Financial Performance Analysis Report: FMA Assignment, MBA

VerifiedAdded on 2022/08/09

|19

|3029

|79

Report

AI Summary

This report presents a financial analysis of three Malaysian rubber glove companies: Kossan Rubber Industries, Supermax Corporation Berhad, and Top Glove Corporation Berhad. The analysis, based on publicly available financial data, assesses the companies' performance using various financial ratios, including profitability (net profit margin, return on equity), liquidity (current ratio, quick ratio), solvency, efficiency, and market valuation (P/E ratio). The report compares the companies' performance over a period of three years, highlighting trends and identifying strengths and weaknesses. The analysis includes recommendations for investors based on the observed financial performance, suggesting Top Gloves as a strong investment choice due to its higher net profit margins and shareholder returns. The report also provides insights into the rubber glove industry landscape, emphasizing Malaysia's leading role in global exports.

Running Head: FINANCIAL ANALYSIS 1

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS

Contents

Overview.....................................................................................................................................................3

Kossar Rubber Industries.........................................................................................................................3

Supermax Corporation Berhad................................................................................................................3

Top Glove Corporation Berhad...............................................................................................................4

Measurement of financial performance.......................................................................................................5

Profitability ratios....................................................................................................................................5

Net Profit margin.................................................................................................................................5

Return on Equity..................................................................................................................................6

Liquidity ratios........................................................................................................................................7

Solvency ratios........................................................................................................................................8

Efficiency ratios......................................................................................................................................9

Market valuation....................................................................................................................................10

Recommendations and Conclusion............................................................................................................11

References.................................................................................................................................................12

Appendix...................................................................................................................................................14

Contents

Overview.....................................................................................................................................................3

Kossar Rubber Industries.........................................................................................................................3

Supermax Corporation Berhad................................................................................................................3

Top Glove Corporation Berhad...............................................................................................................4

Measurement of financial performance.......................................................................................................5

Profitability ratios....................................................................................................................................5

Net Profit margin.................................................................................................................................5

Return on Equity..................................................................................................................................6

Liquidity ratios........................................................................................................................................7

Solvency ratios........................................................................................................................................8

Efficiency ratios......................................................................................................................................9

Market valuation....................................................................................................................................10

Recommendations and Conclusion............................................................................................................11

References.................................................................................................................................................12

Appendix...................................................................................................................................................14

FINANCIAL ANALYSIS

Overview

Kossar Rubber Industries

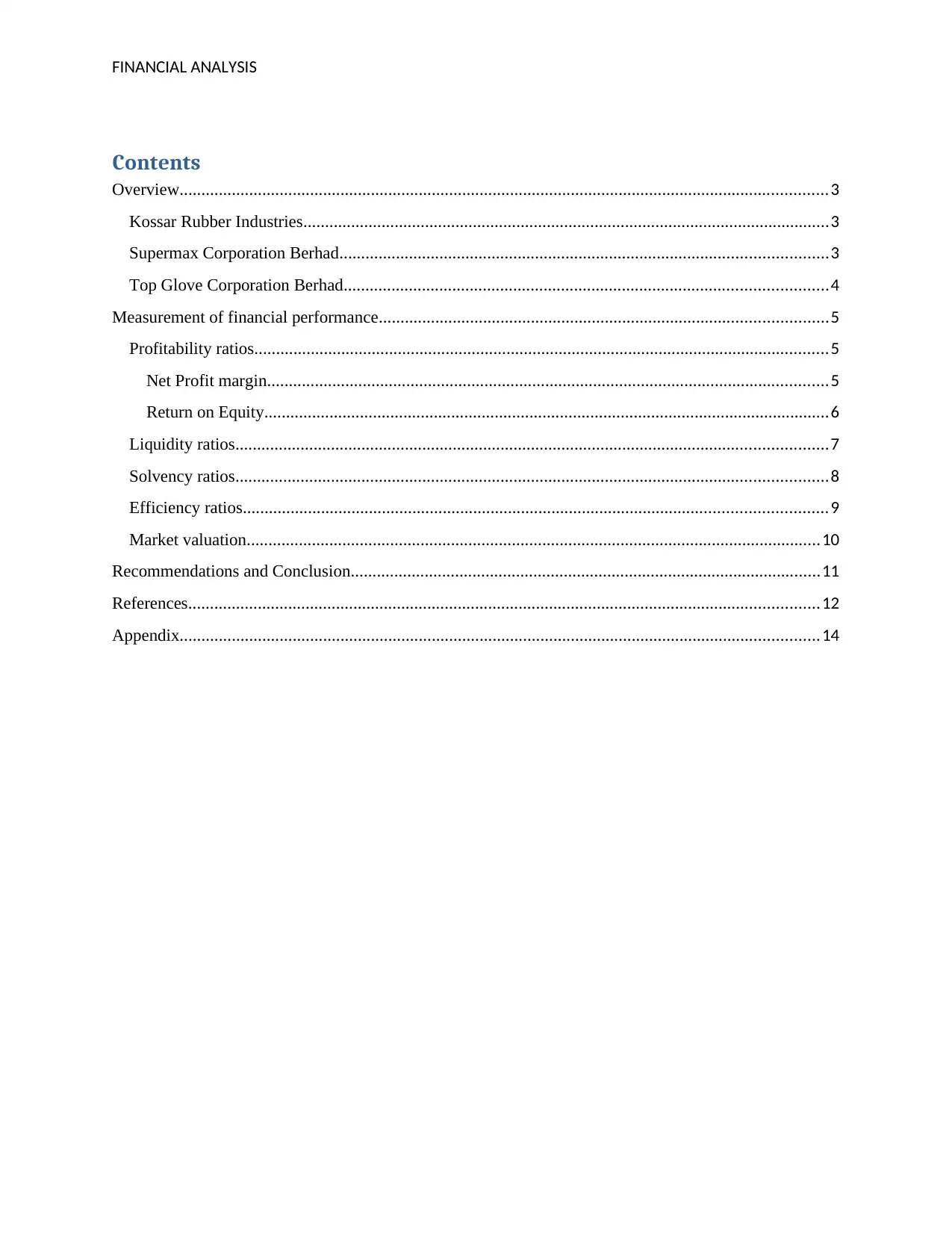

Kossan Rubber Industries or simply known as the Kossan group is one of the public companies

belonging to Malaysia and which came into existence in 1979. Initially, the company was mainly

engaged in cutlass bearing and started manufacturing globes in the year 1989. Recently the

primary activities in which the company is engaged are manufacturing, sale, and export of

rubber-based products. The headquarters of the company is situated in Malaysia. Dato Lim

Kuang Sia was the key person who brought this company into existence. The company has a

team of over 6000 employees and with them, the services and goods are being exported to 180

countries worldwide. The current revenue of the company is RM 21450571 it saw an increase

along with the profits RM 204599 (Kossar Rubber Industries, 2018).

(Source: Kossar Rubber Industries, 2018).

Overview

Kossar Rubber Industries

Kossan Rubber Industries or simply known as the Kossan group is one of the public companies

belonging to Malaysia and which came into existence in 1979. Initially, the company was mainly

engaged in cutlass bearing and started manufacturing globes in the year 1989. Recently the

primary activities in which the company is engaged are manufacturing, sale, and export of

rubber-based products. The headquarters of the company is situated in Malaysia. Dato Lim

Kuang Sia was the key person who brought this company into existence. The company has a

team of over 6000 employees and with them, the services and goods are being exported to 180

countries worldwide. The current revenue of the company is RM 21450571 it saw an increase

along with the profits RM 204599 (Kossar Rubber Industries, 2018).

(Source: Kossar Rubber Industries, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS

Supermax Corporation Berhad

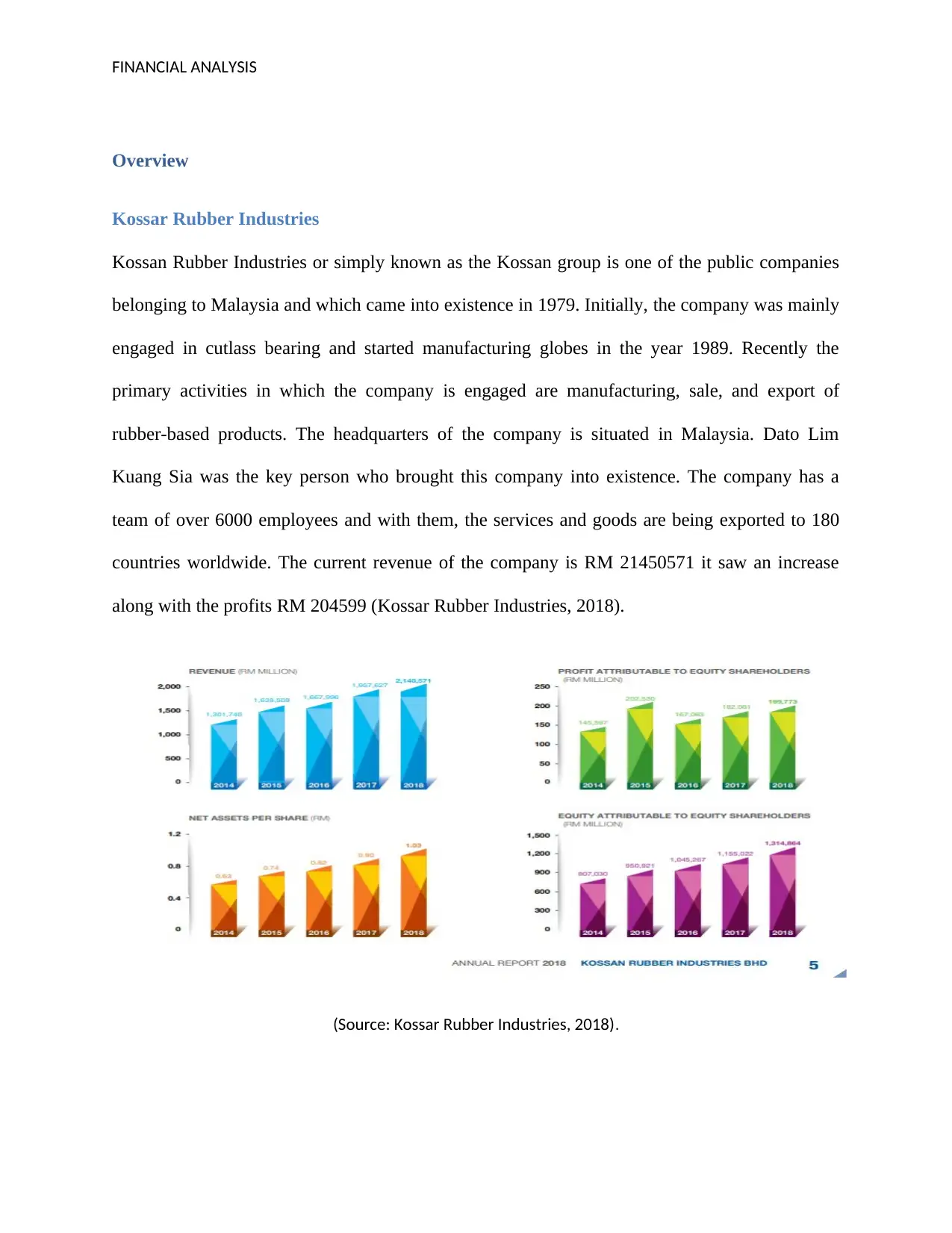

Supermax Corporation Berhad began as a dealer and exporter of latex gloves since the year 1987

preceding wandering into the line of manufacturing in 1989. It is Malaysia's biggest Own Brand

Manufacturer and the world's second-biggest maker of elastic gloves. Supermax has prevailed

with regards to setting up its brands with a solid existence in Canada, the U.S., the United

Kingdom, and Brazil. Practically 100% of its creation is sent out to clinical and dental

purchasers. This publicly-traded company has a revenue of RM 1304460 with a net profit of RM

161894. Over 5 years not much has increased as can be observed from the table below. Mr.

Albert Saychuan Cheok, the chairperson of the company is the key person, driving the company

towards the new medium in the market (Supermax Industries, 2018).

(Source: Supermax Industries, 2018).

Top Glove Corporation Berhad

Top Glove Corporation Berhad is a rubber glove manufacturer company situated in Malaysia.

Not restricted to just Malaysia, the company has also expanded its operations till the United

States, Germany, and Brazil. Founded in the year 1991 as a business venture with 1 glove

production line and 100 staff members the company has reached a team of 18000 employees.

Supermax Corporation Berhad

Supermax Corporation Berhad began as a dealer and exporter of latex gloves since the year 1987

preceding wandering into the line of manufacturing in 1989. It is Malaysia's biggest Own Brand

Manufacturer and the world's second-biggest maker of elastic gloves. Supermax has prevailed

with regards to setting up its brands with a solid existence in Canada, the U.S., the United

Kingdom, and Brazil. Practically 100% of its creation is sent out to clinical and dental

purchasers. This publicly-traded company has a revenue of RM 1304460 with a net profit of RM

161894. Over 5 years not much has increased as can be observed from the table below. Mr.

Albert Saychuan Cheok, the chairperson of the company is the key person, driving the company

towards the new medium in the market (Supermax Industries, 2018).

(Source: Supermax Industries, 2018).

Top Glove Corporation Berhad

Top Glove Corporation Berhad is a rubber glove manufacturer company situated in Malaysia.

Not restricted to just Malaysia, the company has also expanded its operations till the United

States, Germany, and Brazil. Founded in the year 1991 as a business venture with 1 glove

production line and 100 staff members the company has reached a team of 18000 employees.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS

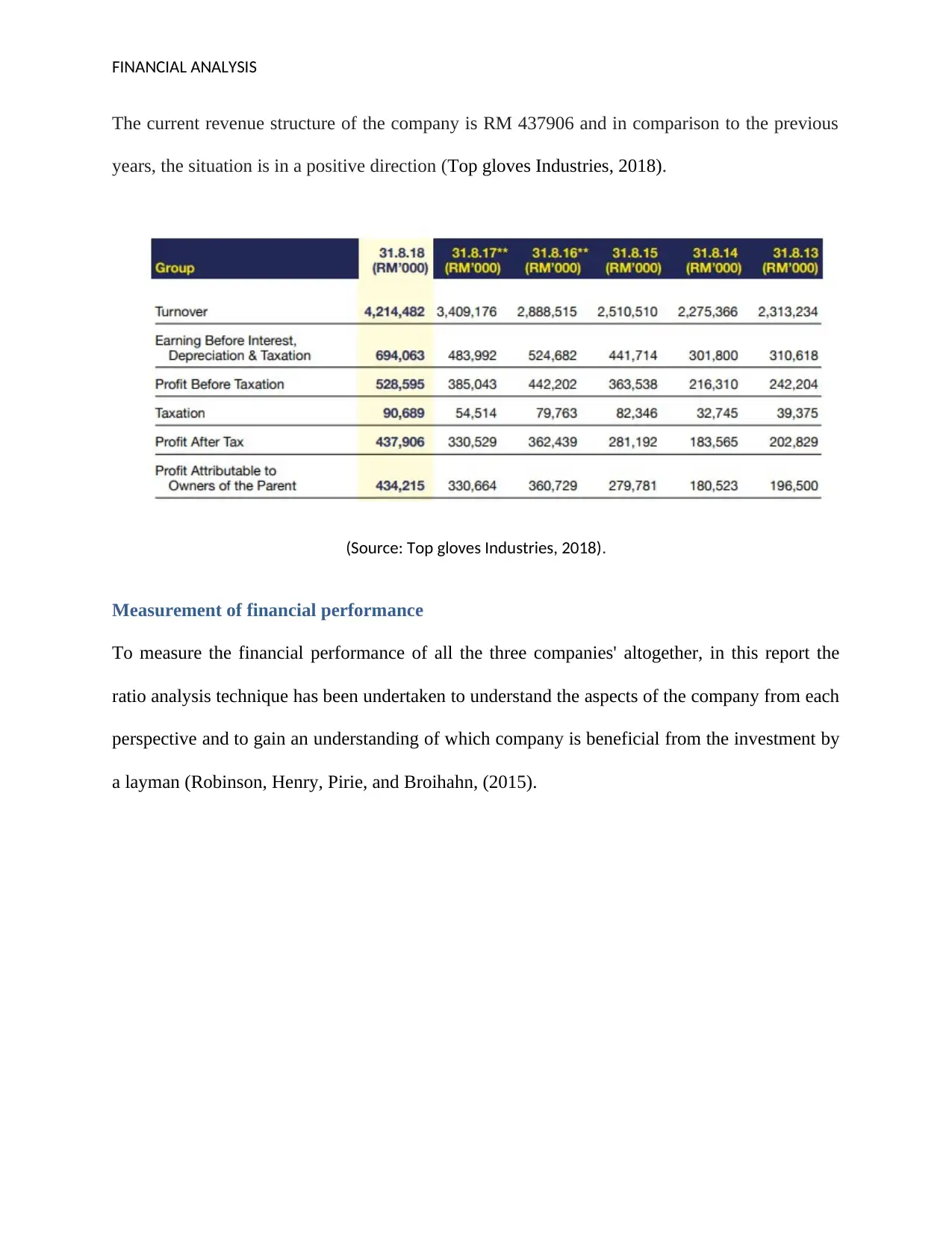

The current revenue structure of the company is RM 437906 and in comparison to the previous

years, the situation is in a positive direction (Top gloves Industries, 2018).

(Source: Top gloves Industries, 2018).

Measurement of financial performance

To measure the financial performance of all the three companies' altogether, in this report the

ratio analysis technique has been undertaken to understand the aspects of the company from each

perspective and to gain an understanding of which company is beneficial from the investment by

a layman (Robinson, Henry, Pirie, and Broihahn, (2015).

The current revenue structure of the company is RM 437906 and in comparison to the previous

years, the situation is in a positive direction (Top gloves Industries, 2018).

(Source: Top gloves Industries, 2018).

Measurement of financial performance

To measure the financial performance of all the three companies' altogether, in this report the

ratio analysis technique has been undertaken to understand the aspects of the company from each

perspective and to gain an understanding of which company is beneficial from the investment by

a layman (Robinson, Henry, Pirie, and Broihahn, (2015).

FINANCIAL ANALYSIS

Profitability ratios

Net Profit margin

2016 2017 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Net Profit Margin

Net Profit %

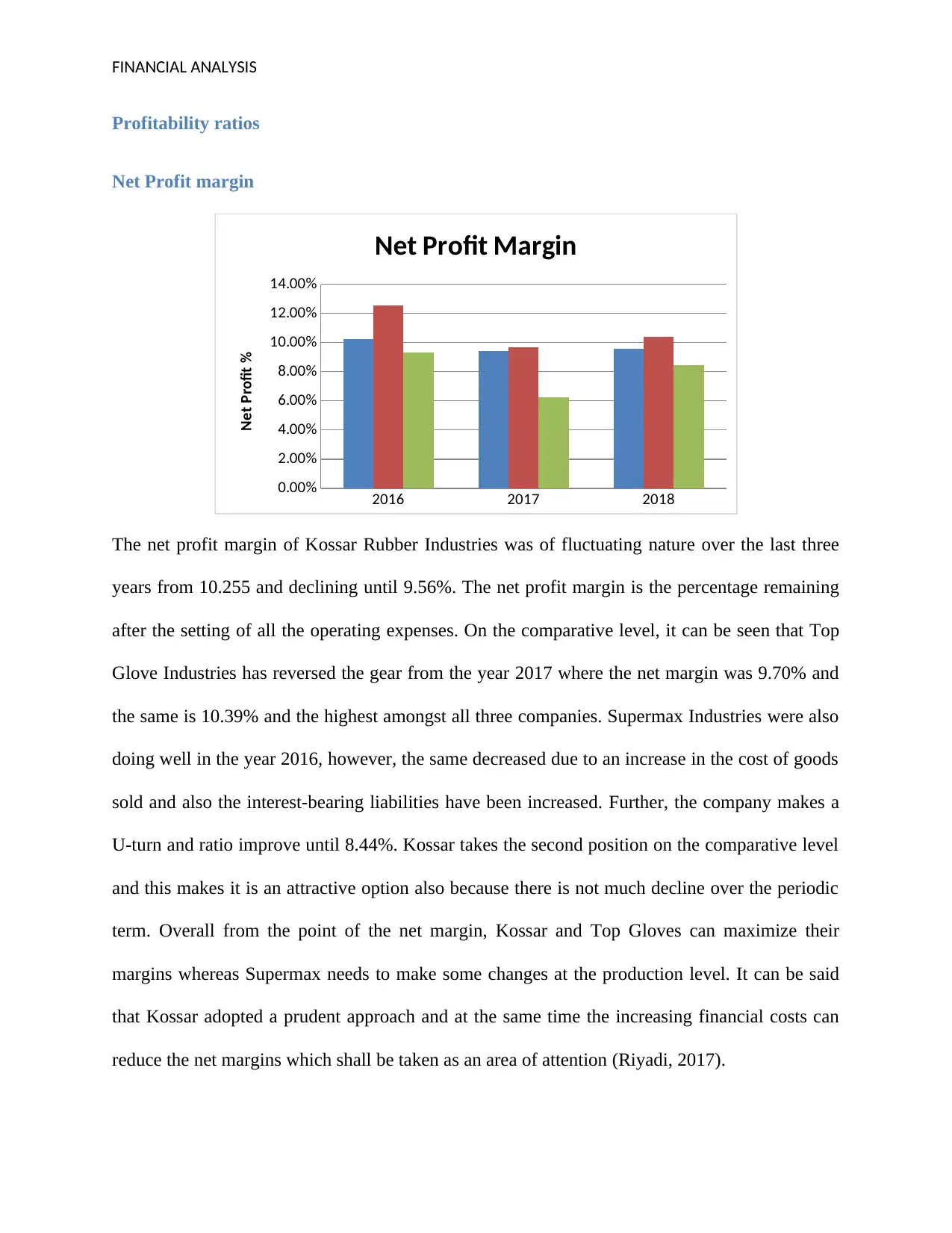

The net profit margin of Kossar Rubber Industries was of fluctuating nature over the last three

years from 10.255 and declining until 9.56%. The net profit margin is the percentage remaining

after the setting of all the operating expenses. On the comparative level, it can be seen that Top

Glove Industries has reversed the gear from the year 2017 where the net margin was 9.70% and

the same is 10.39% and the highest amongst all three companies. Supermax Industries were also

doing well in the year 2016, however, the same decreased due to an increase in the cost of goods

sold and also the interest-bearing liabilities have been increased. Further, the company makes a

U-turn and ratio improve until 8.44%. Kossar takes the second position on the comparative level

and this makes it is an attractive option also because there is not much decline over the periodic

term. Overall from the point of the net margin, Kossar and Top Gloves can maximize their

margins whereas Supermax needs to make some changes at the production level. It can be said

that Kossar adopted a prudent approach and at the same time the increasing financial costs can

reduce the net margins which shall be taken as an area of attention (Riyadi, 2017).

Profitability ratios

Net Profit margin

2016 2017 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Net Profit Margin

Net Profit %

The net profit margin of Kossar Rubber Industries was of fluctuating nature over the last three

years from 10.255 and declining until 9.56%. The net profit margin is the percentage remaining

after the setting of all the operating expenses. On the comparative level, it can be seen that Top

Glove Industries has reversed the gear from the year 2017 where the net margin was 9.70% and

the same is 10.39% and the highest amongst all three companies. Supermax Industries were also

doing well in the year 2016, however, the same decreased due to an increase in the cost of goods

sold and also the interest-bearing liabilities have been increased. Further, the company makes a

U-turn and ratio improve until 8.44%. Kossar takes the second position on the comparative level

and this makes it is an attractive option also because there is not much decline over the periodic

term. Overall from the point of the net margin, Kossar and Top Gloves can maximize their

margins whereas Supermax needs to make some changes at the production level. It can be said

that Kossar adopted a prudent approach and at the same time the increasing financial costs can

reduce the net margins which shall be taken as an area of attention (Riyadi, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS

Return on Equity

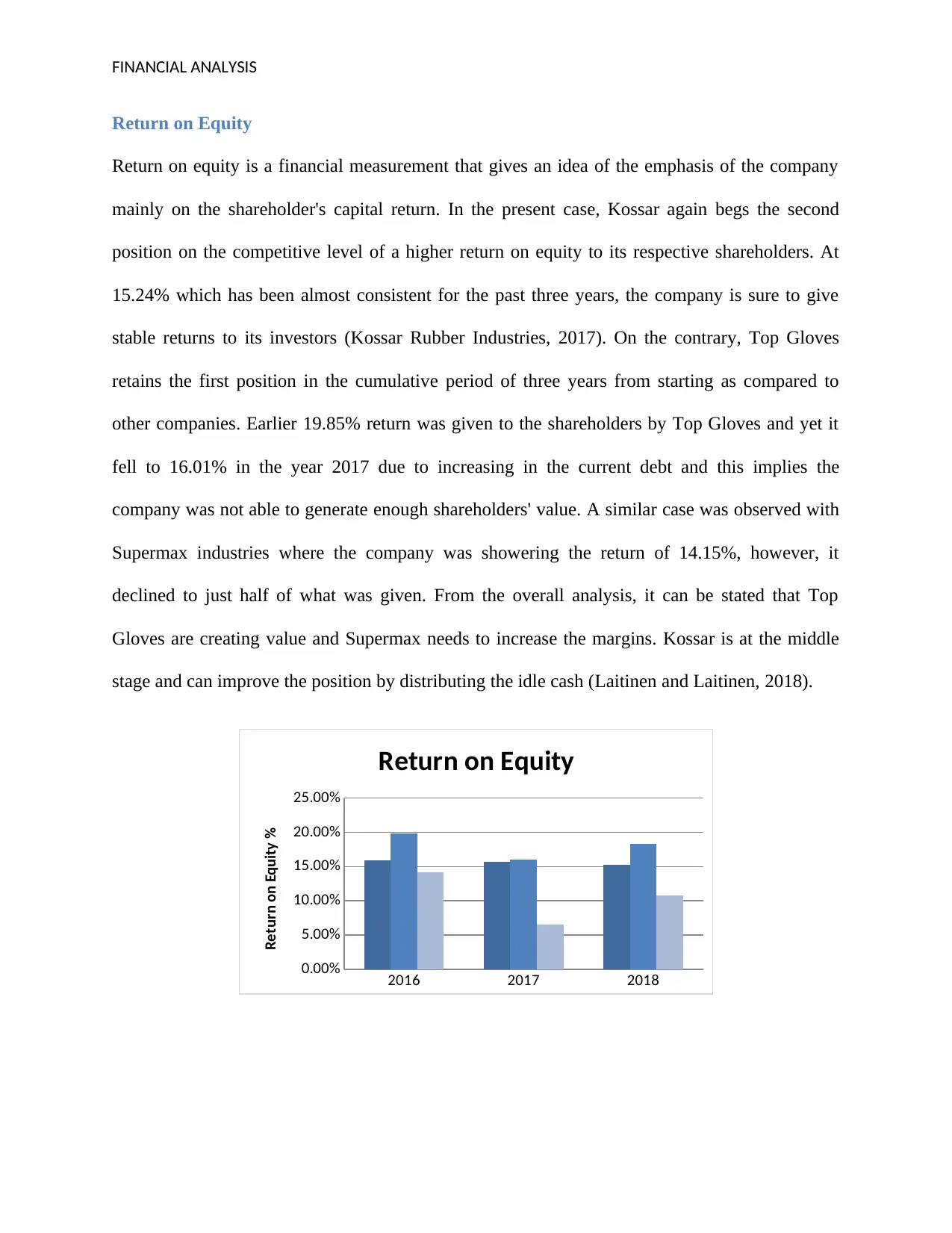

Return on equity is a financial measurement that gives an idea of the emphasis of the company

mainly on the shareholder's capital return. In the present case, Kossar again begs the second

position on the competitive level of a higher return on equity to its respective shareholders. At

15.24% which has been almost consistent for the past three years, the company is sure to give

stable returns to its investors (Kossar Rubber Industries, 2017). On the contrary, Top Gloves

retains the first position in the cumulative period of three years from starting as compared to

other companies. Earlier 19.85% return was given to the shareholders by Top Gloves and yet it

fell to 16.01% in the year 2017 due to increasing in the current debt and this implies the

company was not able to generate enough shareholders' value. A similar case was observed with

Supermax industries where the company was showering the return of 14.15%, however, it

declined to just half of what was given. From the overall analysis, it can be stated that Top

Gloves are creating value and Supermax needs to increase the margins. Kossar is at the middle

stage and can improve the position by distributing the idle cash (Laitinen and Laitinen, 2018).

2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return on Equity

Return on Equity %

Return on Equity

Return on equity is a financial measurement that gives an idea of the emphasis of the company

mainly on the shareholder's capital return. In the present case, Kossar again begs the second

position on the competitive level of a higher return on equity to its respective shareholders. At

15.24% which has been almost consistent for the past three years, the company is sure to give

stable returns to its investors (Kossar Rubber Industries, 2017). On the contrary, Top Gloves

retains the first position in the cumulative period of three years from starting as compared to

other companies. Earlier 19.85% return was given to the shareholders by Top Gloves and yet it

fell to 16.01% in the year 2017 due to increasing in the current debt and this implies the

company was not able to generate enough shareholders' value. A similar case was observed with

Supermax industries where the company was showering the return of 14.15%, however, it

declined to just half of what was given. From the overall analysis, it can be stated that Top

Gloves are creating value and Supermax needs to increase the margins. Kossar is at the middle

stage and can improve the position by distributing the idle cash (Laitinen and Laitinen, 2018).

2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return on Equity

Return on Equity %

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS

Liquidity ratios

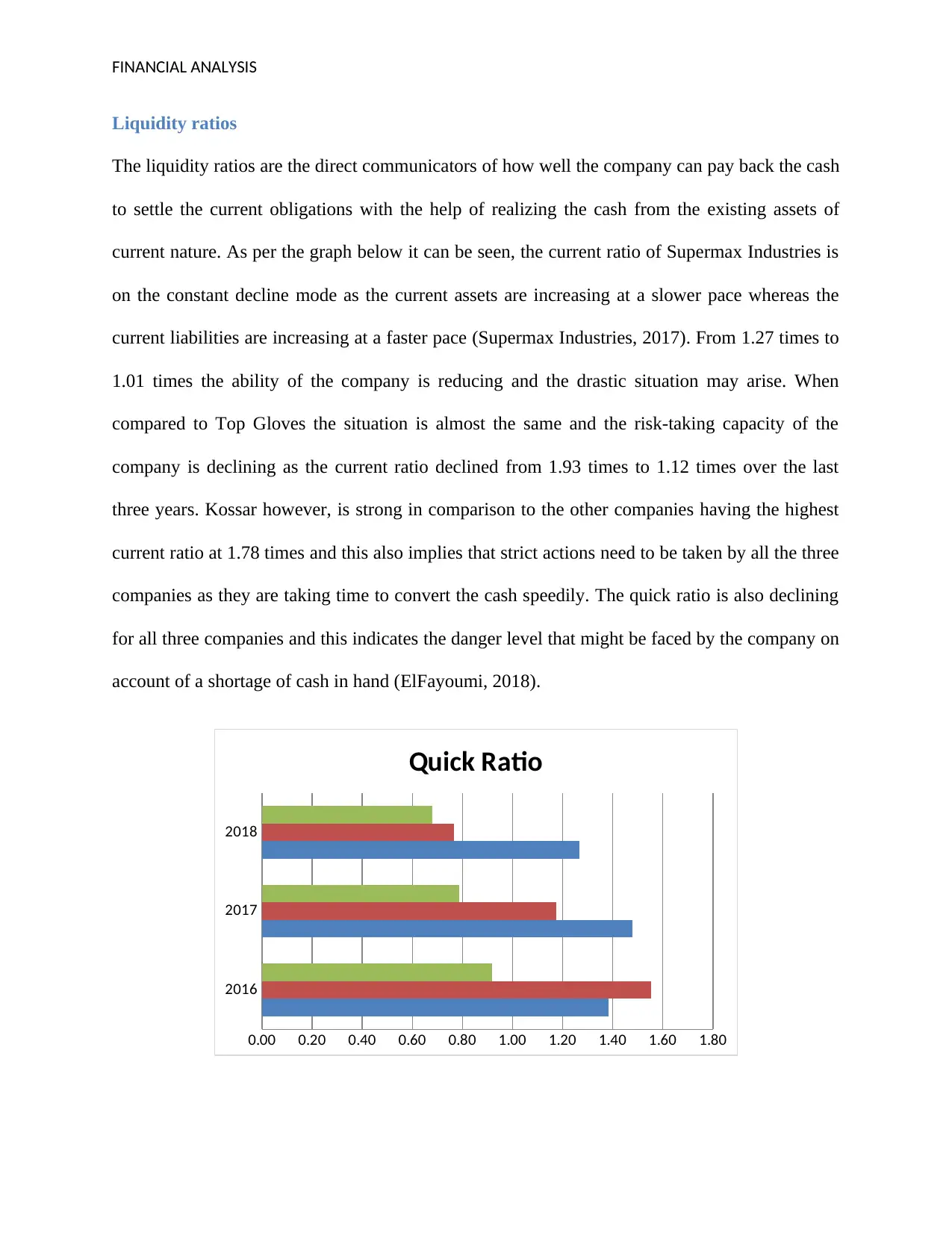

The liquidity ratios are the direct communicators of how well the company can pay back the cash

to settle the current obligations with the help of realizing the cash from the existing assets of

current nature. As per the graph below it can be seen, the current ratio of Supermax Industries is

on the constant decline mode as the current assets are increasing at a slower pace whereas the

current liabilities are increasing at a faster pace (Supermax Industries, 2017). From 1.27 times to

1.01 times the ability of the company is reducing and the drastic situation may arise. When

compared to Top Gloves the situation is almost the same and the risk-taking capacity of the

company is declining as the current ratio declined from 1.93 times to 1.12 times over the last

three years. Kossar however, is strong in comparison to the other companies having the highest

current ratio at 1.78 times and this also implies that strict actions need to be taken by all the three

companies as they are taking time to convert the cash speedily. The quick ratio is also declining

for all three companies and this indicates the danger level that might be faced by the company on

account of a shortage of cash in hand (ElFayoumi, 2018).

2016

2017

2018

0.00 0.20 0.40 0.60 0.80 1.00 1.20 1.40 1.60 1.80

Quick Ratio

Liquidity ratios

The liquidity ratios are the direct communicators of how well the company can pay back the cash

to settle the current obligations with the help of realizing the cash from the existing assets of

current nature. As per the graph below it can be seen, the current ratio of Supermax Industries is

on the constant decline mode as the current assets are increasing at a slower pace whereas the

current liabilities are increasing at a faster pace (Supermax Industries, 2017). From 1.27 times to

1.01 times the ability of the company is reducing and the drastic situation may arise. When

compared to Top Gloves the situation is almost the same and the risk-taking capacity of the

company is declining as the current ratio declined from 1.93 times to 1.12 times over the last

three years. Kossar however, is strong in comparison to the other companies having the highest

current ratio at 1.78 times and this also implies that strict actions need to be taken by all the three

companies as they are taking time to convert the cash speedily. The quick ratio is also declining

for all three companies and this indicates the danger level that might be faced by the company on

account of a shortage of cash in hand (ElFayoumi, 2018).

2016

2017

2018

0.00 0.20 0.40 0.60 0.80 1.00 1.20 1.40 1.60 1.80

Quick Ratio

FINANCIAL ANALYSIS

2016

2017

2018

0.00 0.50 1.00 1.50 2.00 2.50

Current Ratio

Solvency ratios

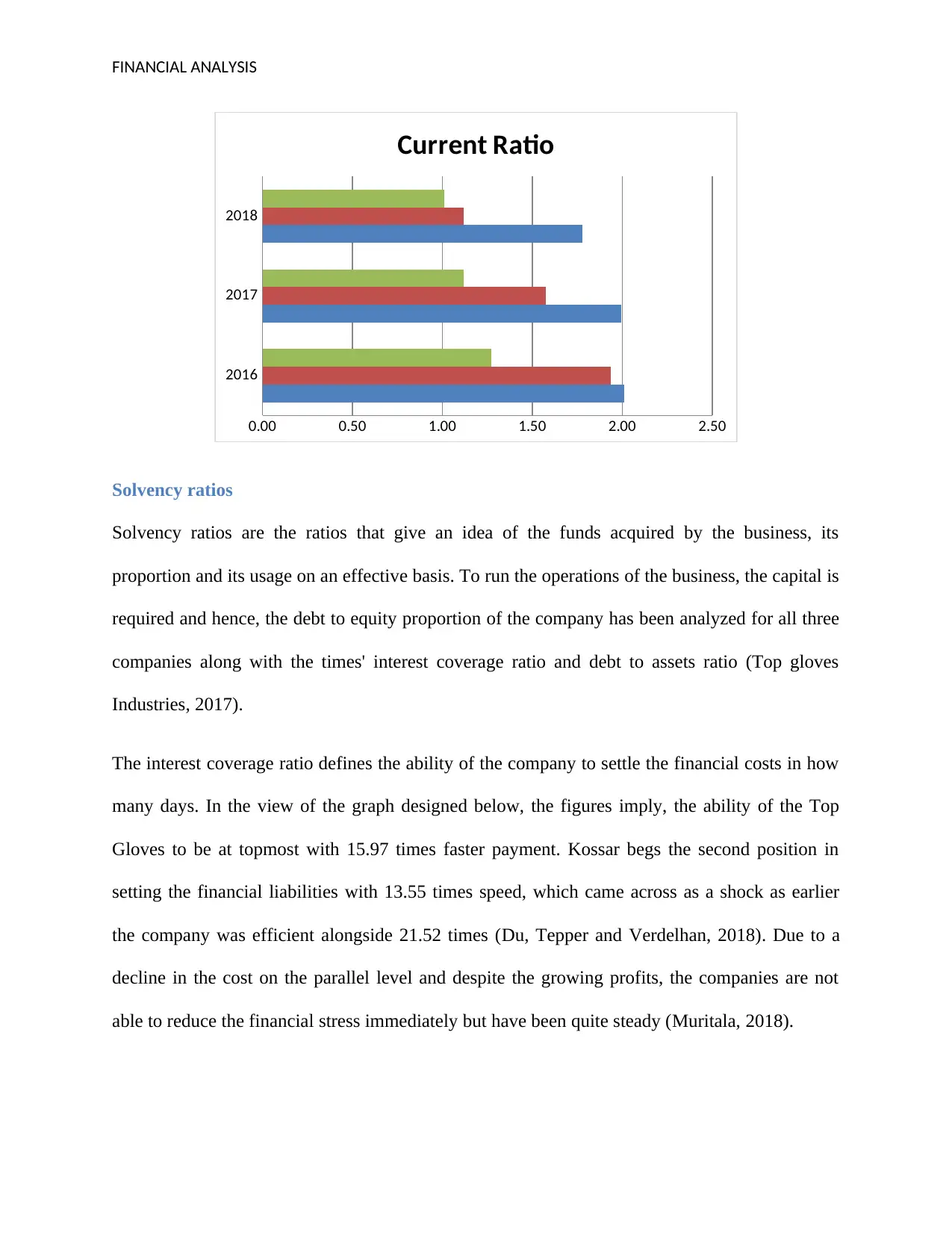

Solvency ratios are the ratios that give an idea of the funds acquired by the business, its

proportion and its usage on an effective basis. To run the operations of the business, the capital is

required and hence, the debt to equity proportion of the company has been analyzed for all three

companies along with the times' interest coverage ratio and debt to assets ratio (Top gloves

Industries, 2017).

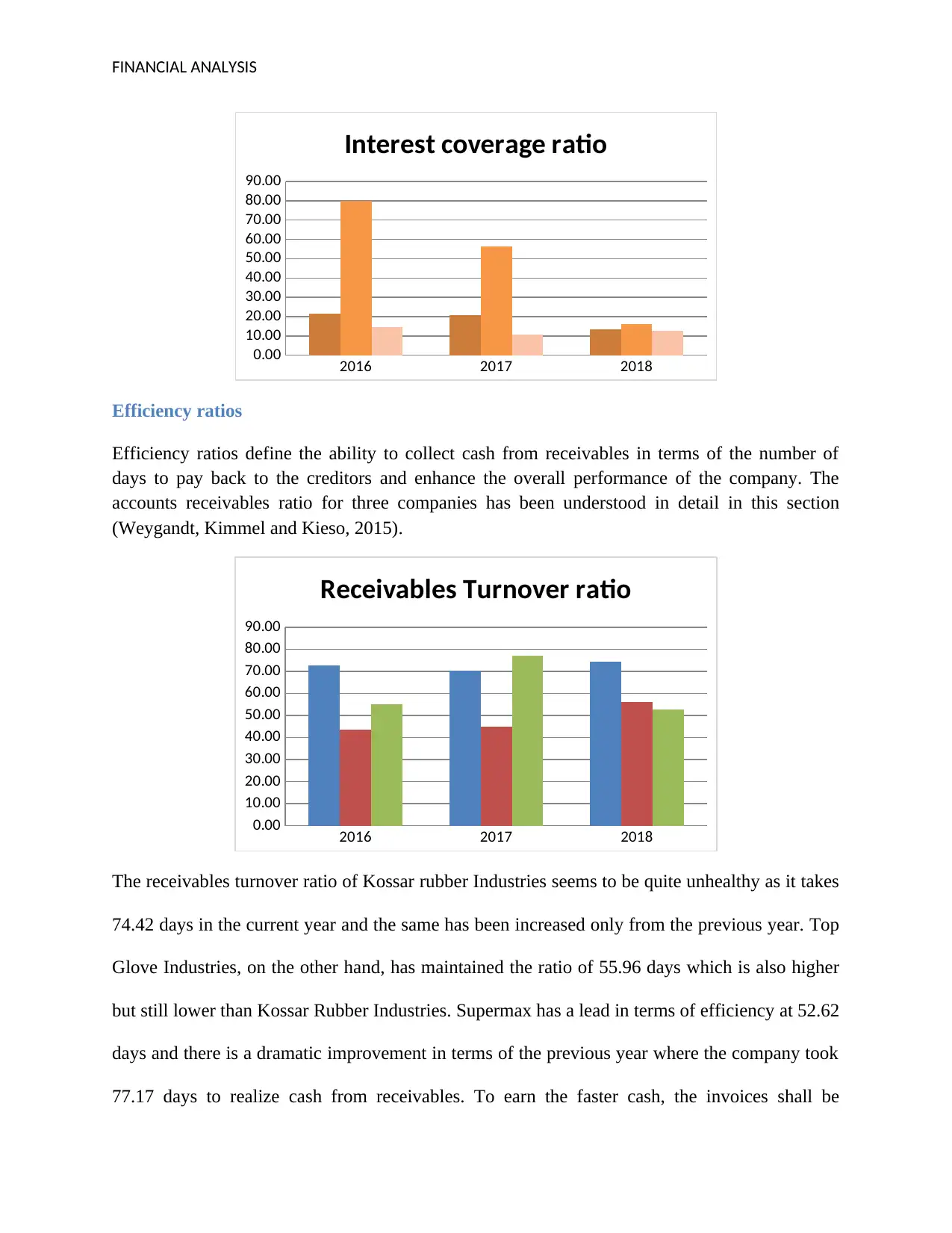

The interest coverage ratio defines the ability of the company to settle the financial costs in how

many days. In the view of the graph designed below, the figures imply, the ability of the Top

Gloves to be at topmost with 15.97 times faster payment. Kossar begs the second position in

setting the financial liabilities with 13.55 times speed, which came across as a shock as earlier

the company was efficient alongside 21.52 times (Du, Tepper and Verdelhan, 2018). Due to a

decline in the cost on the parallel level and despite the growing profits, the companies are not

able to reduce the financial stress immediately but have been quite steady (Muritala, 2018).

2016

2017

2018

0.00 0.50 1.00 1.50 2.00 2.50

Current Ratio

Solvency ratios

Solvency ratios are the ratios that give an idea of the funds acquired by the business, its

proportion and its usage on an effective basis. To run the operations of the business, the capital is

required and hence, the debt to equity proportion of the company has been analyzed for all three

companies along with the times' interest coverage ratio and debt to assets ratio (Top gloves

Industries, 2017).

The interest coverage ratio defines the ability of the company to settle the financial costs in how

many days. In the view of the graph designed below, the figures imply, the ability of the Top

Gloves to be at topmost with 15.97 times faster payment. Kossar begs the second position in

setting the financial liabilities with 13.55 times speed, which came across as a shock as earlier

the company was efficient alongside 21.52 times (Du, Tepper and Verdelhan, 2018). Due to a

decline in the cost on the parallel level and despite the growing profits, the companies are not

able to reduce the financial stress immediately but have been quite steady (Muritala, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS

2016 2017 2018

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

Interest coverage ratio

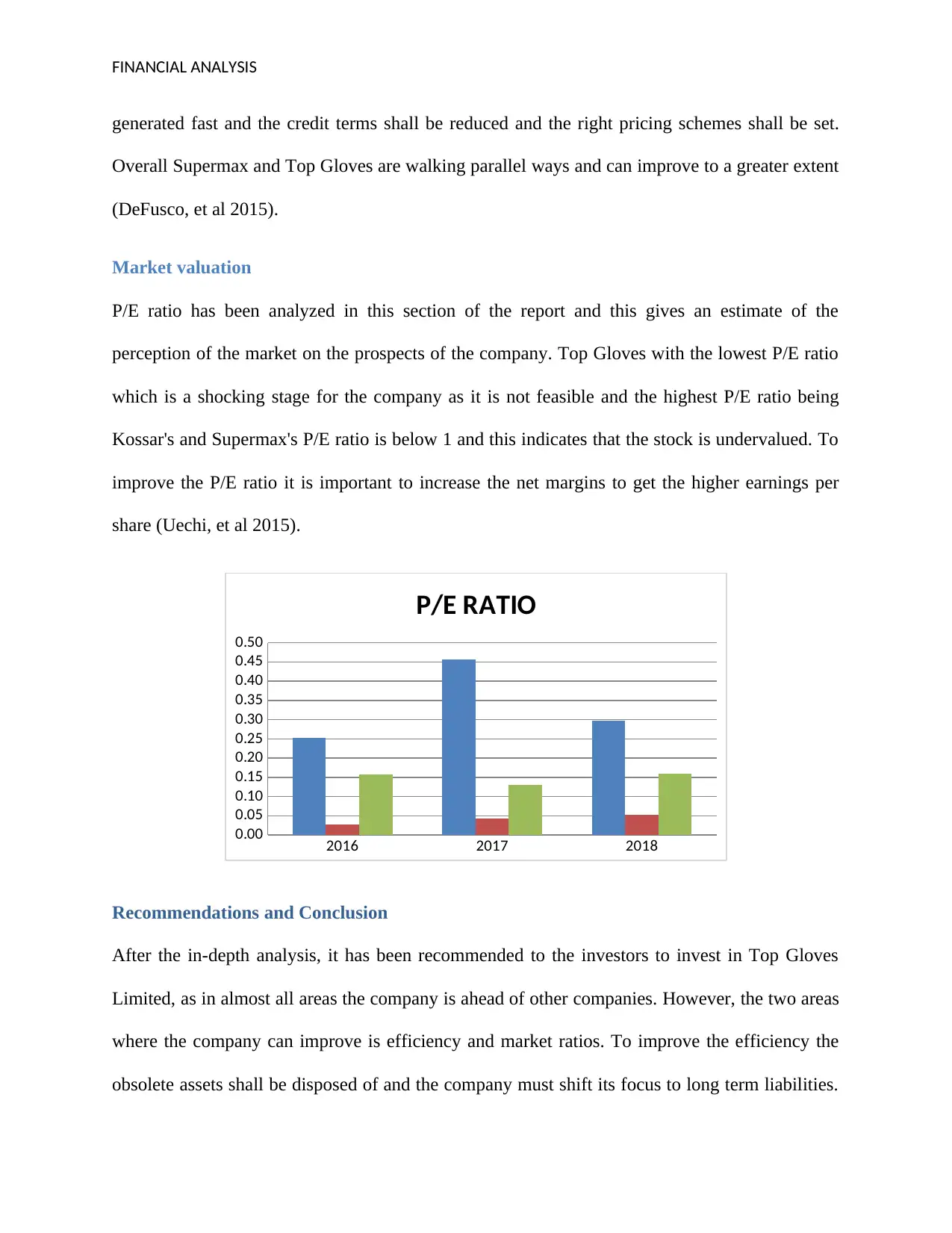

Efficiency ratios

Efficiency ratios define the ability to collect cash from receivables in terms of the number of

days to pay back to the creditors and enhance the overall performance of the company. The

accounts receivables ratio for three companies has been understood in detail in this section

(Weygandt, Kimmel and Kieso, 2015).

2016 2017 2018

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

Receivables Turnover ratio

The receivables turnover ratio of Kossar rubber Industries seems to be quite unhealthy as it takes

74.42 days in the current year and the same has been increased only from the previous year. Top

Glove Industries, on the other hand, has maintained the ratio of 55.96 days which is also higher

but still lower than Kossar Rubber Industries. Supermax has a lead in terms of efficiency at 52.62

days and there is a dramatic improvement in terms of the previous year where the company took

77.17 days to realize cash from receivables. To earn the faster cash, the invoices shall be

2016 2017 2018

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

Interest coverage ratio

Efficiency ratios

Efficiency ratios define the ability to collect cash from receivables in terms of the number of

days to pay back to the creditors and enhance the overall performance of the company. The

accounts receivables ratio for three companies has been understood in detail in this section

(Weygandt, Kimmel and Kieso, 2015).

2016 2017 2018

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

Receivables Turnover ratio

The receivables turnover ratio of Kossar rubber Industries seems to be quite unhealthy as it takes

74.42 days in the current year and the same has been increased only from the previous year. Top

Glove Industries, on the other hand, has maintained the ratio of 55.96 days which is also higher

but still lower than Kossar Rubber Industries. Supermax has a lead in terms of efficiency at 52.62

days and there is a dramatic improvement in terms of the previous year where the company took

77.17 days to realize cash from receivables. To earn the faster cash, the invoices shall be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS

generated fast and the credit terms shall be reduced and the right pricing schemes shall be set.

Overall Supermax and Top Gloves are walking parallel ways and can improve to a greater extent

(DeFusco, et al 2015).

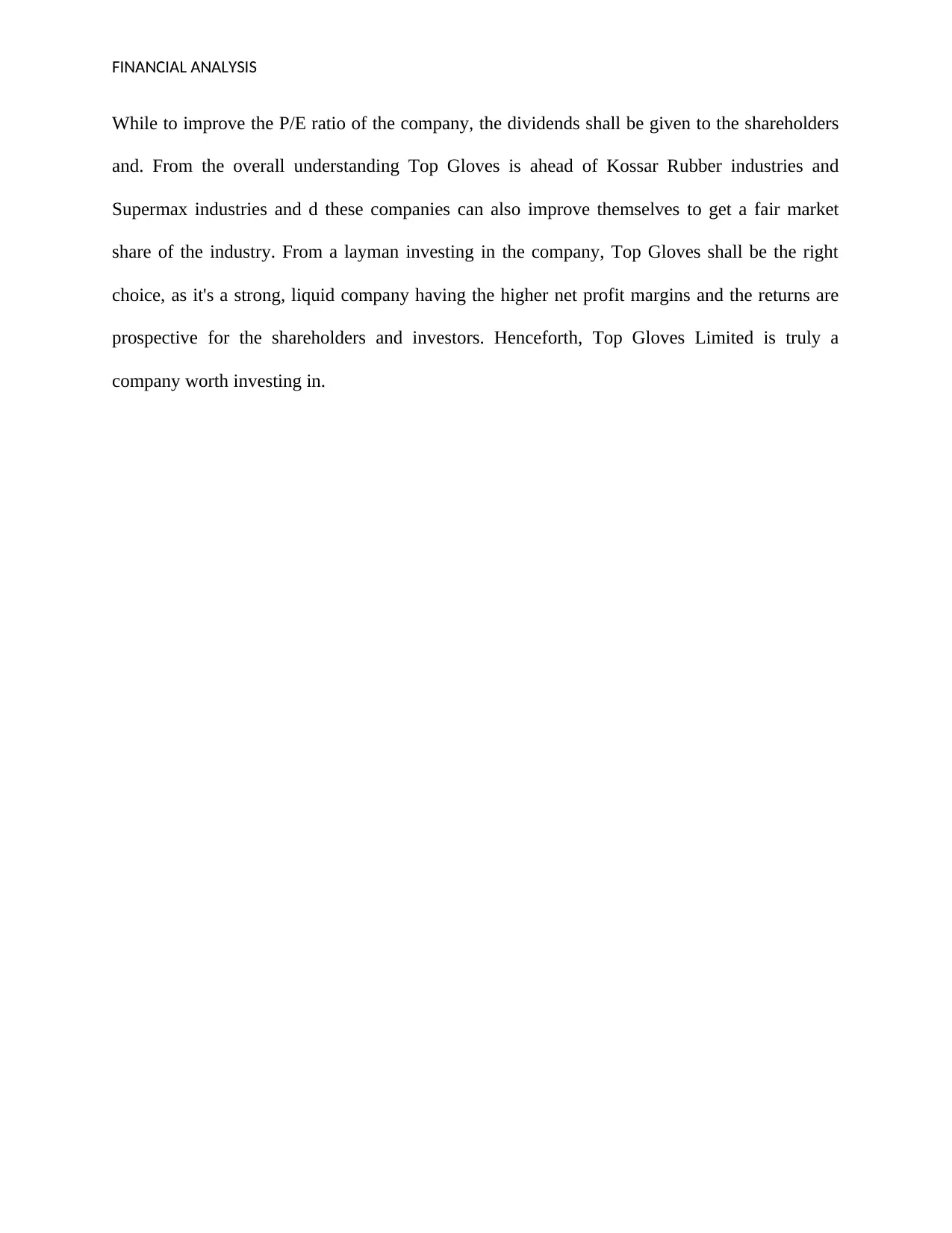

Market valuation

P/E ratio has been analyzed in this section of the report and this gives an estimate of the

perception of the market on the prospects of the company. Top Gloves with the lowest P/E ratio

which is a shocking stage for the company as it is not feasible and the highest P/E ratio being

Kossar's and Supermax's P/E ratio is below 1 and this indicates that the stock is undervalued. To

improve the P/E ratio it is important to increase the net margins to get the higher earnings per

share (Uechi, et al 2015).

2016 2017 2018

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

P/E RATIO

Recommendations and Conclusion

After the in-depth analysis, it has been recommended to the investors to invest in Top Gloves

Limited, as in almost all areas the company is ahead of other companies. However, the two areas

where the company can improve is efficiency and market ratios. To improve the efficiency the

obsolete assets shall be disposed of and the company must shift its focus to long term liabilities.

generated fast and the credit terms shall be reduced and the right pricing schemes shall be set.

Overall Supermax and Top Gloves are walking parallel ways and can improve to a greater extent

(DeFusco, et al 2015).

Market valuation

P/E ratio has been analyzed in this section of the report and this gives an estimate of the

perception of the market on the prospects of the company. Top Gloves with the lowest P/E ratio

which is a shocking stage for the company as it is not feasible and the highest P/E ratio being

Kossar's and Supermax's P/E ratio is below 1 and this indicates that the stock is undervalued. To

improve the P/E ratio it is important to increase the net margins to get the higher earnings per

share (Uechi, et al 2015).

2016 2017 2018

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

P/E RATIO

Recommendations and Conclusion

After the in-depth analysis, it has been recommended to the investors to invest in Top Gloves

Limited, as in almost all areas the company is ahead of other companies. However, the two areas

where the company can improve is efficiency and market ratios. To improve the efficiency the

obsolete assets shall be disposed of and the company must shift its focus to long term liabilities.

FINANCIAL ANALYSIS

While to improve the P/E ratio of the company, the dividends shall be given to the shareholders

and. From the overall understanding Top Gloves is ahead of Kossar Rubber industries and

Supermax industries and d these companies can also improve themselves to get a fair market

share of the industry. From a layman investing in the company, Top Gloves shall be the right

choice, as it's a strong, liquid company having the higher net profit margins and the returns are

prospective for the shareholders and investors. Henceforth, Top Gloves Limited is truly a

company worth investing in.

While to improve the P/E ratio of the company, the dividends shall be given to the shareholders

and. From the overall understanding Top Gloves is ahead of Kossar Rubber industries and

Supermax industries and d these companies can also improve themselves to get a fair market

share of the industry. From a layman investing in the company, Top Gloves shall be the right

choice, as it's a strong, liquid company having the higher net profit margins and the returns are

prospective for the shareholders and investors. Henceforth, Top Gloves Limited is truly a

company worth investing in.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.