LSBM203 Managerial Finance: Financial Analysis & Investment

VerifiedAdded on 2023/06/15

|14

|3819

|150

Portfolio

AI Summary

This portfolio provides a comprehensive financial analysis and capital investment appraisal. It begins with a comparative analysis of two UK retailers, B&M and Morrison's, using ten key financial ratios to assess their profitability, liquidity, efficiency, and gearing. The analysis identifies areas of strength and weakness for each company, with recommendations provided for improving Morrison's financial performance. The portfolio also discusses the limitations of relying solely on financial ratios. Furthermore, it compares two capital investment projects, Alpha and Beta, using investment appraisal techniques to determine their viability and potential returns, while also acknowledging the limitations of these techniques. This document is available on Desklib, a platform offering a wide range of study tools and resources for students.

Financial Analysis & Capital

investment appraisal

investment appraisal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

A. Calculating the 10 financial ratios .........................................................................................3

B. Analysing the performance of both the companies.................................................................5

C. Providing recommendation to the company whose financial performance was poor.............8

D. Discussing the limitation of relying over the financial ratios for interpreting the

performance of the company.......................................................................................................8

TASK- Capital Investment Appraisal..............................................................................................9

Comparison between two projects through investment appraisal techniques.............................9

Limitation of investment appraisal techniques..........................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

A. Calculating the 10 financial ratios .........................................................................................3

B. Analysing the performance of both the companies.................................................................5

C. Providing recommendation to the company whose financial performance was poor.............8

D. Discussing the limitation of relying over the financial ratios for interpreting the

performance of the company.......................................................................................................8

TASK- Capital Investment Appraisal..............................................................................................9

Comparison between two projects through investment appraisal techniques.............................9

Limitation of investment appraisal techniques..........................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial analysis is the process which is used for the evaluation of the business, projects,

budgets and other financial transactions that are helpful for the determination of the

organizations performance. Capital investment is the acquisition of the physical assets by a

company which helps in the management of the long-term business goals and objectives. In this

project there has been comparison between the financial performance of two retailers of UK

B&M and Morrison’s. Different financial ratios are compared for these organizations in order to

understand the difference in the financial performances. This project also provides

recommendations to the financial performance of the organization. In this project two projects

Alpha and Beta are compared for analysing the differences between the

TASK 1

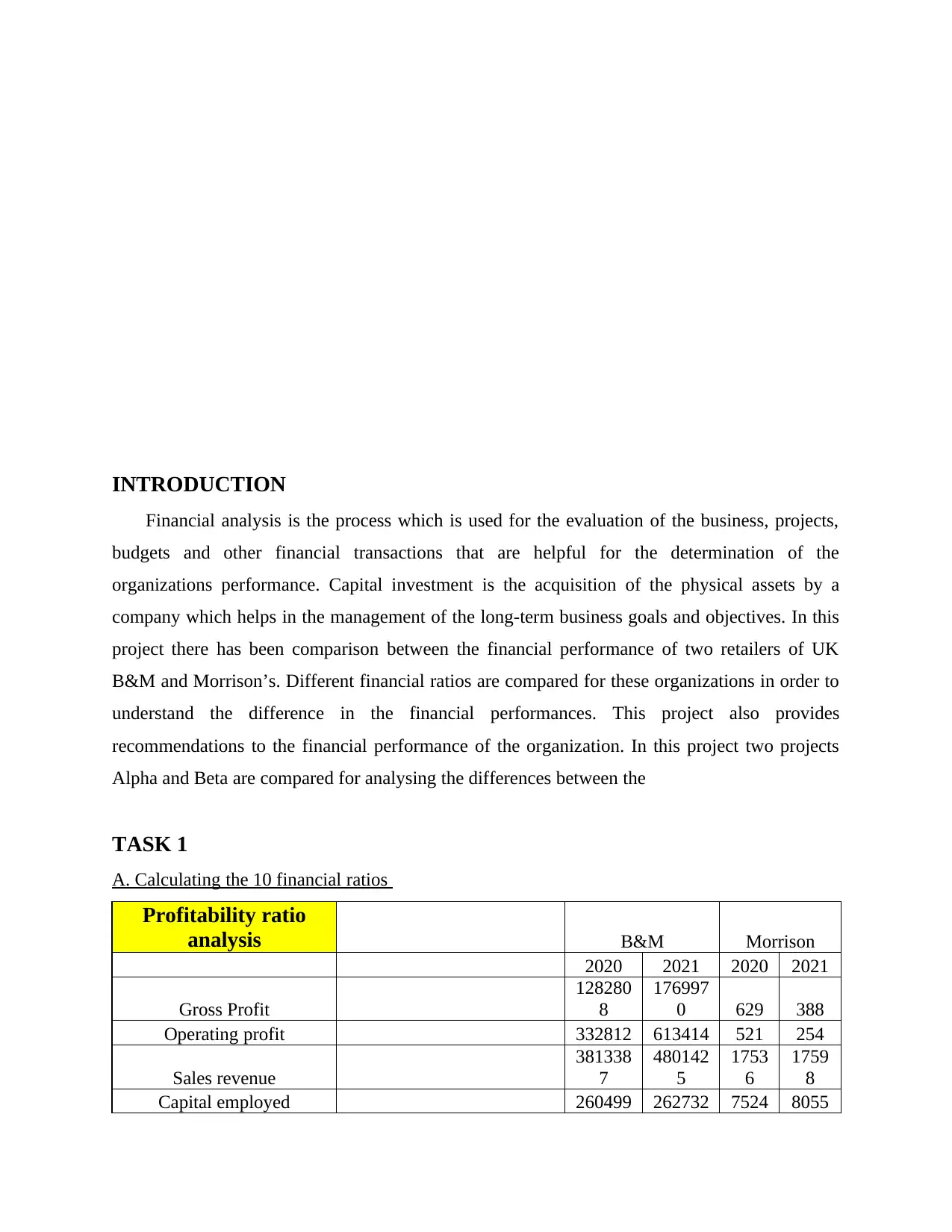

A. Calculating the 10 financial ratios

Profitability ratio

analysis B&M Morrison

2020 2021 2020 2021

Gross Profit

128280

8

176997

0 629 388

Operating profit 332812 613414 521 254

Sales revenue

381338

7

480142

5

1753

6

1759

8

Capital employed 260499 262732 7524 8055

Financial analysis is the process which is used for the evaluation of the business, projects,

budgets and other financial transactions that are helpful for the determination of the

organizations performance. Capital investment is the acquisition of the physical assets by a

company which helps in the management of the long-term business goals and objectives. In this

project there has been comparison between the financial performance of two retailers of UK

B&M and Morrison’s. Different financial ratios are compared for these organizations in order to

understand the difference in the financial performances. This project also provides

recommendations to the financial performance of the organization. In this project two projects

Alpha and Beta are compared for analysing the differences between the

TASK 1

A. Calculating the 10 financial ratios

Profitability ratio

analysis B&M Morrison

2020 2021 2020 2021

Gross Profit

128280

8

176997

0 629 388

Operating profit 332812 613414 521 254

Sales revenue

381338

7

480142

5

1753

6

1759

8

Capital employed 260499 262732 7524 8055

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

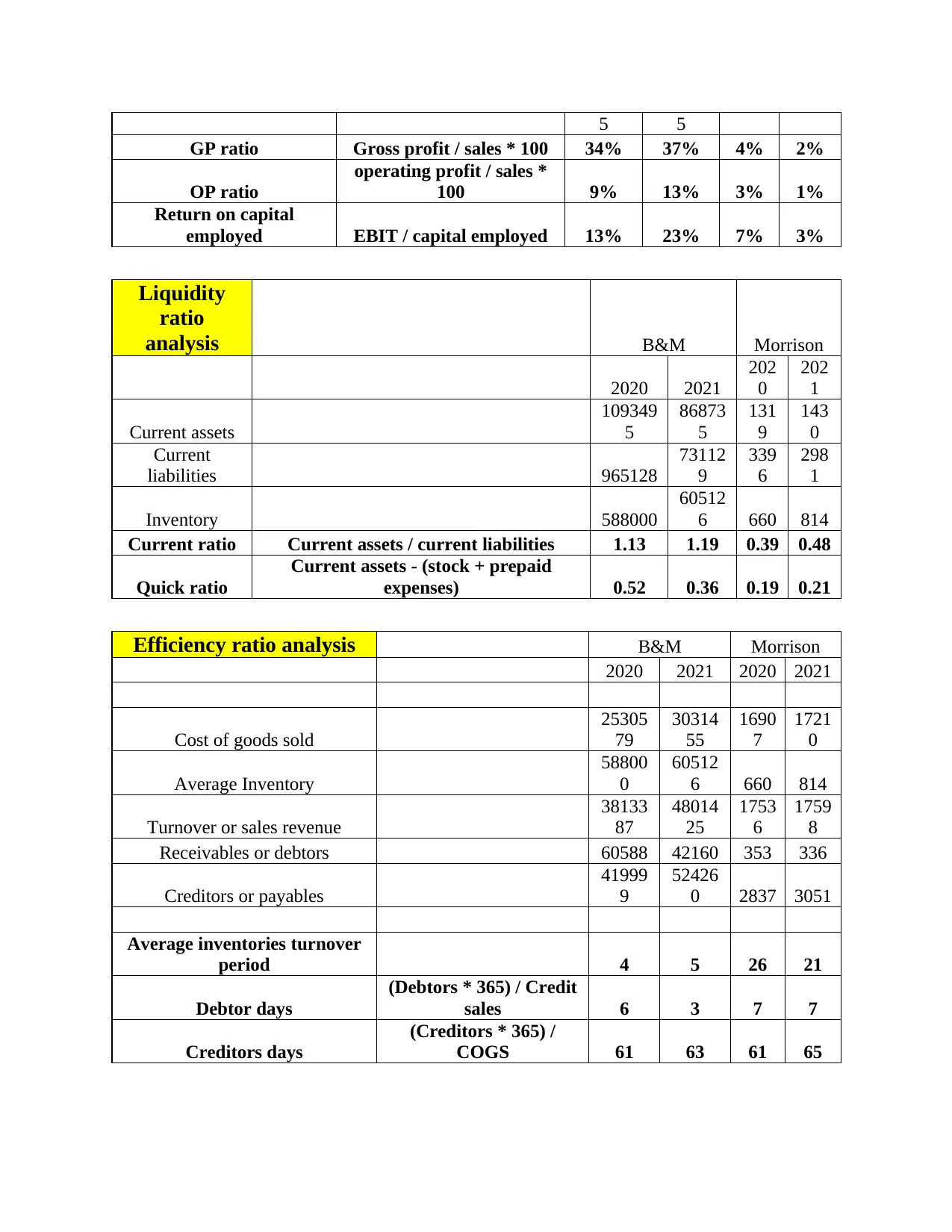

5 5

GP ratio Gross profit / sales * 100 34% 37% 4% 2%

OP ratio

operating profit / sales *

100 9% 13% 3% 1%

Return on capital

employed EBIT / capital employed 13% 23% 7% 3%

Liquidity

ratio

analysis B&M Morrison

2020 2021

202

0

202

1

Current assets

109349

5

86873

5

131

9

143

0

Current

liabilities 965128

73112

9

339

6

298

1

Inventory 588000

60512

6 660 814

Current ratio Current assets / current liabilities 1.13 1.19 0.39 0.48

Quick ratio

Current assets - (stock + prepaid

expenses) 0.52 0.36 0.19 0.21

Efficiency ratio analysis B&M Morrison

2020 2021 2020 2021

Cost of goods sold

25305

79

30314

55

1690

7

1721

0

Average Inventory

58800

0

60512

6 660 814

Turnover or sales revenue

38133

87

48014

25

1753

6

1759

8

Receivables or debtors 60588 42160 353 336

Creditors or payables

41999

9

52426

0 2837 3051

Average inventories turnover

period 4 5 26 21

Debtor days

(Debtors * 365) / Credit

sales 6 3 7 7

Creditors days

(Creditors * 365) /

COGS 61 63 61 65

GP ratio Gross profit / sales * 100 34% 37% 4% 2%

OP ratio

operating profit / sales *

100 9% 13% 3% 1%

Return on capital

employed EBIT / capital employed 13% 23% 7% 3%

Liquidity

ratio

analysis B&M Morrison

2020 2021

202

0

202

1

Current assets

109349

5

86873

5

131

9

143

0

Current

liabilities 965128

73112

9

339

6

298

1

Inventory 588000

60512

6 660 814

Current ratio Current assets / current liabilities 1.13 1.19 0.39 0.48

Quick ratio

Current assets - (stock + prepaid

expenses) 0.52 0.36 0.19 0.21

Efficiency ratio analysis B&M Morrison

2020 2021 2020 2021

Cost of goods sold

25305

79

30314

55

1690

7

1721

0

Average Inventory

58800

0

60512

6 660 814

Turnover or sales revenue

38133

87

48014

25

1753

6

1759

8

Receivables or debtors 60588 42160 353 336

Creditors or payables

41999

9

52426

0 2837 3051

Average inventories turnover

period 4 5 26 21

Debtor days

(Debtors * 365) / Credit

sales 6 3 7 7

Creditors days

(Creditors * 365) /

COGS 61 63 61 65

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

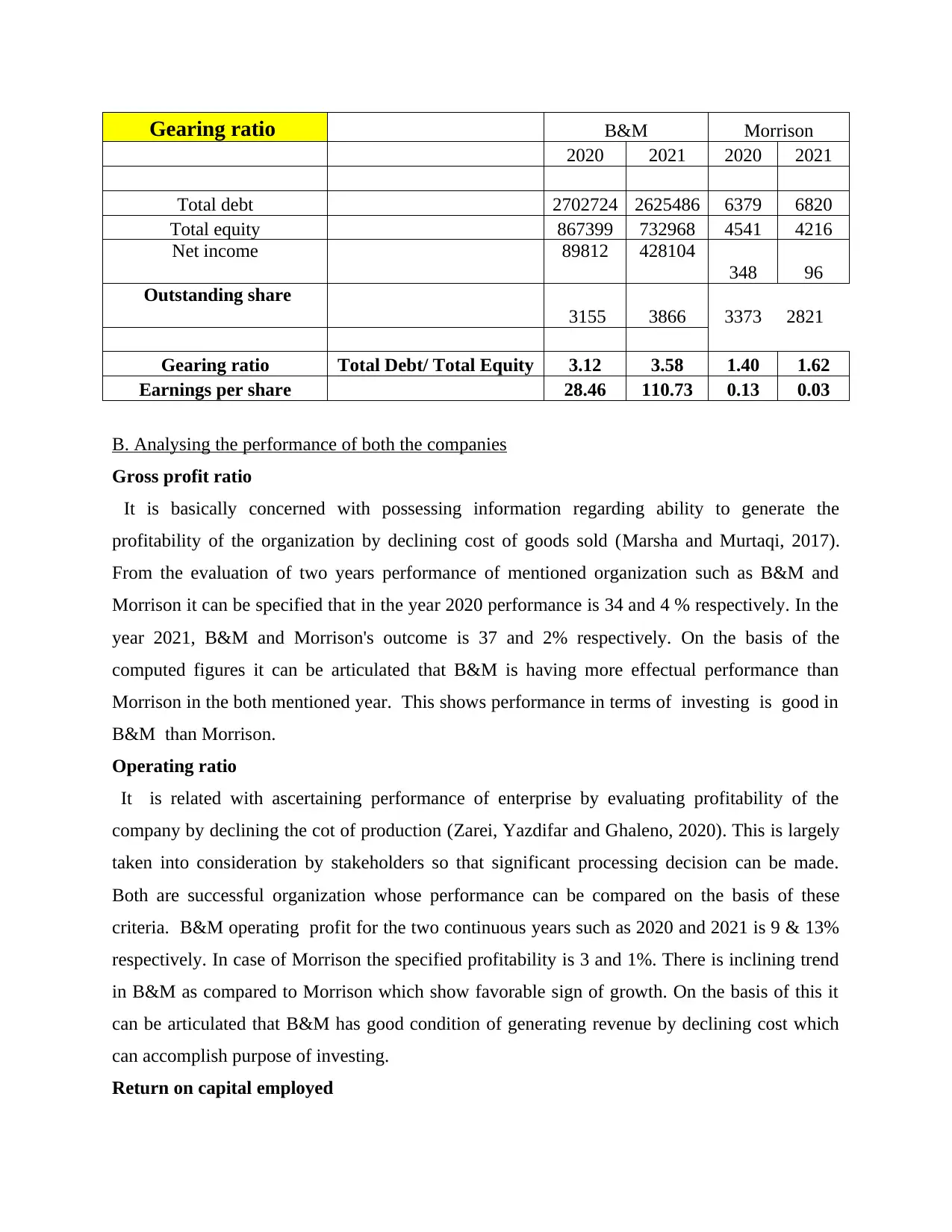

Gearing ratio B&M Morrison

2020 2021 2020 2021

Total debt 2702724 2625486 6379 6820

Total equity 867399 732968 4541 4216

Net income 89812 428104

348 96

Outstanding share

3155 3866 3373 2821

Gearing ratio Total Debt/ Total Equity 3.12 3.58 1.40 1.62

Earnings per share 28.46 110.73 0.13 0.03

B. Analysing the performance of both the companies

Gross profit ratio

It is basically concerned with possessing information regarding ability to generate the

profitability of the organization by declining cost of goods sold (Marsha and Murtaqi, 2017).

From the evaluation of two years performance of mentioned organization such as B&M and

Morrison it can be specified that in the year 2020 performance is 34 and 4 % respectively. In the

year 2021, B&M and Morrison's outcome is 37 and 2% respectively. On the basis of the

computed figures it can be articulated that B&M is having more effectual performance than

Morrison in the both mentioned year. This shows performance in terms of investing is good in

B&M than Morrison.

Operating ratio

It is related with ascertaining performance of enterprise by evaluating profitability of the

company by declining the cot of production (Zarei, Yazdifar and Ghaleno, 2020). This is largely

taken into consideration by stakeholders so that significant processing decision can be made.

Both are successful organization whose performance can be compared on the basis of these

criteria. B&M operating profit for the two continuous years such as 2020 and 2021 is 9 & 13%

respectively. In case of Morrison the specified profitability is 3 and 1%. There is inclining trend

in B&M as compared to Morrison which show favorable sign of growth. On the basis of this it

can be articulated that B&M has good condition of generating revenue by declining cost which

can accomplish purpose of investing.

Return on capital employed

2020 2021 2020 2021

Total debt 2702724 2625486 6379 6820

Total equity 867399 732968 4541 4216

Net income 89812 428104

348 96

Outstanding share

3155 3866 3373 2821

Gearing ratio Total Debt/ Total Equity 3.12 3.58 1.40 1.62

Earnings per share 28.46 110.73 0.13 0.03

B. Analysing the performance of both the companies

Gross profit ratio

It is basically concerned with possessing information regarding ability to generate the

profitability of the organization by declining cost of goods sold (Marsha and Murtaqi, 2017).

From the evaluation of two years performance of mentioned organization such as B&M and

Morrison it can be specified that in the year 2020 performance is 34 and 4 % respectively. In the

year 2021, B&M and Morrison's outcome is 37 and 2% respectively. On the basis of the

computed figures it can be articulated that B&M is having more effectual performance than

Morrison in the both mentioned year. This shows performance in terms of investing is good in

B&M than Morrison.

Operating ratio

It is related with ascertaining performance of enterprise by evaluating profitability of the

company by declining the cot of production (Zarei, Yazdifar and Ghaleno, 2020). This is largely

taken into consideration by stakeholders so that significant processing decision can be made.

Both are successful organization whose performance can be compared on the basis of these

criteria. B&M operating profit for the two continuous years such as 2020 and 2021 is 9 & 13%

respectively. In case of Morrison the specified profitability is 3 and 1%. There is inclining trend

in B&M as compared to Morrison which show favorable sign of growth. On the basis of this it

can be articulated that B&M has good condition of generating revenue by declining cost which

can accomplish purpose of investing.

Return on capital employed

It is associated with showing how much return is generated by organization by using available

capital. This is helpful in showing how effectively an organization uses particular capital to meet

objectives of investment. This is basically viewed by stakeholder like investors, lenders,

financial institutions, etc. On the basis of the provided information it can be specified that B&M

is providing return of 13 & 23% receptively for the year 2020 to 2021. In addition to this,

Morrison pay attention on return on capital employed which is 7 & 3% for the previous and

current year. On the basis of this, it can be interpreted that B&M is having higher ability to

generate revenue on capital employed.

Liquidity ratio

Current ratio is concerned with assessing the capability of the enterprise to ascertain how

effectively an organization can effectively use resources for overcoming short term liabilities

(Tarmidi, Pramukty and Akbar, 2020). In the year 2020 current ratio of B&M possessing 1.13

and 1.19 times outcome for the year2020 and 2021 respectively. On the other side, Morrison's

performance is 0.39 & 0.48 times for the mentioned duration. From the evaluation it can be

compared that Morrison's performance is less than the ideal ratio which is .2-1.5 tines. It

indicates that Morrison performance is not effective as compared to B&M.

Quick ratio

It is related with assessing how defectively an organization can overcome current liabilities

with help of cash & equivalent resources. In addition to this, it is basically taken into

consideration by investor, suppliers, competitors, financial institutions, etc so that significant

ability to make accurate & fair decision. From the assessment of the two years performance for

the year 2020 and 2021 such as of 0.52 & 0.36 B&M and 0.19 and 0.21 of Morrison. The

performance of B&M is greater than Morrison. On the basis of this, it can be specified that

B&M is having higher effectiveness is using cash & equivalent resources to handle the

obligation. Morrison needs few changes in its processing so that modified level of performance

can be derived.

Efficiency ratio

Average inventories turnover period

It is useful in n calculating the average number of days taken by firm for replacing its

inventory (Tran, Nguyen And To, 2020). It is taken into evaluation of the company that how

effectively enterprise can meet market forces so that significant level of growth and development

capital. This is helpful in showing how effectively an organization uses particular capital to meet

objectives of investment. This is basically viewed by stakeholder like investors, lenders,

financial institutions, etc. On the basis of the provided information it can be specified that B&M

is providing return of 13 & 23% receptively for the year 2020 to 2021. In addition to this,

Morrison pay attention on return on capital employed which is 7 & 3% for the previous and

current year. On the basis of this, it can be interpreted that B&M is having higher ability to

generate revenue on capital employed.

Liquidity ratio

Current ratio is concerned with assessing the capability of the enterprise to ascertain how

effectively an organization can effectively use resources for overcoming short term liabilities

(Tarmidi, Pramukty and Akbar, 2020). In the year 2020 current ratio of B&M possessing 1.13

and 1.19 times outcome for the year2020 and 2021 respectively. On the other side, Morrison's

performance is 0.39 & 0.48 times for the mentioned duration. From the evaluation it can be

compared that Morrison's performance is less than the ideal ratio which is .2-1.5 tines. It

indicates that Morrison performance is not effective as compared to B&M.

Quick ratio

It is related with assessing how defectively an organization can overcome current liabilities

with help of cash & equivalent resources. In addition to this, it is basically taken into

consideration by investor, suppliers, competitors, financial institutions, etc so that significant

ability to make accurate & fair decision. From the assessment of the two years performance for

the year 2020 and 2021 such as of 0.52 & 0.36 B&M and 0.19 and 0.21 of Morrison. The

performance of B&M is greater than Morrison. On the basis of this, it can be specified that

B&M is having higher effectiveness is using cash & equivalent resources to handle the

obligation. Morrison needs few changes in its processing so that modified level of performance

can be derived.

Efficiency ratio

Average inventories turnover period

It is useful in n calculating the average number of days taken by firm for replacing its

inventory (Tran, Nguyen And To, 2020). It is taken into evaluation of the company that how

effectively enterprise can meet market forces so that significant level of growth and development

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

can be derived. The outcome derived from the computation it can be articulated that B&M and

Morrison has performance of 4 & 5 times and 6 & 21 times respectively. On the basis of this it

can be interpreted that Morrison is having good inventory turnover ratio is good as it has highly

effectively performance which is capable in meeting market forces. In addition to this, it can be

compared that Morrison is having good average inventory than B&M which shows firm has

good amount of ability to accomplish the purpose of investment.

Debtor Days

There are different kinds of objectives which can be accomplished by business

through assessing its liquidity position. On the basis of the provided information it can be

articulated that it helps in understanding that how business is getting liquidity by collecting

payments from customer. B&M is having 6 and 3 days respectively for the year 2020 & 2021

and Morrison has outcome of 7 days for the respective two years. On the basis of the given

information regarding the debtors' day B&M has good performance as continuous. There is no

change in the Morrison performance which need to be overcome by specified firm through

applying relevant course of action. It includes analyzing credit policy, evaluating relationship

with debtor sending reminders, etc.

Creditors days

It is helpful in showing how effectively an organization is paying off debt with current

assets. In addition to this, for paying off payment to creditors for meeting market forces

effectively. From the evaluation of the determined ratio it can be specified that creditors days of

B&M and Morrison for the year 2020 is 61 & 61 days respectively. In addition to this, B&M and

Morrison has 63 and 65 days respectively. On the basis of the provided information it can be said

that in the current year B&M takes less period to overcome obligation as compared to Morrison.

There should be declining trend in order to maintain the credibility of the enterprise. B&M is

having good credibility as compared to Morrison so h that significant outcome can be derived.

Gearing ratio

It is helpful in assessing financial leverage so that demonstrating degree to which

operations are funded equity capital versus debt financing (Amrutha, Selvam and Kathiravan,

2019). This is one of the factor that contribute in ascertaining financial performance so that

proper sound decision can be made. This can be said that gearing ratio of the B&M and Morrison

for the year 2020 and 2021 is 3.12, 3.58 and 1.40 & 1.62% respectively. Less gearing ratio

Morrison has performance of 4 & 5 times and 6 & 21 times respectively. On the basis of this it

can be interpreted that Morrison is having good inventory turnover ratio is good as it has highly

effectively performance which is capable in meeting market forces. In addition to this, it can be

compared that Morrison is having good average inventory than B&M which shows firm has

good amount of ability to accomplish the purpose of investment.

Debtor Days

There are different kinds of objectives which can be accomplished by business

through assessing its liquidity position. On the basis of the provided information it can be

articulated that it helps in understanding that how business is getting liquidity by collecting

payments from customer. B&M is having 6 and 3 days respectively for the year 2020 & 2021

and Morrison has outcome of 7 days for the respective two years. On the basis of the given

information regarding the debtors' day B&M has good performance as continuous. There is no

change in the Morrison performance which need to be overcome by specified firm through

applying relevant course of action. It includes analyzing credit policy, evaluating relationship

with debtor sending reminders, etc.

Creditors days

It is helpful in showing how effectively an organization is paying off debt with current

assets. In addition to this, for paying off payment to creditors for meeting market forces

effectively. From the evaluation of the determined ratio it can be specified that creditors days of

B&M and Morrison for the year 2020 is 61 & 61 days respectively. In addition to this, B&M and

Morrison has 63 and 65 days respectively. On the basis of the provided information it can be said

that in the current year B&M takes less period to overcome obligation as compared to Morrison.

There should be declining trend in order to maintain the credibility of the enterprise. B&M is

having good credibility as compared to Morrison so h that significant outcome can be derived.

Gearing ratio

It is helpful in assessing financial leverage so that demonstrating degree to which

operations are funded equity capital versus debt financing (Amrutha, Selvam and Kathiravan,

2019). This is one of the factor that contribute in ascertaining financial performance so that

proper sound decision can be made. This can be said that gearing ratio of the B&M and Morrison

for the year 2020 and 2021 is 3.12, 3.58 and 1.40 & 1.62% respectively. Less gearing ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

indicate that company has good amount of profitability and sustainability to meet objectives.

Morrison as compared to B&M as it has lower leverage which shows less risk to invest. On the

basis of thee provided information it can be interpreted that B&M m has higher risk as compared

to Morrison so that significant level of profitability can be achieved by business.

Earning per share

On the basis of calculation it can be specified that organization should have higher

earning per share so that profitability can sustainability can be derived (Pattiasina and et.al.,

2018). There are two companies whose EPS are evaluated on the basis of the presented

information it can be specified that B&M has higher EPS as compared to Morrison. On the basis

of the provided information it can be specified that investing in B&M is more profitable.

Morison need to make changes for having providing effective EPS so that larger number of

investors can be attracted.

C. Providing recommendation to the company whose financial performance was poor

With the above analysis of the ratios and the comparative discussion it was evaluated that

the performance of Morrison is poor. This is pertaining to the fact that on the basis of the

profitability and the liquidity it was analysed that the performance was not good. Hence, it is

necessary for Morrison to improve the working efficiency of the company so that it can increase

its profitability. Some of the recommendation for improving the performance of Morrison are as

follows-

The first and foremost recommendation to the Morrison is that they must try to improve

its liquidity. Hence, for this, it is necessary that they must try to improve the current ratio.

Hence, for this it is essential that they must try to increase the current asset. This is

necessary because when the current asset will be more than the company will be in

position to pay off the current liabilities easily.

Along with this another suggestion to Morrison to improve its performance is that they

must clear all their payment to the creditors in less time. This is pertaining to the fact that

the creditor period has increased which is not good for the company. Thus, it is advisable

to the company that they must try to reduce the time the company take in making

payment to the creditors.

Morrison as compared to B&M as it has lower leverage which shows less risk to invest. On the

basis of thee provided information it can be interpreted that B&M m has higher risk as compared

to Morrison so that significant level of profitability can be achieved by business.

Earning per share

On the basis of calculation it can be specified that organization should have higher

earning per share so that profitability can sustainability can be derived (Pattiasina and et.al.,

2018). There are two companies whose EPS are evaluated on the basis of the presented

information it can be specified that B&M has higher EPS as compared to Morrison. On the basis

of the provided information it can be specified that investing in B&M is more profitable.

Morison need to make changes for having providing effective EPS so that larger number of

investors can be attracted.

C. Providing recommendation to the company whose financial performance was poor

With the above analysis of the ratios and the comparative discussion it was evaluated that

the performance of Morrison is poor. This is pertaining to the fact that on the basis of the

profitability and the liquidity it was analysed that the performance was not good. Hence, it is

necessary for Morrison to improve the working efficiency of the company so that it can increase

its profitability. Some of the recommendation for improving the performance of Morrison are as

follows-

The first and foremost recommendation to the Morrison is that they must try to improve

its liquidity. Hence, for this, it is necessary that they must try to improve the current ratio.

Hence, for this it is essential that they must try to increase the current asset. This is

necessary because when the current asset will be more than the company will be in

position to pay off the current liabilities easily.

Along with this another suggestion to Morrison to improve its performance is that they

must clear all their payment to the creditors in less time. This is pertaining to the fact that

the creditor period has increased which is not good for the company. Thus, it is advisable

to the company that they must try to reduce the time the company take in making

payment to the creditors.

D. Discussing the limitation of relying over the financial ratios for interpreting the performance

of the company

The use of ratio analysis is very important for the company in order to evaluate its

performance on the basis of the past year and also with other competitors. The reason pertaining

to the fact is that in case the ratios will not be evaluated in proper manner then this will result in

ineffective analysis of performance of company. Although there are many different types of

limitation as well which can affect the performance of the company and its proper analysis. The

major limitation involving the use of ratio for interpreting the performance of the company.

The main limitation which affects the interpretation of the performance of the company is

that the size of the company matters. The reason pertaining to the fact is that it is not

necessary that all the companies have same size. Hence, the comparison done of

companies belonging to different sizes will not provide a clear picture of financial

performance of the company.

Moreover, another limitation which the company faces at time of using the ratio analysis

is that this method ignores the price level changes which are being caused by the

inflation. This is pertaining to the fact that the use of ratio is based on the book value data

only and not the current prices changes.

TASK- Capital Investment Appraisal

Comparison between two projects through investment appraisal techniques

In order to compare the viability of the two projects it is important to analyse the

following investment techniques,

NPV:

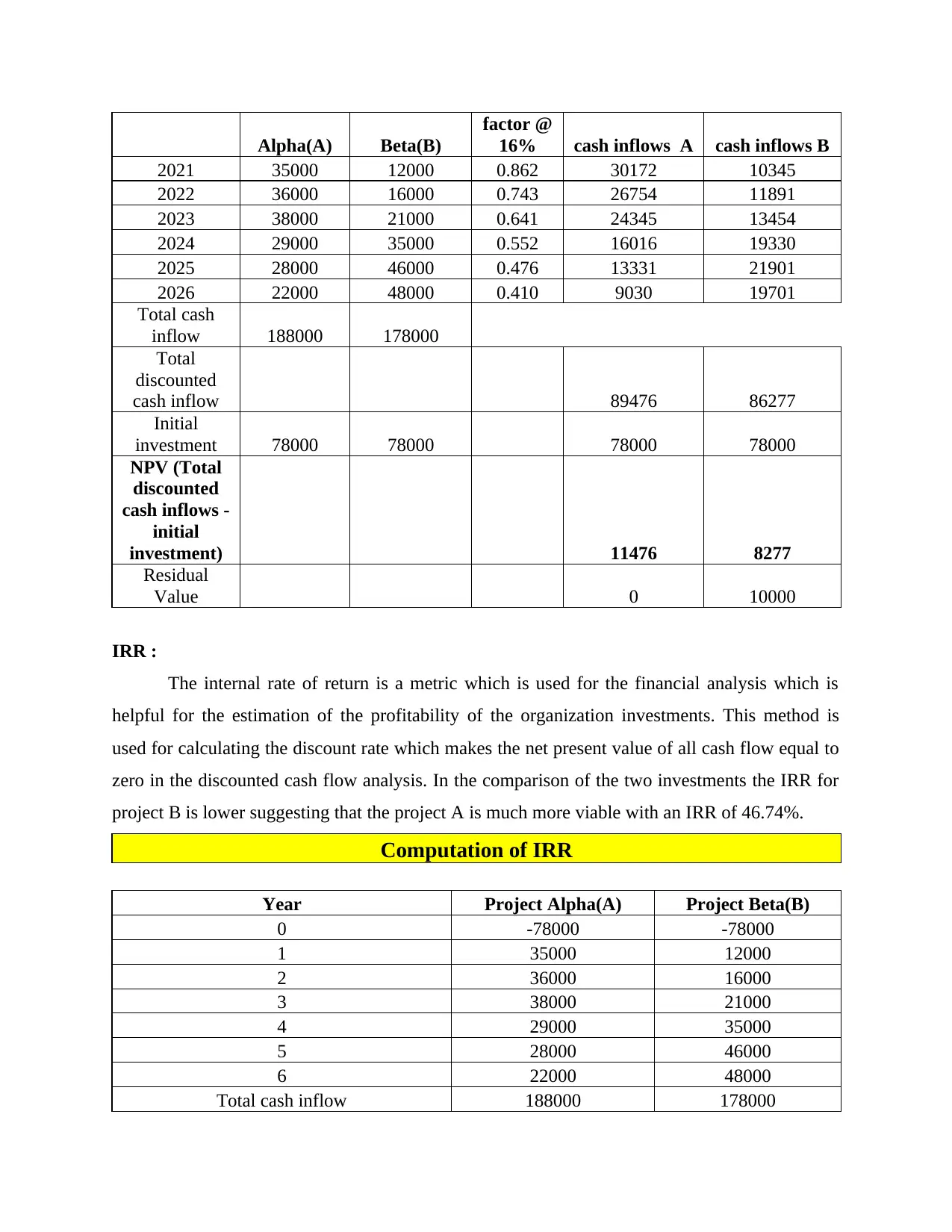

Net present value is the difference between the present value of cash inflow and the

present value of cash outflow which is present over a certain time in the organization. This

method is for capital budgeting and investment planning for the analysation of the profitability of

the project investment (Lawal and et.al., 2021). For the project alpha(A) the total NPV which is

calculated is 11476 however for the project beta the calculated NPV is 8277. Thus, it can be said

that the Project A is more viable for the company as it has a higher Net present value.

Computation of NPV

Year Project Project PV Discounted Discounted

of the company

The use of ratio analysis is very important for the company in order to evaluate its

performance on the basis of the past year and also with other competitors. The reason pertaining

to the fact is that in case the ratios will not be evaluated in proper manner then this will result in

ineffective analysis of performance of company. Although there are many different types of

limitation as well which can affect the performance of the company and its proper analysis. The

major limitation involving the use of ratio for interpreting the performance of the company.

The main limitation which affects the interpretation of the performance of the company is

that the size of the company matters. The reason pertaining to the fact is that it is not

necessary that all the companies have same size. Hence, the comparison done of

companies belonging to different sizes will not provide a clear picture of financial

performance of the company.

Moreover, another limitation which the company faces at time of using the ratio analysis

is that this method ignores the price level changes which are being caused by the

inflation. This is pertaining to the fact that the use of ratio is based on the book value data

only and not the current prices changes.

TASK- Capital Investment Appraisal

Comparison between two projects through investment appraisal techniques

In order to compare the viability of the two projects it is important to analyse the

following investment techniques,

NPV:

Net present value is the difference between the present value of cash inflow and the

present value of cash outflow which is present over a certain time in the organization. This

method is for capital budgeting and investment planning for the analysation of the profitability of

the project investment (Lawal and et.al., 2021). For the project alpha(A) the total NPV which is

calculated is 11476 however for the project beta the calculated NPV is 8277. Thus, it can be said

that the Project A is more viable for the company as it has a higher Net present value.

Computation of NPV

Year Project Project PV Discounted Discounted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Alpha(A) Beta(B)

factor @

16% cash inflows A cash inflows B

2021 35000 12000 0.862 30172 10345

2022 36000 16000 0.743 26754 11891

2023 38000 21000 0.641 24345 13454

2024 29000 35000 0.552 16016 19330

2025 28000 46000 0.476 13331 21901

2026 22000 48000 0.410 9030 19701

Total cash

inflow 188000 178000

Total

discounted

cash inflow 89476 86277

Initial

investment 78000 78000 78000 78000

NPV (Total

discounted

cash inflows -

initial

investment) 11476 8277

Residual

Value 0 10000

IRR :

The internal rate of return is a metric which is used for the financial analysis which is

helpful for the estimation of the profitability of the organization investments. This method is

used for calculating the discount rate which makes the net present value of all cash flow equal to

zero in the discounted cash flow analysis. In the comparison of the two investments the IRR for

project B is lower suggesting that the project A is much more viable with an IRR of 46.74%.

Computation of IRR

Year Project Alpha(A) Project Beta(B)

0 -78000 -78000

1 35000 12000

2 36000 16000

3 38000 21000

4 29000 35000

5 28000 46000

6 22000 48000

Total cash inflow 188000 178000

factor @

16% cash inflows A cash inflows B

2021 35000 12000 0.862 30172 10345

2022 36000 16000 0.743 26754 11891

2023 38000 21000 0.641 24345 13454

2024 29000 35000 0.552 16016 19330

2025 28000 46000 0.476 13331 21901

2026 22000 48000 0.410 9030 19701

Total cash

inflow 188000 178000

Total

discounted

cash inflow 89476 86277

Initial

investment 78000 78000 78000 78000

NPV (Total

discounted

cash inflows -

initial

investment) 11476 8277

Residual

Value 0 10000

IRR :

The internal rate of return is a metric which is used for the financial analysis which is

helpful for the estimation of the profitability of the organization investments. This method is

used for calculating the discount rate which makes the net present value of all cash flow equal to

zero in the discounted cash flow analysis. In the comparison of the two investments the IRR for

project B is lower suggesting that the project A is much more viable with an IRR of 46.74%.

Computation of IRR

Year Project Alpha(A) Project Beta(B)

0 -78000 -78000

1 35000 12000

2 36000 16000

3 38000 21000

4 29000 35000

5 28000 46000

6 22000 48000

Total cash inflow 188000 178000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

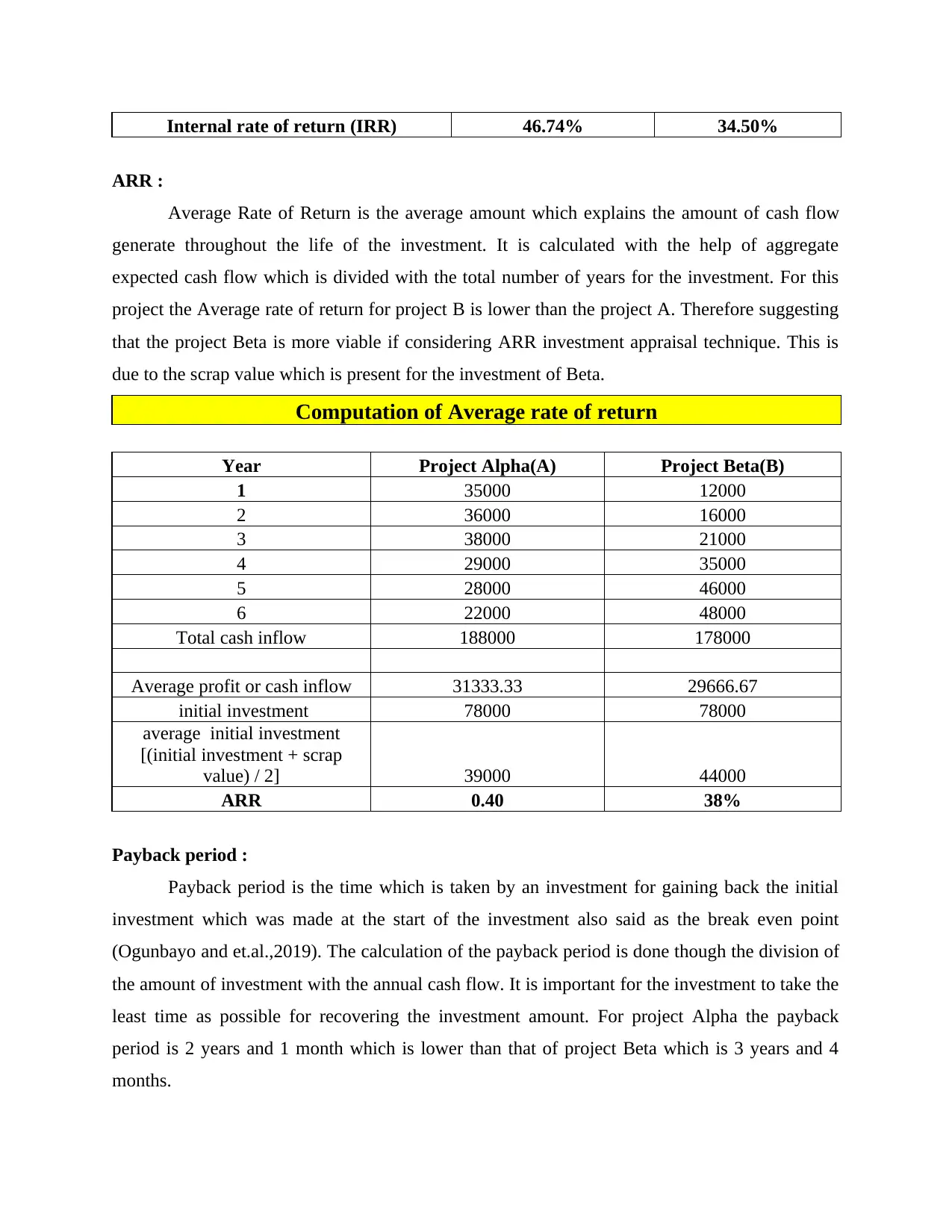

Internal rate of return (IRR) 46.74% 34.50%

ARR :

Average Rate of Return is the average amount which explains the amount of cash flow

generate throughout the life of the investment. It is calculated with the help of aggregate

expected cash flow which is divided with the total number of years for the investment. For this

project the Average rate of return for project B is lower than the project A. Therefore suggesting

that the project Beta is more viable if considering ARR investment appraisal technique. This is

due to the scrap value which is present for the investment of Beta.

Computation of Average rate of return

Year Project Alpha(A) Project Beta(B)

1 35000 12000

2 36000 16000

3 38000 21000

4 29000 35000

5 28000 46000

6 22000 48000

Total cash inflow 188000 178000

Average profit or cash inflow 31333.33 29666.67

initial investment 78000 78000

average initial investment

[(initial investment + scrap

value) / 2] 39000 44000

ARR 0.40 38%

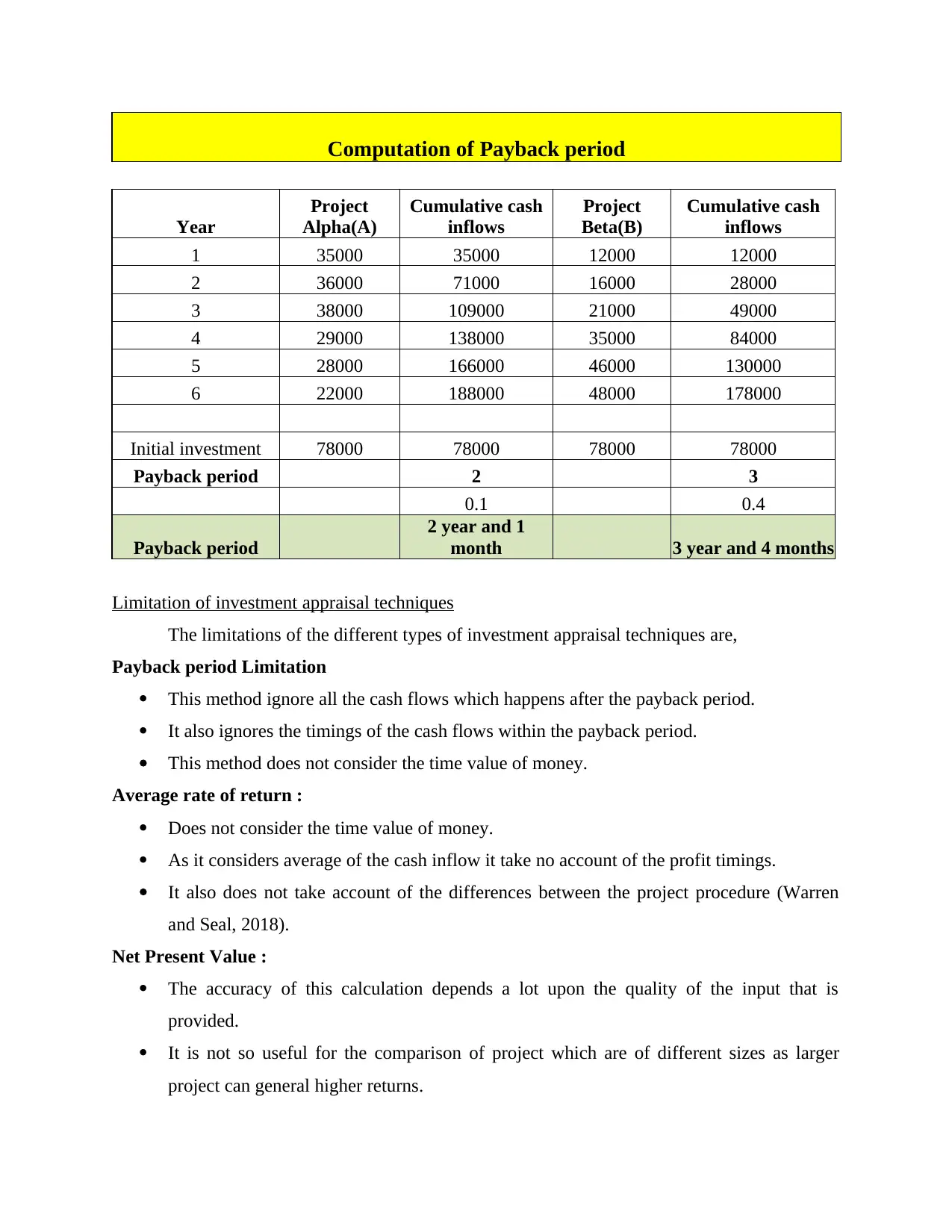

Payback period :

Payback period is the time which is taken by an investment for gaining back the initial

investment which was made at the start of the investment also said as the break even point

(Ogunbayo and et.al.,2019). The calculation of the payback period is done though the division of

the amount of investment with the annual cash flow. It is important for the investment to take the

least time as possible for recovering the investment amount. For project Alpha the payback

period is 2 years and 1 month which is lower than that of project Beta which is 3 years and 4

months.

ARR :

Average Rate of Return is the average amount which explains the amount of cash flow

generate throughout the life of the investment. It is calculated with the help of aggregate

expected cash flow which is divided with the total number of years for the investment. For this

project the Average rate of return for project B is lower than the project A. Therefore suggesting

that the project Beta is more viable if considering ARR investment appraisal technique. This is

due to the scrap value which is present for the investment of Beta.

Computation of Average rate of return

Year Project Alpha(A) Project Beta(B)

1 35000 12000

2 36000 16000

3 38000 21000

4 29000 35000

5 28000 46000

6 22000 48000

Total cash inflow 188000 178000

Average profit or cash inflow 31333.33 29666.67

initial investment 78000 78000

average initial investment

[(initial investment + scrap

value) / 2] 39000 44000

ARR 0.40 38%

Payback period :

Payback period is the time which is taken by an investment for gaining back the initial

investment which was made at the start of the investment also said as the break even point

(Ogunbayo and et.al.,2019). The calculation of the payback period is done though the division of

the amount of investment with the annual cash flow. It is important for the investment to take the

least time as possible for recovering the investment amount. For project Alpha the payback

period is 2 years and 1 month which is lower than that of project Beta which is 3 years and 4

months.

Computation of Payback period

Year

Project

Alpha(A)

Cumulative cash

inflows

Project

Beta(B)

Cumulative cash

inflows

1 35000 35000 12000 12000

2 36000 71000 16000 28000

3 38000 109000 21000 49000

4 29000 138000 35000 84000

5 28000 166000 46000 130000

6 22000 188000 48000 178000

Initial investment 78000 78000 78000 78000

Payback period 2 3

0.1 0.4

Payback period

2 year and 1

month 3 year and 4 months

Limitation of investment appraisal techniques

The limitations of the different types of investment appraisal techniques are,

Payback period Limitation

This method ignore all the cash flows which happens after the payback period.

It also ignores the timings of the cash flows within the payback period.

This method does not consider the time value of money.

Average rate of return :

Does not consider the time value of money.

As it considers average of the cash inflow it take no account of the profit timings.

It also does not take account of the differences between the project procedure (Warren

and Seal, 2018).

Net Present Value :

The accuracy of this calculation depends a lot upon the quality of the input that is

provided.

It is not so useful for the comparison of project which are of different sizes as larger

project can general higher returns.

Year

Project

Alpha(A)

Cumulative cash

inflows

Project

Beta(B)

Cumulative cash

inflows

1 35000 35000 12000 12000

2 36000 71000 16000 28000

3 38000 109000 21000 49000

4 29000 138000 35000 84000

5 28000 166000 46000 130000

6 22000 188000 48000 178000

Initial investment 78000 78000 78000 78000

Payback period 2 3

0.1 0.4

Payback period

2 year and 1

month 3 year and 4 months

Limitation of investment appraisal techniques

The limitations of the different types of investment appraisal techniques are,

Payback period Limitation

This method ignore all the cash flows which happens after the payback period.

It also ignores the timings of the cash flows within the payback period.

This method does not consider the time value of money.

Average rate of return :

Does not consider the time value of money.

As it considers average of the cash inflow it take no account of the profit timings.

It also does not take account of the differences between the project procedure (Warren

and Seal, 2018).

Net Present Value :

The accuracy of this calculation depends a lot upon the quality of the input that is

provided.

It is not so useful for the comparison of project which are of different sizes as larger

project can general higher returns.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.