Financial Analysis Report: Evaluating Investment Options in Healthcare

VerifiedAdded on 2020/05/08

|10

|1394

|82

Report

AI Summary

This report presents a financial analysis of three distinct healthcare scenarios: ABC Hospital, Serenity Health Care, and Montgomery Home and Community-Based Services. The analysis for ABC Hospital evaluates two investment options using Net Present Value (NPV), Return on Investment (ROI), and Internal Rate of Return (IRR) to determine the most feasible choice. For Serenity Health Care, the report assesses the CEO's decision to acquire Hall by examining the organization's liquidity position through current and acid ratio calculations. Finally, the analysis of Montgomery Home and Community-Based Services includes a break-even volume calculation and a detailed financial projection, evaluating the payback period. The report highlights the importance of financial metrics in making sound investment and operational decisions within the healthcare sector, providing a comprehensive overview of financial planning and analysis techniques. The report also includes references to relevant academic literature and industry resources.

Running head: FINANCIAL ANALYSIS

Financial Analysis

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Analysis

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS

Table of Contents

Scenario 1: ABC Hospital..........................................................................................................2

Scenario 2: Serenity Health Care...............................................................................................3

Scenario 3: Montgomery Home and Community-Based Services............................................4

Answer to Part 1:....................................................................................................................4

Answer to Part 2:....................................................................................................................5

References and Bibliographies:..................................................................................................9

Table of Contents

Scenario 1: ABC Hospital..........................................................................................................2

Scenario 2: Serenity Health Care...............................................................................................3

Scenario 3: Montgomery Home and Community-Based Services............................................4

Answer to Part 1:....................................................................................................................4

Answer to Part 2:....................................................................................................................5

References and Bibliographies:..................................................................................................9

2FINANCIAL ANALYSIS

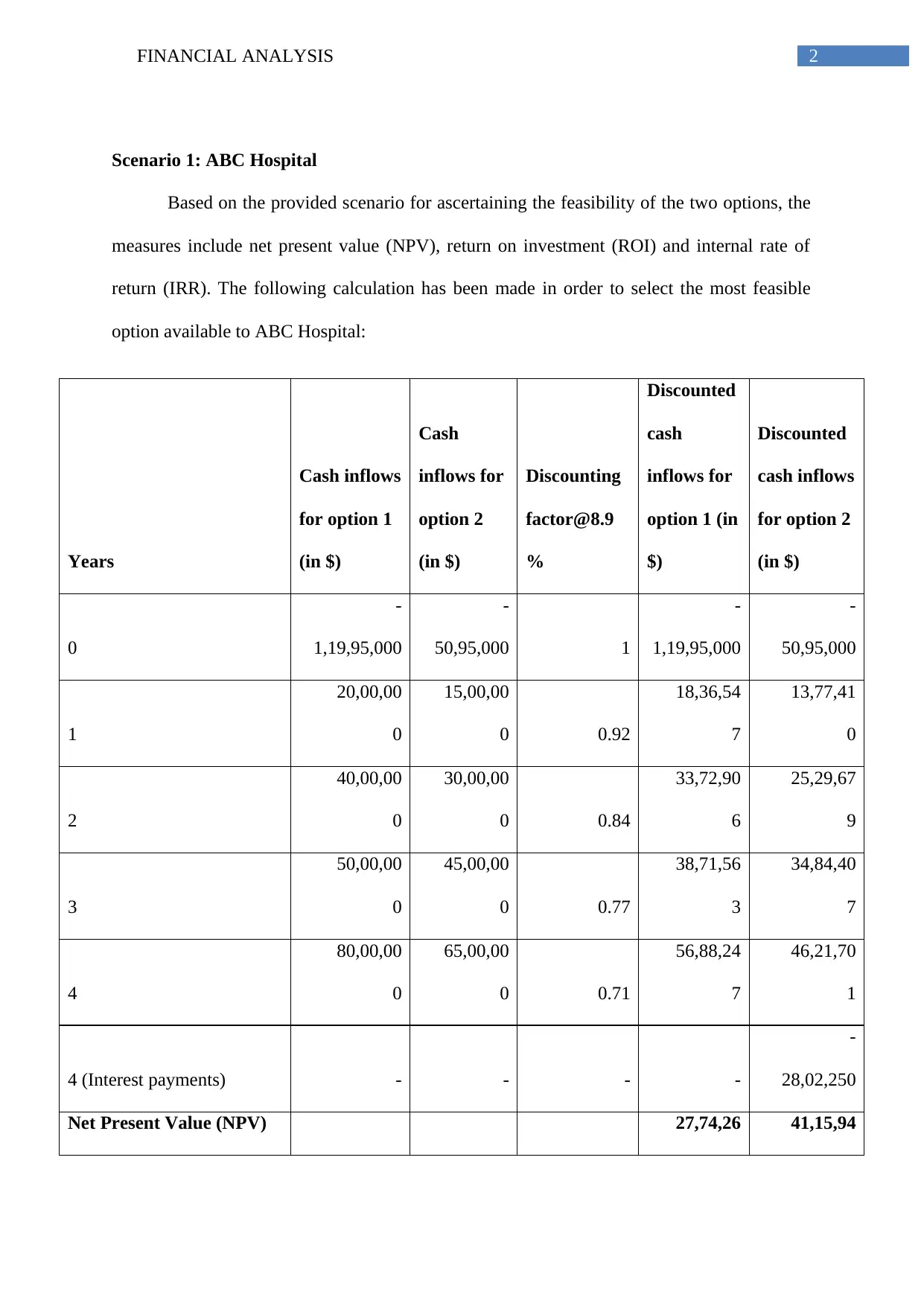

Scenario 1: ABC Hospital

Based on the provided scenario for ascertaining the feasibility of the two options, the

measures include net present value (NPV), return on investment (ROI) and internal rate of

return (IRR). The following calculation has been made in order to select the most feasible

option available to ABC Hospital:

Years

Cash inflows

for option 1

(in $)

Cash

inflows for

option 2

(in $)

Discounting

factor@8.9

%

Discounted

cash

inflows for

option 1 (in

$)

Discounted

cash inflows

for option 2

(in $)

0

-

1,19,95,000

-

50,95,000 1

-

1,19,95,000

-

50,95,000

1

20,00,00

0

15,00,00

0 0.92

18,36,54

7

13,77,41

0

2

40,00,00

0

30,00,00

0 0.84

33,72,90

6

25,29,67

9

3

50,00,00

0

45,00,00

0 0.77

38,71,56

3

34,84,40

7

4

80,00,00

0

65,00,00

0 0.71

56,88,24

7

46,21,70

1

4 (Interest payments) - - - -

-

28,02,250

Net Present Value (NPV) 27,74,26 41,15,94

Scenario 1: ABC Hospital

Based on the provided scenario for ascertaining the feasibility of the two options, the

measures include net present value (NPV), return on investment (ROI) and internal rate of

return (IRR). The following calculation has been made in order to select the most feasible

option available to ABC Hospital:

Years

Cash inflows

for option 1

(in $)

Cash

inflows for

option 2

(in $)

Discounting

factor@8.9

%

Discounted

cash

inflows for

option 1 (in

$)

Discounted

cash inflows

for option 2

(in $)

0

-

1,19,95,000

-

50,95,000 1

-

1,19,95,000

-

50,95,000

1

20,00,00

0

15,00,00

0 0.92

18,36,54

7

13,77,41

0

2

40,00,00

0

30,00,00

0 0.84

33,72,90

6

25,29,67

9

3

50,00,00

0

45,00,00

0 0.77

38,71,56

3

34,84,40

7

4

80,00,00

0

65,00,00

0 0.71

56,88,24

7

46,21,70

1

4 (Interest payments) - - - -

-

28,02,250

Net Present Value (NPV) 27,74,26 41,15,94

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS

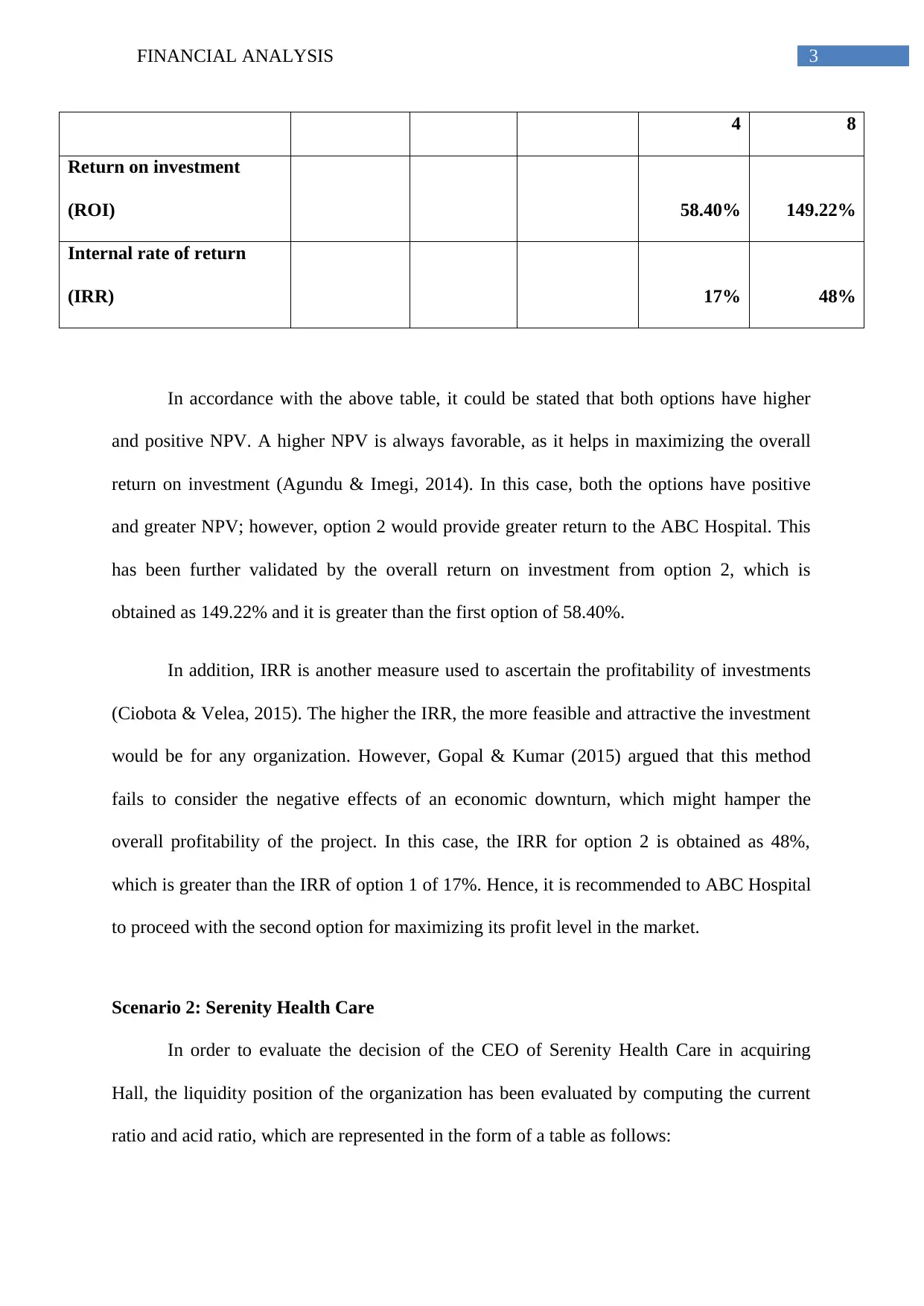

4 8

Return on investment

(ROI) 58.40% 149.22%

Internal rate of return

(IRR) 17% 48%

In accordance with the above table, it could be stated that both options have higher

and positive NPV. A higher NPV is always favorable, as it helps in maximizing the overall

return on investment (Agundu & Imegi, 2014). In this case, both the options have positive

and greater NPV; however, option 2 would provide greater return to the ABC Hospital. This

has been further validated by the overall return on investment from option 2, which is

obtained as 149.22% and it is greater than the first option of 58.40%.

In addition, IRR is another measure used to ascertain the profitability of investments

(Ciobota & Velea, 2015). The higher the IRR, the more feasible and attractive the investment

would be for any organization. However, Gopal & Kumar (2015) argued that this method

fails to consider the negative effects of an economic downturn, which might hamper the

overall profitability of the project. In this case, the IRR for option 2 is obtained as 48%,

which is greater than the IRR of option 1 of 17%. Hence, it is recommended to ABC Hospital

to proceed with the second option for maximizing its profit level in the market.

Scenario 2: Serenity Health Care

In order to evaluate the decision of the CEO of Serenity Health Care in acquiring

Hall, the liquidity position of the organization has been evaluated by computing the current

ratio and acid ratio, which are represented in the form of a table as follows:

4 8

Return on investment

(ROI) 58.40% 149.22%

Internal rate of return

(IRR) 17% 48%

In accordance with the above table, it could be stated that both options have higher

and positive NPV. A higher NPV is always favorable, as it helps in maximizing the overall

return on investment (Agundu & Imegi, 2014). In this case, both the options have positive

and greater NPV; however, option 2 would provide greater return to the ABC Hospital. This

has been further validated by the overall return on investment from option 2, which is

obtained as 149.22% and it is greater than the first option of 58.40%.

In addition, IRR is another measure used to ascertain the profitability of investments

(Ciobota & Velea, 2015). The higher the IRR, the more feasible and attractive the investment

would be for any organization. However, Gopal & Kumar (2015) argued that this method

fails to consider the negative effects of an economic downturn, which might hamper the

overall profitability of the project. In this case, the IRR for option 2 is obtained as 48%,

which is greater than the IRR of option 1 of 17%. Hence, it is recommended to ABC Hospital

to proceed with the second option for maximizing its profit level in the market.

Scenario 2: Serenity Health Care

In order to evaluate the decision of the CEO of Serenity Health Care in acquiring

Hall, the liquidity position of the organization has been evaluated by computing the current

ratio and acid ratio, which are represented in the form of a table as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ANALYSIS

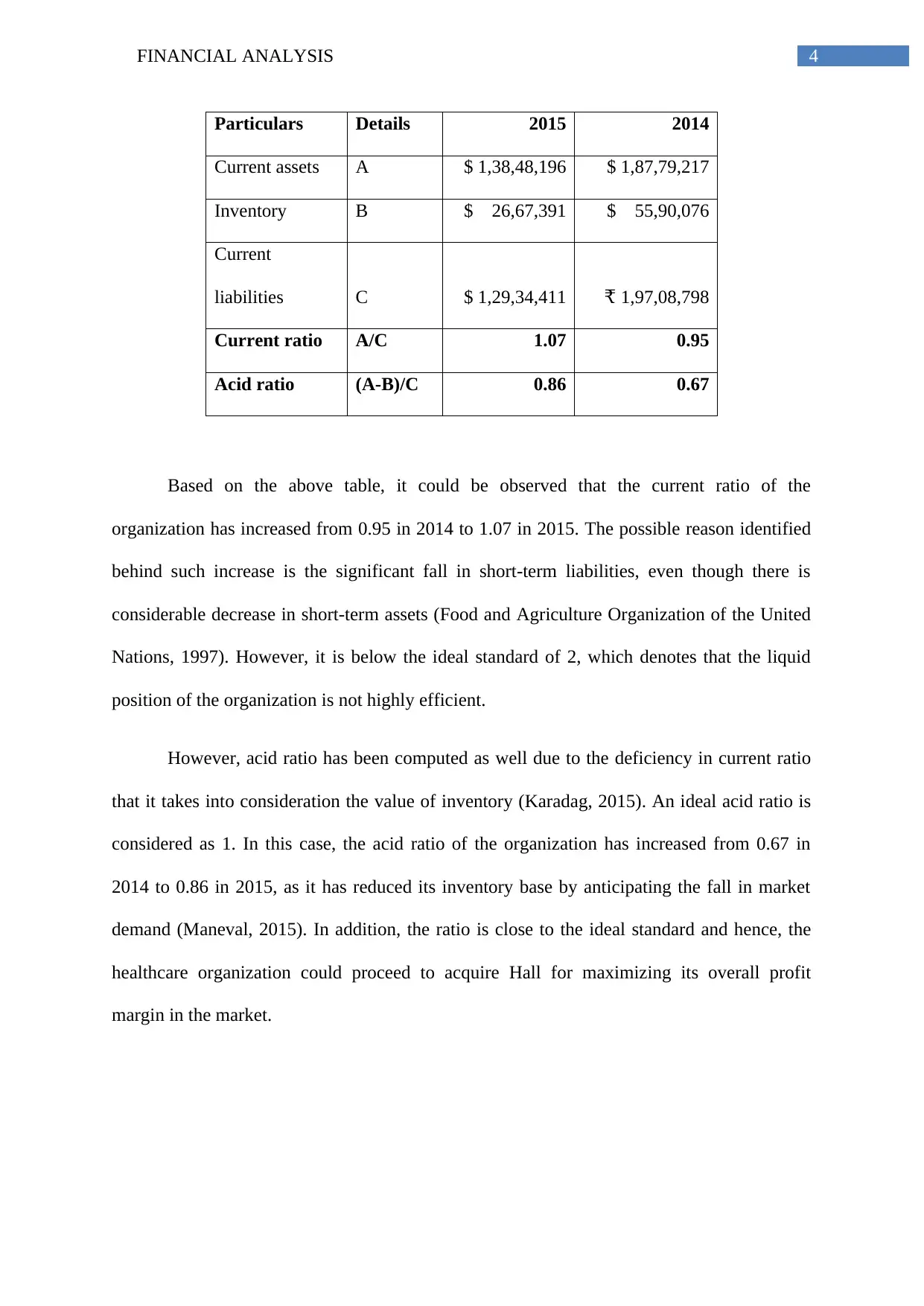

Particulars Details 2015 2014

Current assets A $ 1,38,48,196 $ 1,87,79,217

Inventory B $ 26,67,391 $ 55,90,076

Current

liabilities C $ 1,29,34,411 1,97,08,798₹

Current ratio A/C 1.07 0.95

Acid ratio (A-B)/C 0.86 0.67

Based on the above table, it could be observed that the current ratio of the

organization has increased from 0.95 in 2014 to 1.07 in 2015. The possible reason identified

behind such increase is the significant fall in short-term liabilities, even though there is

considerable decrease in short-term assets (Food and Agriculture Organization of the United

Nations, 1997). However, it is below the ideal standard of 2, which denotes that the liquid

position of the organization is not highly efficient.

However, acid ratio has been computed as well due to the deficiency in current ratio

that it takes into consideration the value of inventory (Karadag, 2015). An ideal acid ratio is

considered as 1. In this case, the acid ratio of the organization has increased from 0.67 in

2014 to 0.86 in 2015, as it has reduced its inventory base by anticipating the fall in market

demand (Maneval, 2015). In addition, the ratio is close to the ideal standard and hence, the

healthcare organization could proceed to acquire Hall for maximizing its overall profit

margin in the market.

Particulars Details 2015 2014

Current assets A $ 1,38,48,196 $ 1,87,79,217

Inventory B $ 26,67,391 $ 55,90,076

Current

liabilities C $ 1,29,34,411 1,97,08,798₹

Current ratio A/C 1.07 0.95

Acid ratio (A-B)/C 0.86 0.67

Based on the above table, it could be observed that the current ratio of the

organization has increased from 0.95 in 2014 to 1.07 in 2015. The possible reason identified

behind such increase is the significant fall in short-term liabilities, even though there is

considerable decrease in short-term assets (Food and Agriculture Organization of the United

Nations, 1997). However, it is below the ideal standard of 2, which denotes that the liquid

position of the organization is not highly efficient.

However, acid ratio has been computed as well due to the deficiency in current ratio

that it takes into consideration the value of inventory (Karadag, 2015). An ideal acid ratio is

considered as 1. In this case, the acid ratio of the organization has increased from 0.67 in

2014 to 0.86 in 2015, as it has reduced its inventory base by anticipating the fall in market

demand (Maneval, 2015). In addition, the ratio is close to the ideal standard and hence, the

healthcare organization could proceed to acquire Hall for maximizing its overall profit

margin in the market.

5FINANCIAL ANALYSIS

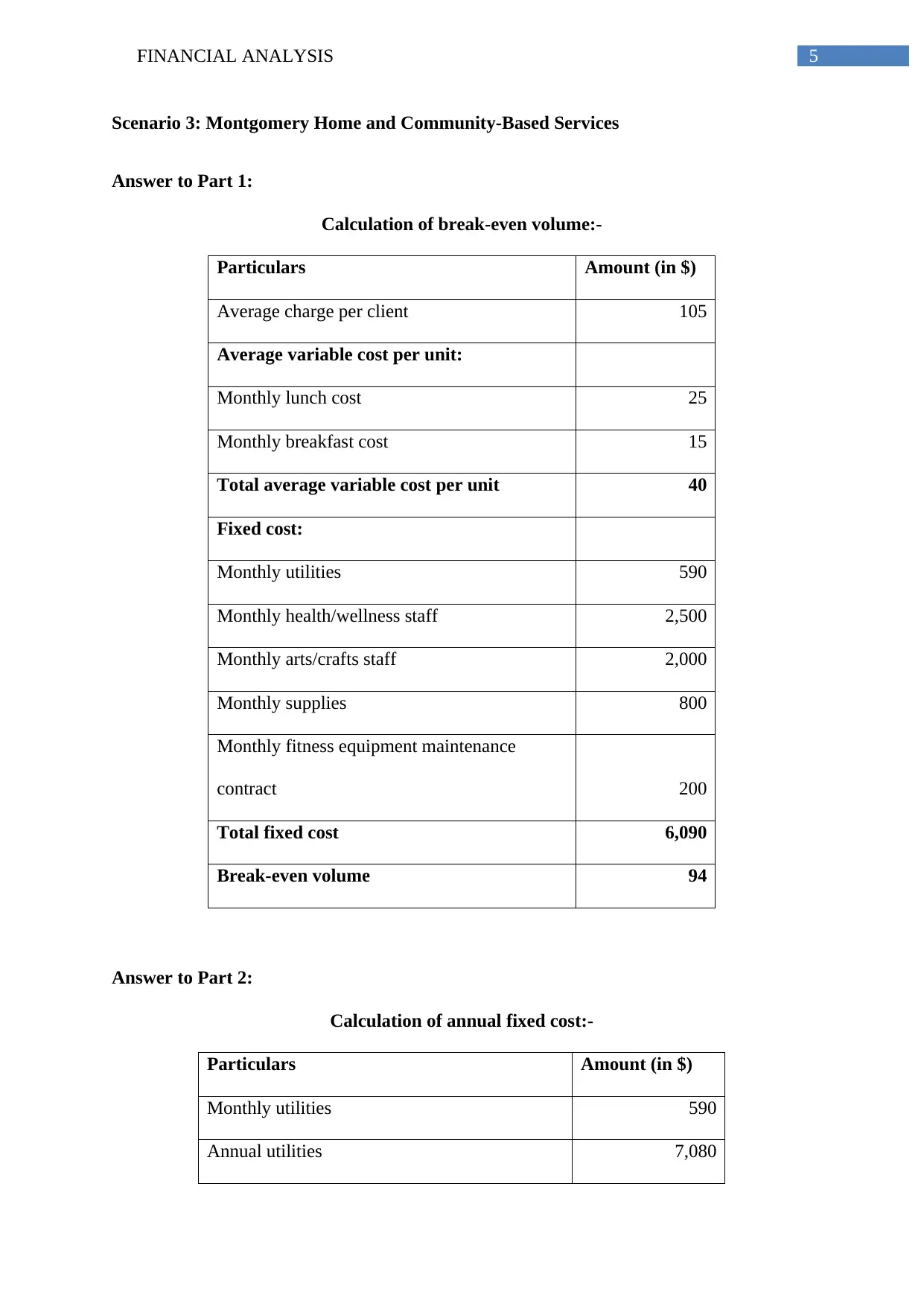

Scenario 3: Montgomery Home and Community-Based Services

Answer to Part 1:

Calculation of break-even volume:-

Particulars Amount (in $)

Average charge per client 105

Average variable cost per unit:

Monthly lunch cost 25

Monthly breakfast cost 15

Total average variable cost per unit 40

Fixed cost:

Monthly utilities 590

Monthly health/wellness staff 2,500

Monthly arts/crafts staff 2,000

Monthly supplies 800

Monthly fitness equipment maintenance

contract 200

Total fixed cost 6,090

Break-even volume 94

Answer to Part 2:

Calculation of annual fixed cost:-

Particulars Amount (in $)

Monthly utilities 590

Annual utilities 7,080

Scenario 3: Montgomery Home and Community-Based Services

Answer to Part 1:

Calculation of break-even volume:-

Particulars Amount (in $)

Average charge per client 105

Average variable cost per unit:

Monthly lunch cost 25

Monthly breakfast cost 15

Total average variable cost per unit 40

Fixed cost:

Monthly utilities 590

Monthly health/wellness staff 2,500

Monthly arts/crafts staff 2,000

Monthly supplies 800

Monthly fitness equipment maintenance

contract 200

Total fixed cost 6,090

Break-even volume 94

Answer to Part 2:

Calculation of annual fixed cost:-

Particulars Amount (in $)

Monthly utilities 590

Annual utilities 7,080

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

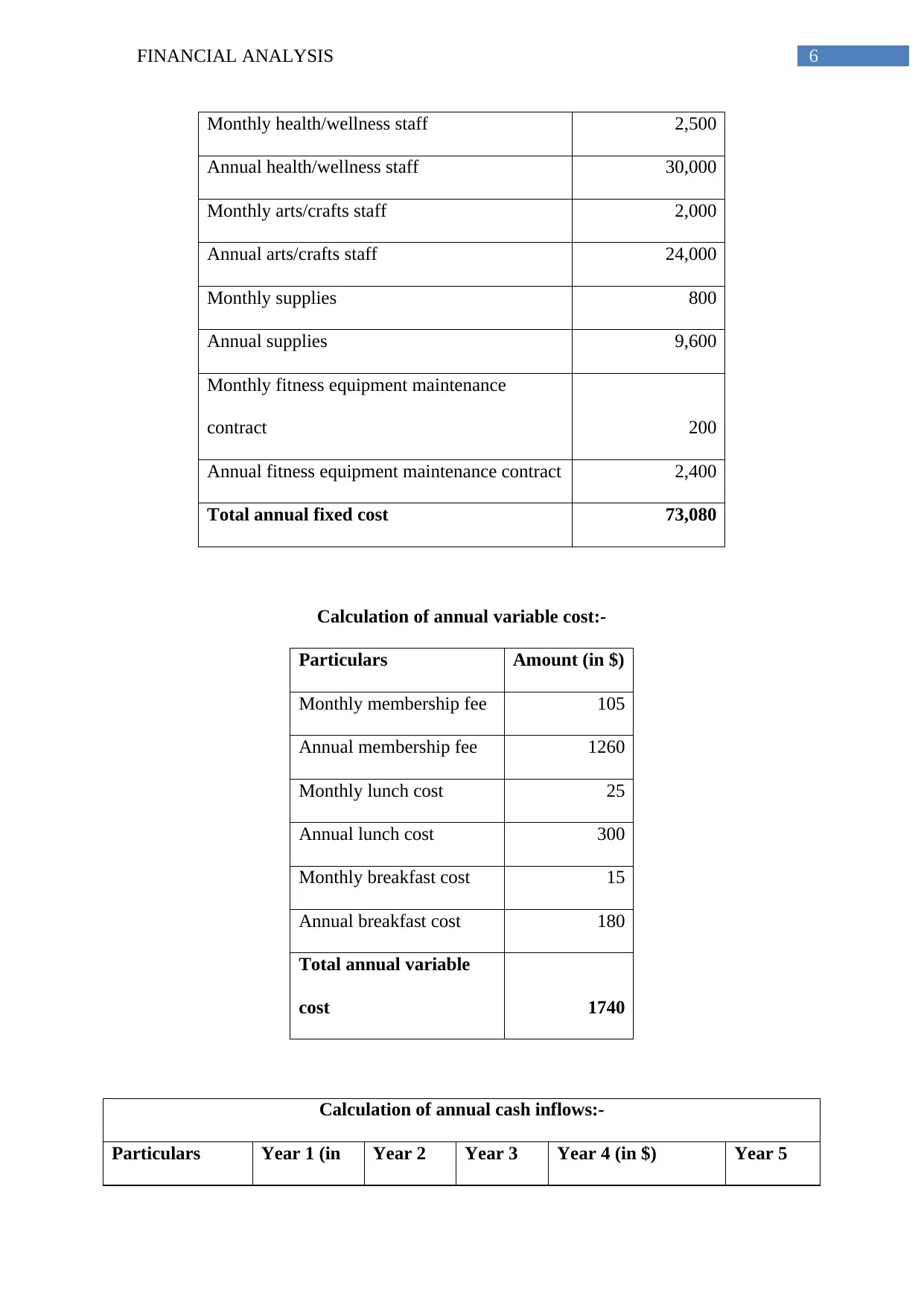

6FINANCIAL ANALYSIS

Monthly health/wellness staff 2,500

Annual health/wellness staff 30,000

Monthly arts/crafts staff 2,000

Annual arts/crafts staff 24,000

Monthly supplies 800

Annual supplies 9,600

Monthly fitness equipment maintenance

contract 200

Annual fitness equipment maintenance contract 2,400

Total annual fixed cost 73,080

Calculation of annual variable cost:-

Particulars Amount (in $)

Monthly membership fee 105

Annual membership fee 1260

Monthly lunch cost 25

Annual lunch cost 300

Monthly breakfast cost 15

Annual breakfast cost 180

Total annual variable

cost 1740

Calculation of annual cash inflows:-

Particulars Year 1 (in Year 2 Year 3 Year 4 (in $) Year 5

Monthly health/wellness staff 2,500

Annual health/wellness staff 30,000

Monthly arts/crafts staff 2,000

Annual arts/crafts staff 24,000

Monthly supplies 800

Annual supplies 9,600

Monthly fitness equipment maintenance

contract 200

Annual fitness equipment maintenance contract 2,400

Total annual fixed cost 73,080

Calculation of annual variable cost:-

Particulars Amount (in $)

Monthly membership fee 105

Annual membership fee 1260

Monthly lunch cost 25

Annual lunch cost 300

Monthly breakfast cost 15

Annual breakfast cost 180

Total annual variable

cost 1740

Calculation of annual cash inflows:-

Particulars Year 1 (in Year 2 Year 3 Year 4 (in $) Year 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS

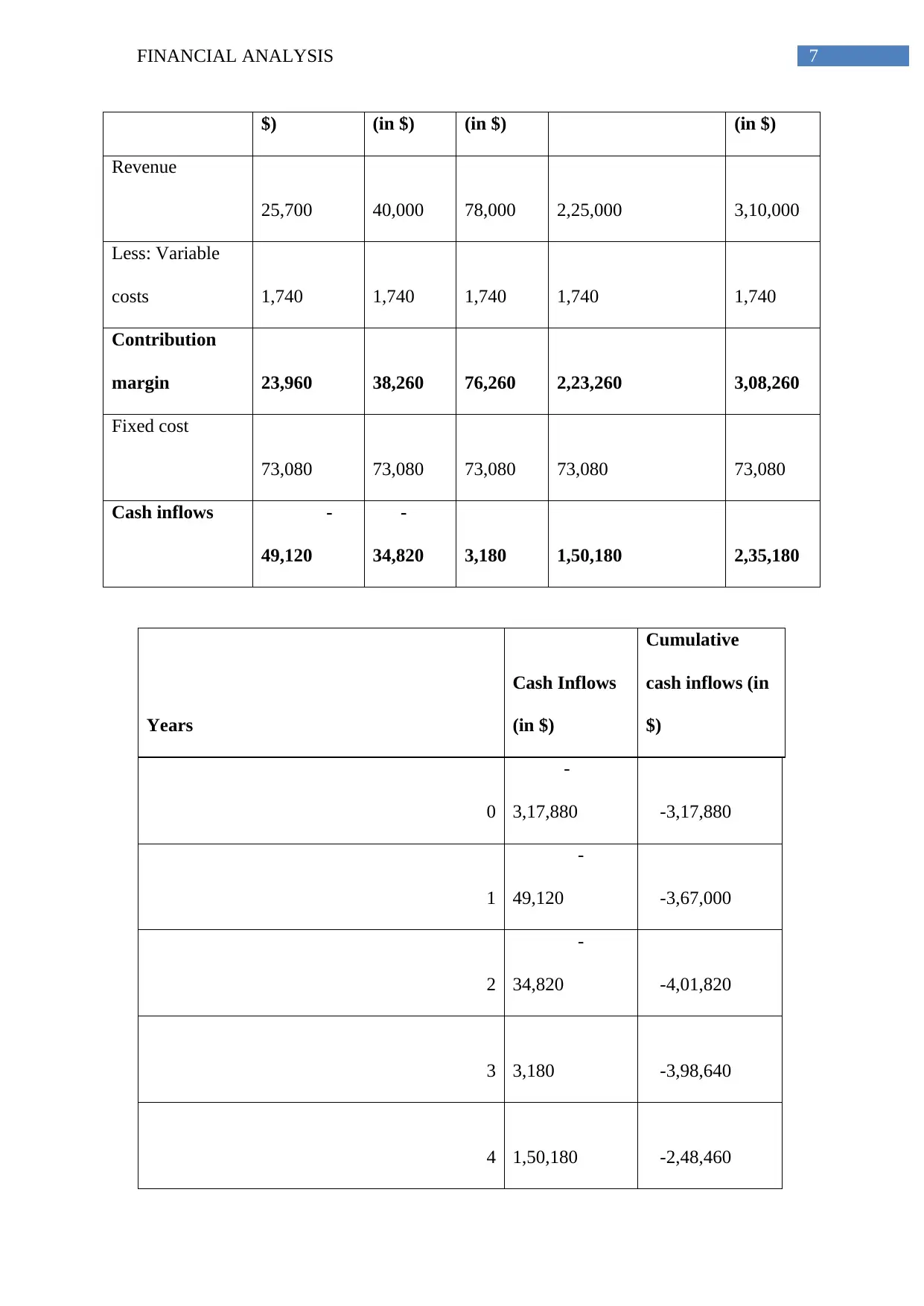

$) (in $) (in $) (in $)

Revenue

25,700 40,000 78,000 2,25,000 3,10,000

Less: Variable

costs 1,740 1,740 1,740 1,740 1,740

Contribution

margin 23,960 38,260 76,260 2,23,260 3,08,260

Fixed cost

73,080 73,080 73,080 73,080 73,080

Cash inflows -

49,120

-

34,820 3,180 1,50,180 2,35,180

Years

Cash Inflows

(in $)

Cumulative

cash inflows (in

$)

0

-

3,17,880 -3,17,880

1

-

49,120 -3,67,000

2

-

34,820 -4,01,820

3 3,180 -3,98,640

4 1,50,180 -2,48,460

$) (in $) (in $) (in $)

Revenue

25,700 40,000 78,000 2,25,000 3,10,000

Less: Variable

costs 1,740 1,740 1,740 1,740 1,740

Contribution

margin 23,960 38,260 76,260 2,23,260 3,08,260

Fixed cost

73,080 73,080 73,080 73,080 73,080

Cash inflows -

49,120

-

34,820 3,180 1,50,180 2,35,180

Years

Cash Inflows

(in $)

Cumulative

cash inflows (in

$)

0

-

3,17,880 -3,17,880

1

-

49,120 -3,67,000

2

-

34,820 -4,01,820

3 3,180 -3,98,640

4 1,50,180 -2,48,460

8FINANCIAL ANALYSIS

5 2,35,180 -13,280

5 2,35,180 -13,280

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS

According to the above table, it is clearly evident that the cumulative cash inflow is

negative even after the end of the fifth year. Therefore, payback period could not be applied

in this case.

According to the above table, it is clearly evident that the cumulative cash inflow is

negative even after the end of the fifth year. Therefore, payback period could not be applied

in this case.

1 out of 10