Financial Analysis of Walmart and Tesco: Performance Evaluation

VerifiedAdded on 2020/06/05

MANAGEMENT &

ENTREPRENEURSHIP

Paraphrase This Document

TASK 1............................................................................................................................................1

Vertical analysis of financial statements................................................................................1

Horizontal analysis of financial statements............................................................................3

Ratio analysis of financial statements....................................................................................4

TASK 2............................................................................................................................................8

Analysing working capital of Walmart and Tesco.................................................................8

TASK 3............................................................................................................................................9

Critical analysis of annual cash flow of Walmart and Tesco for two financial periods.........9

Findings and Recommendations....................................................................................................10

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................14

Appendix 1: Vertical Balance sheet of Walmart company..................................................14

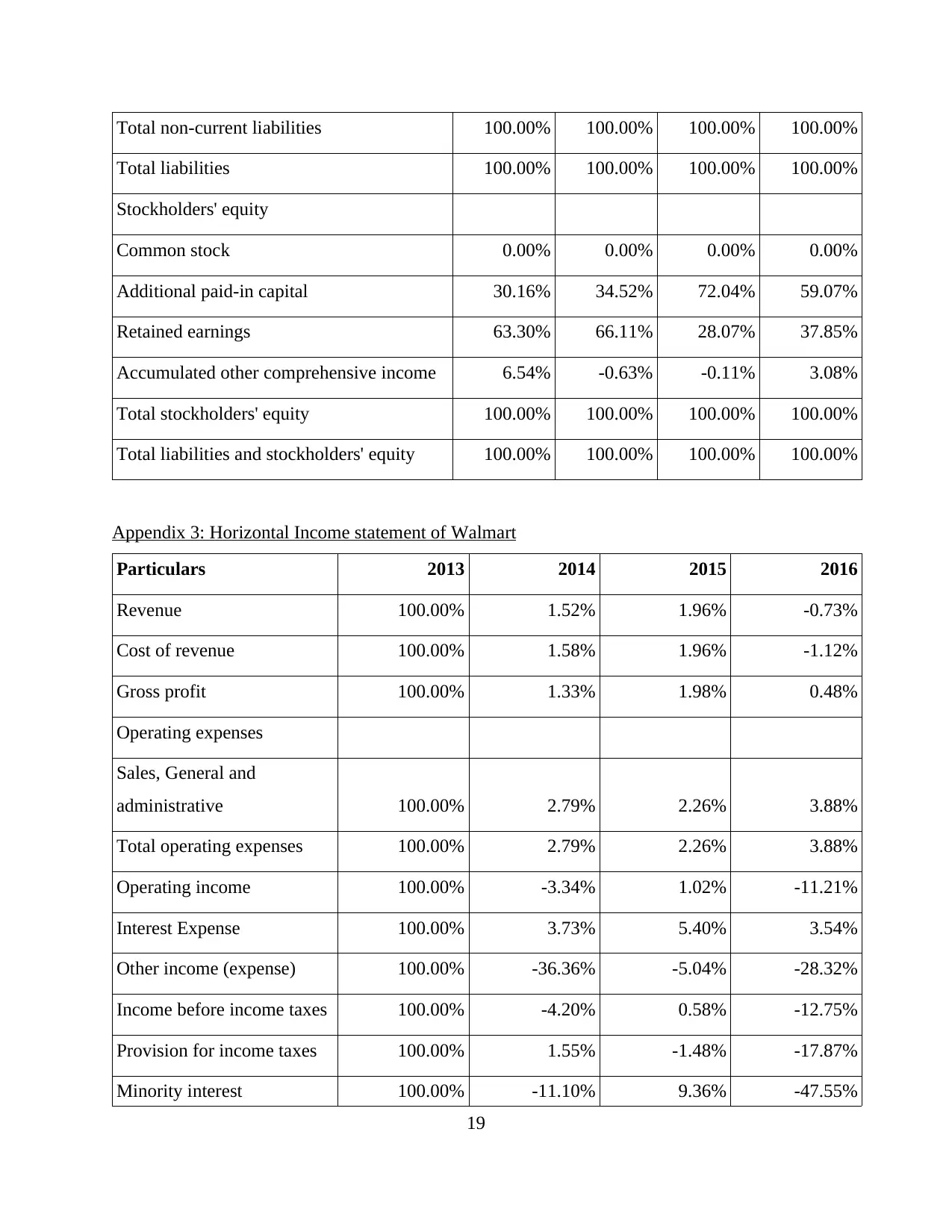

Appendix 2: Vertical balance sheet of Tesco company.......................................................15

Appendix 3: Horizontal Income statement of Walmart.......................................................17

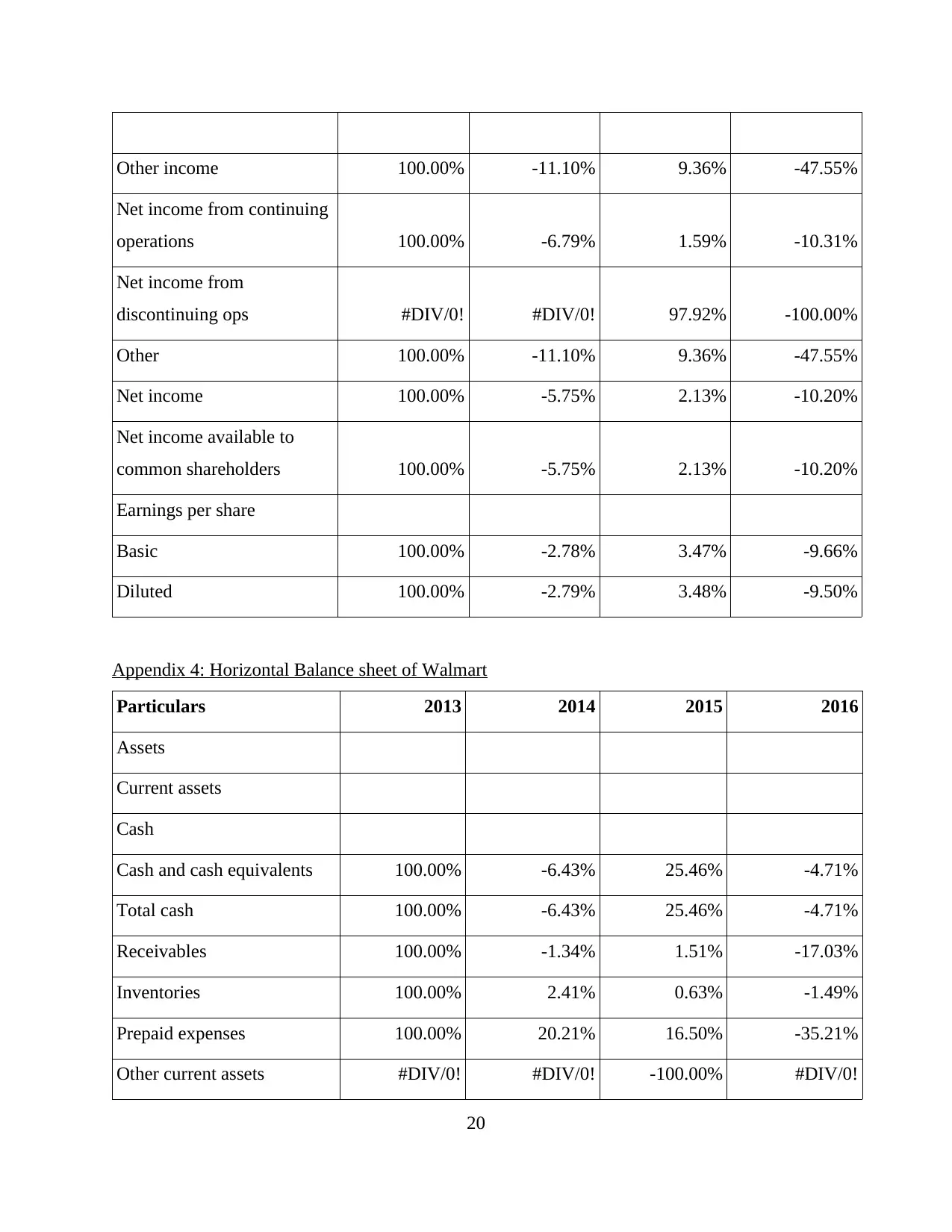

Appendix 4: Horizontal Balance sheet of Walmart..............................................................18

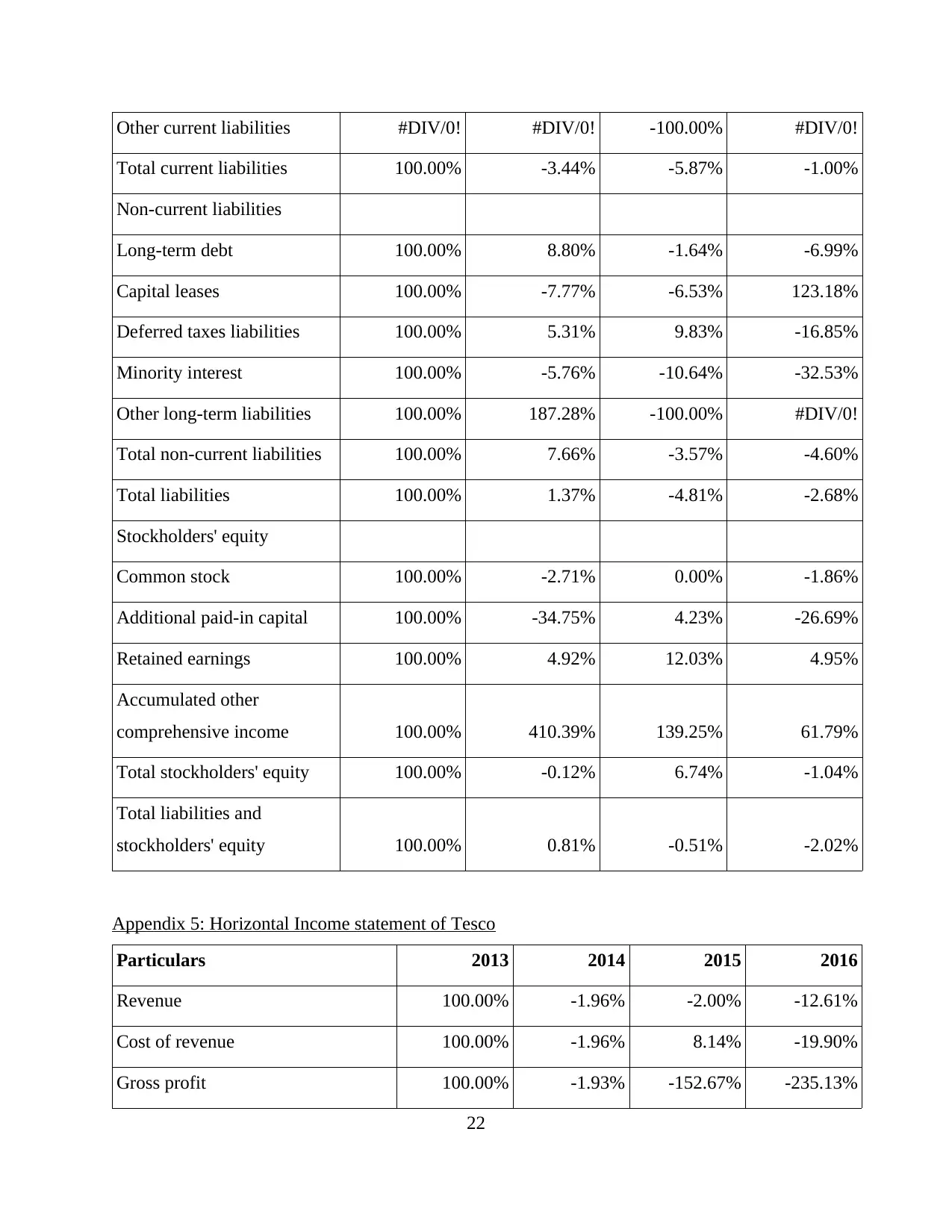

Appendix 5: Horizontal Income statement of Tesco............................................................20

Appendix 6: Horizontal Balance sheet of Tesco..................................................................20

Board of Directors

Asian Food Manufacturer

Date: 8th November 2017

Subject: Financial performance of Walmart and Tesco Plc

TASK 1

Vertical analysis of financial statements

A method which is used to assess relative sizes of various accounts of specific financial

statement is known as vertical analysis. In this, one account is taken as a base and percentages of

its components are computed. When vertical analysis of a balance sheet required to do then total

assets will be taken as a base and percentage change of current and non-current assets is to be

calculated. In order to make this kind of analysis of the income statement then only revenue is

considered as base because all the expenses are covered by this value only (Petruzzo and et.al.,

2015). In the current case two firms are used which operate in retail sector i.e. Tesco and

Walmart. Vertical profit and loss accounts of these both the stated firms are presented and

analysed below:

Vertical income statement of Walmart Company

Particulars 2013 2014 2015 2016

Revenue 100.00% 100.00% 100.00% 100.00%

Cost of revenue 75.13% 75.18% 75.17% 74.87%

Gross profit 24.87% 24.82% 24.83% 25.13%

Operating expenses 0.00% 0.00%

Sales, General and administrative 18.94% 19.18% 19.24% 20.13%

Total operating expenses 18.94% 19.18% 19.24% 20.13%

Operating income 5.93% 5.64% 5.59% 5.00%

Interest Expense 0.48% 0.49% 0.51% 0.53%

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

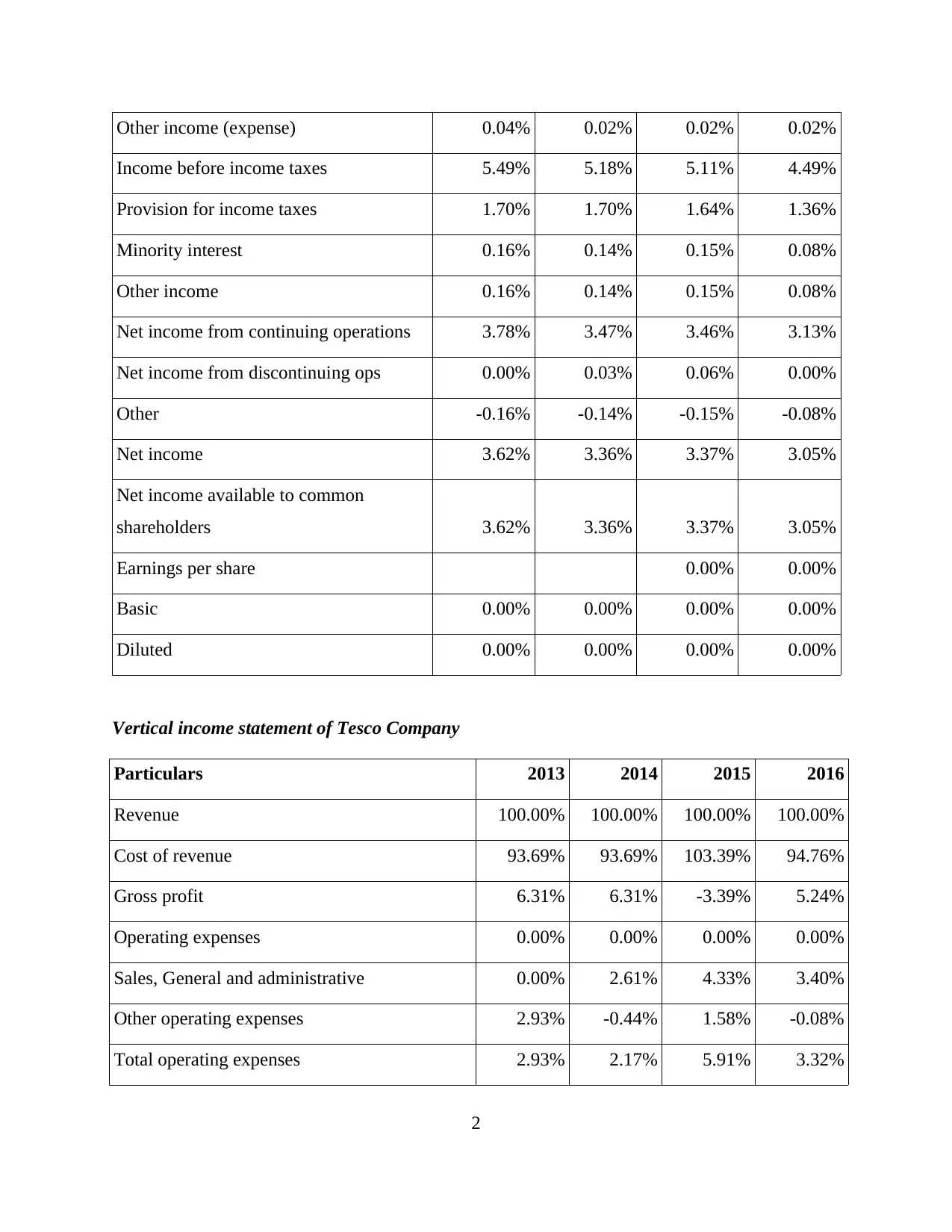

Income before income taxes 5.49% 5.18% 5.11% 4.49%

Provision for income taxes 1.70% 1.70% 1.64% 1.36%

Minority interest 0.16% 0.14% 0.15% 0.08%

Other income 0.16% 0.14% 0.15% 0.08%

Net income from continuing operations 3.78% 3.47% 3.46% 3.13%

Net income from discontinuing ops 0.00% 0.03% 0.06% 0.00%

Other -0.16% -0.14% -0.15% -0.08%

Net income 3.62% 3.36% 3.37% 3.05%

Net income available to common

shareholders 3.62% 3.36% 3.37% 3.05%

Earnings per share 0.00% 0.00%

Basic 0.00% 0.00% 0.00% 0.00%

Diluted 0.00% 0.00% 0.00% 0.00%

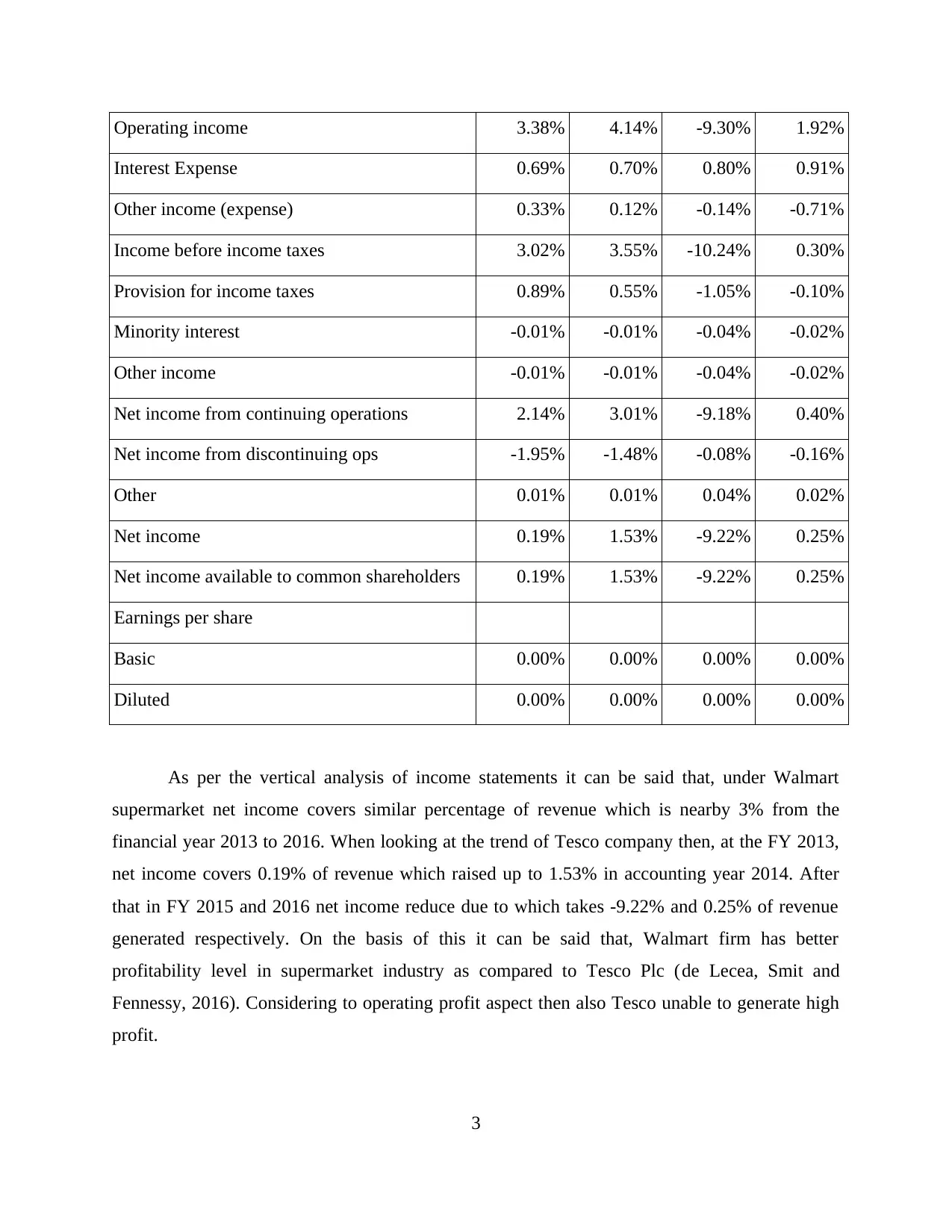

Vertical income statement of Tesco Company

Particulars 2013 2014 2015 2016

Revenue 100.00% 100.00% 100.00% 100.00%

Cost of revenue 93.69% 93.69% 103.39% 94.76%

Gross profit 6.31% 6.31% -3.39% 5.24%

Operating expenses 0.00% 0.00% 0.00% 0.00%

Sales, General and administrative 0.00% 2.61% 4.33% 3.40%

Other operating expenses 2.93% -0.44% 1.58% -0.08%

Total operating expenses 2.93% 2.17% 5.91% 3.32%

2

Paraphrase This Document

Interest Expense 0.69% 0.70% 0.80% 0.91%

Other income (expense) 0.33% 0.12% -0.14% -0.71%

Income before income taxes 3.02% 3.55% -10.24% 0.30%

Provision for income taxes 0.89% 0.55% -1.05% -0.10%

Minority interest -0.01% -0.01% -0.04% -0.02%

Other income -0.01% -0.01% -0.04% -0.02%

Net income from continuing operations 2.14% 3.01% -9.18% 0.40%

Net income from discontinuing ops -1.95% -1.48% -0.08% -0.16%

Other 0.01% 0.01% 0.04% 0.02%

Net income 0.19% 1.53% -9.22% 0.25%

Net income available to common shareholders 0.19% 1.53% -9.22% 0.25%

Earnings per share

Basic 0.00% 0.00% 0.00% 0.00%

Diluted 0.00% 0.00% 0.00% 0.00%

As per the vertical analysis of income statements it can be said that, under Walmart

supermarket net income covers similar percentage of revenue which is nearby 3% from the

financial year 2013 to 2016. When looking at the trend of Tesco company then, at the FY 2013,

net income covers 0.19% of revenue which raised up to 1.53% in accounting year 2014. After

that in FY 2015 and 2016 net income reduce due to which takes -9.22% and 0.25% of revenue

generated respectively. On the basis of this it can be said that, Walmart firm has better

profitability level in supermarket industry as compared to Tesco Plc (de Lecea, Smit and

Fennessy, 2016). Considering to operating profit aspect then also Tesco unable to generate high

profit.

3

covers 69.88% in Walmart and 3.65% in Tesco of total non-current liabilities respectively at the

end of FY 2013. In terms of this specific aspect the Tesco Plc is performing well over the periods

of four accounting years. On the basis of retained earnings, Walmart generates 100.41% and

111.76% at the end of 2014 and 2016 respectively of the total shareholder's equity. The same

values for same years in Tesco are 66.11% and 37.85% which are lower than another stated firm.

Hence, the Tesco Plc performs poor in comparison to its competitor in the industry of retail.

Horizontal analysis of financial statements

Apart from the vertical analysis, when a manager is going to identify percentage change

in the financial statements over the accounting periods then considered as horizontal analysis.

Under this kind of method, base to one particular year is taken and then change up to the last

fiscal year is assessed in terms of percentage. It known as trend analysis also because it helps to

analyse trend of financial data like revenue, profit, assets, liabilities etc (Balanis, 2016). Looking

at the income statement of Walmart and Tesco enterprise then it can be assessed that percentage

change of revenue over the four years i.e. from 2013-16 is better in Walmart firm. The reason is

that, in Tesco firm sales declining each year where percentage change in 2015 and 2016 are -

2.00% as well as -12.61% respectively. However, Walmart generates 1.96% more at the end of

2015 in comparison to previous years. Visualising to the net income then it declines with -

689.43% at the end of 2015 in Tesco whereas increasing in Walmart with 2.13%. At the last

period i.e. 2016 net profit reduces in both the firms where -10.20% in Walmart which is highly

lower than Tesco i.e. -102.40%.

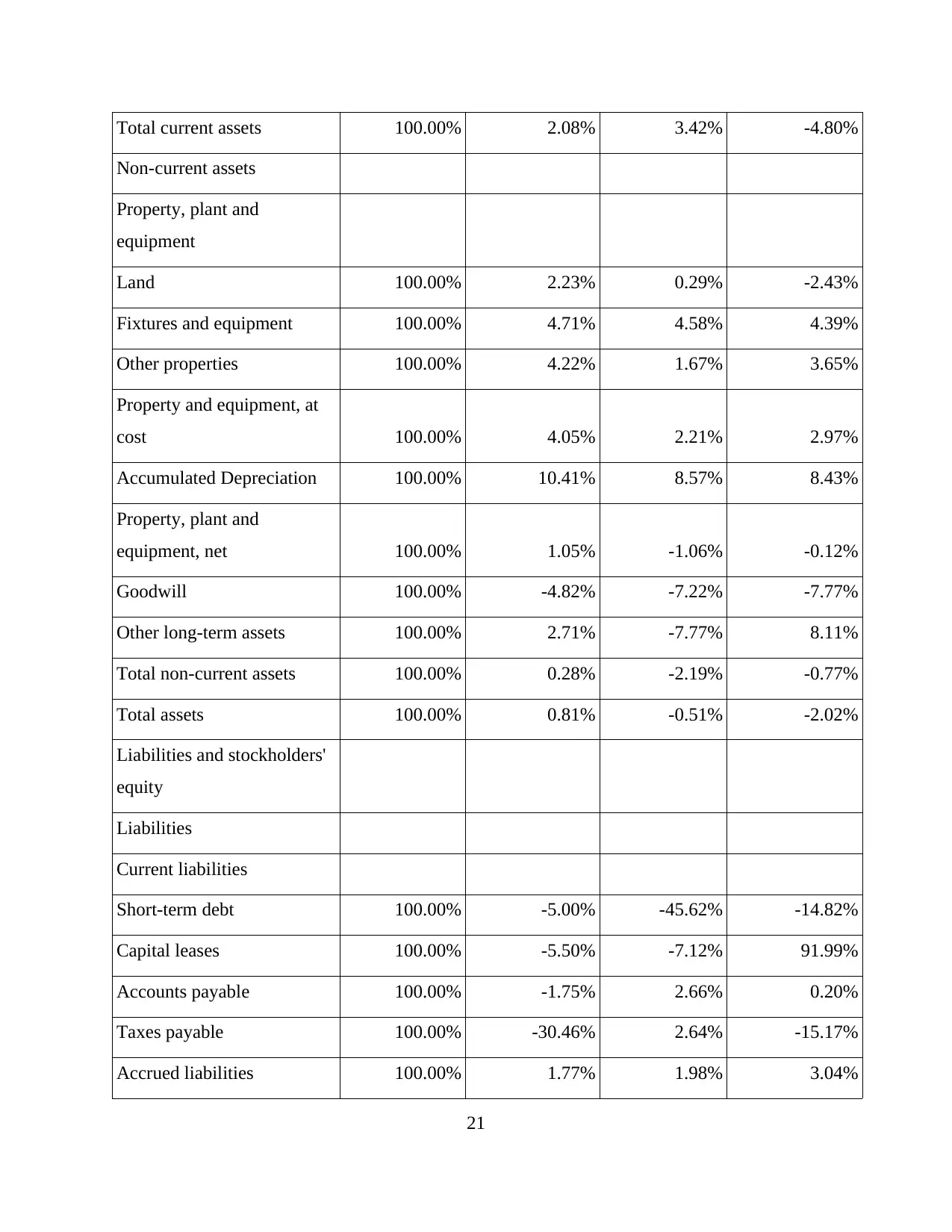

Horizontal balance sheet of Tesco Plc mentioned in appendix shows that, total assets

decreased in the year 2015 and 2016 with -11.86% and -0.70% respectively. Same values in the

another stated company are like -0.51% and -2.02% which are overall better than previous entity.

Debt creates extra financial burden on the firm which must be of the decreasing trend over the

accounting periods at the workplace. In the current case scenario, trend of this aspect is

increasing over the four years in Tesco firm whereas in Walmart it is of the reducing trend (Zhu

and et.al., 2015). In the FY 2014 long-term debt increased with 1636.86% and 8.80% in Tesco

and Walmart respectively. Therefore, it can be said that Tesco not performing well in the

industry of supermarket.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

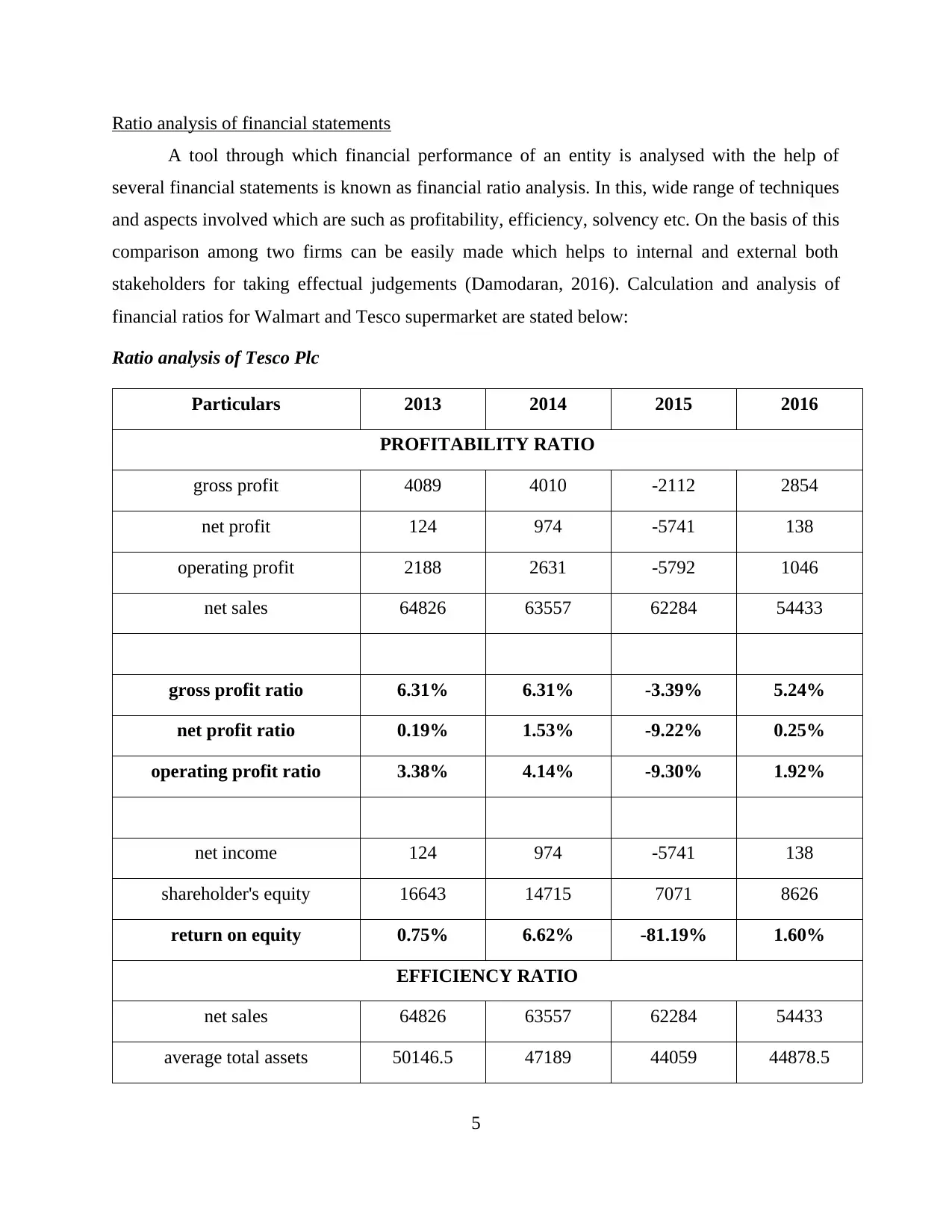

A tool through which financial performance of an entity is analysed with the help of

several financial statements is known as financial ratio analysis. In this, wide range of techniques

and aspects involved which are such as profitability, efficiency, solvency etc. On the basis of this

comparison among two firms can be easily made which helps to internal and external both

stakeholders for taking effectual judgements (Damodaran, 2016). Calculation and analysis of

financial ratios for Walmart and Tesco supermarket are stated below:

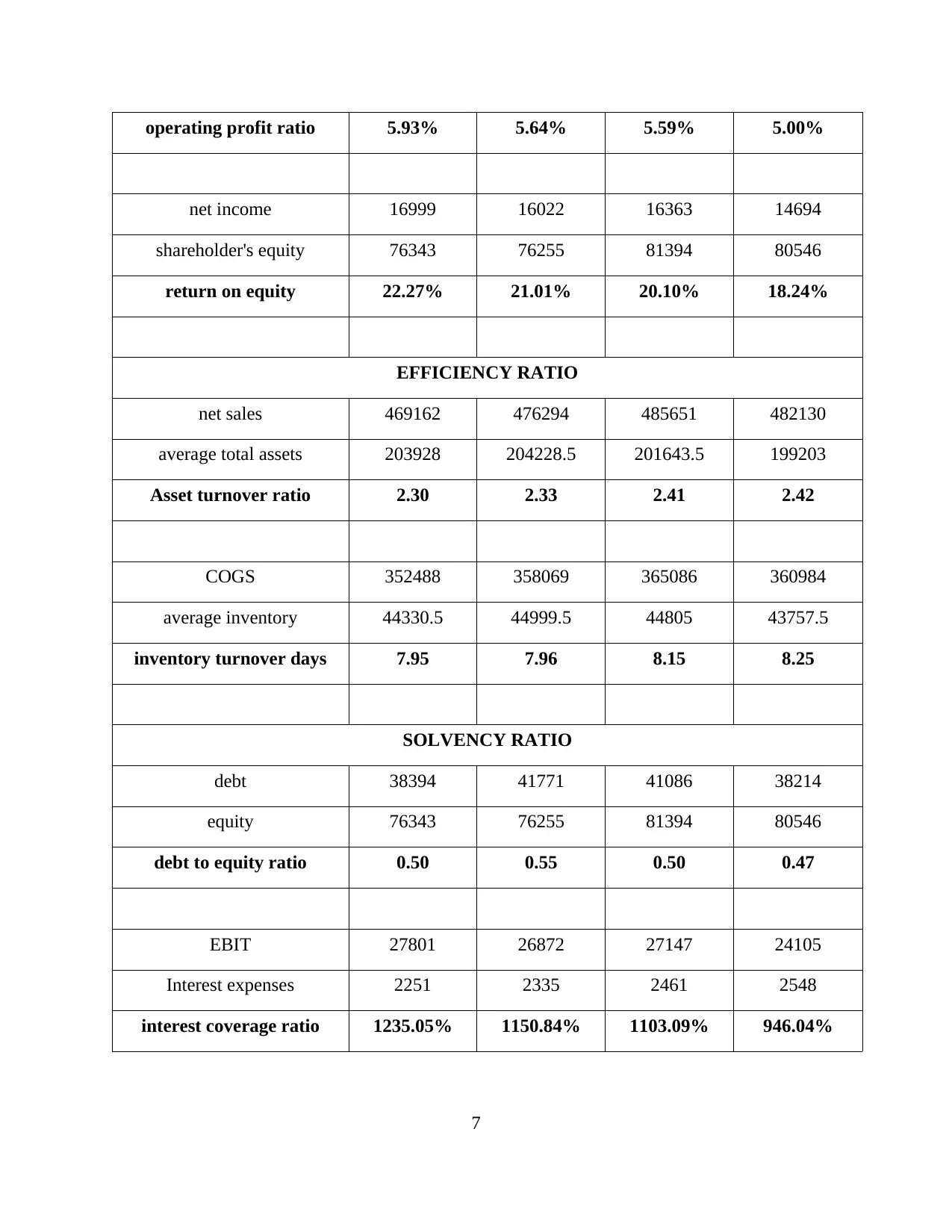

Ratio analysis of Tesco Plc

Particulars 2013 2014 2015 2016

PROFITABILITY RATIO

gross profit 4089 4010 -2112 2854

net profit 124 974 -5741 138

operating profit 2188 2631 -5792 1046

net sales 64826 63557 62284 54433

gross profit ratio 6.31% 6.31% -3.39% 5.24%

net profit ratio 0.19% 1.53% -9.22% 0.25%

operating profit ratio 3.38% 4.14% -9.30% 1.92%

net income 124 974 -5741 138

shareholder's equity 16643 14715 7071 8626

return on equity 0.75% 6.62% -81.19% 1.60%

EFFICIENCY RATIO

net sales 64826 63557 62284 54433

average total assets 50146.5 47189 44059 44878.5

5

Paraphrase This Document

COGS 60737 59547 64396 51579

average inventory 3660 3266.5 2693.5 2365.5

inventory turnover days 16.59 18.23 23.91 21.80

SOLVENCY RATIO

debt 529 9188 10520 10623

equity 16643 14715 7071 8626

debt to equity ratio 0.03 0.62 1.49 1.23

EBIT 2188 2631 -5792 1046

interest expenses 445 447 499 498

interest coverage ratio 491.69% 588.59% -1160.72% 210.04%

Ratio analysis of Walmart Company

Particulars 2013 2014 2015 2016

PROFITABILITY RATIO

gross profit 116674 118225 120565 121146

net profit 16999 16022 16363 14694

operating profit 27801 26872 27147 24105

net sales 469162 476294 485651 482130

gross profit ratio 24.87% 24.82% 24.83% 25.13%

net profit ratio 3.62% 3.36% 3.37% 3.05%

6

net income 16999 16022 16363 14694

shareholder's equity 76343 76255 81394 80546

return on equity 22.27% 21.01% 20.10% 18.24%

EFFICIENCY RATIO

net sales 469162 476294 485651 482130

average total assets 203928 204228.5 201643.5 199203

Asset turnover ratio 2.30 2.33 2.41 2.42

COGS 352488 358069 365086 360984

average inventory 44330.5 44999.5 44805 43757.5

inventory turnover days 7.95 7.96 8.15 8.25

SOLVENCY RATIO

debt 38394 41771 41086 38214

equity 76343 76255 81394 80546

debt to equity ratio 0.50 0.55 0.50 0.47

EBIT 27801 26872 27147 24105

Interest expenses 2251 2335 2461 2548

interest coverage ratio 1235.05% 1150.84% 1103.09% 946.04%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

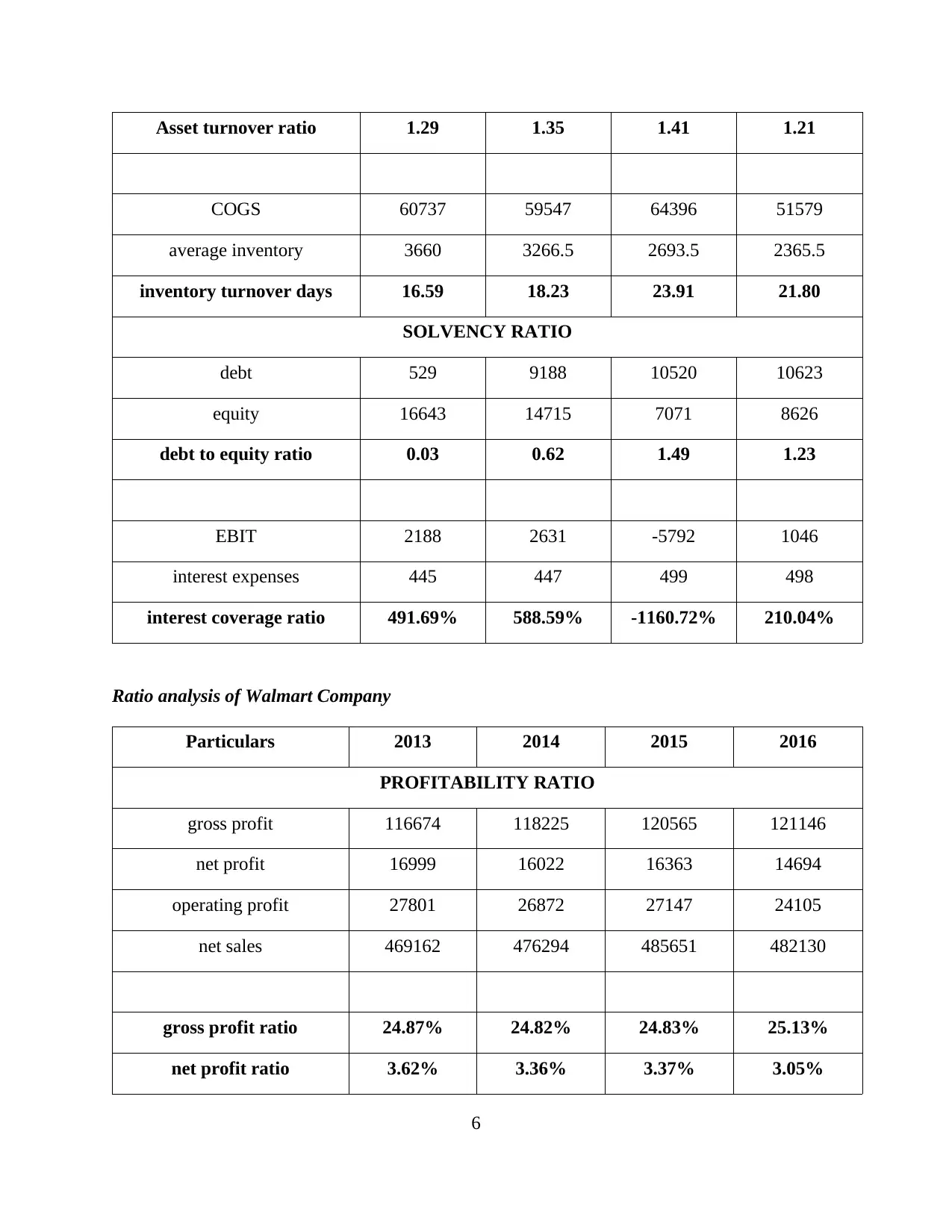

It can be analysed from the above mentioned table that, Tesco company has NP ratio at

the end of FY 2013 was 0.19% which fluctuated over the financial years. In the year 2015 value

of same tool is -9.22% which enhanced and closed at 0.25% in accounting year 2016 (I/S of

Tesco Plc, 2017). When looking at return on equity capital raised from shareholders then it is

also increased or decreased in these four years. Here the management of Tesco is not able to

manage cost aspects and due to which profitability hampers up to the larger extent. On the other

side, net profit ratio of Walmart firm was 3.62% in FY 2013 which was declined over the three

years. Basic reason behind this is that, management not able to decline or administer those

expenses which are indirectly associated with it. Further, at the end of accounting period 2016

same ratio is 3.05% which is higher than Tesco (I/S of Wal-Mart Stores Inc, 2017). It can be

commented on this data that, Tesco's profitability position is highly poor in the supermarket

segment in comparison to Walmart firm.

Efficiency ratios

The ratio through which capacity of an enterprise can be assessed for generating incomes

and revenue using various resources is known as efficiency (Robinson and et.al., 2015). Looking

at the calculation of efficiency ratios it can be pertained that, Tesco's stock turnover ratio is 1.29

times and same in another firm is 2.30 times. In the previous enterprise this value is fluctuating

up to the accounting year 2016 whereas another company has increasing trend in the retail

market. Inventory turnover ratio reflects that stock is how optimum utilised in the workplace in

order to earn net sales at the end of year. Value of this ratio in Tesco enhances continuously and

at the end of 2016 it is 21.80 times. On the other side, stock turnover in same period is 8.25 times

which is very lower compare to Tesco. Therefore, it can be said that Tesco's employees utilising

stock in an optimum direction whereas Walmart unable. In this, second firm needs to implement

highly effectual kind of tactics which will support to utilise inventory in an appropriate manner.

Solvency ratios

This mentioned financial ratio comprises with basically two methods which are like debt

to equity and interest coverage. First ratio shows capital structure of the firm where debt raised

from bank and equity capital raised from shareholders are analysed (Weygandt, Kimmel and

8

Paraphrase This Document

the fiscal year ending 2013. In the previous entity it increases in just second year but after that

reduce consistently which is beneficial for it. On the other side, it was increased and nearby to

0.50:1 which reflects poor business performance of Walmart (B/S of Wal-Mart Stores Inc, 2017).

However, interest coverage ratio in Tesco Plc is highly poor where it not able to generate

adequate operating profit. Due to this, it cannot pay interest amount using EBIT only as

compared to another stated firm.

TASK 2

Analysing working capital of Walmart and Tesco

A tool where basically two terms included in order to make an effective financial analysis

i.e. current assets and current liabilities is considered as working capital. It shows difference and

proportion among current assets as well as liabilities of an entity. On the basis of that liquidity

performance of the is to be analysed properly over the financial periods (Valickova, Havranek

and Horvath, 2015). In order to assess working capital of Walmart and Tesco supermarkets,

current and quick these two ratios are computed. Further, this analysis is stated below:

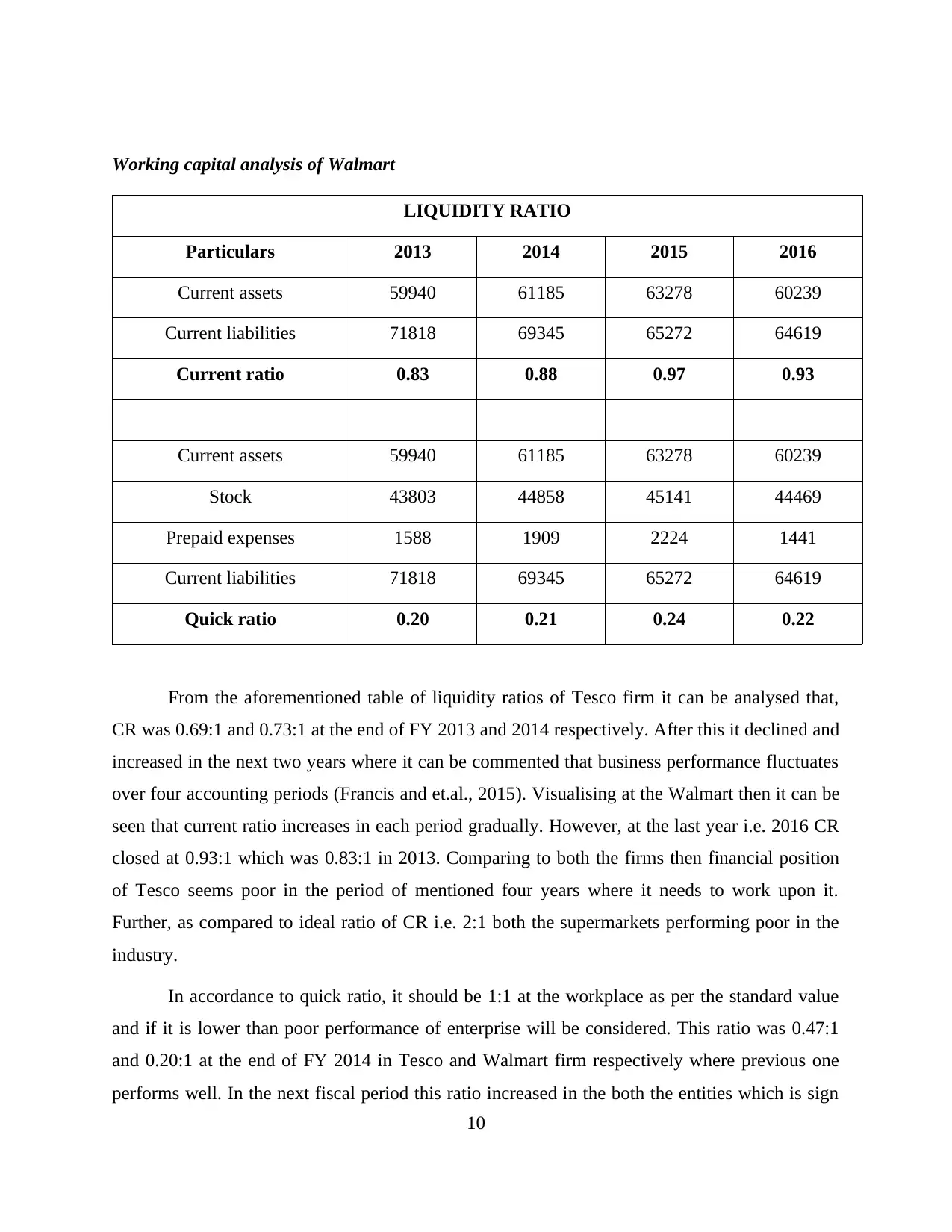

Working capital analysis of Tesco

LIQUIDITY RATIO

Particulars 2013 2014 2015 2016

Current assets 13096 15572 11958 14828

Current liabilities 18985 21399 19810 19714

Current ratio 0.69 0.73 0.60 0.75

Current assets 13096 15572 11958 14828

Stock 3744 3576 2957 2430

Prepaid expenses 417 388 516 440

Current liabilities 18985 21399 19810 19714

Quick ratio 0.47 0.54 0.43 0.61

9

LIQUIDITY RATIO

Particulars 2013 2014 2015 2016

Current assets 59940 61185 63278 60239

Current liabilities 71818 69345 65272 64619

Current ratio 0.83 0.88 0.97 0.93

Current assets 59940 61185 63278 60239

Stock 43803 44858 45141 44469

Prepaid expenses 1588 1909 2224 1441

Current liabilities 71818 69345 65272 64619

Quick ratio 0.20 0.21 0.24 0.22

From the aforementioned table of liquidity ratios of Tesco firm it can be analysed that,

CR was 0.69:1 and 0.73:1 at the end of FY 2013 and 2014 respectively. After this it declined and

increased in the next two years where it can be commented that business performance fluctuates

over four accounting periods (Francis and et.al., 2015). Visualising at the Walmart then it can be

seen that current ratio increases in each period gradually. However, at the last year i.e. 2016 CR

closed at 0.93:1 which was 0.83:1 in 2013. Comparing to both the firms then financial position

of Tesco seems poor in the period of mentioned four years where it needs to work upon it.

Further, as compared to ideal ratio of CR i.e. 2:1 both the supermarkets performing poor in the

industry.

In accordance to quick ratio, it should be 1:1 at the workplace as per the standard value

and if it is lower than poor performance of enterprise will be considered. This ratio was 0.47:1

and 0.20:1 at the end of FY 2014 in Tesco and Walmart firm respectively where previous one

performs well. In the next fiscal period this ratio increased in the both the entities which is sign

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tesco is 0.61:1 whereas same in another chosen company is 0.22:1 (B/S of Tesco Plc, 2017). As

per this tool, financial position of Tesco is better in the retail sector in comparison to another

firm, However, to comment on working capital current ratio is highly considered technique and

on the basis of that Walmart has more cash. Management of Tesco requires taking corrective

actions and apply effective strategies to enhance working capital in the supermarket segment.

TASK 3

Critical analysis of annual cash flow of Walmart and Tesco for two financial periods

Looking at the statement of cash flow (SOCF) of Walmart it can be analysed that, amount

of free cash flow is of the positive value at the end of FY 2015 and 2016 which is 16390 and

15912 respectively. Further, from the operating activities also cash flow is provided positively

over the both years which is worth of 28564 and 27389. When considering to the operating as

well as investing activities of the Walmart then its cash flows are of the negative trend ( Cash

Flow for Wal-Mart Stores Inc, 2017). Overall this firm performs well and appreciable in the

industry of supermarket.

It can be criticised from SOCF of Tesco Plc that at the end of FY 2015 free cash flow is

of the negative value which is worth of -1834. After that, it enhanced in next year and reached up

to 1088 which is not effectual as compared to its rivals. Looking at the operating and investing

activities then the cash flows provided is like 484 and -2015 respectively which is higher than

Walmart in FY 2015. Most of the times cash flows are analysed after taking base to the free cash

flow and on the basis of that Tesco has not effectual cash position (Cash Flow for Tesco Plc,

2017). The reason is that, it has huge debt as compared to Walmart where financial burden is

high on Tesco. Moreover, in terms of cash flows the Walmart supermarket performs well and

beneficial in the retail industry.

Findings and Recommendations

On the basis of the above analysis it can be found that, Walmart company able to perform

well in the market where it operates in comparison to Tesco Plc. Change in revenue over the

financial years i.e. from 2013-16 of the Tesco is of the reducing trend due to lack of utilising

resources properly and effective promotional strategies. Apart from this, management of

Walmart applied highly effectual tactics in order to manage as well as reduce total indirect

11

Paraphrase This Document

has highly effective performance as compared to Tesco Plc. However, the Walmart entity is not

able to utilise available stock in an optimum ways and due to which its stock turnover ratio is

poor. Considering such loopholes and problems, some recommendations for Walmart and Tesco

Plc are stated below:

Tesco firm needs to apply cost management technique at the working place which will

support to raise profitability position in the retail sector.

Management of Tesco must consider attractive kind of promotional and marketing

activities for raising total sales and revenue. Along with this, it should provide goods and

services at lower prices with attractive discounts and schemes.

Tesco requires providing training to the employees for utilising total assets available in

the firm which will help to enhance assets turnover ratio and sales both.

When looking at the Walmart company then it should manage as well as utilise the

available inventory in proper way. So that, it can improve its total stock turnover days

and overall efficiency ratios.

Apart from this, Walmart needs to raise more fund through equity shares rather than

considering the debt or bank loan. Further, its capital structure will be easily and properly

managed in the industry as well as financial burden will be also reduced.

12

Books and Journals

Petruzzo, P. and et.al., 2015. Outcomes after bilateral hand allotransplantation: a risk/benefit

ratio analysis. Annals of surgery. 261(1). pp.213-220.

De Lecea A. M., Smit A. J. and Fennessy S. T., 2016. Riverine dominance of a nearshore marine

demersal food web: evidence from stable isotope and C/N ratio analysis. African Journal

of Marine Science. 38(sup1). pp.S181-S192.

Balanis, C.A., 2016. Antenna theory: analysis and design. John Wiley & Sons.

Zhu, J. and et.al., 2015. Targeted serum metabolite profiling and sequential metabolite ratio

analysis for colorectal cancer progression monitoring. Analytical and bioanalytical

chemistry. 407(26). pp.7857-7863.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance. (324). John Wiley & Sons.

Robinson, T. R. and et.al., 2015. International financial statement analysis. John Wiley & Sons.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2015. Financial & Managerial Accounting.

John Wiley & Sons.

Valickova, P., Havranek, T. and Horvath, R., 2015. Financial Development and Economic

Growth: A Meta-Analysis. Journal of Economic Surveys. 29(3). pp.506-526.

Francis, B. and et.al., 2015. Gender differences in financial reporting decision making: Evidence

from accounting conservatism. Contemporary Accounting Research. 32(3). pp.1285-1318.

Online

I/S of Tesco Plc. 2017. [Online]. Available through: <http://financials.morningstar.com/income-

statement/is.html?t=TSCDY®ion=usa&culture=en-US>

I/S of Wal-Mart Stores Inc. 2017. [Online]. Available through:

<http://financials.morningstar.com/income-statement/is.html?

t=WMT®ion=usa&culture=en-US>

B/S of Tesco Plc. 2017. [Online]. Available through: <http://financials.morningstar.com/balance-

sheet/bs.html?t=TSCDY®ion=usa&culture=en-US>

13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

<http://financials.morningstar.com/balance-sheet/bs.html?

t=WMT®ion=usa&culture=en-US>

Cash Flow for Wal-Mart Stores Inc. 2017. [Online]. Available through:

<http://financials.morningstar.com/cash-flow/cf.html?t=WMT®ion=usa&culture=en-

US>.

Cash Flow for Tesco Plc. 2017. [Online]. Available through:

<http://financials.morningstar.com/cash-flow/cf.html?

t=TSCDY®ion=usa&culture=en-US>.

14

Paraphrase This Document

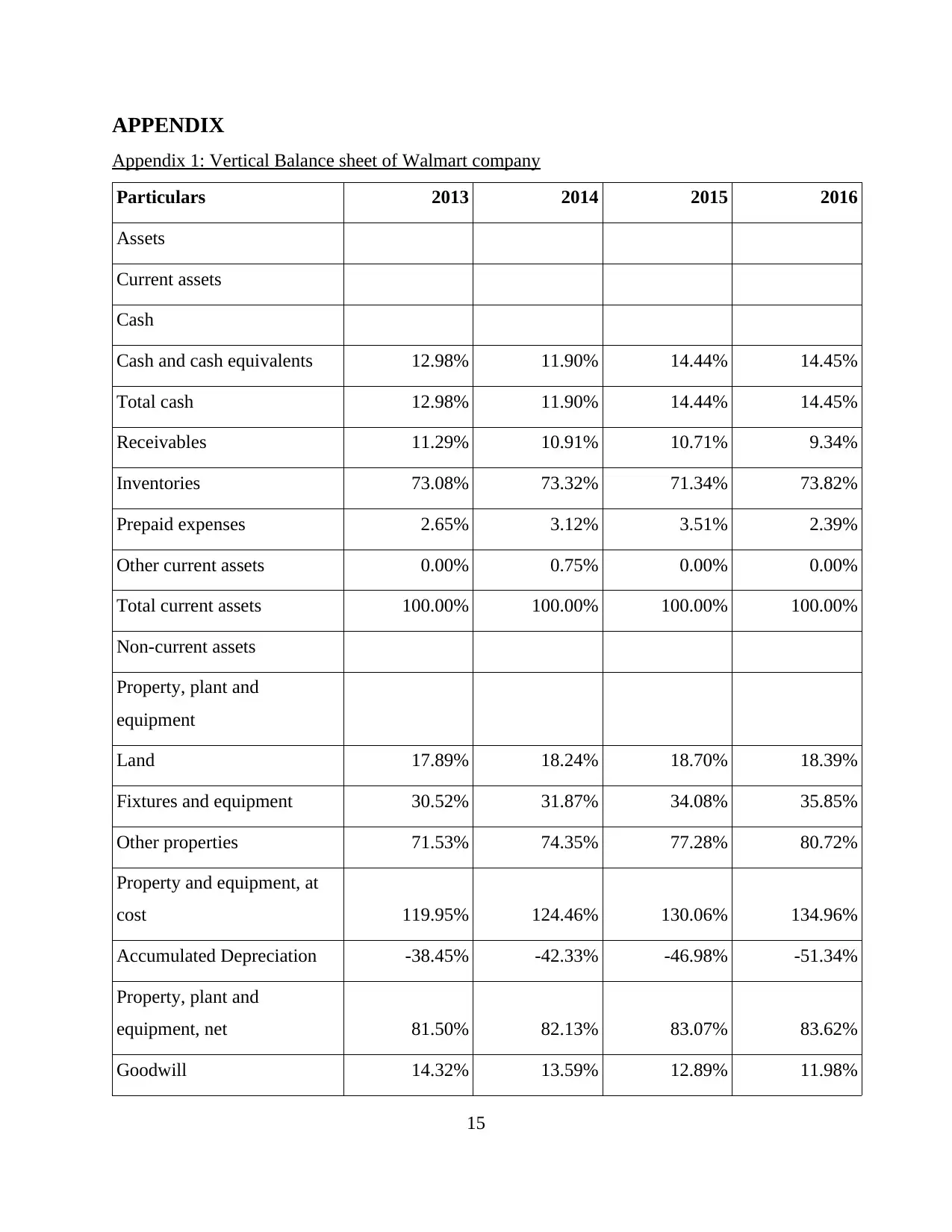

Appendix 1: Vertical Balance sheet of Walmart company

Particulars 2013 2014 2015 2016

Assets

Current assets

Cash

Cash and cash equivalents 12.98% 11.90% 14.44% 14.45%

Total cash 12.98% 11.90% 14.44% 14.45%

Receivables 11.29% 10.91% 10.71% 9.34%

Inventories 73.08% 73.32% 71.34% 73.82%

Prepaid expenses 2.65% 3.12% 3.51% 2.39%

Other current assets 0.00% 0.75% 0.00% 0.00%

Total current assets 100.00% 100.00% 100.00% 100.00%

Non-current assets

Property, plant and

equipment

Land 17.89% 18.24% 18.70% 18.39%

Fixtures and equipment 30.52% 31.87% 34.08% 35.85%

Other properties 71.53% 74.35% 77.28% 80.72%

Property and equipment, at

cost 119.95% 124.46% 130.06% 134.96%

Accumulated Depreciation -38.45% -42.33% -46.98% -51.34%

Property, plant and

equipment, net 81.50% 82.13% 83.07% 83.62%

Goodwill 14.32% 13.59% 12.89% 11.98%

15

Total non-current assets 100.00% 100.00% 100.00% 100.00%

Total assets 100.00% 100.00% 100.00% 100.00%

Liabilities and stockholders'

equity

Liabilities

Current liabilities

Short-term debt 17.25% 16.98% 9.81% 8.44%

Capital leases 0.46% 0.45% 0.44% 0.85%

Accounts payable 53.02% 53.95% 58.85% 59.56%

Taxes payable 7.05% 5.08% 5.54% 4.74%

Accrued liabilities 22.22% 23.42% 25.37% 26.41%

Other current liabilities 0.00% 0.13% 0.00% 0.00%

Total current liabilities 100.00% 100.00% 100.00% 100.00%

Non-current liabilities

Long-term debt 69.88% 70.62% 72.03% 70.23%

Capital leases 5.50% 4.71% 4.57% 10.69%

Deferred taxes liabilities 13.86% 13.55% 15.44% 13.45%

Minority interest 9.82% 8.59% 7.96% 5.63%

Other long-term liabilities 0.94% 2.52% 0.00% 0.00%

Total non-current liabilities 100.00% 100.00% 100.00% 100.00%

Total liabilities 100.00% 100.00% 100.00% 100.00%

Stockholders' equity

Common stock 0.43% 0.42% 0.40% 0.39%

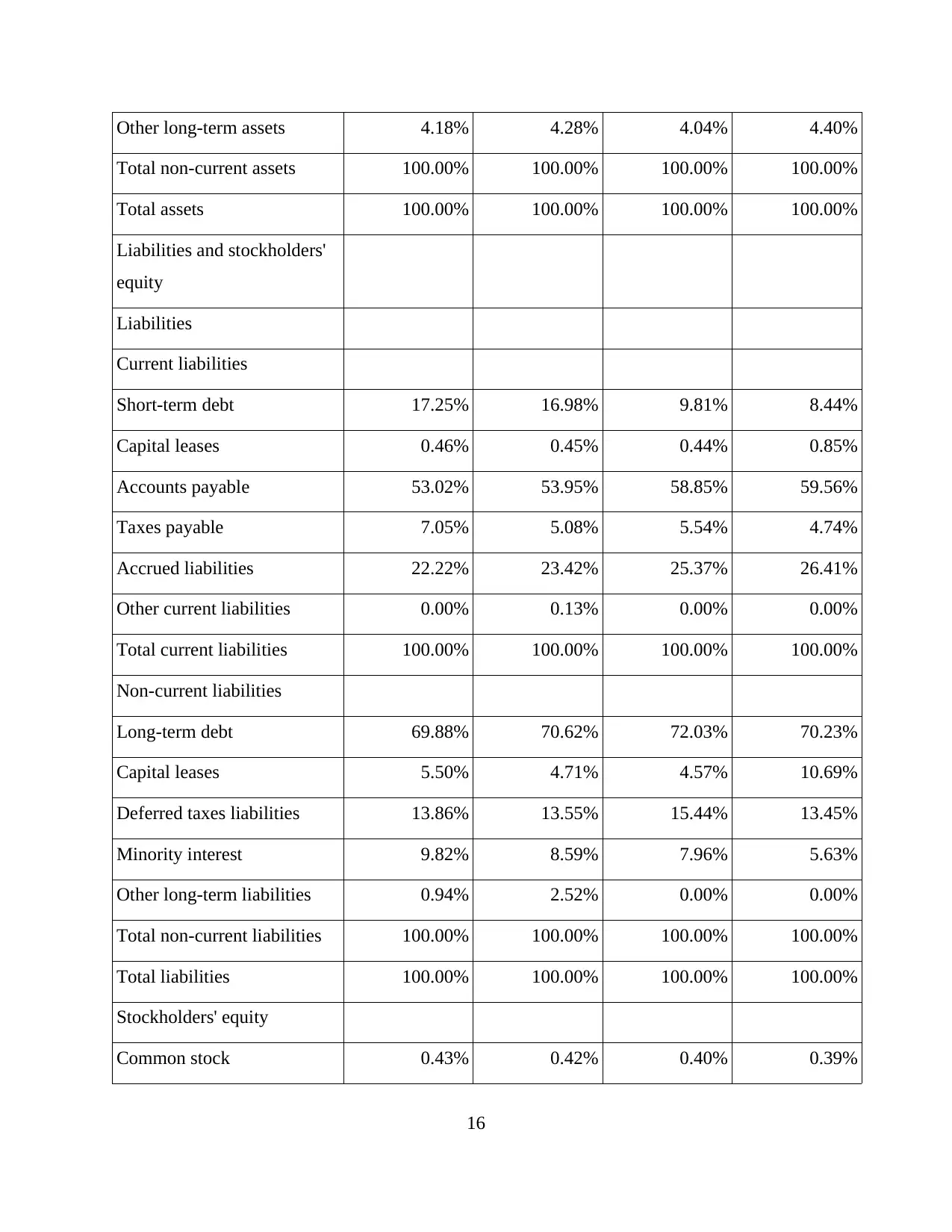

16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Retained earnings 95.59% 100.41% 105.38% 111.76%

Accumulated other

comprehensive income -0.77% -3.93% -8.81% -14.40%

Total stockholders' equity 100.00% 100.00% 100.00% 100.00%

Total liabilities and

stockholders' equity 100.00% 100.00% 100.00% 100.00%

Appendix 2: Vertical balance sheet of Tesco company

Particulars 2013 2014 2015 2016

Assets

Current assets

Cash

Cash and cash equivalents 19.18% 16.09% 18.11% 20.79%

Short-term investments 4.43% 7.04% 6.24% 24.54%

Total cash 23.61% 23.13% 24.34% 45.33%

Inventories 28.59% 22.96% 24.73% 16.39%

Prepaid expenses 3.18% 2.49% 4.32% 2.97%

Other current assets 44.62% 51.41% 46.61% 35.32%

Total current assets 100.00% 100.00% 100.00% 100.00%

Non-current assets

Property, plant and equipment

Land 67.01% 74.39% 78.43% 77.58%

Other properties 29.23% 31.37% 35.63% 36.00%

Property and equipment, at cost 96.25% 105.76% 114.06% 113.58%

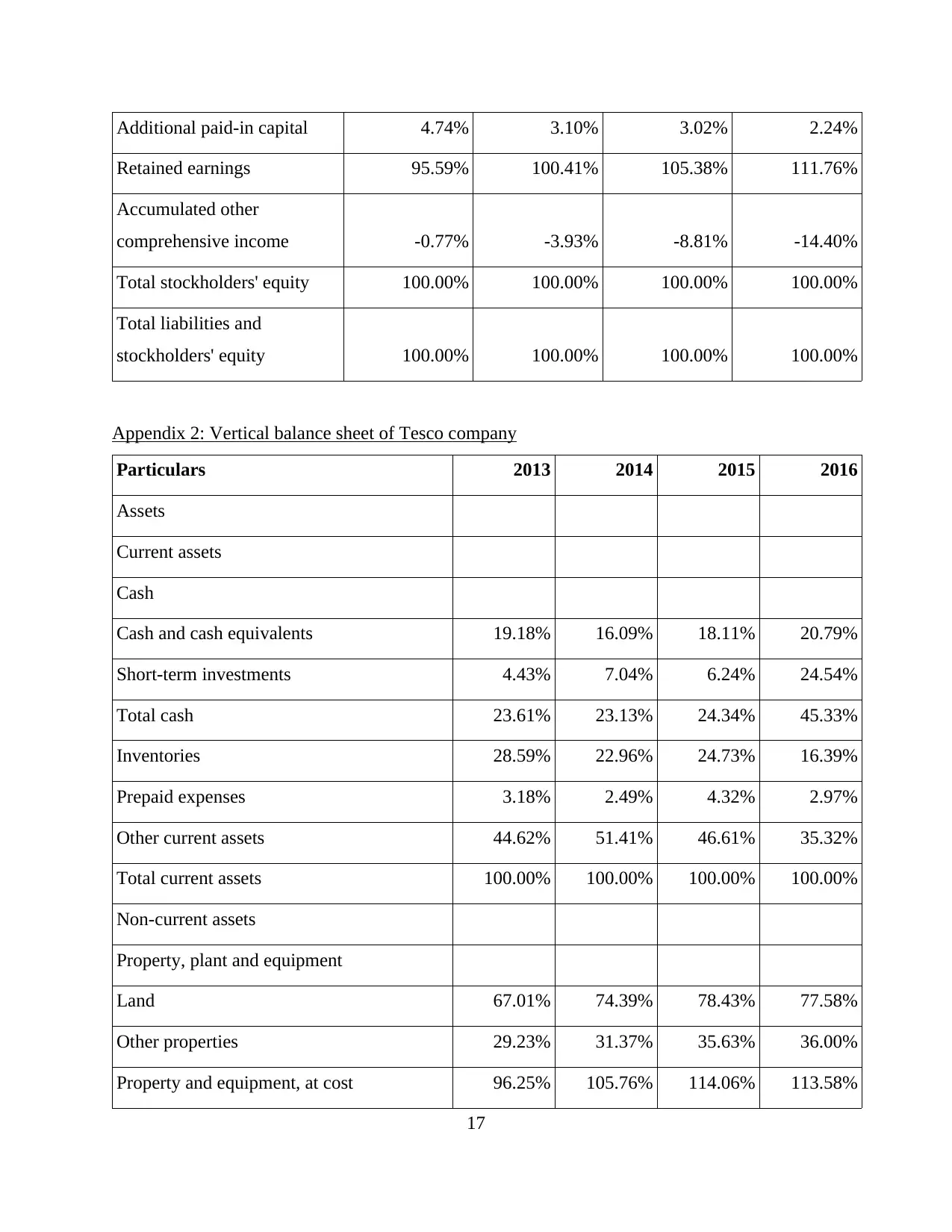

17

Paraphrase This Document

Property, plant and equipment, net 67.16% 70.80% 63.37% 61.56%

Goodwill 7.98% 6.61% 7.09% 8.66%

Intangible assets 3.80% 4.36% 4.60% 1.23%

Deferred income taxes 0.16% 0.21% 1.59% 0.17%

Other long-term assets 20.91% 18.02% 23.35% 28.38%

Total non-current assets 100.00% 100.00% 100.00% 100.00%

Total assets 100.00% 100.00% 100.00% 100.00%

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 4.00% 8.90% 10.09% 14.28%

Capital leases 0.03% 0.03% 0.05% 0.06%

Accounts payable 31.79% 27.25% 25.62% 23.05%

Taxes payable 5.05% 4.17% 2.33% 4.09%

Other current liabilities 59.12% 59.65% 61.91% 58.52%

Total current liabilities 100.00% 100.00% 100.00% 100.00%

Non-current liabilities

Long-term debt 3.65% 65.40% 60.69% 68.25%

Capital leases 65.78% 0.82% 0.76% 0.57%

Deferred taxes liabilities 6.94% 4.23% 1.15% 0.87%

Pensions and other benefits 16.40% 22.73% 27.94% 20.40%

Minority interest 0.12% 0.05% 0.00% -0.06%

Other long-term liabilities 7.11% 6.78% 9.47% 9.98%

18

Total liabilities 100.00% 100.00% 100.00% 100.00%

Stockholders' equity

Common stock 0.00% 0.00% 0.00% 0.00%

Additional paid-in capital 30.16% 34.52% 72.04% 59.07%

Retained earnings 63.30% 66.11% 28.07% 37.85%

Accumulated other comprehensive income 6.54% -0.63% -0.11% 3.08%

Total stockholders' equity 100.00% 100.00% 100.00% 100.00%

Total liabilities and stockholders' equity 100.00% 100.00% 100.00% 100.00%

Appendix 3: Horizontal Income statement of Walmart

Particulars 2013 2014 2015 2016

Revenue 100.00% 1.52% 1.96% -0.73%

Cost of revenue 100.00% 1.58% 1.96% -1.12%

Gross profit 100.00% 1.33% 1.98% 0.48%

Operating expenses

Sales, General and

administrative 100.00% 2.79% 2.26% 3.88%

Total operating expenses 100.00% 2.79% 2.26% 3.88%

Operating income 100.00% -3.34% 1.02% -11.21%

Interest Expense 100.00% 3.73% 5.40% 3.54%

Other income (expense) 100.00% -36.36% -5.04% -28.32%

Income before income taxes 100.00% -4.20% 0.58% -12.75%

Provision for income taxes 100.00% 1.55% -1.48% -17.87%

Minority interest 100.00% -11.10% 9.36% -47.55%

19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net income from continuing

operations 100.00% -6.79% 1.59% -10.31%

Net income from

discontinuing ops #DIV/0! #DIV/0! 97.92% -100.00%

Other 100.00% -11.10% 9.36% -47.55%

Net income 100.00% -5.75% 2.13% -10.20%

Net income available to

common shareholders 100.00% -5.75% 2.13% -10.20%

Earnings per share

Basic 100.00% -2.78% 3.47% -9.66%

Diluted 100.00% -2.79% 3.48% -9.50%

Appendix 4: Horizontal Balance sheet of Walmart

Particulars 2013 2014 2015 2016

Assets

Current assets

Cash

Cash and cash equivalents 100.00% -6.43% 25.46% -4.71%

Total cash 100.00% -6.43% 25.46% -4.71%

Receivables 100.00% -1.34% 1.51% -17.03%

Inventories 100.00% 2.41% 0.63% -1.49%

Prepaid expenses 100.00% 20.21% 16.50% -35.21%

Other current assets #DIV/0! #DIV/0! -100.00% #DIV/0!

20

Paraphrase This Document

Non-current assets

Property, plant and

equipment

Land 100.00% 2.23% 0.29% -2.43%

Fixtures and equipment 100.00% 4.71% 4.58% 4.39%

Other properties 100.00% 4.22% 1.67% 3.65%

Property and equipment, at

cost 100.00% 4.05% 2.21% 2.97%

Accumulated Depreciation 100.00% 10.41% 8.57% 8.43%

Property, plant and

equipment, net 100.00% 1.05% -1.06% -0.12%

Goodwill 100.00% -4.82% -7.22% -7.77%

Other long-term assets 100.00% 2.71% -7.77% 8.11%

Total non-current assets 100.00% 0.28% -2.19% -0.77%

Total assets 100.00% 0.81% -0.51% -2.02%

Liabilities and stockholders'

equity

Liabilities

Current liabilities

Short-term debt 100.00% -5.00% -45.62% -14.82%

Capital leases 100.00% -5.50% -7.12% 91.99%

Accounts payable 100.00% -1.75% 2.66% 0.20%

Taxes payable 100.00% -30.46% 2.64% -15.17%

Accrued liabilities 100.00% 1.77% 1.98% 3.04%

21

Total current liabilities 100.00% -3.44% -5.87% -1.00%

Non-current liabilities

Long-term debt 100.00% 8.80% -1.64% -6.99%

Capital leases 100.00% -7.77% -6.53% 123.18%

Deferred taxes liabilities 100.00% 5.31% 9.83% -16.85%

Minority interest 100.00% -5.76% -10.64% -32.53%

Other long-term liabilities 100.00% 187.28% -100.00% #DIV/0!

Total non-current liabilities 100.00% 7.66% -3.57% -4.60%

Total liabilities 100.00% 1.37% -4.81% -2.68%

Stockholders' equity

Common stock 100.00% -2.71% 0.00% -1.86%

Additional paid-in capital 100.00% -34.75% 4.23% -26.69%

Retained earnings 100.00% 4.92% 12.03% 4.95%

Accumulated other

comprehensive income 100.00% 410.39% 139.25% 61.79%

Total stockholders' equity 100.00% -0.12% 6.74% -1.04%

Total liabilities and

stockholders' equity 100.00% 0.81% -0.51% -2.02%

Appendix 5: Horizontal Income statement of Tesco

Particulars 2013 2014 2015 2016

Revenue 100.00% -1.96% -2.00% -12.61%

Cost of revenue 100.00% -1.96% 8.14% -19.90%

Gross profit 100.00% -1.93% -152.67% -235.13%

22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.