Financial Analysis, Budgeting, and Cash Flow Project for Companies

VerifiedAdded on 2021/01/02

|11

|2015

|380

Project

AI Summary

This project undertakes a comprehensive financial analysis and planning exercise, focusing on key financial concepts and their practical application. It begins by preparing production budgets and revising schedules to optimize resource allocation and reduce costs, specifically addressing overtime working. The project then delves into variance analysis, comparing flexed budgets with actual figures to identify and explain discrepancies, and discussing the underlying problems encountered during the budgeting process. A crucial element is the calculation and graphical representation of the break-even point, providing insights into sales targets necessary for profitability. Furthermore, the project culminates in the creation of a detailed six-month cash budget for Wilkinson Ltd, followed by an analysis of projected variances and a critical evaluation of the cash budget's implications. The analysis incorporates sales, costs, and other financial aspects, making it a useful case study for understanding financial planning and decision-making.

Financial Analysis and

Planning

Planning

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Prepare production budget and to revise schedule in order to reduce overtime working. 1

TASK 2............................................................................................................................................3

A) Analysing variances and giving summary on problems identified in preparation of budget 3

TASK 3............................................................................................................................................5

A) Calculation of break-even point .......................................................................................5

B) Constructing break-even chart from the data gathered......................................................5

TASK 4............................................................................................................................................6

A) Producing Cash Budget for six months of Wilkinson Ltd................................................6

B) Projected variances............................................................................................................6

C) Analyse results of cash budget..........................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Prepare production budget and to revise schedule in order to reduce overtime working. 1

TASK 2............................................................................................................................................3

A) Analysing variances and giving summary on problems identified in preparation of budget 3

TASK 3............................................................................................................................................5

A) Calculation of break-even point .......................................................................................5

B) Constructing break-even chart from the data gathered......................................................5

TASK 4............................................................................................................................................6

A) Producing Cash Budget for six months of Wilkinson Ltd................................................6

B) Projected variances............................................................................................................6

C) Analyse results of cash budget..........................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

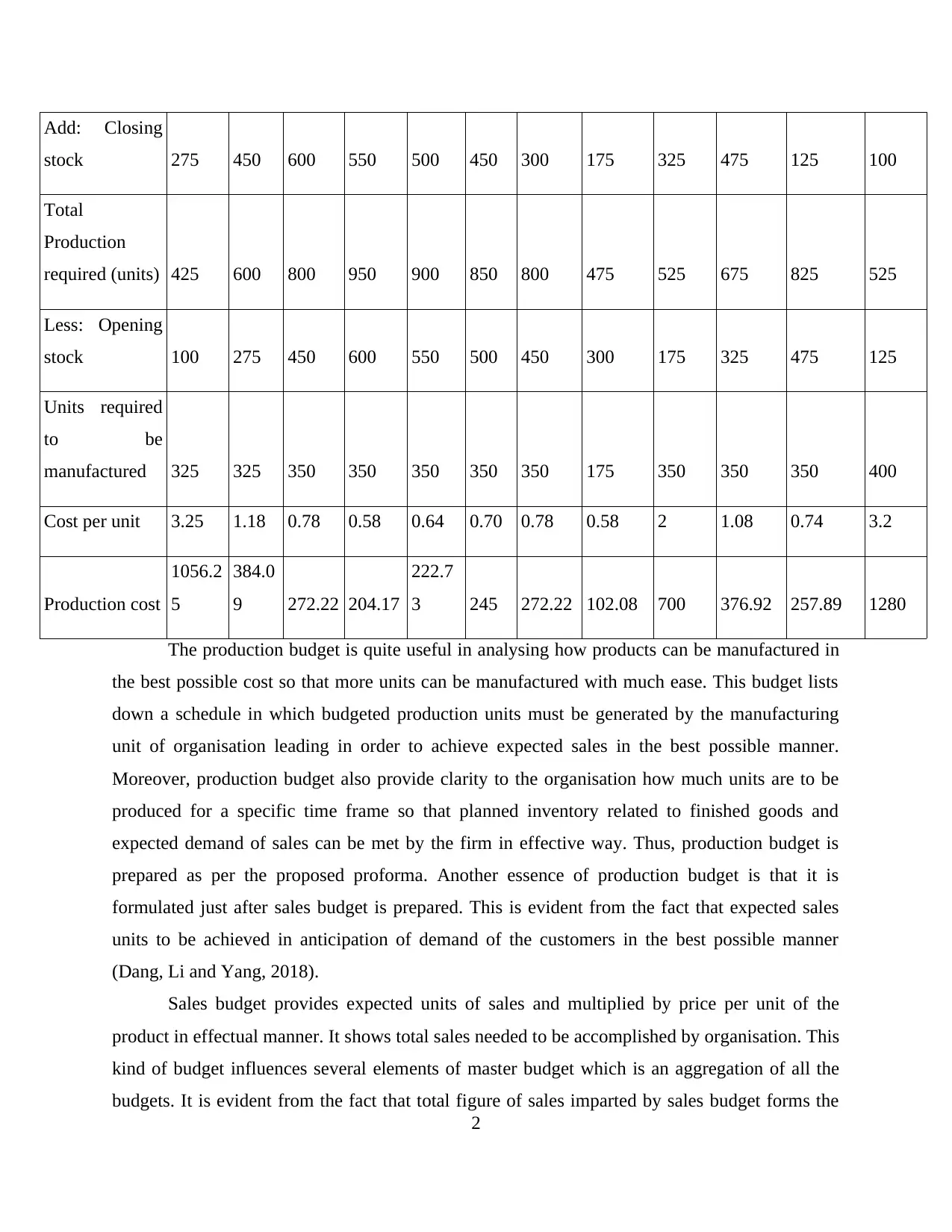

INTRODUCTION

Financial planning and analysis play a crucial role in the company as operational tasks

are to be achieved within stipulated time. Present report deals with various scenarios focusing on

core aspects of finance and importance of concepts in the business. Production and sales budget

both have been prepared which shows units to be manufactured to effectively meet expected

demand of customers in the best possible manner. Furthermore, flexed budget is formulated and

matched with actual figures to find out variances if any. Break-even analysis is conducted which

provides clarity to the organisation as to how many sales are to be achieved to attain profits.

Furthermore, problems associated while preparing budget are discussed. On the other hand, cash

budget is prepared on projected basis for the period of six months. Thus, financial planning and

analysis is much relevant to analyse performance and take decisions accordingly.

TASK 1

A) Preparing production budget and revising schedule in order to reduce overtime working

Sales Budget for Home Gym Ltd

Jan Feb Mar April May June Jul Aug Sep Oct Nov Dec

Sales units 150 150 200 400 400 400 500 300 200 200 700 425

Price per

unit 2.7 3 3.65 3.7 3.8 4 4.1 4.2 4.4 4.8 5 5.1

Total sales 405 450 730 1480 1520 1600 2050 1260 880 960 3500 2167.5

Production Budget for Home Gym Ltd

Production

budget Jan Feb Mar April May June Jul Aug Sep Oct Nov Dec

Forecasted

sales (units) 150 150 200 400 400 400 500 300 200 200 700 425

1

Financial planning and analysis play a crucial role in the company as operational tasks

are to be achieved within stipulated time. Present report deals with various scenarios focusing on

core aspects of finance and importance of concepts in the business. Production and sales budget

both have been prepared which shows units to be manufactured to effectively meet expected

demand of customers in the best possible manner. Furthermore, flexed budget is formulated and

matched with actual figures to find out variances if any. Break-even analysis is conducted which

provides clarity to the organisation as to how many sales are to be achieved to attain profits.

Furthermore, problems associated while preparing budget are discussed. On the other hand, cash

budget is prepared on projected basis for the period of six months. Thus, financial planning and

analysis is much relevant to analyse performance and take decisions accordingly.

TASK 1

A) Preparing production budget and revising schedule in order to reduce overtime working

Sales Budget for Home Gym Ltd

Jan Feb Mar April May June Jul Aug Sep Oct Nov Dec

Sales units 150 150 200 400 400 400 500 300 200 200 700 425

Price per

unit 2.7 3 3.65 3.7 3.8 4 4.1 4.2 4.4 4.8 5 5.1

Total sales 405 450 730 1480 1520 1600 2050 1260 880 960 3500 2167.5

Production Budget for Home Gym Ltd

Production

budget Jan Feb Mar April May June Jul Aug Sep Oct Nov Dec

Forecasted

sales (units) 150 150 200 400 400 400 500 300 200 200 700 425

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Add: Closing

stock 275 450 600 550 500 450 300 175 325 475 125 100

Total

Production

required (units) 425 600 800 950 900 850 800 475 525 675 825 525

Less: Opening

stock 100 275 450 600 550 500 450 300 175 325 475 125

Units required

to be

manufactured 325 325 350 350 350 350 350 175 350 350 350 400

Cost per unit 3.25 1.18 0.78 0.58 0.64 0.70 0.78 0.58 2 1.08 0.74 3.2

Production cost

1056.2

5

384.0

9 272.22 204.17

222.7

3 245 272.22 102.08 700 376.92 257.89 1280

The production budget is quite useful in analysing how products can be manufactured in

the best possible cost so that more units can be manufactured with much ease. This budget lists

down a schedule in which budgeted production units must be generated by the manufacturing

unit of organisation leading in order to achieve expected sales in the best possible manner.

Moreover, production budget also provide clarity to the organisation how much units are to be

produced for a specific time frame so that planned inventory related to finished goods and

expected demand of sales can be met by the firm in effective way. Thus, production budget is

prepared as per the proposed proforma. Another essence of production budget is that it is

formulated just after sales budget is prepared. This is evident from the fact that expected sales

units to be achieved in anticipation of demand of the customers in the best possible manner

(Dang, Li and Yang, 2018).

Sales budget provides expected units of sales and multiplied by price per unit of the

product in effectual manner. It shows total sales needed to be accomplished by organisation. This

kind of budget influences several elements of master budget which is an aggregation of all the

budgets. It is evident from the fact that total figure of sales imparted by sales budget forms the

2

stock 275 450 600 550 500 450 300 175 325 475 125 100

Total

Production

required (units) 425 600 800 950 900 850 800 475 525 675 825 525

Less: Opening

stock 100 275 450 600 550 500 450 300 175 325 475 125

Units required

to be

manufactured 325 325 350 350 350 350 350 175 350 350 350 400

Cost per unit 3.25 1.18 0.78 0.58 0.64 0.70 0.78 0.58 2 1.08 0.74 3.2

Production cost

1056.2

5

384.0

9 272.22 204.17

222.7

3 245 272.22 102.08 700 376.92 257.89 1280

The production budget is quite useful in analysing how products can be manufactured in

the best possible cost so that more units can be manufactured with much ease. This budget lists

down a schedule in which budgeted production units must be generated by the manufacturing

unit of organisation leading in order to achieve expected sales in the best possible manner.

Moreover, production budget also provide clarity to the organisation how much units are to be

produced for a specific time frame so that planned inventory related to finished goods and

expected demand of sales can be met by the firm in effective way. Thus, production budget is

prepared as per the proposed proforma. Another essence of production budget is that it is

formulated just after sales budget is prepared. This is evident from the fact that expected sales

units to be achieved in anticipation of demand of the customers in the best possible manner

(Dang, Li and Yang, 2018).

Sales budget provides expected units of sales and multiplied by price per unit of the

product in effectual manner. It shows total sales needed to be accomplished by organisation. This

kind of budget influences several elements of master budget which is an aggregation of all the

budgets. It is evident from the fact that total figure of sales imparted by sales budget forms the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

base of elements of budgets in the best possible way. This includes customer receipts, proforma

of income statement etc. Thus, estimation of sales required in units can be calculated in effectual

manner. On the other hand, after sales are analysed and estimated, production budget can be

made by estimated sales figures in units to be attained and production of stated units are achieved

in effectual way. This budget is prepared in anticipation so that demand can be met with much

ease. This is evident from the fact that without sales prediction, entity cannot manufacture

products and as a result, demand and needs of customers cannot be accomplished by

organisation. Thus, it is required to prepare both the budgets for assessing demand in effectual

manner.

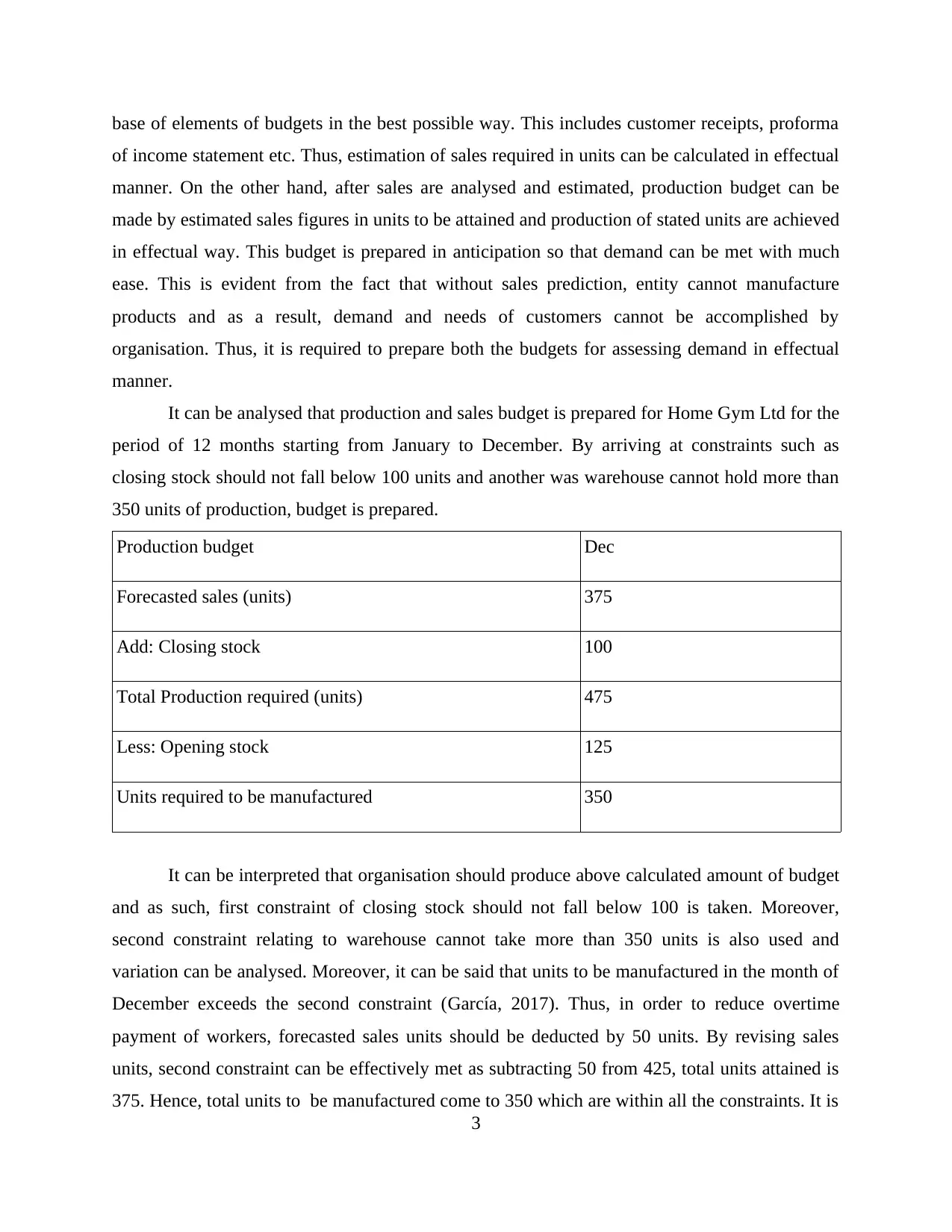

It can be analysed that production and sales budget is prepared for Home Gym Ltd for the

period of 12 months starting from January to December. By arriving at constraints such as

closing stock should not fall below 100 units and another was warehouse cannot hold more than

350 units of production, budget is prepared.

Production budget Dec

Forecasted sales (units) 375

Add: Closing stock 100

Total Production required (units) 475

Less: Opening stock 125

Units required to be manufactured 350

It can be interpreted that organisation should produce above calculated amount of budget

and as such, first constraint of closing stock should not fall below 100 is taken. Moreover,

second constraint relating to warehouse cannot take more than 350 units is also used and

variation can be analysed. Moreover, it can be said that units to be manufactured in the month of

December exceeds the second constraint (García, 2017). Thus, in order to reduce overtime

payment of workers, forecasted sales units should be deducted by 50 units. By revising sales

units, second constraint can be effectively met as subtracting 50 from 425, total units attained is

375. Hence, total units to be manufactured come to 350 which are within all the constraints. It is

3

of income statement etc. Thus, estimation of sales required in units can be calculated in effectual

manner. On the other hand, after sales are analysed and estimated, production budget can be

made by estimated sales figures in units to be attained and production of stated units are achieved

in effectual way. This budget is prepared in anticipation so that demand can be met with much

ease. This is evident from the fact that without sales prediction, entity cannot manufacture

products and as a result, demand and needs of customers cannot be accomplished by

organisation. Thus, it is required to prepare both the budgets for assessing demand in effectual

manner.

It can be analysed that production and sales budget is prepared for Home Gym Ltd for the

period of 12 months starting from January to December. By arriving at constraints such as

closing stock should not fall below 100 units and another was warehouse cannot hold more than

350 units of production, budget is prepared.

Production budget Dec

Forecasted sales (units) 375

Add: Closing stock 100

Total Production required (units) 475

Less: Opening stock 125

Units required to be manufactured 350

It can be interpreted that organisation should produce above calculated amount of budget

and as such, first constraint of closing stock should not fall below 100 is taken. Moreover,

second constraint relating to warehouse cannot take more than 350 units is also used and

variation can be analysed. Moreover, it can be said that units to be manufactured in the month of

December exceeds the second constraint (García, 2017). Thus, in order to reduce overtime

payment of workers, forecasted sales units should be deducted by 50 units. By revising sales

units, second constraint can be effectively met as subtracting 50 from 425, total units attained is

375. Hence, total units to be manufactured come to 350 which are within all the constraints. It is

3

suggested to Jim that in order to avoid overtime working, forecasted sales units should be revised

so that constraints can be met with much ease.

TASK 2

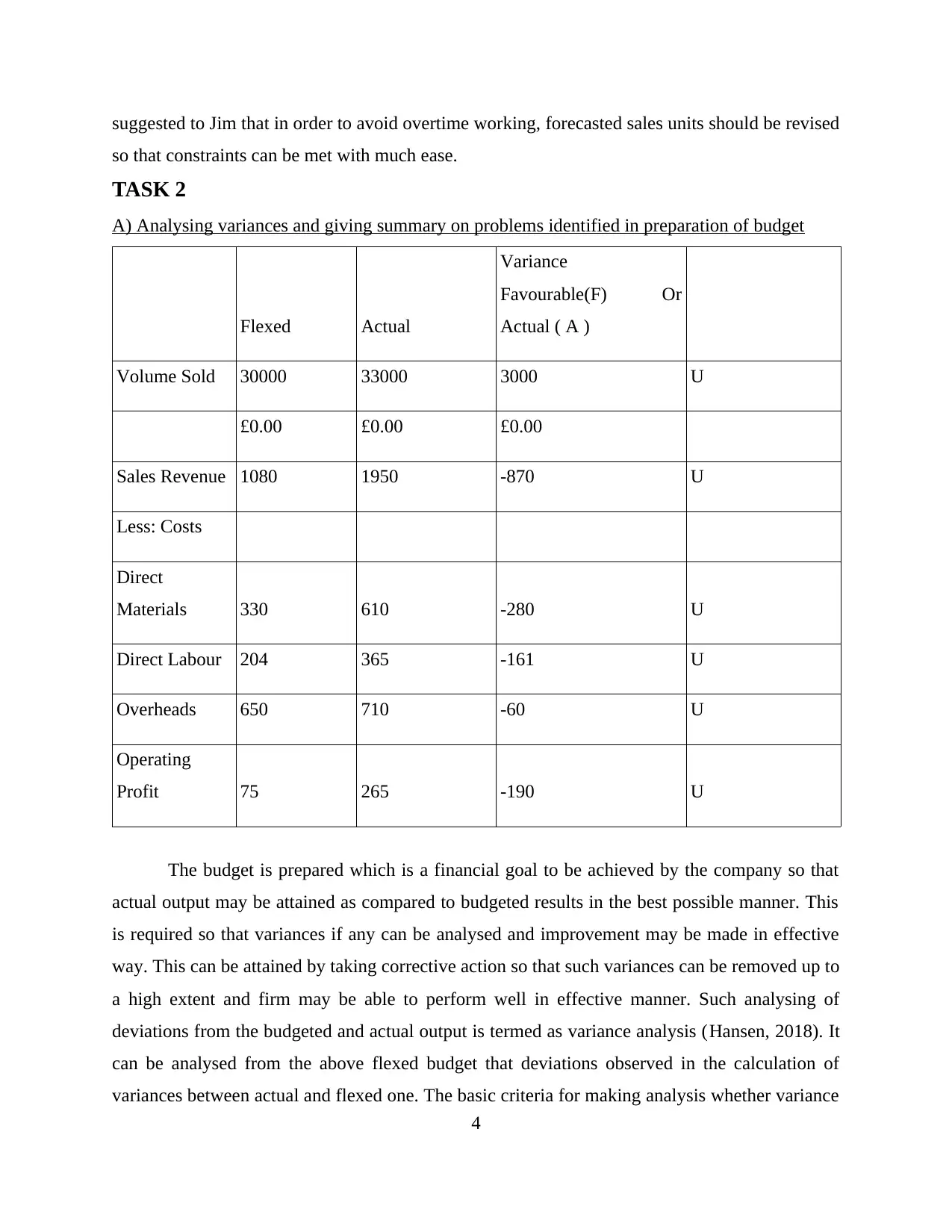

A) Analysing variances and giving summary on problems identified in preparation of budget

Flexed Actual

Variance

Favourable(F) Or

Actual ( A )

Volume Sold 30000 33000 3000 U

£0.00 £0.00 £0.00

Sales Revenue 1080 1950 -870 U

Less: Costs

Direct

Materials 330 610 -280 U

Direct Labour 204 365 -161 U

Overheads 650 710 -60 U

Operating

Profit 75 265 -190 U

The budget is prepared which is a financial goal to be achieved by the company so that

actual output may be attained as compared to budgeted results in the best possible manner. This

is required so that variances if any can be analysed and improvement may be made in effective

way. This can be attained by taking corrective action so that such variances can be removed up to

a high extent and firm may be able to perform well in effective manner. Such analysing of

deviations from the budgeted and actual output is termed as variance analysis (Hansen, 2018). It

can be analysed from the above flexed budget that deviations observed in the calculation of

variances between actual and flexed one. The basic criteria for making analysis whether variance

4

so that constraints can be met with much ease.

TASK 2

A) Analysing variances and giving summary on problems identified in preparation of budget

Flexed Actual

Variance

Favourable(F) Or

Actual ( A )

Volume Sold 30000 33000 3000 U

£0.00 £0.00 £0.00

Sales Revenue 1080 1950 -870 U

Less: Costs

Direct

Materials 330 610 -280 U

Direct Labour 204 365 -161 U

Overheads 650 710 -60 U

Operating

Profit 75 265 -190 U

The budget is prepared which is a financial goal to be achieved by the company so that

actual output may be attained as compared to budgeted results in the best possible manner. This

is required so that variances if any can be analysed and improvement may be made in effective

way. This can be attained by taking corrective action so that such variances can be removed up to

a high extent and firm may be able to perform well in effective manner. Such analysing of

deviations from the budgeted and actual output is termed as variance analysis (Hansen, 2018). It

can be analysed from the above flexed budget that deviations observed in the calculation of

variances between actual and flexed one. The basic criteria for making analysis whether variance

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

exists or not is regarding all the costs, if there is excess of amount of flexed budget than actual

one, favourable variance is achieved. On the other hand, if there is excess of actual figures than

flexed budget, then there is unfavourable variance. Thus, it can be analysed that flexed budget

figures are less than actual figures and as such, there are unfavourable variances in the budget

formulated.

The problems occurred while preparing budgets are inaccuracy, requirement of time, no

flexible decision making etc. In relation to this, inaccuracy is a foremost problem occurred as

budget is formulated on an mere estimation with regards to future which leads to improper

assumptions. Moreover, if market conditions changed and fixed budget is prepared without

taking into consideration because of its rigidity, results are not worthwhile. On the other hand,

next problem associated with budget preparation is that lot of time is consumed and it is not good

for small company where fewer tasks are required to be attained and as such, budget is time-

consuming one. The decision is made by the top management without taking advices or

participating employees to share suggestions and as such, proper allocation of funds are not

made. This increases problem as proper allocation of resources cannot be made and as such,

company faces difficulty while preparing budget (Lombardi and Ravazzolo, 2016). Furthermore,

if more of the resources is allocated to departments without scrutinising their needs, budget

inflation may take place which is another issue while preparing the budget of company.

TASK 3

A) Calculation of break-even point

Selling price (P) = 20

Variable costs (V) = 10

Fixed costs (FC) = 5000

By applying the formula of BEP in sales (units)

= FC / P – V

= 5000 / 20 – 10

= 5000 / 10

= 500

5

one, favourable variance is achieved. On the other hand, if there is excess of actual figures than

flexed budget, then there is unfavourable variance. Thus, it can be analysed that flexed budget

figures are less than actual figures and as such, there are unfavourable variances in the budget

formulated.

The problems occurred while preparing budgets are inaccuracy, requirement of time, no

flexible decision making etc. In relation to this, inaccuracy is a foremost problem occurred as

budget is formulated on an mere estimation with regards to future which leads to improper

assumptions. Moreover, if market conditions changed and fixed budget is prepared without

taking into consideration because of its rigidity, results are not worthwhile. On the other hand,

next problem associated with budget preparation is that lot of time is consumed and it is not good

for small company where fewer tasks are required to be attained and as such, budget is time-

consuming one. The decision is made by the top management without taking advices or

participating employees to share suggestions and as such, proper allocation of funds are not

made. This increases problem as proper allocation of resources cannot be made and as such,

company faces difficulty while preparing budget (Lombardi and Ravazzolo, 2016). Furthermore,

if more of the resources is allocated to departments without scrutinising their needs, budget

inflation may take place which is another issue while preparing the budget of company.

TASK 3

A) Calculation of break-even point

Selling price (P) = 20

Variable costs (V) = 10

Fixed costs (FC) = 5000

By applying the formula of BEP in sales (units)

= FC / P – V

= 5000 / 20 – 10

= 5000 / 10

= 500

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Now, BEP in sales can be calculated by = Price per units * BEP in sales (units)

= 20 * 500

= 10,000

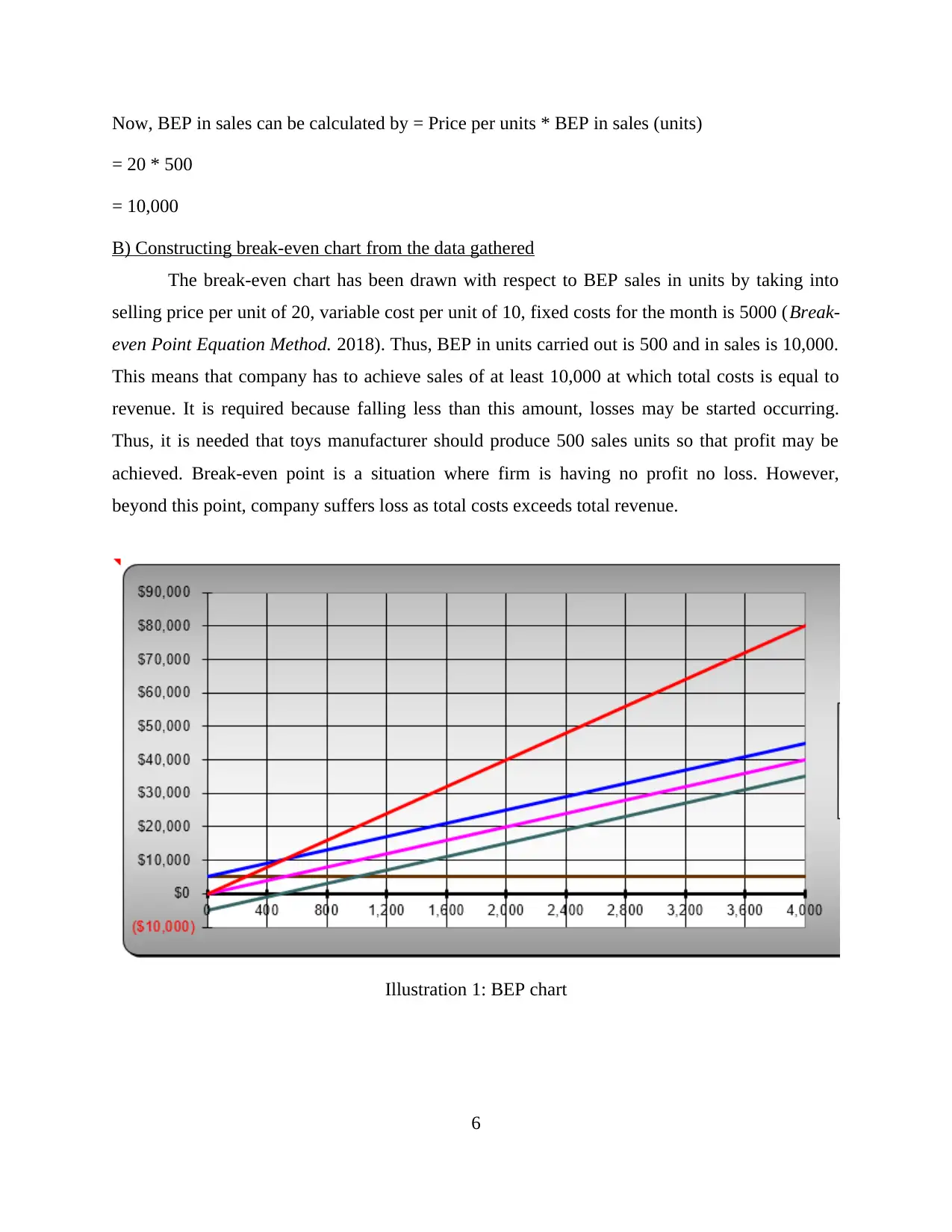

B) Constructing break-even chart from the data gathered

The break-even chart has been drawn with respect to BEP sales in units by taking into

selling price per unit of 20, variable cost per unit of 10, fixed costs for the month is 5000 (Break-

even Point Equation Method. 2018). Thus, BEP in units carried out is 500 and in sales is 10,000.

This means that company has to achieve sales of at least 10,000 at which total costs is equal to

revenue. It is required because falling less than this amount, losses may be started occurring.

Thus, it is needed that toys manufacturer should produce 500 sales units so that profit may be

achieved. Break-even point is a situation where firm is having no profit no loss. However,

beyond this point, company suffers loss as total costs exceeds total revenue.

6

Illustration 1: BEP chart

= 20 * 500

= 10,000

B) Constructing break-even chart from the data gathered

The break-even chart has been drawn with respect to BEP sales in units by taking into

selling price per unit of 20, variable cost per unit of 10, fixed costs for the month is 5000 (Break-

even Point Equation Method. 2018). Thus, BEP in units carried out is 500 and in sales is 10,000.

This means that company has to achieve sales of at least 10,000 at which total costs is equal to

revenue. It is required because falling less than this amount, losses may be started occurring.

Thus, it is needed that toys manufacturer should produce 500 sales units so that profit may be

achieved. Break-even point is a situation where firm is having no profit no loss. However,

beyond this point, company suffers loss as total costs exceeds total revenue.

6

Illustration 1: BEP chart

TASK 4

A) Producing Cash Budget for six months of Wilkinson Ltd

B) Projected variances

C) Analyse results of cash budget

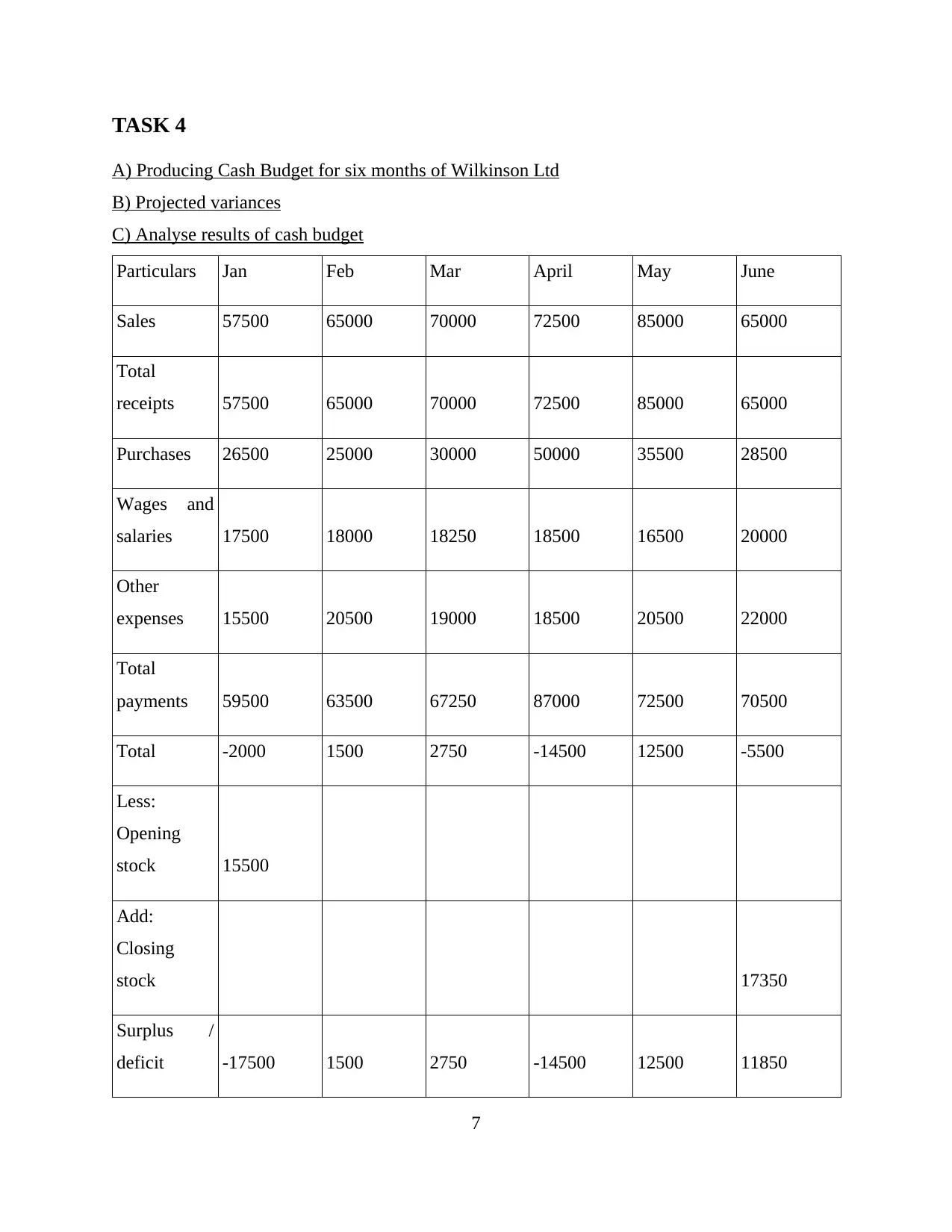

Particulars Jan Feb Mar April May June

Sales 57500 65000 70000 72500 85000 65000

Total

receipts 57500 65000 70000 72500 85000 65000

Purchases 26500 25000 30000 50000 35500 28500

Wages and

salaries 17500 18000 18250 18500 16500 20000

Other

expenses 15500 20500 19000 18500 20500 22000

Total

payments 59500 63500 67250 87000 72500 70500

Total -2000 1500 2750 -14500 12500 -5500

Less:

Opening

stock 15500

Add:

Closing

stock 17350

Surplus /

deficit -17500 1500 2750 -14500 12500 11850

7

A) Producing Cash Budget for six months of Wilkinson Ltd

B) Projected variances

C) Analyse results of cash budget

Particulars Jan Feb Mar April May June

Sales 57500 65000 70000 72500 85000 65000

Total

receipts 57500 65000 70000 72500 85000 65000

Purchases 26500 25000 30000 50000 35500 28500

Wages and

salaries 17500 18000 18250 18500 16500 20000

Other

expenses 15500 20500 19000 18500 20500 22000

Total

payments 59500 63500 67250 87000 72500 70500

Total -2000 1500 2750 -14500 12500 -5500

Less:

Opening

stock 15500

Add:

Closing

stock 17350

Surplus /

deficit -17500 1500 2750 -14500 12500 11850

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Opening

cash balance 2250 -19750 21250 -18500 4000 8500

Closing cash

balance

-19750 21250 -18500 4000 8500 3350

It can be analysed that projected cash budget is prepared which provides clarity about

cash position of the firm by deducting expenses from the receipts. The projected budget sets out

that opening balance of cash in the month of January was 2250 which is been taken into account.

On the other hand, opening stock of January and closing stock is taken and assessed in the cash

budget (Montford and Goldsmith, 2016.). The variances of cash can be analysed in all the

months such as closing cash balance in starting month is -19750, in next month is 21250, while

in month of March is -18500, in April is 4000. On the other hand, closing cash balance in May is

8500 and in June is 3350. Thus, it can be analysed that there are variances in balances. Thus, six

months of cash budget is prepared for the firm in effective manner.

CONCLUSION

Hereby it can be concluded that financial planning and analysis is quite effective to

company as performance may be easily assessed and adequate decision can be taken for the

future with much ease. Furthermore, budgeting help to analyse company how actual output can

be attained as listed in the budgeted one. Variances or deviations if any can be removed up to a

high extent by taking corrective actions in the best possible manner. Moreover, company may be

able to achieve budgeted goal as anticipated and as such, actual results may be accomplished.

Break-even point analysis is another useful for the company so that at least company can easily

analyse how it has to accomplish break-even sales so that profits can be garnered.

8

cash balance 2250 -19750 21250 -18500 4000 8500

Closing cash

balance

-19750 21250 -18500 4000 8500 3350

It can be analysed that projected cash budget is prepared which provides clarity about

cash position of the firm by deducting expenses from the receipts. The projected budget sets out

that opening balance of cash in the month of January was 2250 which is been taken into account.

On the other hand, opening stock of January and closing stock is taken and assessed in the cash

budget (Montford and Goldsmith, 2016.). The variances of cash can be analysed in all the

months such as closing cash balance in starting month is -19750, in next month is 21250, while

in month of March is -18500, in April is 4000. On the other hand, closing cash balance in May is

8500 and in June is 3350. Thus, it can be analysed that there are variances in balances. Thus, six

months of cash budget is prepared for the firm in effective manner.

CONCLUSION

Hereby it can be concluded that financial planning and analysis is quite effective to

company as performance may be easily assessed and adequate decision can be taken for the

future with much ease. Furthermore, budgeting help to analyse company how actual output can

be attained as listed in the budgeted one. Variances or deviations if any can be removed up to a

high extent by taking corrective actions in the best possible manner. Moreover, company may be

able to achieve budgeted goal as anticipated and as such, actual results may be accomplished.

Break-even point analysis is another useful for the company so that at least company can easily

analyse how it has to accomplish break-even sales so that profits can be garnered.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Dang, C., Li, Z. F. and Yang, C., 2018. Measuring firm size in empirical corporate

finance. Journal of Banking & Finance. 86. pp.159-176.

García, F. J. P., 2017. The WACC. In Financial Risk Management (pp. 345-351). Palgrave

Macmillan, Cham.

Hansen, C. B., 2018. Peter Birch Sørensen University of Copenhagen:" Taxation and the optimal

constraint on corporate debt finance: Why a comprehensive business income tax is

suboptimal". Virtual Reality.

Lombardi, M. J. and Ravazzolo, F., 2016. On the correlation between commodity and equity

returns: implications for portfolio allocation. Journal of Commodity Markets. 2(1). pp.45-

57.

9

Books and Journals

Dang, C., Li, Z. F. and Yang, C., 2018. Measuring firm size in empirical corporate

finance. Journal of Banking & Finance. 86. pp.159-176.

García, F. J. P., 2017. The WACC. In Financial Risk Management (pp. 345-351). Palgrave

Macmillan, Cham.

Hansen, C. B., 2018. Peter Birch Sørensen University of Copenhagen:" Taxation and the optimal

constraint on corporate debt finance: Why a comprehensive business income tax is

suboptimal". Virtual Reality.

Lombardi, M. J. and Ravazzolo, F., 2016. On the correlation between commodity and equity

returns: implications for portfolio allocation. Journal of Commodity Markets. 2(1). pp.45-

57.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.