Financial Analysis of British Telecommunications

VerifiedAdded on 2023/06/18

|20

|4147

|94

AI Summary

This report provides a detailed financial analysis of British Telecommunications, including recent developments, dividend policy, sources of finance, and ratio analysis. The report analyzes the impact of Covid-19 and the Italian Accounts Scandal on the company's financial performance. It also discusses the company's dividend policy and sources of finance, along with a ratio analysis of profitability, liquidity, and solvency ratios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

An individual report

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction......................................................................................................................................3

Section-A.........................................................................................................................................3

Development 1: Covid-19......................................................................................................3

Development 2: Italian Accounts Scandal.............................................................................4

Section – B.......................................................................................................................................5

Dividend Policy......................................................................................................................5

Sources of Finances................................................................................................................6

Section – C.......................................................................................................................................9

Ratio Analysis........................................................................................................................9

Conclusion.....................................................................................................................................13

References......................................................................................................................................13

Books & Journals.................................................................................................................13

Appendix........................................................................................................................................15

Introduction......................................................................................................................................3

Section-A.........................................................................................................................................3

Development 1: Covid-19......................................................................................................3

Development 2: Italian Accounts Scandal.............................................................................4

Section – B.......................................................................................................................................5

Dividend Policy......................................................................................................................5

Sources of Finances................................................................................................................6

Section – C.......................................................................................................................................9

Ratio Analysis........................................................................................................................9

Conclusion.....................................................................................................................................13

References......................................................................................................................................13

Books & Journals.................................................................................................................13

Appendix........................................................................................................................................15

Introduction

In order to conduct the present study British Telecommunication is taken into consideration.

British Telecommunications plc is a global broadcast communications organization. As one

of the world's driving correspondences specialist service providers, BT takes into account

clients in 180 nations. BT is additionally the United Kingdom's greatest fixed-voice and

broadband supplier, and offers TV and versatile administrations. BT comprises of four

principle business lines: Consumer, Enterprise, Global Services, and Openreach. The

respective company has made the profit amounting to 1.47 billion British pounds in the

financial year of 2020-21. Also, it has been constantly performing well with high level of

efficiency. For the purpose of study, the analysis of the financial performance British

Telecommunications are traced out. Also, the different risks and their management which

are related to the sources of finance and dividend policy has been critically assessed.

Section-A

Critically analyse any two recent developments in context to the financial environment which

has impacted on the performance and development of the company in the future aspect.

Development is a cycle that makes development, progress, positive change or the

expansion of physical, financial, ecological, social and segment parts (Mather, 2019). The

motivation behind improvement is an ascent in the level and personal satisfaction of the

populace, and the creation or extension of nearby territorial pay and business openings,

without harming the assets of the climate.

Development 1: Covid-19

The COVID-19 pandemic maybe more than some other occasion in mankind's set of

experiences has exhibited the basic significance that broadcast communications

framework plays in keeping organizations, legislatures, and social orders associated and

running. In view of the financial and social interruption brought about by the pandemic,

individuals across the globe depend on innovation for data, for social separating, and

telecommuting. British Telecommunication has been performing well as compared to

other business sectors. Although the profits have fell down to 666 million British pound

in the second half of the financial year of 2019-20 and it went up in the financial year to

856 million British pound in the first half of 2020-21.

In order to conduct the present study British Telecommunication is taken into consideration.

British Telecommunications plc is a global broadcast communications organization. As one

of the world's driving correspondences specialist service providers, BT takes into account

clients in 180 nations. BT is additionally the United Kingdom's greatest fixed-voice and

broadband supplier, and offers TV and versatile administrations. BT comprises of four

principle business lines: Consumer, Enterprise, Global Services, and Openreach. The

respective company has made the profit amounting to 1.47 billion British pounds in the

financial year of 2020-21. Also, it has been constantly performing well with high level of

efficiency. For the purpose of study, the analysis of the financial performance British

Telecommunications are traced out. Also, the different risks and their management which

are related to the sources of finance and dividend policy has been critically assessed.

Section-A

Critically analyse any two recent developments in context to the financial environment which

has impacted on the performance and development of the company in the future aspect.

Development is a cycle that makes development, progress, positive change or the

expansion of physical, financial, ecological, social and segment parts (Mather, 2019). The

motivation behind improvement is an ascent in the level and personal satisfaction of the

populace, and the creation or extension of nearby territorial pay and business openings,

without harming the assets of the climate.

Development 1: Covid-19

The COVID-19 pandemic maybe more than some other occasion in mankind's set of

experiences has exhibited the basic significance that broadcast communications

framework plays in keeping organizations, legislatures, and social orders associated and

running. In view of the financial and social interruption brought about by the pandemic,

individuals across the globe depend on innovation for data, for social separating, and

telecommuting. British Telecommunication has been performing well as compared to

other business sectors. Although the profits have fell down to 666 million British pound

in the second half of the financial year of 2019-20 and it went up in the financial year to

856 million British pound in the first half of 2020-21.

Impacts on the financial performance of British Telecommunication because of the global

pandemic Covid-19.

Impact Details

Business consequences In the buyer business, incomes of British

Telecommunication declined by 7% as

compared to previous year, while the venture

unit saw a downfall of 9% which reduced the

efficiency as well as the consistency of the

company.

Impact on sales Reported income fell by 2% and adjusted

income fell by 3%. This was basically because

of the effect of guideline, decreases in heritage

items, key decreases of low edge business and

divestments.

Disruption in supply Also, the disruptions in the short term supply

of network equipment became a big hurdle for

the company to accelerate the business

operations on a serious note. The major impact

of this shortage in the supply has resulted into

the suspension of the new construction

projects.

Strategy implementation in order to mitigate the impact of the Covid-19.

British telecommunication immediately reduced its workforce considerably and shifted

from the office premises to work from home so that it can abide by the policies of the

government to tackle the situation of covid 19 (Moreale and Zaynutdinova, 2018). Also, the

respective company has tried to improvise the financial position of the company by reducing

the operating costs in the phase of the global pandemic situation. This helped the company to

lower down the product cost.

pandemic Covid-19.

Impact Details

Business consequences In the buyer business, incomes of British

Telecommunication declined by 7% as

compared to previous year, while the venture

unit saw a downfall of 9% which reduced the

efficiency as well as the consistency of the

company.

Impact on sales Reported income fell by 2% and adjusted

income fell by 3%. This was basically because

of the effect of guideline, decreases in heritage

items, key decreases of low edge business and

divestments.

Disruption in supply Also, the disruptions in the short term supply

of network equipment became a big hurdle for

the company to accelerate the business

operations on a serious note. The major impact

of this shortage in the supply has resulted into

the suspension of the new construction

projects.

Strategy implementation in order to mitigate the impact of the Covid-19.

British telecommunication immediately reduced its workforce considerably and shifted

from the office premises to work from home so that it can abide by the policies of the

government to tackle the situation of covid 19 (Moreale and Zaynutdinova, 2018). Also, the

respective company has tried to improvise the financial position of the company by reducing

the operating costs in the phase of the global pandemic situation. This helped the company to

lower down the product cost.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

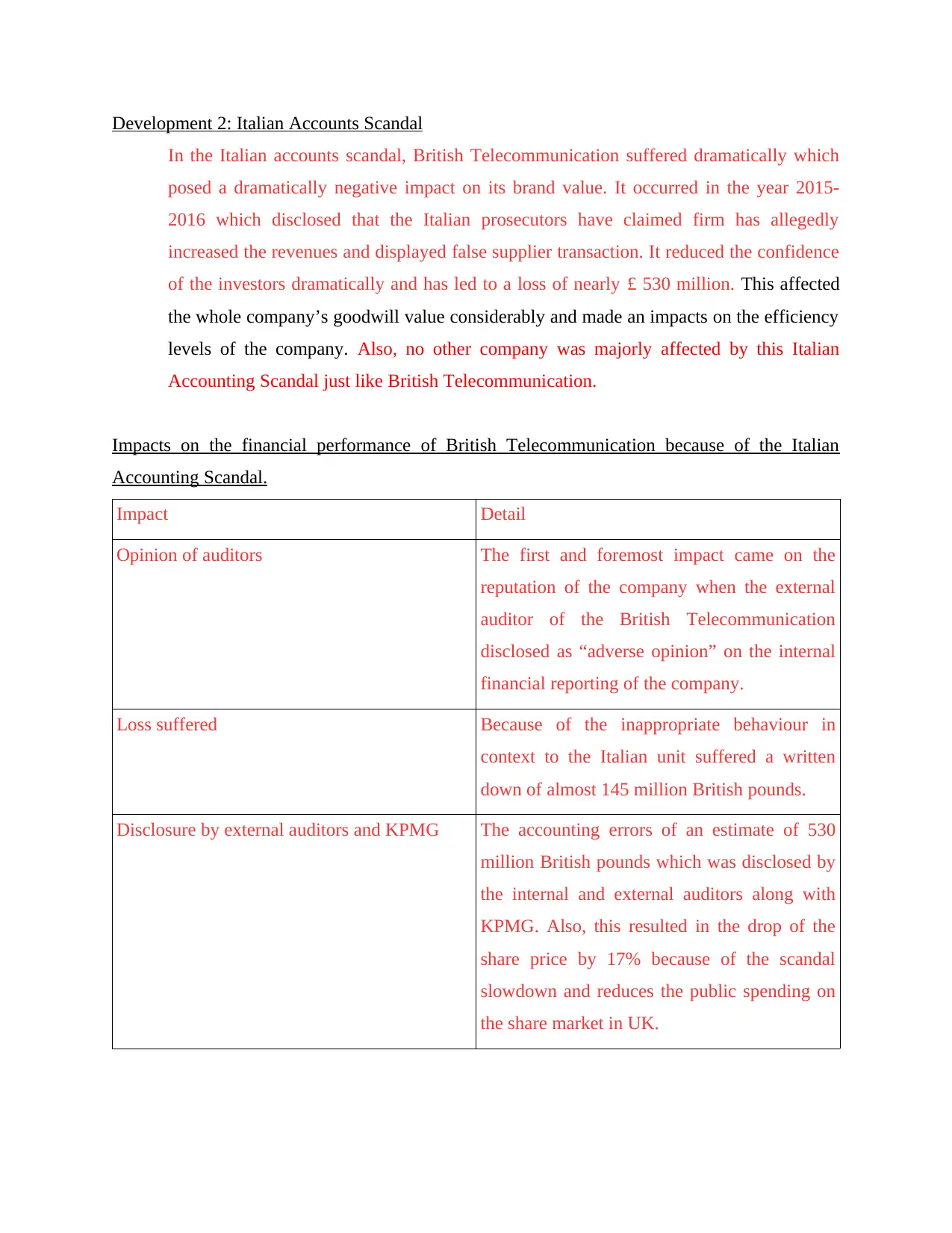

Development 2: Italian Accounts Scandal

In the Italian accounts scandal, British Telecommunication suffered dramatically which

posed a dramatically negative impact on its brand value. It occurred in the year 2015-

2016 which disclosed that the Italian prosecutors have claimed firm has allegedly

increased the revenues and displayed false supplier transaction. It reduced the confidence

of the investors dramatically and has led to a loss of nearly £ 530 million. This affected

the whole company’s goodwill value considerably and made an impacts on the efficiency

levels of the company. Also, no other company was majorly affected by this Italian

Accounting Scandal just like British Telecommunication.

Impacts on the financial performance of British Telecommunication because of the Italian

Accounting Scandal.

Impact Detail

Opinion of auditors The first and foremost impact came on the

reputation of the company when the external

auditor of the British Telecommunication

disclosed as “adverse opinion” on the internal

financial reporting of the company.

Loss suffered Because of the inappropriate behaviour in

context to the Italian unit suffered a written

down of almost 145 million British pounds.

Disclosure by external auditors and KPMG The accounting errors of an estimate of 530

million British pounds which was disclosed by

the internal and external auditors along with

KPMG. Also, this resulted in the drop of the

share price by 17% because of the scandal

slowdown and reduces the public spending on

the share market in UK.

In the Italian accounts scandal, British Telecommunication suffered dramatically which

posed a dramatically negative impact on its brand value. It occurred in the year 2015-

2016 which disclosed that the Italian prosecutors have claimed firm has allegedly

increased the revenues and displayed false supplier transaction. It reduced the confidence

of the investors dramatically and has led to a loss of nearly £ 530 million. This affected

the whole company’s goodwill value considerably and made an impacts on the efficiency

levels of the company. Also, no other company was majorly affected by this Italian

Accounting Scandal just like British Telecommunication.

Impacts on the financial performance of British Telecommunication because of the Italian

Accounting Scandal.

Impact Detail

Opinion of auditors The first and foremost impact came on the

reputation of the company when the external

auditor of the British Telecommunication

disclosed as “adverse opinion” on the internal

financial reporting of the company.

Loss suffered Because of the inappropriate behaviour in

context to the Italian unit suffered a written

down of almost 145 million British pounds.

Disclosure by external auditors and KPMG The accounting errors of an estimate of 530

million British pounds which was disclosed by

the internal and external auditors along with

KPMG. Also, this resulted in the drop of the

share price by 17% because of the scandal

slowdown and reduces the public spending on

the share market in UK.

Strategy implementation in order to mitigate the impact of the Italian accounting scandal.

The company British Telecommunication made it sure that the enforcement of the

laws and policies must be done in such a way that there is no chance of any loophole

which may pop in. Because it was the first, foremost and only way to mitigate the

risk of such kind of scandals (Chris Kraft and PMP, 2018). Also, this type of strict

implementation of rules helped in building a culture of transparency in the

organization.

In addition to this, with its effective and efficient public relation skills, BT tried to

rebuild its brand value in the market place so that it cam regain its lost goodwill and

reputation. The company prioritize building public relations.

Section – B

Dividend Policy

A Dividend policy can be defined as a profit strategy indulged in an arrangement of how

organization uses to structure its profit pay-out to investors.

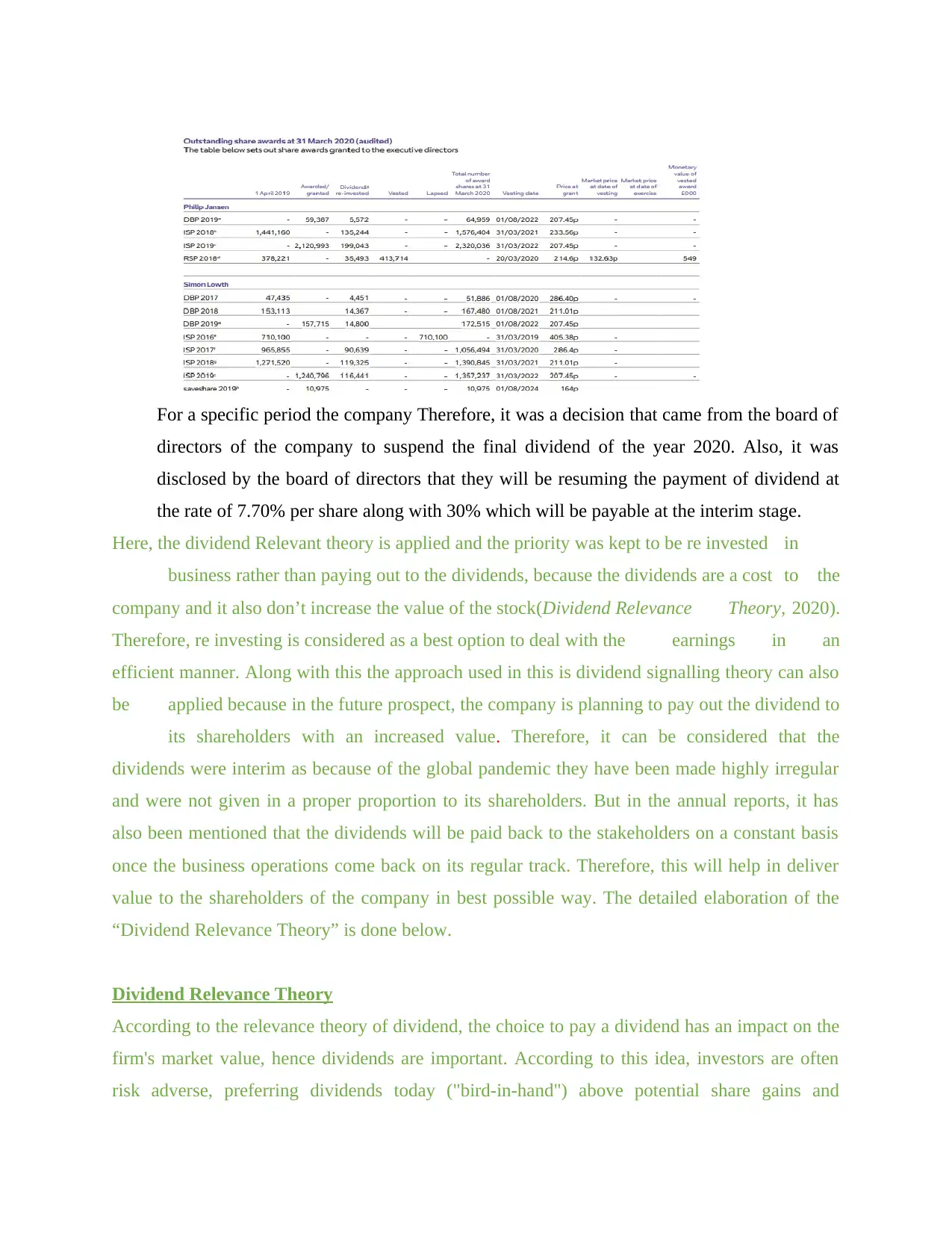

In May 2020, having considered the different dividend interests, specifically the drawn out

interests of the investors, the Board closed the judicious choice was to suspend the last

profit for 2019/20 and all profits for 2020/21 in the form of dividends, and to re-base future

profits to a more maintainable level . This choice will make limit with regards to BT to put

resources into long haul, esteem upgrading openings, including the essential aim for a

change and modernisation program, combined with the more limited term effect of Covid-

19. The Board hopes to proceed with a dynamic profit strategy from this re-based level for

future years. It can be seen from the image below that the dividends paid to the investors

were reduced and the amount of dividends were re invested in the business in order to get

back on track.

The company British Telecommunication made it sure that the enforcement of the

laws and policies must be done in such a way that there is no chance of any loophole

which may pop in. Because it was the first, foremost and only way to mitigate the

risk of such kind of scandals (Chris Kraft and PMP, 2018). Also, this type of strict

implementation of rules helped in building a culture of transparency in the

organization.

In addition to this, with its effective and efficient public relation skills, BT tried to

rebuild its brand value in the market place so that it cam regain its lost goodwill and

reputation. The company prioritize building public relations.

Section – B

Dividend Policy

A Dividend policy can be defined as a profit strategy indulged in an arrangement of how

organization uses to structure its profit pay-out to investors.

In May 2020, having considered the different dividend interests, specifically the drawn out

interests of the investors, the Board closed the judicious choice was to suspend the last

profit for 2019/20 and all profits for 2020/21 in the form of dividends, and to re-base future

profits to a more maintainable level . This choice will make limit with regards to BT to put

resources into long haul, esteem upgrading openings, including the essential aim for a

change and modernisation program, combined with the more limited term effect of Covid-

19. The Board hopes to proceed with a dynamic profit strategy from this re-based level for

future years. It can be seen from the image below that the dividends paid to the investors

were reduced and the amount of dividends were re invested in the business in order to get

back on track.

For a specific period the company Therefore, it was a decision that came from the board of

directors of the company to suspend the final dividend of the year 2020. Also, it was

disclosed by the board of directors that they will be resuming the payment of dividend at

the rate of 7.70% per share along with 30% which will be payable at the interim stage.

Here, the dividend Relevant theory is applied and the priority was kept to be re invested in

business rather than paying out to the dividends, because the dividends are a cost to the

company and it also don’t increase the value of the stock(Dividend Relevance Theory, 2020).

Therefore, re investing is considered as a best option to deal with the earnings in an

efficient manner. Along with this the approach used in this is dividend signalling theory can also

be applied because in the future prospect, the company is planning to pay out the dividend to

its shareholders with an increased value. Therefore, it can be considered that the

dividends were interim as because of the global pandemic they have been made highly irregular

and were not given in a proper proportion to its shareholders. But in the annual reports, it has

also been mentioned that the dividends will be paid back to the stakeholders on a constant basis

once the business operations come back on its regular track. Therefore, this will help in deliver

value to the shareholders of the company in best possible way. The detailed elaboration of the

“Dividend Relevance Theory” is done below.

Dividend Relevance Theory

According to the relevance theory of dividend, the choice to pay a dividend has an impact on the

firm's market value, hence dividends are important. According to this idea, investors are often

risk adverse, preferring dividends today ("bird-in-hand") above potential share gains and

directors of the company to suspend the final dividend of the year 2020. Also, it was

disclosed by the board of directors that they will be resuming the payment of dividend at

the rate of 7.70% per share along with 30% which will be payable at the interim stage.

Here, the dividend Relevant theory is applied and the priority was kept to be re invested in

business rather than paying out to the dividends, because the dividends are a cost to the

company and it also don’t increase the value of the stock(Dividend Relevance Theory, 2020).

Therefore, re investing is considered as a best option to deal with the earnings in an

efficient manner. Along with this the approach used in this is dividend signalling theory can also

be applied because in the future prospect, the company is planning to pay out the dividend to

its shareholders with an increased value. Therefore, it can be considered that the

dividends were interim as because of the global pandemic they have been made highly irregular

and were not given in a proper proportion to its shareholders. But in the annual reports, it has

also been mentioned that the dividends will be paid back to the stakeholders on a constant basis

once the business operations come back on its regular track. Therefore, this will help in deliver

value to the shareholders of the company in best possible way. The detailed elaboration of the

“Dividend Relevance Theory” is done below.

Dividend Relevance Theory

According to the relevance theory of dividend, the choice to pay a dividend has an impact on the

firm's market value, hence dividends are important. According to this idea, investors are often

risk adverse, preferring dividends today ("bird-in-hand") above potential share gains and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

dividends tomorrow. According to the relevance theory of dividends, dividend policy has an

impact on share price.

The approach which is used in the Relevance Theory is the Dividend Signalling. This is a theory

that claims that a company's announcement of increased dividend payments sends strong signals

about the company's excellent future prospects. In practise, changes in a company's dividend

policy can be shown to affect its stock price, with an increase in dividends leading to an increase

in stock price and a drop in pay outs leading to a decrease in stock price. Many observers came

to the conclusion that, contrary to M&M's plan, shareholders prefer dividends to future capital

gains. The change in dividend pay out should be perceived by shareholders and investors as a

signal about the company's future earnings potential. A growth in dividend payment is often

regarded as a positive signal, as it conveys favourable information about a company's future

profits prospects, leading in a rise in share price. A reduction in dividend payment, on the other

hand, is perceived negatively. As a result, according to this idea, the best dividend policy should

be chosen in order to maximise shareholder wealth.

Sources of Finances

It can be defined as the provision that are made to fulfil the financial requirements for the

company mainly to cover short term requirement of working capital and long term requirement

for fixed assets as well as the investments (van Bergen, M., and et. al., 2019). Sources of finance

helps in making its sure that there are enough finances in order to operate the business operations

and for investment purpose. Also, for securing the long term investment with sources of finance.

Sources of finance for British Telecommunications

Just like other large business organization, BT also funds its operations with the help of

equity and debts as its key sources of funds. Also, it utilizes the funds that are generated from the

trading activities of the business.

The total of the shareholder’s equity is at £m 10,167 for the year 2019 and £m 14,763 for

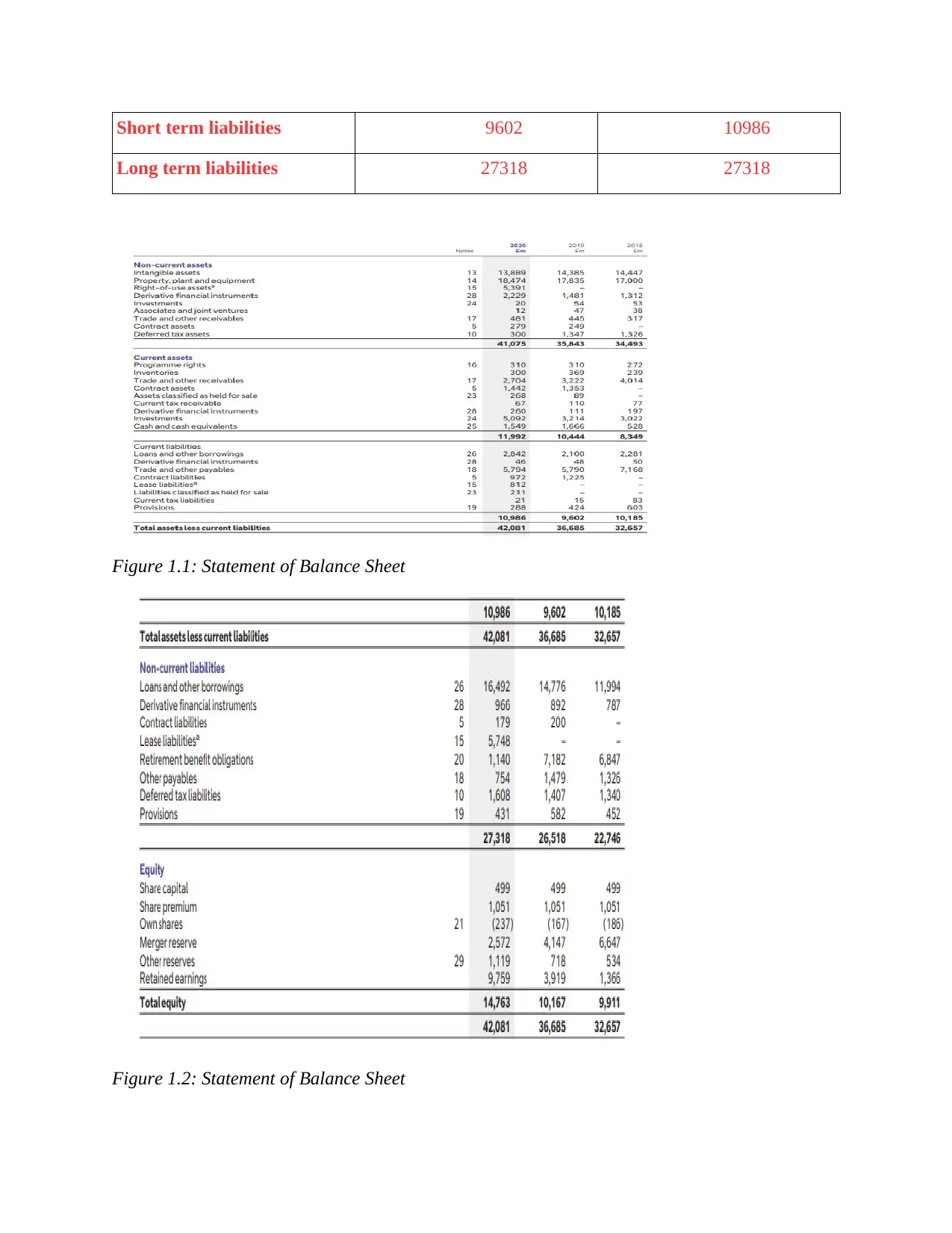

the year 2020. In context to debt, BT is having short term as well as long term liabilities.

Particulars 2019 (£m) 2020 (£m)

impact on share price.

The approach which is used in the Relevance Theory is the Dividend Signalling. This is a theory

that claims that a company's announcement of increased dividend payments sends strong signals

about the company's excellent future prospects. In practise, changes in a company's dividend

policy can be shown to affect its stock price, with an increase in dividends leading to an increase

in stock price and a drop in pay outs leading to a decrease in stock price. Many observers came

to the conclusion that, contrary to M&M's plan, shareholders prefer dividends to future capital

gains. The change in dividend pay out should be perceived by shareholders and investors as a

signal about the company's future earnings potential. A growth in dividend payment is often

regarded as a positive signal, as it conveys favourable information about a company's future

profits prospects, leading in a rise in share price. A reduction in dividend payment, on the other

hand, is perceived negatively. As a result, according to this idea, the best dividend policy should

be chosen in order to maximise shareholder wealth.

Sources of Finances

It can be defined as the provision that are made to fulfil the financial requirements for the

company mainly to cover short term requirement of working capital and long term requirement

for fixed assets as well as the investments (van Bergen, M., and et. al., 2019). Sources of finance

helps in making its sure that there are enough finances in order to operate the business operations

and for investment purpose. Also, for securing the long term investment with sources of finance.

Sources of finance for British Telecommunications

Just like other large business organization, BT also funds its operations with the help of

equity and debts as its key sources of funds. Also, it utilizes the funds that are generated from the

trading activities of the business.

The total of the shareholder’s equity is at £m 10,167 for the year 2019 and £m 14,763 for

the year 2020. In context to debt, BT is having short term as well as long term liabilities.

Particulars 2019 (£m) 2020 (£m)

Short term liabilities 9602 10986

Long term liabilities 27318 27318

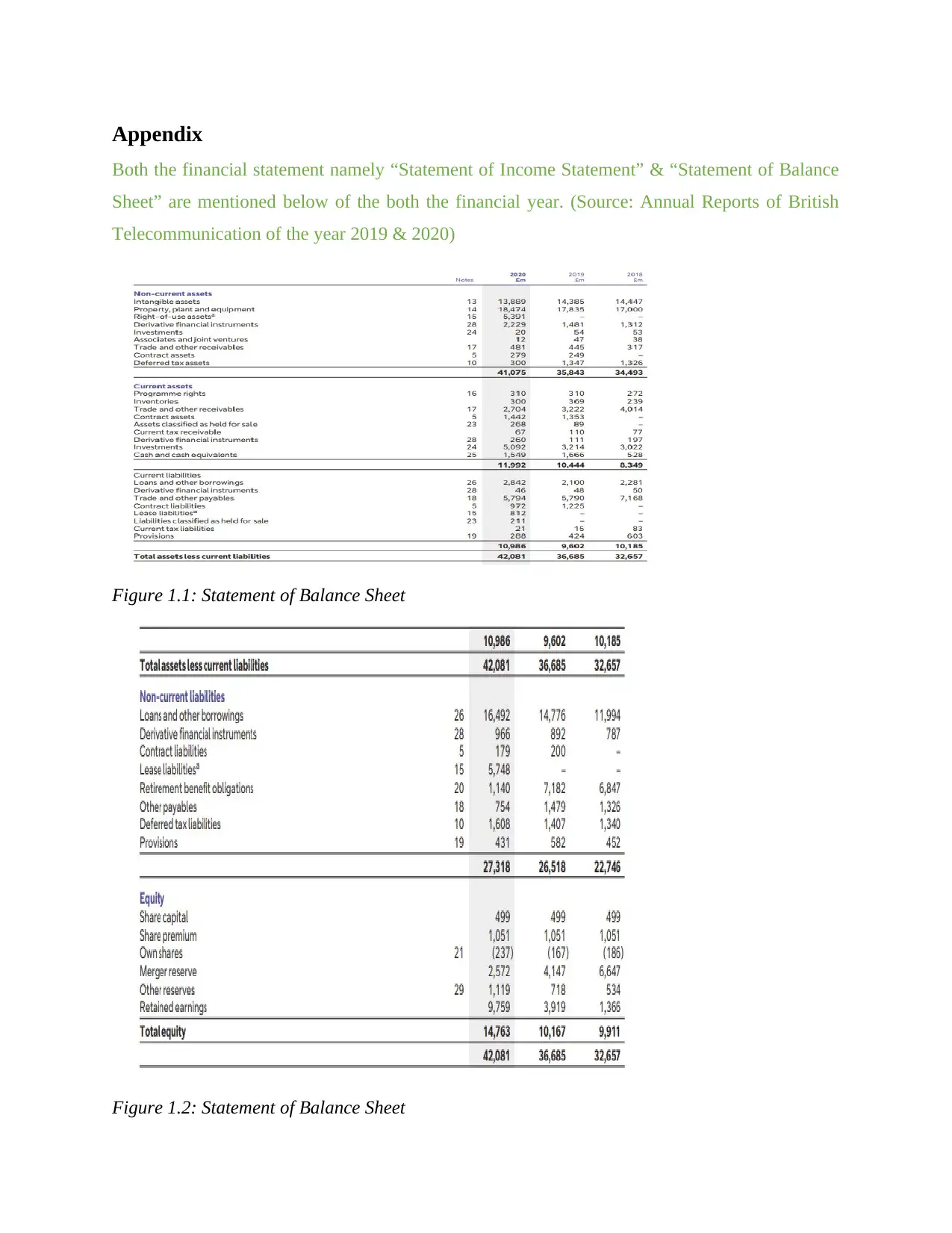

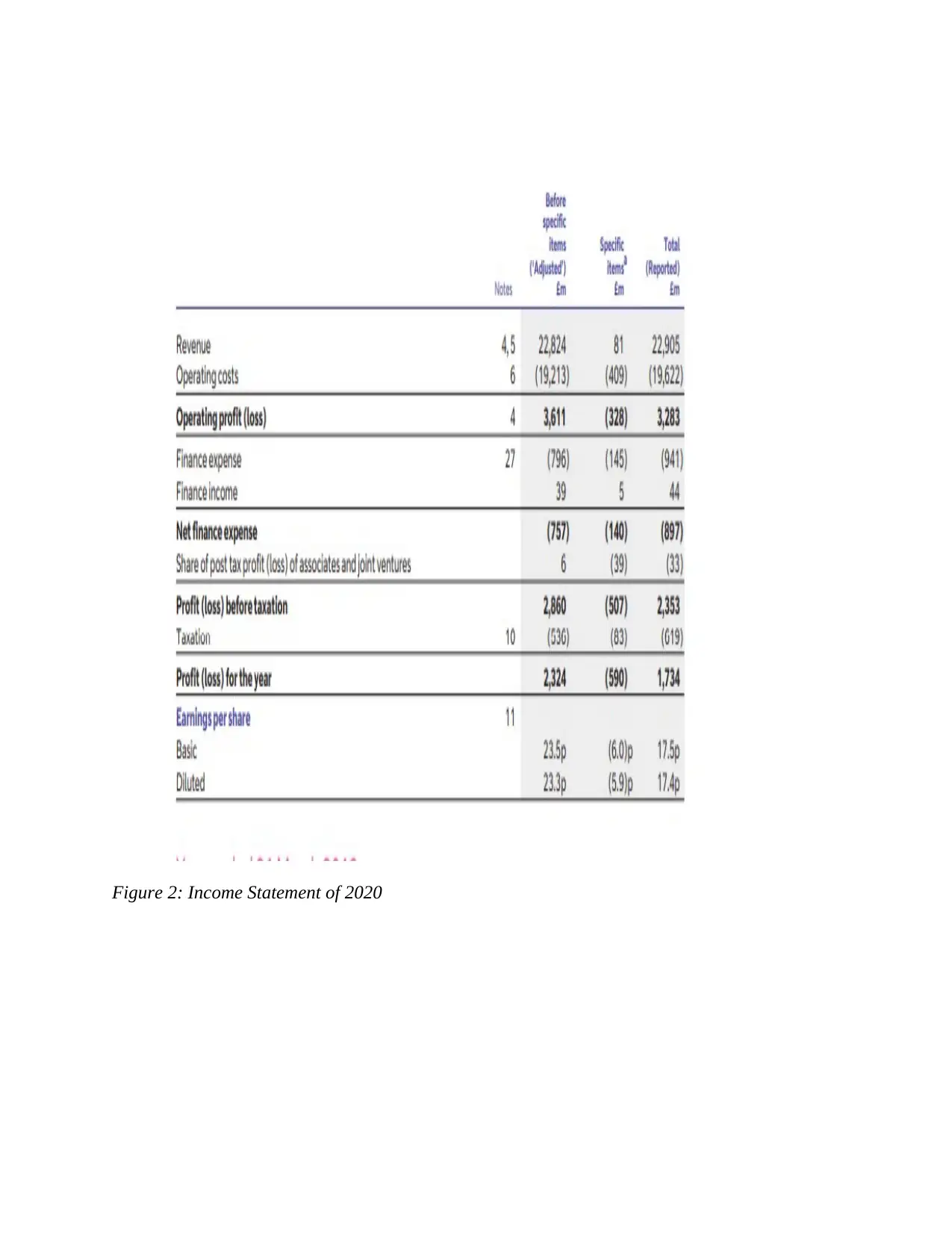

Figure 1.1: Statement of Balance Sheet

Figure 1.2: Statement of Balance Sheet

Long term liabilities 27318 27318

Figure 1.1: Statement of Balance Sheet

Figure 1.2: Statement of Balance Sheet

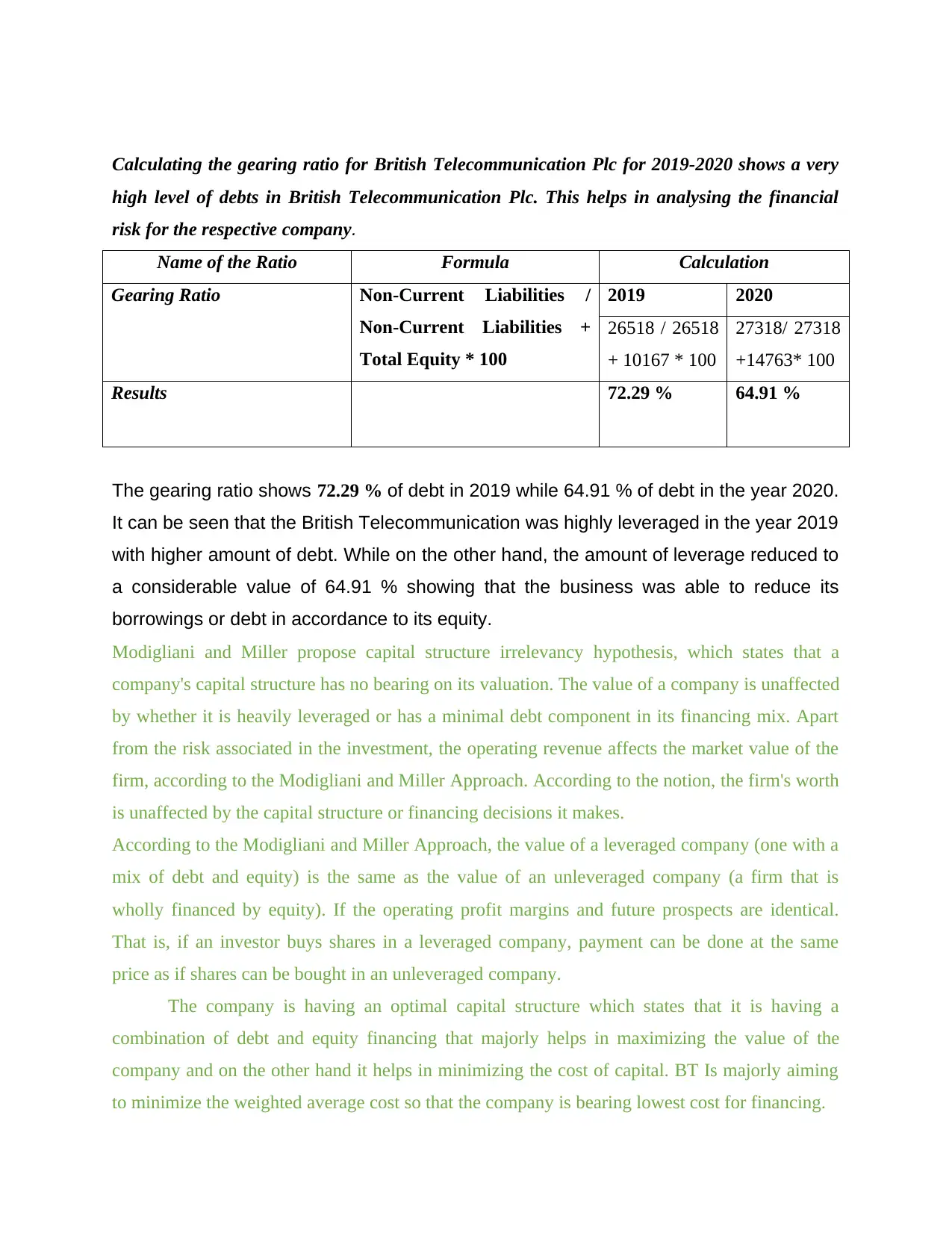

Calculating the gearing ratio for British Telecommunication Plc for 2019-2020 shows a very

high level of debts in British Telecommunication Plc. This helps in analysing the financial

risk for the respective company.

Name of the Ratio Formula Calculation

Gearing Ratio Non-Current Liabilities /

Non-Current Liabilities +

Total Equity * 100

2019 2020

26518 / 26518

+ 10167 * 100

27318/ 27318

+14763* 100

Results 72.29 % 64.91 %

The gearing ratio shows 72.29 % of debt in 2019 while 64.91 % of debt in the year 2020.

It can be seen that the British Telecommunication was highly leveraged in the year 2019

with higher amount of debt. While on the other hand, the amount of leverage reduced to

a considerable value of 64.91 % showing that the business was able to reduce its

borrowings or debt in accordance to its equity.

Modigliani and Miller propose capital structure irrelevancy hypothesis, which states that a

company's capital structure has no bearing on its valuation. The value of a company is unaffected

by whether it is heavily leveraged or has a minimal debt component in its financing mix. Apart

from the risk associated in the investment, the operating revenue affects the market value of the

firm, according to the Modigliani and Miller Approach. According to the notion, the firm's worth

is unaffected by the capital structure or financing decisions it makes.

According to the Modigliani and Miller Approach, the value of a leveraged company (one with a

mix of debt and equity) is the same as the value of an unleveraged company (a firm that is

wholly financed by equity). If the operating profit margins and future prospects are identical.

That is, if an investor buys shares in a leveraged company, payment can be done at the same

price as if shares can be bought in an unleveraged company.

The company is having an optimal capital structure which states that it is having a

combination of debt and equity financing that majorly helps in maximizing the value of the

company and on the other hand it helps in minimizing the cost of capital. BT Is majorly aiming

to minimize the weighted average cost so that the company is bearing lowest cost for financing.

high level of debts in British Telecommunication Plc. This helps in analysing the financial

risk for the respective company.

Name of the Ratio Formula Calculation

Gearing Ratio Non-Current Liabilities /

Non-Current Liabilities +

Total Equity * 100

2019 2020

26518 / 26518

+ 10167 * 100

27318/ 27318

+14763* 100

Results 72.29 % 64.91 %

The gearing ratio shows 72.29 % of debt in 2019 while 64.91 % of debt in the year 2020.

It can be seen that the British Telecommunication was highly leveraged in the year 2019

with higher amount of debt. While on the other hand, the amount of leverage reduced to

a considerable value of 64.91 % showing that the business was able to reduce its

borrowings or debt in accordance to its equity.

Modigliani and Miller propose capital structure irrelevancy hypothesis, which states that a

company's capital structure has no bearing on its valuation. The value of a company is unaffected

by whether it is heavily leveraged or has a minimal debt component in its financing mix. Apart

from the risk associated in the investment, the operating revenue affects the market value of the

firm, according to the Modigliani and Miller Approach. According to the notion, the firm's worth

is unaffected by the capital structure or financing decisions it makes.

According to the Modigliani and Miller Approach, the value of a leveraged company (one with a

mix of debt and equity) is the same as the value of an unleveraged company (a firm that is

wholly financed by equity). If the operating profit margins and future prospects are identical.

That is, if an investor buys shares in a leveraged company, payment can be done at the same

price as if shares can be bought in an unleveraged company.

The company is having an optimal capital structure which states that it is having a

combination of debt and equity financing that majorly helps in maximizing the value of the

company and on the other hand it helps in minimizing the cost of capital. BT Is majorly aiming

to minimize the weighted average cost so that the company is bearing lowest cost for financing.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Section – C

Ratio Analysis

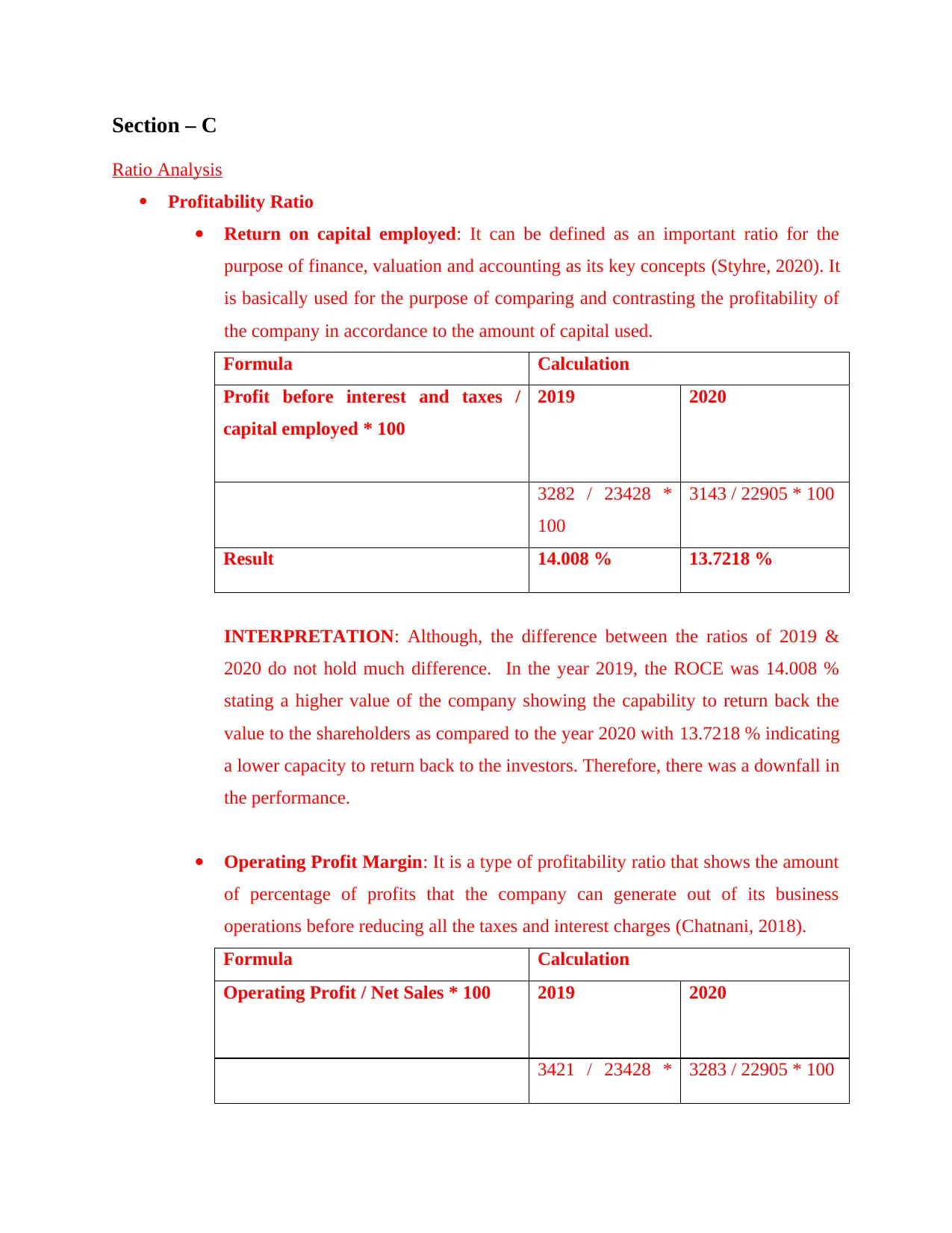

Profitability Ratio

Return on capital employed: It can be defined as an important ratio for the

purpose of finance, valuation and accounting as its key concepts (Styhre, 2020). It

is basically used for the purpose of comparing and contrasting the profitability of

the company in accordance to the amount of capital used.

Formula Calculation

Profit before interest and taxes /

capital employed * 100

2019 2020

3282 / 23428 *

100

3143 / 22905 * 100

Result 14.008 % 13.7218 %

INTERPRETATION: Although, the difference between the ratios of 2019 &

2020 do not hold much difference. In the year 2019, the ROCE was 14.008 %

stating a higher value of the company showing the capability to return back the

value to the shareholders as compared to the year 2020 with 13.7218 % indicating

a lower capacity to return back to the investors. Therefore, there was a downfall in

the performance.

Operating Profit Margin: It is a type of profitability ratio that shows the amount

of percentage of profits that the company can generate out of its business

operations before reducing all the taxes and interest charges (Chatnani, 2018).

Formula Calculation

Operating Profit / Net Sales * 100 2019 2020

3421 / 23428 * 3283 / 22905 * 100

Ratio Analysis

Profitability Ratio

Return on capital employed: It can be defined as an important ratio for the

purpose of finance, valuation and accounting as its key concepts (Styhre, 2020). It

is basically used for the purpose of comparing and contrasting the profitability of

the company in accordance to the amount of capital used.

Formula Calculation

Profit before interest and taxes /

capital employed * 100

2019 2020

3282 / 23428 *

100

3143 / 22905 * 100

Result 14.008 % 13.7218 %

INTERPRETATION: Although, the difference between the ratios of 2019 &

2020 do not hold much difference. In the year 2019, the ROCE was 14.008 %

stating a higher value of the company showing the capability to return back the

value to the shareholders as compared to the year 2020 with 13.7218 % indicating

a lower capacity to return back to the investors. Therefore, there was a downfall in

the performance.

Operating Profit Margin: It is a type of profitability ratio that shows the amount

of percentage of profits that the company can generate out of its business

operations before reducing all the taxes and interest charges (Chatnani, 2018).

Formula Calculation

Operating Profit / Net Sales * 100 2019 2020

3421 / 23428 * 3283 / 22905 * 100

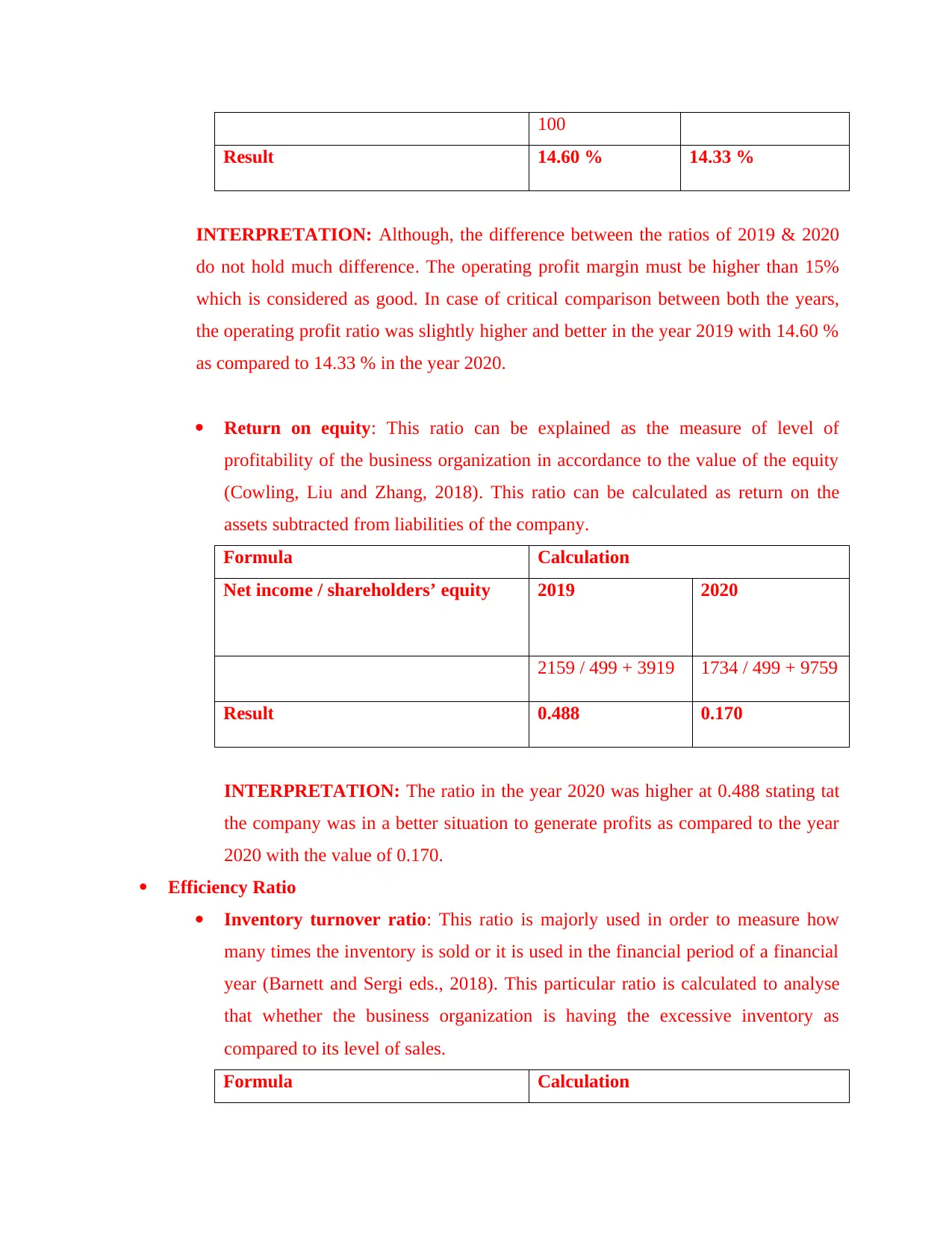

100

Result 14.60 % 14.33 %

INTERPRETATION: Although, the difference between the ratios of 2019 & 2020

do not hold much difference. The operating profit margin must be higher than 15%

which is considered as good. In case of critical comparison between both the years,

the operating profit ratio was slightly higher and better in the year 2019 with 14.60 %

as compared to 14.33 % in the year 2020.

Return on equity: This ratio can be explained as the measure of level of

profitability of the business organization in accordance to the value of the equity

(Cowling, Liu and Zhang, 2018). This ratio can be calculated as return on the

assets subtracted from liabilities of the company.

Formula Calculation

Net income / shareholders’ equity 2019 2020

2159 / 499 + 3919 1734 / 499 + 9759

Result 0.488 0.170

INTERPRETATION: The ratio in the year 2020 was higher at 0.488 stating tat

the company was in a better situation to generate profits as compared to the year

2020 with the value of 0.170.

Efficiency Ratio

Inventory turnover ratio: This ratio is majorly used in order to measure how

many times the inventory is sold or it is used in the financial period of a financial

year (Barnett and Sergi eds., 2018). This particular ratio is calculated to analyse

that whether the business organization is having the excessive inventory as

compared to its level of sales.

Formula Calculation

Result 14.60 % 14.33 %

INTERPRETATION: Although, the difference between the ratios of 2019 & 2020

do not hold much difference. The operating profit margin must be higher than 15%

which is considered as good. In case of critical comparison between both the years,

the operating profit ratio was slightly higher and better in the year 2019 with 14.60 %

as compared to 14.33 % in the year 2020.

Return on equity: This ratio can be explained as the measure of level of

profitability of the business organization in accordance to the value of the equity

(Cowling, Liu and Zhang, 2018). This ratio can be calculated as return on the

assets subtracted from liabilities of the company.

Formula Calculation

Net income / shareholders’ equity 2019 2020

2159 / 499 + 3919 1734 / 499 + 9759

Result 0.488 0.170

INTERPRETATION: The ratio in the year 2020 was higher at 0.488 stating tat

the company was in a better situation to generate profits as compared to the year

2020 with the value of 0.170.

Efficiency Ratio

Inventory turnover ratio: This ratio is majorly used in order to measure how

many times the inventory is sold or it is used in the financial period of a financial

year (Barnett and Sergi eds., 2018). This particular ratio is calculated to analyse

that whether the business organization is having the excessive inventory as

compared to its level of sales.

Formula Calculation

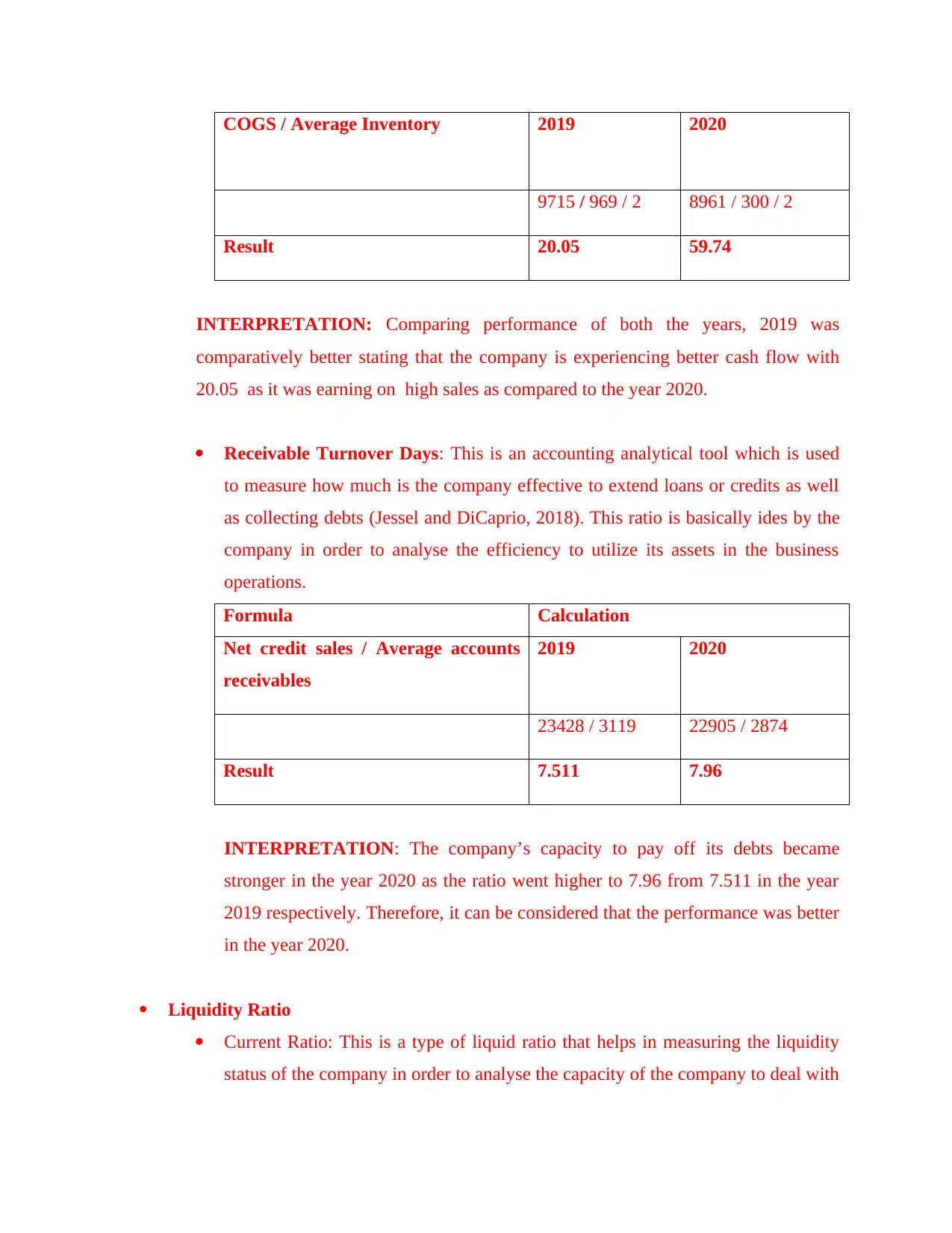

COGS / Average Inventory 2019 2020

9715 / 969 / 2 8961 / 300 / 2

Result 20.05 59.74

INTERPRETATION: Comparing performance of both the years, 2019 was

comparatively better stating that the company is experiencing better cash flow with

20.05 as it was earning on high sales as compared to the year 2020.

Receivable Turnover Days: This is an accounting analytical tool which is used

to measure how much is the company effective to extend loans or credits as well

as collecting debts (Jessel and DiCaprio, 2018). This ratio is basically ides by the

company in order to analyse the efficiency to utilize its assets in the business

operations.

Formula Calculation

Net credit sales / Average accounts

receivables

2019 2020

23428 / 3119 22905 / 2874

Result 7.511 7.96

INTERPRETATION: The company’s capacity to pay off its debts became

stronger in the year 2020 as the ratio went higher to 7.96 from 7.511 in the year

2019 respectively. Therefore, it can be considered that the performance was better

in the year 2020.

Liquidity Ratio

Current Ratio: This is a type of liquid ratio that helps in measuring the liquidity

status of the company in order to analyse the capacity of the company to deal with

9715 / 969 / 2 8961 / 300 / 2

Result 20.05 59.74

INTERPRETATION: Comparing performance of both the years, 2019 was

comparatively better stating that the company is experiencing better cash flow with

20.05 as it was earning on high sales as compared to the year 2020.

Receivable Turnover Days: This is an accounting analytical tool which is used

to measure how much is the company effective to extend loans or credits as well

as collecting debts (Jessel and DiCaprio, 2018). This ratio is basically ides by the

company in order to analyse the efficiency to utilize its assets in the business

operations.

Formula Calculation

Net credit sales / Average accounts

receivables

2019 2020

23428 / 3119 22905 / 2874

Result 7.511 7.96

INTERPRETATION: The company’s capacity to pay off its debts became

stronger in the year 2020 as the ratio went higher to 7.96 from 7.511 in the year

2019 respectively. Therefore, it can be considered that the performance was better

in the year 2020.

Liquidity Ratio

Current Ratio: This is a type of liquid ratio that helps in measuring the liquidity

status of the company in order to analyse the capacity of the company to deal with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

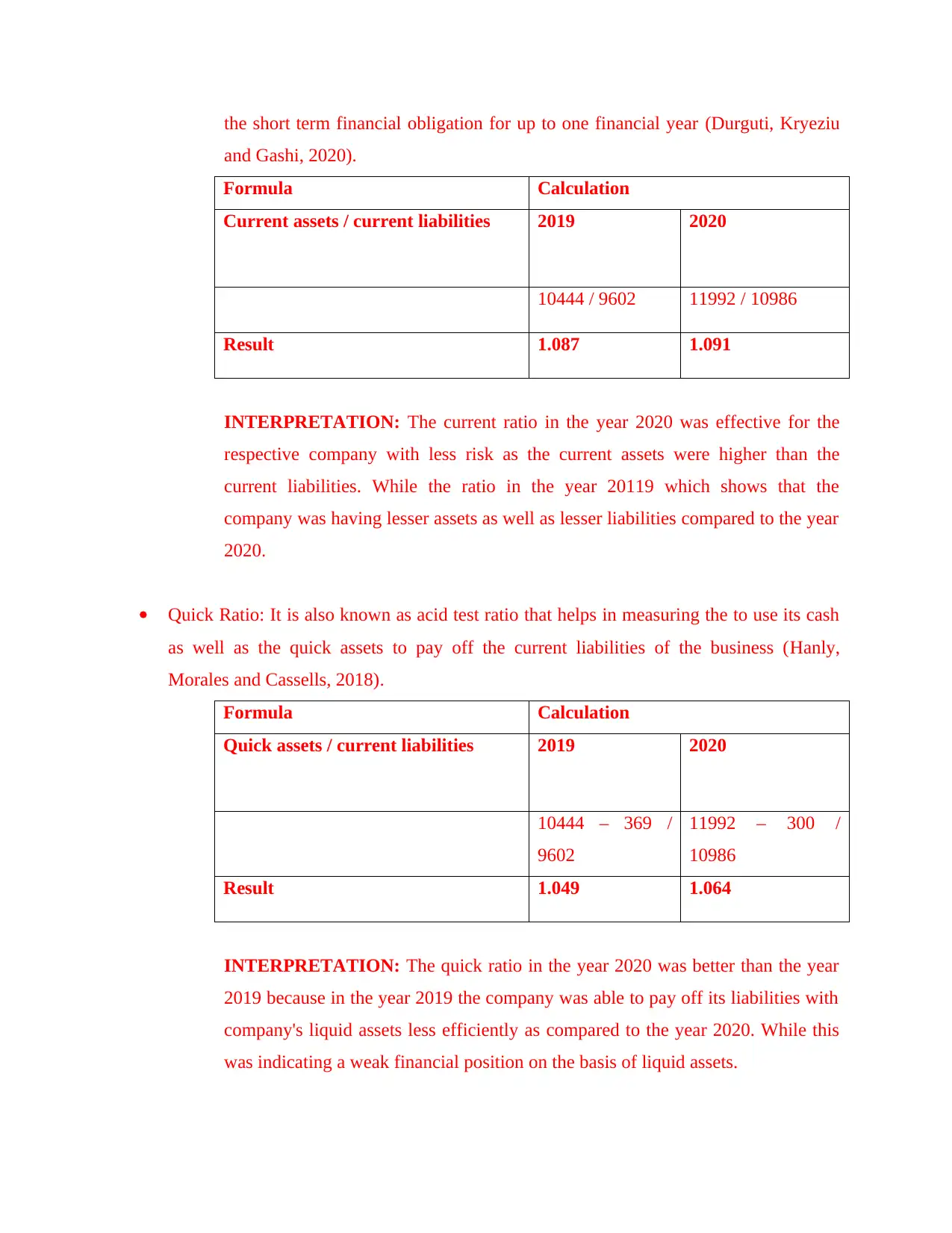

the short term financial obligation for up to one financial year (Durguti, Kryeziu

and Gashi, 2020).

Formula Calculation

Current assets / current liabilities 2019 2020

10444 / 9602 11992 / 10986

Result 1.087 1.091

INTERPRETATION: The current ratio in the year 2020 was effective for the

respective company with less risk as the current assets were higher than the

current liabilities. While the ratio in the year 20119 which shows that the

company was having lesser assets as well as lesser liabilities compared to the year

2020.

Quick Ratio: It is also known as acid test ratio that helps in measuring the to use its cash

as well as the quick assets to pay off the current liabilities of the business (Hanly,

Morales and Cassells, 2018).

Formula Calculation

Quick assets / current liabilities 2019 2020

10444 – 369 /

9602

11992 – 300 /

10986

Result 1.049 1.064

INTERPRETATION: The quick ratio in the year 2020 was better than the year

2019 because in the year 2019 the company was able to pay off its liabilities with

company's liquid assets less efficiently as compared to the year 2020. While this

was indicating a weak financial position on the basis of liquid assets.

and Gashi, 2020).

Formula Calculation

Current assets / current liabilities 2019 2020

10444 / 9602 11992 / 10986

Result 1.087 1.091

INTERPRETATION: The current ratio in the year 2020 was effective for the

respective company with less risk as the current assets were higher than the

current liabilities. While the ratio in the year 20119 which shows that the

company was having lesser assets as well as lesser liabilities compared to the year

2020.

Quick Ratio: It is also known as acid test ratio that helps in measuring the to use its cash

as well as the quick assets to pay off the current liabilities of the business (Hanly,

Morales and Cassells, 2018).

Formula Calculation

Quick assets / current liabilities 2019 2020

10444 – 369 /

9602

11992 – 300 /

10986

Result 1.049 1.064

INTERPRETATION: The quick ratio in the year 2020 was better than the year

2019 because in the year 2019 the company was able to pay off its liabilities with

company's liquid assets less efficiently as compared to the year 2020. While this

was indicating a weak financial position on the basis of liquid assets.

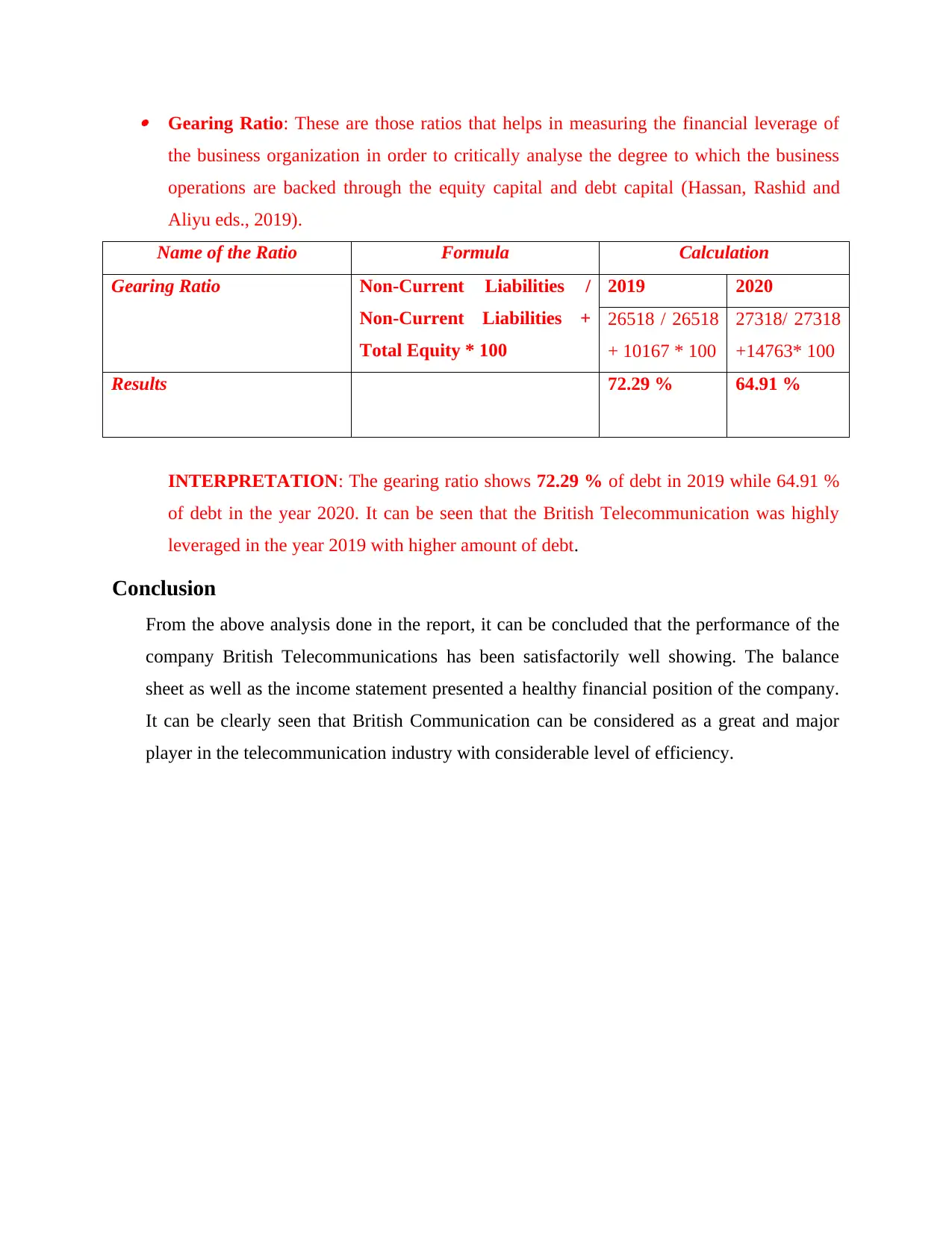

Gearing Ratio: These are those ratios that helps in measuring the financial leverage of

the business organization in order to critically analyse the degree to which the business

operations are backed through the equity capital and debt capital (Hassan, Rashid and

Aliyu eds., 2019).

Name of the Ratio Formula Calculation

Gearing Ratio Non-Current Liabilities /

Non-Current Liabilities +

Total Equity * 100

2019 2020

26518 / 26518

+ 10167 * 100

27318/ 27318

+14763* 100

Results 72.29 % 64.91 %

INTERPRETATION: The gearing ratio shows 72.29 % of debt in 2019 while 64.91 %

of debt in the year 2020. It can be seen that the British Telecommunication was highly

leveraged in the year 2019 with higher amount of debt.

Conclusion

From the above analysis done in the report, it can be concluded that the performance of the

company British Telecommunications has been satisfactorily well showing. The balance

sheet as well as the income statement presented a healthy financial position of the company.

It can be clearly seen that British Communication can be considered as a great and major

player in the telecommunication industry with considerable level of efficiency.

the business organization in order to critically analyse the degree to which the business

operations are backed through the equity capital and debt capital (Hassan, Rashid and

Aliyu eds., 2019).

Name of the Ratio Formula Calculation

Gearing Ratio Non-Current Liabilities /

Non-Current Liabilities +

Total Equity * 100

2019 2020

26518 / 26518

+ 10167 * 100

27318/ 27318

+14763* 100

Results 72.29 % 64.91 %

INTERPRETATION: The gearing ratio shows 72.29 % of debt in 2019 while 64.91 %

of debt in the year 2020. It can be seen that the British Telecommunication was highly

leveraged in the year 2019 with higher amount of debt.

Conclusion

From the above analysis done in the report, it can be concluded that the performance of the

company British Telecommunications has been satisfactorily well showing. The balance

sheet as well as the income statement presented a healthy financial position of the company.

It can be clearly seen that British Communication can be considered as a great and major

player in the telecommunication industry with considerable level of efficiency.

References

Books & Journals

Mather, B., 2019. Artificial Intelligence in Real Estate Investing: How Artificial Intelligence and

Machine Learning technology will cause a transformation in real estate business,

marketing and finance for everyone. Abiprod Pty Ltd.

Moreale, J. and Zaynutdinova, G. R., 2018. A Bloomberg terminal application in an intermediate

finance course. Journal of Financial Education, 44(2). pp.262-283.

Chris Kraft, C. G. F. M. and PMP, P. A., 2018. Agile project management on government

finance projects. The Journal of Government Financial Management, 67(1). pp.12-18.

Demirgüç-Kunt, A. and Levine, R., 2018. Finance and growth. Edward Elgar Publishing

Limited.

van Bergen, M., and et. al., 2019. Supply chain finance schemes in the procurement of

agricultural products. Journal of Purchasing and Supply Management, 25(2). pp.172-184.

Styhre, A., 2020. Thinly and thickly capitalized projects: Theorizing the role of the finance

markets and capital supply in project management studies. Project Management

Journal, 51(4). pp.378-388.

Chatnani, N. N., 2018. Receivables management and supply chain finance for MSMEs: Analysis

of TREDS. Academy of Strategic Management Journal, 17(3). pp.1-8.

Cowling, M., Liu, W. and Zhang, N., 2018. Did firm age, experience, and access to finance

count? SME performance after the global financial crisis. Journal of Evolutionary

Economics, 28(1). pp.77-100.

Barnett, W. A. and Sergi, B. S. eds., 2018. Banking and finance issues in emerging markets.

Emerald Group Publishing.

Jessel, B. and DiCaprio, A., 2018. Can blockchain make trade finance more inclusive?. Journal

of Financial Transformation, 47. pp.35-50.

Durguti, E., Kryeziu, N. and Gashi, E., 2020. How Does the Budget Deficit Affect Inflation

Rate-Evidence from Western Balkans. International Journal of Finance & Banking

Studies, 9(1). pp.01-10.

Hanly, J., Morales, L. and Cassells, D., 2018. The efficacy of financial futures as a hedging tool

in electricity markets. International Journal of Finance & Economics, 23(1). pp.29-40.

Books & Journals

Mather, B., 2019. Artificial Intelligence in Real Estate Investing: How Artificial Intelligence and

Machine Learning technology will cause a transformation in real estate business,

marketing and finance for everyone. Abiprod Pty Ltd.

Moreale, J. and Zaynutdinova, G. R., 2018. A Bloomberg terminal application in an intermediate

finance course. Journal of Financial Education, 44(2). pp.262-283.

Chris Kraft, C. G. F. M. and PMP, P. A., 2018. Agile project management on government

finance projects. The Journal of Government Financial Management, 67(1). pp.12-18.

Demirgüç-Kunt, A. and Levine, R., 2018. Finance and growth. Edward Elgar Publishing

Limited.

van Bergen, M., and et. al., 2019. Supply chain finance schemes in the procurement of

agricultural products. Journal of Purchasing and Supply Management, 25(2). pp.172-184.

Styhre, A., 2020. Thinly and thickly capitalized projects: Theorizing the role of the finance

markets and capital supply in project management studies. Project Management

Journal, 51(4). pp.378-388.

Chatnani, N. N., 2018. Receivables management and supply chain finance for MSMEs: Analysis

of TREDS. Academy of Strategic Management Journal, 17(3). pp.1-8.

Cowling, M., Liu, W. and Zhang, N., 2018. Did firm age, experience, and access to finance

count? SME performance after the global financial crisis. Journal of Evolutionary

Economics, 28(1). pp.77-100.

Barnett, W. A. and Sergi, B. S. eds., 2018. Banking and finance issues in emerging markets.

Emerald Group Publishing.

Jessel, B. and DiCaprio, A., 2018. Can blockchain make trade finance more inclusive?. Journal

of Financial Transformation, 47. pp.35-50.

Durguti, E., Kryeziu, N. and Gashi, E., 2020. How Does the Budget Deficit Affect Inflation

Rate-Evidence from Western Balkans. International Journal of Finance & Banking

Studies, 9(1). pp.01-10.

Hanly, J., Morales, L. and Cassells, D., 2018. The efficacy of financial futures as a hedging tool

in electricity markets. International Journal of Finance & Economics, 23(1). pp.29-40.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Hassan, M. K., Rashid, M. and Aliyu, S. eds., 2019. Islamic Corporate Finance. Routledge.

Online Reference

Dividend Irrelevance Theory, 2020. [Online] Available through:

< https://www.investopedia.com/terms/d/dividendirrelevance.asp/ >

Online Reference

Dividend Irrelevance Theory, 2020. [Online] Available through:

< https://www.investopedia.com/terms/d/dividendirrelevance.asp/ >

Appendix

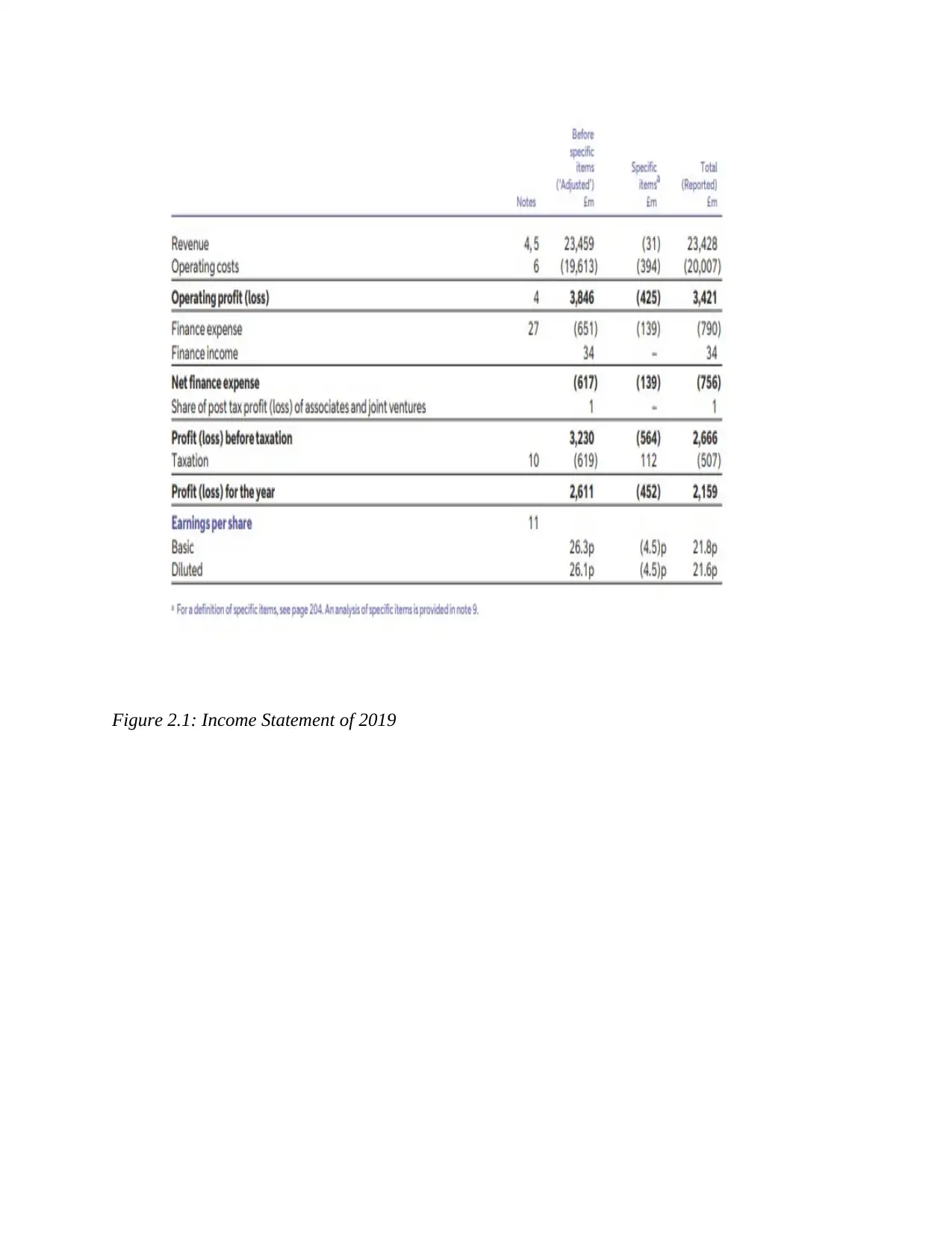

Both the financial statement namely “Statement of Income Statement” & “Statement of Balance

Sheet” are mentioned below of the both the financial year. (Source: Annual Reports of British

Telecommunication of the year 2019 & 2020)

Figure 1.1: Statement of Balance Sheet

Figure 1.2: Statement of Balance Sheet

Both the financial statement namely “Statement of Income Statement” & “Statement of Balance

Sheet” are mentioned below of the both the financial year. (Source: Annual Reports of British

Telecommunication of the year 2019 & 2020)

Figure 1.1: Statement of Balance Sheet

Figure 1.2: Statement of Balance Sheet

Figure 2: Income Statement of 2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 2.1: Income Statement of 2019

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.