Analysis of TAN Plc's Financial Statements and Cash Flow Management

VerifiedAdded on 2023/06/10

|11

|2104

|252

Report

AI Summary

This report presents a comprehensive financial analysis of TAN Plc, encompassing the preparation of an income statement and balance sheet for the year ended December 31, 2021, along with detailed ratio calculations, including profitability, liquidity, and efficiency ratios. The analysis offers insights into the company's financial performance and provides advice to current and potential shareholders based on these results. Furthermore, the report includes a six-month cash budget from October 2022 to March 2023, along with strategic recommendations for AMF Ltd's management to effectively manage cash flow during this period. The report leverages financial data to evaluate the company's financial health, offering valuable perspectives on its performance and potential for future growth. The report also provides a summary of the references used to support the analysis and recommendations.

MSC Accounting and Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 2........................................................................................................................................3

(a) Preparation of Income statement and balance sheet TAN Plc as at 31st December, 2021.....3

(b) Ratio Calculations..................................................................................................................4

(c) Advise to current and potential shareholders of TAN Plc on its financial ratio results.........5

Question 3........................................................................................................................................7

(a) Preparation of cash budget of six months from October 2022 to March 2023......................7

(b) Advise to management of AMF Ltd on strategies they need to adopt in order to properly

manage cash flow from period October 2022 to March 2023.....................................................8

REFERENCES................................................................................................................................1

Question 2........................................................................................................................................3

(a) Preparation of Income statement and balance sheet TAN Plc as at 31st December, 2021.....3

(b) Ratio Calculations..................................................................................................................4

(c) Advise to current and potential shareholders of TAN Plc on its financial ratio results.........5

Question 3........................................................................................................................................7

(a) Preparation of cash budget of six months from October 2022 to March 2023......................7

(b) Advise to management of AMF Ltd on strategies they need to adopt in order to properly

manage cash flow from period October 2022 to March 2023.....................................................8

REFERENCES................................................................................................................................1

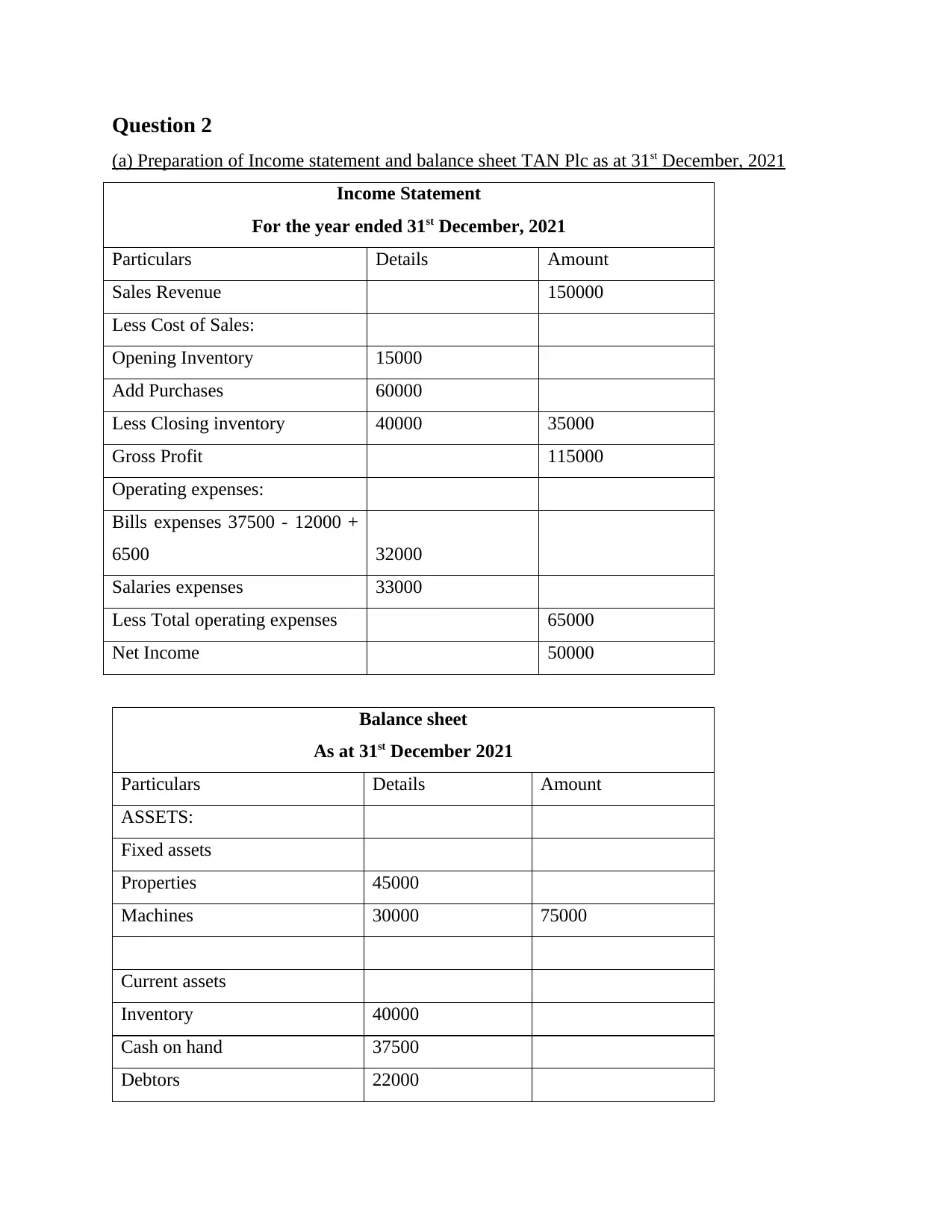

Question 2

(a) Preparation of Income statement and balance sheet TAN Plc as at 31st December, 2021

Income Statement

For the year ended 31st December, 2021

Particulars Details Amount

Sales Revenue 150000

Less Cost of Sales:

Opening Inventory 15000

Add Purchases 60000

Less Closing inventory 40000 35000

Gross Profit 115000

Operating expenses:

Bills expenses 37500 - 12000 +

6500 32000

Salaries expenses 33000

Less Total operating expenses 65000

Net Income 50000

Balance sheet

As at 31st December 2021

Particulars Details Amount

ASSETS:

Fixed assets

Properties 45000

Machines 30000 75000

Current assets

Inventory 40000

Cash on hand 37500

Debtors 22000

(a) Preparation of Income statement and balance sheet TAN Plc as at 31st December, 2021

Income Statement

For the year ended 31st December, 2021

Particulars Details Amount

Sales Revenue 150000

Less Cost of Sales:

Opening Inventory 15000

Add Purchases 60000

Less Closing inventory 40000 35000

Gross Profit 115000

Operating expenses:

Bills expenses 37500 - 12000 +

6500 32000

Salaries expenses 33000

Less Total operating expenses 65000

Net Income 50000

Balance sheet

As at 31st December 2021

Particulars Details Amount

ASSETS:

Fixed assets

Properties 45000

Machines 30000 75000

Current assets

Inventory 40000

Cash on hand 37500

Debtors 22000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

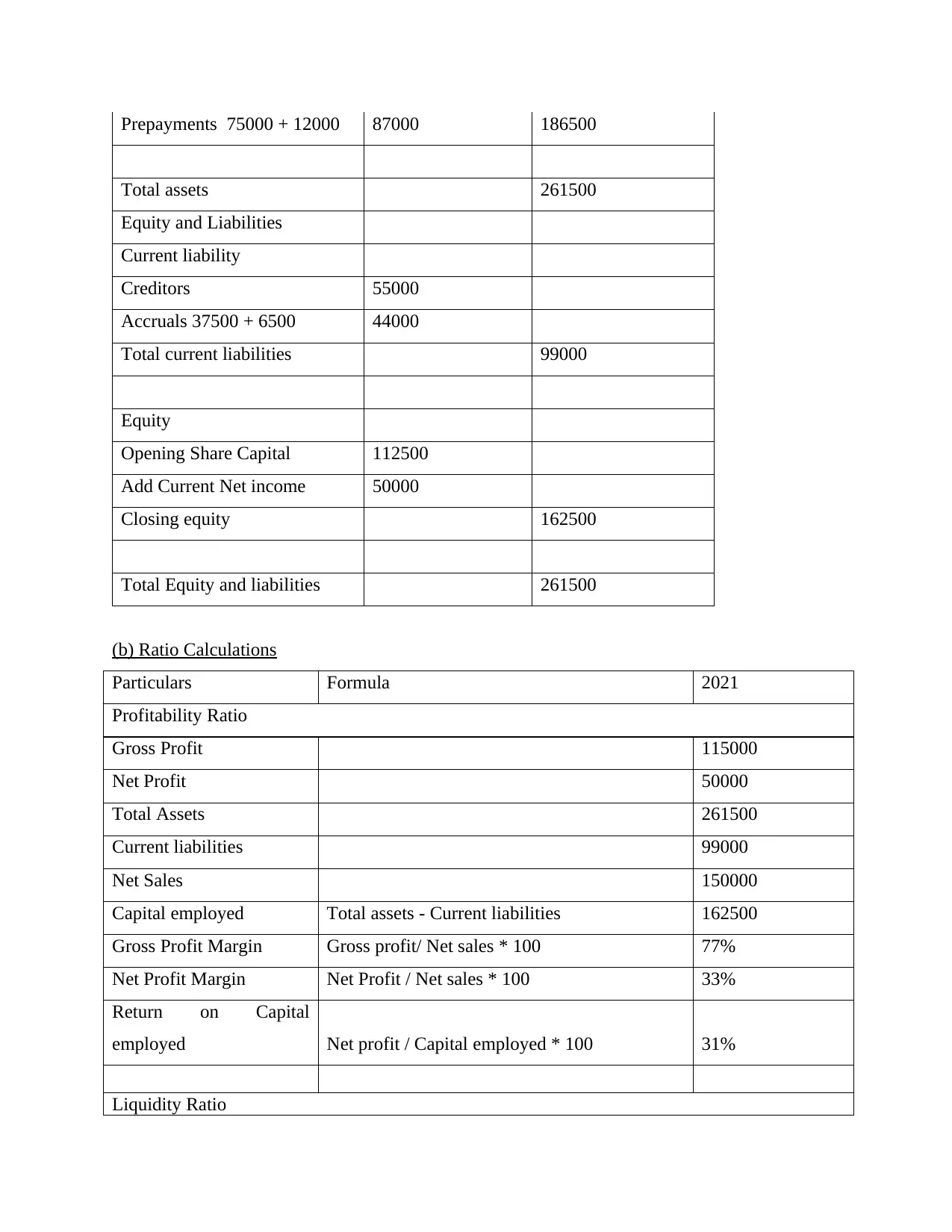

Prepayments 75000 + 12000 87000 186500

Total assets 261500

Equity and Liabilities

Current liability

Creditors 55000

Accruals 37500 + 6500 44000

Total current liabilities 99000

Equity

Opening Share Capital 112500

Add Current Net income 50000

Closing equity 162500

Total Equity and liabilities 261500

(b) Ratio Calculations

Particulars Formula 2021

Profitability Ratio

Gross Profit 115000

Net Profit 50000

Total Assets 261500

Current liabilities 99000

Net Sales 150000

Capital employed Total assets - Current liabilities 162500

Gross Profit Margin Gross profit/ Net sales * 100 77%

Net Profit Margin Net Profit / Net sales * 100 33%

Return on Capital

employed Net profit / Capital employed * 100 31%

Liquidity Ratio

Total assets 261500

Equity and Liabilities

Current liability

Creditors 55000

Accruals 37500 + 6500 44000

Total current liabilities 99000

Equity

Opening Share Capital 112500

Add Current Net income 50000

Closing equity 162500

Total Equity and liabilities 261500

(b) Ratio Calculations

Particulars Formula 2021

Profitability Ratio

Gross Profit 115000

Net Profit 50000

Total Assets 261500

Current liabilities 99000

Net Sales 150000

Capital employed Total assets - Current liabilities 162500

Gross Profit Margin Gross profit/ Net sales * 100 77%

Net Profit Margin Net Profit / Net sales * 100 33%

Return on Capital

employed Net profit / Capital employed * 100 31%

Liquidity Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

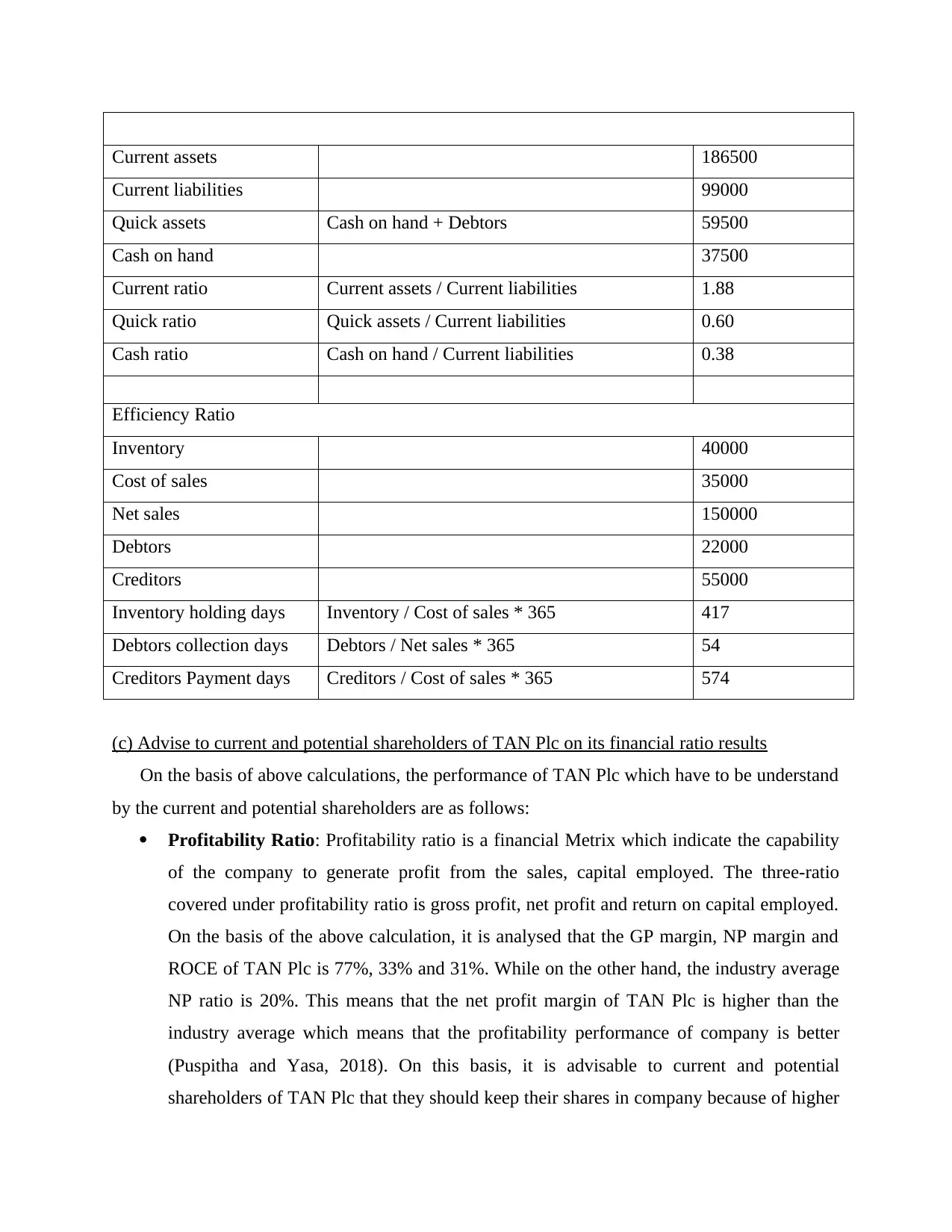

Current assets 186500

Current liabilities 99000

Quick assets Cash on hand + Debtors 59500

Cash on hand 37500

Current ratio Current assets / Current liabilities 1.88

Quick ratio Quick assets / Current liabilities 0.60

Cash ratio Cash on hand / Current liabilities 0.38

Efficiency Ratio

Inventory 40000

Cost of sales 35000

Net sales 150000

Debtors 22000

Creditors 55000

Inventory holding days Inventory / Cost of sales * 365 417

Debtors collection days Debtors / Net sales * 365 54

Creditors Payment days Creditors / Cost of sales * 365 574

(c) Advise to current and potential shareholders of TAN Plc on its financial ratio results

On the basis of above calculations, the performance of TAN Plc which have to be understand

by the current and potential shareholders are as follows:

Profitability Ratio: Profitability ratio is a financial Metrix which indicate the capability

of the company to generate profit from the sales, capital employed. The three-ratio

covered under profitability ratio is gross profit, net profit and return on capital employed.

On the basis of the above calculation, it is analysed that the GP margin, NP margin and

ROCE of TAN Plc is 77%, 33% and 31%. While on the other hand, the industry average

NP ratio is 20%. This means that the net profit margin of TAN Plc is higher than the

industry average which means that the profitability performance of company is better

(Puspitha and Yasa, 2018). On this basis, it is advisable to current and potential

shareholders of TAN Plc that they should keep their shares in company because of higher

Current liabilities 99000

Quick assets Cash on hand + Debtors 59500

Cash on hand 37500

Current ratio Current assets / Current liabilities 1.88

Quick ratio Quick assets / Current liabilities 0.60

Cash ratio Cash on hand / Current liabilities 0.38

Efficiency Ratio

Inventory 40000

Cost of sales 35000

Net sales 150000

Debtors 22000

Creditors 55000

Inventory holding days Inventory / Cost of sales * 365 417

Debtors collection days Debtors / Net sales * 365 54

Creditors Payment days Creditors / Cost of sales * 365 574

(c) Advise to current and potential shareholders of TAN Plc on its financial ratio results

On the basis of above calculations, the performance of TAN Plc which have to be understand

by the current and potential shareholders are as follows:

Profitability Ratio: Profitability ratio is a financial Metrix which indicate the capability

of the company to generate profit from the sales, capital employed. The three-ratio

covered under profitability ratio is gross profit, net profit and return on capital employed.

On the basis of the above calculation, it is analysed that the GP margin, NP margin and

ROCE of TAN Plc is 77%, 33% and 31%. While on the other hand, the industry average

NP ratio is 20%. This means that the net profit margin of TAN Plc is higher than the

industry average which means that the profitability performance of company is better

(Puspitha and Yasa, 2018). On this basis, it is advisable to current and potential

shareholders of TAN Plc that they should keep their shares in company because of higher

profitability of business. The capability of company to provide higher dividend and return

is high.

Liquidity Ratio: The liquidity is another financial ratio metrics which indicate the

capability of the company to pay of the current obligation of company with the use of

cash balance and cash generates from current as well as quick assets. This ratio includes

current ratio, quick ratio and cash ratio. On the basis of above information, it is analysed

that the current ratio, quick ratio and cash ratio of TAN Plc is 1.88, 0.60 and 0.38

respectively. On the other hand, the industry average current ratio is 120%. The 188% of

current ratio of TAN Plc is higher than the industry average of 120% which indicate that

the liquidity performance of TAN company is good. The company have to ability to pay

its current obligation with the use of current assets and they need not to borrow money

from the market (Mahtani and Garg, 2018). On this basis, it is advisable to the

shareholder of company that they should keep their shares without selling in the market.

Efficiency Ratio: Another most significant financial ratio that state the performance of

the company is efficiency ratio. This ratio indicates the capability of the company to

collect payment on time from debtors and pay the supplier on time. The three main ratios

computed under efficiency category includes inventory holding days, debtors’ collection

period and creditors payment days. On the basis of above calculation, it is analysed that

the inventory holding days of TAN Plc is 417 days. Also, the debtor’s collection days and

creditors payment days are 54 days and 574 days respectively. However, on the other

hand, the debtor collection days of industry is 110 days which is higher than the TAN

Plc. This means that the performance of TAN Plc is better and the company has the

capability to collect the dues from the debtors on time. In addition, the creditors payment

days as per average industry is 130 days lower than the TAN Plc. The higher creditors

payment days of TAN Plc indicate that the credit worthiness of company is quite poor

which they need to improve (White and Van Dyk, 2019). This indicate that the overall

efficiency performance of TAN Plc is poor as compared to average industry.

On the basis of the analysis of performance of TAN Plc in the term of profitability, efficiency

and liquidity performance of company, it is analysed that the current and potential shareholders

of TAN Plc should keep their shares. Further, the investors are also allowable to invest in the

is high.

Liquidity Ratio: The liquidity is another financial ratio metrics which indicate the

capability of the company to pay of the current obligation of company with the use of

cash balance and cash generates from current as well as quick assets. This ratio includes

current ratio, quick ratio and cash ratio. On the basis of above information, it is analysed

that the current ratio, quick ratio and cash ratio of TAN Plc is 1.88, 0.60 and 0.38

respectively. On the other hand, the industry average current ratio is 120%. The 188% of

current ratio of TAN Plc is higher than the industry average of 120% which indicate that

the liquidity performance of TAN company is good. The company have to ability to pay

its current obligation with the use of current assets and they need not to borrow money

from the market (Mahtani and Garg, 2018). On this basis, it is advisable to the

shareholder of company that they should keep their shares without selling in the market.

Efficiency Ratio: Another most significant financial ratio that state the performance of

the company is efficiency ratio. This ratio indicates the capability of the company to

collect payment on time from debtors and pay the supplier on time. The three main ratios

computed under efficiency category includes inventory holding days, debtors’ collection

period and creditors payment days. On the basis of above calculation, it is analysed that

the inventory holding days of TAN Plc is 417 days. Also, the debtor’s collection days and

creditors payment days are 54 days and 574 days respectively. However, on the other

hand, the debtor collection days of industry is 110 days which is higher than the TAN

Plc. This means that the performance of TAN Plc is better and the company has the

capability to collect the dues from the debtors on time. In addition, the creditors payment

days as per average industry is 130 days lower than the TAN Plc. The higher creditors

payment days of TAN Plc indicate that the credit worthiness of company is quite poor

which they need to improve (White and Van Dyk, 2019). This indicate that the overall

efficiency performance of TAN Plc is poor as compared to average industry.

On the basis of the analysis of performance of TAN Plc in the term of profitability, efficiency

and liquidity performance of company, it is analysed that the current and potential shareholders

of TAN Plc should keep their shares. Further, the investors are also allowable to invest in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shares of company and current shareholders to reinvest their earnings again in the company. It is

because for shareholders profitability and liquidity performance plays vital role in their decision-

making process (Sihotang, Hasanah and Hayati, 2022). However, on the other hand the poor

efficiency performance of TAN does not affect the shareholders decision. Hence, on this basis it

is advisable to current as well as potential shareholder of company to keep their shares in order

to further earn the higher return and dividend from the company.

Question 3

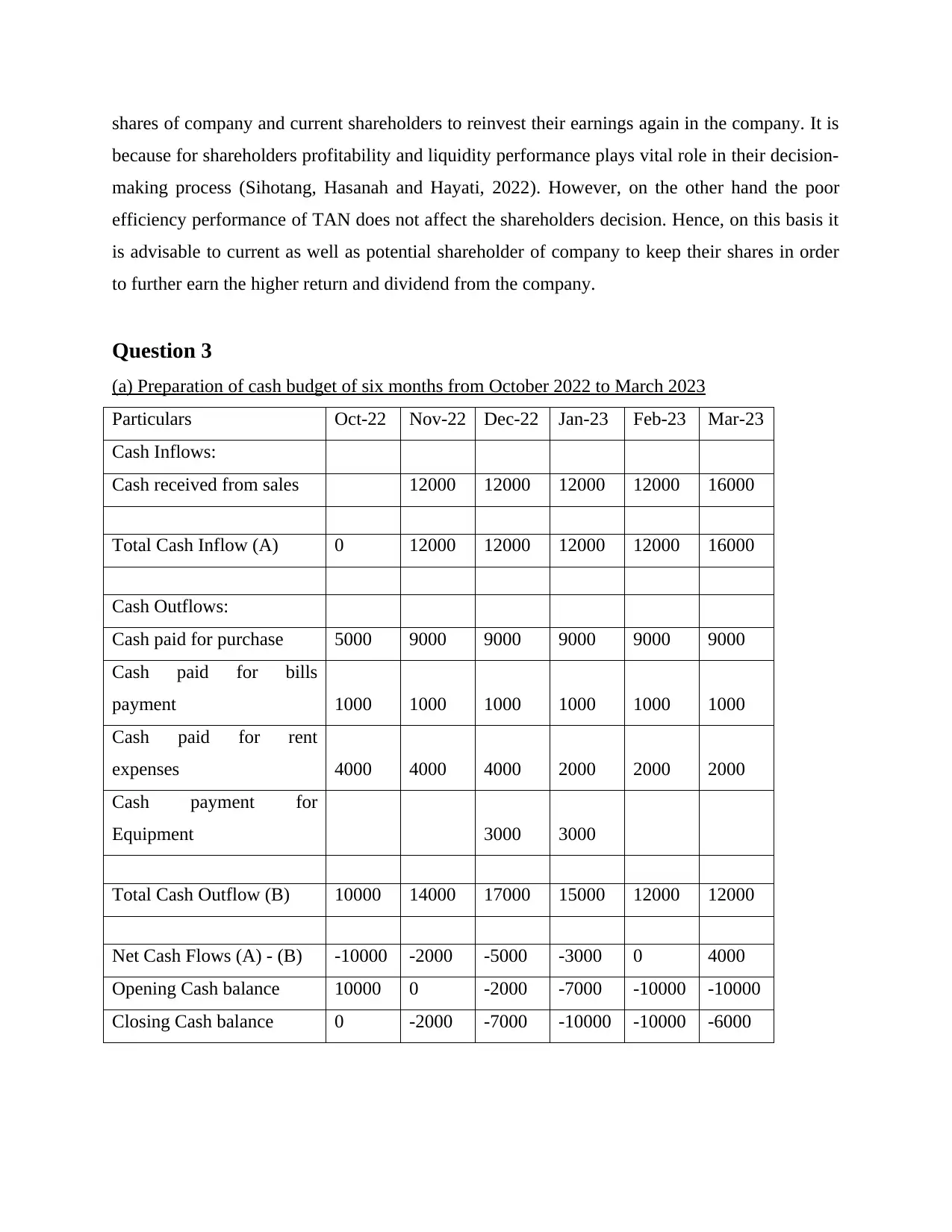

(a) Preparation of cash budget of six months from October 2022 to March 2023

Particulars Oct-22 Nov-22 Dec-22 Jan-23 Feb-23 Mar-23

Cash Inflows:

Cash received from sales 12000 12000 12000 12000 16000

Total Cash Inflow (A) 0 12000 12000 12000 12000 16000

Cash Outflows:

Cash paid for purchase 5000 9000 9000 9000 9000 9000

Cash paid for bills

payment 1000 1000 1000 1000 1000 1000

Cash paid for rent

expenses 4000 4000 4000 2000 2000 2000

Cash payment for

Equipment 3000 3000

Total Cash Outflow (B) 10000 14000 17000 15000 12000 12000

Net Cash Flows (A) - (B) -10000 -2000 -5000 -3000 0 4000

Opening Cash balance 10000 0 -2000 -7000 -10000 -10000

Closing Cash balance 0 -2000 -7000 -10000 -10000 -6000

because for shareholders profitability and liquidity performance plays vital role in their decision-

making process (Sihotang, Hasanah and Hayati, 2022). However, on the other hand the poor

efficiency performance of TAN does not affect the shareholders decision. Hence, on this basis it

is advisable to current as well as potential shareholder of company to keep their shares in order

to further earn the higher return and dividend from the company.

Question 3

(a) Preparation of cash budget of six months from October 2022 to March 2023

Particulars Oct-22 Nov-22 Dec-22 Jan-23 Feb-23 Mar-23

Cash Inflows:

Cash received from sales 12000 12000 12000 12000 16000

Total Cash Inflow (A) 0 12000 12000 12000 12000 16000

Cash Outflows:

Cash paid for purchase 5000 9000 9000 9000 9000 9000

Cash paid for bills

payment 1000 1000 1000 1000 1000 1000

Cash paid for rent

expenses 4000 4000 4000 2000 2000 2000

Cash payment for

Equipment 3000 3000

Total Cash Outflow (B) 10000 14000 17000 15000 12000 12000

Net Cash Flows (A) - (B) -10000 -2000 -5000 -3000 0 4000

Opening Cash balance 10000 0 -2000 -7000 -10000 -10000

Closing Cash balance 0 -2000 -7000 -10000 -10000 -6000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Advise to management of AMF Ltd on strategies they need to adopt in order to properly

manage cash flow from period October 2022 to March 2023

On the basis of above cash forecasting of six months of AMF Ltd, it has been analysed that

the closing cash balance of company is negative in all the six months. Further, to improve the

cash management of the company, the following strategy or steps need to be adopted by AMF

Ltd:

Monitoring cash flow regularly: This is one of the step or ways with the help of which

management of AMF company able to properly manage its cash flow. Here, they need to

monitor its cash budget on regular basis and identify whether the company are able to

maintain minimum cash balance within the company or not (Kusainov and et.al., 2020).

Lease equipment instead of buying it: This is another step which indicate that the

company such as AMF should lease equipment rather than buying the same on cash. It is

because purchasing the assets on lease will require less cash outflow while buying it

require high cash outflow (Thomas, 2022). So, on this basis it can be said that the AMF

company should take equipment on lease to properly manage the cash flow in the

upcoming six month.

Speed Payments via offering discounts: This is another most crucial step that have to be

adopted by the company name AMF which indicate that company should offer different

discounts to its customers or debtors. It is because this helps the company to collect the

dues from the debtors (Khalaf, 2019). The early payment discount attracts the customer

to pay the dues of company on time.

Building relation with supplier: This step indicate that AMF company should build

strong relation with its supplier in order to enhance the credit worthiness of company. It

also helps the company to ask more credit period from its supplier than help the company

to manage the cash flow within the business. Hence, this strategy should adopt by the

company in the favor of its cash flow management.

Cut cost: Lastly, the company should cut its cost of sales in order to further enhance the

cash flow of the company. This means that cutting cost reduces the cost of sales as well

as the cash outflow (Panigrahi, 2021). The reduction in cash outflow ultimately leads to

proper management of cash flow within the business. For example, cutting unnecessary

bills, rents etc.

manage cash flow from period October 2022 to March 2023

On the basis of above cash forecasting of six months of AMF Ltd, it has been analysed that

the closing cash balance of company is negative in all the six months. Further, to improve the

cash management of the company, the following strategy or steps need to be adopted by AMF

Ltd:

Monitoring cash flow regularly: This is one of the step or ways with the help of which

management of AMF company able to properly manage its cash flow. Here, they need to

monitor its cash budget on regular basis and identify whether the company are able to

maintain minimum cash balance within the company or not (Kusainov and et.al., 2020).

Lease equipment instead of buying it: This is another step which indicate that the

company such as AMF should lease equipment rather than buying the same on cash. It is

because purchasing the assets on lease will require less cash outflow while buying it

require high cash outflow (Thomas, 2022). So, on this basis it can be said that the AMF

company should take equipment on lease to properly manage the cash flow in the

upcoming six month.

Speed Payments via offering discounts: This is another most crucial step that have to be

adopted by the company name AMF which indicate that company should offer different

discounts to its customers or debtors. It is because this helps the company to collect the

dues from the debtors (Khalaf, 2019). The early payment discount attracts the customer

to pay the dues of company on time.

Building relation with supplier: This step indicate that AMF company should build

strong relation with its supplier in order to enhance the credit worthiness of company. It

also helps the company to ask more credit period from its supplier than help the company

to manage the cash flow within the business. Hence, this strategy should adopt by the

company in the favor of its cash flow management.

Cut cost: Lastly, the company should cut its cost of sales in order to further enhance the

cash flow of the company. This means that cutting cost reduces the cost of sales as well

as the cash outflow (Panigrahi, 2021). The reduction in cash outflow ultimately leads to

proper management of cash flow within the business. For example, cutting unnecessary

bills, rents etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

Puspitha, M. Y. and Yasa, G. W., 2018. Fraud pentagon analysis in detecting fraudulent financial

reporting (study on Indonesian capital market). International Journal of Sciences: Basic

and Applied Research. 42(5). pp.93-109.

Mahtani, U. S. and Garg, C. P., 2018. An analysis of key factors of financial distress in airline

companies in India using fuzzy AHP framework. Transportation Research Part A: Policy

and Practice. 117. pp.87-102.

White, C. J. and Van Dyk, H., 2019. Theory and practice of the quintile ranking of schools in

South Africa: A financial management perspective. South African Journal of

Education. 39(Supplement 1). pp.s1-19.

Sihotang, M. K., Hasanah, U. and Hayati, I., 2022. Model Of Sharia Bank Profitability

Determination Factors By Measuring Internal And Externals Variables. Indonesian

Interdisciplinary Journal Of Sharia Economics (Iijse). 5(1). pp.235-251.

Kusainov, H. and et.al., 2020. WAYS TO IMPROVE COMPANY VALUE ASSESSMENT. OF

SOCIAL AND HUMAN SCIENCES. 120.

Khalaf, M. A. L., 2019. Cash flow generation and alternatives analysis through BIM and

simulation (Master's thesis, Fen Bilimleri Enstitüsü).

Panigrahi, C. M. A., 2021. Application of discounted cash flow model valuation: The case of

Exide industries. Panigrahi A, Vachhani K, Sisodia M.," Application of Discounted Cash

Flow Model Valuation: The Case of Exide Industries", Journal of Management Research

Thomas, M. G., 2022. 6 Budgeting and Cash Flow Management. De Gruyter Handbook of

Personal Finance, p.87.

1

Books and journals

Puspitha, M. Y. and Yasa, G. W., 2018. Fraud pentagon analysis in detecting fraudulent financial

reporting (study on Indonesian capital market). International Journal of Sciences: Basic

and Applied Research. 42(5). pp.93-109.

Mahtani, U. S. and Garg, C. P., 2018. An analysis of key factors of financial distress in airline

companies in India using fuzzy AHP framework. Transportation Research Part A: Policy

and Practice. 117. pp.87-102.

White, C. J. and Van Dyk, H., 2019. Theory and practice of the quintile ranking of schools in

South Africa: A financial management perspective. South African Journal of

Education. 39(Supplement 1). pp.s1-19.

Sihotang, M. K., Hasanah, U. and Hayati, I., 2022. Model Of Sharia Bank Profitability

Determination Factors By Measuring Internal And Externals Variables. Indonesian

Interdisciplinary Journal Of Sharia Economics (Iijse). 5(1). pp.235-251.

Kusainov, H. and et.al., 2020. WAYS TO IMPROVE COMPANY VALUE ASSESSMENT. OF

SOCIAL AND HUMAN SCIENCES. 120.

Khalaf, M. A. L., 2019. Cash flow generation and alternatives analysis through BIM and

simulation (Master's thesis, Fen Bilimleri Enstitüsü).

Panigrahi, C. M. A., 2021. Application of discounted cash flow model valuation: The case of

Exide industries. Panigrahi A, Vachhani K, Sisodia M.," Application of Discounted Cash

Flow Model Valuation: The Case of Exide Industries", Journal of Management Research

Thomas, M. G., 2022. 6 Budgeting and Cash Flow Management. De Gruyter Handbook of

Personal Finance, p.87.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.