, according to

financial reporting. The credit side of the cash book is where these transactions are entered, and

the debit side is in which all deposits are recorded. Therefore, the corporate individual's bank

also maintains track of its money transfers. This enables the company to maintain control of its

bank accounts and reconcile cash withdrawals with its accounting books. The passbook amounts

must correspond to the cashbook amounts. However, these equilibriums are not always

consistent. Such discrepancies between both the cash book and the passbook are caused by

scheduling variations in documenting accounts payable and receivable, or by mistakes on the

side of the business organization or the bank while transaction processing. As a result, it's

important to figure out what's causing the discrepancies and make appropriate monetary

improvement in the cash book to assure correctness.

QUESTION 2

Control accounts

Overall accounting in the cost ledger that aggregate the sums of separate bank accounts are

known as control accounts (subsidiary ledger). Application will be processed before at the

balance sheet date in such categories, monthly return averages of activities in associated

accounting system and records. The correctness of the assessment is double-checked using

control accounts. The aggregate of the values of all accounting system in the cash book should

match the value of the control account at any moment.

In a major business, all of the finances can be stored in a single accounting system, from

which a trial balance can be derived. Subsidiary ledgers including the cash receipts ledger

(selling ledger) as well as the accounting records ledger (buy ledger) will be established in a

bigger company when the activities are too numerous to be monitored by a single individual. The

subsidiary ledgers are now a part of the dual control account, and in order to release a financial

statement, details mostly on accounts on each of the transactions would be required. Control

accounts with each of the financial statements are established in the accounting system to prevent

this scenario.

QUESTION 3

Suspense Account

A suspense account is a temporary account where monies are entered temporarily.

Whenever it's difficult to discover flaws before creating the final accounts, the difference in the

trial balance is moved to a new fictitious and transitory application maintained the "Suspense

Account." To avoid delays in the production of accounting period, a suspense relationship is

required. The disparity is moved to the credit side of the suspense account unless the total debit

balance of the financial statement includes the actual cash balance. Whereas if entire credit

values of the trial balance are more than the total ledger accounts, the discrepancy is moved to

the suspense item's debit side. Since this proper account could not be limited to the amount the

event was logged, the suspense account is utilized. A suspense account is a short-term account

that can be used for a variety of purposes. The following are by far the most prevalent causes.

1. A trial balance can be achieved that does not equal since total debits and calculate residuals

need not match system interacts.

2. A company's accountant understands where to enter the credit side of a deal, but it's not where

to enter the debit, etc.

A provisional suspense account is established in both situations till the matter is addressed.

Many mistakes are also corrected using suspense accounts. A suspense account is one that has a

value determined by the difference between the trial and final balances.

Reasons of drafting suspense account:

which a trial balance can be derived. Subsidiary ledgers including the cash receipts ledger

(selling ledger) as well as the accounting records ledger (buy ledger) will be established in a

bigger company when the activities are too numerous to be monitored by a single individual. The

subsidiary ledgers are now a part of the dual control account, and in order to release a financial

statement, details mostly on accounts on each of the transactions would be required. Control

accounts with each of the financial statements are established in the accounting system to prevent

this scenario.

QUESTION 3

Suspense Account

A suspense account is a temporary account where monies are entered temporarily.

Whenever it's difficult to discover flaws before creating the final accounts, the difference in the

trial balance is moved to a new fictitious and transitory application maintained the "Suspense

Account." To avoid delays in the production of accounting period, a suspense relationship is

required. The disparity is moved to the credit side of the suspense account unless the total debit

balance of the financial statement includes the actual cash balance. Whereas if entire credit

values of the trial balance are more than the total ledger accounts, the discrepancy is moved to

the suspense item's debit side. Since this proper account could not be limited to the amount the

event was logged, the suspense account is utilized. A suspense account is a short-term account

that can be used for a variety of purposes. The following are by far the most prevalent causes.

1. A trial balance can be achieved that does not equal since total debits and calculate residuals

need not match system interacts.

2. A company's accountant understands where to enter the credit side of a deal, but it's not where

to enter the debit, etc.

A provisional suspense account is established in both situations till the matter is addressed.

Many mistakes are also corrected using suspense accounts. A suspense account is one that has a

value determined by the difference between the trial and final balances.

Reasons of drafting suspense account:

When mistakes in the suspense account are discovered, they are corrected using the

suspense account. The suspense account remains in the records till the mistakes are discovered

and corrected. The financial statement will reflect this balance. Upon on financial assets, the debt

balance will be displayed, while on the liability side, the credit balance will be displayed. The

suspense account is completely determined once all mistakes impacting the trial balance have

been identified and corrected.

Whenever trial balance is already out of range or has an unexplained activity and utilizes

suspense account. The suspense account is a general ledger account that serves as a specially

designated bank until the mistake or unexplained activity is detected. They can create a single

accounting period to keep all of the differences unless uncover them when dealing with the

financial statement. Suspense accounts, on the other hand, are transitory records that should be

terminated at the conclusion of the financial accounting.

QUESTION 4

(a) Required to prepare updated cash book and bank reconciliation statement

Updated cash book as at 28th February 2017:

Revised cash Book

Particulars Dr. Particular Cr.

Balance b/d 1760 D.Park 270

Insurance against fire 170 Mr. Akram 105

Monthly bill 56 Bank Collection 325

Arif Paid 186

Bank Charges 25 Balance c/f 1497

suspense account. The suspense account remains in the records till the mistakes are discovered

and corrected. The financial statement will reflect this balance. Upon on financial assets, the debt

balance will be displayed, while on the liability side, the credit balance will be displayed. The

suspense account is completely determined once all mistakes impacting the trial balance have

been identified and corrected.

Whenever trial balance is already out of range or has an unexplained activity and utilizes

suspense account. The suspense account is a general ledger account that serves as a specially

designated bank until the mistake or unexplained activity is detected. They can create a single

accounting period to keep all of the differences unless uncover them when dealing with the

financial statement. Suspense accounts, on the other hand, are transitory records that should be

terminated at the conclusion of the financial accounting.

QUESTION 4

(a) Required to prepare updated cash book and bank reconciliation statement

Updated cash book as at 28th February 2017:

Revised cash Book

Particulars Dr. Particular Cr.

Balance b/d 1760 D.Park 270

Insurance against fire 170 Mr. Akram 105

Monthly bill 56 Bank Collection 325

Arif Paid 186

Bank Charges 25 Balance c/f 1497

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2197 2197

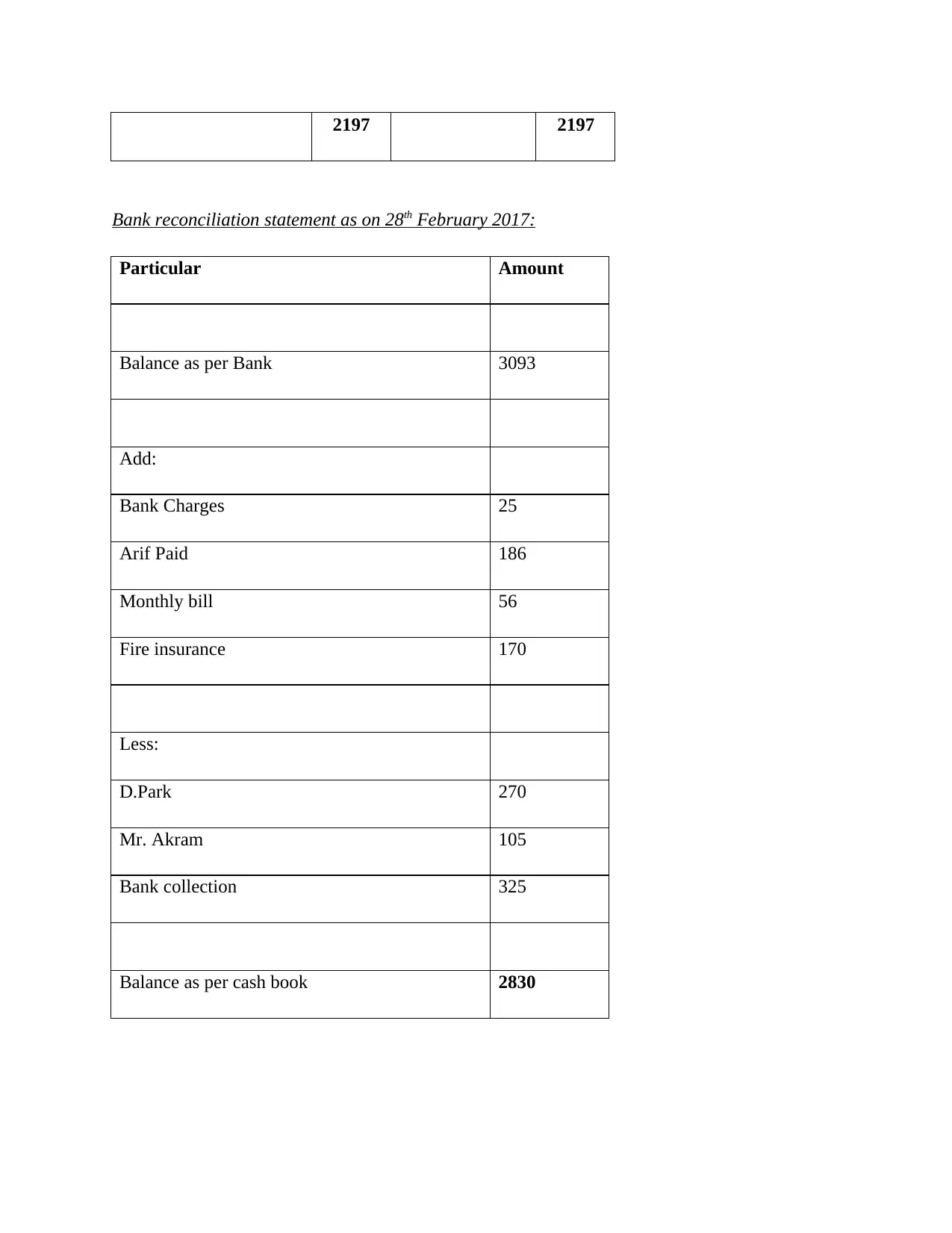

Bank reconciliation statement as on 28th February 2017:

Particular Amount

Balance as per Bank 3093

Add:

Bank Charges 25

Arif Paid 186

Monthly bill 56

Fire insurance 170

Less:

D.Park 270

Mr. Akram 105

Bank collection 325

Balance as per cash book 2830

Bank reconciliation statement as on 28th February 2017:

Particular Amount

Balance as per Bank 3093

Add:

Bank Charges 25

Arif Paid 186

Monthly bill 56

Fire insurance 170

Less:

D.Park 270

Mr. Akram 105

Bank collection 325

Balance as per cash book 2830

QUESTION 5

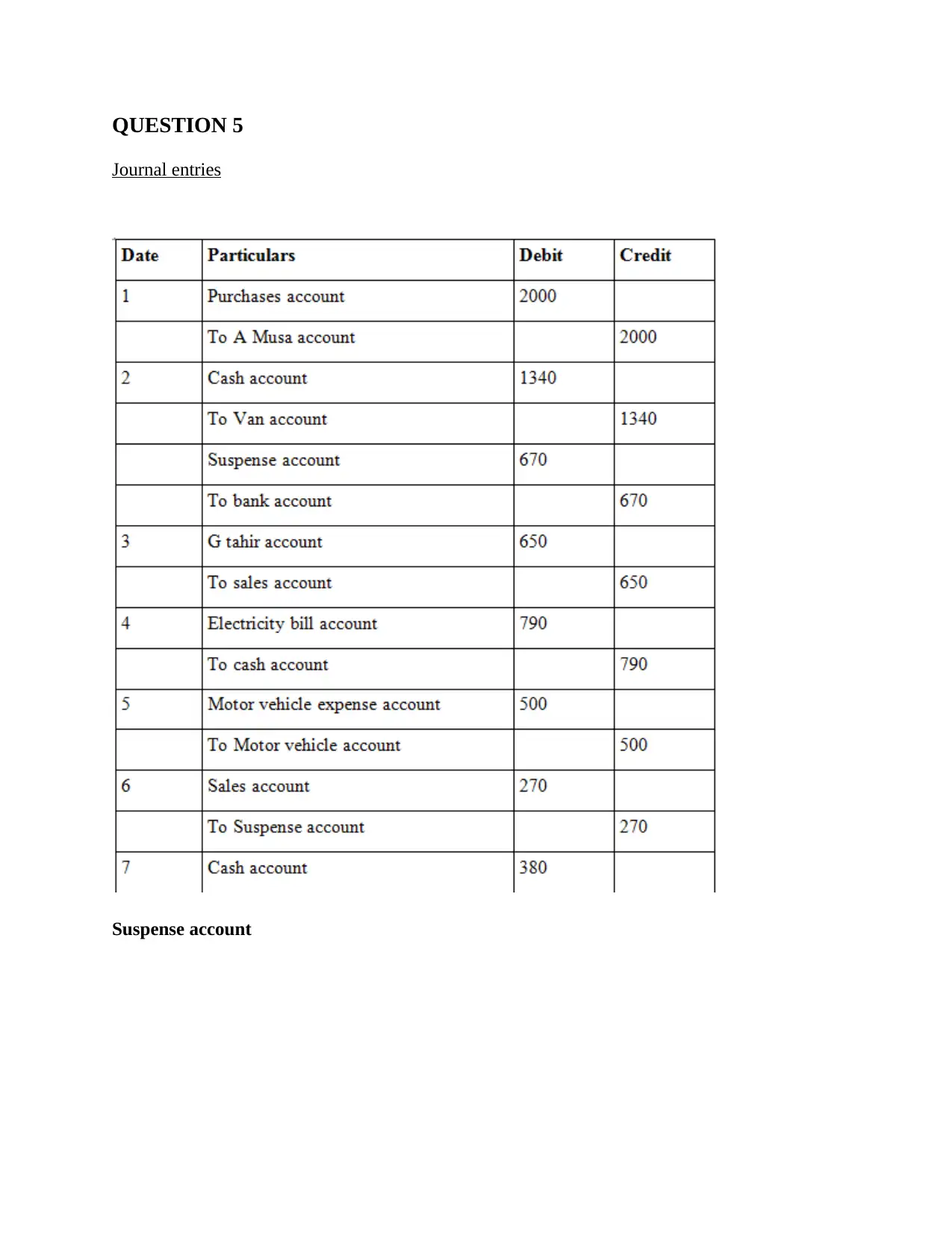

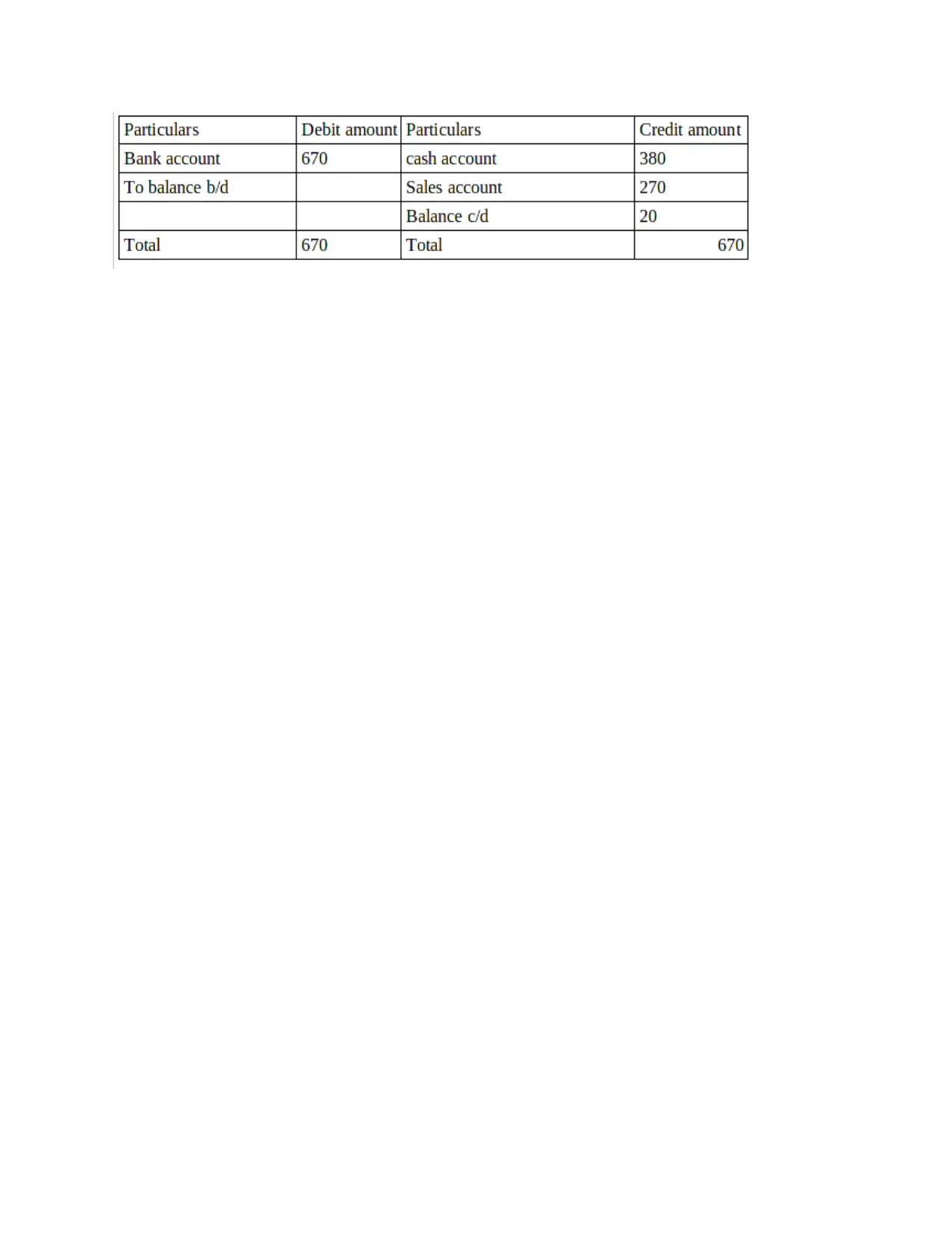

Journal entries

Suspense account

Journal entries

Suspense account

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

As per the above report it has been concluded that financial accounting is the practice of

methodically recording business dealings in the firm's multiple balance sheet in terms of

generating financial statements. Financial accounting exclusively examines operations of a

questionable nature, that is, operations that have already occurred. Forwarded have no position in

financial accounting, irrespective matter how essential they are from a marketing perspective.

As per the above report it has been concluded that financial accounting is the practice of

methodically recording business dealings in the firm's multiple balance sheet in terms of

generating financial statements. Financial accounting exclusively examines operations of a

questionable nature, that is, operations that have already occurred. Forwarded have no position in

financial accounting, irrespective matter how essential they are from a marketing perspective.

REFERENCES

Books and Journal

Karabarbounis, L. and Neiman, B., 2019. Accounting for factorless income. NBER

Macroeconomics Annual. 33(1). pp.167-228.

Loft, A., 2020. Understanding accounting in its social and historical context: the case of cost

accounting in Britain, 1914-1925. Routledge.

Tingey-Holyoak, J. L and et.al, 2020. Water productivity accounting in Australian agriculture:

The need for cost-informed decision-making. Outlook on Agriculture. 49(2). pp.172-

184.

Brusca, I. and Martínez, J. C., 2016. Adopting international public sector accounting standards:

A challenge for modernizing and harmonizing public sector accounting. International

Review of Administrative Sciences. 82(4). pp.724-744.

Belesis, N., Sorros, J. and Karagiorgos, A., 2020. Financial Market Data Versus Accounting

Data: Which Better Explains Stock Returns?. International Advances in Economic

Research, pp.1-14.

Florou, A., Kosi, U. and Pope, P. F., 2017. Are international accounting standards more credit

relevant than domestic standards?. Accounting and Business Research. 47(1). pp.1-29.

Laaksonen, J., 2020. International comparability and translation: how is the concept of

equivalence used and understood in accounting research?. Accounting, Auditing &

Accountability Journal.

Laux, V. and Stocken, P. C., 2018. Accounting standards, regulatory enforcement, and

innovation. Journal of Accounting and Economics. 65(2-3). pp.221-236.

Baskerville, R. and Grossi, G., 2019. Glocalization of accounting standards: Observations on

neo-institutionalism of IPSAS. Public Money & Management. 39(2). pp.95-103.

Moy, M. and et.al, 2020. Conditional accounting conservatism: Exploring the impact of changes

in institutional frameworks in four countries. Journal of Contemporary Accounting &

Economics. 16(3). p.100214.

Bergmann, A. and Fuchs, S., 2017. Accounting standards for complex resources of international

organizations. Global Policy, 8, pp.26-35.

Mnif Sellami, Y. and Gafsi, Y., 2019. Institutional and economic factors affecting the adoption

of international public sector accounting standards. International Journal of Public

Administration. 42(2). pp.119-131.

Shamsudin, A. and et.al, 2020. Utilising SATA in Measuring Students’ Understanding of

Financial Statements: A Survey among Non-Accounting Students. Jurnal Dinamika

Akuntansi. 12(1). pp.24-33.

Books and Journal

Karabarbounis, L. and Neiman, B., 2019. Accounting for factorless income. NBER

Macroeconomics Annual. 33(1). pp.167-228.

Loft, A., 2020. Understanding accounting in its social and historical context: the case of cost

accounting in Britain, 1914-1925. Routledge.

Tingey-Holyoak, J. L and et.al, 2020. Water productivity accounting in Australian agriculture:

The need for cost-informed decision-making. Outlook on Agriculture. 49(2). pp.172-

184.

Brusca, I. and Martínez, J. C., 2016. Adopting international public sector accounting standards:

A challenge for modernizing and harmonizing public sector accounting. International

Review of Administrative Sciences. 82(4). pp.724-744.

Belesis, N., Sorros, J. and Karagiorgos, A., 2020. Financial Market Data Versus Accounting

Data: Which Better Explains Stock Returns?. International Advances in Economic

Research, pp.1-14.

Florou, A., Kosi, U. and Pope, P. F., 2017. Are international accounting standards more credit

relevant than domestic standards?. Accounting and Business Research. 47(1). pp.1-29.

Laaksonen, J., 2020. International comparability and translation: how is the concept of

equivalence used and understood in accounting research?. Accounting, Auditing &

Accountability Journal.

Laux, V. and Stocken, P. C., 2018. Accounting standards, regulatory enforcement, and

innovation. Journal of Accounting and Economics. 65(2-3). pp.221-236.

Baskerville, R. and Grossi, G., 2019. Glocalization of accounting standards: Observations on

neo-institutionalism of IPSAS. Public Money & Management. 39(2). pp.95-103.

Moy, M. and et.al, 2020. Conditional accounting conservatism: Exploring the impact of changes

in institutional frameworks in four countries. Journal of Contemporary Accounting &

Economics. 16(3). p.100214.

Bergmann, A. and Fuchs, S., 2017. Accounting standards for complex resources of international

organizations. Global Policy, 8, pp.26-35.

Mnif Sellami, Y. and Gafsi, Y., 2019. Institutional and economic factors affecting the adoption

of international public sector accounting standards. International Journal of Public

Administration. 42(2). pp.119-131.

Shamsudin, A. and et.al, 2020. Utilising SATA in Measuring Students’ Understanding of

Financial Statements: A Survey among Non-Accounting Students. Jurnal Dinamika

Akuntansi. 12(1). pp.24-33.

AL-ANI, M.K. and TAWFIK, O. I., 2021. Effect of Intangible Assets on the Value Relevance of

Accounting Information: Evidence from Emerging Markets. The Journal of Asian

Finance, Economics, and Business, 8(2), pp.387-399.

Samanglangi, A., Lannai, D. and Rahim, S., 2020. Moderation of Corporate Good Governance

on Competence and Accounting Systems on Quality of Financial Statements. Point of

View Research Accounting and Auditing, 1(4), pp.150-160.

Accounting Information: Evidence from Emerging Markets. The Journal of Asian

Finance, Economics, and Business, 8(2), pp.387-399.

Samanglangi, A., Lannai, D. and Rahim, S., 2020. Moderation of Corporate Good Governance

on Competence and Accounting Systems on Quality of Financial Statements. Point of

View Research Accounting and Auditing, 1(4), pp.150-160.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.