Financial Analysis and Valuation Models for Barclays Plc. Report

VerifiedAdded on 2023/04/21

|19

|3796

|484

Report

AI Summary

This report presents a financial analysis of Barclays Plc., evaluating its performance through various valuation models to aid in investment decisions. The report begins with an executive summary and table of contents, followed by an introduction to Barclays, a multinational banking company. It delves into three stock evaluation methods: the Dividend Discount Model (DDM), Discounted Cash Flow (DCF), and Price to Earnings ratio (P/E). The report then applies these models to value Barclays shares, providing interpretations of each method's results. Furthermore, it includes a past performance analysis, examining share price, market capitalization, financial ratios, and comparative financial statements. The conclusion summarizes the findings, offering insights into investment strategies based on the financial analysis and valuation models employed.

Running head: FINANCIAL ANALYSIS AND VALUATION MODELS

Financial Analysis and Valuation Models

Name of the student:

Name of the university:

Author’s Note:

Financial Analysis and Valuation Models

Name of the student:

Name of the university:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Executive Summary:

This report is prepared to show the effect of different valuation models on the investment

decision of the investor. In this report, financial performance of the Barclays Plc. has been

analyzed in such a way that investment decision can be made considered for different factors

affecting investment. This report covers the ratio analysis for four previous financial year of

the Barclays Plc., from the information obtained from the financial statement of the company.

This report also indicates the choice of the strategy an investor can made from Buy, Hold and

Sell strategy based on three valuation models and financial performance of the company.

Executive Summary:

This report is prepared to show the effect of different valuation models on the investment

decision of the investor. In this report, financial performance of the Barclays Plc. has been

analyzed in such a way that investment decision can be made considered for different factors

affecting investment. This report covers the ratio analysis for four previous financial year of

the Barclays Plc., from the information obtained from the financial statement of the company.

This report also indicates the choice of the strategy an investor can made from Buy, Hold and

Sell strategy based on three valuation models and financial performance of the company.

2

Table of Contents

1. Introduction:...........................................................................................................................3

2. Stock Evaluation Method:......................................................................................................3

2.1 Dividend Discount Model:...............................................................................................3

2.2 Discounted Cash Flow:....................................................................................................4

2.3 Price to Earnings ratio:.....................................................................................................5

3. Valuation of Share Using Different Models of Valuation:....................................................7

3.1 Valuation Based on Dividend Discount Method (DDM):...............................................7

3.2 Valuation Based on Cash Flow Method:.........................................................................8

3.3 Valuation Based on P/E Ratio:.........................................................................................9

4. Past performance Analysis:....................................................................................................9

4.1 Using Price And Market Capitalization of The Company:..............................................9

4.2 Using Financial Ratios:..................................................................................................12

4.3 Using Comparative Statement of Balance sheet and Income Statement:......................14

5. Conclusion:..........................................................................................................................15

6. References:...........................................................................................................................17

Table of Contents

1. Introduction:...........................................................................................................................3

2. Stock Evaluation Method:......................................................................................................3

2.1 Dividend Discount Model:...............................................................................................3

2.2 Discounted Cash Flow:....................................................................................................4

2.3 Price to Earnings ratio:.....................................................................................................5

3. Valuation of Share Using Different Models of Valuation:....................................................7

3.1 Valuation Based on Dividend Discount Method (DDM):...............................................7

3.2 Valuation Based on Cash Flow Method:.........................................................................8

3.3 Valuation Based on P/E Ratio:.........................................................................................9

4. Past performance Analysis:....................................................................................................9

4.1 Using Price And Market Capitalization of The Company:..............................................9

4.2 Using Financial Ratios:..................................................................................................12

4.3 Using Comparative Statement of Balance sheet and Income Statement:......................14

5. Conclusion:..........................................................................................................................15

6. References:...........................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

1. Introduction:

Barclays is a multinational banking company engaged in investing as well as financial

services in London. It provides various financial services in different European countries. it

provides personal as well as business banking services in which facilities like credit and debit

cards, investment planning, locker services, wealth management are offered to the different

types of clients based on their net worth. It was established by john freame as Goldsmith

Bankers but in the end of 1736, it become Barclays bank when the son-in-law of James

Freame has taken over the business of Goldsmith. Through acquisitions and mergers with

different banking companies like the Colonial Bank, National Bank of South Africa and the

Anglo-Egyptian Bank and Non-Banking companies like Mercantile Credit Company,

American Credit Corporation etc , it expended its business to different regions of the world.

2. Stock Evaluation Method:

2.1 Dividend Discount Model:

Dividend Discount Model is a process of valuation of stock price of accompany where the

dividend payment is discounted to the present value of stock price. The stocks are valued on

the basis of net present value for the dividends of the future. Gordon’s growth model is a

renowned growth used in this model. If the DDM of a particular stock is higher then it can be

said that the current value of the stock is undervalued and in case DDM of a particular stock

is lower then it can be said that the value of the stock is overvalued currently (Mohammadian

and Rezaee 2018).

The valuation of the stock can be done in following way:

P = D/ (r – g)

1. Introduction:

Barclays is a multinational banking company engaged in investing as well as financial

services in London. It provides various financial services in different European countries. it

provides personal as well as business banking services in which facilities like credit and debit

cards, investment planning, locker services, wealth management are offered to the different

types of clients based on their net worth. It was established by john freame as Goldsmith

Bankers but in the end of 1736, it become Barclays bank when the son-in-law of James

Freame has taken over the business of Goldsmith. Through acquisitions and mergers with

different banking companies like the Colonial Bank, National Bank of South Africa and the

Anglo-Egyptian Bank and Non-Banking companies like Mercantile Credit Company,

American Credit Corporation etc , it expended its business to different regions of the world.

2. Stock Evaluation Method:

2.1 Dividend Discount Model:

Dividend Discount Model is a process of valuation of stock price of accompany where the

dividend payment is discounted to the present value of stock price. The stocks are valued on

the basis of net present value for the dividends of the future. Gordon’s growth model is a

renowned growth used in this model. If the DDM of a particular stock is higher then it can be

said that the current value of the stock is undervalued and in case DDM of a particular stock

is lower then it can be said that the value of the stock is overvalued currently (Mohammadian

and Rezaee 2018).

The valuation of the stock can be done in following way:

P = D/ (r – g)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Where,

P = Price per share, D = estimated value of dividend of next year, g = constant growth rate of

dividend, r = company’s cost of capital equity

The Gordon’s growth model has an assumption, which is that the dividend has a stable

growth rate. The growth rate of this model is stable as the dividend year after year is also

remains stable in that case. It is a process of finding the value of stock with the process of

discounting all the expected future dividends.

The flaws of the dividend discount model are that, with the constant increase in the rate of

dividend. In that case, if the dividend increases then it does not increase at a constant rate. In

order to buy a stock an investor must not only consider that particular stock even if it is cheap

or expensive based on DDM. The particular investor must also consider the following

parameters in case of buying a particular stock, which are return on equity, revenue and

earnings growth, price earnings ratio and the company’s dividend payout ratio, are certain

parameters needed to be considered while purchasing a stock.

2.2 Discounted Cash Flow:

Discounted Cash Flow (DCF) is a method of evaluating the value of investment, which is

based on cash flow related to the future. The expected cash flow of the future converted into

the present value of cash flow by using discount rate. The calculated value of the DCF if it is

higher than the cost of current investment, then such opportunity cost must be considered.

The formula is that DCF = CF1/ (1 + r)1 + CF2/ (1 + r)2 + … CFn/ (1 + r)n

Where,

CF = Cash Flow, r = discount rate

Where,

P = Price per share, D = estimated value of dividend of next year, g = constant growth rate of

dividend, r = company’s cost of capital equity

The Gordon’s growth model has an assumption, which is that the dividend has a stable

growth rate. The growth rate of this model is stable as the dividend year after year is also

remains stable in that case. It is a process of finding the value of stock with the process of

discounting all the expected future dividends.

The flaws of the dividend discount model are that, with the constant increase in the rate of

dividend. In that case, if the dividend increases then it does not increase at a constant rate. In

order to buy a stock an investor must not only consider that particular stock even if it is cheap

or expensive based on DDM. The particular investor must also consider the following

parameters in case of buying a particular stock, which are return on equity, revenue and

earnings growth, price earnings ratio and the company’s dividend payout ratio, are certain

parameters needed to be considered while purchasing a stock.

2.2 Discounted Cash Flow:

Discounted Cash Flow (DCF) is a method of evaluating the value of investment, which is

based on cash flow related to the future. The expected cash flow of the future converted into

the present value of cash flow by using discount rate. The calculated value of the DCF if it is

higher than the cost of current investment, then such opportunity cost must be considered.

The formula is that DCF = CF1/ (1 + r)1 + CF2/ (1 + r)2 + … CFn/ (1 + r)n

Where,

CF = Cash Flow, r = discount rate

5

The main purpose of this model is that the discounting of cash flow is done in such a

situation when the investment is high or rather complicated when the investors is not able to

access the cash flow of the future. DCF analysis is based on the discount rate and there are

various ways to correct the rate of discount, which is depended on the purpose of the

investment. During the time of investment, an investor also could set the DCF rate of

discount, which is equal to the expected return from an alternative investment of the same

kind of risk. This kind of analysis is used in the following cases, which are investment

finance, financial management and valuation of patent. DCF analysis is used in order to

evaluate the Net Present Value, which is considered as input cash flows, and a discount rate,

which further gives output as a present value. The discount rate considered in this method is

the weighted average cost of capital (WACC) which shows the risk in the flow of cash. The

discount rate shows the two things, which are the time value of money and risk premium.

The assumptions that can be made in this case is that the cash flow occurs at the end of the

year. DCF is mostly associated with the big investment projects where there is uncertainty in

the business and the adjustments are made accordingly. All cash flows are invested in various

projects in order to generate return of the company.

2.3 Price to Earnings ratio:

Price to Earnings ratio is a ratio, which is used for the purpose of valuation of a company,

which further measures the current price of the share related to its EPS (Earning Per Share). It

is also termed as the earnings multiples because the current price of share of the company is

related to EPS of the company.

The formula of the P/E Ratio = Market Value per Share / Earning per Share

The P/E ratio is a tool, which is used for determining the value of the stock by the investor for

the purpose of investing. The P/E ratio of a company shows that the market is based on future

The main purpose of this model is that the discounting of cash flow is done in such a

situation when the investment is high or rather complicated when the investors is not able to

access the cash flow of the future. DCF analysis is based on the discount rate and there are

various ways to correct the rate of discount, which is depended on the purpose of the

investment. During the time of investment, an investor also could set the DCF rate of

discount, which is equal to the expected return from an alternative investment of the same

kind of risk. This kind of analysis is used in the following cases, which are investment

finance, financial management and valuation of patent. DCF analysis is used in order to

evaluate the Net Present Value, which is considered as input cash flows, and a discount rate,

which further gives output as a present value. The discount rate considered in this method is

the weighted average cost of capital (WACC) which shows the risk in the flow of cash. The

discount rate shows the two things, which are the time value of money and risk premium.

The assumptions that can be made in this case is that the cash flow occurs at the end of the

year. DCF is mostly associated with the big investment projects where there is uncertainty in

the business and the adjustments are made accordingly. All cash flows are invested in various

projects in order to generate return of the company.

2.3 Price to Earnings ratio:

Price to Earnings ratio is a ratio, which is used for the purpose of valuation of a company,

which further measures the current price of the share related to its EPS (Earning Per Share). It

is also termed as the earnings multiples because the current price of share of the company is

related to EPS of the company.

The formula of the P/E Ratio = Market Value per Share / Earning per Share

The P/E ratio is a tool, which is used for determining the value of the stock by the investor for

the purpose of investing. The P/E ratio of a company shows that the market is based on future

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

earnings the market pays according to that. According to the P/E, if the P/E of the company is

high then the investors will go for that company and if the P/E of the company is low then the

investors does not prefer those companies. The P/E ratio consists of two types, which are the

Absolute P/E and Relative P/E. Thus, P/E is an important tool considered by the investors in

terms of taking the investment decisions of the company. High P/E of the company will

automatically drag the potential investors in the market. This will help the company to

increase the efficiency of the business smoothly and efficiently. If the return of a company

increases then the stock price of that company decreases. If the risk of investment is higher

then the price of the stock becomes low in that case.

The flaws of the P/E ratio is that in case of taking the investment decision, the investor may

take into their mind that if there is one single metric then it will provide the complete view

into the investment decision taken by the investor which may not be the case most of the

time. When the P/E ratio is compared with different companies then it becomes one of the

flaws in P/E ratio. The valuations along with the rate of growth of the companies between the

various sectors of the companies earn money in various timelines. In case of the same sectors

the P/E is used as an analysis tool and comparisons in this case will give productive return for

the investors. If the growth of the expected dividend increases then the P/E of the particular

company also increases in that case.

If the P/E ratio of different companies within the same sector is high then it will be of less

cause when the entire other sectors has high P/E ratios. In case of debt of the company, the

company having higher debt will have low P/E ratio then the company having low debt. The

business having high debt will considerably have high P/E ratio as that particular company

has taken leverage in that case.

earnings the market pays according to that. According to the P/E, if the P/E of the company is

high then the investors will go for that company and if the P/E of the company is low then the

investors does not prefer those companies. The P/E ratio consists of two types, which are the

Absolute P/E and Relative P/E. Thus, P/E is an important tool considered by the investors in

terms of taking the investment decisions of the company. High P/E of the company will

automatically drag the potential investors in the market. This will help the company to

increase the efficiency of the business smoothly and efficiently. If the return of a company

increases then the stock price of that company decreases. If the risk of investment is higher

then the price of the stock becomes low in that case.

The flaws of the P/E ratio is that in case of taking the investment decision, the investor may

take into their mind that if there is one single metric then it will provide the complete view

into the investment decision taken by the investor which may not be the case most of the

time. When the P/E ratio is compared with different companies then it becomes one of the

flaws in P/E ratio. The valuations along with the rate of growth of the companies between the

various sectors of the companies earn money in various timelines. In case of the same sectors

the P/E is used as an analysis tool and comparisons in this case will give productive return for

the investors. If the growth of the expected dividend increases then the P/E of the particular

company also increases in that case.

If the P/E ratio of different companies within the same sector is high then it will be of less

cause when the entire other sectors has high P/E ratios. In case of debt of the company, the

company having higher debt will have low P/E ratio then the company having low debt. The

business having high debt will considerably have high P/E ratio as that particular company

has taken leverage in that case.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

3. Valuation of Share Using Different Models of Valuation:

3.1 Valuation Based on Dividend Discount Method (DDM):

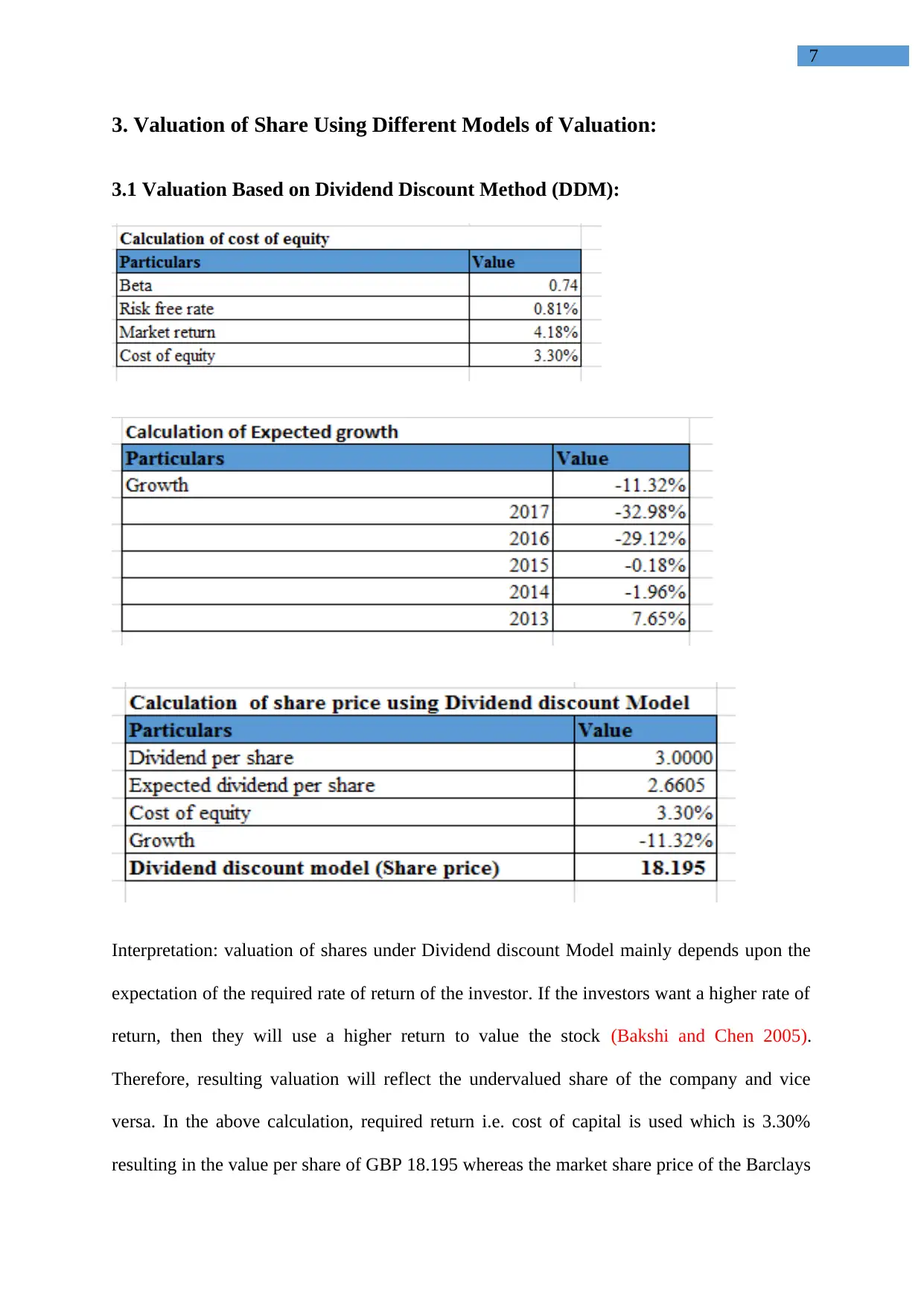

Interpretation: valuation of shares under Dividend discount Model mainly depends upon the

expectation of the required rate of return of the investor. If the investors want a higher rate of

return, then they will use a higher return to value the stock (Bakshi and Chen 2005).

Therefore, resulting valuation will reflect the undervalued share of the company and vice

versa. In the above calculation, required return i.e. cost of capital is used which is 3.30%

resulting in the value per share of GBP 18.195 whereas the market share price of the Barclays

3. Valuation of Share Using Different Models of Valuation:

3.1 Valuation Based on Dividend Discount Method (DDM):

Interpretation: valuation of shares under Dividend discount Model mainly depends upon the

expectation of the required rate of return of the investor. If the investors want a higher rate of

return, then they will use a higher return to value the stock (Bakshi and Chen 2005).

Therefore, resulting valuation will reflect the undervalued share of the company and vice

versa. In the above calculation, required return i.e. cost of capital is used which is 3.30%

resulting in the value per share of GBP 18.195 whereas the market share price of the Barclays

8

plc at valuation date was GBP 198.59. Therefore, the stock is overvalued based on DDM

analysis. The investor should sell the stock and to wait till the stock price below the price as

determined by DDM to get expected return on the stock (Bakshi and Chen 2005).

3.2 Valuation Based on Cash Flow Method:

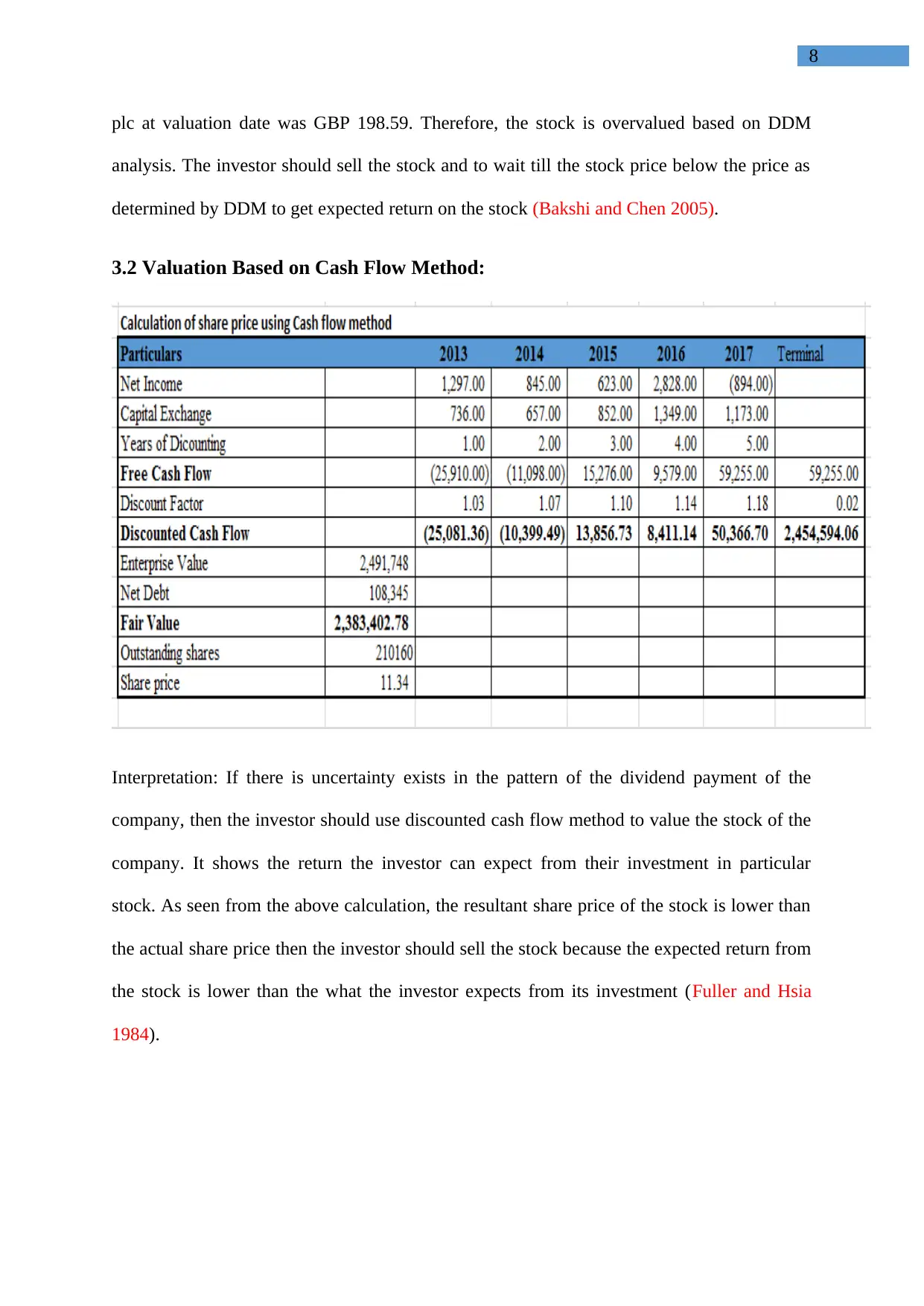

Interpretation: If there is uncertainty exists in the pattern of the dividend payment of the

company, then the investor should use discounted cash flow method to value the stock of the

company. It shows the return the investor can expect from their investment in particular

stock. As seen from the above calculation, the resultant share price of the stock is lower than

the actual share price then the investor should sell the stock because the expected return from

the stock is lower than the what the investor expects from its investment (Fuller and Hsia

1984).

plc at valuation date was GBP 198.59. Therefore, the stock is overvalued based on DDM

analysis. The investor should sell the stock and to wait till the stock price below the price as

determined by DDM to get expected return on the stock (Bakshi and Chen 2005).

3.2 Valuation Based on Cash Flow Method:

Interpretation: If there is uncertainty exists in the pattern of the dividend payment of the

company, then the investor should use discounted cash flow method to value the stock of the

company. It shows the return the investor can expect from their investment in particular

stock. As seen from the above calculation, the resultant share price of the stock is lower than

the actual share price then the investor should sell the stock because the expected return from

the stock is lower than the what the investor expects from its investment (Fuller and Hsia

1984).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

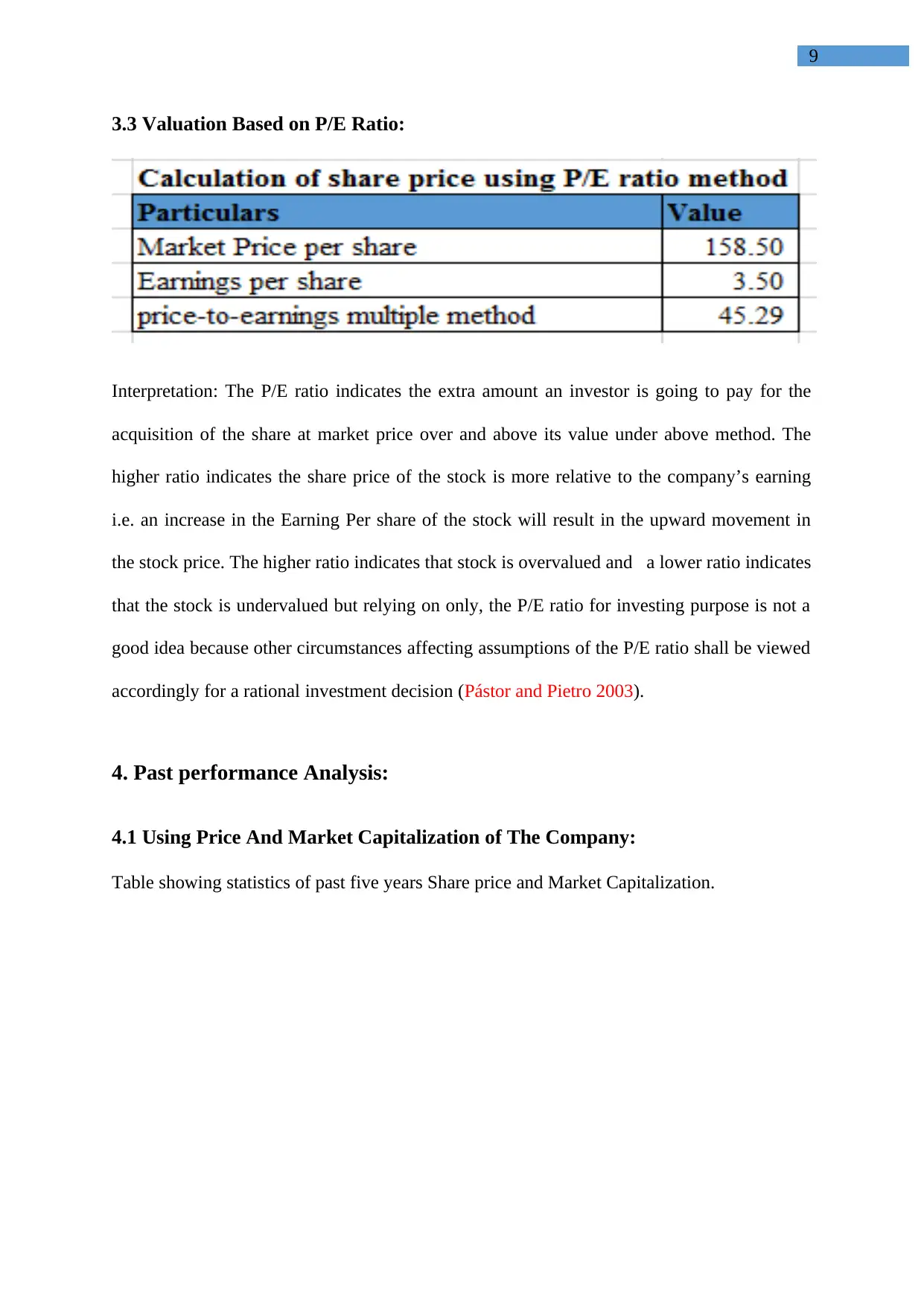

3.3 Valuation Based on P/E Ratio:

Interpretation: The P/E ratio indicates the extra amount an investor is going to pay for the

acquisition of the share at market price over and above its value under above method. The

higher ratio indicates the share price of the stock is more relative to the company’s earning

i.e. an increase in the Earning Per share of the stock will result in the upward movement in

the stock price. The higher ratio indicates that stock is overvalued and a lower ratio indicates

that the stock is undervalued but relying on only, the P/E ratio for investing purpose is not a

good idea because other circumstances affecting assumptions of the P/E ratio shall be viewed

accordingly for a rational investment decision (Pástor and Pietro 2003).

4. Past performance Analysis:

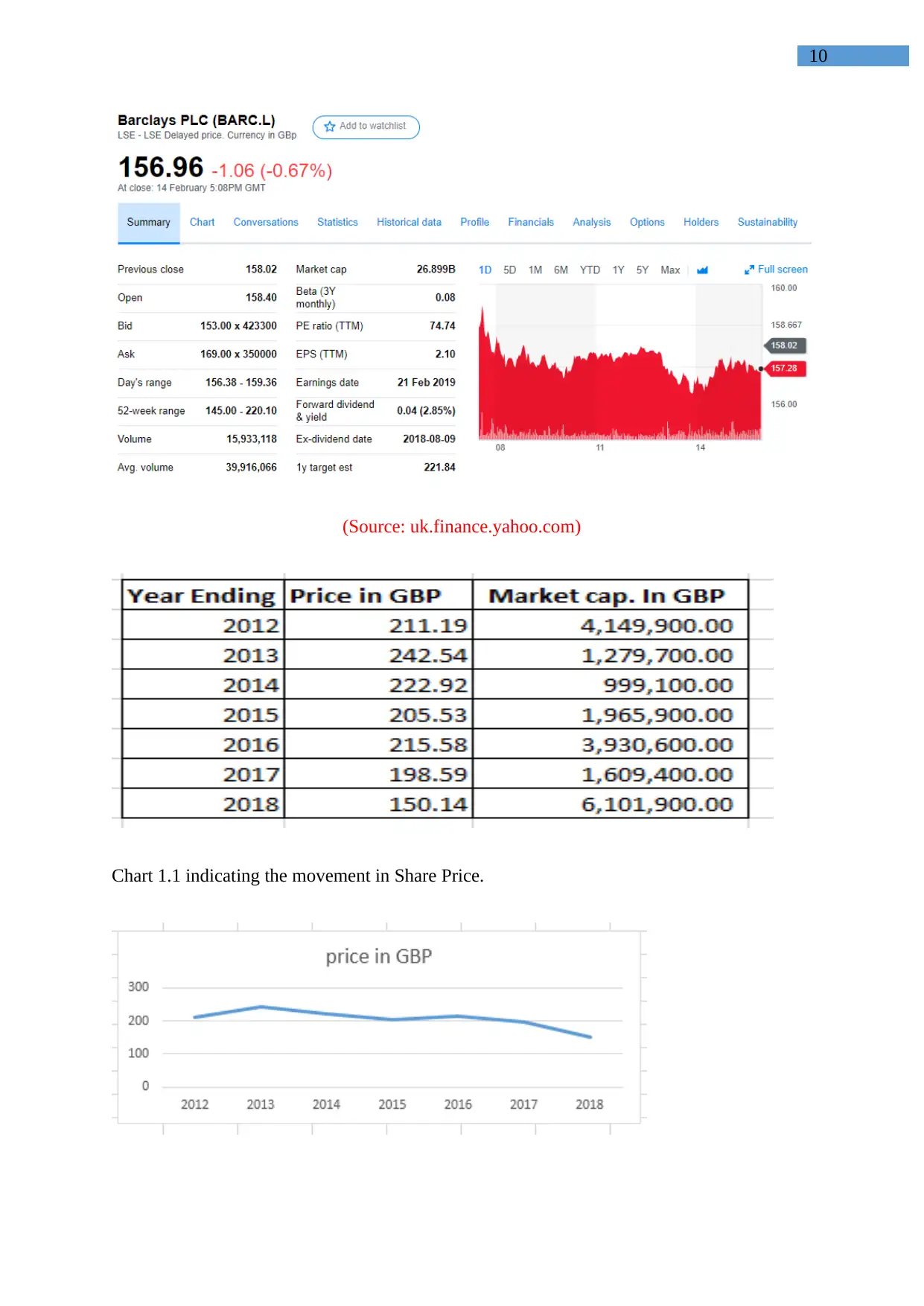

4.1 Using Price And Market Capitalization of The Company:

Table showing statistics of past five years Share price and Market Capitalization.

3.3 Valuation Based on P/E Ratio:

Interpretation: The P/E ratio indicates the extra amount an investor is going to pay for the

acquisition of the share at market price over and above its value under above method. The

higher ratio indicates the share price of the stock is more relative to the company’s earning

i.e. an increase in the Earning Per share of the stock will result in the upward movement in

the stock price. The higher ratio indicates that stock is overvalued and a lower ratio indicates

that the stock is undervalued but relying on only, the P/E ratio for investing purpose is not a

good idea because other circumstances affecting assumptions of the P/E ratio shall be viewed

accordingly for a rational investment decision (Pástor and Pietro 2003).

4. Past performance Analysis:

4.1 Using Price And Market Capitalization of The Company:

Table showing statistics of past five years Share price and Market Capitalization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

(Source: uk.finance.yahoo.com)

Chart 1.1 indicating the movement in Share Price.

(Source: uk.finance.yahoo.com)

Chart 1.1 indicating the movement in Share Price.

11

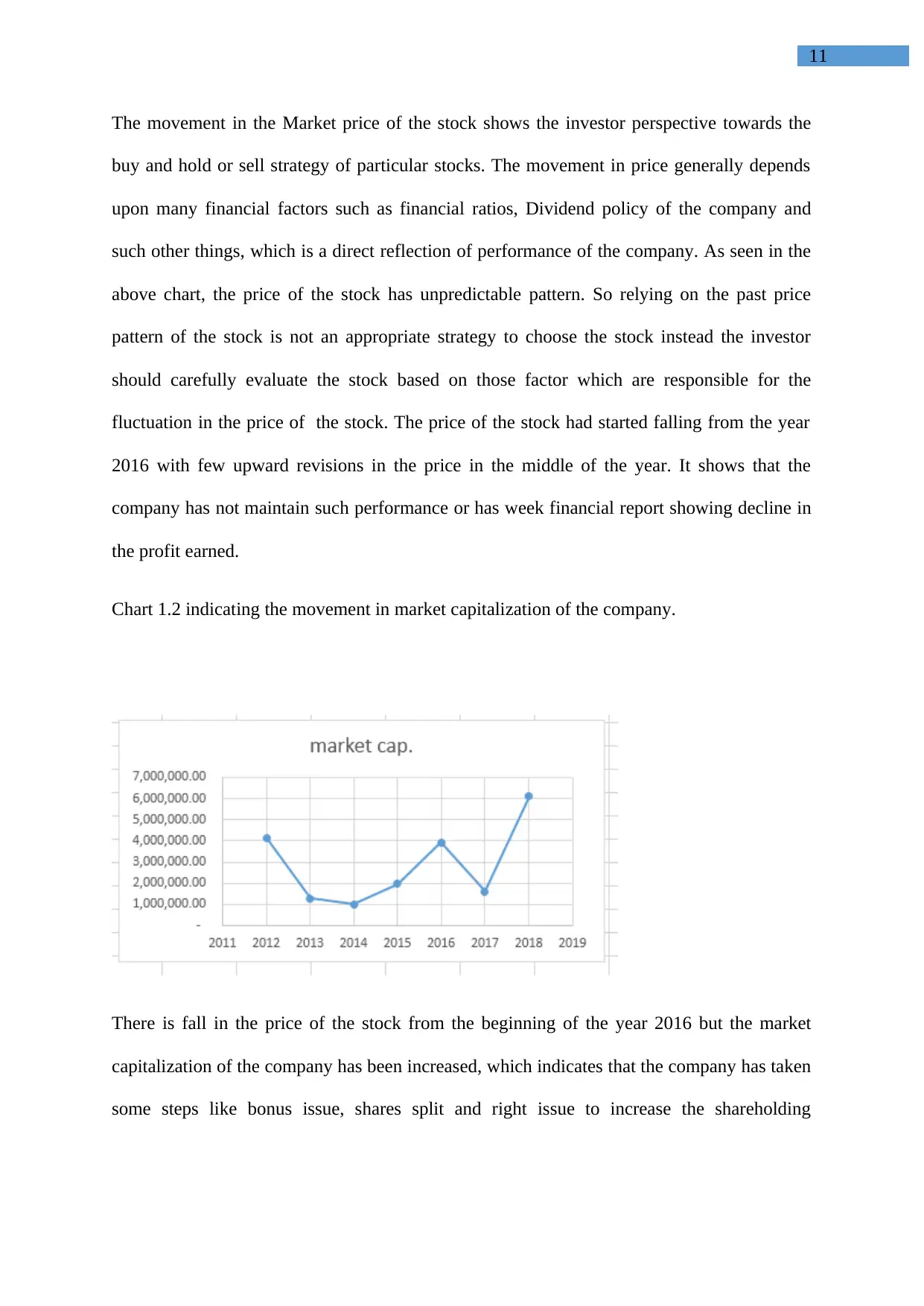

The movement in the Market price of the stock shows the investor perspective towards the

buy and hold or sell strategy of particular stocks. The movement in price generally depends

upon many financial factors such as financial ratios, Dividend policy of the company and

such other things, which is a direct reflection of performance of the company. As seen in the

above chart, the price of the stock has unpredictable pattern. So relying on the past price

pattern of the stock is not an appropriate strategy to choose the stock instead the investor

should carefully evaluate the stock based on those factor which are responsible for the

fluctuation in the price of the stock. The price of the stock had started falling from the year

2016 with few upward revisions in the price in the middle of the year. It shows that the

company has not maintain such performance or has week financial report showing decline in

the profit earned.

Chart 1.2 indicating the movement in market capitalization of the company.

There is fall in the price of the stock from the beginning of the year 2016 but the market

capitalization of the company has been increased, which indicates that the company has taken

some steps like bonus issue, shares split and right issue to increase the shareholding

The movement in the Market price of the stock shows the investor perspective towards the

buy and hold or sell strategy of particular stocks. The movement in price generally depends

upon many financial factors such as financial ratios, Dividend policy of the company and

such other things, which is a direct reflection of performance of the company. As seen in the

above chart, the price of the stock has unpredictable pattern. So relying on the past price

pattern of the stock is not an appropriate strategy to choose the stock instead the investor

should carefully evaluate the stock based on those factor which are responsible for the

fluctuation in the price of the stock. The price of the stock had started falling from the year

2016 with few upward revisions in the price in the middle of the year. It shows that the

company has not maintain such performance or has week financial report showing decline in

the profit earned.

Chart 1.2 indicating the movement in market capitalization of the company.

There is fall in the price of the stock from the beginning of the year 2016 but the market

capitalization of the company has been increased, which indicates that the company has taken

some steps like bonus issue, shares split and right issue to increase the shareholding

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.