Financial Accounting Report: Whirl Limited and AASB Standards

VerifiedAdded on 2023/01/17

|11

|1370

|89

Report

AI Summary

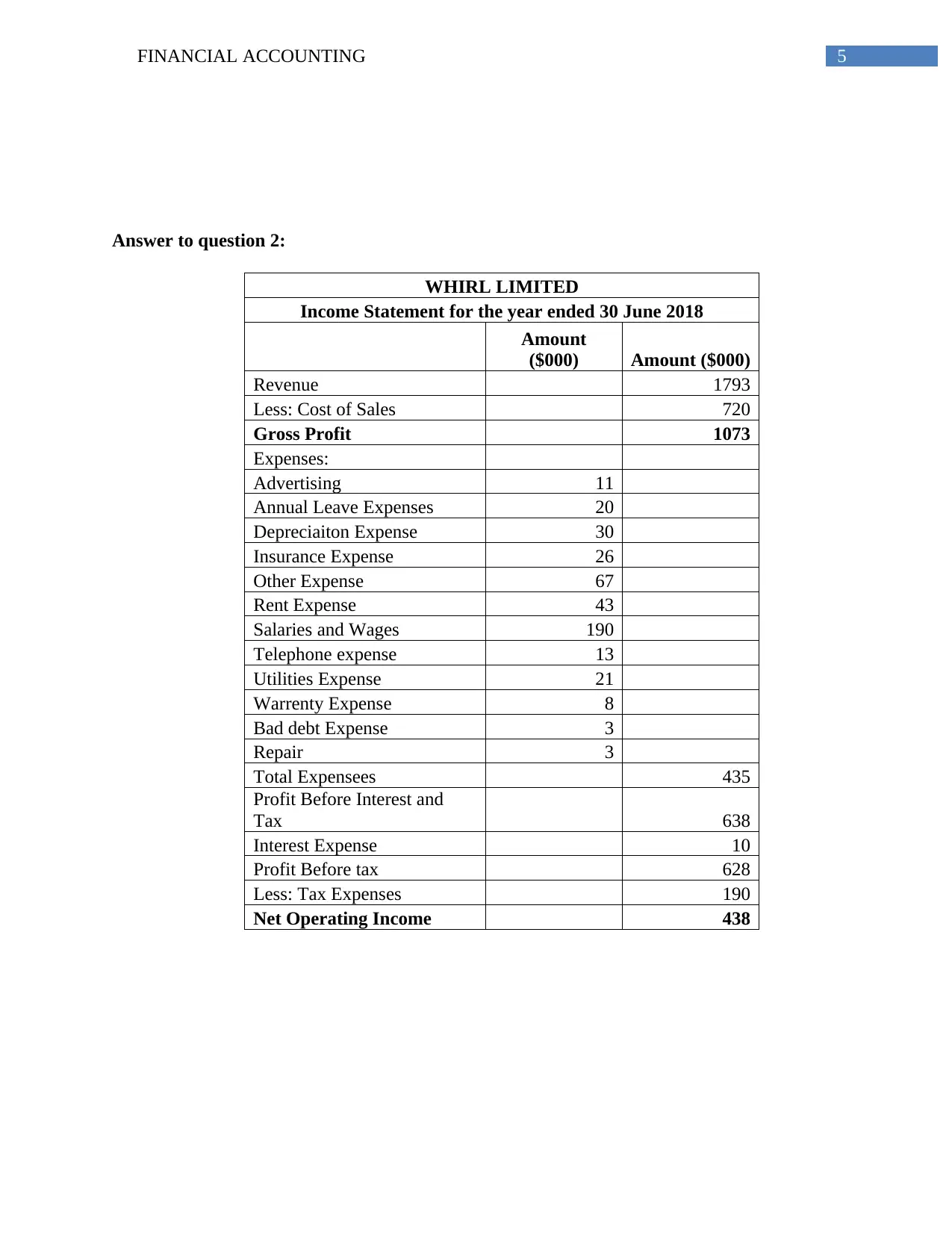

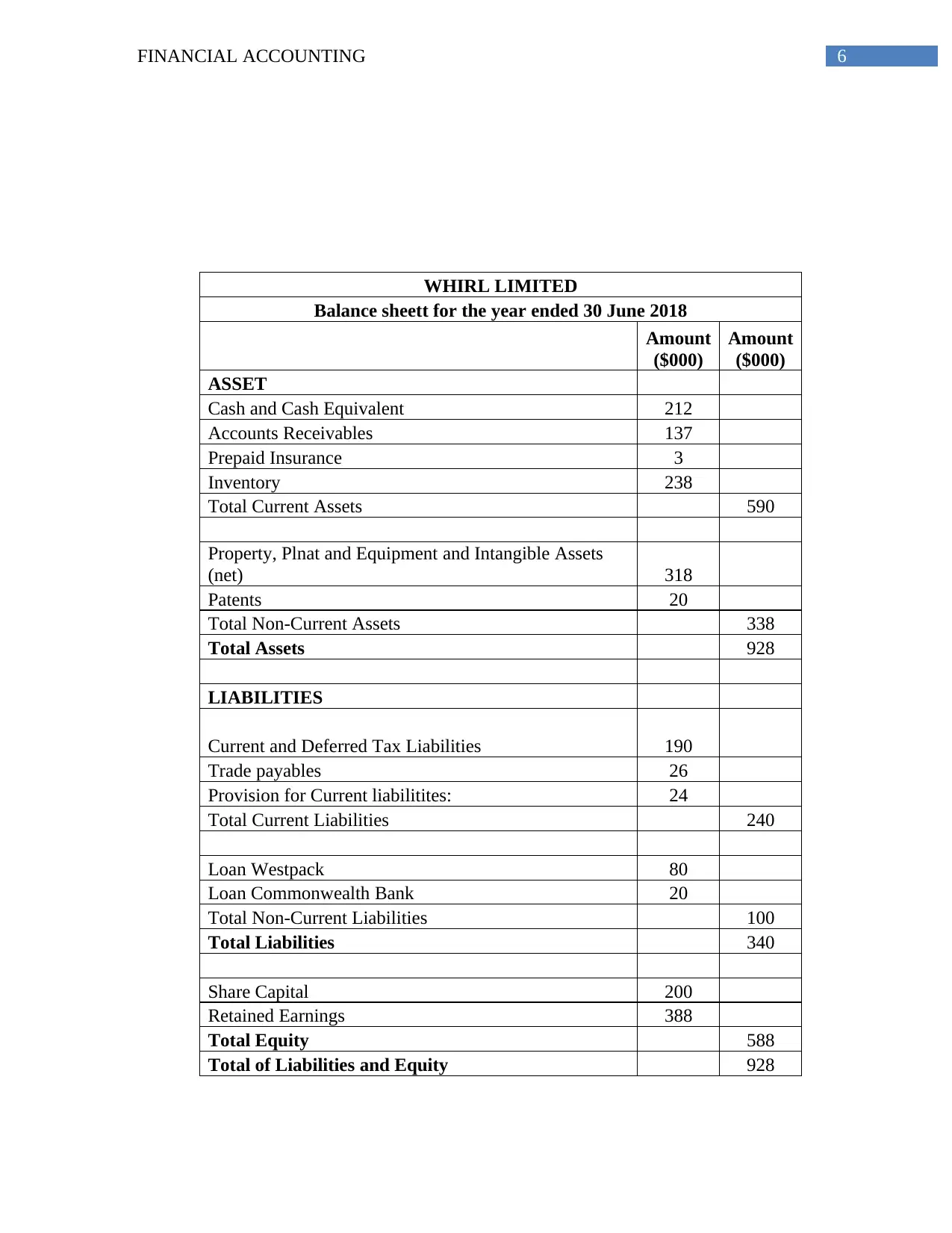

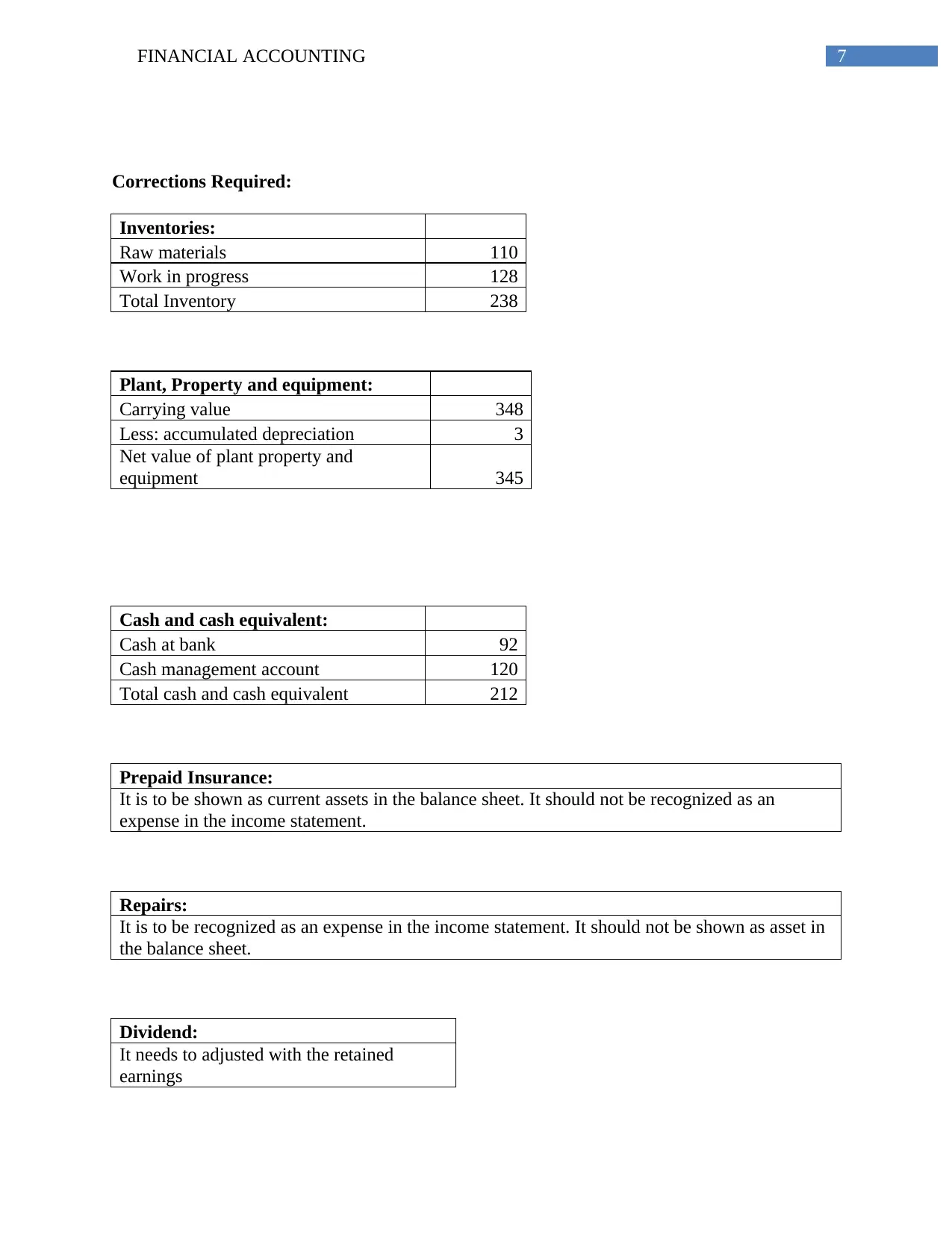

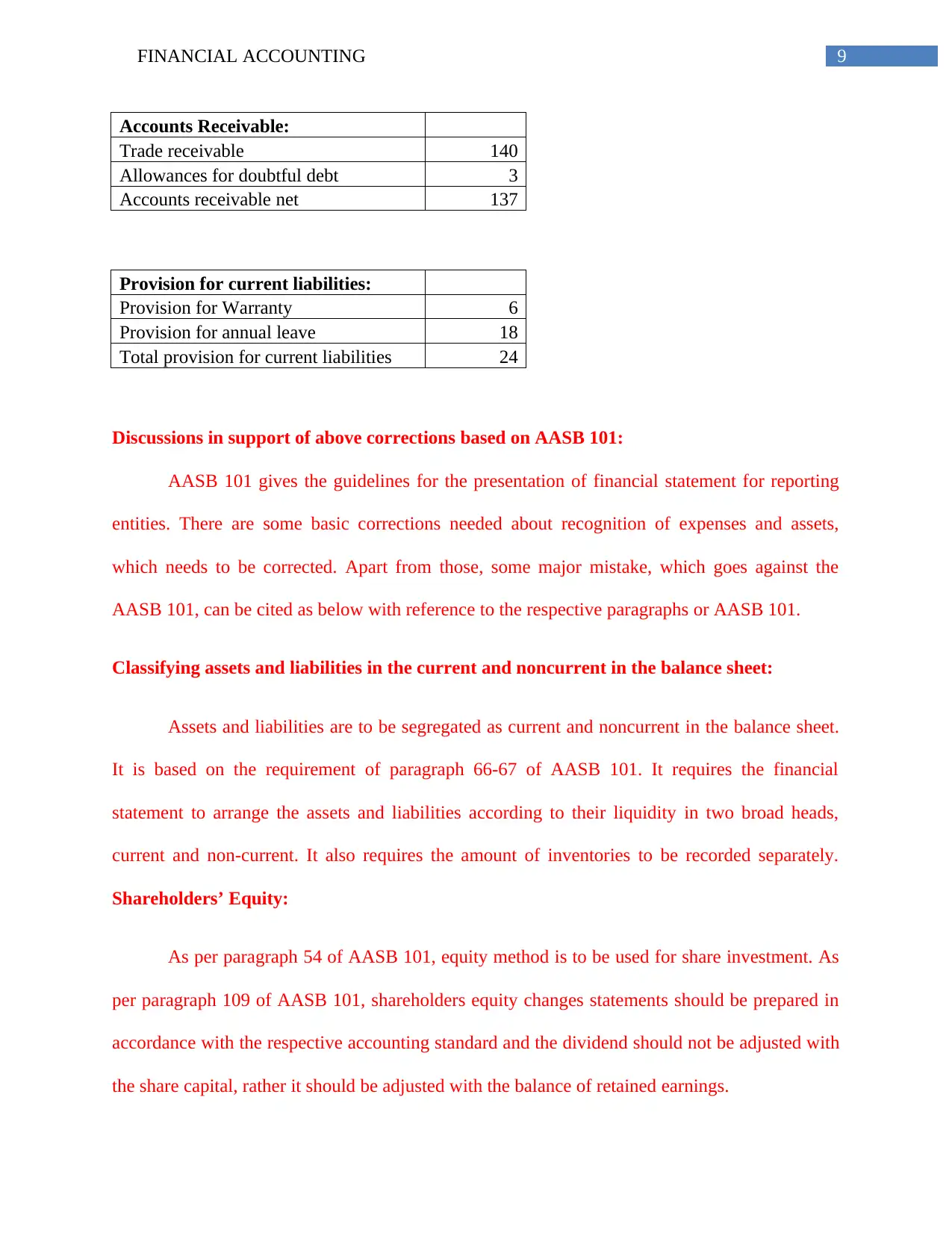

This financial accounting report addresses two key questions related to financial reporting. The first section analyzes the regulatory environment, specifically focusing on changes and developments in Australian Accounting Standards (AASB) from December 2018 to March 2019, including amendments, new standards, and exposure drafts. It details the impact of these changes on companies, particularly regarding climate change and the introduction of new standards for various sectors. The second section presents an income statement and balance sheet for Whirl Limited, followed by a detailed analysis of required corrections to align with AASB 101. The corrections cover areas such as inventory valuation, prepaid insurance, repairs, dividends, and the classification of assets and liabilities. The report supports these corrections with references to specific paragraphs within AASB 101, emphasizing the importance of accurate financial statement presentation and compliance with accounting standards. A bibliography of relevant resources is also included.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.